Taxation Law Assignment: Deductions, GST, and Foreign Tax

VerifiedAdded on 2019/11/26

|13

|3001

|130

Homework Assignment

AI Summary

This assignment solution addresses several key aspects of taxation law. Question 1 explores general deductions under the Income Tax Assessment Act 1997, examining the deductibility of various expenses. Question 2 analyzes a GST case involving Big Bank Limited and its advertising expenditure, applying the IRAC method to determine eligibility for input tax credits. Question 3 focuses on foreign income tax offsets, detailing how to calculate the offset limit for an individual with foreign income. Finally, Question 4 examines the taxation of a partnership firm, outlining the treatment of income, deductions, and capital gains tax for partners. The solution provides detailed calculations, justifications, and references to relevant legislation and case law.

Taxation law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................6

Question 4..................................................................................................................................9

References................................................................................................................................11

Question 1..................................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................6

Question 4..................................................................................................................................9

References................................................................................................................................11

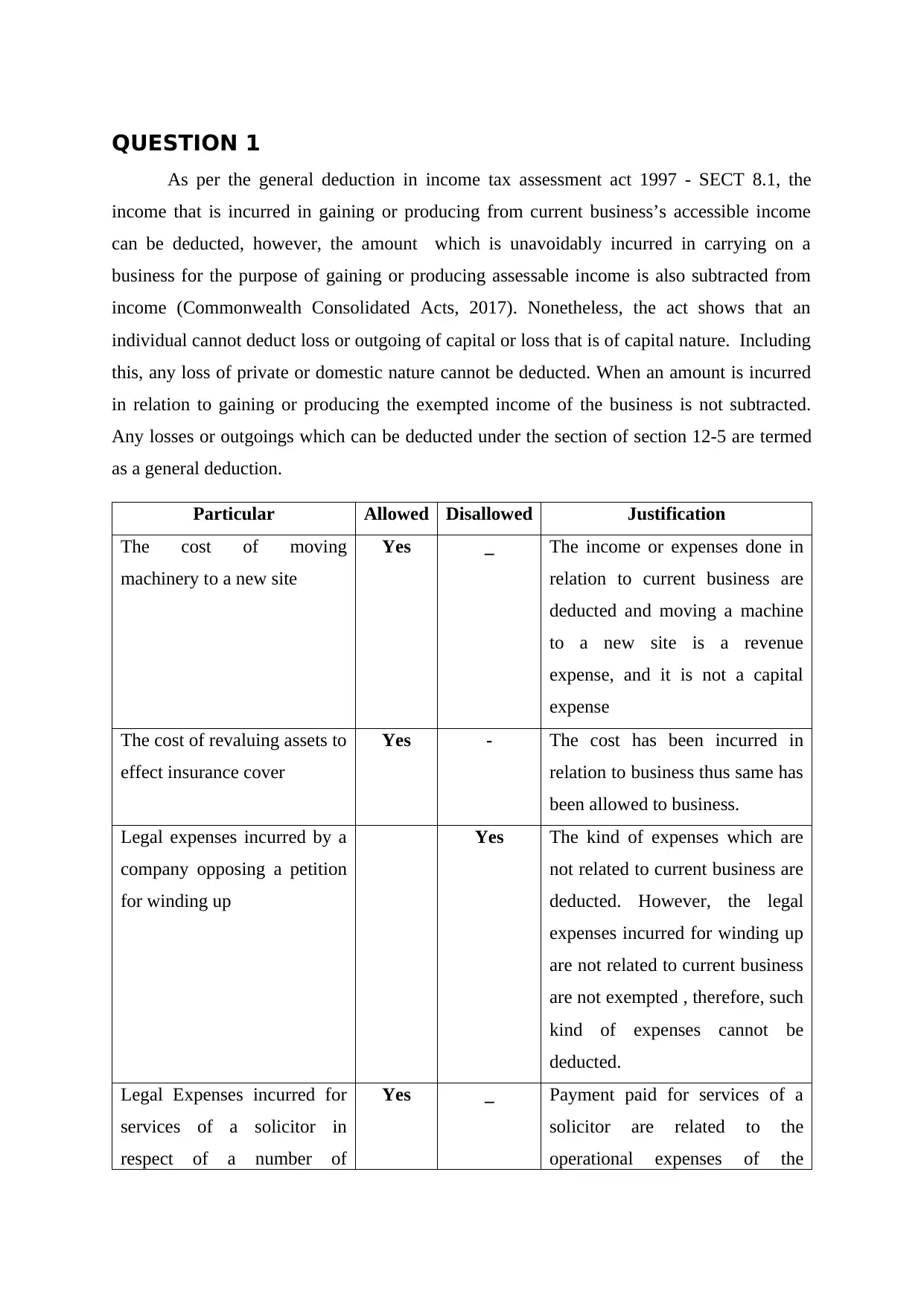

QUESTION 1

As per the general deduction in income tax assessment act 1997 - SECT 8.1, the

income that is incurred in gaining or producing from current business’s accessible income

can be deducted, however, the amount which is unavoidably incurred in carrying on a

business for the purpose of gaining or producing assessable income is also subtracted from

income (Commonwealth Consolidated Acts, 2017). Nonetheless, the act shows that an

individual cannot deduct loss or outgoing of capital or loss that is of capital nature. Including

this, any loss of private or domestic nature cannot be deducted. When an amount is incurred

in relation to gaining or producing the exempted income of the business is not subtracted.

Any losses or outgoings which can be deducted under the section of section 12-5 are termed

as a general deduction.

Particular Allowed Disallowed Justification

The cost of moving

machinery to a new site

Yes _ The income or expenses done in

relation to current business are

deducted and moving a machine

to a new site is a revenue

expense, and it is not a capital

expense

The cost of revaluing assets to

effect insurance cover

Yes - The cost has been incurred in

relation to business thus same has

been allowed to business.

Legal expenses incurred by a

company opposing a petition

for winding up

Yes The kind of expenses which are

not related to current business are

deducted. However, the legal

expenses incurred for winding up

are not related to current business

are not exempted , therefore, such

kind of expenses cannot be

deducted.

Legal Expenses incurred for

services of a solicitor in

respect of a number of

Yes _ Payment paid for services of a

solicitor are related to the

operational expenses of the

As per the general deduction in income tax assessment act 1997 - SECT 8.1, the

income that is incurred in gaining or producing from current business’s accessible income

can be deducted, however, the amount which is unavoidably incurred in carrying on a

business for the purpose of gaining or producing assessable income is also subtracted from

income (Commonwealth Consolidated Acts, 2017). Nonetheless, the act shows that an

individual cannot deduct loss or outgoing of capital or loss that is of capital nature. Including

this, any loss of private or domestic nature cannot be deducted. When an amount is incurred

in relation to gaining or producing the exempted income of the business is not subtracted.

