Holmes Institute Taxation Law Individual Assignment - T3 2019

VerifiedAdded on 2022/08/21

|11

|2750

|11

Homework Assignment

AI Summary

This assignment solution addresses taxation law principles through a case study and problem-solving approach. The first part examines the tax liability of various income receipts, including tips, employment income, gifts, and fringe benefits, referencing relevant legislation and case law such as ITAA 1997 and cases like Calvert v Wainwright and Moorhouse v Dooland. The second part focuses on Capital Gains Tax (CGT), exploring pre-CGT assets, personal use assets, small business CGT concessions, and collectibles. It analyzes scenarios involving the sale of a house, a car, a photography business, furniture, and paintings, applying relevant sections of the ITAA 1997 to determine tax implications and eligibility for concessions. The assignment demonstrates an understanding of Australian income tax, CGT, and their practical application.

Running head: TAXATION LAW

.

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

.

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................8

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Issues:

The case study will be taking into the account the tax liability of numerous receipts

that is received by the taxpayer derived in the course of employment.

Rule:

The taxable income of the taxpayer involves the assessable income following the

deductions. As given in the “sec 6-5 (1)” the assessable earnings includes the income in

agreement with the “ordinary concepts”. The general characteristics of income states that it

must be income and should convertible into money (James, Sawyer and Wallschutzky 2015).

Certain unanticipated or voluntary payment that a taxpayer receives in the form of incidence

of employment it is regarded as ordinary income. As noted in “Calvert v Wainwright

(1947)” tips that is received by the taxi driver taxable as ordinary income under “sec 6-5 (1)

ITA Act 1997”.

Where an employee gets any receipts that is related to employment and from

rendering any personal service then it is subjected to tax for the recipient or may amount to

fringe benefit for the employer. A relation or nexus with the receipts originating from the

taxpayer’s personal service amounts to ordinary income (Dixon and Nassios 2016). Nexus is

commonly established on the items of personal service such as salary and wages. The

taxation commissioner in “Moorhouse v Dooland (1955)” stated that amounts which a

taxpayer gets directly or indirectly from the personal service of taxpayer is regarded as

ordinary earnings.

Gifts that a person gets for their personal qualities cannot be regarded as ordinary

income and it is not included into the taxable income of the receiver (Evans, Minas and Lim

2015). Accordingly in “Scott v FCT (1966)” a solicited gift cannot be viewed as ordinary

Answer to question 1:

Issues:

The case study will be taking into the account the tax liability of numerous receipts

that is received by the taxpayer derived in the course of employment.

Rule:

The taxable income of the taxpayer involves the assessable income following the

deductions. As given in the “sec 6-5 (1)” the assessable earnings includes the income in

agreement with the “ordinary concepts”. The general characteristics of income states that it

must be income and should convertible into money (James, Sawyer and Wallschutzky 2015).

Certain unanticipated or voluntary payment that a taxpayer receives in the form of incidence

of employment it is regarded as ordinary income. As noted in “Calvert v Wainwright

(1947)” tips that is received by the taxi driver taxable as ordinary income under “sec 6-5 (1)

ITA Act 1997”.

Where an employee gets any receipts that is related to employment and from

rendering any personal service then it is subjected to tax for the recipient or may amount to

fringe benefit for the employer. A relation or nexus with the receipts originating from the

taxpayer’s personal service amounts to ordinary income (Dixon and Nassios 2016). Nexus is

commonly established on the items of personal service such as salary and wages. The

taxation commissioner in “Moorhouse v Dooland (1955)” stated that amounts which a

taxpayer gets directly or indirectly from the personal service of taxpayer is regarded as

ordinary earnings.

Gifts that a person gets for their personal qualities cannot be regarded as ordinary

income and it is not included into the taxable income of the receiver (Evans, Minas and Lim

2015). Accordingly in “Scott v FCT (1966)” a solicited gift cannot be viewed as ordinary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

income only for the reason that it was prompted by appreciation for certain services, since

other factors should also be considered.

