LAW5230 Taxation Law Assignment - Semester 2, University Name

VerifiedAdded on 2023/06/09

|21

|5728

|387

Homework Assignment

AI Summary

This assignment solution addresses a taxation law problem involving Anna's jewelry business, focusing on determining allowable income tax deductions for the financial year 2018. Part A analyzes various expenses, including bank interest, rent, legal fees, and travel costs, to ascertain their deductibility under section 8-1 of the ITAA 1997. It also covers the purchase of assets like laptops and trading stock, and assesses the impact of private use. Part B explores the small business CGT concession in Australia, its objectives, and critical evaluations of the scheme. It examines the criteria for eligibility, the benefits of the concession, and the challenges faced by small businesses in applying it. The solution also includes a discussion of overall policy objectives, potential reforms, and amendments to the CGT concessions, providing a comprehensive understanding of the Australian taxation landscape for small businesses and individuals.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Part A:.......................................................................................................................2

Issue:..........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................3

Conclusion:................................................................................................................................5

Part B: Small Business Concession............................................................................................6

Introduction:...............................................................................................................................6

The small business CGT concession:.........................................................................................7

Overall policy objective under present system of taxation:.......................................................9

Critical evaluation of SBE concession:....................................................................................11

Reformations and further amendments of CGT Concessions:.................................................13

Conclusion:..............................................................................................................................15

References:...............................................................................................................................16

Table of Contents

Answer to Part A:.......................................................................................................................2

Issue:..........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................3

Conclusion:................................................................................................................................5

Part B: Small Business Concession............................................................................................6

Introduction:...............................................................................................................................6

The small business CGT concession:.........................................................................................7

Overall policy objective under present system of taxation:.......................................................9

Critical evaluation of SBE concession:....................................................................................11

Reformations and further amendments of CGT Concessions:.................................................13

Conclusion:..............................................................................................................................15

References:...............................................................................................................................16

2TAXATION LAW

Answer to Part A:

Issue:

The issue involved in the current case of Anna is based on determining the income tax

consequences for the financial year ended 2018. The issue surrounding the case is whether

the taxpayer qualifies for claiming an allowable deduction under “section 8-1 of the ITAA

1997”?

Rule:

The main provision of the “section 8-1” a taxpayer can claim deductions relating to

the expenditure which is under the provision of general deduction. An expense or loss might

be considered as deductible under “section 8-1” and under the specific provision (Barkoczy

2014). A taxpayer is allowed to claim deductions from their taxable earnings only to the

extent that the expenses are incurred in producing the taxable income. An individual is not

allowed to claim deductions under the negative limbs of “section 8-1 (2) of the ITAA 1997”.

Expenses of capital, private or domestic in nature is not allowed for permissible deductions.

If a person takes loan for the purchase of the equipment and stock is allowed for

deductions under the positive limbs of “section 8-1 of the ITAA 1997” (Grange, Jover-

Ledesma and Maydew 2014). This is because the expenses are incurred in producing the

assessable income or in carrying on of the business with the objective of producing taxable

income.

The taxation commissioner in “Lunney v FCT” held that necessary character of

outgoings that are prerequisite in deriving taxable income should be considered (Jover-

Ledesma 2014). A taxpayer is not allowed to claim deductions under the general provision of

“section 8-1 of the ITAA 1997” relating to the pre-commencement of income generating

Answer to Part A:

Issue:

The issue involved in the current case of Anna is based on determining the income tax

consequences for the financial year ended 2018. The issue surrounding the case is whether

the taxpayer qualifies for claiming an allowable deduction under “section 8-1 of the ITAA

1997”?

Rule:

The main provision of the “section 8-1” a taxpayer can claim deductions relating to

the expenditure which is under the provision of general deduction. An expense or loss might

be considered as deductible under “section 8-1” and under the specific provision (Barkoczy

2014). A taxpayer is allowed to claim deductions from their taxable earnings only to the

extent that the expenses are incurred in producing the taxable income. An individual is not

allowed to claim deductions under the negative limbs of “section 8-1 (2) of the ITAA 1997”.

Expenses of capital, private or domestic in nature is not allowed for permissible deductions.

