Taxation Law Assignment: HI6028, Holmes Institute, T2 2019

VerifiedAdded on 2022/10/18

|12

|2682

|205

Homework Assignment

AI Summary

This taxation law assignment solution addresses key issues related to Goods and Services Tax (GST) and Capital Gains Tax (CGT) within the Australian context. The assignment analyzes the tax implications of purchasing vacant land, considering GST exemptions and the reverse charge mechanism. It examines the case of City Sky Co., which acquired vacant land for residential development and sought legal advice, assessing the GST liabilities and input tax credit entitlements. Furthermore, the assignment delves into CGT principles, specifically focusing on the sale of land, shares, a stamp collection, and a piano, detailing the calculation of capital gains or losses based on cost base elements and pre-CGT assets. The solution provides a comprehensive understanding of taxation laws, including the application of relevant legislation and case law to real-life scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

The transaction that is considered for study is the tax related matters for the GST and

the entitlements that arises from the purchase of vacant land is dealt in this case.

Rule:

As all the transactions relating to the real estate is considered different, the only rule

that is followed is the laws relating to GST. As the beginning point, the registered business

are required to be aware that GST is very commonly payable on the purchase of the real

estate property unless any kind of specific exemption is applicable (Richardson and Smith

2013). The residential and the non-residential property are taken into consideration in the

different manner. The most common type of exemption that is available on the residential

properties is that when they are resold since the GST is commonly paid on the new residential

property and the resale is commonly exempted. For instance the transactions that are

involving the farm and the farm house or the store having a suite inside might have to pay

GST but not on the purchase price.

Special consideration must be paid to the transactions that involve the builders (Kraal

and Kasipillai 2016). The new residential property cannot be considered as exempted from

GST therefore it must be noted that if in the contract GST is not included in the purchase

price then there cannot be entitlement of claiming input tax credit. GST us commonly paid on

the commercial property and the company that is obtaining the real property may be

considered liable for GST. The entity can recover the GST with the help of input tax credit.

As the starting point, vacant land is commonly considered as exempted from GST

when the land is sold by the individual (Edmundson 2013). There are several exclusions

Answer to question 1:

Issues:

The transaction that is considered for study is the tax related matters for the GST and

the entitlements that arises from the purchase of vacant land is dealt in this case.

Rule:

As all the transactions relating to the real estate is considered different, the only rule

that is followed is the laws relating to GST. As the beginning point, the registered business

are required to be aware that GST is very commonly payable on the purchase of the real

estate property unless any kind of specific exemption is applicable (Richardson and Smith

2013). The residential and the non-residential property are taken into consideration in the

different manner. The most common type of exemption that is available on the residential

properties is that when they are resold since the GST is commonly paid on the new residential

property and the resale is commonly exempted. For instance the transactions that are

involving the farm and the farm house or the store having a suite inside might have to pay

GST but not on the purchase price.

Special consideration must be paid to the transactions that involve the builders (Kraal

and Kasipillai 2016). The new residential property cannot be considered as exempted from

GST therefore it must be noted that if in the contract GST is not included in the purchase

price then there cannot be entitlement of claiming input tax credit. GST us commonly paid on

the commercial property and the company that is obtaining the real property may be

considered liable for GST. The entity can recover the GST with the help of input tax credit.

As the starting point, vacant land is commonly considered as exempted from GST

when the land is sold by the individual (Edmundson 2013). There are several exclusions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

associated to the exemption that needs examination. For instance if the land is held by the

taxpayer while conducting or performing the business activities then the exemption is not

allowed to the taxpayer. The taxpayer should denote that the vacant is typically considered as

the asset. The vacant is generally considered as the subject of CGT rather than the subject of

GST.

There are also specific rules that is associated to the reverse charge. The reverse

charge should be viewed as the type of tax that moves the accountability of reporting the tax

transaction from the seller to the purchaser of good or service (Benedict 2014). When the

transaction is considered as the subject of reverse charge, the one that receive the good and

service reports both the purchase (input vat) and the supplier’s sale (output vat) into their tax

return. This represents the circumstances when the GST is paid by the purchaser. This is

known as the reverse charge. Transactions that involves the offshore purchase commonly

attracts the reverse charge. The buyer might choose to pay the GST on purchase in spite of

the fact that they are the purchaser. The amount of reverse charge rate is usually the 10% of

the purchase price.

Accordingly there are some important rules that are related to the reverse charge. This

amounts to the things excluding the actual property and the tangible goods which attracts

GST liability when it is acquired by the business that are operating in Australia (CCH

Australia Limited 2013). The reverse charge also includes the activities that are carried

outside Australia and the acquisition of thing that is made by the Australian business is with

the help of the sellers that are out of Australia. As a result of this, the taxpayer will be

considered liable for paying the GST under the rules of reverse charge.

