Taxation Law Assignment - University of Australia, LAWS20060

VerifiedAdded on 2023/01/12

|17

|3984

|52

Homework Assignment

AI Summary

This document presents a detailed solution to a taxation law assignment, addressing various aspects of Australian taxation. The assignment covers several questions, including those related to depreciating assets, tax offsets, assessable income brackets, exemptions for capital gains and losses, CGT events, the formula for income tax calculation, deductibility of legal outlays, average and marginal tax rates, and consumption tax. The answers delve into specific sections of the ITAA 1997, relevant tax rulings, and case laws to provide comprehensive explanations. The assignment also examines scenarios involving deductions for expenses, capital gains tax events, and main residence exemptions, providing calculations and legal analysis. The solution utilizes the AGLC 3rd Edition referencing method, ensuring accurate citations of legislation and case law. This resource is designed to help students understand complex taxation concepts and excel in their coursework.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................4

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer to I:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................7

Answer to D:..........................................................................................................................7

Answer to E:...........................................................................................................................8

Answer to question 3:.................................................................................................................8

Answer to A:..........................................................................................................................8

Answer to B:..........................................................................................................................9

Answer to C:..........................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................4

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer to I:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................7

Answer to D:..........................................................................................................................7

Answer to E:...........................................................................................................................8

Answer to question 3:.................................................................................................................8

Answer to A:..........................................................................................................................8

Answer to B:..........................................................................................................................9

Answer to C:..........................................................................................................................9

2TAXATION LAW

Answer to D:..........................................................................................................................9

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................12

Answer to question 5:...............................................................................................................13

Issues:...................................................................................................................................13

Rule:.....................................................................................................................................13

Applications:........................................................................................................................14

Conclusion............................................................................................................................14

References:...............................................................................................................................15

Answer to D:..........................................................................................................................9

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................12

Answer to question 5:...............................................................................................................13

Issues:...................................................................................................................................13

Rule:.....................................................................................................................................13

Applications:........................................................................................................................14

Conclusion............................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

