LAWS20060: Taxation Law of Australia Individual Assignment - Term 2

VerifiedAdded on 2022/09/18

|12

|3522

|20

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing key aspects of Australian taxation. The assignment covers various topics, including the determination of when a company is considered to be carrying on a business, deductibility of contributions and gifts, and the highest applicable tax rates for resident taxpayers. It delves into the capital gains tax (CGT) treatment of assets, the tax-free threshold for individuals, and the legal principle established in Hayes v FCT regarding CGT gains. Furthermore, the solution explores different classes of income, distinguishing between ordinary and statutory income, and explains the Medicare Levy and Medicare Levy Surcharge. The assignment also examines residency tests under s 6.1 ITAA 36, clarifying the concepts of 'usual place of abode' and 'permanent place of abode' with reference to relevant case law. Finally, the solution analyzes the deductibility of various expenditures, such as HECS-HELP repayments, work-related travel expenses, book purchases, and childcare costs, based on s 8.1 and s 25.100 of the ITAA 97, providing a detailed understanding of the relevant tax provisions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Author Note

Taxation Law

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Q. 1

a) The topic covered by TR 2019/11 is the time when a company would be rendered to carry out

an activity, which depicts business.

b) The legal provisions that has been contained in div 30 of ITAA 972, deals with the

deductibility of the contributions as well as gifts.

c) The highest tax rate that will be applicable 21 individual who is a resident taxpayer for the year

2019-20 will be the amount of $54097 with an additional of 45% rate over any amount exceeding

$1800003.

d) Car as well as motorcycle is required to be treated as an exempt from being subjected to capital

gain taxation as per the provisions contained in s 118.5 of the ITAA 974.

e) Any asset of capital nature that has been owned by the taxpayer but has been destroyed or has

been lost from here would be required to be dealt with as a CGT event of C1 category as per the

provisions contained in s 104.20 of the ITAA 975.

f) The threshold that has been recently applicable for the resident individual for being tax free

with respect to his assessable income is an income amounting below $18200.

g) The main legal principle that has evolved with the decision of the High Court in the case of

Hayes v FCT (1956) 96 CLR 476 was the fact that any amount that has been received by the taxpayer

against any of the services he has rendered in the past would be required to be treated as a CGT gain for

the purpose of assessability. In this context, it can be stated that the amount received by a person being an

employee from his employer with respect to the services of employment he has rendered previously and

1 TR 2019/1

2 The Income Tax Assessment Act 1997 (Cth), div 30

3 www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

4 The Income Tax Assessment Act 1997 (Cth), s 118.5

5 The Income Tax Assessment Act 1997 (Cth), s 104.20

6 Hayes v FCT (1956) 96 CLR 47

Q. 1

a) The topic covered by TR 2019/11 is the time when a company would be rendered to carry out

an activity, which depicts business.

b) The legal provisions that has been contained in div 30 of ITAA 972, deals with the

deductibility of the contributions as well as gifts.

c) The highest tax rate that will be applicable 21 individual who is a resident taxpayer for the year

2019-20 will be the amount of $54097 with an additional of 45% rate over any amount exceeding

$1800003.

d) Car as well as motorcycle is required to be treated as an exempt from being subjected to capital

gain taxation as per the provisions contained in s 118.5 of the ITAA 974.

e) Any asset of capital nature that has been owned by the taxpayer but has been destroyed or has

been lost from here would be required to be dealt with as a CGT event of C1 category as per the

provisions contained in s 104.20 of the ITAA 975.

f) The threshold that has been recently applicable for the resident individual for being tax free

with respect to his assessable income is an income amounting below $18200.

g) The main legal principle that has evolved with the decision of the High Court in the case of

Hayes v FCT (1956) 96 CLR 476 was the fact that any amount that has been received by the taxpayer

against any of the services he has rendered in the past would be required to be treated as a CGT gain for

the purpose of assessability. In this context, it can be stated that the amount received by a person being an

employee from his employer with respect to the services of employment he has rendered previously and