Any losses or outgoings which can be deducted under the section of section 12-5 are termed

as a general deduction.

Particular Allowed Disallowed Justification

The cost of moving

machinery to a new site

Yes _ The income or expenses done in

relation to current business are

deducted and moving a machine

to a new site is a revenue

expense, and it is not a capital

expense

The cost of revaluing assets to

effect insurance cover

Yes - The cost has been incurred in

relation to business thus same has

been allowed to business.

Legal expenses incurred by a

company opposing a petition

for winding up

Yes The kind of expenses which are

not related to current business are

deducted. However, the legal

expenses incurred for winding up

are not related to current business

are not exempted , therefore, such

kind of expenses cannot be

deducted.

Legal Expenses incurred for

services of a solicitor in

respect of a number of

Yes _ Payment paid for services of a

solicitor are related to the

operational expenses of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

matters business, therefore such kinds of

expenses are legal expenses

related to current business. Thus,

can be deducted.

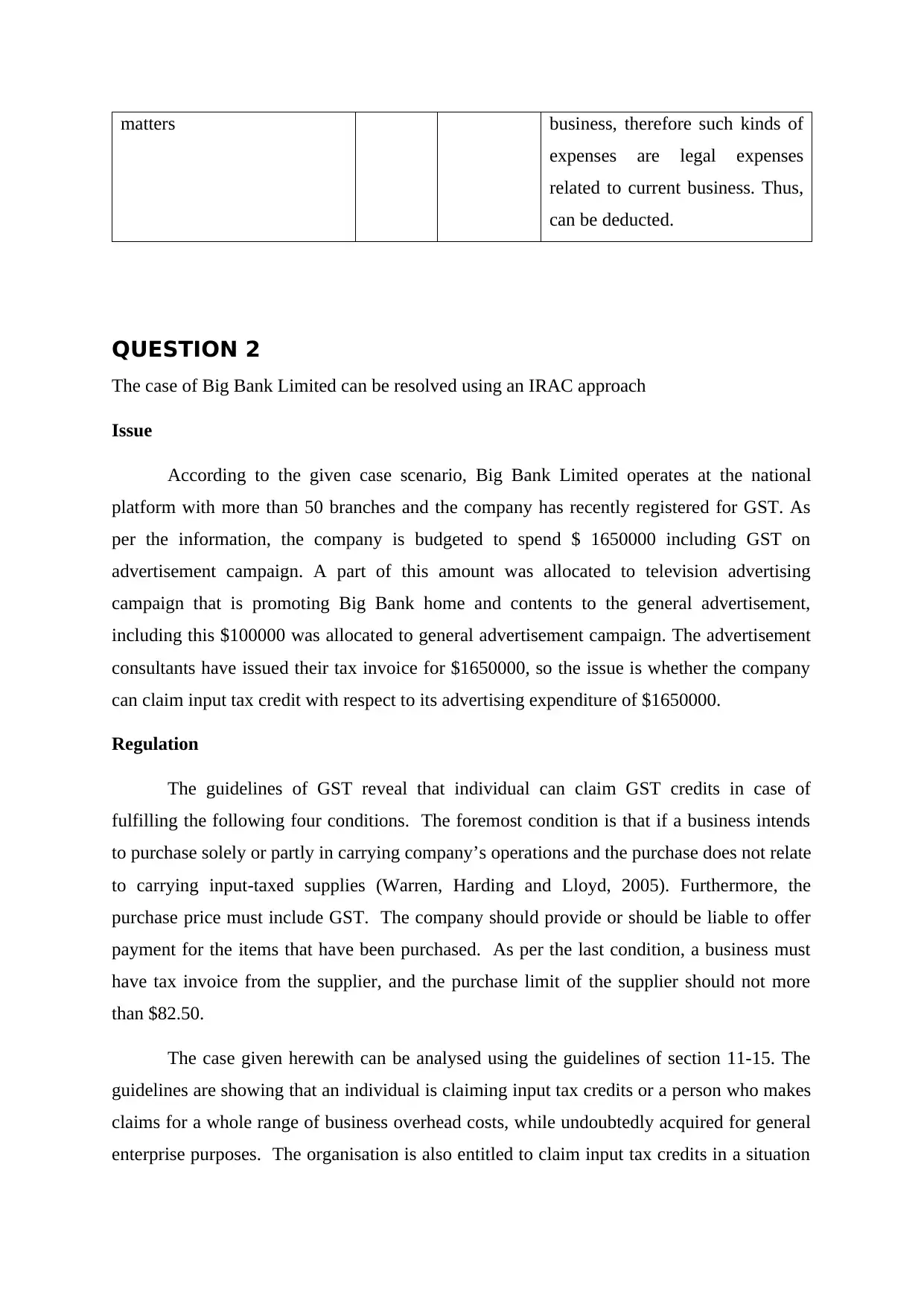

QUESTION 2

The case of Big Bank Limited can be resolved using an IRAC approach

Issue

According to the given case scenario, Big Bank Limited operates at the national

platform with more than 50 branches and the company has recently registered for GST. As

per the information, the company is budgeted to spend $ 1650000 including GST on

advertisement campaign. A part of this amount was allocated to television advertising

campaign that is promoting Big Bank home and contents to the general advertisement,

including this $100000 was allocated to general advertisement campaign. The advertisement

consultants have issued their tax invoice for $1650000, so the issue is whether the company

can claim input tax credit with respect to its advertising expenditure of $1650000.

Regulation

The guidelines of GST reveal that individual can claim GST credits in case of

fulfilling the following four conditions. The foremost condition is that if a business intends

to purchase solely or partly in carrying company’s operations and the purchase does not relate

to carrying input-taxed supplies (Warren, Harding and Lloyd, 2005). Furthermore, the

purchase price must include GST. The company should provide or should be liable to offer

payment for the items that have been purchased. As per the last condition, a business must

have tax invoice from the supplier, and the purchase limit of the supplier should not more

than $82.50.

The case given herewith can be analysed using the guidelines of section 11-15. The

guidelines are showing that an individual is claiming input tax credits or a person who makes

claims for a whole range of business overhead costs, while undoubtedly acquired for general

enterprise purposes. The organisation is also entitled to claim input tax credits in a situation

expenses are legal expenses

related to current business. Thus,

can be deducted.

QUESTION 2

The case of Big Bank Limited can be resolved using an IRAC approach

Issue

According to the given case scenario, Big Bank Limited operates at the national

platform with more than 50 branches and the company has recently registered for GST. As

per the information, the company is budgeted to spend $ 1650000 including GST on

advertisement campaign. A part of this amount was allocated to television advertising

campaign that is promoting Big Bank home and contents to the general advertisement,

including this $100000 was allocated to general advertisement campaign. The advertisement

consultants have issued their tax invoice for $1650000, so the issue is whether the company

can claim input tax credit with respect to its advertising expenditure of $1650000.

