LAWS20060: Taxation Law of Australia Individual Assignment - Term 1

VerifiedAdded on 2023/01/18

|19

|4400

|95

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment, addressing various aspects of Australian taxation. It covers topics such as the effective life of depreciating assets, tax offsets, tax rates, capital gains tax (CGT) events, and the calculation of income tax. The assignment delves into specific sections of the Income Tax Assessment Act 1997 (ITAA 1997) and relevant tax rulings, including TR 2018/4. The solution analyzes several scenarios, including deductions for interest on loans, apportionment of expenses, and the application of CGT to different situations like lease agreements and share sales. Key legal cases, such as Ure v FCT (1981), Ronpibon Tin NL v FCT (1949), and Charles Moore & Co (WA) Pty Ltd v FC of T (1956), are referenced to support arguments. The document also explores the differences between average and marginal tax rates and provides detailed calculations for capital gains tax, offering a thorough understanding of taxation principles and their practical application.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1..................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................3

Answer to D:..........................................................................................................................3

Answer to E:...........................................................................................................................4

Answer to F:...........................................................................................................................4

Answer to G:..........................................................................................................................4

Answer to H:..........................................................................................................................5

Answer to I:............................................................................................................................5

Answer to Question 2:................................................................................................................6

Answer to A:..........................................................................................................................6

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................7

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer to A:..........................................................................................................................9

Answer to B:..........................................................................................................................9

Answer to C:..........................................................................................................................9

Table of Contents

Answer to question 1..................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................3

Answer to D:..........................................................................................................................3

Answer to E:...........................................................................................................................4

Answer to F:...........................................................................................................................4

Answer to G:..........................................................................................................................4

Answer to H:..........................................................................................................................5

Answer to I:............................................................................................................................5

Answer to Question 2:................................................................................................................6

Answer to A:..........................................................................................................................6

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................7

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer to A:..........................................................................................................................9

Answer to B:..........................................................................................................................9

Answer to C:..........................................................................................................................9

2TAXATION LAW

Answer to D:........................................................................................................................10

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................12

Answer to question 5:...............................................................................................................13

Issues:...................................................................................................................................13

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................15

References:...............................................................................................................................16

Answer to D:........................................................................................................................10

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................12

Answer to question 5:...............................................................................................................13

Issues:...................................................................................................................................13