1 TR 2019/1

2 The Income Tax Assessment Act 1997 (Cth), div 30

3 www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

4 The Income Tax Assessment Act 1997 (Cth), s 118.5

5 The Income Tax Assessment Act 1997 (Cth), s 104.20

6 Hayes v FCT (1956) 96 CLR 47

2TAXATION LAW

received of the same has been accrued at the past would be included in the assessable income of that

employee as a capital gain. However, for the purpose of deciding upon a situation, where there is a

dilemma between the treatment of a receipt that has been received from past employer for the

employment services rendered previously, whether to include the receipt with the capital gain or with

respect to ordinary income. All the income has been received for the application of personal exertion is

required to be treated as an ordinary income, however, in case of receipt from former employer, where the

receipt has already been accrued but the same has not been provided to the taxpayer. This would render

the receive to have been acquired the nature of a capital asset as the same has been received by the

taxpayer as a lump sum amount on a subsequent period from that of the accrual of the same.

h) Two classes of income can be earned by an individual taxpayer, as per the categories of taxable

income that has been provided in the taxation law. The first income that needs to be recognised for this

purpose is the ordinary income. The other taxable income would include the statutory income. The

income that can be construed as a income from the general definitions as well as common contentions

apprehended by the public not having adequate legal knowledge would be treated as ordinary income. For

the purpose of assessing such incomes no stringent rules needs to be complied with as provided by the

statutes. In the absence of any express mention within the statutes related to taxation, an ordinary income

would be assessable income. Hence, it can be stated that any income that can be rendered as an income

through the ordinary concepts existing would be treated as an ordinary income. Again, any income that

has been expressly provided in the statute relating to taxation to be an income of a particular nature is

required to be treated as a statutory income. Statutory income would only be taxable if the same has been

supported by a legal provision contained in a statute. This form of income does not follow from the

ordinary concepts but needs statutory recognition for the purpose of being assessable as an income7.

i) The Medicare Levy and the Medicare Levy Surcharge implies two additional rates that are

imposed upon the taxpayers eligible for the same. There are certain taxpayers who are required to make

7 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

received of the same has been accrued at the past would be included in the assessable income of that

employee as a capital gain. However, for the purpose of deciding upon a situation, where there is a

dilemma between the treatment of a receipt that has been received from past employer for the

employment services rendered previously, whether to include the receipt with the capital gain or with

respect to ordinary income. All the income has been received for the application of personal exertion is

required to be treated as an ordinary income, however, in case of receipt from former employer, where the

receipt has already been accrued but the same has not been provided to the taxpayer. This would render

the receive to have been acquired the nature of a capital asset as the same has been received by the

taxpayer as a lump sum amount on a subsequent period from that of the accrual of the same.

h) Two classes of income can be earned by an individual taxpayer, as per the categories of taxable

income that has been provided in the taxation law. The first income that needs to be recognised for this

purpose is the ordinary income. The other taxable income would include the statutory income. The

income that can be construed as a income from the general definitions as well as common contentions

apprehended by the public not having adequate legal knowledge would be treated as ordinary income. For

the purpose of assessing such incomes no stringent rules needs to be complied with as provided by the

statutes. In the absence of any express mention within the statutes related to taxation, an ordinary income

would be assessable income. Hence, it can be stated that any income that can be rendered as an income

through the ordinary concepts existing would be treated as an ordinary income. Again, any income that

has been expressly provided in the statute relating to taxation to be an income of a particular nature is

required to be treated as a statutory income. Statutory income would only be taxable if the same has been

supported by a legal provision contained in a statute. This form of income does not follow from the

ordinary concepts but needs statutory recognition for the purpose of being assessable as an income7.

i) The Medicare Levy and the Medicare Levy Surcharge implies two additional rates that are

imposed upon the taxpayers eligible for the same. There are certain taxpayers who are required to make

7 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

payment with respect to do additional taxes over the income tax payable by them. These include the

Medicare Levy and the Medicare Levy Surcharge. The Medicare Levy has been introduced for the

purpose of finding the Medicare that depicts the public health system of Australia. The same is to be

imposed upon the taxable income of an individual. The same is to be paid at a flat rate of two percent.

This tax is imposed by the Medicare Levy Act 19868 and the ITAA 369. Again, Medicare Levy Surcharge

has been introduced for the purpose of encouraging the individual taxpayers earning higher incomes to

make payment towards private health insurance for the purpose of reducing the burden upon the

Medicare. This form of taxation is only applied to the individual taxpayers who are not having any private

health Insurance. This levy is required to be imposed upon the total of the taxable income as well as

Fringe Benefits pertaining to an individual taxpayer. Depending upon the income of a taxpayer the rates

of this form of levy may vary between 1%, 1.25% and 1.5%10.