As stated under “sec 136 (1) FBTAA” a fringe benefit is viewed as benefit that is

given to an employee by an employer during any time or in relation to the tax year. Fringe

benefits normally includes any type of rights, interest in the real or personal property,

privilege services or facilities. The benefits commonly involves the non-salary benefits given

in relation to employment of employee. Under the “sec 66 (1)” the FBT is to be paid by

employer based on the grossed up assessable value of benefit (Kudrna 2015). The relation

among the employment and the benefit might be either direct or indirect. The law court in

“FCT v J&G Knowles (2000)” explained that there should be a reasonable and discernable

and rational connection amongst the benefit and the service.

Cash gifts that is received by a person is not held as ordinary income rather it amounts

to capital receipts. As noted in “Hayes v FCT (1956)” whether there is any kind of personal

relationship amongst the donor and the recipient, the presence of any pre-existing personal

relation would result the voluntary payment to be less likely an ordinary earnings (Graetz and

Warren 2016). Commonly, money given as gift from a member of family due to personal

reason and the gift is not related to any income generating activity then such amount is not

assessable and not needed to be reported in the tax return.

Application:

The case study provides that Emmi is studying accounting and works in part-time

basis in Crown Melbourne Restaurant. She reports the receipts of tips that amounted to $335

from her customers. The tips received by Emmi amounts to unanticipated or voluntary

payment that received in the form of “incidence of employment”. Citing “Calvert v

income only for the reason that it was prompted by appreciation for certain services, since

other factors should also be considered.

As stated under “sec 136 (1) FBTAA” a fringe benefit is viewed as benefit that is

given to an employee by an employer during any time or in relation to the tax year. Fringe

benefits normally includes any type of rights, interest in the real or personal property,

privilege services or facilities. The benefits commonly involves the non-salary benefits given

in relation to employment of employee. Under the “sec 66 (1)” the FBT is to be paid by

employer based on the grossed up assessable value of benefit (Kudrna 2015). The relation

among the employment and the benefit might be either direct or indirect. The law court in

“FCT v J&G Knowles (2000)” explained that there should be a reasonable and discernable

and rational connection amongst the benefit and the service.

Cash gifts that is received by a person is not held as ordinary income rather it amounts

to capital receipts. As noted in “Hayes v FCT (1956)” whether there is any kind of personal

relationship amongst the donor and the recipient, the presence of any pre-existing personal

relation would result the voluntary payment to be less likely an ordinary earnings (Graetz and

Warren 2016). Commonly, money given as gift from a member of family due to personal

reason and the gift is not related to any income generating activity then such amount is not

assessable and not needed to be reported in the tax return.

Application:

The case study provides that Emmi is studying accounting and works in part-time

basis in Crown Melbourne Restaurant. She reports the receipts of tips that amounted to $335

from her customers. The tips received by Emmi amounts to unanticipated or voluntary

payment that received in the form of “incidence of employment”. Citing “Calvert v

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Wainwright (1947)” it is regarded as ordinary income “sec 6-5 (1) ITA Act 1997” because it

holds essential relation with her income producing activity.

Later in the year Emmi also got a payment of $25,000 from her employment in Crown

Melbourne restaurant. Referring to “Moorhouse v Dooland (1955)” the receipts of income

for Emmi is related to her employment and from rendering any personal service (Ford and

Dibden 2019). A relation or nexus with the receipts is established with the personal service

and amounts to chargeable ordinary income under “sec 6-5 ITAA 1997”.

During the Christmas time, a customer of Emmi gave her an expensive perfume that

had the value of $250. The perfume that is received by Emmi is for their personal qualities

and cannot be regarded as ordinary income under “sec 6-5 ITA Act 1997”. Referring to

“Scott v FCT (1966)” it is a solicited gift and cannot be viewed as ordinary income only for

the reason that it was prompted by appreciation for Emmi’s services.