There are also conditions that a taxpayer are required to meet at the time of applying

the reverse charge rules. The conditions are the purchase of things which is exclusively or

associated to the exemption that needs examination. For instance if the land is held by the

taxpayer while conducting or performing the business activities then the exemption is not

allowed to the taxpayer. The taxpayer should denote that the vacant is typically considered as

the asset. The vacant is generally considered as the subject of CGT rather than the subject of

GST.

There are also specific rules that is associated to the reverse charge. The reverse

charge should be viewed as the type of tax that moves the accountability of reporting the tax

transaction from the seller to the purchaser of good or service (Benedict 2014). When the

transaction is considered as the subject of reverse charge, the one that receive the good and

service reports both the purchase (input vat) and the supplier’s sale (output vat) into their tax

return. This represents the circumstances when the GST is paid by the purchaser. This is

known as the reverse charge. Transactions that involves the offshore purchase commonly

attracts the reverse charge. The buyer might choose to pay the GST on purchase in spite of

the fact that they are the purchaser. The amount of reverse charge rate is usually the 10% of

the purchase price.

Accordingly there are some important rules that are related to the reverse charge. This

amounts to the things excluding the actual property and the tangible goods which attracts

GST liability when it is acquired by the business that are operating in Australia (CCH

Australia Limited 2013). The reverse charge also includes the activities that are carried

outside Australia and the acquisition of thing that is made by the Australian business is with

the help of the sellers that are out of Australia. As a result of this, the taxpayer will be

considered liable for paying the GST under the rules of reverse charge.

There are also conditions that a taxpayer are required to meet at the time of applying

the reverse charge rules. The conditions are the purchase of things which is exclusively or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

moderately made in the business activities of the taxpayer that they are conducting in

Australia (McCouat 2013). The purchase made is partially for the domestic purpose or for

making any input tax supplies. The sale that is made to entity is for the payment and the

entity is considered as the registered entity within the rules of GST. Furthermore, there

should also be certain circumstances that an Australian entity is also required to satisfy. The

circumstances denotes that things that is purchased is carried out of Australia and the sale

made to the entity is not made with the help of business that the seller is conducting in

Australia. It also includes that the sale is connected with Australia and the entity is the

Australian based business receiver.

Application:

The case materials of City Sky Co is concerned in this study. Noting into the facts

established by the case it is noticed that the business has obtained the GST registration and its

business activities are based in Australia (Alexiou and Morrison 2014). The circumstances

that is bought forward is regarding the City Sky Co case is that the company acquired the

vacant land. The main objective of acquiring the vacant land is to construct a total of 15

residential premises for sale in the market. As understood it should be noted that the purchase

of vacant land is not a GST related transaction. In regard to the laws that is discussed above

GST is not applicable on the vacant land. Reasonably, land is an non-movable capital asset so

there cannot be any GST on the land. In addition to this vacant land acquisition is falling

within the ambit of black credit provision. In other words, when a goods and service that is

acquired by the taxable person for constructing any non-movable property then they are not

falling within the eligibility of input tax credit entitlements.

As the case develops further, an occurrence relating to the legal advice is sought by

City Sky Co for the land developmental purpose from the Maurice Blackburn. City Sky Co

moderately made in the business activities of the taxpayer that they are conducting in

Australia (McCouat 2013). The purchase made is partially for the domestic purpose or for

making any input tax supplies. The sale that is made to entity is for the payment and the

entity is considered as the registered entity within the rules of GST. Furthermore, there

should also be certain circumstances that an Australian entity is also required to satisfy. The

circumstances denotes that things that is purchased is carried out of Australia and the sale

made to the entity is not made with the help of business that the seller is conducting in

Australia. It also includes that the sale is connected with Australia and the entity is the

Australian based business receiver.

Application:

The case materials of City Sky Co is concerned in this study. Noting into the facts

established by the case it is noticed that the business has obtained the GST registration and its

business activities are based in Australia (Alexiou and Morrison 2014). The circumstances

that is bought forward is regarding the City Sky Co case is that the company acquired the

vacant land. The main objective of acquiring the vacant land is to construct a total of 15

residential premises for sale in the market. As understood it should be noted that the purchase

of vacant land is not a GST related transaction. In regard to the laws that is discussed above

GST is not applicable on the vacant land. Reasonably, land is an non-movable capital asset so

there cannot be any GST on the land. In addition to this vacant land acquisition is falling

within the ambit of black credit provision. In other words, when a goods and service that is

acquired by the taxable person for constructing any non-movable property then they are not

falling within the eligibility of input tax credit entitlements.

As the case develops further, an occurrence relating to the legal advice is sought by

City Sky Co for the land developmental purpose from the Maurice Blackburn. City Sky Co

5TAXATION LAW

should be mindful that advice that the company has taken is considered liable for GST since

the seller will not be required to pay GST (Millar and McCarthy 2012). The legal advice

expenses amounts to reverse charge and the GST needs to be paid by City Sky Co. The

company here can be considered as the eligible company for claiming the input tax credit.

