Taxation Law Assignment: Comprehensive Analysis of Tax Law Principles

VerifiedAdded on 2023/01/16

|16

|3702

|55

Homework Assignment

AI Summary

This taxation law assignment solution provides comprehensive answers to several questions related to Australian tax law. It covers a range of topics including the useful life of depreciable assets, tax offsets, marginal tax rates, consumption tax, and capital gains tax (CGT) events. The assignment delves into specific sections of the ITAA 1997, such as those concerning tax deductions for loan interest, apportionment of losses and outgoings, and non-deductible expenses. The solution analyzes various case studies, including those related to CGT events, main residence exemptions, and the application of CGT discounts. Furthermore, the assignment addresses the taxability of prizes, reimbursements, gifts, and compensation for personal injuries, referencing relevant case law and statutory provisions to support the analysis. The document offers detailed explanations and applications of tax principles to real-world scenarios, providing a valuable resource for students studying taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................3

Answer to D:..........................................................................................................................3

Answer to E:...........................................................................................................................3

Answer to F:...........................................................................................................................4

Answer to G:..........................................................................................................................4

Answer to H:..........................................................................................................................4

Answer to I:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer to E:...........................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to A:..........................................................................................................................7

Answer to B:..........................................................................................................................7

Answer to C:..........................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................3

Answer to D:..........................................................................................................................3

Answer to E:...........................................................................................................................3

Answer to F:...........................................................................................................................4

Answer to G:..........................................................................................................................4

Answer to H:..........................................................................................................................4

Answer to I:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer to E:...........................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to A:..........................................................................................................................7

Answer to B:..........................................................................................................................7

Answer to C:..........................................................................................................................8

2TAXATION LAW

Answer to D:..........................................................................................................................8

Answer to question 4:.................................................................................................................9

Answer to A:..........................................................................................................................9

Answer to B:........................................................................................................................10

Answer to C:........................................................................................................................10

Answer to D:........................................................................................................................10

Answer to E:.........................................................................................................................11

Answer to question 5:...............................................................................................................11

Issues:...................................................................................................................................11

Laws:....................................................................................................................................11

Applications:........................................................................................................................12

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

Answer to D:..........................................................................................................................8

Answer to question 4:.................................................................................................................9

Answer to A:..........................................................................................................................9

Answer to B:........................................................................................................................10

Answer to C:........................................................................................................................10

Answer to D:........................................................................................................................10

Answer to E:.........................................................................................................................11

Answer to question 5:...............................................................................................................11

Issues:...................................................................................................................................11

Laws:....................................................................................................................................11

Applications:........................................................................................................................12

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer to A:

The taxation ruling TR 2018/14 covers the topic related to useful life of depreciable

assets within “section 40-100, ITAA 1997”1.

Answer to B:

Matters relating to the tax offsets are given under the Division 13, ITAA 19972.

Answer to C:

The highest rate of tax that is applied on the resident taxpayer during the year 2018/19

is as follows;

Limit of Assessable Income Tax ($)

$180,000 and over $54,097 + 45c for each $1 over $180,000

Answer to D:

Personal use assets under “section 118-10 (3) of the ITAA 1997” that are acquired at

$10,000 or less must be ignored from the capital gains tax.

1 "Ato.Gov.Au", Ato.Gov.Au (Webpage, 2019) <https://www.ato.gov.au/law/view/document?

DocID=TXR%2FTR20184%2FNAT%2FATO%2F00001>

2 "INCOME TAX ASSESSMENT ACT 1997 - SECT 13.1List Of Tax

Offsets", Classic.Austlii.Edu.Au (Webpage, 2019)

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s13.1.html>

Answer to question 1:

Answer to A:

The taxation ruling TR 2018/14 covers the topic related to useful life of depreciable

assets within “section 40-100, ITAA 1997”1.

Answer to B:

Matters relating to the tax offsets are given under the Division 13, ITAA 19972.

Answer to C:

The highest rate of tax that is applied on the resident taxpayer during the year 2018/19

is as follows;

Limit of Assessable Income Tax ($)

$180,000 and over $54,097 + 45c for each $1 over $180,000

Answer to D:

Personal use assets under “section 118-10 (3) of the ITAA 1997” that are acquired at

$10,000 or less must be ignored from the capital gains tax.