Regulation

The guidelines of GST reveal that individual can claim GST credits in case of

fulfilling the following four conditions. The foremost condition is that if a business intends

to purchase solely or partly in carrying company’s operations and the purchase does not relate

to carrying input-taxed supplies (Warren, Harding and Lloyd, 2005). Furthermore, the

purchase price must include GST. The company should provide or should be liable to offer

payment for the items that have been purchased. As per the last condition, a business must

have tax invoice from the supplier, and the purchase limit of the supplier should not more

than $82.50.

The case given herewith can be analysed using the guidelines of section 11-15. The

guidelines are showing that an individual is claiming input tax credits or a person who makes

claims for a whole range of business overhead costs, while undoubtedly acquired for general

enterprise purposes. The organisation is also entitled to claim input tax credits in a situation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

where business acquisition can be linked to potentiality, and as opposed to the fact of taxable

supplies (Rametse and Pope, 2002). In such case, credit is available in full, and costs were

natural in connection with the takeover and business assets receipts. .However, such assets

must be subsequently deployed post-takeover then they are fully conjectural.

The similar situation has arisen in the case given in C& E Commrs v/s UBAF Bank

Ltd; however, it has not presented any problem under this statutory test. In such case, UBAF

Bank has acquired 3 leasing companies through initially acquiring share capital then it was

subsequently transferred to the bank’s leasing businesses (Martin, 2001). At the time when

the Bank sought out to deduct upfront the input tax that was charged on it, in the use of some

professional services associated with the acquisitions, then English Customs Department has

denied the claim by wording that the services obtained bore no relation to the taxable leasing

outputs of to UBAF. However, these services were claimed to be related to the acquisition by

UBAF of the shares and businesses of some of the companies. These companies were the part

of the general expansion of UAF's holdings. Nonetheless, some of the credits were allowable,

but most of them were not till the UBAF Bank made taxable supplies. When the case was

transferred to the English Court of Appeal, the authority has rejected the Customs

Department’s position, on the basis of various intermediate steps in the transaction. At the

time when the business was analysed at the ground of commercial, there was little doubt that

the acquisitions could be demonstrated as a link to future taxable outputs by UBAF (Martin,

2001).

Applicability

The above-discussed regulation is applied to the case of Big Bank limited. At the time

when Bank has launched home and contents insurance policies, it was forecasted that home

and contents insurance policies would constitute 2% of entire enterprise and rest 98% of its

enterprise is made up its traditional loans and deposits facilities business. The budgeted

expenditure includes GST as advertising expenditure of $1650000 includes GST;

therefore, it satisfies the guidelines of GST. Both the advertisement expenses are related to

business expenses, in respective of business categorization, thus, conditions are satisfied. As

home and contents insurance policies are expected to 2% of entire enterprise and rest 98% are

related to traditional loans and deposits facilities business. Thus both are considered as

business expenses and company can claim for input tax credit.

Conclusion

supplies (Rametse and Pope, 2002). In such case, credit is available in full, and costs were

natural in connection with the takeover and business assets receipts. .However, such assets

must be subsequently deployed post-takeover then they are fully conjectural.

The similar situation has arisen in the case given in C& E Commrs v/s UBAF Bank

Ltd; however, it has not presented any problem under this statutory test. In such case, UBAF

Bank has acquired 3 leasing companies through initially acquiring share capital then it was

subsequently transferred to the bank’s leasing businesses (Martin, 2001). At the time when

the Bank sought out to deduct upfront the input tax that was charged on it, in the use of some

professional services associated with the acquisitions, then English Customs Department has

denied the claim by wording that the services obtained bore no relation to the taxable leasing

outputs of to UBAF. However, these services were claimed to be related to the acquisition by

UBAF of the shares and businesses of some of the companies. These companies were the part

of the general expansion of UAF's holdings. Nonetheless, some of the credits were allowable,

but most of them were not till the UBAF Bank made taxable supplies. When the case was

transferred to the English Court of Appeal, the authority has rejected the Customs

Department’s position, on the basis of various intermediate steps in the transaction. At the

time when the business was analysed at the ground of commercial, there was little doubt that

the acquisitions could be demonstrated as a link to future taxable outputs by UBAF (Martin,

2001).

Applicability

The above-discussed regulation is applied to the case of Big Bank limited. At the time

when Bank has launched home and contents insurance policies, it was forecasted that home

and contents insurance policies would constitute 2% of entire enterprise and rest 98% of its

enterprise is made up its traditional loans and deposits facilities business. The budgeted

expenditure includes GST as advertising expenditure of $1650000 includes GST;

therefore, it satisfies the guidelines of GST. Both the advertisement expenses are related to

business expenses, in respective of business categorization, thus, conditions are satisfied. As

home and contents insurance policies are expected to 2% of entire enterprise and rest 98% are

related to traditional loans and deposits facilities business. Thus both are considered as

business expenses and company can claim for input tax credit.

Conclusion

Thus, Big Bank is fulfilling all the guidelines given in latest regulation in GST;

therefore, this bank is entitled to input tax credit.

therefore, this bank is entitled to input tax credit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