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................15

References:...............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

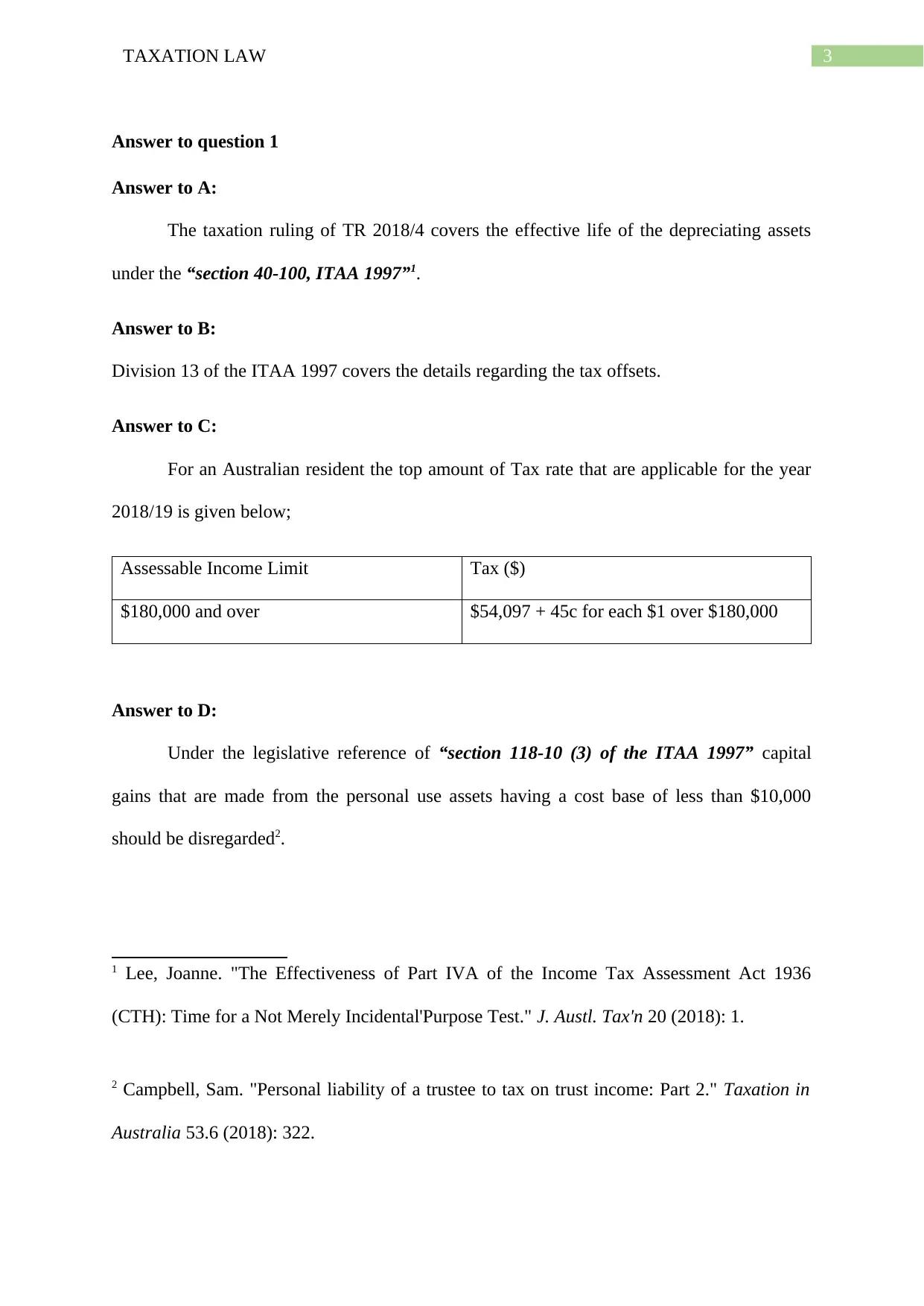

Answer to question 1

Answer to A:

The taxation ruling of TR 2018/4 covers the effective life of the depreciating assets

under the “section 40-100, ITAA 1997”1.

Answer to B:

Division 13 of the ITAA 1997 covers the details regarding the tax offsets.

Answer to C:

For an Australian resident the top amount of Tax rate that are applicable for the year

2018/19 is given below;

Assessable Income Limit Tax ($)

$180,000 and over $54,097 + 45c for each $1 over $180,000

Answer to D:

Under the legislative reference of “section 118-10 (3) of the ITAA 1997” capital

gains that are made from the personal use assets having a cost base of less than $10,000

should be disregarded2.

1 Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936

(CTH): Time for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

2 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 2." Taxation in

Australia 53.6 (2018): 322.

Answer to question 1

Answer to A:

The taxation ruling of TR 2018/4 covers the effective life of the depreciating assets

under the “section 40-100, ITAA 1997”1.

Answer to B:

Division 13 of the ITAA 1997 covers the details regarding the tax offsets.

Answer to C:

For an Australian resident the top amount of Tax rate that are applicable for the year

2018/19 is given below;

Assessable Income Limit Tax ($)

$180,000 and over $54,097 + 45c for each $1 over $180,000

Answer to D:

Under the legislative reference of “section 118-10 (3) of the ITAA 1997” capital

gains that are made from the personal use assets having a cost base of less than $10,000

should be disregarded2.