The employer of Emmi paid her every month with an entertainment event expenses.

Furthermore, the employer of Emmi also spend $380 on meals that was consumed by her.

Under the “sec 136 (1)”, the food and entertainment event is a non-salary fringe benefits that

is given in relation to employment of Emmi. Referring to “FCT v J&G Knowles (2000)” the

benefit is directly given to her and holds necessary connection with the service. As a result,

under “sec 66 (1)” the employer of Crown Melbourne restaurant is required to pay FBT

based on the grossed up assessable value of benefit.

Finally during the year Emmi received $15,000 as a Christmas gift from her father.

Referring to “Hayes v FCT (1956)” there is a personal relationship between Emmi and

father. Because of the presence of pre-existing personal relation, the voluntary payment is

less likely to be an ordinary earnings (Kenny, Blissenden and Villios 2018). The money was

Wainwright (1947)” it is regarded as ordinary income “sec 6-5 (1) ITA Act 1997” because it

holds essential relation with her income producing activity.

Later in the year Emmi also got a payment of $25,000 from her employment in Crown

Melbourne restaurant. Referring to “Moorhouse v Dooland (1955)” the receipts of income

for Emmi is related to her employment and from rendering any personal service (Ford and

Dibden 2019). A relation or nexus with the receipts is established with the personal service

and amounts to chargeable ordinary income under “sec 6-5 ITAA 1997”.

During the Christmas time, a customer of Emmi gave her an expensive perfume that

had the value of $250. The perfume that is received by Emmi is for their personal qualities

and cannot be regarded as ordinary income under “sec 6-5 ITA Act 1997”. Referring to

“Scott v FCT (1966)” it is a solicited gift and cannot be viewed as ordinary income only for

the reason that it was prompted by appreciation for Emmi’s services.

The employer of Emmi paid her every month with an entertainment event expenses.

Furthermore, the employer of Emmi also spend $380 on meals that was consumed by her.

Under the “sec 136 (1)”, the food and entertainment event is a non-salary fringe benefits that

is given in relation to employment of Emmi. Referring to “FCT v J&G Knowles (2000)” the

benefit is directly given to her and holds necessary connection with the service. As a result,

under “sec 66 (1)” the employer of Crown Melbourne restaurant is required to pay FBT

based on the grossed up assessable value of benefit.

Finally during the year Emmi received $15,000 as a Christmas gift from her father.

Referring to “Hayes v FCT (1956)” there is a personal relationship between Emmi and

father. Because of the presence of pre-existing personal relation, the voluntary payment is

less likely to be an ordinary earnings (Kenny, Blissenden and Villios 2018). The money was

5TAXATION LAW

given as a result of personal reason and it is not related to any income generating activity.

The amount is not assessable and Emmi is not needed to report the same in her tax return.

