LAW5230 Taxation Law Assignment: Problem Solving & Research, 2019

VerifiedAdded on 2022/08/28

|19

|5062

|16

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing both a problem-solving scenario (Part A) and a research-based component (Part B). Part A analyzes the residency status and assessable income of Catherine, a working holidaymaker in Australia, under the ITAA 1936 and ITAA 1997, considering relevant case law such as Gregory v FC of T and Nathan v FCT. It examines whether Catherine is a resident or foreign resident and determines which income is taxable. Part B delves into Australia's residency rules, comparing them to New Zealand's and critically evaluating potential amendments suggested by the Board of Taxation, including the 'resides test' and the '183-day test'. The assignment explores the evolution of these rules and their implications in a globalized world, offering recommendations for improvements to ensure equity, simplicity, integrity, and efficiency. The references include various taxation law textbooks and guides.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................2

Conclusion:............................................................................................................................5

Requirement (I):.....................................................................................................................5

Requirement (II):....................................................................................................................5

References:.................................................................................................................................6

Part B: Australia’s Residency Rules:.........................................................................................7

References:...............................................................................................................................17

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................2

Conclusion:............................................................................................................................5

Requirement (I):.....................................................................................................................5

Requirement (II):....................................................................................................................5

References:.................................................................................................................................6

Part B: Australia’s Residency Rules:.........................................................................................7

References:...............................................................................................................................17

2TAXATION LAW

Part A:

Issues:

Will Catherine working in Australia on twelve months working holiday, will be

viewed as resident under “section 6 (1) ITAA 1936” or a foreign resident under

“section 6-5 (3) ITAA 1997”?

Is the income earned by Catherine could be added in her assessable income and

charged taxable inside the ordinary concept of “section 6-5, ITAA 1997”?

Laws: “Section 6 (1) ITAA 1997” “Section 6-5 (2) ITAA 1997” “Section 6-5 (3) ITAA 1997” “Gregory v FC of T (1937)” “Nathan v FCT (1918)” “Moore v Griffiths (1972)” “FCT v Spotless Services (1995)”

Application:

As in the concern of residential purpose, Catherine will not be considered as

Australian resident even though he used to stay in Australia for 12 months. In other

perspective, Catherine is a foreign resident under “section 6-5 (3) ITAA 1997”. Citing

“Gregory v FC of T (1937)” even though Catherine stayed in Australia during a period of 12

months, her characteristics shows that she was a visitor1. The main objective was to enjoy a

1 Deutsch, Robert Et Al. Australian Tax Handbook 2018. [Place Of Publication Not

Identified]: Thomson Reuters Australia, 2018.

Part A:

Issues:

Will Catherine working in Australia on twelve months working holiday, will be

viewed as resident under “section 6 (1) ITAA 1936” or a foreign resident under

“section 6-5 (3) ITAA 1997”?

Is the income earned by Catherine could be added in her assessable income and

charged taxable inside the ordinary concept of “section 6-5, ITAA 1997”?

Laws: “Section 6 (1) ITAA 1997” “Section 6-5 (2) ITAA 1997” “Section 6-5 (3) ITAA 1997” “Gregory v FC of T (1937)” “Nathan v FCT (1918)” “Moore v Griffiths (1972)” “FCT v Spotless Services (1995)”

Application:

As in the concern of residential purpose, Catherine will not be considered as

Australian resident even though he used to stay in Australia for 12 months. In other

perspective, Catherine is a foreign resident under “section 6-5 (3) ITAA 1997”. Citing

“Gregory v FC of T (1937)” even though Catherine stayed in Australia during a period of 12

months, her characteristics shows that she was a visitor1. The main objective was to enjoy a

1 Deutsch, Robert Et Al. Australian Tax Handbook 2018. [Place Of Publication Not

Identified]: Thomson Reuters Australia, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

working holiday in Australia and invest the same with the help of casual employment and

intermittent work. At the time of staying in Brisbane she did not explore any place as it was

also her “home” or different from any other place where someone stay as they were on

working holiday2. Following to the description made by the ATO it should be noted that

maximum number of people who came to Australia for a working holiday or visit are not

treated as Australian resident under the ordinary meaning of “section 6 (1) ITAA 1997”.