The services has be acquired in exchange of payment and the legal advice sought holds the

relation with the business that is carried on by City Sky Co inside Australia. The legal advice

was for the furtherance of the business activity of City Sky Co and as a result input tax credit

can be claimed in this regard.

Conclusion:

The study makes a contribution to the understanding that the land that is acquired by

the City Sky Co is a non-movable capital asset and as a result there cannot be any

entitlements associated with the input tax credit. But the legal service that the company has

taken from the Maurice Blackburn is a reverse charge mechanism. Consequently, the GST

paid on the services will be allowed as input tax credit to the company.

Answer to question 2:

Sale of block of land:

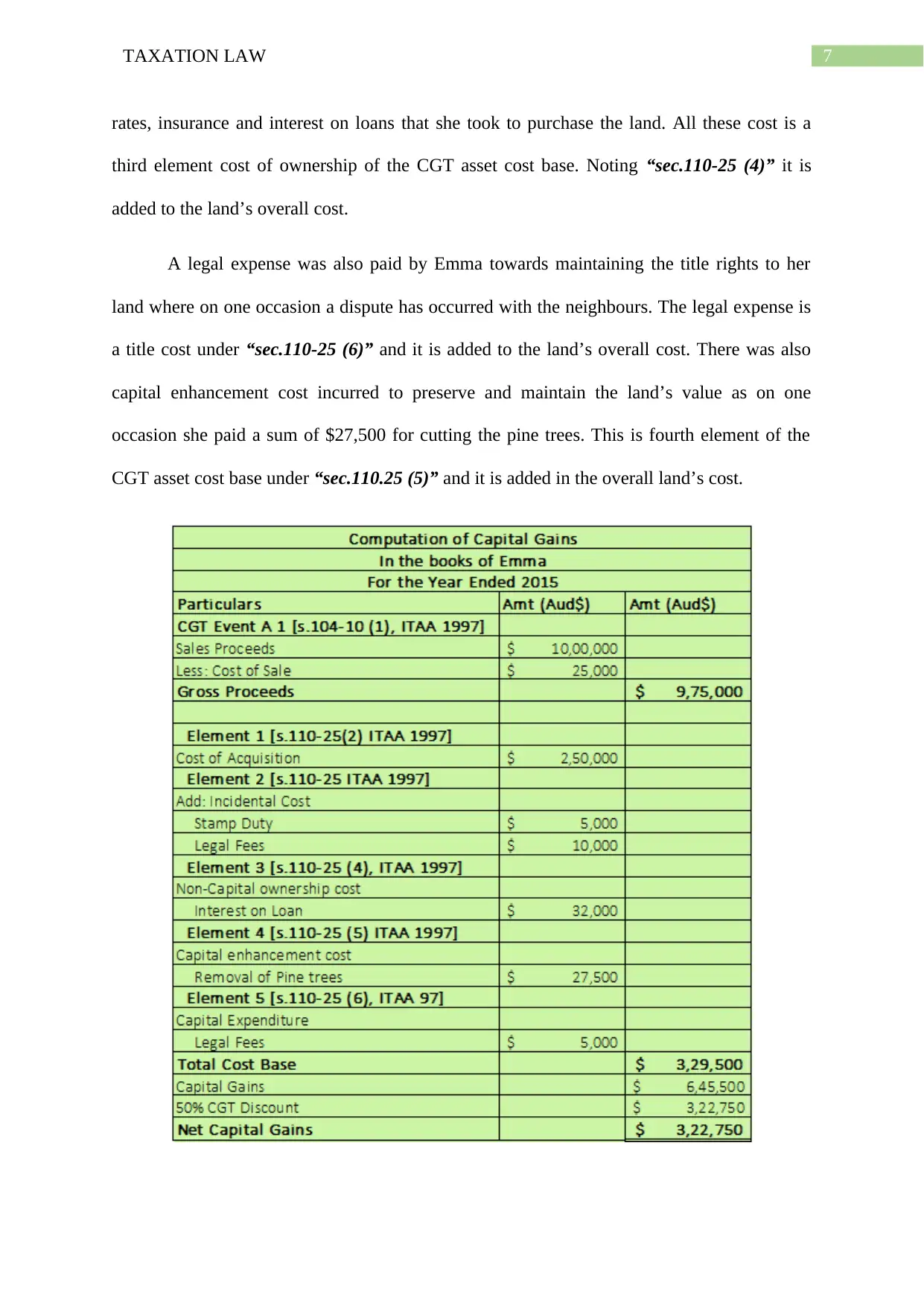

By referring to the “section 116-20” the capital proceeds present the proceeds that is

obtained by the taxpayer as the money or the market value of the property that is received in

respect of the CGT event. Capital proceeds are generally termed as the market value of the

asset that the taxpayer is about to receive or has received (Faccio and Xu 2015). The

calculation of the capital gains or loss involves the recognition of the cost base. Noting the

explanation given in the “sec 110-25 ITAA 97” there are regularly five types of elements that

is given in the CGT asset.

should be mindful that advice that the company has taken is considered liable for GST since

the seller will not be required to pay GST (Millar and McCarthy 2012). The legal advice

expenses amounts to reverse charge and the GST needs to be paid by City Sky Co. The

company here can be considered as the eligible company for claiming the input tax credit.