1 "Ato.Gov.Au", Ato.Gov.Au (Webpage, 2019) <https://www.ato.gov.au/law/view/document?

DocID=TXR%2FTR20184%2FNAT%2FATO%2F00001>

2 "INCOME TAX ASSESSMENT ACT 1997 - SECT 13.1List Of Tax

Offsets", Classic.Austlii.Edu.Au (Webpage, 2019)

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s13.1.html>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to E:

As per the “section 104-15, ITAA 1997” a CGT event B1 happens when the taxpayer

forms an arrangement with alternative entity with the right of using the CGT assets they own

is passed to alternative entity and the title of the asset may be handed to an alternative entity

or in advance the conclusion of the agreement.

Answer to F:

The formula given under “section 4-10 (3) of the ITAA 1997” is as follows;

Income Tax = [ Taxable Income x Rate] – Tax Offsets

Answer to G:

The decision that was given in the “FC of T v Day 2008 ATC 20-064” stated that

where relation among the legal expenditure and income is identified as incurred in relation to

the claim of breach of negative duties imposed based on the terms of employment was

adequate to satisfy the criteria of “paragraph 8-1 (1) (a) of the ITAA 1997”. The law court

found that the legal outgoings which was incurred by the respondent was in relation to

disciplinary action which was taken by his employer were not considered as private

outgoings. Hence, the expenses were permissible deduction within the “paragraph 8-1 (1)

(a) of the ITAA 1997”.

Answer to H:

Marginal Tax Rate Average Tax Rate

The marginal rate of tax evaluates the

impact of taxes on the earnings, expenditure

and spending3.

The average tax evaluates the taxation

burden.

3 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Answer to E:

As per the “section 104-15, ITAA 1997” a CGT event B1 happens when the taxpayer

forms an arrangement with alternative entity with the right of using the CGT assets they own

is passed to alternative entity and the title of the asset may be handed to an alternative entity

or in advance the conclusion of the agreement.

Answer to F:

The formula given under “section 4-10 (3) of the ITAA 1997” is as follows;

Income Tax = [ Taxable Income x Rate] – Tax Offsets

Answer to G:

The decision that was given in the “FC of T v Day 2008 ATC 20-064” stated that

where relation among the legal expenditure and income is identified as incurred in relation to

the claim of breach of negative duties imposed based on the terms of employment was

adequate to satisfy the criteria of “paragraph 8-1 (1) (a) of the ITAA 1997”. The law court

found that the legal outgoings which was incurred by the respondent was in relation to

disciplinary action which was taken by his employer were not considered as private

outgoings. Hence, the expenses were permissible deduction within the “paragraph 8-1 (1)

(a) of the ITAA 1997”.

Answer to H:

Marginal Tax Rate Average Tax Rate

The marginal rate of tax evaluates the

impact of taxes on the earnings, expenditure

and spending3.

The average tax evaluates the taxation

burden.

3 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

5TAXATION LAW

The marginal tax rate is regarded as the

rising value of tax which is paid on

increased revenues.

The average rate of tax constitutes the total

sum of tax that are divided by the total

earnings.

Answer to I:

The consumption tax is the tax regarding the purchase of products and services.

Consumption tax generally takes the size of sales tax, excise, tariffs and other taxes that are

imposed on the products and services.

Answer to question 2:

Answer to A:

As explained in the “section 8-1, ITAA 1997” a taxpayer is permitted to claim an

allowable income tax deduction for outlays occurred on loan interest while producing

income. As held in “Ure v FCT (1981)” taxpayer here was allowed deduction for borrowing

the sum in discharge of the mortgages on residential property4. The interest on loan occurred

by Brent to pay the employee wages is treated as allowable deduction under “section 8-1,

ITAA 1997” as it happened in ordinary business course.