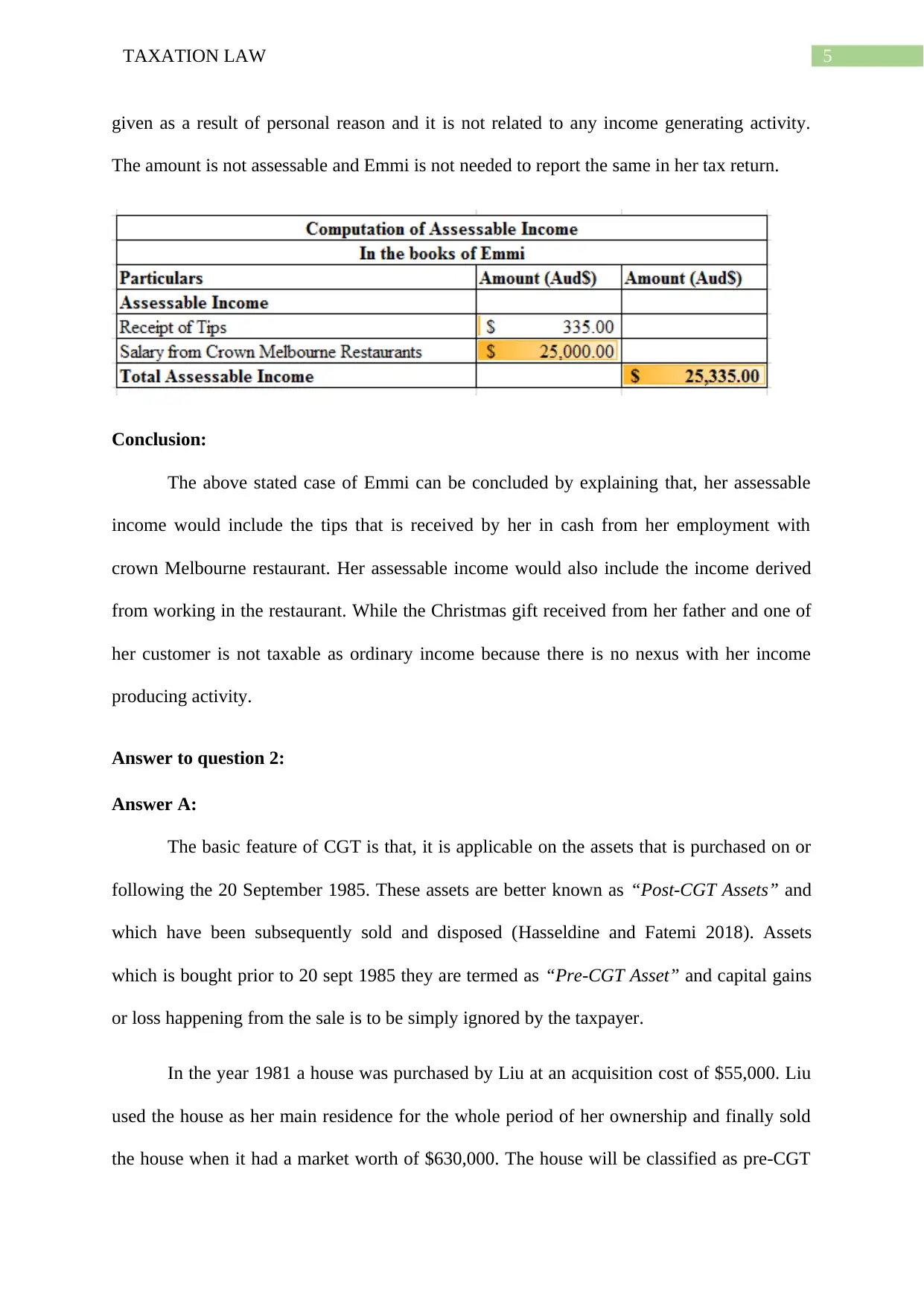

Conclusion:

The above stated case of Emmi can be concluded by explaining that, her assessable

income would include the tips that is received by her in cash from her employment with

crown Melbourne restaurant. Her assessable income would also include the income derived

from working in the restaurant. While the Christmas gift received from her father and one of

her customer is not taxable as ordinary income because there is no nexus with her income

producing activity.

Answer to question 2:

Answer A:

The basic feature of CGT is that, it is applicable on the assets that is purchased on or

following the 20 September 1985. These assets are better known as “Post-CGT Assets” and

which have been subsequently sold and disposed (Hasseldine and Fatemi 2018). Assets

which is bought prior to 20 sept 1985 they are termed as “Pre-CGT Asset” and capital gains

or loss happening from the sale is to be simply ignored by the taxpayer.

In the year 1981 a house was purchased by Liu at an acquisition cost of $55,000. Liu

used the house as her main residence for the whole period of her ownership and finally sold

the house when it had a market worth of $630,000. The house will be classified as pre-CGT

given as a result of personal reason and it is not related to any income generating activity.

The amount is not assessable and Emmi is not needed to report the same in her tax return.