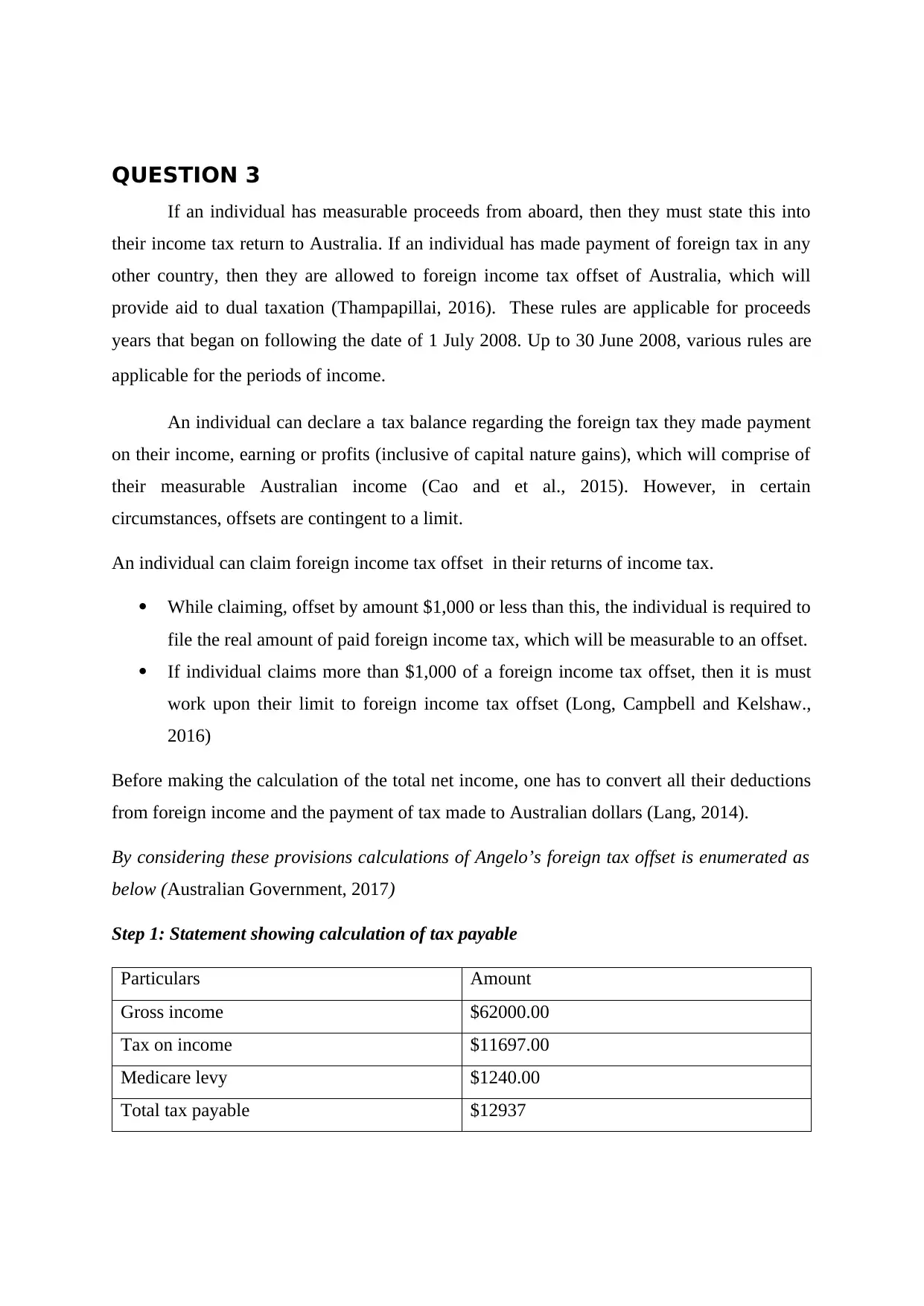

QUESTION 3

If an individual has measurable proceeds from aboard, then they must state this into

their income tax return to Australia. If an individual has made payment of foreign tax in any

other country, then they are allowed to foreign income tax offset of Australia, which will

provide aid to dual taxation (Thampapillai, 2016). These rules are applicable for proceeds

years that began on following the date of 1 July 2008. Up to 30 June 2008, various rules are

applicable for the periods of income.

An individual can declare a tax balance regarding the foreign tax they made payment

on their income, earning or profits (inclusive of capital nature gains), which will comprise of

their measurable Australian income (Cao and et al., 2015). However, in certain

circumstances, offsets are contingent to a limit.

An individual can claim foreign income tax offset in their returns of income tax.

While claiming, offset by amount $1,000 or less than this, the individual is required to

file the real amount of paid foreign income tax, which will be measurable to an offset.

If individual claims more than $1,000 of a foreign income tax offset, then it is must

work upon their limit to foreign income tax offset (Long, Campbell and Kelshaw.,

2016)

Before making the calculation of the total net income, one has to convert all their deductions

from foreign income and the payment of tax made to Australian dollars (Lang, 2014).

By considering these provisions calculations of Angelo’s foreign tax offset is enumerated as

below (Australian Government, 2017)

Step 1: Statement showing calculation of tax payable

Particulars Amount

Gross income $62000.00

Tax on income $11697.00

Medicare levy $1240.00

Total tax payable $12937

If an individual has measurable proceeds from aboard, then they must state this into

their income tax return to Australia. If an individual has made payment of foreign tax in any

other country, then they are allowed to foreign income tax offset of Australia, which will

provide aid to dual taxation (Thampapillai, 2016). These rules are applicable for proceeds

years that began on following the date of 1 July 2008. Up to 30 June 2008, various rules are

applicable for the periods of income.

An individual can declare a tax balance regarding the foreign tax they made payment

on their income, earning or profits (inclusive of capital nature gains), which will comprise of

their measurable Australian income (Cao and et al., 2015). However, in certain

circumstances, offsets are contingent to a limit.

An individual can claim foreign income tax offset in their returns of income tax.

While claiming, offset by amount $1,000 or less than this, the individual is required to

file the real amount of paid foreign income tax, which will be measurable to an offset.

If individual claims more than $1,000 of a foreign income tax offset, then it is must

work upon their limit to foreign income tax offset (Long, Campbell and Kelshaw.,

2016)

Before making the calculation of the total net income, one has to convert all their deductions

from foreign income and the payment of tax made to Australian dollars (Lang, 2014).

By considering these provisions calculations of Angelo’s foreign tax offset is enumerated as

below (Australian Government, 2017)