Q.2

As per the provisions contained in s 6.1 ITAA 3611, three tests are required to be involved in the

assessment of the residency of an individual within Australia. The domicile test, resides test, super

admission test as well as the 183 day test are required to be applied for the purpose of assessing the

taxability of an individual living in Australia or has any attachment with Australia. However, there are

two concepts that can be found in this section while discussing regarding the abovementioned tests.

Although, the two concepts namely usual place of abode and permanent place of abode sound similar but

the same has been assigned with distinct meaning as per the contentions of the taxation law prevailing in

Australia. Both the concepts has a similarity with respect to the concept of place of abode. For the

purpose of assessing these two concepts the meaning of the term place of abode is required to be clarified.

The concept of place of a boat is required to be analysed under the legal rule laid down in the decision of

8 The Medicare Levy Act 1986

9 The Income Tax Assessment Act 1936 (Cth)

10 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

11 The Income Tax Assessment Act 1936 (Cth), s 6.1

payment with respect to do additional taxes over the income tax payable by them. These include the

Medicare Levy and the Medicare Levy Surcharge. The Medicare Levy has been introduced for the

purpose of finding the Medicare that depicts the public health system of Australia. The same is to be

imposed upon the taxable income of an individual. The same is to be paid at a flat rate of two percent.

This tax is imposed by the Medicare Levy Act 19868 and the ITAA 369. Again, Medicare Levy Surcharge

has been introduced for the purpose of encouraging the individual taxpayers earning higher incomes to

make payment towards private health insurance for the purpose of reducing the burden upon the

Medicare. This form of taxation is only applied to the individual taxpayers who are not having any private

health Insurance. This levy is required to be imposed upon the total of the taxable income as well as

Fringe Benefits pertaining to an individual taxpayer. Depending upon the income of a taxpayer the rates

of this form of levy may vary between 1%, 1.25% and 1.5%10.

Q.2

As per the provisions contained in s 6.1 ITAA 3611, three tests are required to be involved in the

assessment of the residency of an individual within Australia. The domicile test, resides test, super

admission test as well as the 183 day test are required to be applied for the purpose of assessing the

taxability of an individual living in Australia or has any attachment with Australia. However, there are

two concepts that can be found in this section while discussing regarding the abovementioned tests.

Although, the two concepts namely usual place of abode and permanent place of abode sound similar but

the same has been assigned with distinct meaning as per the contentions of the taxation law prevailing in

Australia. Both the concepts has a similarity with respect to the concept of place of abode. For the

purpose of assessing these two concepts the meaning of the term place of abode is required to be clarified.

The concept of place of a boat is required to be analysed under the legal rule laid down in the decision of

8 The Medicare Levy Act 1986

9 The Income Tax Assessment Act 1936 (Cth)

10 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

11 The Income Tax Assessment Act 1936 (Cth), s 6.1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

I.R.C. v. Lysaght (1928) A.C.23412. As per the principles of this case, place of abode would be treated as

any residential property, which the taxpayer has been holding by way of either ownership or lease with an

intention to live or dwell in that place with all the surroundings and family he has. The motive of the

person living in the property is required to be assessed for the purpose of rendering the residence as a

place of abode.

Permanent place of abode is a concept that can be best explained with the decision of FC of T v

Applegate 79 ATC 430713. As per the provisions established in this case, a permanent place of a boat

depicts a place where the taxpayer has been living with an intention of residing there for a considerable

amount of time without any contention of leaving that place. The time period for which an individual is

required to residing in that place is indefinite but not forever. In this case any time period of more than

three years with the intention of living in that place would render the place to be a permanent place of

abode. Due consideration is required to be extended towards the motive of the individual living in that

property. There has been no intention of the individual to abandon that place in which he has been

residing. This can further be supported with the case of F.C. of T. v. Jenkins 82 ATC 409814.

Again, the concept of usual place of abode is required to be assessed in relation to domicile. This

requires a person to live in a property for the main purpose of for the sole purpose of living in that place

as per the custom or habit. A rented accommodation can also be brought under the purview of usual place

of abode as the person has been living in that place for a considerable time for the purpose of his stay at a

particular place. Such a residence should not be confused with a permanent place of abode. This can

further be illustrated with the case of Levene v. I.R.C.(1928) A.C.21715.