Conclusion:

The above stated case of Emmi can be concluded by explaining that, her assessable

income would include the tips that is received by her in cash from her employment with

crown Melbourne restaurant. Her assessable income would also include the income derived

from working in the restaurant. While the Christmas gift received from her father and one of

her customer is not taxable as ordinary income because there is no nexus with her income

producing activity.

Answer to question 2:

Answer A:

The basic feature of CGT is that, it is applicable on the assets that is purchased on or

following the 20 September 1985. These assets are better known as “Post-CGT Assets” and

which have been subsequently sold and disposed (Hasseldine and Fatemi 2018). Assets

which is bought prior to 20 sept 1985 they are termed as “Pre-CGT Asset” and capital gains

or loss happening from the sale is to be simply ignored by the taxpayer.

In the year 1981 a house was purchased by Liu at an acquisition cost of $55,000. Liu

used the house as her main residence for the whole period of her ownership and finally sold

the house when it had a market worth of $630,000. The house will be classified as pre-CGT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

asset because Liu had purchased in 1981 for a sum of $55,000. Furthermore, the capital gains

which Liu has made upon its disposal will not attract any tax liability.

Answer B:

Accordingly in “sec 108-5 ITAA 1997” the definition of CGT asset include any type

of property or lawful rights which is not a property. The CGT asset of a taxpayer might be

categorized as collectables, personal use asset or other assets. Denoting “sec 108-20 ITAA

1997”, a CGT asset represents the personal use asset (besides collectible) that is used or kept

by taxpayer for their own use (Pert, Chen and Carvosso 2018). The special rules explains

under “sec 118-20 (1)” that capital loss should be ignored by taxpayer.

Accordingly Liu reported disposal of a car that worth $8,000. The car was originally

purchased by Liu for a sum of $37,000. Car must be categorized as personal use asset under

sec 108-20 for the reason that she kept the car for her own use and enjoyment. When the car

was sold a capital loss was suffered by Liu. Referring to the special rules given in the “sec

108-20 (1)”, Liu should ignore the capital loss suffered from selling her car.

Answer C:

According to the “Division 152 ITAA 1997” concessions is given to the small business

from capital gains (Dixon and Nassios 2016). In order to obtain concessions certain basic

conditions needs to be satisfied by the taxpayer of small business. These are;

a. A business should be small in size with the aggregate net worth of assets is not more

than $6 million.

b. The small business has successfully met the criteria that all its CGT assets are active

assets.

On meeting the above given eligibility criteria the small business are provided with

the access four concessions. These are;

asset because Liu had purchased in 1981 for a sum of $55,000. Furthermore, the capital gains

which Liu has made upon its disposal will not attract any tax liability.

Answer B:

Accordingly in “sec 108-5 ITAA 1997” the definition of CGT asset include any type

of property or lawful rights which is not a property. The CGT asset of a taxpayer might be

categorized as collectables, personal use asset or other assets. Denoting “sec 108-20 ITAA

1997”, a CGT asset represents the personal use asset (besides collectible) that is used or kept

by taxpayer for their own use (Pert, Chen and Carvosso 2018). The special rules explains

under “sec 118-20 (1)” that capital loss should be ignored by taxpayer.

Accordingly Liu reported disposal of a car that worth $8,000. The car was originally

purchased by Liu for a sum of $37,000. Car must be categorized as personal use asset under

sec 108-20 for the reason that she kept the car for her own use and enjoyment. When the car

was sold a capital loss was suffered by Liu. Referring to the special rules given in the “sec

108-20 (1)”, Liu should ignore the capital loss suffered from selling her car.

Answer C:

According to the “Division 152 ITAA 1997” concessions is given to the small business

from capital gains (Dixon and Nassios 2016). In order to obtain concessions certain basic

conditions needs to be satisfied by the taxpayer of small business. These are;

a. A business should be small in size with the aggregate net worth of assets is not more

than $6 million.

b. The small business has successfully met the criteria that all its CGT assets are active

assets.