The services has be acquired in exchange of payment and the legal advice sought holds the

relation with the business that is carried on by City Sky Co inside Australia. The legal advice

was for the furtherance of the business activity of City Sky Co and as a result input tax credit

can be claimed in this regard.

Conclusion:

The study makes a contribution to the understanding that the land that is acquired by

the City Sky Co is a non-movable capital asset and as a result there cannot be any

entitlements associated with the input tax credit. But the legal service that the company has

taken from the Maurice Blackburn is a reverse charge mechanism. Consequently, the GST

paid on the services will be allowed as input tax credit to the company.

Answer to question 2:

Sale of block of land:

By referring to the “section 116-20” the capital proceeds present the proceeds that is

obtained by the taxpayer as the money or the market value of the property that is received in

respect of the CGT event. Capital proceeds are generally termed as the market value of the

asset that the taxpayer is about to receive or has received (Faccio and Xu 2015). The

calculation of the capital gains or loss involves the recognition of the cost base. Noting the

explanation given in the “sec 110-25 ITAA 97” there are regularly five types of elements that

is given in the CGT asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

a) The money that is paid or the market value that is prevailing for acquiring the

property under “sec 110-25 (2)” is known as the first element of the CGT asset cost

base.

b) Any kind of expenses that is occurred during the process of acquisition or the sale of

the CGT asset is known as the incidental expenses relating to the asset under

“sec.110-25 (3)”. These expenses are added as the second element of the CGT asset

cost base (Auerbach and Hassett 2015).

c) The third elements is mainly for the assets that is purchased by the taxpayer following

the 20/8/1991. This is better known as the ownership cost under “sec 110.25 (4)” and

this element includes expenses relating to loan interest, rates etc.

d) The capital outgoing when a taxpayer pays to improve the value of asset or expenses

incurred as the improvement to the asset that relates to the installation or the moving

of asset is known as the enhancement cost. This is fourth element of the CGT asset

cost base under “sec.110.25 (5)”.

e) The fifth and the last element of the CGT asset cost base under “sec.110.25 (6)” is the

title cost of asset. This expenses is incurred when maintaining the rights to the assets.

Emma being the owner of land decides on one occasion to sell it for $1,000,000.

Before the sale there were some cost that has occurred in respect of the land. At first the

purchase price when Emma has paid based on the market value of the property is included in

first element with respect to “sec 110-25 (2)” of the CGT asset cost base (Badel and Huggett

2014).

Emma paid incidental cost that she has incurred during the process of purchasing the

asset. The stamp duty and legal fees is an incidental cost of the CGT asset cost base under

“sec 110.25 (3)”. This expenses is simply added to the cost base of land. There was also the

instance when Emma incurred ownership cost of land. This included her expense towards

a) The money that is paid or the market value that is prevailing for acquiring the

property under “sec 110-25 (2)” is known as the first element of the CGT asset cost

base.

b) Any kind of expenses that is occurred during the process of acquisition or the sale of

the CGT asset is known as the incidental expenses relating to the asset under

“sec.110-25 (3)”. These expenses are added as the second element of the CGT asset

cost base (Auerbach and Hassett 2015).

c) The third elements is mainly for the assets that is purchased by the taxpayer following

the 20/8/1991. This is better known as the ownership cost under “sec 110.25 (4)” and

this element includes expenses relating to loan interest, rates etc.

d) The capital outgoing when a taxpayer pays to improve the value of asset or expenses

incurred as the improvement to the asset that relates to the installation or the moving

of asset is known as the enhancement cost. This is fourth element of the CGT asset

cost base under “sec.110.25 (5)”.

e) The fifth and the last element of the CGT asset cost base under “sec.110.25 (6)” is the

title cost of asset. This expenses is incurred when maintaining the rights to the assets.

Emma being the owner of land decides on one occasion to sell it for $1,000,000.

Before the sale there were some cost that has occurred in respect of the land. At first the

purchase price when Emma has paid based on the market value of the property is included in

first element with respect to “sec 110-25 (2)” of the CGT asset cost base (Badel and Huggett

2014).