If a person takes loan for the purchase of the equipment and stock is allowed for

deductions under the positive limbs of “section 8-1 of the ITAA 1997” (Grange, Jover-

Ledesma and Maydew 2014). This is because the expenses are incurred in producing the

assessable income or in carrying on of the business with the objective of producing taxable

income.

The taxation commissioner in “Lunney v FCT” held that necessary character of

outgoings that are prerequisite in deriving taxable income should be considered (Jover-

Ledesma 2014). A taxpayer is not allowed to claim deductions under the general provision of

“section 8-1 of the ITAA 1997” relating to the pre-commencement of income generating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

activity. As held in “Softwood Pulp and Paper v FCT” the commissioner denied deductions

to the taxpayer for cost incurred in establishing the business since it was not incurred in the

course of income producing activity. If a taxpayer purchases any tools, equipment or any

other assets that assist them in deriving income then a deduction can be claimed in this regard

for the entire or part of the cost depending upon the business and private use of the asset.

An individual can claim for the deductions when they incur while travelling for the

business or paying for the employee travel expenses. As explained under “section 25-100 of

the ITAA 1997” expenses relating to travel can be claimed by the taxpayer if the travel is

directly associated between two places where the income generating activities are covered

(Kenny 2013). Generally, a taxpayer can claim deductions for travel that forms the part of

performing the work duties away from the home.

An individual taxpayer is allowed to claim deduction for majority of the expenses that

is incurred in carrying or running the business. The expenses incurred for purchase of

jewellery represents the trading stock expense and same is allowed as deductions (Krever

2013). On the other hand, an individual taxpayer is allowed to claim for the salaries and

wages that is paid to the employee or workers. If an individual operates as the sole trader, or

the business owner and not as the employee of the business and therefore the owner of the

business cannot pay salary to themselves. However, on making any form of nominal payment

in the form of salary or wages is generally held as the profit distribution which does not

forms the part of deductions.

Application:

The present situation of Anna provides that she carries on the business of selling

jewellery. Anna incurred the bank interest of $6,000 for the purchase of equipment and stock.

Anna can claim deductions for the purchase of the equipment and stock under the positive

activity. As held in “Softwood Pulp and Paper v FCT” the commissioner denied deductions

to the taxpayer for cost incurred in establishing the business since it was not incurred in the

course of income producing activity. If a taxpayer purchases any tools, equipment or any

other assets that assist them in deriving income then a deduction can be claimed in this regard

for the entire or part of the cost depending upon the business and private use of the asset.

An individual can claim for the deductions when they incur while travelling for the

business or paying for the employee travel expenses. As explained under “section 25-100 of

the ITAA 1997” expenses relating to travel can be claimed by the taxpayer if the travel is

directly associated between two places where the income generating activities are covered

(Kenny 2013). Generally, a taxpayer can claim deductions for travel that forms the part of

performing the work duties away from the home.

An individual taxpayer is allowed to claim deduction for majority of the expenses that

is incurred in carrying or running the business. The expenses incurred for purchase of

jewellery represents the trading stock expense and same is allowed as deductions (Krever

2013). On the other hand, an individual taxpayer is allowed to claim for the salaries and

wages that is paid to the employee or workers. If an individual operates as the sole trader, or

the business owner and not as the employee of the business and therefore the owner of the

business cannot pay salary to themselves. However, on making any form of nominal payment

in the form of salary or wages is generally held as the profit distribution which does not

forms the part of deductions.

Application:

The present situation of Anna provides that she carries on the business of selling

jewellery. Anna incurred the bank interest of $6,000 for the purchase of equipment and stock.

Anna can claim deductions for the purchase of the equipment and stock under the positive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

limbs of “section 8-1 of the ITAA 1997” (Morgan, Mortimer and Pinto 2013). Anna incurred

the expenses in producing the assessable income and in the course of carrying on of the

business with the objective of producing taxable income.

Anna reported an expense of $2,000 for paying monthly rent of the leased small shop.

Citing the case of “Ronpibon Tin NL v FCT (1949)” the monthly rent expenses is allowable

for deductions since it is relevant and incidental in production of assessable income.