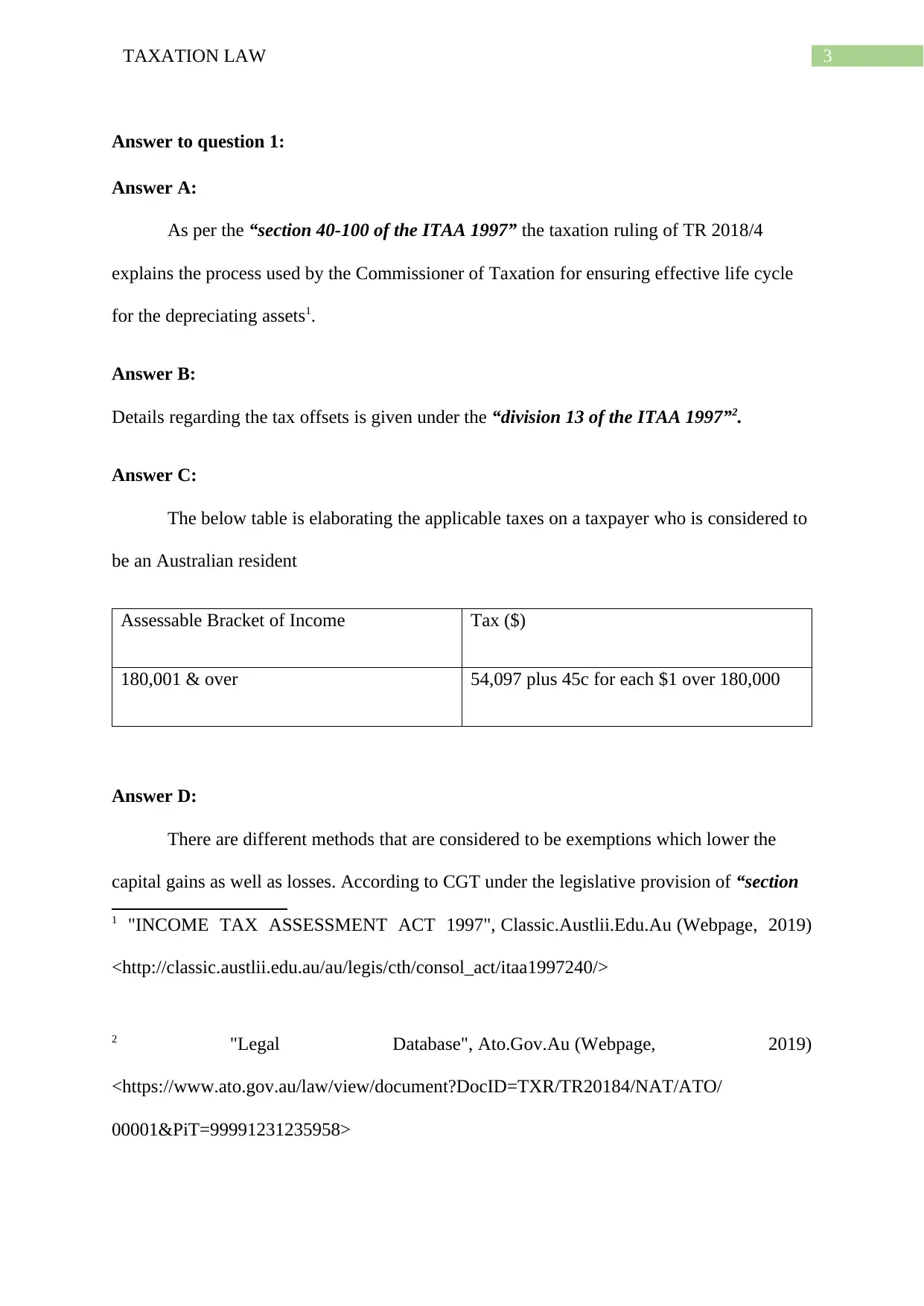

Answer to question 1:

Answer A:

As per the “section 40-100 of the ITAA 1997” the taxation ruling of TR 2018/4

explains the process used by the Commissioner of Taxation for ensuring effective life cycle

for the depreciating assets1.

Answer B:

Details regarding the tax offsets is given under the “division 13 of the ITAA 1997”2.

Answer C:

The below table is elaborating the applicable taxes on a taxpayer who is considered to

be an Australian resident

Assessable Bracket of Income Tax ($)

180,001 & over 54,097 plus 45c for each $1 over 180,000

Answer D:

There are different methods that are considered to be exemptions which lower the

capital gains as well as losses. According to CGT under the legislative provision of “section

1 "INCOME TAX ASSESSMENT ACT 1997", Classic.Austlii.Edu.Au (Webpage, 2019)

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/>

2 "Legal Database", Ato.Gov.Au (Webpage, 2019)

<https://www.ato.gov.au/law/view/document?DocID=TXR/TR20184/NAT/ATO/

00001&PiT=99991231235958>

Answer to question 1:

Answer A:

As per the “section 40-100 of the ITAA 1997” the taxation ruling of TR 2018/4

explains the process used by the Commissioner of Taxation for ensuring effective life cycle

for the depreciating assets1.

Answer B:

Details regarding the tax offsets is given under the “division 13 of the ITAA 1997”2.

Answer C:

The below table is elaborating the applicable taxes on a taxpayer who is considered to

be an Australian resident

Assessable Bracket of Income Tax ($)

180,001 & over 54,097 plus 45c for each $1 over 180,000

Answer D:

There are different methods that are considered to be exemptions which lower the

capital gains as well as losses. According to CGT under the legislative provision of “section

1 "INCOME TAX ASSESSMENT ACT 1997", Classic.Austlii.Edu.Au (Webpage, 2019)

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/>

2 "Legal Database", Ato.Gov.Au (Webpage, 2019)