1 Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936

(CTH): Time for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

2 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 2." Taxation in

Australia 53.6 (2018): 322.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

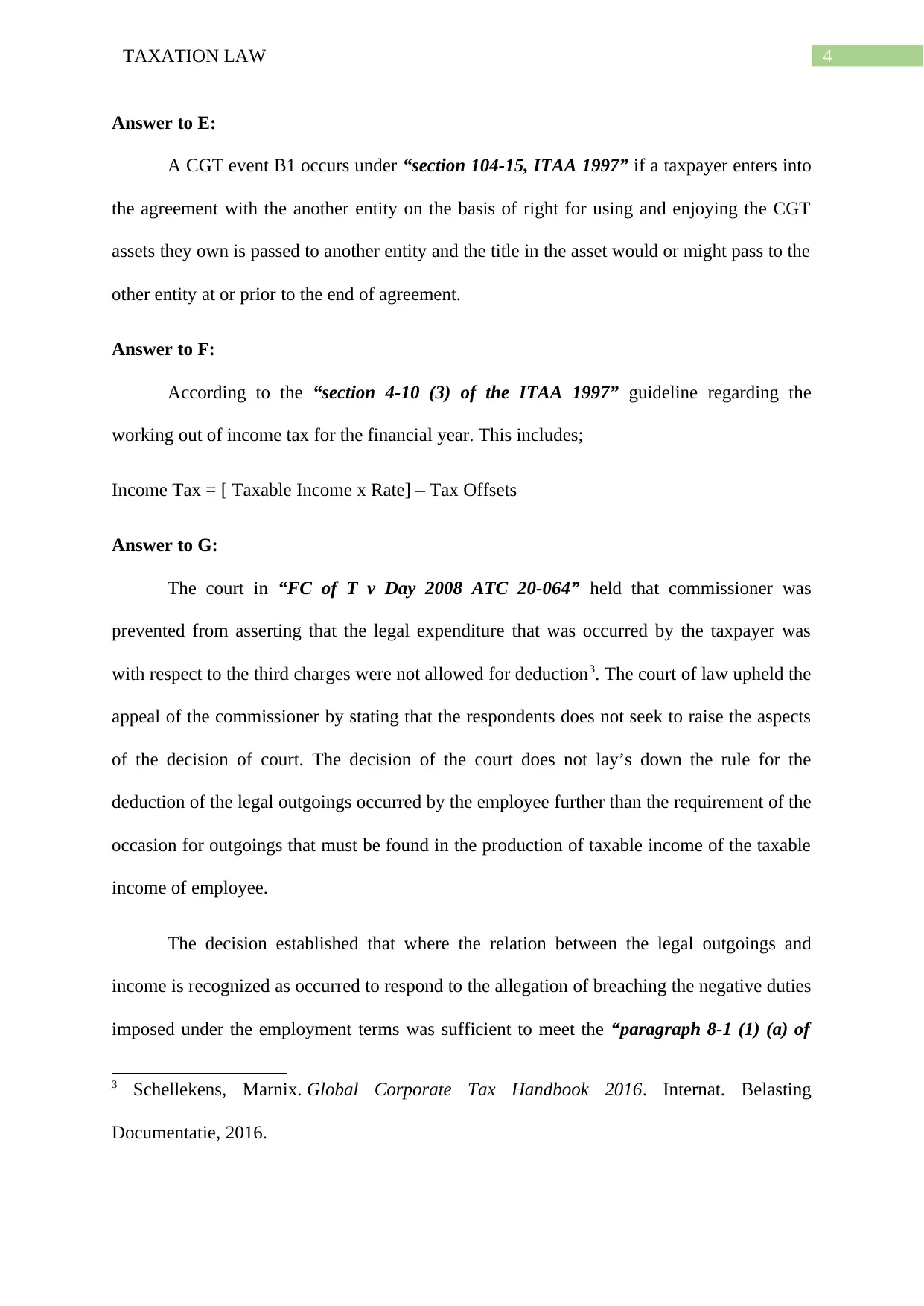

Answer to E:

A CGT event B1 occurs under “section 104-15, ITAA 1997” if a taxpayer enters into

the agreement with the another entity on the basis of right for using and enjoying the CGT

assets they own is passed to another entity and the title in the asset would or might pass to the

other entity at or prior to the end of agreement.

Answer to F:

According to the “section 4-10 (3) of the ITAA 1997” guideline regarding the

working out of income tax for the financial year. This includes;

Income Tax = [ Taxable Income x Rate] – Tax Offsets

Answer to G:

The court in “FC of T v Day 2008 ATC 20-064” held that commissioner was

prevented from asserting that the legal expenditure that was occurred by the taxpayer was

with respect to the third charges were not allowed for deduction3. The court of law upheld the

appeal of the commissioner by stating that the respondents does not seek to raise the aspects

of the decision of court. The decision of the court does not lay’s down the rule for the

deduction of the legal outgoings occurred by the employee further than the requirement of the

occasion for outgoings that must be found in the production of taxable income of the taxable

income of employee.

The decision established that where the relation between the legal outgoings and

income is recognized as occurred to respond to the allegation of breaching the negative duties

imposed under the employment terms was sufficient to meet the “paragraph 8-1 (1) (a) of

3 Schellekens, Marnix. Global Corporate Tax Handbook 2016. Internat. Belasting

Documentatie, 2016.