The prime motive of treating Catherine as a non-resident as her visit was more

consistent along with her visa requirements and she did not have any intention for staying in

Australia; however, she had the motive of enjoying a holiday with working for a short-term

period. Unlike majority of the people, Catherine holds the working and holiday visas, which

was consistent what her visa demands and she did not carry any motive to stay in Australia.

She just wanted to enjoy the change for a while with her work, before coming back to home.

Not following to the other individuals, her behaviour was not consistent as per her

purpose of visit and not so consistent with Australian possessor. Hence Catherine will not be

considered as an Australian resident within the ordinary concept of “section 6 (1) ITAA

1997” because she rented a house and stayed in a sharing basis with her colleague for the

extended time period3. Since the working holidaymaker, the first $37,000 of Catherine’s

income will be levied on tax at the rate of 15 percent and the balance is taxed at an ordinary

rate.

2 Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 principles of business

taxation.

3 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018.

working holiday in Australia and invest the same with the help of casual employment and

intermittent work. At the time of staying in Brisbane she did not explore any place as it was

also her “home” or different from any other place where someone stay as they were on

working holiday2. Following to the description made by the ATO it should be noted that

maximum number of people who came to Australia for a working holiday or visit are not

treated as Australian resident under the ordinary meaning of “section 6 (1) ITAA 1997”.

The prime motive of treating Catherine as a non-resident as her visit was more

consistent along with her visa requirements and she did not have any intention for staying in

Australia; however, she had the motive of enjoying a holiday with working for a short-term

period. Unlike majority of the people, Catherine holds the working and holiday visas, which

was consistent what her visa demands and she did not carry any motive to stay in Australia.

She just wanted to enjoy the change for a while with her work, before coming back to home.

Not following to the other individuals, her behaviour was not consistent as per her

purpose of visit and not so consistent with Australian possessor. Hence Catherine will not be

considered as an Australian resident within the ordinary concept of “section 6 (1) ITAA

1997” because she rented a house and stayed in a sharing basis with her colleague for the

extended time period3. Since the working holidaymaker, the first $37,000 of Catherine’s

income will be levied on tax at the rate of 15 percent and the balance is taxed at an ordinary

rate.

2 Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 principles of business

taxation.

3 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Except the residential status of Catherine, the sources of generating income are

specifically relevant for the Non-residents. Referring to “Nathan v FCT (1918)” the main

source of income is ethically practical, hard matter of concern. Apportionment will be

considered in an appropriate manner where the income is earned from the various sources4.

Salary that generate from employment in Wales, which was earned by Catherine did not have

any Australian sources and thus it is not involved with her assessable income. Her income

will be assessed if she has been paid out for her work like in cafe, hotel and cattle station, as

this income is came from Australian sources.

Catherine has been also conferred by the prize winnings of $250. Citing “Moore v

Griffiths (1972)”, since the value of $250 was mere income from other sources like prize

winning hence it was not considered as taxable. While she also reports an interest, income of

$50 received from Australian bank account5. Citing “FCT v Spotless Services (1995)”,

Catherine has received an interest from Australian bank account, which has indigenous

sources and will be subjected to tax.

Further reports sent by Catherine, over selling of clothing, sleeping bags and other

personal items through the eBay in the month of June before leaving Australia. However,

Catherine was not carrying out any business in online selling, amounting of $350 thus it will

not be proposed to tax in her assessable income6.

4 Taylor, C. J et al. Understanding taxation law 2018.

5 McCouat, Philip. Australian master GST guide 2018.

6 Sadiq, Kerrie et al. Principles of taxation law 2018.

Except the residential status of Catherine, the sources of generating income are

specifically relevant for the Non-residents. Referring to “Nathan v FCT (1918)” the main

source of income is ethically practical, hard matter of concern. Apportionment will be

considered in an appropriate manner where the income is earned from the various sources4.

Salary that generate from employment in Wales, which was earned by Catherine did not have

any Australian sources and thus it is not involved with her assessable income. Her income

will be assessed if she has been paid out for her work like in cafe, hotel and cattle station, as

this income is came from Australian sources.

Catherine has been also conferred by the prize winnings of $250. Citing “Moore v

Griffiths (1972)”, since the value of $250 was mere income from other sources like prize

winning hence it was not considered as taxable. While she also reports an interest, income of

$50 received from Australian bank account5. Citing “FCT v Spotless Services (1995)”,

Catherine has received an interest from Australian bank account, which has indigenous

sources and will be subjected to tax.

