Taxation Law Assignment: Francis and Tom's Tax Implications

VerifiedAdded on 2023/01/11

|8

|2465

|92

Homework Assignment

AI Summary

This assignment analyzes Australian taxation law through two case studies. The first case study focuses on Francis, a businessman who recently purchased a restaurant and needs to repair the kitchen. The analysis covers the deductibility of expenses related to replacing the kitchen and repairing appliances, referencing ITAA 1997 and related sections. The second case study examines Tom, a businessman and guitar teacher, and involves calculating his business income, taxable income, and tax payable for the year 2019-20, based on various income sources like sales, salary, and dividends. The assignment provides detailed calculations and explanations, considering relevant tax rules and regulations and provides a comprehensive understanding of tax implications for both individuals and businesses. It highlights key aspects of Australian taxation, including deductions and tax calculations.

Taxation Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1....................................................................................................................................1

Questions 2..................................................................................................................................3

CONCLUSION................................................................................................................................5

REFERNECES................................................................................................................................6

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1....................................................................................................................................1

Questions 2..................................................................................................................................3

CONCLUSION................................................................................................................................5

REFERNECES................................................................................................................................6

INTRODUCTION

Tax is a type of liability of every individual as well as a business because for all of them

it is very important to pay right amount of taxation on the income which is generated for the

year. If companies or entities are not able to pay the tax properly then it may result in legal

actions of the government. In Australia taxation rules are very strict and for all the individuals as

well as companies it is very important to make sure that they are following all of them pay tax

(Allen, 2018). Present report is based upon analysis of taxation laws so that understanding of

them could be enhanced. This assignment is segregated in tow parts first one is based upon

analysis of taxation rules for a commercial kitchen. The second part of the report is based upon

calculation of total and taxable income along with the total tax payable on the same. For this

purpose, different factors are focused in this project these are ITAA, 1936, ITAA 1997, their

sections, income tax rules and regulations etc.

MAIN BODY

Question 1

Francis is a business man who has bought a restaurant recently. The kitchen in it is not in

good condition and for Francis it will be very important to repair it so that all the activities in

future could be performed systematically. If the whole kitchen will be replaced then cost of it

will be around 23000 dollars and the appliances which are used in it will be replaced then the

cost of them will be 4900 dollars. Francis have decided to replace the whole kitchen with new

appliances as they are having better features and durability (Barkoczy, 2017).

All the expenses which will be made by Francis are deductible to a limit but all of them

could not be deducted. As these will be made for the purpose of repair so according to taxation

law of Australia if a restaurant which is small in size purchase business assets up to 20000

dollars then it will be deductible immediately (Australian taxation laws for deduction, 2020). If

the value of the asset will be less than this amount then the cost will be deductible from the tax

and the cost of asset will be high then it will not be deductible only 20000’s deduction will be

allowed. As Francis has planned to replace the whole kitchen with a new one and the cost of it is

23000 so the amount which will be deductible under the taxation law of Australia will be 20000.

Remaining 3000 will be deductible under the taxation rules. Francis cannot get deduction of

3000.

1

Tax is a type of liability of every individual as well as a business because for all of them

it is very important to pay right amount of taxation on the income which is generated for the

year. If companies or entities are not able to pay the tax properly then it may result in legal

actions of the government. In Australia taxation rules are very strict and for all the individuals as

well as companies it is very important to make sure that they are following all of them pay tax

(Allen, 2018). Present report is based upon analysis of taxation laws so that understanding of

them could be enhanced. This assignment is segregated in tow parts first one is based upon

analysis of taxation rules for a commercial kitchen. The second part of the report is based upon

calculation of total and taxable income along with the total tax payable on the same. For this

purpose, different factors are focused in this project these are ITAA, 1936, ITAA 1997, their

sections, income tax rules and regulations etc.

MAIN BODY

Question 1

Francis is a business man who has bought a restaurant recently. The kitchen in it is not in

good condition and for Francis it will be very important to repair it so that all the activities in

future could be performed systematically. If the whole kitchen will be replaced then cost of it

will be around 23000 dollars and the appliances which are used in it will be replaced then the

cost of them will be 4900 dollars. Francis have decided to replace the whole kitchen with new

appliances as they are having better features and durability (Barkoczy, 2017).