Answer to E:

A CGT event B1 occurs under “section 104-15, ITAA 1997” if a taxpayer enters into

the agreement with the another entity on the basis of right for using and enjoying the CGT

assets they own is passed to another entity and the title in the asset would or might pass to the

other entity at or prior to the end of agreement.

Answer to F:

According to the “section 4-10 (3) of the ITAA 1997” guideline regarding the

working out of income tax for the financial year. This includes;

Income Tax = [ Taxable Income x Rate] – Tax Offsets

Answer to G:

The court in “FC of T v Day 2008 ATC 20-064” held that commissioner was

prevented from asserting that the legal expenditure that was occurred by the taxpayer was

with respect to the third charges were not allowed for deduction3. The court of law upheld the

appeal of the commissioner by stating that the respondents does not seek to raise the aspects

of the decision of court. The decision of the court does not lay’s down the rule for the

deduction of the legal outgoings occurred by the employee further than the requirement of the

occasion for outgoings that must be found in the production of taxable income of the taxable

income of employee.

The decision established that where the relation between the legal outgoings and

income is recognized as occurred to respond to the allegation of breaching the negative duties

imposed under the employment terms was sufficient to meet the “paragraph 8-1 (1) (a) of

3 Schellekens, Marnix. Global Corporate Tax Handbook 2016. Internat. Belasting

Documentatie, 2016.

5TAXATION LAW

the ITAA 1997”4. The court noticed that legal outgoings that was occurred by the taxpayer in

respect of disciplinary action taken by his employer are not treated as outgoings of private or

domestic nature. Therefore, the legal expenditure was allowed as deduction under

“paragraph 8-1 (1) (a) of the ITAA 1997”.

Answer to H:

The difference between average tax rate and marginal tax rate is given below

Average Tax Rate Marginal Tax Rate

Average tax rate assesses the burden of

taxation

The marginal tax rate assesses the effect of

taxes on incentives to earn, invest, or spend.

The average tax rate represents the total

value of tax divided by the total earnings

The marginal tax rate represents the

incremental value of tax that are paid on the

incremental earnings.

The average rate of tax evaluates the tax

burden of the households. In other words, it

assesses how the taxes create an impact on

the ability of the households to consume

presently or in future.

The marginal rate of tax assesses the extent

to which the taxes create an impact on the

household economic incentives.

Answer to I:

The consumption tax can be defined as the tax that is levied on the consumption

expenditure of goods and services. The base of such tax represents the amount of money that

4 Peiros, Katerina, and Christine Smyth. "Successful succession: Tax treatment of executor's

commission." Taxation in Australia 51.7 (2017): 394.

the ITAA 1997”4. The court noticed that legal outgoings that was occurred by the taxpayer in

respect of disciplinary action taken by his employer are not treated as outgoings of private or

domestic nature. Therefore, the legal expenditure was allowed as deduction under

“paragraph 8-1 (1) (a) of the ITAA 1997”.

Answer to H:

The difference between average tax rate and marginal tax rate is given below

Average Tax Rate Marginal Tax Rate

Average tax rate assesses the burden of

taxation

The marginal tax rate assesses the effect of

taxes on incentives to earn, invest, or spend.

The average tax rate represents the total

value of tax divided by the total earnings

The marginal tax rate represents the

incremental value of tax that are paid on the

incremental earnings.

The average rate of tax evaluates the tax

burden of the households. In other words, it

assesses how the taxes create an impact on

the ability of the households to consume

presently or in future.

The marginal rate of tax assesses the extent

to which the taxes create an impact on the

household economic incentives.

Answer to I:

The consumption tax can be defined as the tax that is levied on the consumption

expenditure of goods and services. The base of such tax represents the amount of money that

4 Peiros, Katerina, and Christine Smyth. "Successful succession: Tax treatment of executor's

commission." Taxation in Australia 51.7 (2017): 394.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

is spend on consumption. The consumption taxes are generally the indirect taxes namely the

value added tax or the sales tax5. Consumption taxation can also be referred to the entire

system of taxation where taxes are levied on the people for the amount they consume instead

of how much they add to the economy.

Answer to Question 2:

Answer to A:

The legislative provision of “section 8-1, ITAA 1997” provides an explanation that

every taxpayer is permitted to obtain deduction for the expenditure on interest on loan at the

time of generating income. The court in “Ure v FCT (1981)” held that the taxpayer was

permitted deduction for borrowed money for discharging the mortgages on the residential

property.