The legal fees of $4,400 that is occurred by Anna for obtaining the advice for

establishing the business is a preliminary to the beginning of income generating activity. By

referring to “Softwood Pulp & Paper v FCT” non-deductible under general provision of

“section 8-1” (Sadiq 2014). Anna reports an expenses of $2200 for the purchase of laptop.

She used laptop 10% of the time for personal purpose. Anna can only claim 90% of the

laptop cost for deductions as 10% of the laptop used comprised of personal use.

The expenses of $2,500 incurred for opening party of shop with local celebrities can

be categorized as private or domestic expenditure and non-deductible since the expenses fails

to meet the positive limbs and non-deductible under second negative limb of “section 8-1 (2)

(b)”. A sole trader is allowed to claim deductions relating to the purchase of trading stock

since these expenses forms the part of carrying on of the business in producing the assessable

income (Woellner 2013). Similarly, the cost incurred in surveillance of shop is also

deductible under the positive limbs of “section 8-1” since the costs is necessarily incurred

and relevant in the taxpayer’s income producing activity.

The travelling expenses for travelling with business class that is incurred by Anna for

attending the New York fashion can be classified as the private in nature. Anna will be

denied to claim deductions under “section 8-1” (Hart et al. 2015). Additionally, she incurred

expenses on accommodation and food that was in relation for the business purpose.

limbs of “section 8-1 of the ITAA 1997” (Morgan, Mortimer and Pinto 2013). Anna incurred

the expenses in producing the assessable income and in the course of carrying on of the

business with the objective of producing taxable income.

Anna reported an expense of $2,000 for paying monthly rent of the leased small shop.

Citing the case of “Ronpibon Tin NL v FCT (1949)” the monthly rent expenses is allowable

for deductions since it is relevant and incidental in production of assessable income.

The legal fees of $4,400 that is occurred by Anna for obtaining the advice for

establishing the business is a preliminary to the beginning of income generating activity. By

referring to “Softwood Pulp & Paper v FCT” non-deductible under general provision of

“section 8-1” (Sadiq 2014). Anna reports an expenses of $2200 for the purchase of laptop.

She used laptop 10% of the time for personal purpose. Anna can only claim 90% of the

laptop cost for deductions as 10% of the laptop used comprised of personal use.

The expenses of $2,500 incurred for opening party of shop with local celebrities can

be categorized as private or domestic expenditure and non-deductible since the expenses fails

to meet the positive limbs and non-deductible under second negative limb of “section 8-1 (2)

(b)”. A sole trader is allowed to claim deductions relating to the purchase of trading stock

since these expenses forms the part of carrying on of the business in producing the assessable

income (Woellner 2013). Similarly, the cost incurred in surveillance of shop is also

deductible under the positive limbs of “section 8-1” since the costs is necessarily incurred

and relevant in the taxpayer’s income producing activity.

The travelling expenses for travelling with business class that is incurred by Anna for

attending the New York fashion can be classified as the private in nature. Anna will be

denied to claim deductions under “section 8-1” (Hart et al. 2015). Additionally, she incurred

expenses on accommodation and food that was in relation for the business purpose.