Further reports sent by Catherine, over selling of clothing, sleeping bags and other

personal items through the eBay in the month of June before leaving Australia. However,

Catherine was not carrying out any business in online selling, amounting of $350 thus it will

not be proposed to tax in her assessable income6.

4 Taylor, C. J et al. Understanding taxation law 2018.

5 McCouat, Philip. Australian master GST guide 2018.

6 Sadiq, Kerrie et al. Principles of taxation law 2018.

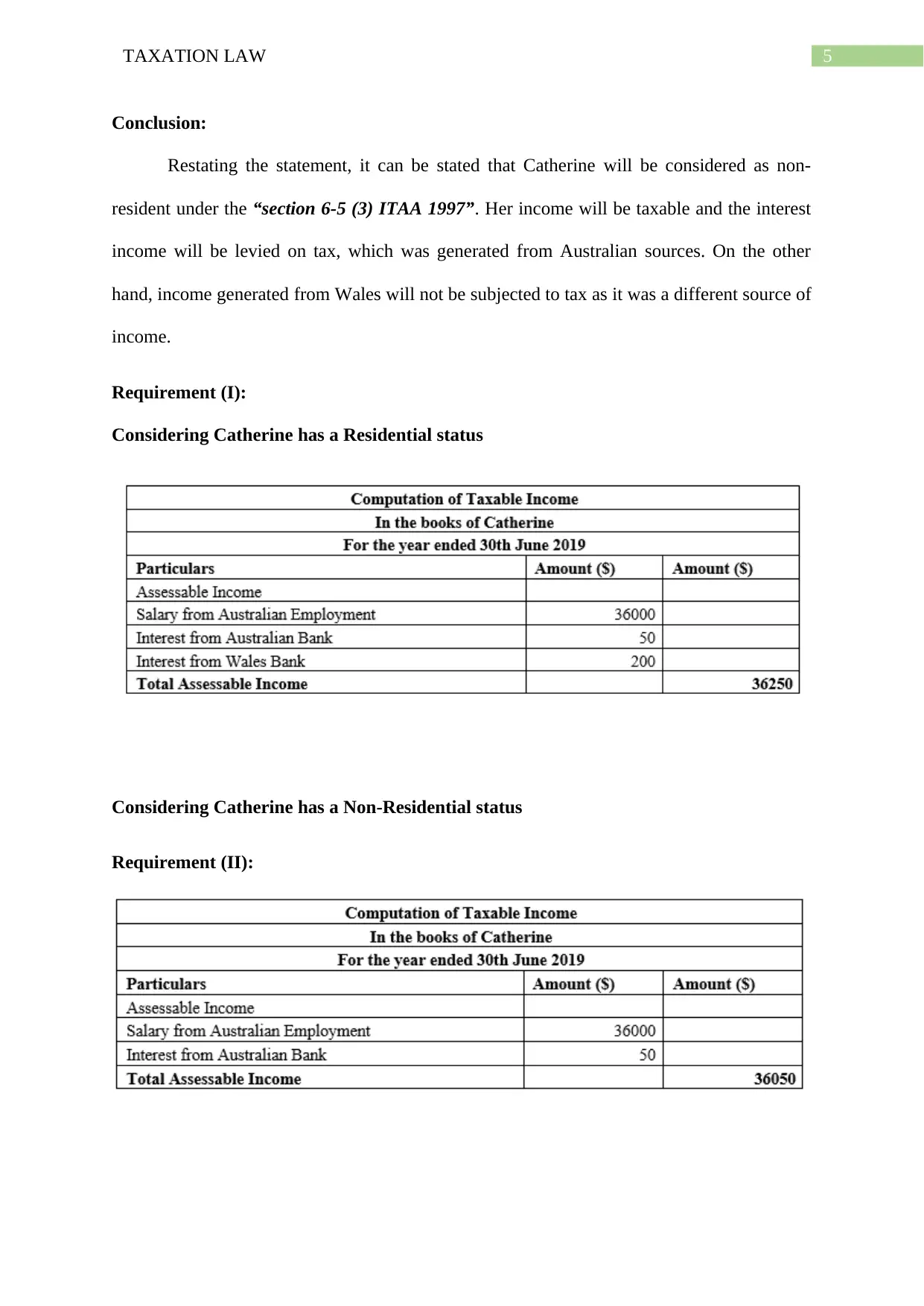

5TAXATION LAW

Conclusion:

Restating the statement, it can be stated that Catherine will be considered as non-

resident under the “section 6-5 (3) ITAA 1997”. Her income will be taxable and the interest

income will be levied on tax, which was generated from Australian sources. On the other

hand, income generated from Wales will not be subjected to tax as it was a different source of

income.