Emma paid incidental cost that she has incurred during the process of purchasing the

asset. The stamp duty and legal fees is an incidental cost of the CGT asset cost base under

“sec 110.25 (3)”. This expenses is simply added to the cost base of land. There was also the

instance when Emma incurred ownership cost of land. This included her expense towards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

rates, insurance and interest on loans that she took to purchase the land. All these cost is a

third element cost of ownership of the CGT asset cost base. Noting “sec.110-25 (4)” it is

added to the land’s overall cost.

A legal expense was also paid by Emma towards maintaining the title rights to her

land where on one occasion a dispute has occurred with the neighbours. The legal expense is

a title cost under “sec.110-25 (6)” and it is added to the land’s overall cost. There was also

capital enhancement cost incurred to preserve and maintain the land’s value as on one

occasion she paid a sum of $27,500 for cutting the pine trees. This is fourth element of the

CGT asset cost base under “sec.110.25 (5)” and it is added in the overall land’s cost.

rates, insurance and interest on loans that she took to purchase the land. All these cost is a

third element cost of ownership of the CGT asset cost base. Noting “sec.110-25 (4)” it is

added to the land’s overall cost.

A legal expense was also paid by Emma towards maintaining the title rights to her

land where on one occasion a dispute has occurred with the neighbours. The legal expense is

a title cost under “sec.110-25 (6)” and it is added to the land’s overall cost. There was also

capital enhancement cost incurred to preserve and maintain the land’s value as on one

occasion she paid a sum of $27,500 for cutting the pine trees. This is fourth element of the

CGT asset cost base under “sec.110.25 (5)” and it is added in the overall land’s cost.

8TAXATION LAW

Sale of shares:

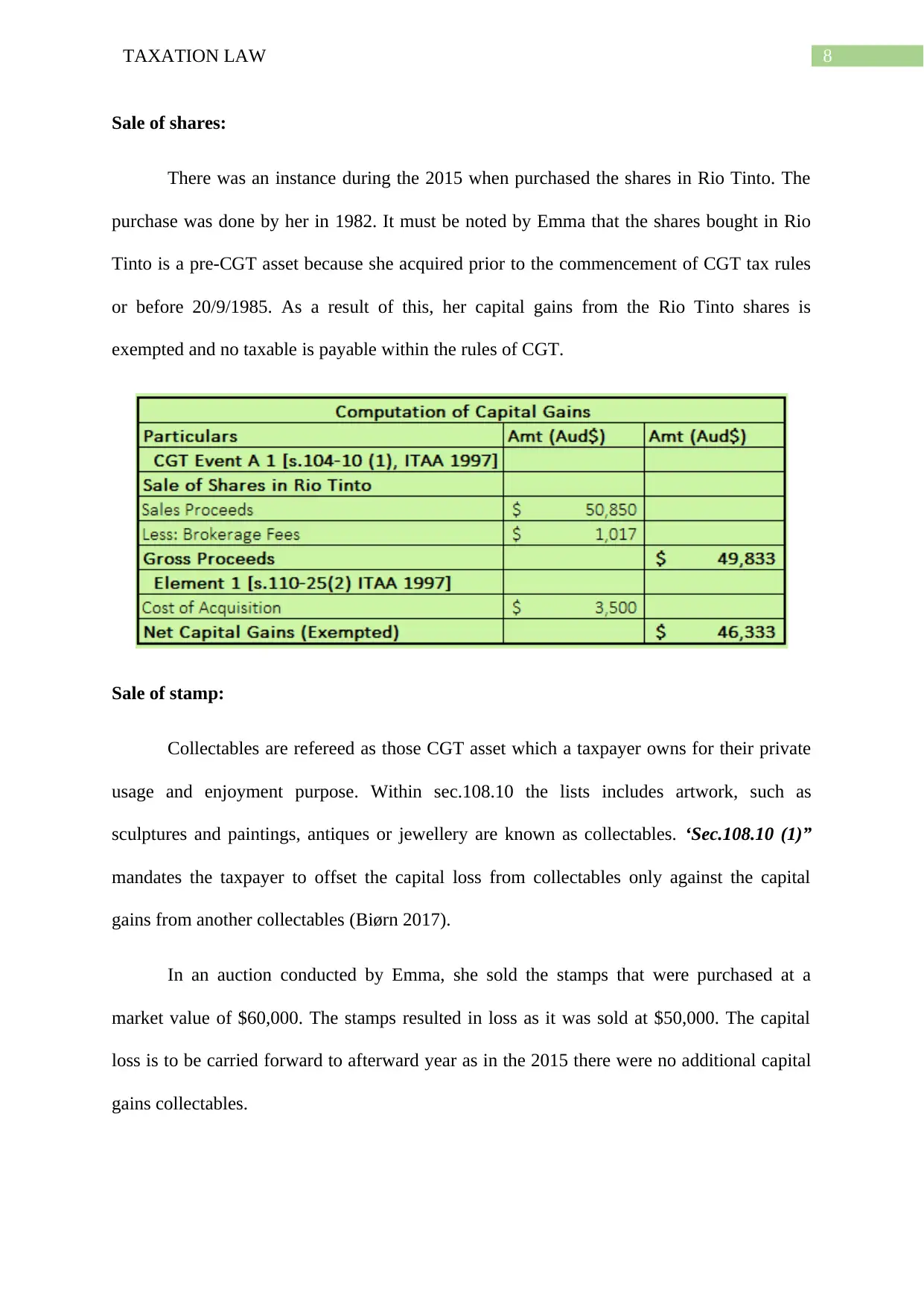

There was an instance during the 2015 when purchased the shares in Rio Tinto. The

purchase was done by her in 1982. It must be noted by Emma that the shares bought in Rio