5TAXATION LAW

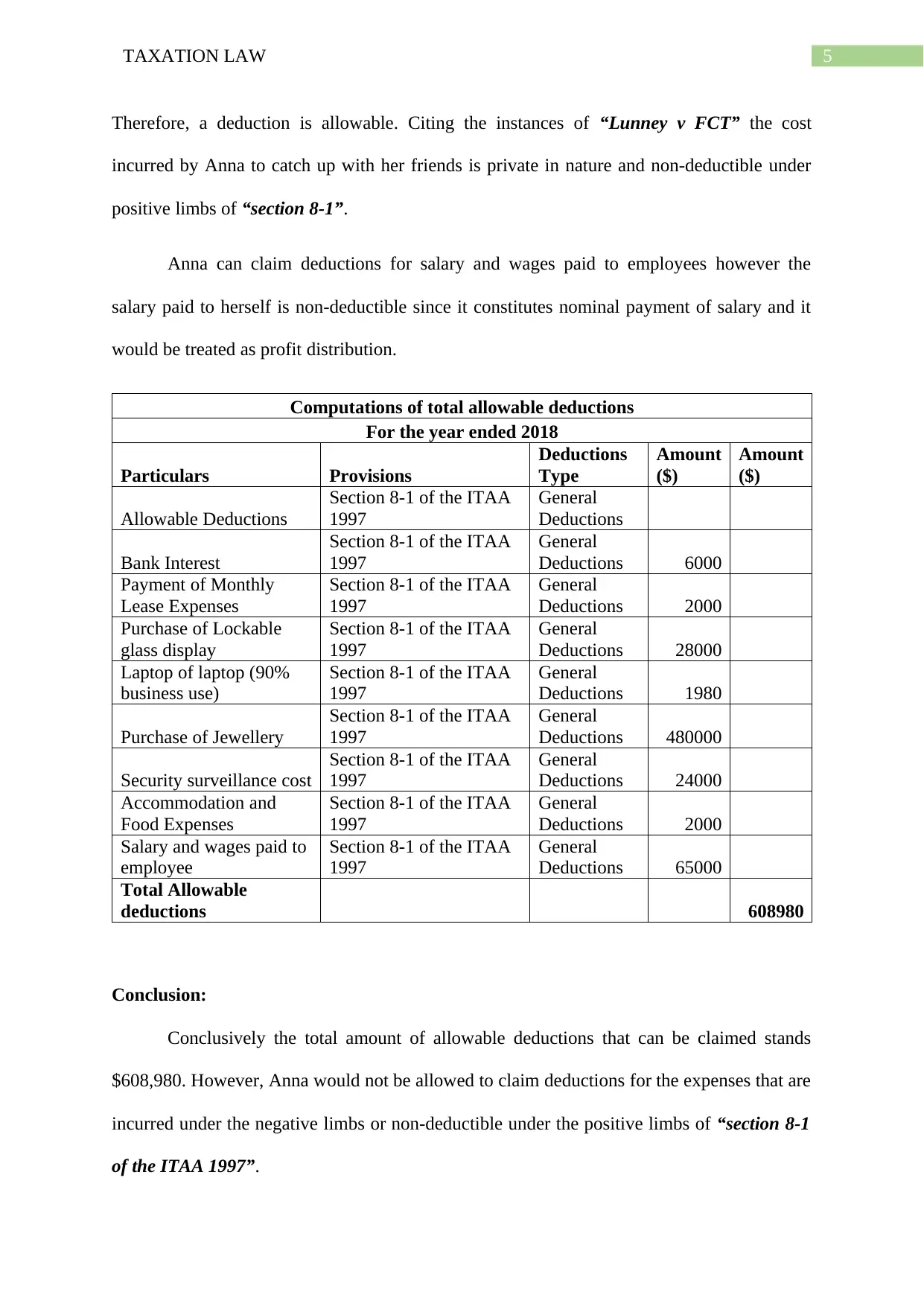

Therefore, a deduction is allowable. Citing the instances of “Lunney v FCT” the cost

incurred by Anna to catch up with her friends is private in nature and non-deductible under

positive limbs of “section 8-1”.

Anna can claim deductions for salary and wages paid to employees however the

salary paid to herself is non-deductible since it constitutes nominal payment of salary and it

would be treated as profit distribution.

Computations of total allowable deductions

For the year ended 2018

Particulars Provisions

Deductions

Type

Amount

($)

Amount

($)

Allowable Deductions

Section 8-1 of the ITAA

1997

General

Deductions

Bank Interest

Section 8-1 of the ITAA

1997

General

Deductions 6000

Payment of Monthly

Lease Expenses

Section 8-1 of the ITAA

1997

General

Deductions 2000

Purchase of Lockable

glass display

Section 8-1 of the ITAA

1997

General

Deductions 28000

Laptop of laptop (90%

business use)

Section 8-1 of the ITAA

1997

General

Deductions 1980

Purchase of Jewellery

Section 8-1 of the ITAA

1997

General

Deductions 480000

Security surveillance cost

Section 8-1 of the ITAA

1997

General

Deductions 24000

Accommodation and

Food Expenses

Section 8-1 of the ITAA

1997

General

Deductions 2000

Salary and wages paid to

employee

Section 8-1 of the ITAA

1997

General

Deductions 65000

Total Allowable

deductions 608980

Conclusion:

Conclusively the total amount of allowable deductions that can be claimed stands

$608,980. However, Anna would not be allowed to claim deductions for the expenses that are

incurred under the negative limbs or non-deductible under the positive limbs of “section 8-1

of the ITAA 1997”.