Answer to B:

There are some conditions where the loss or outgoings must be apportioned up to the

limit where fractional deduction is allowed. The judgement in “Ronpibon Tin NL v FCT

(1949)” held that administrative expenses and director’s fees should be ascertained to the

extent that are incurred in producing the taxable income. Quoting “Ronpibon Tin NL v FCT

4 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

The marginal tax rate is regarded as the

rising value of tax which is paid on

increased revenues.

The average rate of tax constitutes the total

sum of tax that are divided by the total

earnings.

Answer to I:

The consumption tax is the tax regarding the purchase of products and services.

Consumption tax generally takes the size of sales tax, excise, tariffs and other taxes that are

imposed on the products and services.

Answer to question 2:

Answer to A:

As explained in the “section 8-1, ITAA 1997” a taxpayer is permitted to claim an

allowable income tax deduction for outlays occurred on loan interest while producing

income. As held in “Ure v FCT (1981)” taxpayer here was allowed deduction for borrowing

the sum in discharge of the mortgages on residential property4. The interest on loan occurred

by Brent to pay the employee wages is treated as allowable deduction under “section 8-1,

ITAA 1997” as it happened in ordinary business course.

Answer to B:

There are some conditions where the loss or outgoings must be apportioned up to the

limit where fractional deduction is allowed. The judgement in “Ronpibon Tin NL v FCT

(1949)” held that administrative expenses and director’s fees should be ascertained to the

extent that are incurred in producing the taxable income. Quoting “Ronpibon Tin NL v FCT

4 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

(1949)” the mobile phone expenses of Julie is allowable for deduction up to 60% as it is

related to work purpose while the remaining portion is a private expense and non-deductible5.

Answer to C:

Rendering “section 8-1 (2) (b), ITAA 1997” expenditure that are private and does not

satisfy the positive limbs is non-deductible under the negative limbs. As held in “Lodge v

FCT (1972)” a deduction is not permitted to taxpayer for childcare expenditure as it was not

incidental to generating taxable income6. Similarly, the babysitting expenses occurred by

Sally is non-allowable deduction under “section 8-1 (2) (b), ITAA 1997” because it is a

private expenditure.

Answer to D:

“Section 8-1, ITAA 1997” is implemented for both the loss and outgoings incurred by

taxpayer. As held in “Charles Moore & Co (WA) Pty Ltd v FCT (1956)” the taxpayer is

permitted deduction for the money that was stolen from day to day activities. Similarly, Jerry

will be permitted deduction for the theft of goods that amounted to $20,000 since it was

related to the taxpayer’s everyday business activities7.

5 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

6 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

7 Abrams, Howard E., and Don Leatherman. Federal income taxation of corporations and

partnerships. Wolters Kluwer Law & Business, 2019.

(1949)” the mobile phone expenses of Julie is allowable for deduction up to 60% as it is

related to work purpose while the remaining portion is a private expense and non-deductible5.

Answer to C:

Rendering “section 8-1 (2) (b), ITAA 1997” expenditure that are private and does not

satisfy the positive limbs is non-deductible under the negative limbs. As held in “Lodge v

FCT (1972)” a deduction is not permitted to taxpayer for childcare expenditure as it was not

incidental to generating taxable income6. Similarly, the babysitting expenses occurred by

Sally is non-allowable deduction under “section 8-1 (2) (b), ITAA 1997” because it is a

private expenditure.

Answer to D:

“Section 8-1, ITAA 1997” is implemented for both the loss and outgoings incurred by

taxpayer. As held in “Charles Moore & Co (WA) Pty Ltd v FCT (1956)” the taxpayer is

permitted deduction for the money that was stolen from day to day activities. Similarly, Jerry

will be permitted deduction for the theft of goods that amounted to $20,000 since it was

related to the taxpayer’s everyday business activities7.

5 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

6 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

7 Abrams, Howard E., and Don Leatherman. Federal income taxation of corporations and

partnerships. Wolters Kluwer Law & Business, 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to E:

Outgoings of preliminary nature or pre-commencement of income producing acts are

not in the course of earning income and hence non-deductible under “section 8-1, ITAA

1997”. The taxpayer was denied deduction in “FCT v Maddalena v FCT (1971)” for the

expenditure incurred in gaining a new employment as it occurred at a point too soon and not

in the course of earning income. Evidently, the expenditure occurred by taxpayer for

contesting a government election is non-deductible under “section 8-1, ITAA 1997” because

it is pre-commencement to income generating acts.

