HI3042 Taxation Law T2 2017 Individual Assignment - Analysis

VerifiedAdded on 2019/10/30

|9

|2189

|148

Homework Assignment

AI Summary

This assignment solution for HI3042 Taxation Law (T2 2017) provides a comprehensive analysis of various tax-related scenarios. Question 1 examines the deductibility of business expenses under s 8-1 of ITAA 1997, analyzing expenses like machinery relocation, asset revaluation for insurance, legal expenses for winding up, and legal expenses for various matters. Question 2 focuses on GST implications for a company's advertising expenditure, considering input tax credits. Question 3 deals with foreign tax offsets, computing tax liabilities with and without foreign income. Finally, Question 4 computes the net income of a partnership, considering assessable income, deductions, and taxable loss. The solution includes relevant regulations, applicability of legal provisions, and conclusions for each question, supported by references. The assignment is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

HI3042 Taxation Law

T2 2017 Individual Assignment

T2 2017 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

Question 3..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

Question 4..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

References..................................................................................................................................4

Question 1..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

Question 3..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

Question 4..................................................................................................................................3

Introduction............................................................................................................................3

Regulations.............................................................................................................................3

Applicability of legal provisions............................................................................................3

Conclusion..............................................................................................................................3

References..................................................................................................................................4

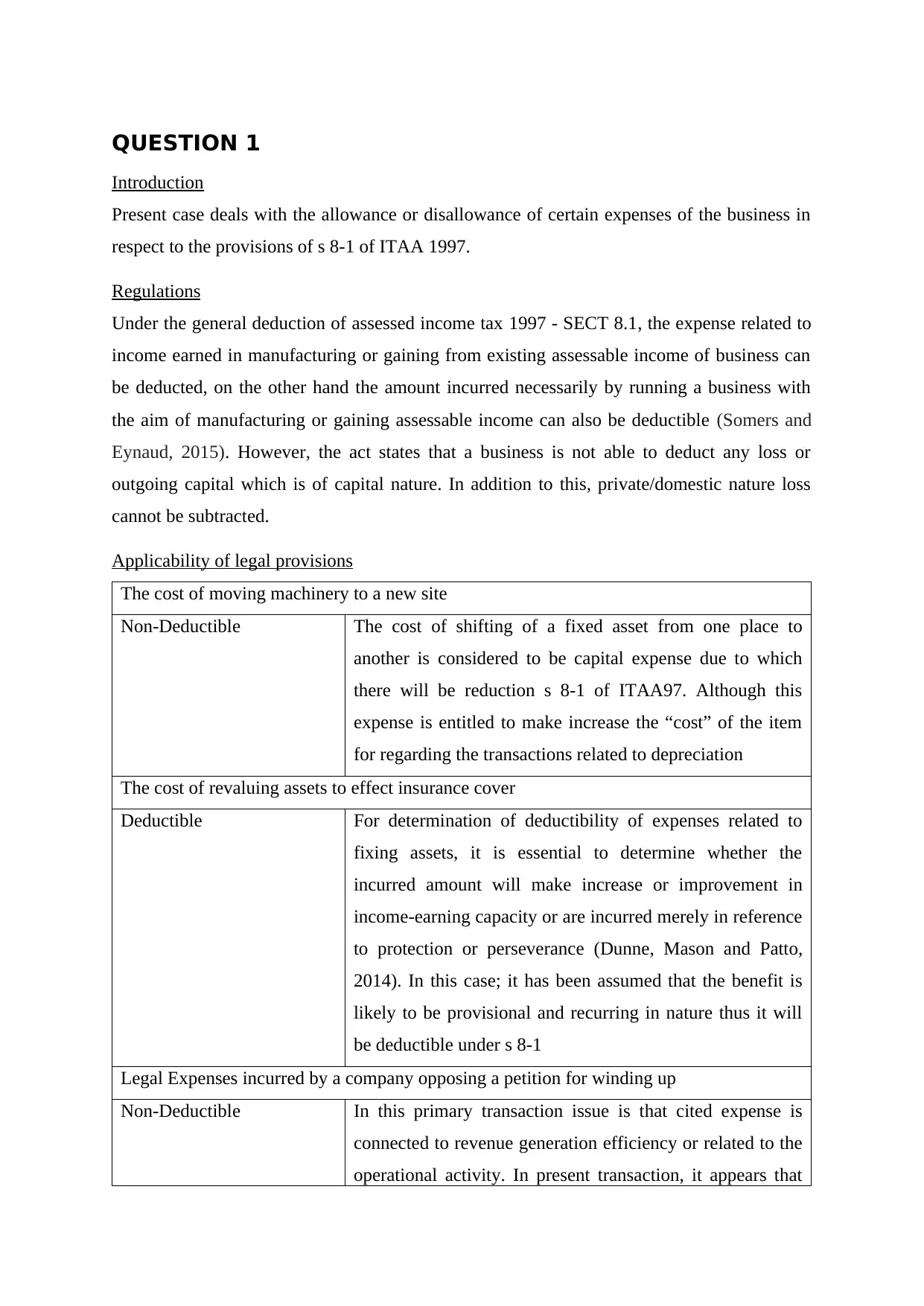

QUESTION 1

Introduction

Present case deals with the allowance or disallowance of certain expenses of the business in

respect to the provisions of s 8-1 of ITAA 1997.