Step 1: Statement showing calculation of tax payable

Particulars Amount

Gross income $62000.00

Tax on income $11697.00

Medicare levy $1240.00

Total tax payable $12937

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

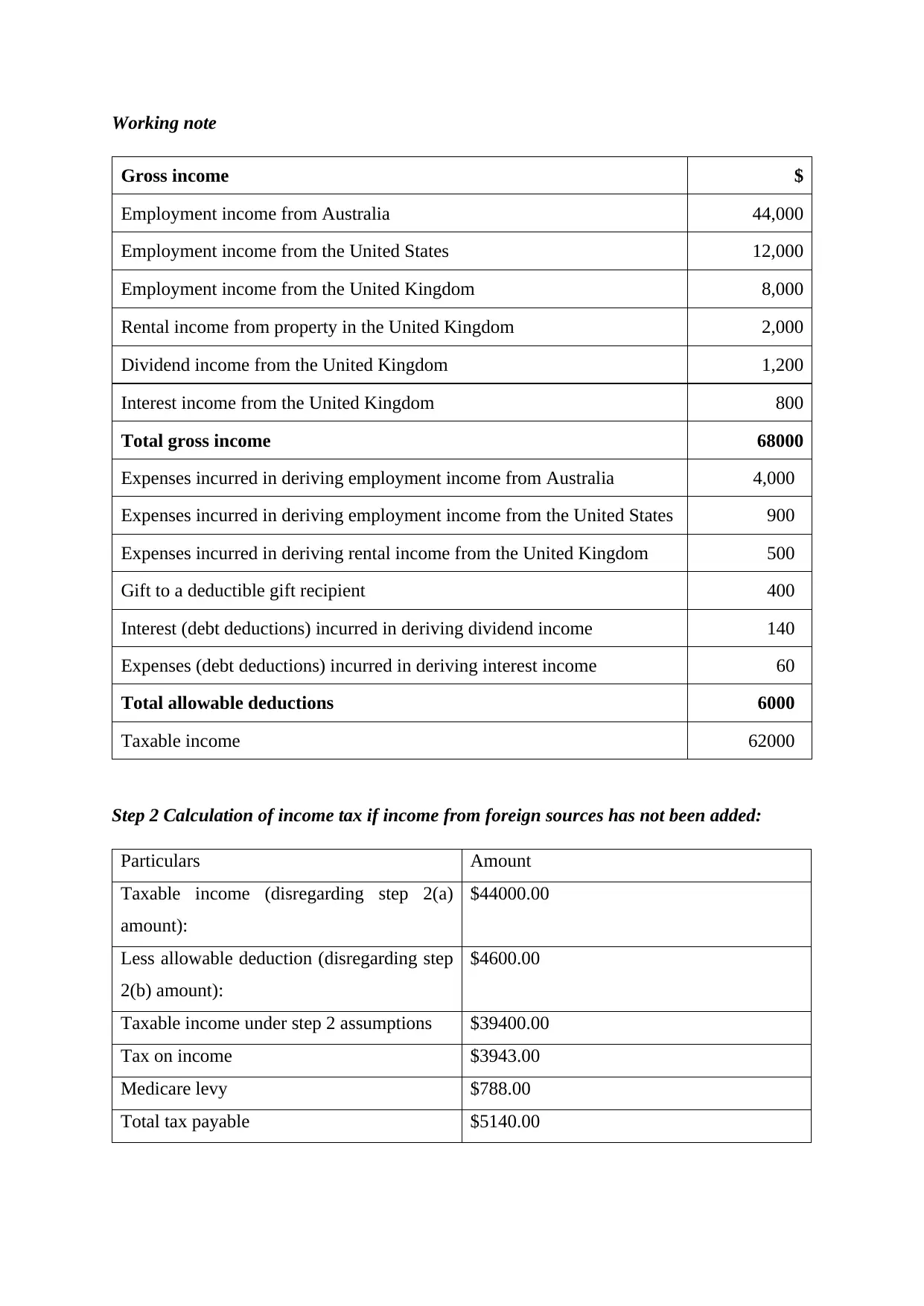

Working note

Gross income $

Employment income from Australia 44,000

Employment income from the United States 12,000

Employment income from the United Kingdom 8,000

Rental income from property in the United Kingdom 2,000

Dividend income from the United Kingdom 1,200

Interest income from the United Kingdom 800

Total gross income 68000

Expenses incurred in deriving employment income from Australia 4,000

Expenses incurred in deriving employment income from the United States 900

Expenses incurred in deriving rental income from the United Kingdom 500

Gift to a deductible gift recipient 400

Interest (debt deductions) incurred in deriving dividend income 140

Expenses (debt deductions) incurred in deriving interest income 60

Total allowable deductions 6000

Taxable income 62000

Step 2 Calculation of income tax if income from foreign sources has not been added:

Particulars Amount

Taxable income (disregarding step 2(a)

amount):

$44000.00

Less allowable deduction (disregarding step

2(b) amount):

$4600.00

Taxable income under step 2 assumptions $39400.00

Tax on income $3943.00

Medicare levy $788.00

Total tax payable $5140.00

Gross income $

Employment income from Australia 44,000

Employment income from the United States 12,000

Employment income from the United Kingdom 8,000

Rental income from property in the United Kingdom 2,000

Dividend income from the United Kingdom 1,200

Interest income from the United Kingdom 800

Total gross income 68000

Expenses incurred in deriving employment income from Australia 4,000

Expenses incurred in deriving employment income from the United States 900

Expenses incurred in deriving rental income from the United Kingdom 500

Gift to a deductible gift recipient 400

Interest (debt deductions) incurred in deriving dividend income 140

Expenses (debt deductions) incurred in deriving interest income 60

Total allowable deductions 6000

Taxable income 62000

Step 2 Calculation of income tax if income from foreign sources has not been added:

Particulars Amount

Taxable income (disregarding step 2(a)

amount):

$44000.00

Less allowable deduction (disregarding step

2(b) amount):