12 I.R.C. v. Lysaght (1928) A.C.234

13 FC of T v Applegate 79 ATC 4307

14 F.C. of T. v. Jenkins 82 ATC 4098

15 Levene v. I.R.C.(1928) A.C.217

I.R.C. v. Lysaght (1928) A.C.23412. As per the principles of this case, place of abode would be treated as

any residential property, which the taxpayer has been holding by way of either ownership or lease with an

intention to live or dwell in that place with all the surroundings and family he has. The motive of the

person living in the property is required to be assessed for the purpose of rendering the residence as a

place of abode.

Permanent place of abode is a concept that can be best explained with the decision of FC of T v

Applegate 79 ATC 430713. As per the provisions established in this case, a permanent place of a boat

depicts a place where the taxpayer has been living with an intention of residing there for a considerable

amount of time without any contention of leaving that place. The time period for which an individual is

required to residing in that place is indefinite but not forever. In this case any time period of more than

three years with the intention of living in that place would render the place to be a permanent place of

abode. Due consideration is required to be extended towards the motive of the individual living in that

property. There has been no intention of the individual to abandon that place in which he has been

residing. This can further be supported with the case of F.C. of T. v. Jenkins 82 ATC 409814.

Again, the concept of usual place of abode is required to be assessed in relation to domicile. This

requires a person to live in a property for the main purpose of for the sole purpose of living in that place

as per the custom or habit. A rented accommodation can also be brought under the purview of usual place

of abode as the person has been living in that place for a considerable time for the purpose of his stay at a

particular place. Such a residence should not be confused with a permanent place of abode. This can

further be illustrated with the case of Levene v. I.R.C.(1928) A.C.21715.

12 I.R.C. v. Lysaght (1928) A.C.234

13 FC of T v Applegate 79 ATC 4307

14 F.C. of T. v. Jenkins 82 ATC 4098

15 Levene v. I.R.C.(1928) A.C.217

5TAXATION LAW

Q.3

a) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9716. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. In

the present scenario, the expenditure towards HECS-HELP amounting to $850 has been incurred with

respect to a personal student loan. This expenditure has nothing to do with the assessable income of the

person. Hence, would not be allowed as a deduction.

b) The expenditure that an individual taxpayer in course while travelling towards the workplace is

to be allowed as an expense which is deductible as per the rule mentioned in s 25.100 of ITAA 9717. In

the present situation the expenditure that has been incurred from travelling to the university from

workplace amounting to $110 would be required to be treated as a deductible amount.

c) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9718. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. In

the present case the expenditure that has been incurred by the taxpayer for the purpose of acquiring books

worth $200 is required to be treated as a deductible expense. This is because the income has been incurred

for the betterment of the knowledge and skills of the accountant which would in turn assist him in his

income earning process. Hence, this amount will be deductible.

16 The Income Tax Assessment Act 1997 (Cth), s 8.1

17 The Income Tax Assessment Act 1997 (Cth), s 25.100

18 The Income Tax Assessment Act 1997 (Cth), s 8.1

Q.3

a) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9716. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. In

the present scenario, the expenditure towards HECS-HELP amounting to $850 has been incurred with

respect to a personal student loan. This expenditure has nothing to do with the assessable income of the

person. Hence, would not be allowed as a deduction.

b) The expenditure that an individual taxpayer in course while travelling towards the workplace is

to be allowed as an expense which is deductible as per the rule mentioned in s 25.100 of ITAA 9717. In

the present situation the expenditure that has been incurred from travelling to the university from

workplace amounting to $110 would be required to be treated as a deductible amount.

c) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9718. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. In

the present case the expenditure that has been incurred by the taxpayer for the purpose of acquiring books

worth $200 is required to be treated as a deductible expense. This is because the income has been incurred

for the betterment of the knowledge and skills of the accountant which would in turn assist him in his

income earning process. Hence, this amount will be deductible.

16 The Income Tax Assessment Act 1997 (Cth), s 8.1

17 The Income Tax Assessment Act 1997 (Cth), s 25.100

18 The Income Tax Assessment Act 1997 (Cth), s 8.1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

d) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9719. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. This

can further be illustrated with the case of Lodge v Federal Commissioner of Taxation [1972] HCA 4920.