All the expenses which will be made by Francis are deductible to a limit but all of them

could not be deducted. As these will be made for the purpose of repair so according to taxation

law of Australia if a restaurant which is small in size purchase business assets up to 20000

dollars then it will be deductible immediately (Australian taxation laws for deduction, 2020). If

the value of the asset will be less than this amount then the cost will be deductible from the tax

and the cost of asset will be high then it will not be deductible only 20000’s deduction will be

allowed. As Francis has planned to replace the whole kitchen with a new one and the cost of it is

23000 so the amount which will be deductible under the taxation law of Australia will be 20000.

Remaining 3000 will be deductible under the taxation rules. Francis cannot get deduction of

3000.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Francis has also determined that repair of old appliances will cost around 4900 dollars

and willing to get deduction for the same. The repair of the commercial kitchen appliances could

be deducted from the total taxable income under section 25 – 10 of the Tax assessment Act 1997.

According to ITAA 1997 repair is a capital expenditure and it could be deducted from the total

taxable income so Francis will be able to get the rebate of 4900 dollars which will be made for

the repair of appliances of kitchen (ITAA 1997, 2020).

The section 25 – 10 of the ITAA 1997 states that when the property is bought from

another party and the new owners have decided to spend some money on the repair then it will

be allowed to deducted form the total taxable income. This section states that initial repair which

will be made by the tax payer that remedies some defects in the property of reduce the damage to

it could be deducted from the total income. Initial repair is the repair which is made to the

property for the first time but the kitchen appliances in the commercial kitchen of the restaurant

would have repaired by the old owner. This tax consequence could be faced by Francis because

the repair will not be made for the first time. In order to deal with it, Francis will be required to

be aware of all the rules of section 25 – 10 of ITAA 1997. According to 5th regulation of the

section if the property is bought recently and the repair will be made after acquisition then it will

be treated as initial repair because it will be made by new owner for the property. When a newly

bought property is damaged and require repair then all the expenses which will be made by the

new owner are deductible under the taxation law as it will be treated as initial repair (Haines,

2017).

While planning to get the rebate of 4900 dollars which will be spent by Francis for the

repair of old appliances it will be very important to make sure that these expenses are not

covering maintenance. According to Section 8 – 1 and 42 – 15 of ITAA 1997 the repair may

include the expenses of maintenance but it will be allowed for deduction when it is done in

conjunction with the work which is repair. Only maintenance expenses could not be included in

the repair cost and if it will be done by an entity then it will be treated as legal offence and no

deduction will be allowed to the tax payer (Hobson, 2019).

In order to get the deductions, it will be very important for Francis to have detailed

information of all the laws or hire a tax consultant who can provide appropriate information of it.

The material facts which are required to be focused by Francis for the commercial kitchen are as

follows:

2

and willing to get deduction for the same. The repair of the commercial kitchen appliances could

be deducted from the total taxable income under section 25 – 10 of the Tax assessment Act 1997.

According to ITAA 1997 repair is a capital expenditure and it could be deducted from the total

taxable income so Francis will be able to get the rebate of 4900 dollars which will be made for

the repair of appliances of kitchen (ITAA 1997, 2020).

The section 25 – 10 of the ITAA 1997 states that when the property is bought from

another party and the new owners have decided to spend some money on the repair then it will

be allowed to deducted form the total taxable income. This section states that initial repair which

will be made by the tax payer that remedies some defects in the property of reduce the damage to

it could be deducted from the total income. Initial repair is the repair which is made to the

property for the first time but the kitchen appliances in the commercial kitchen of the restaurant

would have repaired by the old owner. This tax consequence could be faced by Francis because

the repair will not be made for the first time. In order to deal with it, Francis will be required to

be aware of all the rules of section 25 – 10 of ITAA 1997. According to 5th regulation of the

section if the property is bought recently and the repair will be made after acquisition then it will

be treated as initial repair because it will be made by new owner for the property. When a newly

bought property is damaged and require repair then all the expenses which will be made by the

new owner are deductible under the taxation law as it will be treated as initial repair (Haines,

2017).

