Taxation Law Assignment: Analysis of Tax Law Questions and Answers

VerifiedAdded on 2022/10/10

|19

|3489

|67

Homework Assignment

AI Summary

This document presents a detailed solution to a taxation law assignment, addressing five key questions with thorough analysis and referencing. The assignment covers various aspects of Australian taxation law, including business processes, deductibility of gifts, taxable income, capital gains tax (CGT), ordinary and statutory income, Medicare Levy, and residential status. The solution provides in-depth explanations, references to relevant legislation (ITAA97, ITAA36), tax rulings, and case law to support the arguments. It includes analysis of specific scenarios, such as lease of land, deductible expenses (HECS-HELP, travel, books, childcare, fridge repairs, clothing, legal expenses) and CGT events. The answers are well-structured and provide a comprehensive understanding of the concepts discussed. The document adheres to the Australian Guide to Legal Citation (AGLC) 4th Edition referencing method.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:......................................................................................................................3

Answer A:....................................................................................................................................3

Answer B:....................................................................................................................................3

Answer C:....................................................................................................................................3

Answer D:....................................................................................................................................3

Answer F:.....................................................................................................................................4

Answer H:....................................................................................................................................4

Answer I:.....................................................................................................................................5

Answer to question 2:......................................................................................................................6

Answer to Question – 3...................................................................................................................8

Answer to Question – 4.................................................................................................................12

Answer (a).................................................................................................................................12

Answer (b).................................................................................................................................12

Answer (c).................................................................................................................................13

Answer (d).................................................................................................................................14

Answer to Question – 5.................................................................................................................15

Answer (a).................................................................................................................................15

Answer (b).................................................................................................................................15

Table of Contents

Answer to question 1:......................................................................................................................3

Answer A:....................................................................................................................................3

Answer B:....................................................................................................................................3

Answer C:....................................................................................................................................3

Answer D:....................................................................................................................................3

Answer F:.....................................................................................................................................4

Answer H:....................................................................................................................................4

Answer I:.....................................................................................................................................5

Answer to question 2:......................................................................................................................6

Answer to Question – 3...................................................................................................................8

Answer to Question – 4.................................................................................................................12

Answer (a).................................................................................................................................12

Answer (b).................................................................................................................................12

Answer (c).................................................................................................................................13

Answer (d).................................................................................................................................14

Answer to Question – 5.................................................................................................................15

Answer (a).................................................................................................................................15

Answer (b).................................................................................................................................15

2TAXATION LAW

Answer (c).................................................................................................................................16

Answer (d).................................................................................................................................16

Answer (e).................................................................................................................................17

References:....................................................................................................................................18

Answer (c).................................................................................................................................16

Answer (d).................................................................................................................................16

Answer (e).................................................................................................................................17

References:....................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

The “taxation ruling of TR 2019/1” deals with the business process through which a

company is carried out1. Under “s-23, ITRA 1986”, the company carries its business entity and

it is valid from 2015-16 and 2016-17 income years, as per the commissioners under ‘s328-110,

IITA 1997”.

Answer B:

The procedure and the rules for working out the deduction for any contribution or gifts, is

explained under “Division 30, ITAA 1997” a taxpayer during the year.

Answer C:

The taxable income for the Australian resident is beyond the $108,000 and the top

marginal tax of 45% is applied over $180,000; it is levied for the income year of 2019-20.

Answer D:

Neither the motorcycle nor the car is exempted from the capital gains. Thus, it will be

treated as personal use asset under the “Sec-108-20, IITA 1997”2. An exemption can be allowed

from the capital gains or loss, if the first element of the asset cost base is below $10,000.

Answer E:

1 Woellner, Robin H., et al. Australian taxation law. CCH Australia, 2015.

2 Coleman, Geoffrey Lehmann Cynthia. "Taxation law in Australia." (2017)

Answer to question 1:

Answer A:

The “taxation ruling of TR 2019/1” deals with the business process through which a

company is carried out1. Under “s-23, ITRA 1986”, the company carries its business entity and

it is valid from 2015-16 and 2016-17 income years, as per the commissioners under ‘s328-110,

IITA 1997”.

Answer B:

The procedure and the rules for working out the deduction for any contribution or gifts, is

explained under “Division 30, ITAA 1997” a taxpayer during the year.

Answer C:

The taxable income for the Australian resident is beyond the $108,000 and the top

marginal tax of 45% is applied over $180,000; it is levied for the income year of 2019-20.

Answer D:

Neither the motorcycle nor the car is exempted from the capital gains. Thus, it will be

treated as personal use asset under the “Sec-108-20, IITA 1997”2. An exemption can be allowed

from the capital gains or loss, if the first element of the asset cost base is below $10,000.

Answer E:

1 Woellner, Robin H., et al. Australian taxation law. CCH Australia, 2015.

2 Coleman, Geoffrey Lehmann Cynthia. "Taxation law in Australia." (2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The CGT assets is mainly dealt by the CGT event, under the “s 104-20(1), IITA 1997”.

Thus, when the owner who is the tax payer gets destroyed or loss of the CGT assets, then the

CGT event happens3. Thus the compensation by the taxpayer is received when the event

happens.

Answer F:

The receipt will not be considered as ordinary earnings, because as per the case of

“Hayes v FCT (1956)”, the reward of services or the occupational production is not found in the

receipt. As the gift is considered as which gives a personal qualities, then it will not be included

in the assessable income of the recipient and it will not be considered as taxable ordinary

income4. The nature of receipts which the recipient received has more emphasis which has been

placed by the court, which is related to the services and can be found in time of distinguishing

the assessable voluntary payments and non-taxable personal gifts. The services which they

offered is appreciated and the unsolicited gifts cannot be considered as unsolicited gifts.