<https://www.ato.gov.au/law/view/document?DocID=TXR/TR20184/NAT/ATO/

00001&PiT=99991231235958>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

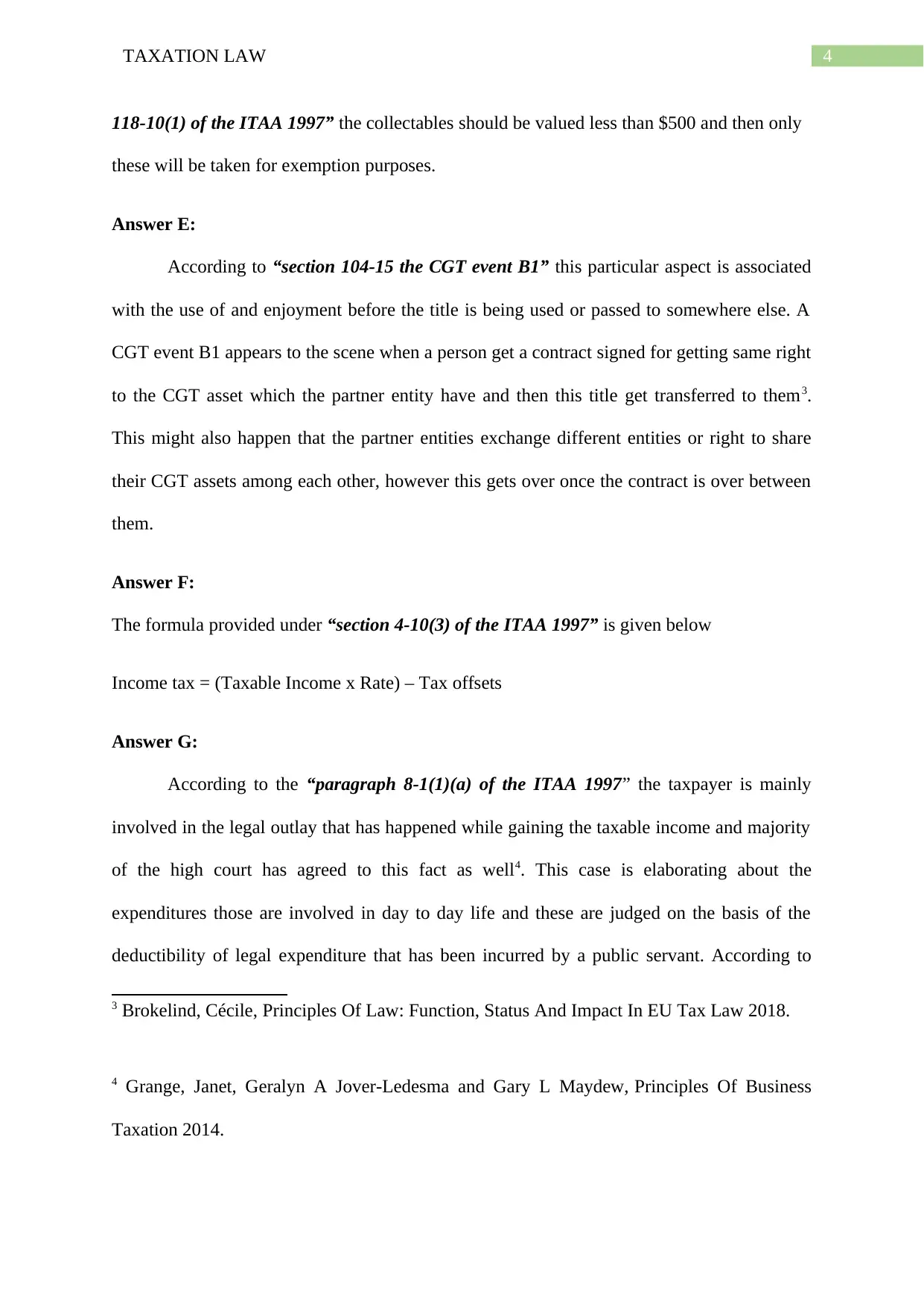

118-10(1) of the ITAA 1997” the collectables should be valued less than $500 and then only

these will be taken for exemption purposes.

Answer E:

According to “section 104-15 the CGT event B1” this particular aspect is associated

with the use of and enjoyment before the title is being used or passed to somewhere else. A

CGT event B1 appears to the scene when a person get a contract signed for getting same right

to the CGT asset which the partner entity have and then this title get transferred to them3.

This might also happen that the partner entities exchange different entities or right to share

their CGT assets among each other, however this gets over once the contract is over between

them.

Answer F:

The formula provided under “section 4-10(3) of the ITAA 1997” is given below

Income tax = (Taxable Income x Rate) – Tax offsets

Answer G:

According to the “paragraph 8-1(1)(a) of the ITAA 1997” the taxpayer is mainly

involved in the legal outlay that has happened while gaining the taxable income and majority

of the high court has agreed to this fact as well4. This case is elaborating about the

expenditures those are involved in day to day life and these are judged on the basis of the

deductibility of legal expenditure that has been incurred by a public servant. According to

3 Brokelind, Cécile, Principles Of Law: Function, Status And Impact In EU Tax Law 2018.

4 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, Principles Of Business

Taxation 2014.

118-10(1) of the ITAA 1997” the collectables should be valued less than $500 and then only

these will be taken for exemption purposes.