Therefore, a deduction is allowable. Citing the instances of “Lunney v FCT” the cost

incurred by Anna to catch up with her friends is private in nature and non-deductible under

positive limbs of “section 8-1”.

Anna can claim deductions for salary and wages paid to employees however the

salary paid to herself is non-deductible since it constitutes nominal payment of salary and it

would be treated as profit distribution.

Computations of total allowable deductions

For the year ended 2018

Particulars Provisions

Deductions

Type

Amount

($)

Amount

($)

Allowable Deductions

Section 8-1 of the ITAA

1997

General

Deductions

Bank Interest

Section 8-1 of the ITAA

1997

General

Deductions 6000

Payment of Monthly

Lease Expenses

Section 8-1 of the ITAA

1997

General

Deductions 2000

Purchase of Lockable

glass display

Section 8-1 of the ITAA

1997

General

Deductions 28000

Laptop of laptop (90%

business use)

Section 8-1 of the ITAA

1997

General

Deductions 1980

Purchase of Jewellery

Section 8-1 of the ITAA

1997

General

Deductions 480000

Security surveillance cost

Section 8-1 of the ITAA

1997

General

Deductions 24000

Accommodation and

Food Expenses

Section 8-1 of the ITAA

1997

General

Deductions 2000

Salary and wages paid to

employee

Section 8-1 of the ITAA

1997

General

Deductions 65000

Total Allowable

deductions 608980

Conclusion:

Conclusively the total amount of allowable deductions that can be claimed stands

$608,980. However, Anna would not be allowed to claim deductions for the expenses that are

incurred under the negative limbs or non-deductible under the positive limbs of “section 8-1

of the ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Part B: Small Business Concession

Introduction:

The small business sector of Australia has regularly pursued the challenging

requirements equity, simplicity and efficiency under the income tax regime by especially

placing focus on the concept of simplicity (Sadiq et al. 2014). Over the last decade, numerous

attempts has been made to offer the small business in Australian with simplicity and reduce

burden of tax compliance with the help of simplified system of taxation. Nevertheless, in

spite of making several amendments over the last decade, the simplified tax system has been

widely criticized by the tax practitioners.

The small business forms the significant part of Australian economy. The small

business of Australia is approximately valued at $1.5 trillion. In a report published by

Australian Bureau of Statistics these small business with less than $2 million turnover per

annum makes up around 97% of the business in Australia. The small business is often termed

as the engine for the Australian economy (Coleman et al. 2014). The small business are

particularly unable to attain the economies of large scale benefits from their greater

counterparts. With growing importance of small business, the government has regularly made

an attempt of reducing the tax compliance cost. Eventually, with very low acceptance rate

and widespread criticism, led the modernized and rebadged systems for concessions known

as SBE regime.

According to the board of taxation a well-made tax concessionary regime and

subsidisations is aimed at assisting the small business that are faced with specific challenges.

The small business concession can play a vital role in assisting the small businesses at every

phase of their business lifespan (Lignier and Evans 2013). This ranges from important start

up face to maturity and retirement of business owners. The present literature would outline

Part B: Small Business Concession

Introduction:

The small business sector of Australia has regularly pursued the challenging

requirements equity, simplicity and efficiency under the income tax regime by especially

placing focus on the concept of simplicity (Sadiq et al. 2014). Over the last decade, numerous

attempts has been made to offer the small business in Australian with simplicity and reduce

burden of tax compliance with the help of simplified system of taxation. Nevertheless, in

spite of making several amendments over the last decade, the simplified tax system has been

widely criticized by the tax practitioners.

The small business forms the significant part of Australian economy. The small

business of Australia is approximately valued at $1.5 trillion. In a report published by

Australian Bureau of Statistics these small business with less than $2 million turnover per

annum makes up around 97% of the business in Australia. The small business is often termed

as the engine for the Australian economy (Coleman et al. 2014). The small business are

particularly unable to attain the economies of large scale benefits from their greater

counterparts. With growing importance of small business, the government has regularly made

an attempt of reducing the tax compliance cost. Eventually, with very low acceptance rate

and widespread criticism, led the modernized and rebadged systems for concessions known

as SBE regime.