Requirement (I):

Considering Catherine has a Residential status

Considering Catherine has a Non-Residential status

Requirement (II):

Conclusion:

Restating the statement, it can be stated that Catherine will be considered as non-

resident under the “section 6-5 (3) ITAA 1997”. Her income will be taxable and the interest

income will be levied on tax, which was generated from Australian sources. On the other

hand, income generated from Wales will not be subjected to tax as it was a different source of

income.

Requirement (I):

Considering Catherine has a Residential status

Considering Catherine has a Non-Residential status

Requirement (II):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

References:

Deutsch, Robert Et Al. Australian Tax Handbook 2018. [Place Of Publication Not

Identified]: Thomson Reuters Australia, 2018.

Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 principles of business

taxation.

Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018.

McCouat, Philip. Australian master GST guide 2018.

Sadiq, Kerrie et al. Principles of taxation law 2018.

Taylor, C. J et al. Understanding taxation law 2018.

References:

Deutsch, Robert Et Al. Australian Tax Handbook 2018. [Place Of Publication Not

Identified]: Thomson Reuters Australia, 2018.

Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 principles of business

taxation.

Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018.

McCouat, Philip. Australian master GST guide 2018.

Sadiq, Kerrie et al. Principles of taxation law 2018.

Taylor, C. J et al. Understanding taxation law 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Part B: Australia’s Residency Rules:

Introduction:

The main area of international taxation has been designed by rise in globalization that

creates an impact on the trade and flow of capital. Peoples are now moving their employment

capital from one place to another place in more frequent way than before and companies have

expanding business intentions and transactions with jurisdictions out of Australia (Miller and

Oats 2016). The main purpose of taking into account the fundaments relating to international

taxation is to obtain an understanding when the taxpayers or the amounts falls inside the tax

jurisdiction of Australia and how claims associated to taxation would interact with the other

nations.

Recently, the tax policy considerations relating to global taxation system have placed

their focus on making sure that the international tax relating to tax are suitable and adequately

robust to deal with rising globalization of organizations and their workers. (Barkoczy 2016)

The taxation board of Australia opinions that it is now time to place focus on whether the

Australian individual income tax residency rules continue to be sufficient, taking into account

the Australia’s changing modern economy and civilization and in respect of the integrity

concerns raised with the board of taxation.

In this essay, the residency rules currently applied to an individual taxpayer on

Australia will be considered. A critical evaluation of the board of taxation recently made

suggestion of amending the residency rules along with the case laws. A comparative

evaluation of Australia’s residency rules with New Zealand will be considered as well,

combined with a conclusive recommendations as whether the present rules needs to be

modified to better suit the principles of equity, simplicity, integrity and efficiency.

Part B: Australia’s Residency Rules:

Introduction:

The main area of international taxation has been designed by rise in globalization that

creates an impact on the trade and flow of capital. Peoples are now moving their employment

capital from one place to another place in more frequent way than before and companies have

expanding business intentions and transactions with jurisdictions out of Australia (Miller and

Oats 2016). The main purpose of taking into account the fundaments relating to international

taxation is to obtain an understanding when the taxpayers or the amounts falls inside the tax

jurisdiction of Australia and how claims associated to taxation would interact with the other

nations.

Recently, the tax policy considerations relating to global taxation system have placed

their focus on making sure that the international tax relating to tax are suitable and adequately

robust to deal with rising globalization of organizations and their workers. (Barkoczy 2016)

The taxation board of Australia opinions that it is now time to place focus on whether the

Australian individual income tax residency rules continue to be sufficient, taking into account

the Australia’s changing modern economy and civilization and in respect of the integrity

concerns raised with the board of taxation.

In this essay, the residency rules currently applied to an individual taxpayer on

Australia will be considered. A critical evaluation of the board of taxation recently made

suggestion of amending the residency rules along with the case laws. A comparative

evaluation of Australia’s residency rules with New Zealand will be considered as well,

combined with a conclusive recommendations as whether the present rules needs to be

modified to better suit the principles of equity, simplicity, integrity and efficiency.