The expense of $80 incurred for child care at the time of evening classes cannot be treated as an expense

related to the profession of the person earning income for the taxpayer. It is required to be treated as more

of a domestic or private expense. Hence, it will not be permitted as deductible.

e) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9721. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. This

can further be illustrated with the case of Lodge v Federal Commissioner of Taxation [1972] HCA 4922.

The expense of $250 incurred for repairing the fridge at home cannot be treated as an expense related to

the profession of the person earning income for the taxpayer. It is required to be treated as more of a

domestic or private expense. Hence, it will not be permitted as deductible.

f) The expenditure incurred for making a purchase of clothing for being worn in the workplace

cannot be e permitted as deductible as per the provisions in s 8.1 of ITAA 9723. Therefore, amount of 145

dollars for the purpose of purchasing black trousers as well as shirts will not be permitted as an amount

which is deductible.

19 ibid

20 Lodge v Federal Commissioner of Taxation [1972] HCA 49

21 The Income Tax Assessment Act 1997 (Cth), s 8.1

22 Lodge v Federal Commissioner of Taxation [1972] HCA 49

23 The Income Tax Assessment Act 1997 (Cth), s 8.1

d) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9719. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. This

can further be illustrated with the case of Lodge v Federal Commissioner of Taxation [1972] HCA 4920.

The expense of $80 incurred for child care at the time of evening classes cannot be treated as an expense

related to the profession of the person earning income for the taxpayer. It is required to be treated as more

of a domestic or private expense. Hence, it will not be permitted as deductible.

e) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9721. Again, for the purpose of

claiming such deduction the taxpayer would be required to represent that the expenditure was not having

a connection with a domestic or private purpose but is solely based upon the income earning process. This

can further be illustrated with the case of Lodge v Federal Commissioner of Taxation [1972] HCA 4922.

The expense of $250 incurred for repairing the fridge at home cannot be treated as an expense related to

the profession of the person earning income for the taxpayer. It is required to be treated as more of a

domestic or private expense. Hence, it will not be permitted as deductible.

f) The expenditure incurred for making a purchase of clothing for being worn in the workplace

cannot be e permitted as deductible as per the provisions in s 8.1 of ITAA 9723. Therefore, amount of 145

dollars for the purpose of purchasing black trousers as well as shirts will not be permitted as an amount

which is deductible.