According to the board of taxation a well-made tax concessionary regime and

subsidisations is aimed at assisting the small business that are faced with specific challenges.

The small business concession can play a vital role in assisting the small businesses at every

phase of their business lifespan (Lignier and Evans 2013). This ranges from important start

up face to maturity and retirement of business owners. The present literature would outline

8TAXATION LAW

the small business CGT concession in Australia and would critically assess the CGT

concession for small business together with the overall objectives of policy. The study would

also assess whether the concessionary regime meets the policy objectives accompanied with

further essential recommendations to the scheme.

The small business CGT concession:

Any small business entity that satisfies the basic criteria that is outlined under the

“section 152 of the ITAA 1997” is entitled to a wide variety of CGT concessions that are

stated under the “subdivision 152Bto 152E”. The vital impact of the concessions provided to

small business includes that the capital gains that originates on making the active asset sale

can be lowered by 50% and 100% (Geljic, Koustas and Burke 2016). Nevertheless, different

from the other five concessions that are available to small business, the taxpayers of small

business entity hardly elects to implement these requirements. Given that a small business

unit fulfils the basic conditions, the entity obtains the CGT relief. As a result of this, the tax

consultants would often use provision of small business CGT concessions that are provided

under the “Division 152 of the ITAA 1997” when the clients of small business makes the sale

of active asset.

By implementing the specific provisions of concessions, the tax consultants are able

to lower tax liability of capital gains originating from the sale of their customer’s business to

$Nil (Tucker 2016). As evident the only chief roles of the tax consultants are to reduce the

taxpayer’s affairs of reduced tax liability however the small business CGT concessions is

regarded as one of the method through which the tax practitioners can significantly obtain the

concession for the small business entity.

According to Sadiq and Marsden (2014) the small business CGT concessions is

regarded as one of most difficult provision under the ITAA. While the taxpayers are eager to

the small business CGT concession in Australia and would critically assess the CGT

concession for small business together with the overall objectives of policy. The study would

also assess whether the concessionary regime meets the policy objectives accompanied with

further essential recommendations to the scheme.

The small business CGT concession:

Any small business entity that satisfies the basic criteria that is outlined under the

“section 152 of the ITAA 1997” is entitled to a wide variety of CGT concessions that are

stated under the “subdivision 152Bto 152E”. The vital impact of the concessions provided to

small business includes that the capital gains that originates on making the active asset sale

can be lowered by 50% and 100% (Geljic, Koustas and Burke 2016). Nevertheless, different

from the other five concessions that are available to small business, the taxpayers of small

business entity hardly elects to implement these requirements. Given that a small business

unit fulfils the basic conditions, the entity obtains the CGT relief. As a result of this, the tax

consultants would often use provision of small business CGT concessions that are provided

under the “Division 152 of the ITAA 1997” when the clients of small business makes the sale

of active asset.

By implementing the specific provisions of concessions, the tax consultants are able

to lower tax liability of capital gains originating from the sale of their customer’s business to

$Nil (Tucker 2016). As evident the only chief roles of the tax consultants are to reduce the

taxpayer’s affairs of reduced tax liability however the small business CGT concessions is

regarded as one of the method through which the tax practitioners can significantly obtain the

concession for the small business entity.

According to Sadiq and Marsden (2014) the small business CGT concessions is

regarded as one of most difficult provision under the ITAA. While the taxpayers are eager to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

implement the small business CGT concessions but some taxpayers have cited that the

provision is not easy to implement and often consumes time to navigate through which

ultimately adds up the tax compliance costs. There were comments that the CGT concessions

is definitely popular method but involves extensive amount of effort. As stated by Yuan

(2017) a business can incur a cost that would range between $5000 and $10,000 for their

company to ascertain whether the business qualifies for the concessions under the small

business CGT regime.

In spite of the difficulty and higher inherent costs related with the use of small

business CGT concessions, taxpayers view the tax concession regime as the highly

appreciated concession. This can be described through the sheer size of tax minimization

benefit which can be obtained through using the small business CGT concession (Evans et al.