Answer E:

According to “section 104-15 the CGT event B1” this particular aspect is associated

with the use of and enjoyment before the title is being used or passed to somewhere else. A

CGT event B1 appears to the scene when a person get a contract signed for getting same right

to the CGT asset which the partner entity have and then this title get transferred to them3.

This might also happen that the partner entities exchange different entities or right to share

their CGT assets among each other, however this gets over once the contract is over between

them.

Answer F:

The formula provided under “section 4-10(3) of the ITAA 1997” is given below

Income tax = (Taxable Income x Rate) – Tax offsets

Answer G:

According to the “paragraph 8-1(1)(a) of the ITAA 1997” the taxpayer is mainly

involved in the legal outlay that has happened while gaining the taxable income and majority

of the high court has agreed to this fact as well4. This case is elaborating about the

expenditures those are involved in day to day life and these are judged on the basis of the

deductibility of legal expenditure that has been incurred by a public servant. According to

3 Brokelind, Cécile, Principles Of Law: Function, Status And Impact In EU Tax Law 2018.

4 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, Principles Of Business

Taxation 2014.

5TAXATION LAW

“section 8-1, ITAA 1997” the taxpayer is supposed to get the deductions for the expenses

occurred in his day to day activities for the income year of 2002. These elaborations

highlighted the defensive program where he was protected for these expenditures under

“section 8-1, ITAA 1997”.

Answer H:

Average tax rate can be defined as the result of the division between total sum of the

tax and total earning. In this case the marginal tax rate can be defined as the incremental tax

calculated for the incremental income5. The average tax rate depicts the household burden of

tax that is impacting the daily life for the taxpayers. In contrary with this elaboration, the

marginal tax rate defines up to which extent the taxpayer’s income can be impacted for this

tax rates in case of their household expenses.

Answer to I:

Consumption tax is defined as the tax which is forced on the expenses those are made

for the good and services required for daily life. The money involved in consumption of these

products are the base for the consumption tax. These consumption taxes are considered as the

value added tax for purchasing these materials.

Answer to question 2:

Answer to A:

As per the Australian taxation office, every taxpayer is allowed for a deduction on

their expenses if they have spent these on gaining the taxable income. Along with this, any

interest on loans are allowed for the deductions6. According to “section 8-1, ITAA 1997” a

5 James, Simon, The Economics Of Taxation 2015.

6 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

“section 8-1, ITAA 1997” the taxpayer is supposed to get the deductions for the expenses

occurred in his day to day activities for the income year of 2002. These elaborations

highlighted the defensive program where he was protected for these expenditures under

“section 8-1, ITAA 1997”.

Answer H:

Average tax rate can be defined as the result of the division between total sum of the

tax and total earning. In this case the marginal tax rate can be defined as the incremental tax

calculated for the incremental income5. The average tax rate depicts the household burden of

tax that is impacting the daily life for the taxpayers. In contrary with this elaboration, the

marginal tax rate defines up to which extent the taxpayer’s income can be impacted for this

tax rates in case of their household expenses.

Answer to I:

Consumption tax is defined as the tax which is forced on the expenses those are made

for the good and services required for daily life. The money involved in consumption of these

products are the base for the consumption tax. These consumption taxes are considered as the

value added tax for purchasing these materials.

Answer to question 2:

Answer to A:

As per the Australian taxation office, every taxpayer is allowed for a deduction on

their expenses if they have spent these on gaining the taxable income. Along with this, any

interest on loans are allowed for the deductions6. According to “section 8-1, ITAA 1997” a

5 James, Simon, The Economics Of Taxation 2015.

6 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

taxpayer can claim these deductions for their expenditures that has occurred for gaining the

taxable income or ordinary income.

This evident can be taken from the Brett’s case that he has interest on his loan as he

had to pay his employees. Now, this interest on the loan has been generated while producing

the taxable income by Brett, hence he is eligible for getting deductions over this interest.

Therefore, according to “section 8-1, ITAA 1997” Brett will be allowed for the deductions

for the interest generated over his loan amount.

Answer to B:

Australian taxation office states that the taxpayers are allowed to claim the deductions

for their expenses which they have incurred while gaining the taxable income. There is also

one condition while claiming for the deductions, if the taxpayer has spent money over their

private and work purposes, then they are only allowed to claim the deductions for the work

purposes.

The consideration of Julie’s case, she has spent $500 for her mobile bills, out of

which 60% was spent for calls related to work. Hence, according to “section 8-1, ITAA

1997” her phone bill is following for positive limbs for those 60% of amount from the

taxable deductions. Whereas, 40% of the bill amount was spent on the private purposes,

hence she will not be able to claim deduction for that part. As per “section 8-1(2)” this is

falling under the non- deductible expenditure.