Regulations

Under the general deduction of assessed income tax 1997 - SECT 8.1, the expense related to

income earned in manufacturing or gaining from existing assessable income of business can

be deducted, on the other hand the amount incurred necessarily by running a business with

the aim of manufacturing or gaining assessable income can also be deductible (Somers and

Eynaud, 2015). However, the act states that a business is not able to deduct any loss or

outgoing capital which is of capital nature. In addition to this, private/domestic nature loss

cannot be subtracted.

Applicability of legal provisions

The cost of moving machinery to a new site

Non-Deductible The cost of shifting of a fixed asset from one place to

another is considered to be capital expense due to which

there will be reduction s 8-1 of ITAA97. Although this

expense is entitled to make increase the “cost” of the item

for regarding the transactions related to depreciation

The cost of revaluing assets to effect insurance cover

Deductible For determination of deductibility of expenses related to

fixing assets, it is essential to determine whether the

incurred amount will make increase or improvement in

income-earning capacity or are incurred merely in reference

to protection or perseverance (Dunne, Mason and Patto,

2014). In this case; it has been assumed that the benefit is

likely to be provisional and recurring in nature thus it will

be deductible under s 8-1

Legal Expenses incurred by a company opposing a petition for winding up

Non-Deductible In this primary transaction issue is that cited expense is

connected to revenue generation efficiency or related to the

operational activity. In present transaction, it appears that

Introduction

Present case deals with the allowance or disallowance of certain expenses of the business in

respect to the provisions of s 8-1 of ITAA 1997.

Regulations

Under the general deduction of assessed income tax 1997 - SECT 8.1, the expense related to

income earned in manufacturing or gaining from existing assessable income of business can

be deducted, on the other hand the amount incurred necessarily by running a business with

the aim of manufacturing or gaining assessable income can also be deductible (Somers and

Eynaud, 2015). However, the act states that a business is not able to deduct any loss or

outgoing capital which is of capital nature. In addition to this, private/domestic nature loss

cannot be subtracted.

Applicability of legal provisions

The cost of moving machinery to a new site

Non-Deductible The cost of shifting of a fixed asset from one place to

another is considered to be capital expense due to which

there will be reduction s 8-1 of ITAA97. Although this

expense is entitled to make increase the “cost” of the item

for regarding the transactions related to depreciation

The cost of revaluing assets to effect insurance cover

Deductible For determination of deductibility of expenses related to

fixing assets, it is essential to determine whether the

incurred amount will make increase or improvement in

income-earning capacity or are incurred merely in reference

to protection or perseverance (Dunne, Mason and Patto,

2014). In this case; it has been assumed that the benefit is

likely to be provisional and recurring in nature thus it will

be deductible under s 8-1

Legal Expenses incurred by a company opposing a petition for winding up

Non-Deductible In this primary transaction issue is that cited expense is

connected to revenue generation efficiency or related to the

operational activity. In present transaction, it appears that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this transaction will assist business in winding up due to

which it is considered to be capital in nature.

Legal Expenses incurred for services of a solicitor in respect of a number of matters

Deductible For determination of further deductibility, information is

required such as nature of expenses, apportionment and

other related aspects. However, these expenses seem to be

in revenue in nature, so it has been assumed that it satisfies

the conditions cited under s 8-1.

Conclusion

By considering above described provisions and its applicability, it can be said that first and

third expenses cannot be deducted but second and fourth are deductible under s 8-1 of ITAA

1997.

QUESTION 2

Introduction

In accordance with the given case situation, Big Bank Ltd is having more than 50 branches

and various call centres, and it registered under GST. The company had spent $1,650,000

(inclusive of GST) on advertising campaigns for promotion of bank. In this expense;

$1,100,000 was in relation to a general advertising campaign and remaining was in respect of

specific television advertising campaign for promotion home and contents insurance policies

of Big Bank. According to forecast home and contents insurance policies constitutes 2% of

the entire business and remaining is covered by customary loans and businesses related to

deposit facilities. Now the issue is related to the ability of Big bank regarding the claim of

input tax credits for incurred advertising expenditure.

Regulations

GST guidelines state that a business can claim GST credits while meeting this

following conditions; the primary condition is that when a company tends to buy exclusively

or partially in carrying out the operations of the business, further the purchase will not

concern carrying supplies of input-tax.

Moreover, the purchase price will be inclusive of GST (Liu, Huang and Freudenberg, 2014).

The business must offer or is liable to provide payment against items purchased. The last but

which it is considered to be capital in nature.

Legal Expenses incurred for services of a solicitor in respect of a number of matters

Deductible For determination of further deductibility, information is

required such as nature of expenses, apportionment and

other related aspects. However, these expenses seem to be

in revenue in nature, so it has been assumed that it satisfies

the conditions cited under s 8-1.