As evident Brett incurred interest on loan for paying out the wages to employee.

Referring to “Ure v FCT (1981)” the interest on loan occurred by the taxpayer for paying the

interest on loan will be allowed for deduction because it is occurred in earning assessable

income.

Answer to B:

There are certain situations where the loss or outgoings should be apportioned or only

allowed a partial deduction. The court in “Ronpibon Tin NL v FCT (1949)” held that the

administrative expenditure and director’s fees needs to be determined up to what extent it was

occurred in gaining or producing the assessable income6.

5 Dodds, Nicholas, and Keith Kendall. "Effective disclaimers." Taxation in Australia 52.7

(2018): 375.

6 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and

Quantitative Analysis 50.3 (2015): 277-300.

is spend on consumption. The consumption taxes are generally the indirect taxes namely the

value added tax or the sales tax5. Consumption taxation can also be referred to the entire

system of taxation where taxes are levied on the people for the amount they consume instead

of how much they add to the economy.

Answer to Question 2:

Answer to A:

The legislative provision of “section 8-1, ITAA 1997” provides an explanation that

every taxpayer is permitted to obtain deduction for the expenditure on interest on loan at the

time of generating income. The court in “Ure v FCT (1981)” held that the taxpayer was

permitted deduction for borrowed money for discharging the mortgages on the residential

property.

As evident Brett incurred interest on loan for paying out the wages to employee.

Referring to “Ure v FCT (1981)” the interest on loan occurred by the taxpayer for paying the

interest on loan will be allowed for deduction because it is occurred in earning assessable

income.

Answer to B:

There are certain situations where the loss or outgoings should be apportioned or only

allowed a partial deduction. The court in “Ronpibon Tin NL v FCT (1949)” held that the

administrative expenditure and director’s fees needs to be determined up to what extent it was

occurred in gaining or producing the assessable income6.

5 Dodds, Nicholas, and Keith Kendall. "Effective disclaimers." Taxation in Australia 52.7

(2018): 375.

6 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and

Quantitative Analysis 50.3 (2015): 277-300.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Expenses related to mobile phone bill were incurred by Julie where 60% of the calls

were associated for work purpose. Citing “Ronpibon Tin NL v FCT (1949)” a deduction up

to 60% of the total mobile phone expenses will be allowed to Julie under section “section 8-

1, ITAA 1997” whereas the remaining 40% represents private outgoings that are non-

deductible.

Answer to C:

Under “section 8-1 (2) (b), ITAA 1997” loss or outgoings of domestic or private in

nature that fails to meet positive limbs are not permitted for tax deduction under negative

limbs7. In “Lodge v FCT (1972)” a deduction was not allowed to taxpayer for childcare

expenses because it was not related to producing taxable income.

Citing “Lodge v FCT (1972)” the babysitter expenses incurred by Sally is not

permitted for general deduction and it constitutes private or domestic spending under

“section 8-1 (2) (b), ITAA 1997”.

Answer to D:

The applicability of “Section 8-1, ITAA 1997” is for both the expenses and losses

that are occurred by the taxpayer8. In “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)”

deduction was allowed to taxpayer for money that was stolen from the daily earnings.

7 Auerbach, Alan J., and Kevin Hassett. "Capital taxation in the twenty-first

century." American Economic Review 105.5 (2015): 38-42.

8 Jacob, Martin. "Tax regimes and capital gains realizations." European Accounting

Review 27.1 (2018): 1-21.

Expenses related to mobile phone bill were incurred by Julie where 60% of the calls

were associated for work purpose. Citing “Ronpibon Tin NL v FCT (1949)” a deduction up

to 60% of the total mobile phone expenses will be allowed to Julie under section “section 8-

1, ITAA 1997” whereas the remaining 40% represents private outgoings that are non-

deductible.

Answer to C:

Under “section 8-1 (2) (b), ITAA 1997” loss or outgoings of domestic or private in

nature that fails to meet positive limbs are not permitted for tax deduction under negative

limbs7. In “Lodge v FCT (1972)” a deduction was not allowed to taxpayer for childcare

expenses because it was not related to producing taxable income.