Answer to C:

As stated in “section 8-1(2)” the losses or expenditures those are involved for

domestic or private purposes are not supported for the claiming of deductions. This happens

as these expenditures are not meeting the expectations of positive limbs for the above section

taxpayer can claim these deductions for their expenditures that has occurred for gaining the

taxable income or ordinary income.

This evident can be taken from the Brett’s case that he has interest on his loan as he

had to pay his employees. Now, this interest on the loan has been generated while producing

the taxable income by Brett, hence he is eligible for getting deductions over this interest.

Therefore, according to “section 8-1, ITAA 1997” Brett will be allowed for the deductions

for the interest generated over his loan amount.

Answer to B:

Australian taxation office states that the taxpayers are allowed to claim the deductions

for their expenses which they have incurred while gaining the taxable income. There is also

one condition while claiming for the deductions, if the taxpayer has spent money over their

private and work purposes, then they are only allowed to claim the deductions for the work

purposes.

The consideration of Julie’s case, she has spent $500 for her mobile bills, out of

which 60% was spent for calls related to work. Hence, according to “section 8-1, ITAA

1997” her phone bill is following for positive limbs for those 60% of amount from the

taxable deductions. Whereas, 40% of the bill amount was spent on the private purposes,

hence she will not be able to claim deduction for that part. As per “section 8-1(2)” this is

falling under the non- deductible expenditure.

Answer to C:

As stated in “section 8-1(2)” the losses or expenditures those are involved for

domestic or private purposes are not supported for the claiming of deductions. This happens

as these expenditures are not meeting the expectations of positive limbs for the above section

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

is falling under the negative limbs, hence these are restricted for applying for the deductions

in taxable payment7. According to “Lodge v FC of T (1972)” the law court has denied to

provide deductions for the childcare expenditures through which the taxpayers uses for taking

care of her child while being at work. The court has mentioned that this expense is not a part

of the productive income which is considered to be a taxable income for the taxpayer.

According to this discussion, in the case of Sally, she has spent $1,200 for taking care

of her child to the babysitter. However, this amount is not falling under the deductions as this

expense was utilized for private purpose and this is not a productive expenditure for gaining

taxable income.

Answer to D:

According to positive limbs of “section 8-1” the connection between the involuntary

losses which is initiated from the activities which produces income for the taxpayer.

According to “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)” the court grants

deductions for the losses that has incurred to the taxpayer’s income which were supposed to

go his bank as a savings8.

Accordingly, Jerry should be allowed for the deductions under the positive limbs of

“section 8-1, ITAA 1997” for the products that were stolen by his employees. This is because

those goods were utilized to produce taxable incomes for his company.

7 Krever, Richard E, Australian Taxation Law Cases 2015

8 Kenny, Paul, Australian Tax 2013 LexisNexis Butterworths, 2013.

is falling under the negative limbs, hence these are restricted for applying for the deductions

in taxable payment7. According to “Lodge v FC of T (1972)” the law court has denied to

provide deductions for the childcare expenditures through which the taxpayers uses for taking

care of her child while being at work. The court has mentioned that this expense is not a part

of the productive income which is considered to be a taxable income for the taxpayer.

According to this discussion, in the case of Sally, she has spent $1,200 for taking care

of her child to the babysitter. However, this amount is not falling under the deductions as this

expense was utilized for private purpose and this is not a productive expenditure for gaining

taxable income.

Answer to D:

According to positive limbs of “section 8-1” the connection between the involuntary

losses which is initiated from the activities which produces income for the taxpayer.

According to “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)” the court grants

deductions for the losses that has incurred to the taxpayer’s income which were supposed to

go his bank as a savings8.

Accordingly, Jerry should be allowed for the deductions under the positive limbs of

“section 8-1, ITAA 1997” for the products that were stolen by his employees. This is because

those goods were utilized to produce taxable incomes for his company.

7 Krever, Richard E, Australian Taxation Law Cases 2015

8 Kenny, Paul, Australian Tax 2013 LexisNexis Butterworths, 2013.

8TAXATION LAW

Answer to E:

According to “section 8-1, ITAA 1997” losses or expenditures those occurred before

the revenue generating activities has happened are not allowed for the deductions in taxable

income as these are not a part of the revenue generation9. As per “FC of T v Madallena

(1971)” expenses incurred to gain new employments are also not considered for the

deductions.