Answer to question 3:

Answer to A:

The taxpayer has to follow the “CGT event F2” if they are following any lease or

contract. This impacts on the taxpayer who will be getting the lease from the owner and they

gain the same right8. According to the scenario of Andy, he gave the land for lease purpose to

Brian with respect to the premium of $5,000 for five years. Hence this has resulted in “CGT

event F2” and as a result of which Andy is not eligible for getting 50% of CGT discount as

this operation is not eligible for CGT F2.

Answer to B:

As per ATO, “CGT event B1” comes into the picture when a property or land is being

leased to some new owner9. The new owner enjoys the rights and the facilities of that

particular land when the contract starts or he starts paying the rent for that particular property.

8 Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

9 Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19

(2017): 21.

Answer to E:

Outgoings of preliminary nature or pre-commencement of income producing acts are

not in the course of earning income and hence non-deductible under “section 8-1, ITAA

1997”. The taxpayer was denied deduction in “FCT v Maddalena v FCT (1971)” for the

expenditure incurred in gaining a new employment as it occurred at a point too soon and not

in the course of earning income. Evidently, the expenditure occurred by taxpayer for

contesting a government election is non-deductible under “section 8-1, ITAA 1997” because

it is pre-commencement to income generating acts.

Answer to question 3:

Answer to A:

The taxpayer has to follow the “CGT event F2” if they are following any lease or

contract. This impacts on the taxpayer who will be getting the lease from the owner and they

gain the same right8. According to the scenario of Andy, he gave the land for lease purpose to

Brian with respect to the premium of $5,000 for five years. Hence this has resulted in “CGT

event F2” and as a result of which Andy is not eligible for getting 50% of CGT discount as

this operation is not eligible for CGT F2.

Answer to B:

As per ATO, “CGT event B1” comes into the picture when a property or land is being

leased to some new owner9. The new owner enjoys the rights and the facilities of that

particular land when the contract starts or he starts paying the rent for that particular property.

8 Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

9 Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19

(2017): 21.

8TAXATION LAW

In contrast with this discussion, Farm Ltd was eligible in purchasing 100-acre farm for a sum

of $800,000 as they were paying to the land owner $40,000. Here, the CGT event B1 has

taken place hence John is eligible in getting the 50% discount as per the CGT criteria or

based on the transaction he made after being in contract.

Answer to C:

According to the Australian Taxation Office, the taxpayer is allowed for partial

residential exemption if they are not living in residence while maintaining the ownership of

that particular property. Jamie and Olivia has come across such situation as they rented one

property for two years and then they have used that particular property for generating their

taxable income. Apart from this they have also used it as a main residence before selling it

out in 2018. Hence, they are only eligible for partial main residence exemption. Olivia and

Jamie is also allowed to get 50% of the CGT discount for maintaining their capital gain tax.

Answer to D:

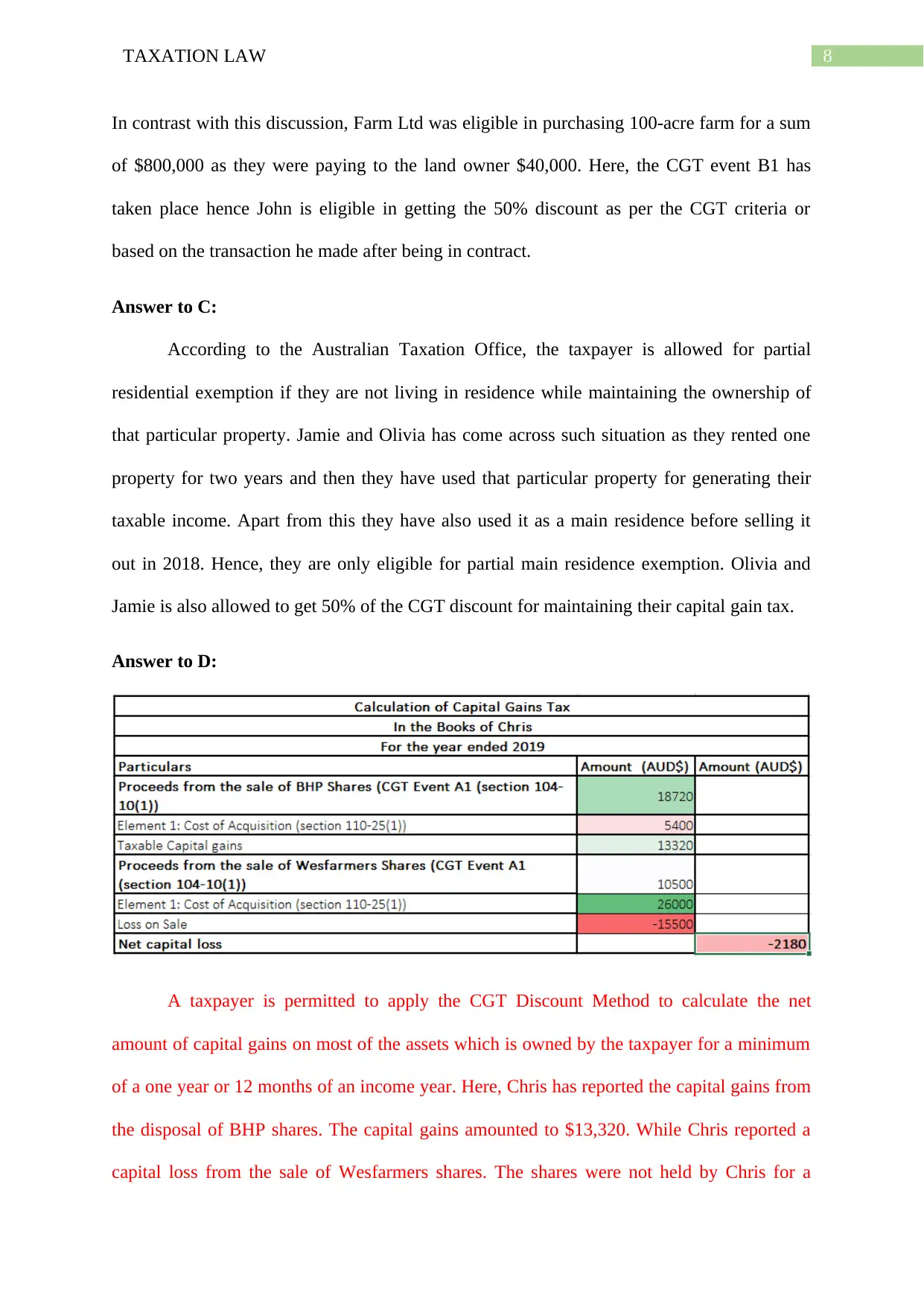

A taxpayer is permitted to apply the CGT Discount Method to calculate the net

amount of capital gains on most of the assets which is owned by the taxpayer for a minimum

of a one year or 12 months of an income year. Here, Chris has reported the capital gains from

the disposal of BHP shares. The capital gains amounted to $13,320. While Chris reported a

capital loss from the sale of Wesfarmers shares. The shares were not held by Chris for a

In contrast with this discussion, Farm Ltd was eligible in purchasing 100-acre farm for a sum

of $800,000 as they were paying to the land owner $40,000. Here, the CGT event B1 has

taken place hence John is eligible in getting the 50% discount as per the CGT criteria or

based on the transaction he made after being in contract.

Answer to C:

According to the Australian Taxation Office, the taxpayer is allowed for partial

residential exemption if they are not living in residence while maintaining the ownership of

that particular property. Jamie and Olivia has come across such situation as they rented one

property for two years and then they have used that particular property for generating their

taxable income. Apart from this they have also used it as a main residence before selling it

out in 2018. Hence, they are only eligible for partial main residence exemption. Olivia and

Jamie is also allowed to get 50% of the CGT discount for maintaining their capital gain tax.