On meeting the above given eligibility criteria the small business are provided with

the access four concessions. These are;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

15-year exemption: The total sum of capital gains made from selling the CGT asset is

exempted given the owner of asset has held for a minimum of 15 years and the age of

taxpayer is 55 years or more.

50% reduction: The taxpayer that simply qualifies for concessions is allowed to lower the

capital gains by 50%, following the general 50% discount percentage.

Retirement concession: Under this concession a taxpayer is given the permission of

disregarding the capital gains following the sale of CGT asset related with the small business

up to a limit of $500,000, given the capital gains proceeds is used for retirement purpose.

Roll-over relief: Under this, the capital gains is deferred where the taxpayer simply

purchases a replacement asset.

As evident in the current situation it is noticed that Liu had a small business of

photography studio. The photography business was sold by Liu and a buyer had took over it

for $125,000. The sale price of photography asset involved $53,000 and goodwill amounted

to $50,000. Liu is eligible for claiming small business CGT concession because the net value

of the asset is within the limit of $6 million. Furthermore, Liu can obtain a 15-year exemption

under “Subdivision 152-B” because she owned the asset for greater than 15 year and also

ages more than 55 years old. As a result, Liu will be granted full exemption from CGT under

the 15-year asset ownership.

Answer D:

There are special rules which is applied on the personal use asset. Under the “sec

108-20 (1)” the capital loss happening from sale of personal use asset must be simply

disregarded by the taxpayer. Evidently in the current situation it is noticed that Liu had

bought a furniture for a sum of $4,800 which was sold for $2,000. The furniture is classified

15-year exemption: The total sum of capital gains made from selling the CGT asset is

exempted given the owner of asset has held for a minimum of 15 years and the age of

taxpayer is 55 years or more.

50% reduction: The taxpayer that simply qualifies for concessions is allowed to lower the

capital gains by 50%, following the general 50% discount percentage.

Retirement concession: Under this concession a taxpayer is given the permission of

disregarding the capital gains following the sale of CGT asset related with the small business

up to a limit of $500,000, given the capital gains proceeds is used for retirement purpose.

Roll-over relief: Under this, the capital gains is deferred where the taxpayer simply

purchases a replacement asset.

As evident in the current situation it is noticed that Liu had a small business of

photography studio. The photography business was sold by Liu and a buyer had took over it

for $125,000. The sale price of photography asset involved $53,000 and goodwill amounted

to $50,000. Liu is eligible for claiming small business CGT concession because the net value

of the asset is within the limit of $6 million. Furthermore, Liu can obtain a 15-year exemption

under “Subdivision 152-B” because she owned the asset for greater than 15 year and also

ages more than 55 years old. As a result, Liu will be granted full exemption from CGT under

the 15-year asset ownership.

Answer D:

There are special rules which is applied on the personal use asset. Under the “sec

108-20 (1)” the capital loss happening from sale of personal use asset must be simply

disregarded by the taxpayer. Evidently in the current situation it is noticed that Liu had

bought a furniture for a sum of $4,800 which was sold for $2,000. The furniture is classified

8TAXATION LAW

as personal use asset under “sec 108-20 ITAA 1997”. Therefore, the capital loss suffered

from selling the furniture should be disregarded by Liu under “sec 118-20 (1)”.

Answer E:

Namely under the “sec 108-10 ITAA 1997” collectible refers to those assets that is

mainly used by tax payer or kept by taxpayer for their private use and enjoyment (Pert, Chen

and Carvosso 2018). The list of asset given in “sec 108-10 (2)” includes antiques, jewellery,

rate stamp, coins, paintings, sculpture etc. Besides this there is also a special rules given for

collectables. Under the “sec 118-10 (1)” capital gains is required to be simply ignored when

the cost of the asset is not more than $500 or less.