Accordingly, expenditures incurred while arranging a local government election will

not be considered for the deductions as this is not generating revenues or this has happened

before those revenue generating activities has taken place. Hence these are not permitted for

deductions under the positive limbs of “section 8-1, ITAA 1997”.

Answer to question 3:

Answer to A:

In accordance with “CGT event F2” in case of renewal, granting or extending the

lease the taxpayer can allow right to his partner in this deal but the taxpayer have to grant the

sub- lease for that. In contrast with this fact, Andy granted a lease to Brain for period of five

year and the premium for it was $5,00010. This particular aspect gave rise to the CGT event

F2. Hence Andy will not be able to get the 50% of CGT as he denied following the CGT

event F2.

9 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law CCH Australia, 2013.

10 Sadiq, Kerrie, Principles Of Taxation Law 2014.

Answer to E:

According to “section 8-1, ITAA 1997” losses or expenditures those occurred before

the revenue generating activities has happened are not allowed for the deductions in taxable

income as these are not a part of the revenue generation9. As per “FC of T v Madallena

(1971)” expenses incurred to gain new employments are also not considered for the

deductions.

Accordingly, expenditures incurred while arranging a local government election will

not be considered for the deductions as this is not generating revenues or this has happened

before those revenue generating activities has taken place. Hence these are not permitted for

deductions under the positive limbs of “section 8-1, ITAA 1997”.

Answer to question 3:

Answer to A:

In accordance with “CGT event F2” in case of renewal, granting or extending the

lease the taxpayer can allow right to his partner in this deal but the taxpayer have to grant the

sub- lease for that. In contrast with this fact, Andy granted a lease to Brain for period of five

year and the premium for it was $5,00010. This particular aspect gave rise to the CGT event

F2. Hence Andy will not be able to get the 50% of CGT as he denied following the CGT

event F2.

9 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law CCH Australia, 2013.

10 Sadiq, Kerrie, Principles Of Taxation Law 2014.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to B:

The CGT event B1 in considered when the new owner of the land or entity enjoys the

right over that particular aspect. The use and enjoyment is mainly considered when the new

owner gets the right to use the property or he starts paying the rent to the partner entity. Now

this fact can be eventually proved by the case of providing right to Farm Ltd with sum of

$40,000 and also they got an option purchase 100-acre farm outside the Adelaide for the sum

of $800,000. Hence John will be getting 50% of CGT discount for his 100-acre farm.

Answer to C:

As per the ruling of Australian Taxation Office, taxpayer will be allowed for

residence exemption if he stayed at temporary residence however used for that particular

period in gaining taxable income11. Jamie and Olivia bought rented the property immediately

while purchasing it for two year of span. In contrary with this discussion, this property was

continuously used for gaining taxable income until it was sold in 2018. Hence Jamie and

Olivia will be allowed for partial main residence exemption throughout the period of time.

However, Jamie and Olivia could have been utilized the Discount method to calculate the net

capital gain and tax over this period.