Conclusion

By considering above described provisions and its applicability, it can be said that first and

third expenses cannot be deducted but second and fourth are deductible under s 8-1 of ITAA

1997.

QUESTION 2

Introduction

In accordance with the given case situation, Big Bank Ltd is having more than 50 branches

and various call centres, and it registered under GST. The company had spent $1,650,000

(inclusive of GST) on advertising campaigns for promotion of bank. In this expense;

$1,100,000 was in relation to a general advertising campaign and remaining was in respect of

specific television advertising campaign for promotion home and contents insurance policies

of Big Bank. According to forecast home and contents insurance policies constitutes 2% of

the entire business and remaining is covered by customary loans and businesses related to

deposit facilities. Now the issue is related to the ability of Big bank regarding the claim of

input tax credits for incurred advertising expenditure.

Regulations

GST guidelines state that a business can claim GST credits while meeting this

following conditions; the primary condition is that when a company tends to buy exclusively

or partially in carrying out the operations of the business, further the purchase will not

concern carrying supplies of input-tax.

Moreover, the purchase price will be inclusive of GST (Liu, Huang and Freudenberg, 2014).

The business must offer or is liable to provide payment against items purchased. The last but

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

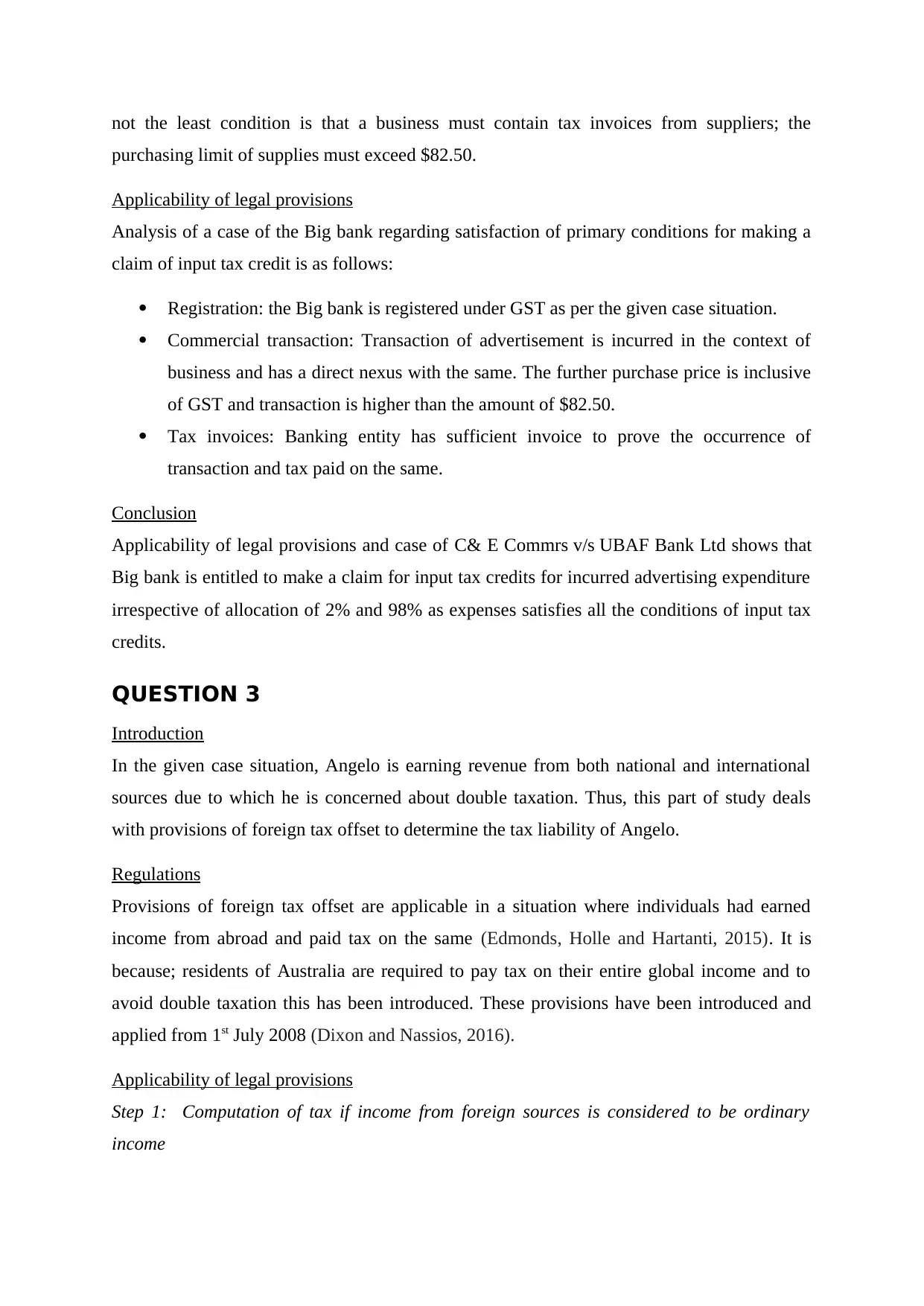

not the least condition is that a business must contain tax invoices from suppliers; the

purchasing limit of supplies must exceed $82.50.