Citing “Lodge v FCT (1972)” the babysitter expenses incurred by Sally is not

permitted for general deduction and it constitutes private or domestic spending under

“section 8-1 (2) (b), ITAA 1997”.

Answer to D:

The applicability of “Section 8-1, ITAA 1997” is for both the expenses and losses

that are occurred by the taxpayer8. In “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)”

deduction was allowed to taxpayer for money that was stolen from the daily earnings.

7 Auerbach, Alan J., and Kevin Hassett. "Capital taxation in the twenty-first

century." American Economic Review 105.5 (2015): 38-42.

8 Jacob, Martin. "Tax regimes and capital gains realizations." European Accounting

Review 27.1 (2018): 1-21.

8TAXATION LAW

Referring to “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)” Jerry will be

permitted deduction under “Section 8-1, ITAA 1997” for the theft of $20,000 goods from the

business because it incurred out of daily business activities.

Answer to E:

Expenditure which is preliminary to the beginning of revenue generating activities

and not in the due course of such activity is not deduction under “section 8-1, ITAA 1997”.

Similarly, in “FCT v Maddalena v FCT (1971)” where expenses that are occurred in

obtaining a new employment was not in the course of generating income because the

expenses were incurred at a point too soon and therefore not allowed for deduction under

“section 8-1, ITAA 1997”9.

Similarly, the expenses incurred in contesting the government election should be

treated as preliminary to the commencement of income generating activities which was not

for generating assessable income. Therefore, these expenses non-deductible under “section

8-1, ITAA 1997” because it occurred at a point too soon.

Answer to question 3:

Answer to A:

When a taxpayer extends, grants or renews the long term lease then a “CGT event

F2” is applied. The “CGT event F2” is applied on the owners of underlying land or the

taxpayer that are granted with sub-lease10. Andy as the owner of land grants a five-year term

9 Dimmock, Stephen G., et al. "Capital gains lock-in and governance choices." Journal of

Financial Economics 127.1 (2018): 113-135.

10 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

Referring to “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)” Jerry will be

permitted deduction under “Section 8-1, ITAA 1997” for the theft of $20,000 goods from the

business because it incurred out of daily business activities.

Answer to E:

Expenditure which is preliminary to the beginning of revenue generating activities

and not in the due course of such activity is not deduction under “section 8-1, ITAA 1997”.

Similarly, in “FCT v Maddalena v FCT (1971)” where expenses that are occurred in

obtaining a new employment was not in the course of generating income because the

expenses were incurred at a point too soon and therefore not allowed for deduction under

“section 8-1, ITAA 1997”9.

Similarly, the expenses incurred in contesting the government election should be

treated as preliminary to the commencement of income generating activities which was not

for generating assessable income. Therefore, these expenses non-deductible under “section

8-1, ITAA 1997” because it occurred at a point too soon.

Answer to question 3:

Answer to A:

When a taxpayer extends, grants or renews the long term lease then a “CGT event

F2” is applied. The “CGT event F2” is applied on the owners of underlying land or the

taxpayer that are granted with sub-lease10. Andy as the owner of land grants a five-year term

9 Dimmock, Stephen G., et al. "Capital gains lock-in and governance choices." Journal of

Financial Economics 127.1 (2018): 113-135.

10 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

lease to Brian for a premium of $50,000. For that reason, a “CGT event F2” happened. Andy

would not be allowed a 50% CGT discount because it is not applied on “CGT event F2”.

Answer to B:

As per the ATO a “CGT event B1” happens when the use of land is mainly obtained

by the new owner. The use of land happens based on the situation when the acquisition of

land is done by new owner and the date based on which the profits and rents are permitted to

new owner11. Farm land was granted with the opportunity of acquiring the land for $800,000

in exchange of $40,000. Therefore, a CGT event B1 took place for John and hence 50%

discount can be obtained on the above stated transaction.

Answer to C:

Where a taxpayer dwelling does not sum up as the main residence for the entire

period of ownership and used for producing income then a partial main residence exemption

from CGT is permitted. Jamie and Olivia bought a property and let it on rent for two years

prior to selling the same on 2018. Jamie and Olivia would be entitled to partial main

residence exemption after selling the property. Consequently, 50% CGT is applicable for

Jamie and Olivia to calculate the net capital gains tax.

11 Burns, Andrew. "Mid market focus: Tax considerations when doing business

offshore." Taxation in Australia 51.10 (2017): 535.

lease to Brian for a premium of $50,000. For that reason, a “CGT event F2” happened. Andy

would not be allowed a 50% CGT discount because it is not applied on “CGT event F2”.