19 ibid

20 Lodge v Federal Commissioner of Taxation [1972] HCA 49

21 The Income Tax Assessment Act 1997 (Cth), s 8.1

22 Lodge v Federal Commissioner of Taxation [1972] HCA 49

23 The Income Tax Assessment Act 1997 (Cth), s 8.1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

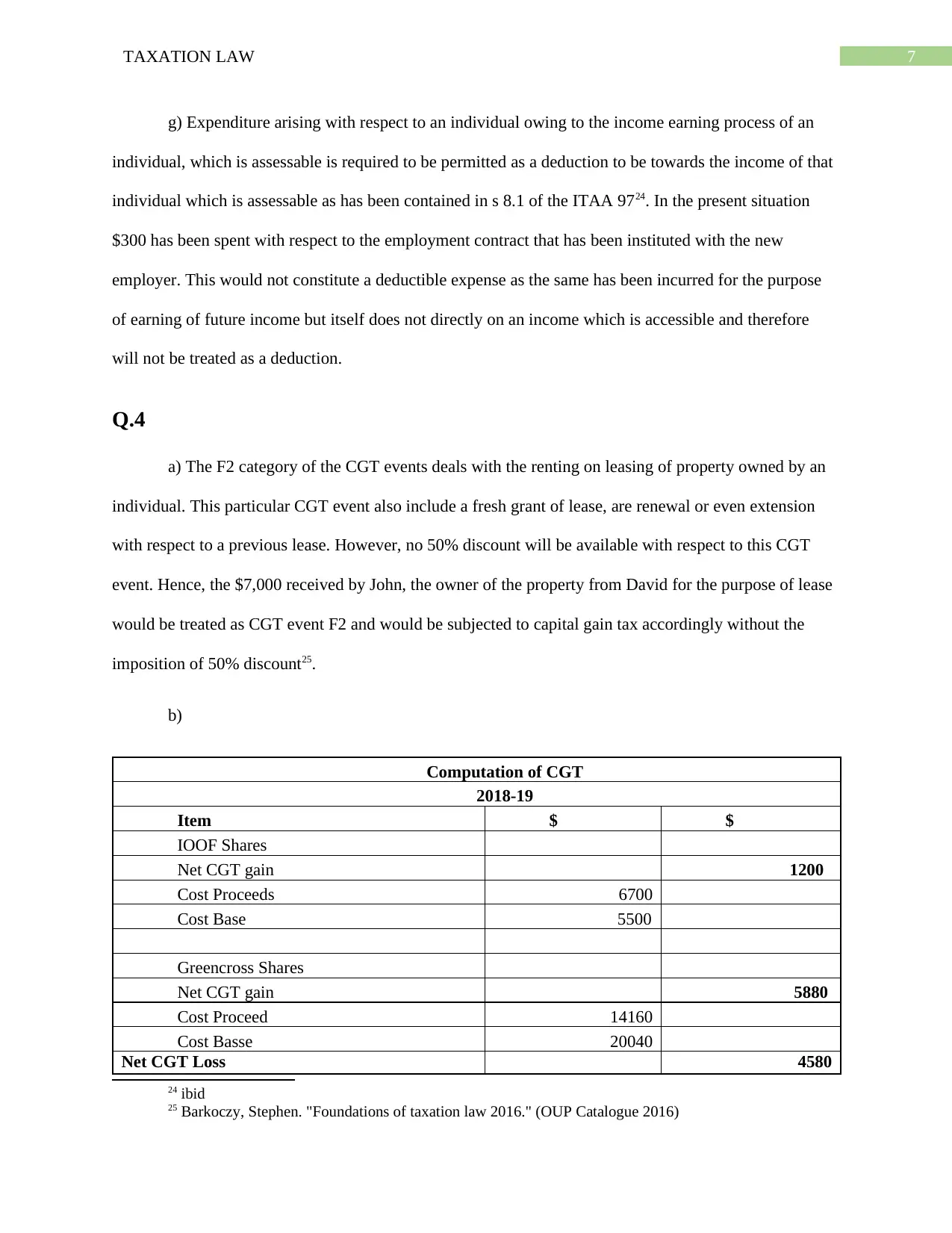

g) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9724. In the present situation

$300 has been spent with respect to the employment contract that has been instituted with the new

employer. This would not constitute a deductible expense as the same has been incurred for the purpose

of earning of future income but itself does not directly on an income which is accessible and therefore

will not be treated as a deduction.

Q.4

a) The F2 category of the CGT events deals with the renting on leasing of property owned by an

individual. This particular CGT event also include a fresh grant of lease, are renewal or even extension

with respect to a previous lease. However, no 50% discount will be available with respect to this CGT

event. Hence, the $7,000 received by John, the owner of the property from David for the purpose of lease

would be treated as CGT event F2 and would be subjected to capital gain tax accordingly without the

imposition of 50% discount25.

b)

Computation of CGT

2018-19

Item $ $

IOOF Shares

Net CGT gain 1200

Cost Proceeds 6700

Cost Base 5500

Greencross Shares

Net CGT gain 5880

Cost Proceed 14160

Cost Basse 20040

Net CGT Loss 4580

24 ibid

25 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016)

g) Expenditure arising with respect to an individual owing to the income earning process of an

individual, which is assessable is required to be permitted as a deduction to be towards the income of that

individual which is assessable as has been contained in s 8.1 of the ITAA 9724. In the present situation

$300 has been spent with respect to the employment contract that has been instituted with the new

employer. This would not constitute a deductible expense as the same has been incurred for the purpose

of earning of future income but itself does not directly on an income which is accessible and therefore

will not be treated as a deduction.

Q.4

a) The F2 category of the CGT events deals with the renting on leasing of property owned by an

individual. This particular CGT event also include a fresh grant of lease, are renewal or even extension

with respect to a previous lease. However, no 50% discount will be available with respect to this CGT

event. Hence, the $7,000 received by John, the owner of the property from David for the purpose of lease

would be treated as CGT event F2 and would be subjected to capital gain tax accordingly without the

imposition of 50% discount25.

b)

Computation of CGT

2018-19

Item $ $

IOOF Shares

Net CGT gain 1200

Cost Proceeds 6700

Cost Base 5500

Greencross Shares

Net CGT gain 5880

Cost Proceed 14160

Cost Basse 20040

Net CGT Loss 4580

24 ibid

25 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016)

8TAXATION LAW

c) As per the legal principle enumerated in s 118.100 of ITAA 9726, if a property is occupied by a

person with a view to treated as the main residence, the proceeds from the sale of such a property will be

e allowed as an exemption from the capital gain tax. Again, for availing such an exemption, the property

is actually required to be lived upon as a main residence. The renting out of a property will not be treated

as a property used for residential purposes. Again, in case of any business or similar profit making

scheme being carried out in a part of that particular property and the rest is being used for residential

purposes, the proceeds from the sale of such property is required to be treated as exemption as to the

extent of that part only which has been used as a residence and is to be calculated proportionally.

d) Cost base implies the expense incurred for the acquisition of an asset u/s 110.25 of ITAA 9727.