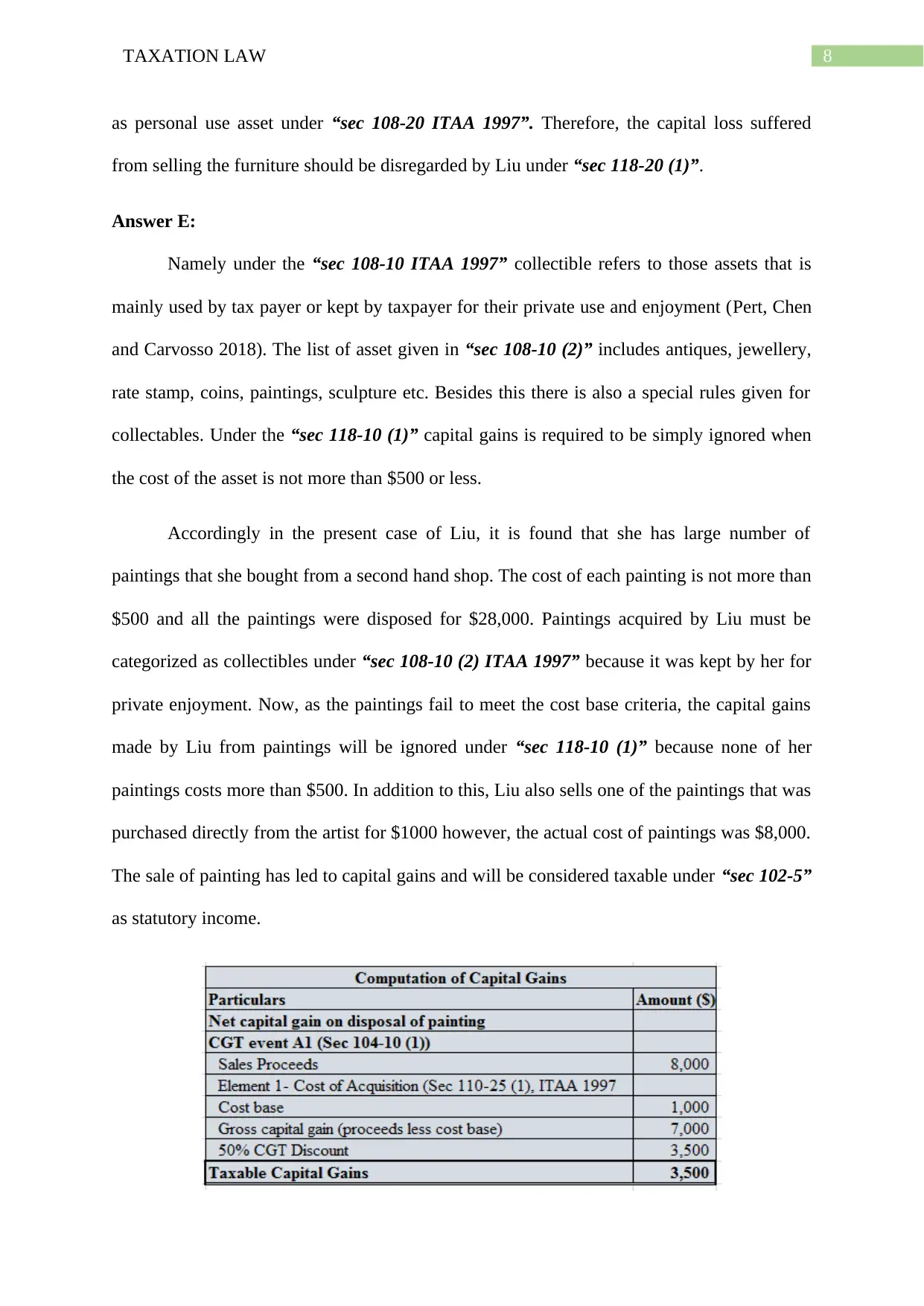

Accordingly in the present case of Liu, it is found that she has large number of

paintings that she bought from a second hand shop. The cost of each painting is not more than