$4600.00

Taxable income under step 2 assumptions $39400.00

Tax on income $3943.00

Medicare levy $788.00

Total tax payable $5140.00

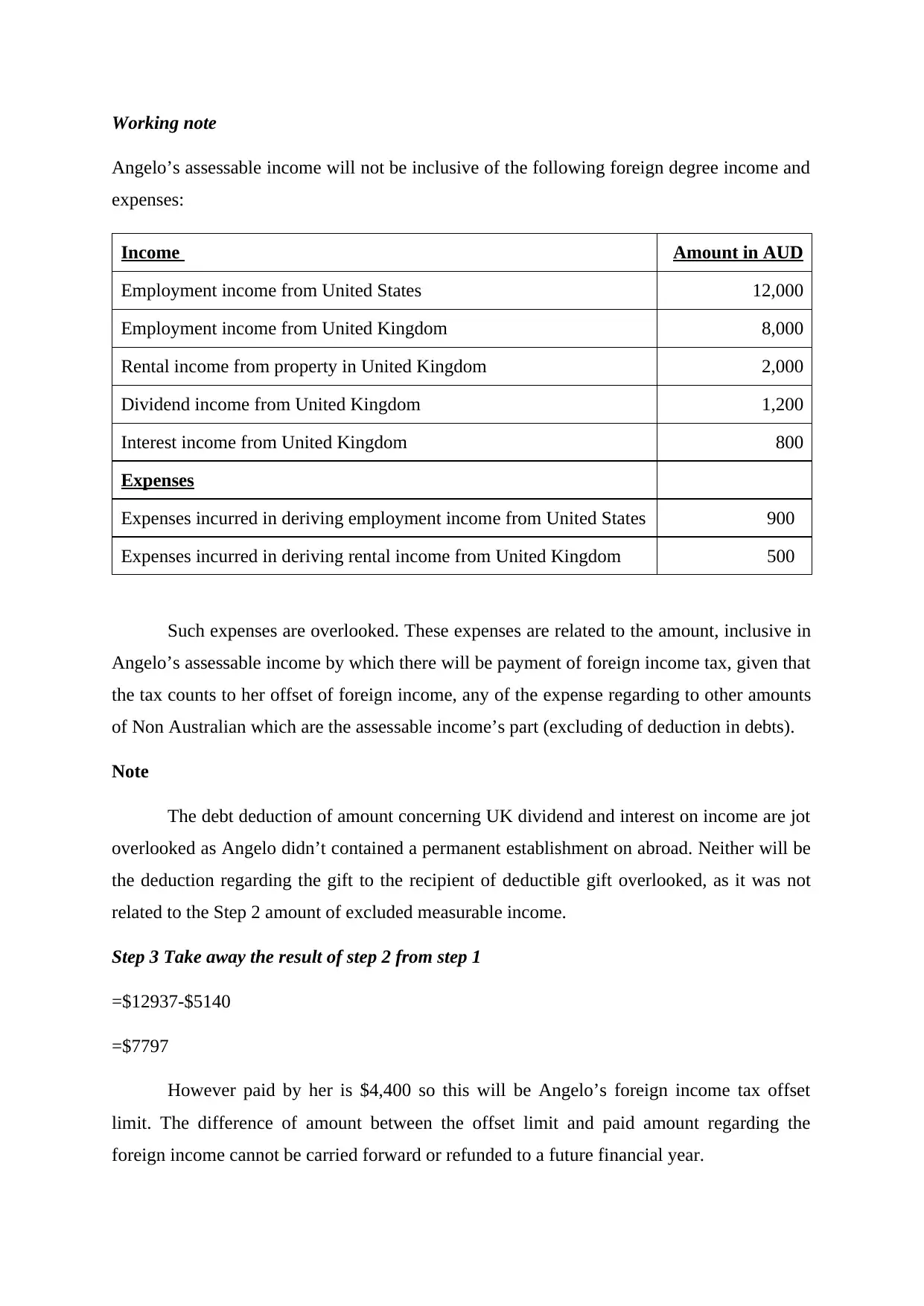

Working note

Angelo’s assessable income will not be inclusive of the following foreign degree income and

expenses:

Income Amount in AUD

Employment income from United States 12,000

Employment income from United Kingdom 8,000

Rental income from property in United Kingdom 2,000

Dividend income from United Kingdom 1,200

Interest income from United Kingdom 800

Expenses

Expenses incurred in deriving employment income from United States 900

Expenses incurred in deriving rental income from United Kingdom 500

Such expenses are overlooked. These expenses are related to the amount, inclusive in

Angelo’s assessable income by which there will be payment of foreign income tax, given that

the tax counts to her offset of foreign income, any of the expense regarding to other amounts

of Non Australian which are the assessable income’s part (excluding of deduction in debts).

Note

The debt deduction of amount concerning UK dividend and interest on income are jot

overlooked as Angelo didn’t contained a permanent establishment on abroad. Neither will be

the deduction regarding the gift to the recipient of deductible gift overlooked, as it was not

related to the Step 2 amount of excluded measurable income.

Step 3 Take away the result of step 2 from step 1

=$12937-$5140

=$7797

However paid by her is $4,400 so this will be Angelo’s foreign income tax offset

limit. The difference of amount between the offset limit and paid amount regarding the

foreign income cannot be carried forward or refunded to a future financial year.

Angelo’s assessable income will not be inclusive of the following foreign degree income and

expenses:

Income Amount in AUD

Employment income from United States 12,000

Employment income from United Kingdom 8,000

Rental income from property in United Kingdom 2,000

Dividend income from United Kingdom 1,200

Interest income from United Kingdom 800

Expenses

Expenses incurred in deriving employment income from United States 900

Expenses incurred in deriving rental income from United Kingdom 500

Such expenses are overlooked. These expenses are related to the amount, inclusive in

Angelo’s assessable income by which there will be payment of foreign income tax, given that

the tax counts to her offset of foreign income, any of the expense regarding to other amounts

of Non Australian which are the assessable income’s part (excluding of deduction in debts).

Note

The debt deduction of amount concerning UK dividend and interest on income are jot

overlooked as Angelo didn’t contained a permanent establishment on abroad. Neither will be

the deduction regarding the gift to the recipient of deductible gift overlooked, as it was not

related to the Step 2 amount of excluded measurable income.

Step 3 Take away the result of step 2 from step 1

=$12937-$5140

=$7797

However paid by her is $4,400 so this will be Angelo’s foreign income tax offset

limit. The difference of amount between the offset limit and paid amount regarding the

foreign income cannot be carried forward or refunded to a future financial year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