Such a cost includes the cost of purchase of that asset and in addition the holding and the disposal cost

pertaining to the asset. Cost base consists of five components which include acquisition cost, incidental

cost, owning cost, conversion cost and preservation cost.

On the other hand, reduced cost base is not the same as cost base and is required to be calculated

in case the transaction of capital nature has not been presenting any gain. This amount is required to be

assessed for the purpose of discovering any loss that has accrued from the transaction. The principal

regarding the same has been contained in s 110.55 of ITAA 9728.

Q.5

a) Any income earned by way of illegal ventures will not generally be assessable. However, it

will only be treated as assessable if the same has been executed in a way which depicts business. This can

26 The Income Tax Assessment Act 1997 (Cth), s 118.100

27 The Income Tax Assessment Act 1997 (Cth), s 110.25

28 The Income Tax Assessment Act 1997 (Cth), s 110.55

c) As per the legal principle enumerated in s 118.100 of ITAA 9726, if a property is occupied by a

person with a view to treated as the main residence, the proceeds from the sale of such a property will be

e allowed as an exemption from the capital gain tax. Again, for availing such an exemption, the property

is actually required to be lived upon as a main residence. The renting out of a property will not be treated

as a property used for residential purposes. Again, in case of any business or similar profit making

scheme being carried out in a part of that particular property and the rest is being used for residential

purposes, the proceeds from the sale of such property is required to be treated as exemption as to the

extent of that part only which has been used as a residence and is to be calculated proportionally.

d) Cost base implies the expense incurred for the acquisition of an asset u/s 110.25 of ITAA 9727.

Such a cost includes the cost of purchase of that asset and in addition the holding and the disposal cost

pertaining to the asset. Cost base consists of five components which include acquisition cost, incidental

cost, owning cost, conversion cost and preservation cost.

On the other hand, reduced cost base is not the same as cost base and is required to be calculated

in case the transaction of capital nature has not been presenting any gain. This amount is required to be

assessed for the purpose of discovering any loss that has accrued from the transaction. The principal

regarding the same has been contained in s 110.55 of ITAA 9728.

Q.5

a) Any income earned by way of illegal ventures will not generally be assessable. However, it

will only be treated as assessable if the same has been executed in a way which depicts business. This can

26 The Income Tax Assessment Act 1997 (Cth), s 118.100

27 The Income Tax Assessment Act 1997 (Cth), s 110.25

28 The Income Tax Assessment Act 1997 (Cth), s 110.55

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

be illustrated with the case of FC of T v La Rosa 2003 ATC 451029. Again the expenditure that are related

to such an income would not be permitted as deduction.

b) Any interest that is earned by virtue of a fixed money would be treated as ordinary income

under the fruit and tree concept. According to the principle enumerated in Adelaide Fruit and Produce

Exchange Co Ltd v DFC of T (1932) 2 ATD 130, income earned from exploiting a property by way of rent

would be ordinary income. According to the principle enumerated in Evans v. F.C. of T. 89 ATC 454031,

income from an activity involving gambling if not done in business like manner will not earn assessable

income. Hence, in this case, $500 from bank as an interest is an assessable income, winnings from the

casino will not be included in taxable income and the rent amount into $2000 would be treated as in

assessable income.

c) An amount provided as an allowance to an employee by the employer against the employment

will be assessable for the employee according to the legal principle enumerated in s 15.2 of ITAA 9732.