While planning to get the rebate of 4900 dollars which will be spent by Francis for the

repair of old appliances it will be very important to make sure that these expenses are not

covering maintenance. According to Section 8 – 1 and 42 – 15 of ITAA 1997 the repair may

include the expenses of maintenance but it will be allowed for deduction when it is done in

conjunction with the work which is repair. Only maintenance expenses could not be included in

the repair cost and if it will be done by an entity then it will be treated as legal offence and no

deduction will be allowed to the tax payer (Hobson, 2019).

In order to get the deductions, it will be very important for Francis to have detailed

information of all the laws or hire a tax consultant who can provide appropriate information of it.

The material facts which are required to be focused by Francis for the commercial kitchen are as

follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The total cost of repair does not include only the maintenance amount as maintenances

are not allowed to be deducted from the taxable income according to section 8 – 1 and 42

– 15 of ITAA 1997.

If the maintenance is included in the cost of repair then it should be made in conjunction.

In this case the total amount of repair will be deducted from the taxation liability.

The total deduction related to the replacing the whole kitchen will be limited to 20000

dollars according to Australian taxation law. Francis cannot claim the total value of

replacement which is 23000 dollars (Hodgson, Castelyn and Marriott, 2019).

In order to ignore the potential implications of all the above described material facts

Francis will be required to claim the appropriate deductions. It can help to comply with all the

Australian Taxation laws.

The taxation rule which was required to be followed by all the companies which are

operating business in Australia was ITAA 1936 (ITAA 1936, 2020). There were some specific

amendments were made in it and ITAA 1997 was launched. According to the old rule all the

expenses which will be made for replacement by small restaurants will be allowed for deduction

but in the new rule some changes were made in context to it and the limit for 20000 dollars was

made. It was made because if small restaurants can make replacements of over 30000 or 50000

then they will not be treated as small. They will have to follow the taxation rules that are made

for medium sized or large entities. One of the key issues which may take place for Francis in

future in context of tax is lack of awareness of amendments in ITAA 1936. If the new owners

will file the taxation law by deducting the total cost of replacement which is 23000 then it will

not be allowed. It may also result in legal actions. In order to ignore this consequence Francis

will be required to follow the taxation rules that are amended under ITAA 1997. There are

various new matters are now added in it so that accurate tax liability could be analysed.

Questions 2

Tom is a business man and owns a business named Tom’s Band. It is established in

Westfield and musical instruments are sold by it in the market. Tom is also a guitar teacher.

There are several incomes were received by Tom for year ending 2019 – 20. It has been

proposed that no deductions will be allowed to Tom for the year and the business income,

taxable income, tax and tax payable on the same is require dot be calculated (Kenny, Blissenden

and Villios, 2017). The calculations of the same are as follows:

3

are not allowed to be deducted from the taxable income according to section 8 – 1 and 42

– 15 of ITAA 1997.

If the maintenance is included in the cost of repair then it should be made in conjunction.

In this case the total amount of repair will be deducted from the taxation liability.

The total deduction related to the replacing the whole kitchen will be limited to 20000

dollars according to Australian taxation law. Francis cannot claim the total value of

replacement which is 23000 dollars (Hodgson, Castelyn and Marriott, 2019).

In order to ignore the potential implications of all the above described material facts

Francis will be required to claim the appropriate deductions. It can help to comply with all the

Australian Taxation laws.

The taxation rule which was required to be followed by all the companies which are

operating business in Australia was ITAA 1936 (ITAA 1936, 2020). There were some specific

amendments were made in it and ITAA 1997 was launched. According to the old rule all the

expenses which will be made for replacement by small restaurants will be allowed for deduction

but in the new rule some changes were made in context to it and the limit for 20000 dollars was

made. It was made because if small restaurants can make replacements of over 30000 or 50000

then they will not be treated as small. They will have to follow the taxation rules that are made

for medium sized or large entities. One of the key issues which may take place for Francis in

future in context of tax is lack of awareness of amendments in ITAA 1936. If the new owners

will file the taxation law by deducting the total cost of replacement which is 23000 then it will

not be allowed. It may also result in legal actions. In order to ignore this consequence Francis

will be required to follow the taxation rules that are amended under ITAA 1997. There are

various new matters are now added in it so that accurate tax liability could be analysed.

Questions 2

Tom is a business man and owns a business named Tom’s Band. It is established in

Westfield and musical instruments are sold by it in the market. Tom is also a guitar teacher.