2014). Empirical evidences has suggested that the small business concessions stated under

Division 152 is highly complex and eventually results in noteworthy cost of compliance for

the taxpayers. In contrary, the tax consultant’s comments appeared opposite. The tax expert

viewed the CGT concession as the benefit that possibly flow in the direction of the taxpayers

and by implementing this tax concession regime they can outweigh the cost compliance costs.

Existing literature has noticed that the CGT concession for small business disrupts the

principle of simplicity. According to Sanderson (2015) the taxpayers are more often forced to

spend a substantial amount of time in determining whether their business satisfy the basic

conditions and are henceforth entitled to one or more CGT concessions. This kind of

difficulty existent in the eligibility rule leads the client to face increase sum of accounting

fees because of the time that is spend by the tax agent in assessing each concession and

ascertaining which concessions fits well to the business.

implement the small business CGT concessions but some taxpayers have cited that the

provision is not easy to implement and often consumes time to navigate through which

ultimately adds up the tax compliance costs. There were comments that the CGT concessions

is definitely popular method but involves extensive amount of effort. As stated by Yuan

(2017) a business can incur a cost that would range between $5000 and $10,000 for their

company to ascertain whether the business qualifies for the concessions under the small

business CGT regime.

In spite of the difficulty and higher inherent costs related with the use of small

business CGT concessions, taxpayers view the tax concession regime as the highly

appreciated concession. This can be described through the sheer size of tax minimization

benefit which can be obtained through using the small business CGT concession (Evans et al.

2014). Empirical evidences has suggested that the small business concessions stated under

Division 152 is highly complex and eventually results in noteworthy cost of compliance for

the taxpayers. In contrary, the tax consultant’s comments appeared opposite. The tax expert

viewed the CGT concession as the benefit that possibly flow in the direction of the taxpayers

and by implementing this tax concession regime they can outweigh the cost compliance costs.

Existing literature has noticed that the CGT concession for small business disrupts the

principle of simplicity. According to Sanderson (2015) the taxpayers are more often forced to

spend a substantial amount of time in determining whether their business satisfy the basic

conditions and are henceforth entitled to one or more CGT concessions. This kind of

difficulty existent in the eligibility rule leads the client to face increase sum of accounting

fees because of the time that is spend by the tax agent in assessing each concession and

ascertaining which concessions fits well to the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

As a consequence of this, it is probable where the practitioners believe that the

obtainability of the discount is marginal with taxpayers might be advised that the expenses

that are incurred in researching the obtainability of the tax concession and implementing the

same might be very high to justify (Festa 2018). This represents that the inherent cost that are

related with the tax concessions complexity, few eligible business may not be able to use

those regimes of tax concession as they are unable to afford the risk of shouldering the costs

without any benefits related to it. Therefore, the regimes of tax concessions violates the tax

principle of equity. On a conclusive note, the small business CGT concessions is viewed as a

tool of greater benefit however the difficulty in eligibility rules is very restricting and

expensive, perhaps require a direct far-reaching evaluation.

Overall policy objective under present system of taxation:

The tax concessions for the taxpayers of small business forms an important element of

the present system of Australian taxation system. There are numerous policy objectives that

underpins the tax concession (Chung 2016). Certain policies are aimed at reducing the burden

of compliance while other policies are aimed at offering greater tax relief to promote the

access to business success. While other policies are aimed at promoting wider access to

obtain fund for their retirement and with concessions that are created to meet the combination

of the above stated objectives.

The lower company tax rate concession was introduced during 2015-16 to reduce the

rate of company tax to 28.5 for business that have an annual aggregated turnover of lower

than $2 million. In the following year 2015-17 the rate of company tax rate was further

lowered to 27.5% for business that have the annual turnover of lower than $10 million (Hicks

and Tran 2014). Capital gains tax concession is another policy where the owners of the net

assets of not greater than $6 million or yearly sales turnover of lower than $2 million are

eligible for a small business CGT concession on the small business active assets which is

As a consequence of this, it is probable where the practitioners believe that the

obtainability of the discount is marginal with taxpayers might be advised that the expenses

that are incurred in researching the obtainability of the tax concession and implementing the

same might be very high to justify (Festa 2018). This represents that the inherent cost that are

related with the tax concessions complexity, few eligible business may not be able to use

those regimes of tax concession as they are unable to afford the risk of shouldering the costs

without any benefits related to it. Therefore, the regimes of tax concessions violates the tax

principle of equity. On a conclusive note, the small business CGT concessions is viewed as a

tool of greater benefit however the difficulty in eligibility rules is very restricting and

expensive, perhaps require a direct far-reaching evaluation.