Hence, in this case the $500 received as allowance will be assessable income.

d) For the income of $ 20,000,

no imposition of Medicare Levy

For the income of $ 24900,

2% Levy amounting to $ 498

For the taxable income $100,000

2% Levy amounting to $ 2000.

e) For income amounting to $ 25,000, tax rate applicable will be 19 percent over $18,200

29 FC of T v La Rosa 2003 ATC 4510

30 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

31 Evans v. F.C. of T. 89 ATC 4540

32 The Income Tax Assessment Act 1997 (Cth), s 15.2

be illustrated with the case of FC of T v La Rosa 2003 ATC 451029. Again the expenditure that are related

to such an income would not be permitted as deduction.

b) Any interest that is earned by virtue of a fixed money would be treated as ordinary income

under the fruit and tree concept. According to the principle enumerated in Adelaide Fruit and Produce

Exchange Co Ltd v DFC of T (1932) 2 ATD 130, income earned from exploiting a property by way of rent

would be ordinary income. According to the principle enumerated in Evans v. F.C. of T. 89 ATC 454031,

income from an activity involving gambling if not done in business like manner will not earn assessable

income. Hence, in this case, $500 from bank as an interest is an assessable income, winnings from the

casino will not be included in taxable income and the rent amount into $2000 would be treated as in

assessable income.

c) An amount provided as an allowance to an employee by the employer against the employment

will be assessable for the employee according to the legal principle enumerated in s 15.2 of ITAA 9732.

Hence, in this case the $500 received as allowance will be assessable income.

d) For the income of $ 20,000,

no imposition of Medicare Levy

For the income of $ 24900,

2% Levy amounting to $ 498

For the taxable income $100,000

2% Levy amounting to $ 2000.

e) For income amounting to $ 25,000, tax rate applicable will be 19 percent over $18,200

29 FC of T v La Rosa 2003 ATC 4510

30 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

31 Evans v. F.C. of T. 89 ATC 4540

32 The Income Tax Assessment Act 1997 (Cth), s 15.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

($25000 – $18200) * 19% = $6800 * 19% = $ 1,292

The gross payable tax = $1292.

For income amounting to $ 40,000, tax rate applicable will be 3,572 and 32.5 percent over $

37,000

$3572 + (40000-37000) * 32.5% = $ 3572 + 32.5% * $3000 = ($3572 + $975)

The gross payable tax = $ 4547.

For income amounting to $ 95,000, tax rate applicable will be 20,797 and 37 percent over $

90,000

$ 20,797 + (95,000-90,000)* 37% = $20,797 + 37% * $5000 = ($20,797 + $1850)

The gross payable tax = $ 22647.

($25000 – $18200) * 19% = $6800 * 19% = $ 1,292

The gross payable tax = $1292.

For income amounting to $ 40,000, tax rate applicable will be 3,572 and 32.5 percent over $

37,000

$3572 + (40000-37000) * 32.5% = $ 3572 + 32.5% * $3000 = ($3572 + $975)

The gross payable tax = $ 4547.

For income amounting to $ 95,000, tax rate applicable will be 20,797 and 37 percent over $

90,000

$ 20,797 + (95,000-90,000)* 37% = $20,797 + 37% * $5000 = ($20,797 + $1850)

The gross payable tax = $ 22647.

11TAXATION LAW

Bibliography

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

Evans v. F.C. of T. 89 ATC 4540

F.C. of T. v. Jenkins 82 ATC 4098

FC of T v Applegate 79 ATC 4307

FC of T v La Rosa 2003 ATC 4510

Hayes v FCT (1956) 96 CLR 47

I.R.C. v. Lysaght (1928) A.C.234

Levene v. I.R.C.(1928) A.C.217

Lodge v Federal Commissioner of Taxation [1972] HCA 49

The Income Tax Assessment Act 1936 (Cth)

The Income Tax Assessment Act 1997 (Cth)

The Medicare Levy Act 1986

TR 2019/1

www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

https://www.ato.gov.au/Rates/Individual-income-tax-rates/

Bibliography

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

Evans v. F.C. of T. 89 ATC 4540

F.C. of T. v. Jenkins 82 ATC 4098

FC of T v Applegate 79 ATC 4307

FC of T v La Rosa 2003 ATC 4510

Hayes v FCT (1956) 96 CLR 47

I.R.C. v. Lysaght (1928) A.C.234

Levene v. I.R.C.(1928) A.C.217

Lodge v Federal Commissioner of Taxation [1972] HCA 49

The Income Tax Assessment Act 1936 (Cth)

The Income Tax Assessment Act 1997 (Cth)

The Medicare Levy Act 1986

TR 2019/1

www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

https://www.ato.gov.au/Rates/Individual-income-tax-rates/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.