Applicability of legal provisions

Analysis of a case of the Big bank regarding satisfaction of primary conditions for making a

claim of input tax credit is as follows:

Registration: the Big bank is registered under GST as per the given case situation.

Commercial transaction: Transaction of advertisement is incurred in the context of

business and has a direct nexus with the same. The further purchase price is inclusive

of GST and transaction is higher than the amount of $82.50.

Tax invoices: Banking entity has sufficient invoice to prove the occurrence of

transaction and tax paid on the same.

Conclusion

Applicability of legal provisions and case of C& E Commrs v/s UBAF Bank Ltd shows that

Big bank is entitled to make a claim for input tax credits for incurred advertising expenditure

irrespective of allocation of 2% and 98% as expenses satisfies all the conditions of input tax

credits.

QUESTION 3

Introduction

In the given case situation, Angelo is earning revenue from both national and international

sources due to which he is concerned about double taxation. Thus, this part of study deals

with provisions of foreign tax offset to determine the tax liability of Angelo.

Regulations

Provisions of foreign tax offset are applicable in a situation where individuals had earned

income from abroad and paid tax on the same (Edmonds, Holle and Hartanti, 2015). It is

because; residents of Australia are required to pay tax on their entire global income and to

avoid double taxation this has been introduced. These provisions have been introduced and

applied from 1st July 2008 (Dixon and Nassios, 2016).

Applicability of legal provisions

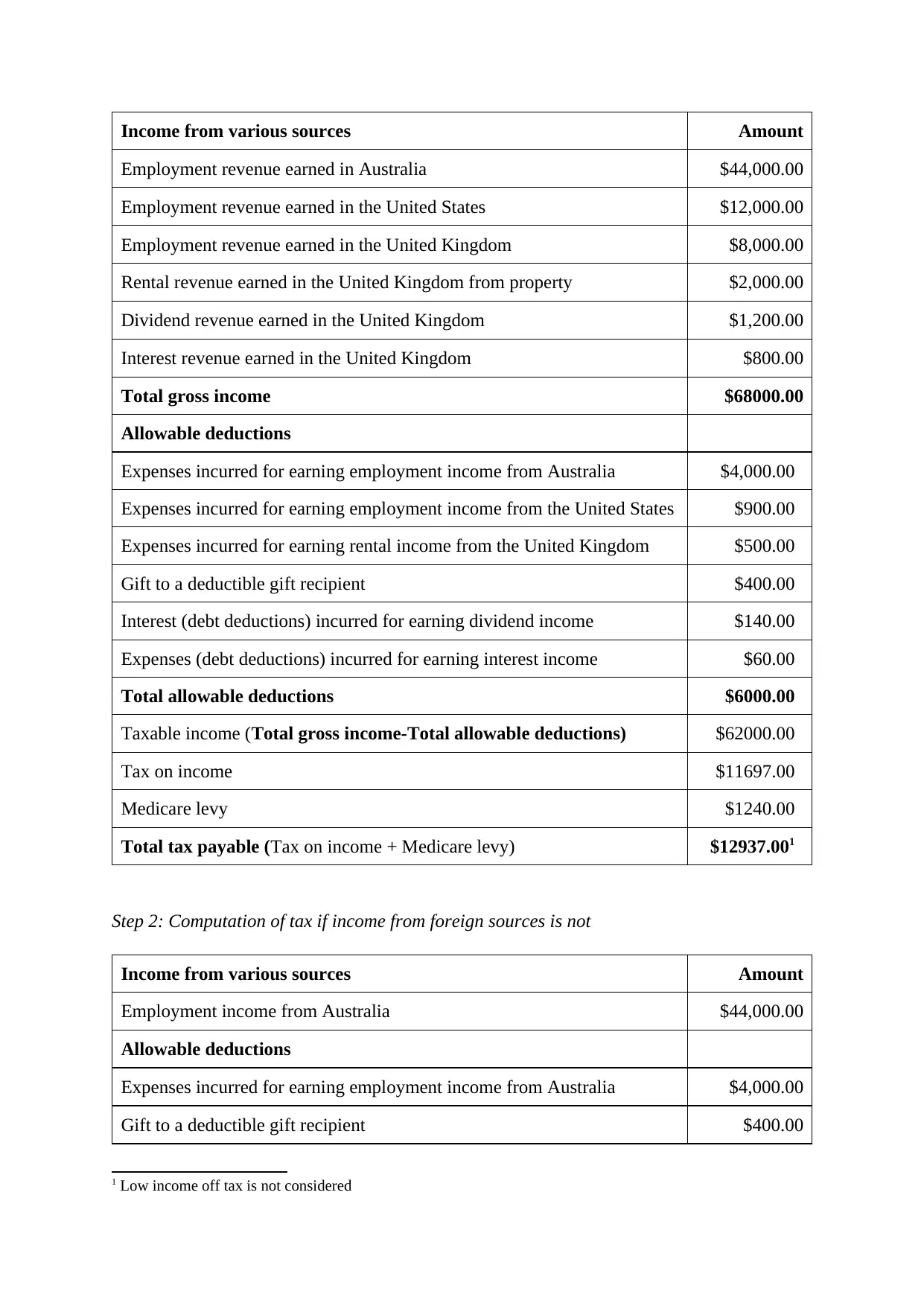

Step 1: Computation of tax if income from foreign sources is considered to be ordinary

income

purchasing limit of supplies must exceed $82.50.

