Taxation Law Assignment: Deductions, Credits, and Income Calculations

VerifiedAdded on 2020/04/01

|10

|1908

|49

Homework Assignment

AI Summary

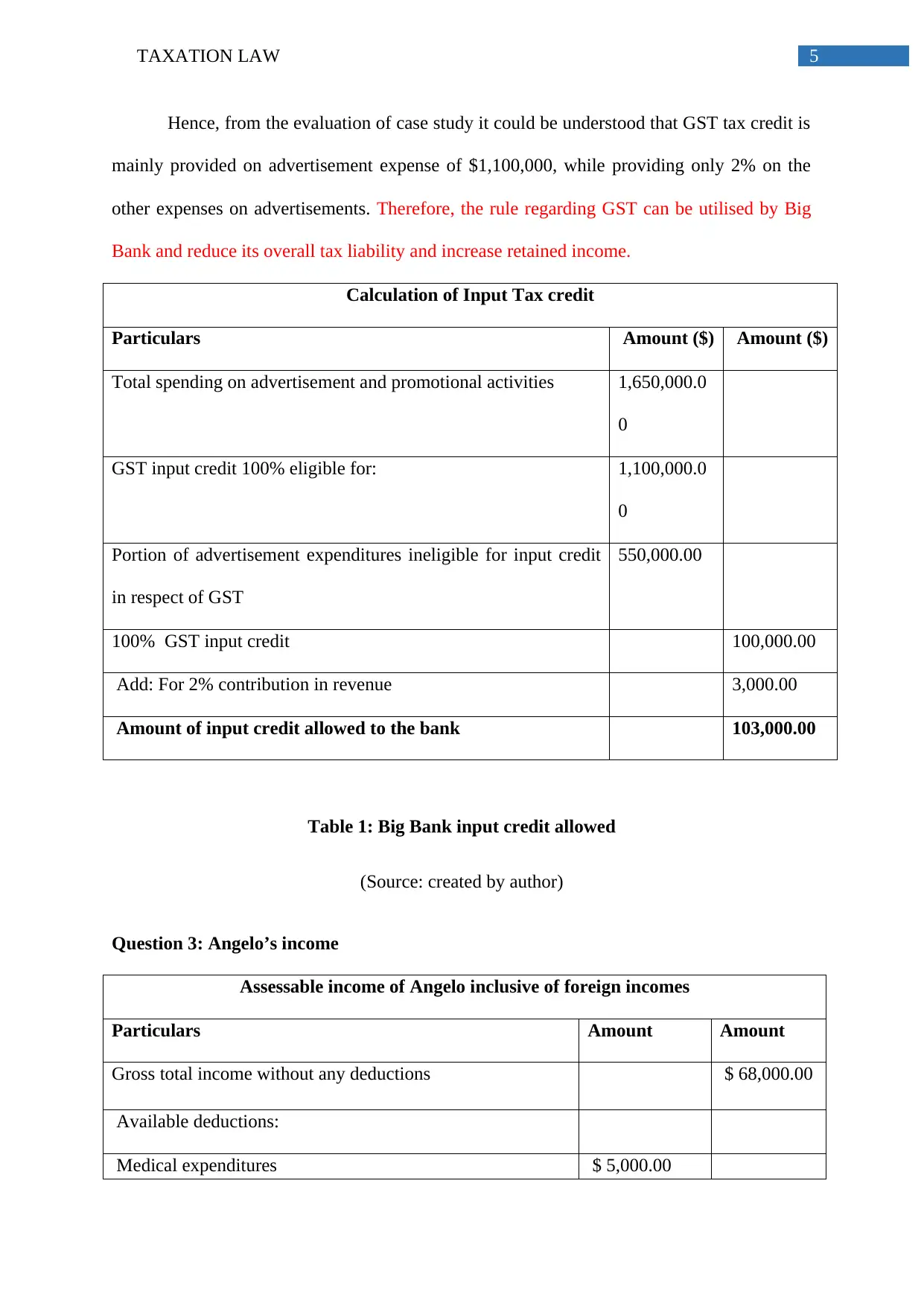

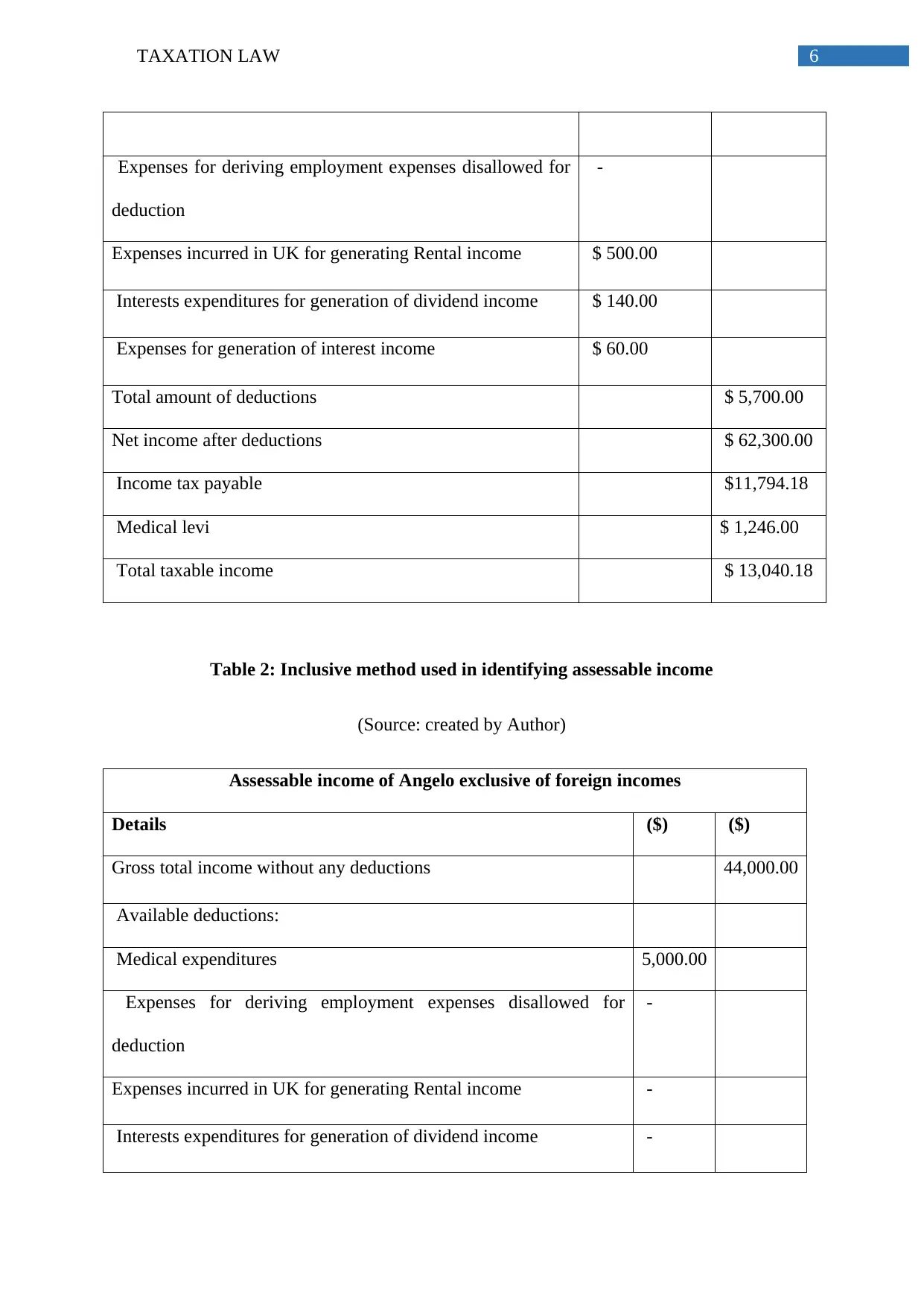

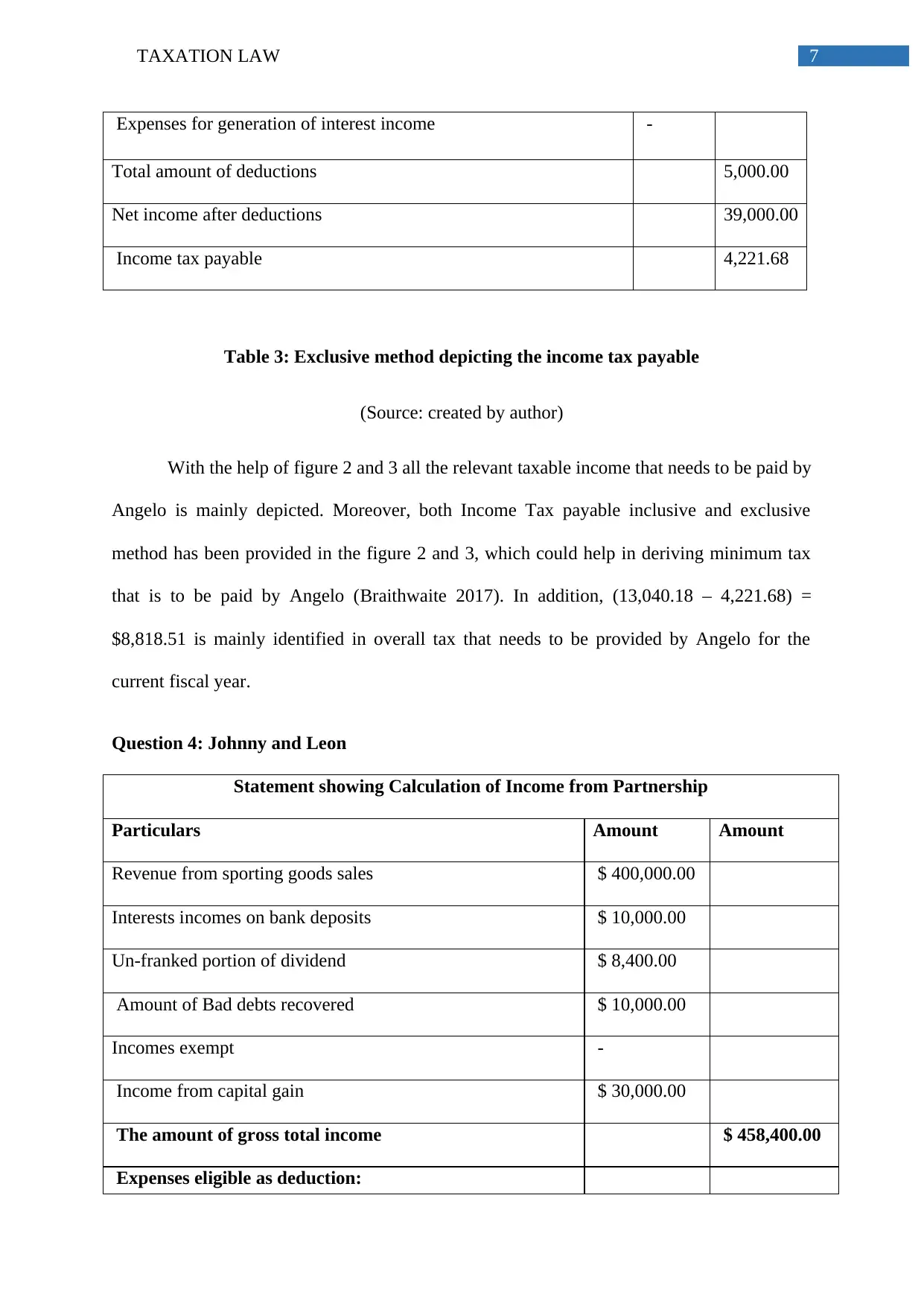

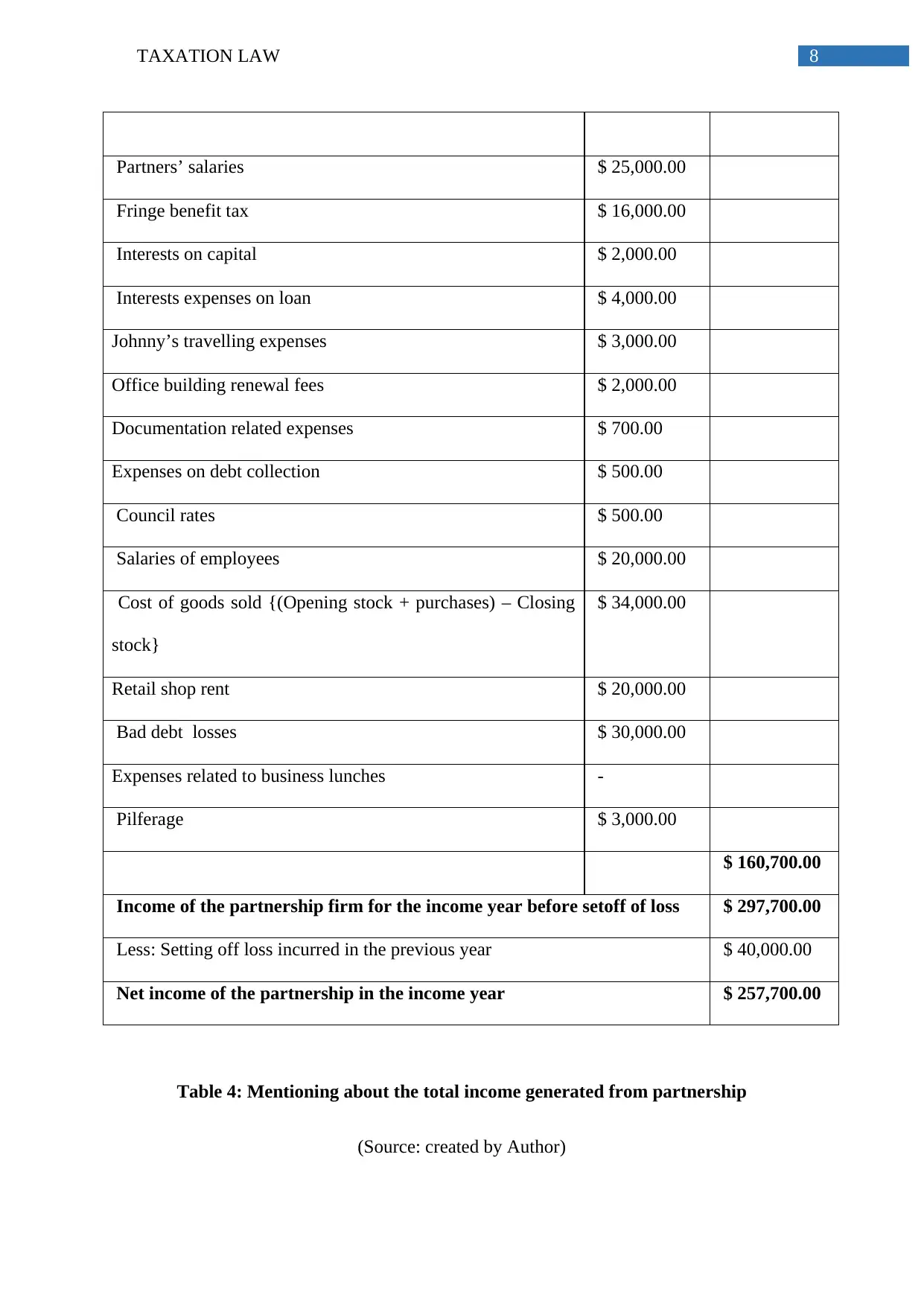

This taxation law assignment delves into several key areas of Australian tax law. Question 1 evaluates Section 8-1 of the ITAA 1997, identifying deductible expenses such as machinery transfer costs and law proceeding expenses. Question 2 examines the GST implications for Big Bank Ltd's advertising expenses, distinguishing between promotional activities and new product promotions to determine eligible tax credits. Question 3 calculates Angelo's assessable income, both including and excluding foreign income, and determines his income tax payable. Finally, Question 4 analyzes the income of a partnership firm, Johnny and Leon, detailing revenue, deductions (including partner salaries, interest, and various business expenses), and the calculation of net partnership income after setting off previous year losses. The assignment utilizes tables to present financial data and provides references to relevant tax legislation and literature.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.