Answer to D:

A taxpayer is permitted to apply the CGT Discount Method to calculate the net

amount of capital gains on most of the assets which is owned by the taxpayer for a minimum

of a one year or 12 months of an income year. Here, Chris has reported the capital gains from

the disposal of BHP shares. The capital gains amounted to $13,320. While Chris reported a

capital loss from the sale of Wesfarmers shares. The shares were not held by Chris for a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

period 12 months. Therefore, no CGT discount method can be applied for the capital gains

made on the sale BHP shares that amounted to $13,320 in case of Chris. While Chris can

carry forward the capital loss from Wesfarmers in the next income year.

Answer to question 4:

Answer to A:

A taxpayer is not considered taxable for their prizes. However, if these prizes are

relevant to their taxable income then that might be considered to be taxable as ordinary

income. According to “FCT v Kelly (1985)” the taxpayer had received an award from

Channel 7 for being the fairest and the best player, in this scenario this award is considered as

the ordinary income because this award was associated with taxpayer’s skills which was

helpful to him for earning ordinary or taxable income10.

Referring “section 6-5, ITAA 1997” the taxpayer’s prize money of $2,000 was

considered as the ordinary income. This gain was taxable for the taxpayer as this was directly

in relation with taxpayer’s income producing activities.

Answer to B:

According to “section 6-1 of the ITAA 1936” the taxpayer is should include income

for assessment purpose obtained from the personal exertion income. This includes gratuity,

remuneration, wages and allowances11.

10 James, Kieran. "The Australian Taxation Office perspective on work-related travel expense

deductions for academics." International Journal of Critical Accounting 8.5-6 (2016): 345-

362.

11 Burton, Hughlene A., and Stewart Karlinsky. "Tax professionals' perception of large and

mid-size business US tax law complexity." eJTR 14 (2016): 61.

period 12 months. Therefore, no CGT discount method can be applied for the capital gains

made on the sale BHP shares that amounted to $13,320 in case of Chris. While Chris can

carry forward the capital loss from Wesfarmers in the next income year.

Answer to question 4:

Answer to A:

A taxpayer is not considered taxable for their prizes. However, if these prizes are

relevant to their taxable income then that might be considered to be taxable as ordinary

income. According to “FCT v Kelly (1985)” the taxpayer had received an award from

Channel 7 for being the fairest and the best player, in this scenario this award is considered as

the ordinary income because this award was associated with taxpayer’s skills which was

helpful to him for earning ordinary or taxable income10.

Referring “section 6-5, ITAA 1997” the taxpayer’s prize money of $2,000 was

considered as the ordinary income. This gain was taxable for the taxpayer as this was directly

in relation with taxpayer’s income producing activities.

Answer to B:

According to “section 6-1 of the ITAA 1936” the taxpayer is should include income

for assessment purpose obtained from the personal exertion income. This includes gratuity,

remuneration, wages and allowances11.

10 James, Kieran. "The Australian Taxation Office perspective on work-related travel expense

deductions for academics." International Journal of Critical Accounting 8.5-6 (2016): 345-

362.

11 Burton, Hughlene A., and Stewart Karlinsky. "Tax professionals' perception of large and

mid-size business US tax law complexity." eJTR 14 (2016): 61.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

According to the considered case study, the employee gained $500 from his employer

as he visited Sydney and came back to his workspace for the purpose of his work. In contrast

with this scenario, the amount $500 will be considered as reimbursement of expenses for the

expenses that was occurred by the taxpayer. Therefor it is not an income under ordinary

concepts.

Answer to C:

The tax payer can be given personal gifts, however, if these are not related to their

income then these will not be considered as their ordinary gain. As per “FCT v Scott (1966)”,

the court has suggested, the gift of 10,000 pounds from the longstanding wife of client will

not be considered as the income in the absence of husband. Along with this the iPhone

received by the taxpayer is worth $1,000, however this will not be considered as income as

well because it is a simple gift.

Answer to D:

As held in “paragraph 118-37 (1) (b) of the ITAA 1997”, the taxpayer should

disregard the money which he has received for his personal injury or illness or damages

which has been caused by personal reason.

The taxpayer had meet with an accident and he received about $10,000 for his

personal injuries. In this case the compensation amount will not be considered as taxable

income and taxpayer should not pay the tax for this.