Applicability of legal provisions

Analysis of a case of the Big bank regarding satisfaction of primary conditions for making a

claim of input tax credit is as follows:

Registration: the Big bank is registered under GST as per the given case situation.

Commercial transaction: Transaction of advertisement is incurred in the context of

business and has a direct nexus with the same. The further purchase price is inclusive

of GST and transaction is higher than the amount of $82.50.

Tax invoices: Banking entity has sufficient invoice to prove the occurrence of

transaction and tax paid on the same.

Conclusion

Applicability of legal provisions and case of C& E Commrs v/s UBAF Bank Ltd shows that

Big bank is entitled to make a claim for input tax credits for incurred advertising expenditure

irrespective of allocation of 2% and 98% as expenses satisfies all the conditions of input tax

credits.

QUESTION 3

Introduction

In the given case situation, Angelo is earning revenue from both national and international

sources due to which he is concerned about double taxation. Thus, this part of study deals

with provisions of foreign tax offset to determine the tax liability of Angelo.

Regulations

Provisions of foreign tax offset are applicable in a situation where individuals had earned

income from abroad and paid tax on the same (Edmonds, Holle and Hartanti, 2015). It is

because; residents of Australia are required to pay tax on their entire global income and to

avoid double taxation this has been introduced. These provisions have been introduced and

applied from 1st July 2008 (Dixon and Nassios, 2016).

Applicability of legal provisions

Step 1: Computation of tax if income from foreign sources is considered to be ordinary