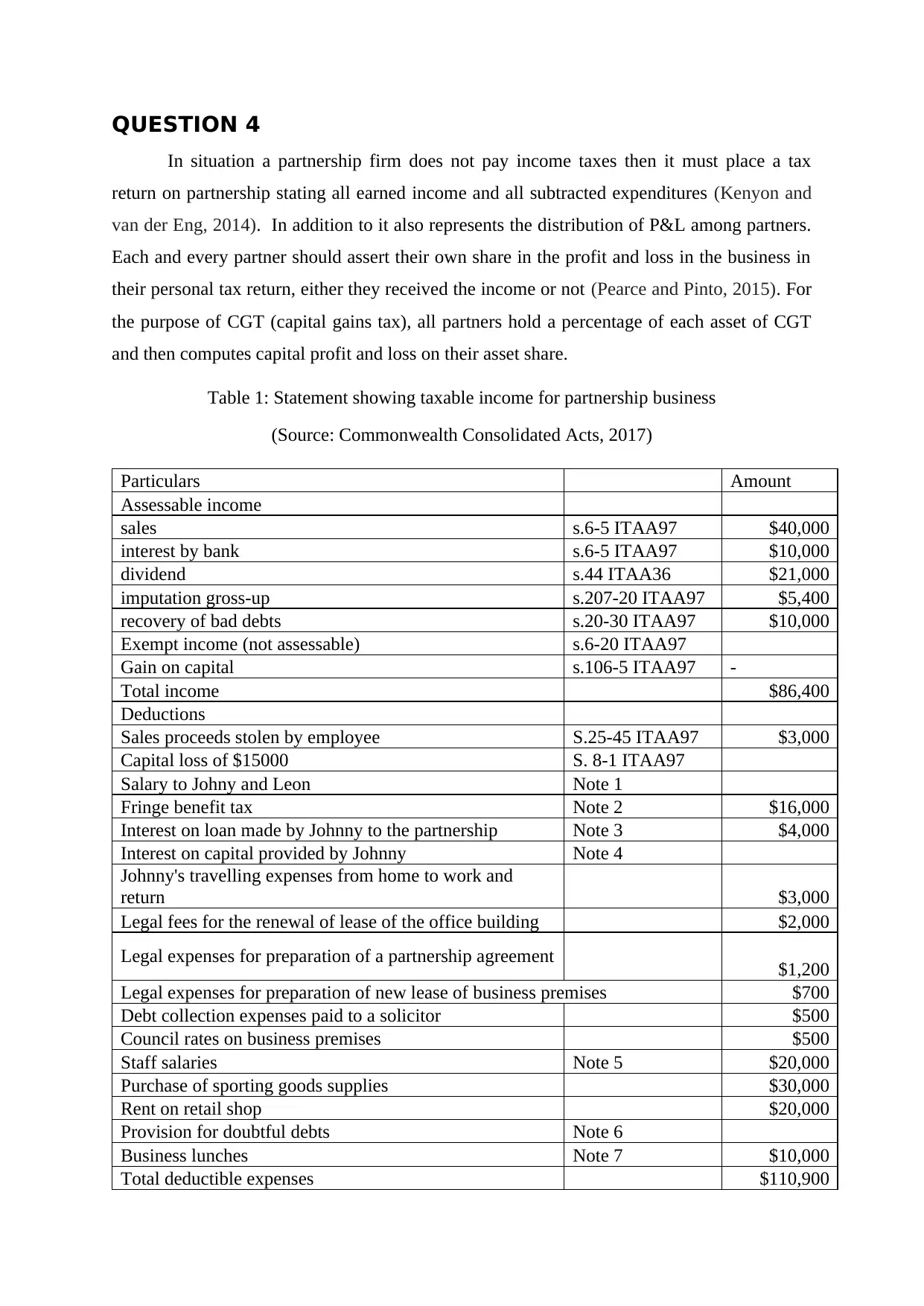

QUESTION 4

In situation a partnership firm does not pay income taxes then it must place a tax

return on partnership stating all earned income and all subtracted expenditures (Kenyon and

van der Eng, 2014). In addition to it also represents the distribution of P&L among partners.

Each and every partner should assert their own share in the profit and loss in the business in

their personal tax return, either they received the income or not (Pearce and Pinto, 2015). For

the purpose of CGT (capital gains tax), all partners hold a percentage of each asset of CGT

and then computes capital profit and loss on their asset share.

Table 1: Statement showing taxable income for partnership business

(Source: Commonwealth Consolidated Acts, 2017)

Particulars Amount

Assessable income

sales s.6-5 ITAA97 $40,000

interest by bank s.6-5 ITAA97 $10,000

dividend s.44 ITAA36 $21,000

imputation gross-up s.207-20 ITAA97 $5,400

recovery of bad debts s.20-30 ITAA97 $10,000

Exempt income (not assessable) s.6-20 ITAA97

Gain on capital s.106-5 ITAA97 -

Total income $86,400

Deductions

Sales proceeds stolen by employee S.25-45 ITAA97 $3,000

Capital loss of $15000 S. 8-1 ITAA97

Salary to Johny and Leon Note 1

Fringe benefit tax Note 2 $16,000

Interest on loan made by Johnny to the partnership Note 3 $4,000

Interest on capital provided by Johnny Note 4

Johnny's travelling expenses from home to work and

return $3,000

Legal fees for the renewal of lease of the office building $2,000

Legal expenses for preparation of a partnership agreement $1,200

Legal expenses for preparation of new lease of business premises $700

Debt collection expenses paid to a solicitor $500

Council rates on business premises $500

Staff salaries Note 5 $20,000

Purchase of sporting goods supplies $30,000

Rent on retail shop $20,000

Provision for doubtful debts Note 6

Business lunches Note 7 $10,000

Total deductible expenses $110,900

In situation a partnership firm does not pay income taxes then it must place a tax

return on partnership stating all earned income and all subtracted expenditures (Kenyon and

van der Eng, 2014). In addition to it also represents the distribution of P&L among partners.

Each and every partner should assert their own share in the profit and loss in the business in

their personal tax return, either they received the income or not (Pearce and Pinto, 2015). For

the purpose of CGT (capital gains tax), all partners hold a percentage of each asset of CGT

and then computes capital profit and loss on their asset share.

Table 1: Statement showing taxable income for partnership business

(Source: Commonwealth Consolidated Acts, 2017)

Particulars Amount

Assessable income

sales s.6-5 ITAA97 $40,000

interest by bank s.6-5 ITAA97 $10,000

dividend s.44 ITAA36 $21,000

imputation gross-up s.207-20 ITAA97 $5,400

recovery of bad debts s.20-30 ITAA97 $10,000

Exempt income (not assessable) s.6-20 ITAA97

Gain on capital s.106-5 ITAA97 -

Total income $86,400

Deductions

Sales proceeds stolen by employee S.25-45 ITAA97 $3,000

Capital loss of $15000 S. 8-1 ITAA97

Salary to Johny and Leon Note 1

Fringe benefit tax Note 2 $16,000

Interest on loan made by Johnny to the partnership Note 3 $4,000

Interest on capital provided by Johnny Note 4

Johnny's travelling expenses from home to work and

return $3,000

Legal fees for the renewal of lease of the office building $2,000

Legal expenses for preparation of a partnership agreement $1,200

Legal expenses for preparation of new lease of business premises $700

Debt collection expenses paid to a solicitor $500

Council rates on business premises $500

Staff salaries Note 5 $20,000

Purchase of sporting goods supplies $30,000

Rent on retail shop $20,000

Provision for doubtful debts Note 6

Business lunches Note 7 $10,000

Total deductible expenses $110,900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