8TAXATION LAW

Discussion:

During the year 1930, Australia decided to replace its actual territorial based personal

income tax system with the residency based tax system. Ever since 1st July 1930 an individual

who is considered as the resident of Australia will be considered taxable in Australia on all

the income derived from the worldwide sources, while individual who is not held as resident

of Australia or non-resident are commonly considered taxable for income that is sourced in

Australia (Gashenko, Zima and Davidyan 2019). More precisely, an individual that are

considered resident will be considered as the subject of tax only for the income that are above

the tax-free threshold. The Medicare levy is only applicable on the residents. The non-

resident withholding taxes are only applicable on certain types of income. A wide range of

CGT concessions is also made available to the residents as well. All these consequences

suggest that there is a significant amount of variation in the tax liability of an individual

would originate solely on the basis of whether they are held as resident or non-resident.

As stated by (Morgan and Castelyn 2018) the residency status of a person is

ascertained for taxation purpose in agreement with the definition that has been operating ever

since 1st July 1930. According to “subsection 6 (1) ITAA 1936” resident includes someone

apart from company, that resides in Australia and comprises of a person that has the domicile

in Australia except the commissioner is content that an individual has the permanent dwelling

place outside Australia. As apparent there are four types of test to ascertain whether a person

is held to be an Australian resident within the definition. Firstly, it involves residency in

agreement with the ordinary concepts. Secondly, it involves the domicile test or the test of

permanent place of abode (Du Preez 2016). Third test is the 183-day test and lastly, the

commonwealth superannuation fund test. In order to be viewed as resident a person is only

needed to be pass one of the above given test in order to be held as a resident of Australia.

Discussion:

During the year 1930, Australia decided to replace its actual territorial based personal

income tax system with the residency based tax system. Ever since 1st July 1930 an individual

who is considered as the resident of Australia will be considered taxable in Australia on all

the income derived from the worldwide sources, while individual who is not held as resident

of Australia or non-resident are commonly considered taxable for income that is sourced in

Australia (Gashenko, Zima and Davidyan 2019). More precisely, an individual that are

considered resident will be considered as the subject of tax only for the income that are above

the tax-free threshold. The Medicare levy is only applicable on the residents. The non-

resident withholding taxes are only applicable on certain types of income. A wide range of

CGT concessions is also made available to the residents as well. All these consequences

suggest that there is a significant amount of variation in the tax liability of an individual

would originate solely on the basis of whether they are held as resident or non-resident.

As stated by (Morgan and Castelyn 2018) the residency status of a person is

ascertained for taxation purpose in agreement with the definition that has been operating ever

since 1st July 1930. According to “subsection 6 (1) ITAA 1936” resident includes someone

apart from company, that resides in Australia and comprises of a person that has the domicile

in Australia except the commissioner is content that an individual has the permanent dwelling

place outside Australia. As apparent there are four types of test to ascertain whether a person

is held to be an Australian resident within the definition. Firstly, it involves residency in

agreement with the ordinary concepts. Secondly, it involves the domicile test or the test of

permanent place of abode (Du Preez 2016). Third test is the 183-day test and lastly, the

commonwealth superannuation fund test. In order to be viewed as resident a person is only

needed to be pass one of the above given test in order to be held as a resident of Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Under the inbound residency test, the relevant test includes the “resides test” and

“183-day test”. To ascertain whether a person has established residency these test is held

important. The resides test is commonly viewed as primary test in determining the residency

and the term is normally derived from the expression “a person, apart from company that

lives in Australia”. If a person is found to be residing in Australia on the basis of ordinary

meaning of the term “resident” they are held as resident and does not need any additional

analysis (Blakelock and King 2017). While the 183-day test is aimed at simplifying the

processes of the residency directions for individuals that are inbound for enacting the law. A

prima facia assumption includes that a person who is in Australia for a period of 183 days is

held to be Australian resident except on those circumstances when the commissioner is

content that a person’s “usual place of dwelling is out of Australia” and the person do not

have any kind of intention to take up the residency in Australia.

On the other hand, to ascertain the outbound residency of a person whether they have

ceased their residency the relevant test includes the domicile test and the superannuation test.