Tinto is a pre-CGT asset because she acquired prior to the commencement of CGT tax rules

or before 20/9/1985. As a result of this, her capital gains from the Rio Tinto shares is

exempted and no taxable is payable within the rules of CGT.

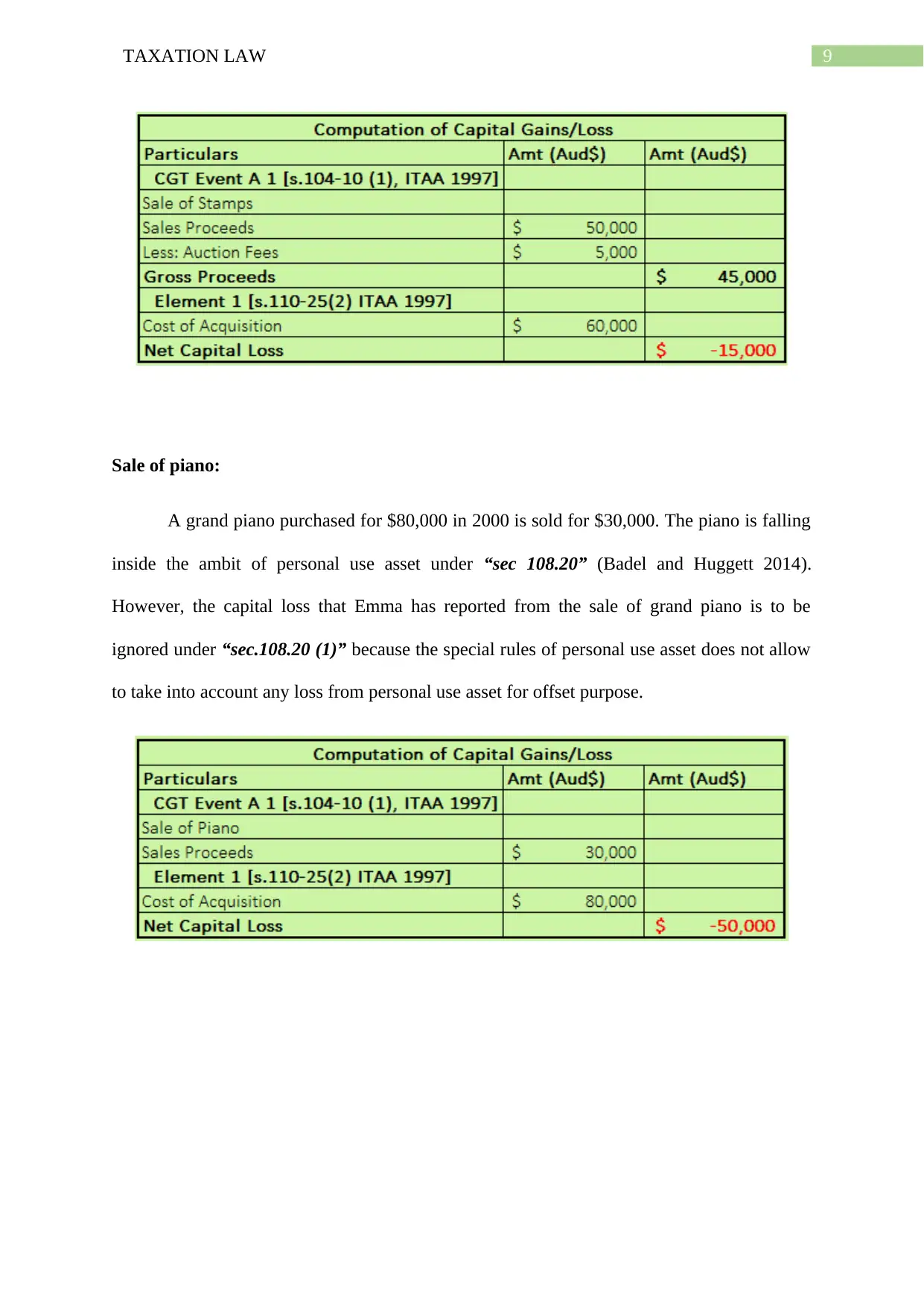

Sale of stamp:

Collectables are refereed as those CGT asset which a taxpayer owns for their private

usage and enjoyment purpose. Within sec.108.10 the lists includes artwork, such as

sculptures and paintings, antiques or jewellery are known as collectables. ‘Sec.108.10 (1)”

mandates the taxpayer to offset the capital loss from collectables only against the capital

gains from another collectables (Biørn 2017).