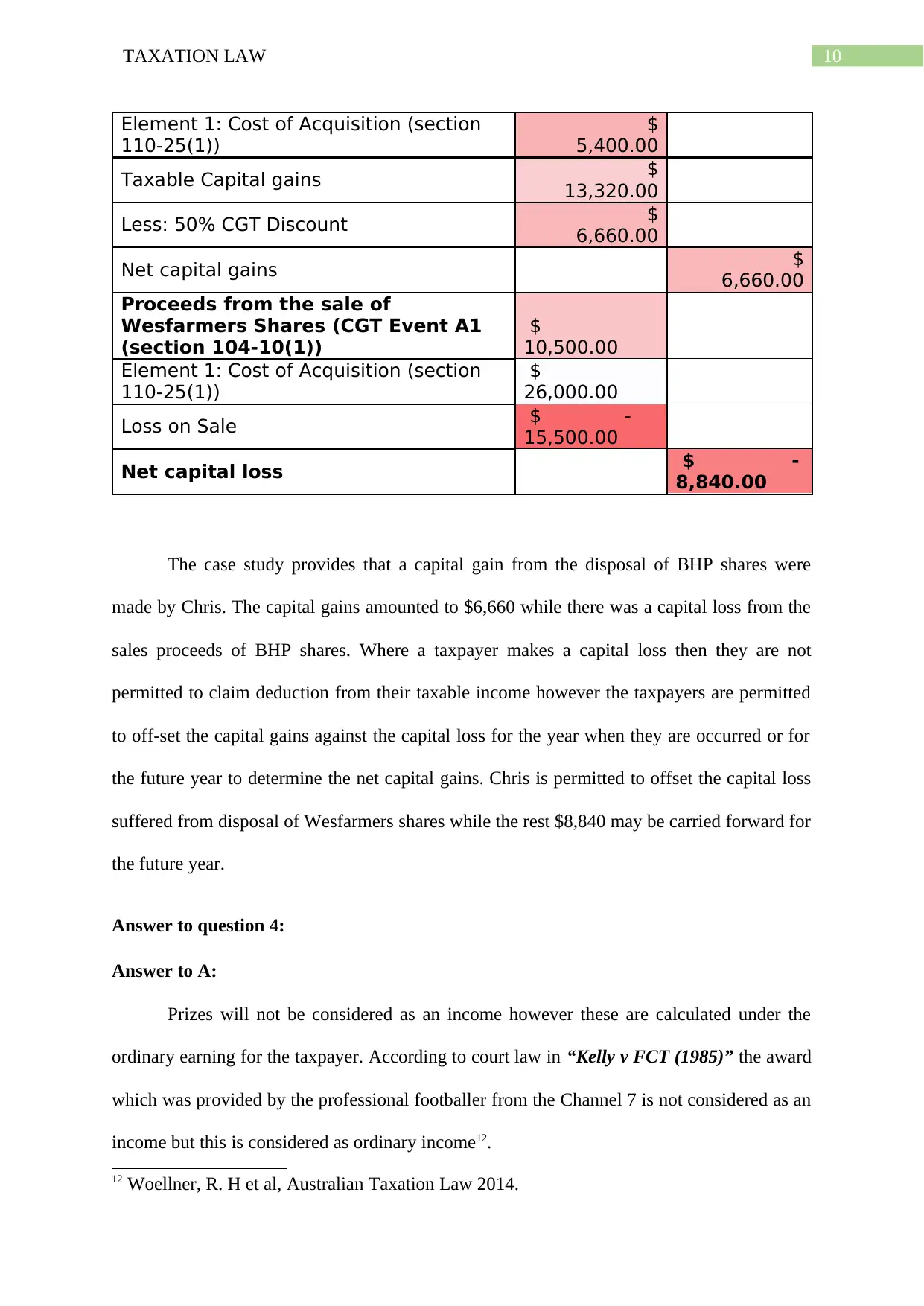

Answer to D:

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Particulars Amount

(AUD$)

Amount

(AUD$)

Proceeds from the sale of BHP

Shares (CGT Event A1 (section 104-

10(1))

$

18,720.00

11 Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 Lawbook

Co./Thomson Reuters, 2013.

Answer to B:

The CGT event B1 in considered when the new owner of the land or entity enjoys the

right over that particular aspect. The use and enjoyment is mainly considered when the new

owner gets the right to use the property or he starts paying the rent to the partner entity. Now

this fact can be eventually proved by the case of providing right to Farm Ltd with sum of

$40,000 and also they got an option purchase 100-acre farm outside the Adelaide for the sum

of $800,000. Hence John will be getting 50% of CGT discount for his 100-acre farm.

Answer to C:

As per the ruling of Australian Taxation Office, taxpayer will be allowed for

residence exemption if he stayed at temporary residence however used for that particular

period in gaining taxable income11. Jamie and Olivia bought rented the property immediately

while purchasing it for two year of span. In contrary with this discussion, this property was

continuously used for gaining taxable income until it was sold in 2018. Hence Jamie and

Olivia will be allowed for partial main residence exemption throughout the period of time.

However, Jamie and Olivia could have been utilized the Discount method to calculate the net

capital gain and tax over this period.

Answer to D:

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Particulars Amount

(AUD$)

Amount

(AUD$)

Proceeds from the sale of BHP

Shares (CGT Event A1 (section 104-

10(1))

$

18,720.00

11 Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 Lawbook

Co./Thomson Reuters, 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Element 1: Cost of Acquisition (section

110-25(1))

$

5,400.00

Taxable Capital gains $

13,320.00

Less: 50% CGT Discount $

6,660.00

Net capital gains $

6,660.00

Proceeds from the sale of

Wesfarmers Shares (CGT Event A1

(section 104-10(1))

$

10,500.00

Element 1: Cost of Acquisition (section

110-25(1))

$

26,000.00

Loss on Sale $ -

15,500.00

Net capital loss $ -

8,840.00

The case study provides that a capital gain from the disposal of BHP shares were

made by Chris. The capital gains amounted to $6,660 while there was a capital loss from the

sales proceeds of BHP shares. Where a taxpayer makes a capital loss then they are not

permitted to claim deduction from their taxable income however the taxpayers are permitted

to off-set the capital gains against the capital loss for the year when they are occurred or for

the future year to determine the net capital gains. Chris is permitted to offset the capital loss

suffered from disposal of Wesfarmers shares while the rest $8,840 may be carried forward for

the future year.