income

Income from various sources Amount

Employment revenue earned in Australia $44,000.00

Employment revenue earned in the United States $12,000.00

Employment revenue earned in the United Kingdom $8,000.00

Rental revenue earned in the United Kingdom from property $2,000.00

Dividend revenue earned in the United Kingdom $1,200.00

Interest revenue earned in the United Kingdom $800.00

Total gross income $68000.00

Allowable deductions

Expenses incurred for earning employment income from Australia $4,000.00

Expenses incurred for earning employment income from the United States $900.00

Expenses incurred for earning rental income from the United Kingdom $500.00

Gift to a deductible gift recipient $400.00

Interest (debt deductions) incurred for earning dividend income $140.00

Expenses (debt deductions) incurred for earning interest income $60.00

Total allowable deductions $6000.00

Taxable income (Total gross income-Total allowable deductions) $62000.00

Tax on income $11697.00

Medicare levy $1240.00

Total tax payable (Tax on income + Medicare levy) $12937.001

Step 2: Computation of tax if income from foreign sources is not

Income from various sources Amount

Employment income from Australia $44,000.00

Allowable deductions

Expenses incurred for earning employment income from Australia $4,000.00

Gift to a deductible gift recipient $400.00

1 Low income off tax is not considered

Employment revenue earned in Australia $44,000.00

Employment revenue earned in the United States $12,000.00

Employment revenue earned in the United Kingdom $8,000.00

Rental revenue earned in the United Kingdom from property $2,000.00

Dividend revenue earned in the United Kingdom $1,200.00

Interest revenue earned in the United Kingdom $800.00

Total gross income $68000.00

Allowable deductions

Expenses incurred for earning employment income from Australia $4,000.00

Expenses incurred for earning employment income from the United States $900.00

Expenses incurred for earning rental income from the United Kingdom $500.00

Gift to a deductible gift recipient $400.00

Interest (debt deductions) incurred for earning dividend income $140.00

Expenses (debt deductions) incurred for earning interest income $60.00

Total allowable deductions $6000.00

Taxable income (Total gross income-Total allowable deductions) $62000.00

Tax on income $11697.00

Medicare levy $1240.00

Total tax payable (Tax on income + Medicare levy) $12937.001

Step 2: Computation of tax if income from foreign sources is not

Income from various sources Amount

Employment income from Australia $44,000.00

Allowable deductions

Expenses incurred for earning employment income from Australia $4,000.00

Gift to a deductible gift recipient $400.00

1 Low income off tax is not considered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

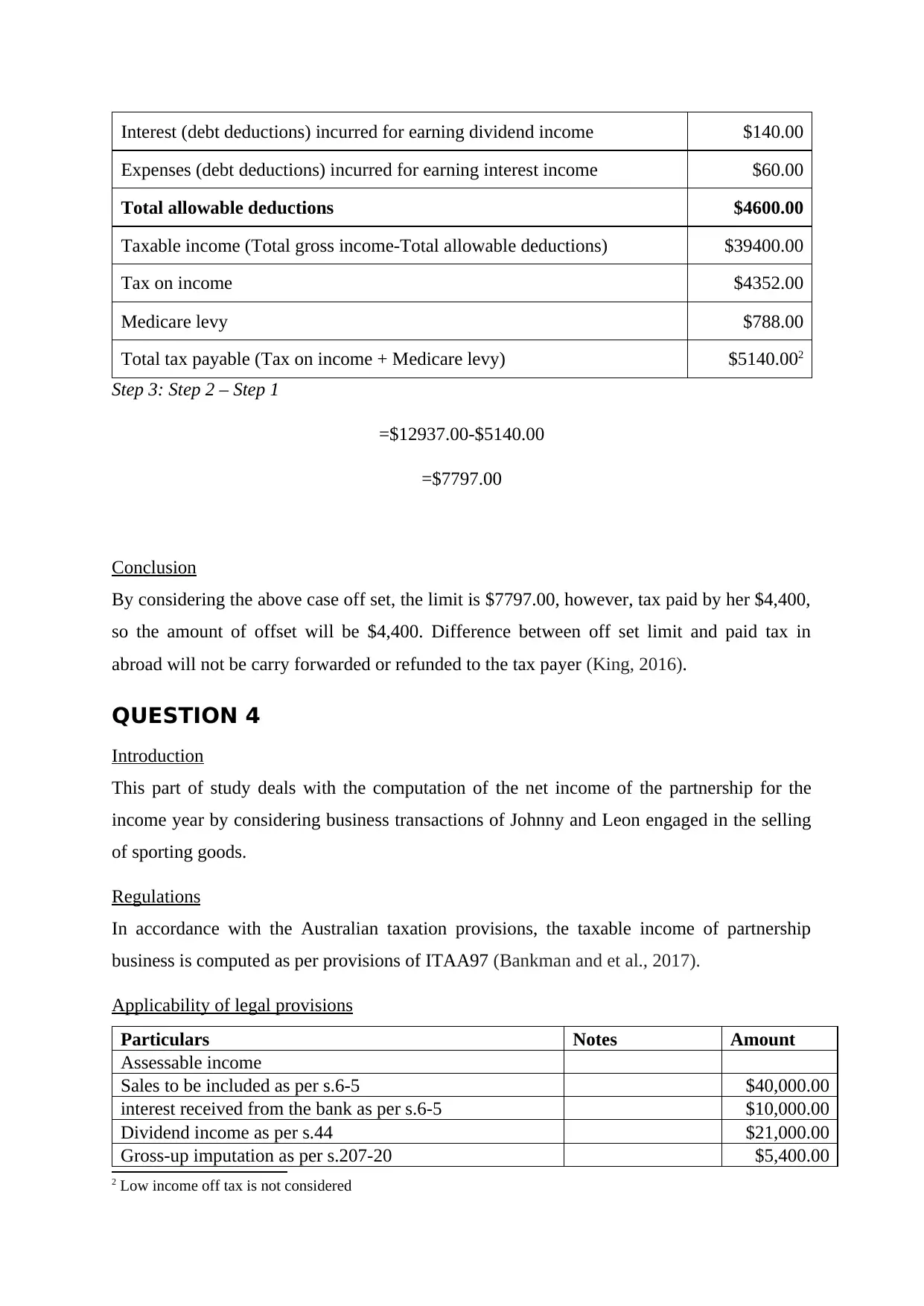

Interest (debt deductions) incurred for earning dividend income $140.00

Expenses (debt deductions) incurred for earning interest income $60.00

Total allowable deductions $4600.00

Taxable income (Total gross income-Total allowable deductions) $39400.00

Tax on income $4352.00

Medicare levy $788.00

Total tax payable (Tax on income + Medicare levy) $5140.002

Step 3: Step 2 – Step 1

=$12937.00-$5140.00

=$7797.00

Conclusion

By considering the above case off set, the limit is $7797.00, however, tax paid by her $4,400,

so the amount of offset will be $4,400. Difference between off set limit and paid tax in

abroad will not be carry forwarded or refunded to the tax payer (King, 2016).

QUESTION 4

Introduction

This part of study deals with the computation of the net income of the partnership for the

income year by considering business transactions of Johnny and Leon engaged in the selling

of sporting goods.

Regulations

In accordance with the Australian taxation provisions, the taxable income of partnership

business is computed as per provisions of ITAA97 (Bankman and et al., 2017).

Applicability of legal provisions

Particulars Notes Amount

Assessable income

Sales to be included as per s.6-5 $40,000.00

interest received from the bank as per s.6-5 $10,000.00

Dividend income as per s.44 $21,000.00

Gross-up imputation as per s.207-20 $5,400.00

2 Low income off tax is not considered

Expenses (debt deductions) incurred for earning interest income $60.00

Total allowable deductions $4600.00

Taxable income (Total gross income-Total allowable deductions) $39400.00

Tax on income $4352.00

Medicare levy $788.00

Total tax payable (Tax on income + Medicare levy) $5140.002

Step 3: Step 2 – Step 1

=$12937.00-$5140.00

=$7797.00

Conclusion

By considering the above case off set, the limit is $7797.00, however, tax paid by her $4,400,

so the amount of offset will be $4,400. Difference between off set limit and paid tax in

abroad will not be carry forwarded or refunded to the tax payer (King, 2016).