The domicile test is mainly aimed at treating a person as Australian dweller if they are not

residing in Australia but they are domiciled in Australia, except when it is proven that a

person has the permanent place of dwelling out of Australia (Murphy 2019). This test is

normally applicable on those people that have moved overseas to work or live for a certain

time period. Approximately, the superannuation test is only applicable to the outgoing

persons that cannot be considered citizens under other tests. Usually, this test considers a

person to be occupant of Australia if they are considered as the member of specific

government superannuation funds that is set up the “Superannuation Act 1990” or the

“Superannuation Act 1976” (Taylor et al. 2017). The “domicile” and the “superannuation

test” is applied in those situations where the resides test is not met. It involves the extension

of class of individuals that are taxable as residents.

Under the inbound residency test, the relevant test includes the “resides test” and

“183-day test”. To ascertain whether a person has established residency these test is held

important. The resides test is commonly viewed as primary test in determining the residency

and the term is normally derived from the expression “a person, apart from company that

lives in Australia”. If a person is found to be residing in Australia on the basis of ordinary

meaning of the term “resident” they are held as resident and does not need any additional

analysis (Blakelock and King 2017). While the 183-day test is aimed at simplifying the

processes of the residency directions for individuals that are inbound for enacting the law. A

prima facia assumption includes that a person who is in Australia for a period of 183 days is

held to be Australian resident except on those circumstances when the commissioner is

content that a person’s “usual place of dwelling is out of Australia” and the person do not

have any kind of intention to take up the residency in Australia.

On the other hand, to ascertain the outbound residency of a person whether they have

ceased their residency the relevant test includes the domicile test and the superannuation test.

The domicile test is mainly aimed at treating a person as Australian dweller if they are not

residing in Australia but they are domiciled in Australia, except when it is proven that a

person has the permanent place of dwelling out of Australia (Murphy 2019). This test is

normally applicable on those people that have moved overseas to work or live for a certain

time period. Approximately, the superannuation test is only applicable to the outgoing

persons that cannot be considered citizens under other tests. Usually, this test considers a

person to be occupant of Australia if they are considered as the member of specific

government superannuation funds that is set up the “Superannuation Act 1990” or the

“Superannuation Act 1976” (Taylor et al. 2017). The “domicile” and the “superannuation

test” is applied in those situations where the resides test is not met. It involves the extension

of class of individuals that are taxable as residents.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

The present description of resident was adopted during the year 1930 which is around

90 years ago, during the time when majority of the Australians did not have any access to the

international travel. Accordingly, when the definition of resident was introduced, the question

as whether a person lives was straightforwardly established in most of the cases (Long,

Campbell and Kelshaw 2016). Over the time, the taxation commissioner has issued public

rulings and other type of guidance to help individuals to ascertain their residency position

with additional guidance material and checklists that is given on the ATO websites.

Nevertheless, these materials simply lack the force of law and they do not offer any form of

absolute certainty. The procedure involved in self-assessment can be complex. The board of

taxation has developed a view that on the basis of its criticism outlined and common

feedback received all through the consultation the rules of residency is considered uncertain

and difficult to apply.

As stated by Morgan, Mortimer and Pinto (2018) industry consultation have explained

that the cost of tax advice which is given on the residency rules has increased significantly in

the recent years for these persons. Figures obtained from research have suggested that a

simple letter of between $5000 and $10,000 per person. There are number of people that are

affected by this substantial cost. This results in rules which lacks effectiveness provided that

these costs can be uneven to the complication of taxpayer’s fundamental matters related to

taxation. The board views that the extent of such compliance fee justifies additional

consideration as whether the rules of residency can be simplified to lower the cost of

compliance and increase the certainty. There is a huge equity and integrity concerns.

The taxation board understands that positions taken by persons can differ not only on

fundamental evidences and situations but also on persons or their consultants understanding

of legal and administrative regulation. This simply highlights the concern that equity is not

attained for individuals and the present operations of the rules offers the taxpayers with

The present description of resident was adopted during the year 1930 which is around

90 years ago, during the time when majority of the Australians did not have any access to the

international travel. Accordingly, when the definition of resident was introduced, the question

as whether a person lives was straightforwardly established in most of the cases (Long,

Campbell and Kelshaw 2016). Over the time, the taxation commissioner has issued public

rulings and other type of guidance to help individuals to ascertain their residency position

with additional guidance material and checklists that is given on the ATO websites.