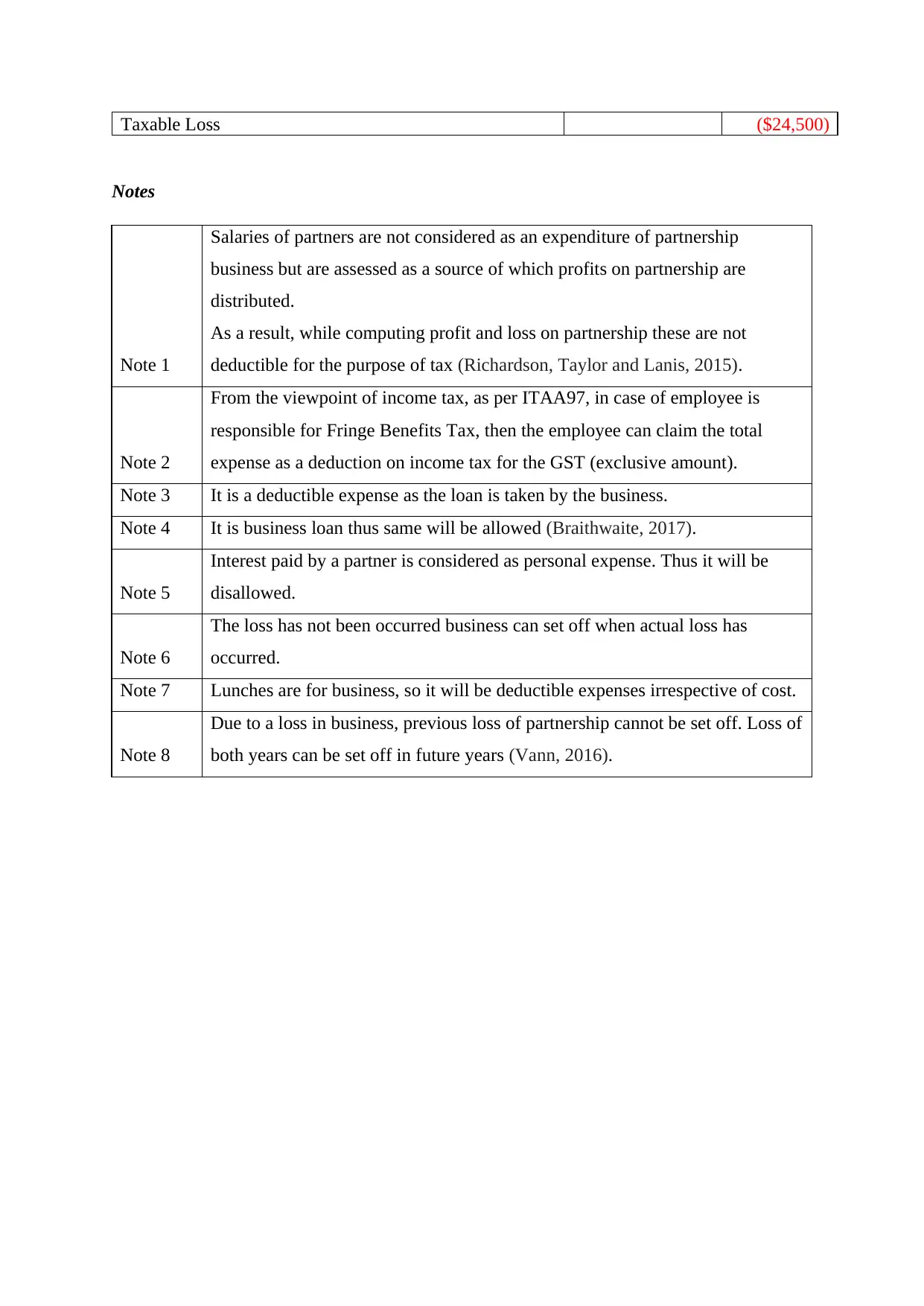

Taxable Loss ($24,500)

Notes

Note 1

Salaries of partners are not considered as an expenditure of partnership

business but are assessed as a source of which profits on partnership are

distributed.

As a result, while computing profit and loss on partnership these are not

deductible for the purpose of tax (Richardson, Taylor and Lanis, 2015).

Note 2

From the viewpoint of income tax, as per ITAA97, in case of employee is

responsible for Fringe Benefits Tax, then the employee can claim the total

expense as a deduction on income tax for the GST (exclusive amount).

Note 3 It is a deductible expense as the loan is taken by the business.

Note 4 It is business loan thus same will be allowed (Braithwaite, 2017).

Note 5

Interest paid by a partner is considered as personal expense. Thus it will be

disallowed.

Note 6

The loss has not been occurred business can set off when actual loss has

occurred.

Note 7 Lunches are for business, so it will be deductible expenses irrespective of cost.

Note 8

Due to a loss in business, previous loss of partnership cannot be set off. Loss of

both years can be set off in future years (Vann, 2016).

Notes

Note 1

Salaries of partners are not considered as an expenditure of partnership

business but are assessed as a source of which profits on partnership are

distributed.

As a result, while computing profit and loss on partnership these are not

deductible for the purpose of tax (Richardson, Taylor and Lanis, 2015).

Note 2

From the viewpoint of income tax, as per ITAA97, in case of employee is

responsible for Fringe Benefits Tax, then the employee can claim the total

expense as a deduction on income tax for the GST (exclusive amount).

Note 3 It is a deductible expense as the loan is taken by the business.

Note 4 It is business loan thus same will be allowed (Braithwaite, 2017).

Note 5

Interest paid by a partner is considered as personal expense. Thus it will be

disallowed.

Note 6

The loss has not been occurred business can set off when actual loss has

occurred.

Note 7 Lunches are for business, so it will be deductible expenses irrespective of cost.

Note 8

Due to a loss in business, previous loss of partnership cannot be set off. Loss of

both years can be set off in future years (Vann, 2016).

REFERENCES

Australian Government, 2017. Goods and services tax (GST). Available at <

https://www.ato.gov.au/Business/Business-activity-statements-(BAS)/Goods-and-services-

tax-(GST)/ > [Accessed from 11th September 2017]

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Commonwealth Consolidated Acts, 2017. INCOME TAX ASSESSMENT ACT 1997 - SECT

8.1 General deductions. Available at <

http://www6.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.1.html>.

[Accessed on 9th September 2017]

Kenyon, D. and van der Eng, P., 2014. 6. Australia and Latin America: Shared experiences

and prospects for a new partnership. Australia and Latin America, p.141.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Martin, D., 2001. Input Tax Credits - The Core Mechanism of GST. Available at <

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2001,_Sound_Education_in_GST,_Input_Tax_Credits___The_Core_Mechanism_of_G

ST.html> [Accessed from 11th September 2017]

Pearce, P. and Pinto, D., 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

Rametse, N. and Pope, J., 2002. Start-up tax compliance costs of the GST: Empirical

evidence from Western Australian small businesses. Austl. Tax F., 17, p.407.

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate

tax avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, pp.44-53.

Australian Government, 2017. Goods and services tax (GST). Available at <

https://www.ato.gov.au/Business/Business-activity-statements-(BAS)/Goods-and-services-

tax-(GST)/ > [Accessed from 11th September 2017]

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Commonwealth Consolidated Acts, 2017. INCOME TAX ASSESSMENT ACT 1997 - SECT

8.1 General deductions. Available at <

http://www6.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.1.html>.

[Accessed on 9th September 2017]

Kenyon, D. and van der Eng, P., 2014. 6. Australia and Latin America: Shared experiences

and prospects for a new partnership. Australia and Latin America, p.141.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Martin, D., 2001. Input Tax Credits - The Core Mechanism of GST. Available at <

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2001,_Sound_Education_in_GST,_Input_Tax_Credits___The_Core_Mechanism_of_G

ST.html> [Accessed from 11th September 2017]

Pearce, P. and Pinto, D., 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

Rametse, N. and Pope, J., 2002. Start-up tax compliance costs of the GST: Empirical

evidence from Western Australian small businesses. Austl. Tax F., 17, p.407.

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate

tax avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, pp.44-53.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.