Overall policy objective under present system of taxation:

The tax concessions for the taxpayers of small business forms an important element of

the present system of Australian taxation system. There are numerous policy objectives that

underpins the tax concession (Chung 2016). Certain policies are aimed at reducing the burden

of compliance while other policies are aimed at offering greater tax relief to promote the

access to business success. While other policies are aimed at promoting wider access to

obtain fund for their retirement and with concessions that are created to meet the combination

of the above stated objectives.

The lower company tax rate concession was introduced during 2015-16 to reduce the

rate of company tax to 28.5 for business that have an annual aggregated turnover of lower

than $2 million. In the following year 2015-17 the rate of company tax rate was further

lowered to 27.5% for business that have the annual turnover of lower than $10 million (Hicks

and Tran 2014). Capital gains tax concession is another policy where the owners of the net

assets of not greater than $6 million or yearly sales turnover of lower than $2 million are

eligible for a small business CGT concession on the small business active assets which is

11TAXATION LAW

held constantly for a period of 15 years or where the taxpayers attains the age of 55 and

retires.

The small business CGT concession provide 50% reduction of the capital gains that

originates from the sale of active small business assets together with the general CGT

discount. The policy provides the small business with the exemption till the lifetime cap of

$500,000 on the capital gains originating from the sale of active small business assets and

where the sale proceeds of the assets are used to fund the retirement (Jones 2018). The

current policy provides the small business with the CGT rollover relief for the capital gains

originating upon the sale of the small business active assets given the sales proceeds are

employed in the purchase of active small business assets.

The present policy provides the small business with the instant asset writing off under

the simplified depreciation rules. The small business entities that have the aggregate turnover

of lower than $10 million is able to obtain the access of concessional depreciation

arrangement for its business assets. Under such concessions the business entities are allowed

to immediately claim deductions for those assets that costs lower than the threshold limit

(Somers and Eynaud 2015). Policies such as restructure rollover relief provides the small

business owners of active assets with the CGT and income tax rollover relief relating to

genuine business restructure based on the conditions that the economic ownership of the

assets is unchanged. The rollover is available for the business that have the aggregate

turnover of lower than $10 million.

The present policy objective provides the small business with simplified rules of

trading stock. Small businesses that have the aggregated yearly sales turnover of lower than

$10 million might choose to use the simplified trading stock regimes (Trad and Freudenberg

2018). Under this regimes, the small business can select not to account for the changes in the

held constantly for a period of 15 years or where the taxpayers attains the age of 55 and

retires.

The small business CGT concession provide 50% reduction of the capital gains that

originates from the sale of active small business assets together with the general CGT

discount. The policy provides the small business with the exemption till the lifetime cap of

$500,000 on the capital gains originating from the sale of active small business assets and

where the sale proceeds of the assets are used to fund the retirement (Jones 2018). The

current policy provides the small business with the CGT rollover relief for the capital gains

originating upon the sale of the small business active assets given the sales proceeds are

employed in the purchase of active small business assets.

The present policy provides the small business with the instant asset writing off under

the simplified depreciation rules. The small business entities that have the aggregate turnover

of lower than $10 million is able to obtain the access of concessional depreciation

arrangement for its business assets. Under such concessions the business entities are allowed

to immediately claim deductions for those assets that costs lower than the threshold limit

(Somers and Eynaud 2015). Policies such as restructure rollover relief provides the small

business owners of active assets with the CGT and income tax rollover relief relating to

genuine business restructure based on the conditions that the economic ownership of the

assets is unchanged. The rollover is available for the business that have the aggregate

turnover of lower than $10 million.

The present policy objective provides the small business with simplified rules of

trading stock. Small businesses that have the aggregated yearly sales turnover of lower than

$10 million might choose to use the simplified trading stock regimes (Trad and Freudenberg

2018). Under this regimes, the small business can select not to account for the changes in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.