Answer to question 4:

Answer to A:

Prizes will not be considered as an income however these are calculated under the

ordinary earning for the taxpayer. According to court law in “Kelly v FCT (1985)” the award

which was provided by the professional footballer from the Channel 7 is not considered as an

income but this is considered as ordinary income12.

12 Woellner, R. H et al, Australian Taxation Law 2014.

Element 1: Cost of Acquisition (section

110-25(1))

$

5,400.00

Taxable Capital gains $

13,320.00

Less: 50% CGT Discount $

6,660.00

Net capital gains $

6,660.00

Proceeds from the sale of

Wesfarmers Shares (CGT Event A1

(section 104-10(1))

$

10,500.00

Element 1: Cost of Acquisition (section

110-25(1))

$

26,000.00

Loss on Sale $ -

15,500.00

Net capital loss $ -

8,840.00

The case study provides that a capital gain from the disposal of BHP shares were

made by Chris. The capital gains amounted to $6,660 while there was a capital loss from the

sales proceeds of BHP shares. Where a taxpayer makes a capital loss then they are not

permitted to claim deduction from their taxable income however the taxpayers are permitted

to off-set the capital gains against the capital loss for the year when they are occurred or for

the future year to determine the net capital gains. Chris is permitted to offset the capital loss

suffered from disposal of Wesfarmers shares while the rest $8,840 may be carried forward for

the future year.

Answer to question 4:

Answer to A:

Prizes will not be considered as an income however these are calculated under the

ordinary earning for the taxpayer. According to court law in “Kelly v FCT (1985)” the award

which was provided by the professional footballer from the Channel 7 is not considered as an

income but this is considered as ordinary income12.

12 Woellner, R. H et al, Australian Taxation Law 2014.

11TAXATION LAW

The prize of $2,000 for the best advertisement for that particular income year was

considered as income as this was in relation to his revenue generating activities. This award

was incidental as this was a gain for him.

Answer to B:

According to “section 6-1 of the ITAA 1936” taxpayer is liable in paying the wages,

salaries or commissions that are managed by him for personally13. These expenses are carried

on by himself with his own expenses. However, the gains from these companies will be held

as his income.

The total amount of $500 is delivered to an employee for completing a business trip in

Sydney. This will be held as the income for the employee as this happened during the course

of his employment with that particular company.

Answer to C:

A gift cannot be considered as income for the taxpayer. According to “Scott v F C of

T (1966)”14, the solicitor received the amount of $10,000 from his client’s wife will not be

considered as an income for him.

Answer to D:

According to “paragraph 118-37 (1) (b) of the ITAA 1997” receipts form a lump

sum amounts increases the capital gains for the taxpayer however, taxpayer should not

13 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

14 Jacob, Martin. "Tax regimes and capital gains realizations." European Accounting

Review 27.1 (2018): 1-21.

The prize of $2,000 for the best advertisement for that particular income year was

considered as income as this was in relation to his revenue generating activities. This award

was incidental as this was a gain for him.

Answer to B:

According to “section 6-1 of the ITAA 1936” taxpayer is liable in paying the wages,

salaries or commissions that are managed by him for personally13. These expenses are carried

on by himself with his own expenses. However, the gains from these companies will be held

as his income.

The total amount of $500 is delivered to an employee for completing a business trip in

Sydney. This will be held as the income for the employee as this happened during the course

of his employment with that particular company.

Answer to C:

A gift cannot be considered as income for the taxpayer. According to “Scott v F C of

T (1966)”14, the solicitor received the amount of $10,000 from his client’s wife will not be

considered as an income for him.

Answer to D:

According to “paragraph 118-37 (1) (b) of the ITAA 1997” receipts form a lump

sum amounts increases the capital gains for the taxpayer however, taxpayer should not

13 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

14 Jacob, Martin. "Tax regimes and capital gains realizations." European Accounting

Review 27.1 (2018): 1-21.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.