QUESTION 4

Introduction

This part of study deals with the computation of the net income of the partnership for the

income year by considering business transactions of Johnny and Leon engaged in the selling

of sporting goods.

Regulations

In accordance with the Australian taxation provisions, the taxable income of partnership

business is computed as per provisions of ITAA97 (Bankman and et al., 2017).

Applicability of legal provisions

Particulars Notes Amount

Assessable income

Sales to be included as per s.6-5 $40,000.00

interest received from the bank as per s.6-5 $10,000.00

Dividend income as per s.44 $21,000.00

Gross-up imputation as per s.207-20 $5,400.00

2 Low income off tax is not considered

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

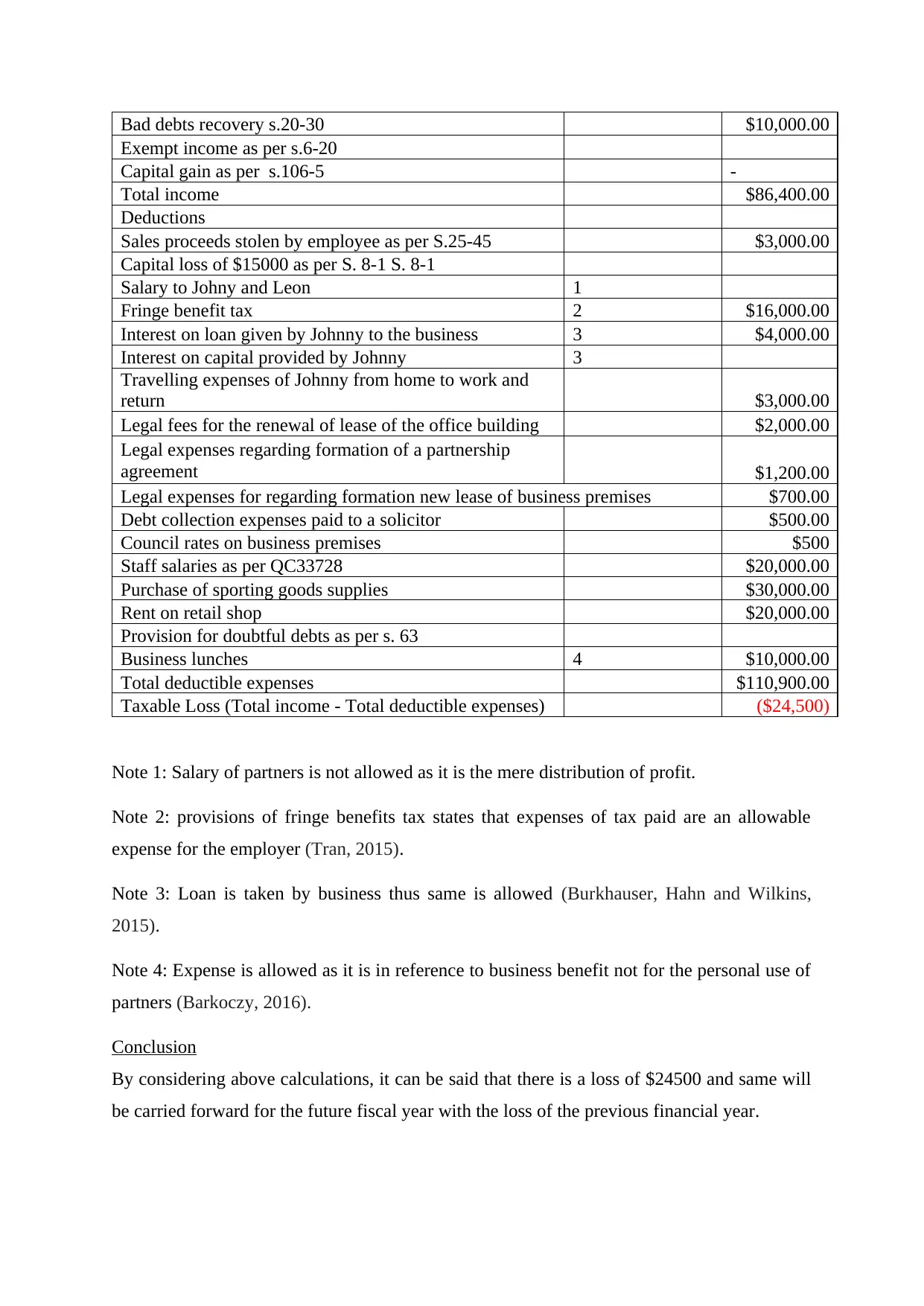

Bad debts recovery s.20-30 $10,000.00

Exempt income as per s.6-20

Capital gain as per s.106-5 -

Total income $86,400.00

Deductions

Sales proceeds stolen by employee as per S.25-45 $3,000.00

Capital loss of $15000 as per S. 8-1 S. 8-1

Salary to Johny and Leon 1

Fringe benefit tax 2 $16,000.00

Interest on loan given by Johnny to the business 3 $4,000.00

Interest on capital provided by Johnny 3

Travelling expenses of Johnny from home to work and

return $3,000.00

Legal fees for the renewal of lease of the office building $2,000.00

Legal expenses regarding formation of a partnership

agreement $1,200.00

Legal expenses for regarding formation new lease of business premises $700.00

Debt collection expenses paid to a solicitor $500.00

Council rates on business premises $500

Staff salaries as per QC33728 $20,000.00

Purchase of sporting goods supplies $30,000.00

Rent on retail shop $20,000.00

Provision for doubtful debts as per s. 63

Business lunches 4 $10,000.00

Total deductible expenses $110,900.00

Taxable Loss (Total income - Total deductible expenses) ($24,500)

Note 1: Salary of partners is not allowed as it is the mere distribution of profit.

Note 2: provisions of fringe benefits tax states that expenses of tax paid are an allowable

expense for the employer (Tran, 2015).

Note 3: Loan is taken by business thus same is allowed (Burkhauser, Hahn and Wilkins,

2015).

Note 4: Expense is allowed as it is in reference to business benefit not for the personal use of

partners (Barkoczy, 2016).

Conclusion

By considering above calculations, it can be said that there is a loss of $24500 and same will

be carried forward for the future fiscal year with the loss of the previous financial year.

Exempt income as per s.6-20

Capital gain as per s.106-5 -

Total income $86,400.00

Deductions

Sales proceeds stolen by employee as per S.25-45 $3,000.00

Capital loss of $15000 as per S. 8-1 S. 8-1

Salary to Johny and Leon 1

Fringe benefit tax 2 $16,000.00

Interest on loan given by Johnny to the business 3 $4,000.00

Interest on capital provided by Johnny 3

Travelling expenses of Johnny from home to work and

return $3,000.00

Legal fees for the renewal of lease of the office building $2,000.00

Legal expenses regarding formation of a partnership

agreement $1,200.00