Nevertheless, these materials simply lack the force of law and they do not offer any form of

absolute certainty. The procedure involved in self-assessment can be complex. The board of

taxation has developed a view that on the basis of its criticism outlined and common

feedback received all through the consultation the rules of residency is considered uncertain

and difficult to apply.

As stated by Morgan, Mortimer and Pinto (2018) industry consultation have explained

that the cost of tax advice which is given on the residency rules has increased significantly in

the recent years for these persons. Figures obtained from research have suggested that a

simple letter of between $5000 and $10,000 per person. There are number of people that are

affected by this substantial cost. This results in rules which lacks effectiveness provided that

these costs can be uneven to the complication of taxpayer’s fundamental matters related to

taxation. The board views that the extent of such compliance fee justifies additional

consideration as whether the rules of residency can be simplified to lower the cost of

compliance and increase the certainty. There is a huge equity and integrity concerns.

The taxation board understands that positions taken by persons can differ not only on

fundamental evidences and situations but also on persons or their consultants understanding

of legal and administrative regulation. This simply highlights the concern that equity is not

attained for individuals and the present operations of the rules offers the taxpayers with

11TAXATION LAW

opportunity of manipulation of residency results. As outlined by (Robin and Barkoczy 2019)

there is an absence of certainty in the inbound individual residency test. These test are very

difficult to apply and needs an understanding regarding the common law. It also requires a

person to seek the advice of third-party tax consultants. In addition to this uncertainty, the

taxation boards also understand that this may result in sensible minds to reach different

assumption (Butler 2019). This may undermine the principles of equity and integrity of the

present residential rules. According to the board the residency status rules associated to

inbound individuals brings forward significant concerns, especially those that need the

analysis of undefined terms which has been clarified within the common law and needs

further considerations.

The taxation board also considers the uncertainty which the term “domicile and

permanent place of abode” brings to this test is manifested in the word itself. Subsequent

judicial analysis in the case of “FCT v Applegate (1979)” interpreted the difficulty of this

provision. Several consultees have given advise to taxation board that this difficulty remains

to persist in the present date (Lam and Whitney 2016). Under this test there is a differences in

opinion on identical or analogous facts which ultimately increases the uncertainty of this test.

It additionally provides identical potential of manipulation as well. There are also several

consultees that have cited that the relevant superannuation test is not anymore open to new

members. As a result, the effectiveness of this test in fulfilling its actual objectives must be

the subject of additional considerations.

The outbound individual residency test is presently complex and difficult to apply

because of the use of concepts particularly the “domicile” and “permanent place of abode”.

This contributes to significant amount of uncertainty for individuals in ascertaining their

citizenship position (Kenny, Blissenden and Villios 2018). The “domicile test” needs the

assessment of a person’s “permanent place of abode” whereas the superannuation test

opportunity of manipulation of residency results. As outlined by (Robin and Barkoczy 2019)

there is an absence of certainty in the inbound individual residency test. These test are very

difficult to apply and needs an understanding regarding the common law. It also requires a

person to seek the advice of third-party tax consultants. In addition to this uncertainty, the

taxation boards also understand that this may result in sensible minds to reach different

assumption (Butler 2019). This may undermine the principles of equity and integrity of the

present residential rules. According to the board the residency status rules associated to

inbound individuals brings forward significant concerns, especially those that need the

analysis of undefined terms which has been clarified within the common law and needs

further considerations.

The taxation board also considers the uncertainty which the term “domicile and

permanent place of abode” brings to this test is manifested in the word itself. Subsequent

judicial analysis in the case of “FCT v Applegate (1979)” interpreted the difficulty of this

provision. Several consultees have given advise to taxation board that this difficulty remains

to persist in the present date (Lam and Whitney 2016). Under this test there is a differences in

opinion on identical or analogous facts which ultimately increases the uncertainty of this test.

It additionally provides identical potential of manipulation as well. There are also several

consultees that have cited that the relevant superannuation test is not anymore open to new

members. As a result, the effectiveness of this test in fulfilling its actual objectives must be

the subject of additional considerations.

The outbound individual residency test is presently complex and difficult to apply

because of the use of concepts particularly the “domicile” and “permanent place of abode”.

This contributes to significant amount of uncertainty for individuals in ascertaining their

citizenship position (Kenny, Blissenden and Villios 2018). The “domicile test” needs the

assessment of a person’s “permanent place of abode” whereas the superannuation test

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.