There are several incomes were received by Tom for year ending 2019 – 20. It has been

proposed that no deductions will be allowed to Tom for the year and the business income,

taxable income, tax and tax payable on the same is require dot be calculated (Kenny, Blissenden

and Villios, 2017). The calculations of the same are as follows:

3

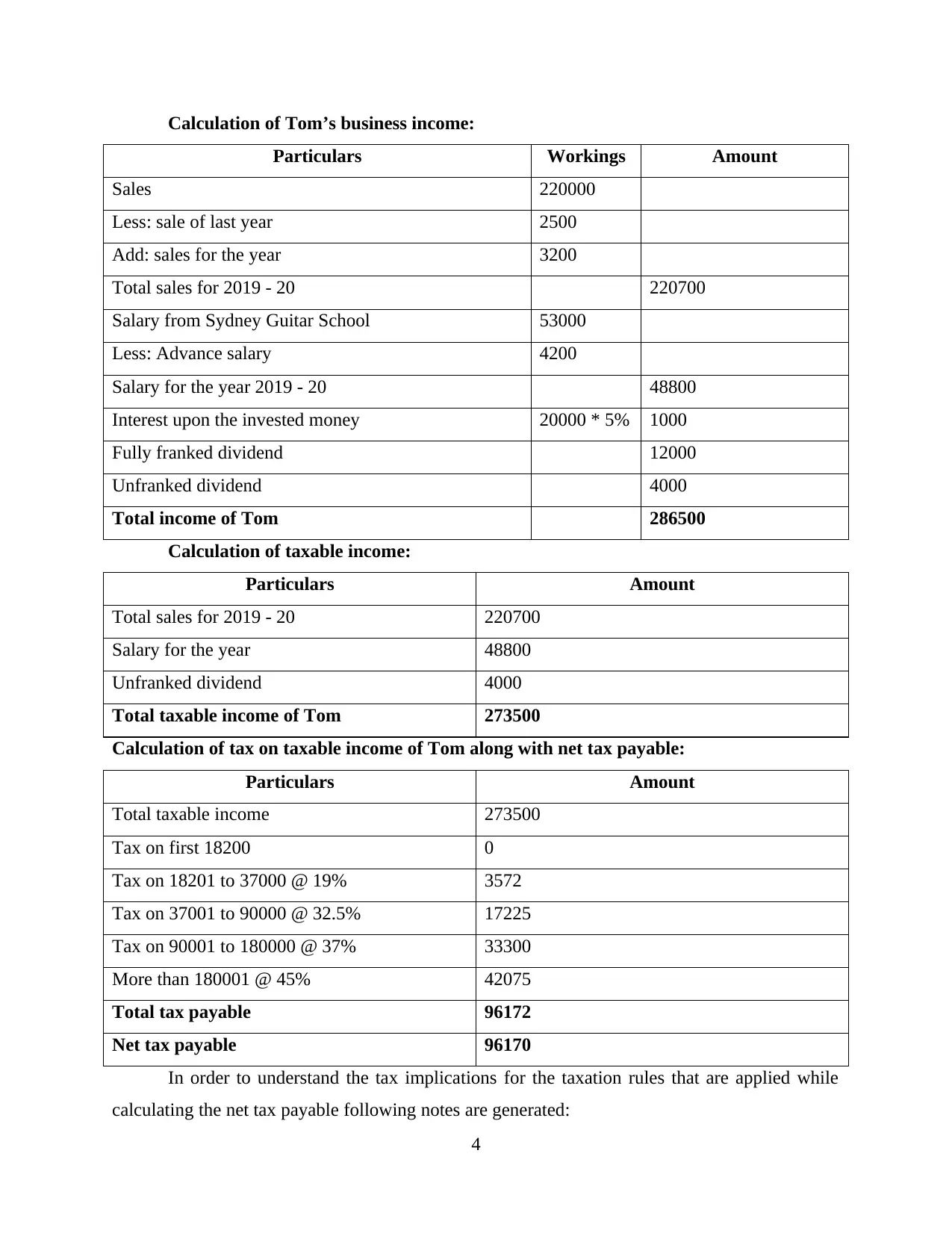

Calculation of Tom’s business income:

Particulars Workings Amount

Sales 220000

Less: sale of last year 2500

Add: sales for the year 3200

Total sales for 2019 - 20 220700

Salary from Sydney Guitar School 53000

Less: Advance salary 4200

Salary for the year 2019 - 20 48800

Interest upon the invested money 20000 * 5% 1000

Fully franked dividend 12000

Unfranked dividend 4000

Total income of Tom 286500

Calculation of taxable income:

Particulars Amount

Total sales for 2019 - 20 220700

Salary for the year 48800

Unfranked dividend 4000

Total taxable income of Tom 273500

Calculation of tax on taxable income of Tom along with net tax payable:

Particulars Amount

Total taxable income 273500

Tax on first 18200 0

Tax on 18201 to 37000 @ 19% 3572

Tax on 37001 to 90000 @ 32.5% 17225

Tax on 90001 to 180000 @ 37% 33300

More than 180001 @ 45% 42075

Total tax payable 96172

Net tax payable 96170

In order to understand the tax implications for the taxation rules that are applied while

calculating the net tax payable following notes are generated:

4

Particulars Workings Amount

Sales 220000

Less: sale of last year 2500

Add: sales for the year 3200

Total sales for 2019 - 20 220700

Salary from Sydney Guitar School 53000

Less: Advance salary 4200

Salary for the year 2019 - 20 48800

Interest upon the invested money 20000 * 5% 1000

Fully franked dividend 12000

Unfranked dividend 4000

Total income of Tom 286500

Calculation of taxable income:

Particulars Amount

Total sales for 2019 - 20 220700

Salary for the year 48800

Unfranked dividend 4000

Total taxable income of Tom 273500

Calculation of tax on taxable income of Tom along with net tax payable:

Particulars Amount

Total taxable income 273500

Tax on first 18200 0

Tax on 18201 to 37000 @ 19% 3572

Tax on 37001 to 90000 @ 32.5% 17225

Tax on 90001 to 180000 @ 37% 33300

More than 180001 @ 45% 42075

Total tax payable 96172

Net tax payable 96170

In order to understand the tax implications for the taxation rules that are applied while

calculating the net tax payable following notes are generated:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales for last year us deducted from the total value of sales because the income of past

years would have taxed in the same year. If the income for the year in received in

upcoming year then also it is taxed in the same year when it was generated.

The sale of 3200 which is made for current year but the amount of it is not recovered is

added to the present year’s sales because it is income of present year and it is also taxable

for the same year (Trad and Freudenberg, 2018).

Tom has received advance salary for the July Month for the long leave. As it is not

related to current year so it is deducted from the income of year 2019 – 20. This step is

taken to analyse the actual income for the year.

Fully franked credit of worth 5143 were not deducted from the dividend as these were the

part of income and it will be treated as the income for Tom so it is not deducted from the

total dividends (Wu and Tran-Nam, 2017).

While calculating the taxable income for Frank fully franked dividends were not taken in

to consideration because all the dividends which are received as fully franked are taxable

for the companies not investors. On the other hand, dividends which are not fully franked

are taxable foe the investors so the amount of 4000 is considered as the part of taxable

income for Tom for year 2019 – 20.

The total tax on the income of Tom is calculated according to taxation rules and

regulations of Australia (Australian tax percentage for business, 2020).

CONCLUSION

From the above project report, it has been concluded that for all the individuals as well as

the businesses it is very important to pay the appropriate tax on income. It can help to ignore the

legal consequences that may take place in future. There are various taxation rules that are

required to be followed by all the individuals as well as entities operating business in Australia.

These are ITAA 1936, ITAA 1997, Australian taxation rules etc. By complying with all of them

all the business can pay the appropriate tax on the income.

5

years would have taxed in the same year. If the income for the year in received in

upcoming year then also it is taxed in the same year when it was generated.

The sale of 3200 which is made for current year but the amount of it is not recovered is

added to the present year’s sales because it is income of present year and it is also taxable

for the same year (Trad and Freudenberg, 2018).

Tom has received advance salary for the July Month for the long leave. As it is not

related to current year so it is deducted from the income of year 2019 – 20. This step is

taken to analyse the actual income for the year.

Fully franked credit of worth 5143 were not deducted from the dividend as these were the

part of income and it will be treated as the income for Tom so it is not deducted from the

total dividends (Wu and Tran-Nam, 2017).