Legal expenses for regarding formation new lease of business premises $700.00

Debt collection expenses paid to a solicitor $500.00

Council rates on business premises $500

Staff salaries as per QC33728 $20,000.00

Purchase of sporting goods supplies $30,000.00

Rent on retail shop $20,000.00

Provision for doubtful debts as per s. 63

Business lunches 4 $10,000.00

Total deductible expenses $110,900.00

Taxable Loss (Total income - Total deductible expenses) ($24,500)

Note 1: Salary of partners is not allowed as it is the mere distribution of profit.

Note 2: provisions of fringe benefits tax states that expenses of tax paid are an allowable

expense for the employer (Tran, 2015).

Note 3: Loan is taken by business thus same is allowed (Burkhauser, Hahn and Wilkins,

2015).

Note 4: Expense is allowed as it is in reference to business benefit not for the personal use of

partners (Barkoczy, 2016).

Conclusion

By considering above calculations, it can be said that there is a loss of $24500 and same will

be carried forward for the future fiscal year with the loss of the previous financial year.

REFERENCES

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Dixon, J.M. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in

Australia. Centre for Policy Studies, Victoria University.

Dunne, J., Mason, J. and Patto, J., 2014. 2013 cases show high ATO success rate. Taxation in

Australia, 48(8), p.429.

Edmonds, M., Holle, C. and Hartanti, W., 2015. Alternative assets insights: Super funds-tax

impediments to going global. Taxation in Australia, 49(7), p.413.

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part 2. Taxation

in Australia, 51(1), p.12.

Liu, B., Huang, A. and Freudenberg, B., 2014. The impact of the GST on mortgage pricing of

Australian credit unions: An empirical analysis. Accounting Research Journal, 27(1), pp.37-

51.

Somers, R. and Eynaud, A., 2015. A matter of trusts: The ATO's proposed treatment of

present unpaid entitlements: Part 1. Taxation in Australia, 50(2), p.90.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia?. Browser Download This Paper.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Dixon, J.M. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in

Australia. Centre for Policy Studies, Victoria University.

Dunne, J., Mason, J. and Patto, J., 2014. 2013 cases show high ATO success rate. Taxation in

Australia, 48(8), p.429.

Edmonds, M., Holle, C. and Hartanti, W., 2015. Alternative assets insights: Super funds-tax

impediments to going global. Taxation in Australia, 49(7), p.413.

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part 2. Taxation

in Australia, 51(1), p.12.

Liu, B., Huang, A. and Freudenberg, B., 2014. The impact of the GST on mortgage pricing of

Australian credit unions: An empirical analysis. Accounting Research Journal, 27(1), pp.37-

51.

Somers, R. and Eynaud, A., 2015. A matter of trusts: The ATO's proposed treatment of

present unpaid entitlements: Part 1. Taxation in Australia, 50(2), p.90.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia?. Browser Download This Paper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.