$500 and all the paintings were disposed for $28,000. Paintings acquired by Liu must be

categorized as collectibles under “sec 108-10 (2) ITAA 1997” because it was kept by her for

private enjoyment. Now, as the paintings fail to meet the cost base criteria, the capital gains

made by Liu from paintings will be ignored under “sec 118-10 (1)” because none of her

paintings costs more than $500. In addition to this, Liu also sells one of the paintings that was

purchased directly from the artist for $1000 however, the actual cost of paintings was $8,000.

The sale of painting has led to capital gains and will be considered taxable under “sec 102-5”

as statutory income.

as personal use asset under “sec 108-20 ITAA 1997”. Therefore, the capital loss suffered

from selling the furniture should be disregarded by Liu under “sec 118-20 (1)”.

Answer E:

Namely under the “sec 108-10 ITAA 1997” collectible refers to those assets that is

mainly used by tax payer or kept by taxpayer for their private use and enjoyment (Pert, Chen

and Carvosso 2018). The list of asset given in “sec 108-10 (2)” includes antiques, jewellery,

rate stamp, coins, paintings, sculpture etc. Besides this there is also a special rules given for

collectables. Under the “sec 118-10 (1)” capital gains is required to be simply ignored when

the cost of the asset is not more than $500 or less.

Accordingly in the present case of Liu, it is found that she has large number of

paintings that she bought from a second hand shop. The cost of each painting is not more than

$500 and all the paintings were disposed for $28,000. Paintings acquired by Liu must be

categorized as collectibles under “sec 108-10 (2) ITAA 1997” because it was kept by her for

private enjoyment. Now, as the paintings fail to meet the cost base criteria, the capital gains

made by Liu from paintings will be ignored under “sec 118-10 (1)” because none of her

paintings costs more than $500. In addition to this, Liu also sells one of the paintings that was

purchased directly from the artist for $1000 however, the actual cost of paintings was $8,000.

The sale of painting has led to capital gains and will be considered taxable under “sec 102-5”

as statutory income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Ford, S. and Dibden, A., 2019. Gifted assets, valuation and ordinary income. Taxation in

Australia, 53(10), p.560.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, pp.16-36.

Hasseldine, J. and Fatemi, D., 2018. Tax practitioner judgements and client advocacy: the

blurred boundary between capital gains vs. ordinary income. eJTR, 16, p.303.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives

in Australia, New Zealand and the United Kingdom. eJTR, 13, p.280.

Kenny, P., Blissenden, M. and Villios, S., 2018. Australian Tax 2018.

Kudrna, G., 2015. Means Testing of Public Pensions: The Case of Australia. Michigan

Retirement Research Center Research Paper, (2016-338).

Pert, A., Chen, H. and Carvosso, R., 2018. 'Tech Mahindra Ltd v Federal Commissioner of

Taxation'(2016) 250 FCR 287. Australian Year Book of International Law, 35, p.276.

References:

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Ford, S. and Dibden, A., 2019. Gifted assets, valuation and ordinary income. Taxation in

Australia, 53(10), p.560.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, pp.16-36.

Hasseldine, J. and Fatemi, D., 2018. Tax practitioner judgements and client advocacy: the

blurred boundary between capital gains vs. ordinary income. eJTR, 16, p.303.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives

in Australia, New Zealand and the United Kingdom. eJTR, 13, p.280.

Kenny, P., Blissenden, M. and Villios, S., 2018. Australian Tax 2018.

Kudrna, G., 2015. Means Testing of Public Pensions: The Case of Australia. Michigan

Retirement Research Center Research Paper, (2016-338).

Pert, A., Chen, H. and Carvosso, R., 2018. 'Tech Mahindra Ltd v Federal Commissioner of

Taxation'(2016) 250 FCR 287. Australian Year Book of International Law, 35, p.276.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.