While calculating the taxable income for Frank fully franked dividends were not taken in

to consideration because all the dividends which are received as fully franked are taxable

for the companies not investors. On the other hand, dividends which are not fully franked

are taxable foe the investors so the amount of 4000 is considered as the part of taxable

income for Tom for year 2019 – 20.

The total tax on the income of Tom is calculated according to taxation rules and

regulations of Australia (Australian tax percentage for business, 2020).

CONCLUSION

From the above project report, it has been concluded that for all the individuals as well as

the businesses it is very important to pay the appropriate tax on income. It can help to ignore the

legal consequences that may take place in future. There are various taxation rules that are

required to be followed by all the individuals as well as entities operating business in Australia.

These are ITAA 1936, ITAA 1997, Australian taxation rules etc. By complying with all of them

all the business can pay the appropriate tax on the income.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERNECES

Books and Journals:

Allen, C., 2018. Potential failure of the Australian CFC rules in the digital economy. Australian

Tax Review. 47(2). pp.114-127.

Barkoczy, S., 2017. Core tax legislation and study guide. OUP Catalogue.

Haines, A., 2017. Rio Tinto to challenge A $447 million Australian tax bill. International Tax

Review.

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian Tax

Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences,

The Australian National University.

Hodgson, H., Castelyn, D. and Marriott, L., 2019. Income equalisation: is all fair in primary

production and tax law?. In Australian Tax Forum: a journal of taxation policy, law and

reform (Vol. 34, No. 2).

Kenny, P., Blissenden, M. and Villios, S., 2017. Wine options of Australian tax

reform. eJTR. 15. p.22.

Trad, B. and Freudenberg, B., 2018. A Dual Income Tax System for Australian Small Business:

Achieving Greater Tax Neutrality. J. Austl. Tax'n. 20. p.93.

Wu, H. and Tran-Nam, B., 2017. Estimating Aggregate Tax Complicate Costs: A New Approach

Using a State Space Model. Austl. Tax F.. 32. p.197.

Online

ITAA 1997. 2020. [Online]. Available through:

<https://www.ato.gov.au/law/view/document?docid=TXR/TR9723/nat/ato/00001>

ITAA 1936. 2020. [Online]. Available through:

<https://www.legislation.gov.au/Details/C2009C00176>

Australian taxation laws for deduction. 2020. [Online]. Available through:

<http://rca.asn.au/magazine/get-deductions-right/>

Australian tax percentage for business. 2020. [Online]. Available through:

<https://www.canstar.com.au/calculators/income-tax-calculator/>

6

Books and Journals:

Allen, C., 2018. Potential failure of the Australian CFC rules in the digital economy. Australian

Tax Review. 47(2). pp.114-127.

Barkoczy, S., 2017. Core tax legislation and study guide. OUP Catalogue.

Haines, A., 2017. Rio Tinto to challenge A $447 million Australian tax bill. International Tax

Review.

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian Tax

Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences,

The Australian National University.

Hodgson, H., Castelyn, D. and Marriott, L., 2019. Income equalisation: is all fair in primary

production and tax law?. In Australian Tax Forum: a journal of taxation policy, law and

reform (Vol. 34, No. 2).

Kenny, P., Blissenden, M. and Villios, S., 2017. Wine options of Australian tax

reform. eJTR. 15. p.22.

Trad, B. and Freudenberg, B., 2018. A Dual Income Tax System for Australian Small Business:

Achieving Greater Tax Neutrality. J. Austl. Tax'n. 20. p.93.

Wu, H. and Tran-Nam, B., 2017. Estimating Aggregate Tax Complicate Costs: A New Approach

Using a State Space Model. Austl. Tax F.. 32. p.197.

Online

ITAA 1997. 2020. [Online]. Available through:

<https://www.ato.gov.au/law/view/document?docid=TXR/TR9723/nat/ato/00001>

ITAA 1936. 2020. [Online]. Available through:

<https://www.legislation.gov.au/Details/C2009C00176>

Australian taxation laws for deduction. 2020. [Online]. Available through:

<http://rca.asn.au/magazine/get-deductions-right/>

Australian tax percentage for business. 2020. [Online]. Available through:

<https://www.canstar.com.au/calculators/income-tax-calculator/>

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.