Answer to E:

The taxpayer is eligible to involve himself in different earning activities however if he

is involving himself for the earning activities which are yet to be executed in the current

income year and also planned for the future years, it will not be considered as the income for

the current income year. In respect of above the discussion, the case study highlights that the

According to the considered case study, the employee gained $500 from his employer

as he visited Sydney and came back to his workspace for the purpose of his work. In contrast

with this scenario, the amount $500 will be considered as reimbursement of expenses for the

expenses that was occurred by the taxpayer. Therefor it is not an income under ordinary

concepts.

Answer to C:

The tax payer can be given personal gifts, however, if these are not related to their

income then these will not be considered as their ordinary gain. As per “FCT v Scott (1966)”,

the court has suggested, the gift of 10,000 pounds from the longstanding wife of client will

not be considered as the income in the absence of husband. Along with this the iPhone

received by the taxpayer is worth $1,000, however this will not be considered as income as

well because it is a simple gift.

Answer to D:

As held in “paragraph 118-37 (1) (b) of the ITAA 1997”, the taxpayer should

disregard the money which he has received for his personal injury or illness or damages

which has been caused by personal reason.

The taxpayer had meet with an accident and he received about $10,000 for his

personal injuries. In this case the compensation amount will not be considered as taxable

income and taxpayer should not pay the tax for this.

Answer to E:

The taxpayer is eligible to involve himself in different earning activities however if he

is involving himself for the earning activities which are yet to be executed in the current

income year and also planned for the future years, it will not be considered as the income for

the current income year. In respect of above the discussion, the case study highlights that the

11TAXATION LAW

taxpayer purchased the shares with the value of $5 however the current market value of this

share is $7.50. Hence, this increase in price will not be considered as his income as he has not

earned this gain. As per “section 6-5, ITAA 1997” the taxpayer is not eligible to include his

gain in the ordinary year’s income if that is planned for any future perspectives12.

Answer to question 5:

Issues:

This section is highlighting discussion if the migrant to Australia will be considered

as Australian occupant or not under “section 6 (1), ITAA 1936”.

Rule:

According to “section 6-1 of the ITAA 1997”, people who are residing in Australia

from a long time and who are having permanent residence in Australia will be considered as

the Australian resident. However, to discuss this fact from the perspective of commissioner of

taxation people who are residing in Australia might have residence outside of Australia will

not be held Australian resident13. Hence, to judge who is actually residing in Australia there

are four residence tests in Australia. The person can be Australian resident if they meet one of

these four criteria. These tests are Ordinary concepts test, resides test, 183 day’s test and

superannuation test. A person needs to meet one of these tests to be an Australian resident.

According to reside test the person should be present for a longer span of time in

Australia regardless of their nationality, religion or any other specific parameter. Whereas,

12 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

13 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

taxpayer purchased the shares with the value of $5 however the current market value of this

share is $7.50. Hence, this increase in price will not be considered as his income as he has not

earned this gain. As per “section 6-5, ITAA 1997” the taxpayer is not eligible to include his

gain in the ordinary year’s income if that is planned for any future perspectives12.

Answer to question 5:

Issues:

This section is highlighting discussion if the migrant to Australia will be considered

as Australian occupant or not under “section 6 (1), ITAA 1936”.

Rule:

According to “section 6-1 of the ITAA 1997”, people who are residing in Australia

from a long time and who are having permanent residence in Australia will be considered as

the Australian resident. However, to discuss this fact from the perspective of commissioner of

taxation people who are residing in Australia might have residence outside of Australia will

not be held Australian resident13. Hence, to judge who is actually residing in Australia there

are four residence tests in Australia. The person can be Australian resident if they meet one of

these four criteria. These tests are Ordinary concepts test, resides test, 183 day’s test and

superannuation test. A person needs to meet one of these tests to be an Australian resident.

According to reside test the person should be present for a longer span of time in

Australia regardless of their nationality, religion or any other specific parameter. Whereas,

12 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

13 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

![Taxation Law Assignment - LAWS20060, Semester 1, [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fzu%2F803f7afcdaf14edca4b16cd62f859dfd.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.