Answer to B:

As per the ATO a “CGT event B1” happens when the use of land is mainly obtained

by the new owner. The use of land happens based on the situation when the acquisition of

land is done by new owner and the date based on which the profits and rents are permitted to

new owner11. Farm land was granted with the opportunity of acquiring the land for $800,000

in exchange of $40,000. Therefore, a CGT event B1 took place for John and hence 50%

discount can be obtained on the above stated transaction.

Answer to C:

Where a taxpayer dwelling does not sum up as the main residence for the entire

period of ownership and used for producing income then a partial main residence exemption

from CGT is permitted. Jamie and Olivia bought a property and let it on rent for two years

prior to selling the same on 2018. Jamie and Olivia would be entitled to partial main

residence exemption after selling the property. Consequently, 50% CGT is applicable for

Jamie and Olivia to calculate the net capital gains tax.

11 Burns, Andrew. "Mid market focus: Tax considerations when doing business

offshore." Taxation in Australia 51.10 (2017): 535.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

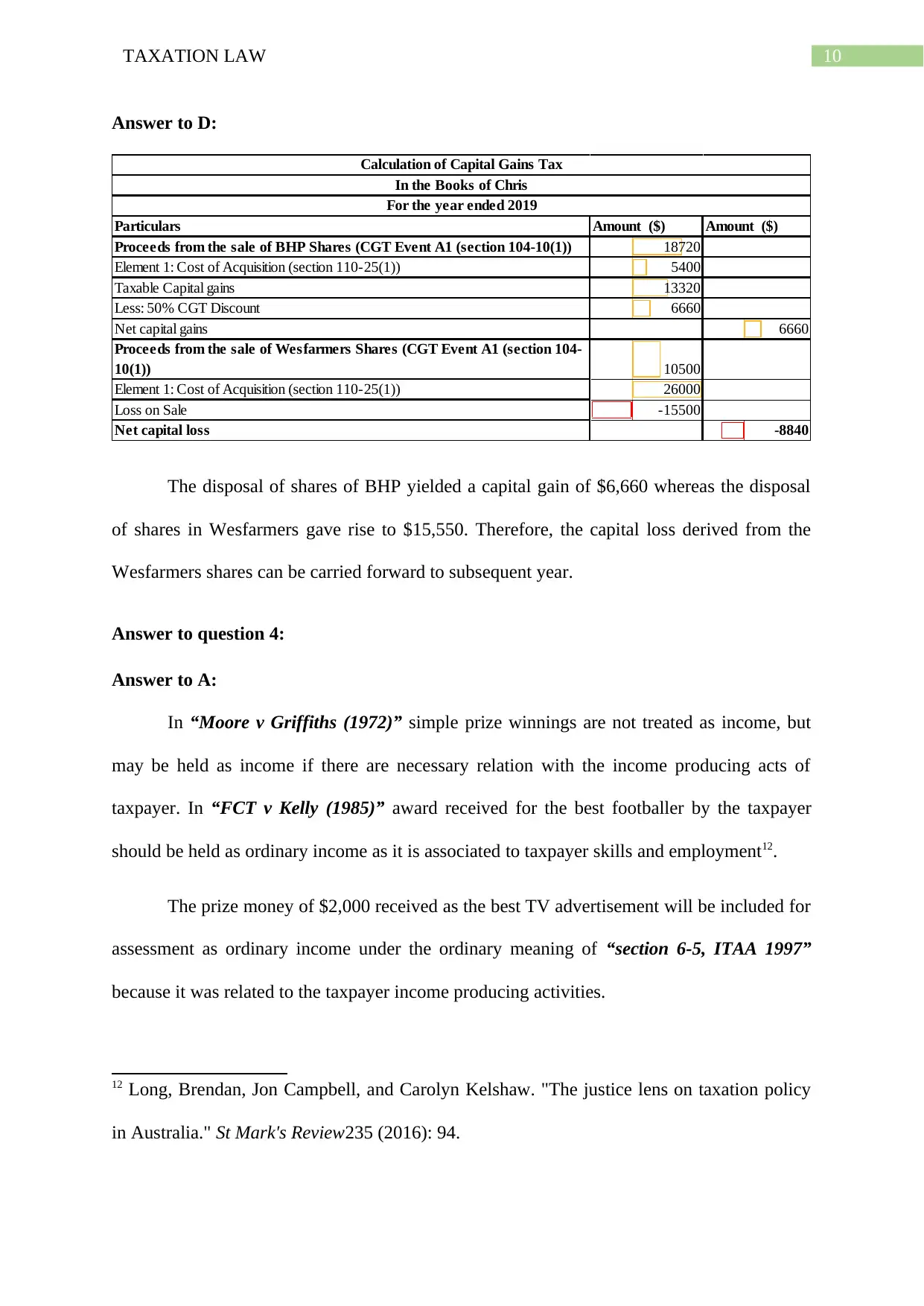

Answer to D:

Particulars Amount ($) Amount ($)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Less: 50% CGT Discount 6660

Net capital gains 6660

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -8840

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

The disposal of shares of BHP yielded a capital gain of $6,660 whereas the disposal

of shares in Wesfarmers gave rise to $15,550. Therefore, the capital loss derived from the

Wesfarmers shares can be carried forward to subsequent year.

Answer to question 4:

Answer to A:

In “Moore v Griffiths (1972)” simple prize winnings are not treated as income, but

may be held as income if there are necessary relation with the income producing acts of

taxpayer. In “FCT v Kelly (1985)” award received for the best footballer by the taxpayer

should be held as ordinary income as it is associated to taxpayer skills and employment12.

The prize money of $2,000 received as the best TV advertisement will be included for

assessment as ordinary income under the ordinary meaning of “section 6-5, ITAA 1997”

because it was related to the taxpayer income producing activities.

12 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

Answer to D:

Particulars Amount ($) Amount ($)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Less: 50% CGT Discount 6660

Net capital gains 6660

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -8840

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

The disposal of shares of BHP yielded a capital gain of $6,660 whereas the disposal

of shares in Wesfarmers gave rise to $15,550. Therefore, the capital loss derived from the

Wesfarmers shares can be carried forward to subsequent year.

Answer to question 4:

Answer to A:

In “Moore v Griffiths (1972)” simple prize winnings are not treated as income, but

may be held as income if there are necessary relation with the income producing acts of

taxpayer. In “FCT v Kelly (1985)” award received for the best footballer by the taxpayer

should be held as ordinary income as it is associated to taxpayer skills and employment12.

The prize money of $2,000 received as the best TV advertisement will be included for

assessment as ordinary income under the ordinary meaning of “section 6-5, ITAA 1997”

because it was related to the taxpayer income producing activities.

12 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

11TAXATION LAW

Answer to B:

According to the “section 6-1 of the ITAA 1936” income obtained from the private

efforts of an individual or personal exertion comprises of the remunerations, wages,

allowances, gratuities, bonus etc. that is received in capacity of the employee13.

The sum of $500 received in capacity of employee for travelling expenses from

Sydney to the workplace should be included as assessable income because it is an allowance

that is received in relation to employment.

Answer to C:

Receipt of personal gift in contrast to the other unpaid payments that are incidental to

the employment or services that are rendered is not held as income. In “Scott v FCT (1966)”

the law court held that amount given in the form of gift was not treated as taxable under the

“section 25 (1) or section 26 (e), ITAA 1936”14.

The iphone that is received by the client amounting to $1,000 cannot be included into

the assessable income because it is not an income under “section 25 (1) or section 26 (e),

ITAA 1936”.

13 Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), p.263.

14 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

Answer to B:

According to the “section 6-1 of the ITAA 1936” income obtained from the private

efforts of an individual or personal exertion comprises of the remunerations, wages,

allowances, gratuities, bonus etc. that is received in capacity of the employee13.

The sum of $500 received in capacity of employee for travelling expenses from

Sydney to the workplace should be included as assessable income because it is an allowance

that is received in relation to employment.

Answer to C:

Receipt of personal gift in contrast to the other unpaid payments that are incidental to

the employment or services that are rendered is not held as income. In “Scott v FCT (1966)”

the law court held that amount given in the form of gift was not treated as taxable under the

“section 25 (1) or section 26 (e), ITAA 1936”14.

The iphone that is received by the client amounting to $1,000 cannot be included into

the assessable income because it is not an income under “section 25 (1) or section 26 (e),

ITAA 1936”.

13 Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), p.263.

14 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.