In an auction conducted by Emma, she sold the stamps that were purchased at a

market value of $60,000. The stamps resulted in loss as it was sold at $50,000. The capital

loss is to be carried forward to afterward year as in the 2015 there were no additional capital

gains collectables.

Sale of shares:

There was an instance during the 2015 when purchased the shares in Rio Tinto. The

purchase was done by her in 1982. It must be noted by Emma that the shares bought in Rio

Tinto is a pre-CGT asset because she acquired prior to the commencement of CGT tax rules

or before 20/9/1985. As a result of this, her capital gains from the Rio Tinto shares is

exempted and no taxable is payable within the rules of CGT.

Sale of stamp:

Collectables are refereed as those CGT asset which a taxpayer owns for their private

usage and enjoyment purpose. Within sec.108.10 the lists includes artwork, such as

sculptures and paintings, antiques or jewellery are known as collectables. ‘Sec.108.10 (1)”

mandates the taxpayer to offset the capital loss from collectables only against the capital

gains from another collectables (Biørn 2017).

In an auction conducted by Emma, she sold the stamps that were purchased at a

market value of $60,000. The stamps resulted in loss as it was sold at $50,000. The capital

loss is to be carried forward to afterward year as in the 2015 there were no additional capital

gains collectables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

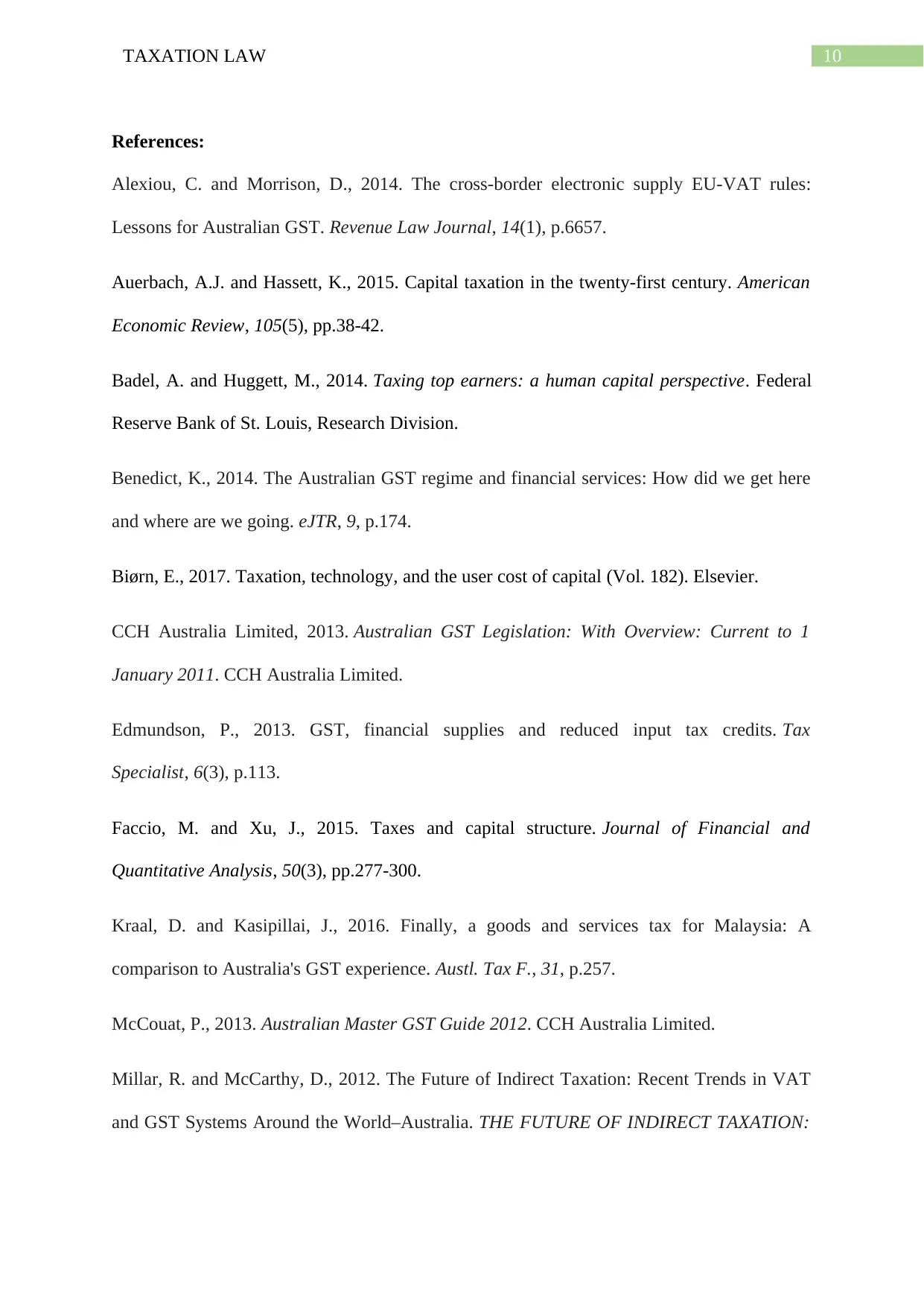

Sale of piano:

A grand piano purchased for $80,000 in 2000 is sold for $30,000. The piano is falling

inside the ambit of personal use asset under “sec 108.20” (Badel and Huggett 2014).

However, the capital loss that Emma has reported from the sale of grand piano is to be

ignored under “sec.108.20 (1)” because the special rules of personal use asset does not allow

to take into account any loss from personal use asset for offset purpose.

Sale of piano:

A grand piano purchased for $80,000 in 2000 is sold for $30,000. The piano is falling

inside the ambit of personal use asset under “sec 108.20” (Badel and Huggett 2014).

However, the capital loss that Emma has reported from the sale of grand piano is to be

ignored under “sec.108.20 (1)” because the special rules of personal use asset does not allow

to take into account any loss from personal use asset for offset purpose.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Alexiou, C. and Morrison, D., 2014. The cross-border electronic supply EU-VAT rules:

Lessons for Australian GST. Revenue Law Journal, 14(1), p.6657.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Badel, A. and Huggett, M., 2014. Taxing top earners: a human capital perspective. Federal

Reserve Bank of St. Louis, Research Division.

Benedict, K., 2014. The Australian GST regime and financial services: How did we get here

and where are we going. eJTR, 9, p.174.

Biørn, E., 2017. Taxation, technology, and the user cost of capital (Vol. 182). Elsevier.

CCH Australia Limited, 2013. Australian GST Legislation: With Overview: Current to 1

January 2011. CCH Australia Limited.

Edmundson, P., 2013. GST, financial supplies and reduced input tax credits. Tax

Specialist, 6(3), p.113.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Kraal, D. and Kasipillai, J., 2016. Finally, a goods and services tax for Malaysia: A

comparison to Australia's GST experience. Austl. Tax F., 31, p.257.

McCouat, P., 2013. Australian Master GST Guide 2012. CCH Australia Limited.

Millar, R. and McCarthy, D., 2012. The Future of Indirect Taxation: Recent Trends in VAT

and GST Systems Around the World–Australia. THE FUTURE OF INDIRECT TAXATION:

References:

Alexiou, C. and Morrison, D., 2014. The cross-border electronic supply EU-VAT rules:

Lessons for Australian GST. Revenue Law Journal, 14(1), p.6657.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Badel, A. and Huggett, M., 2014. Taxing top earners: a human capital perspective. Federal

Reserve Bank of St. Louis, Research Division.

Benedict, K., 2014. The Australian GST regime and financial services: How did we get here

and where are we going. eJTR, 9, p.174.

Biørn, E., 2017. Taxation, technology, and the user cost of capital (Vol. 182). Elsevier.

CCH Australia Limited, 2013. Australian GST Legislation: With Overview: Current to 1

January 2011. CCH Australia Limited.

Edmundson, P., 2013. GST, financial supplies and reduced input tax credits. Tax

Specialist, 6(3), p.113.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Kraal, D. and Kasipillai, J., 2016. Finally, a goods and services tax for Malaysia: A

comparison to Australia's GST experience. Austl. Tax F., 31, p.257.

McCouat, P., 2013. Australian Master GST Guide 2012. CCH Australia Limited.

Millar, R. and McCarthy, D., 2012. The Future of Indirect Taxation: Recent Trends in VAT

and GST Systems Around the World–Australia. THE FUTURE OF INDIRECT TAXATION:

11TAXATION LAW

RECENT TRENDS IN VAT AND GST SYSTEMS AROUND THE WORLD, T. Ecker, M.

Lang, and I. Lejeune, eds., Kluwer Law International: The Netherlands, pp.21-96.

Richardson, G. and Smith, D., 2013. The Readability of Australia's Goods and Services Tax

Legislation: An Empirical Investigation. Federal Law Review, 30(3), pp.475-506.

RECENT TRENDS IN VAT AND GST SYSTEMS AROUND THE WORLD, T. Ecker, M.

Lang, and I. Lejeune, eds., Kluwer Law International: The Netherlands, pp.21-96.

Richardson, G. and Smith, D., 2013. The Readability of Australia's Goods and Services Tax

Legislation: An Empirical Investigation. Federal Law Review, 30(3), pp.475-506.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.