Answer H:

Ordinary Income Statutory Income

3 Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1

(2017): 3-10.

4 Kewley, Gretchen M. Australian Taxation: principles and practice. Longman Professional,

2017.

The CGT assets is mainly dealt by the CGT event, under the “s 104-20(1), IITA 1997”.

Thus, when the owner who is the tax payer gets destroyed or loss of the CGT assets, then the

CGT event happens3. Thus the compensation by the taxpayer is received when the event

happens.

Answer F:

The receipt will not be considered as ordinary earnings, because as per the case of

“Hayes v FCT (1956)”, the reward of services or the occupational production is not found in the

receipt. As the gift is considered as which gives a personal qualities, then it will not be included

in the assessable income of the recipient and it will not be considered as taxable ordinary

income4. The nature of receipts which the recipient received has more emphasis which has been

placed by the court, which is related to the services and can be found in time of distinguishing

the assessable voluntary payments and non-taxable personal gifts. The services which they

offered is appreciated and the unsolicited gifts cannot be considered as unsolicited gifts.

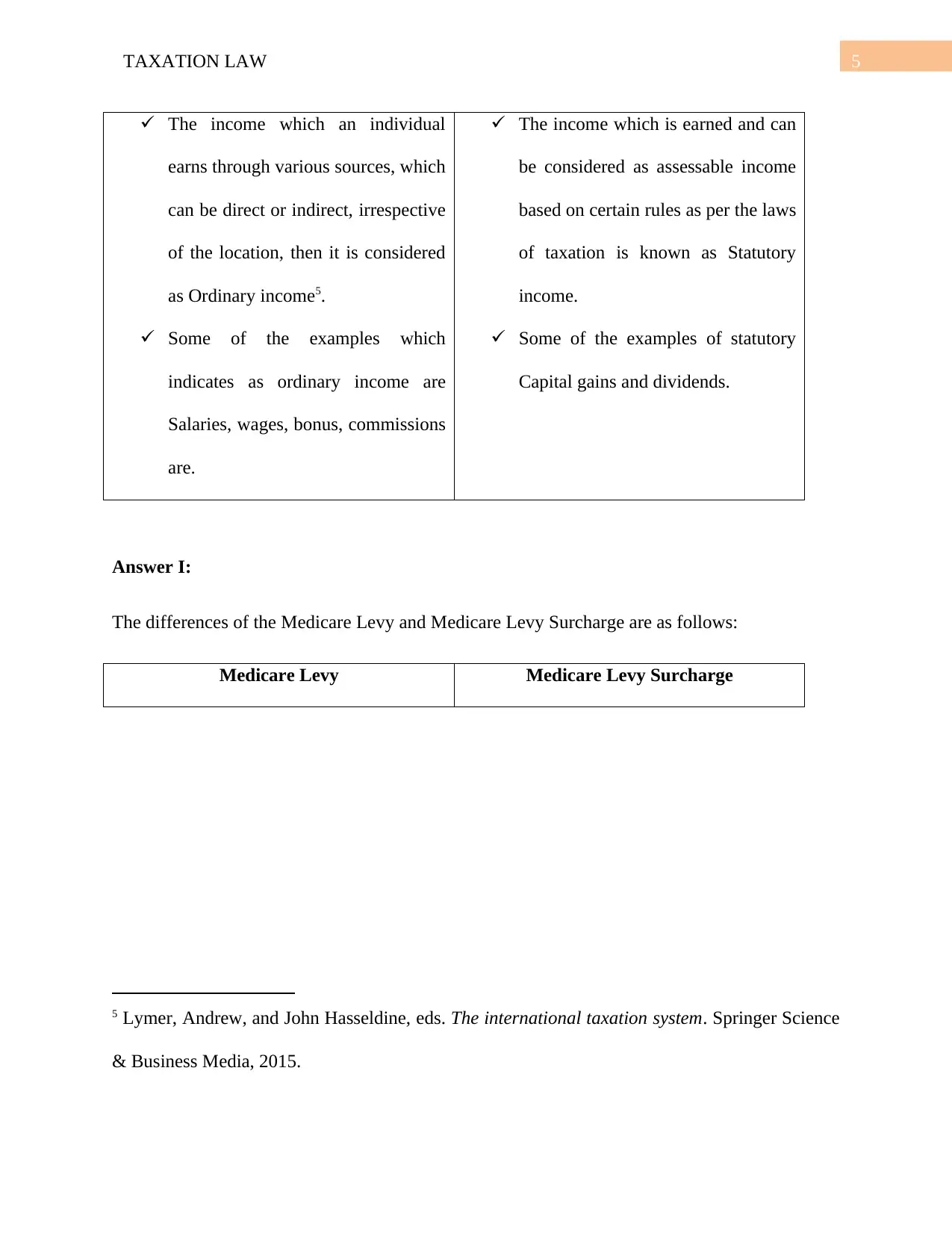

Answer H:

Ordinary Income Statutory Income

3 Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1

(2017): 3-10.

4 Kewley, Gretchen M. Australian Taxation: principles and practice. Longman Professional,

2017.

5TAXATION LAW

The income which an individual

earns through various sources, which

can be direct or indirect, irrespective

of the location, then it is considered

as Ordinary income5.

Some of the examples which

indicates as ordinary income are

Salaries, wages, bonus, commissions

are.

The income which is earned and can

be considered as assessable income

based on certain rules as per the laws

of taxation is known as Statutory

income.

Some of the examples of statutory

Capital gains and dividends.

Answer I:

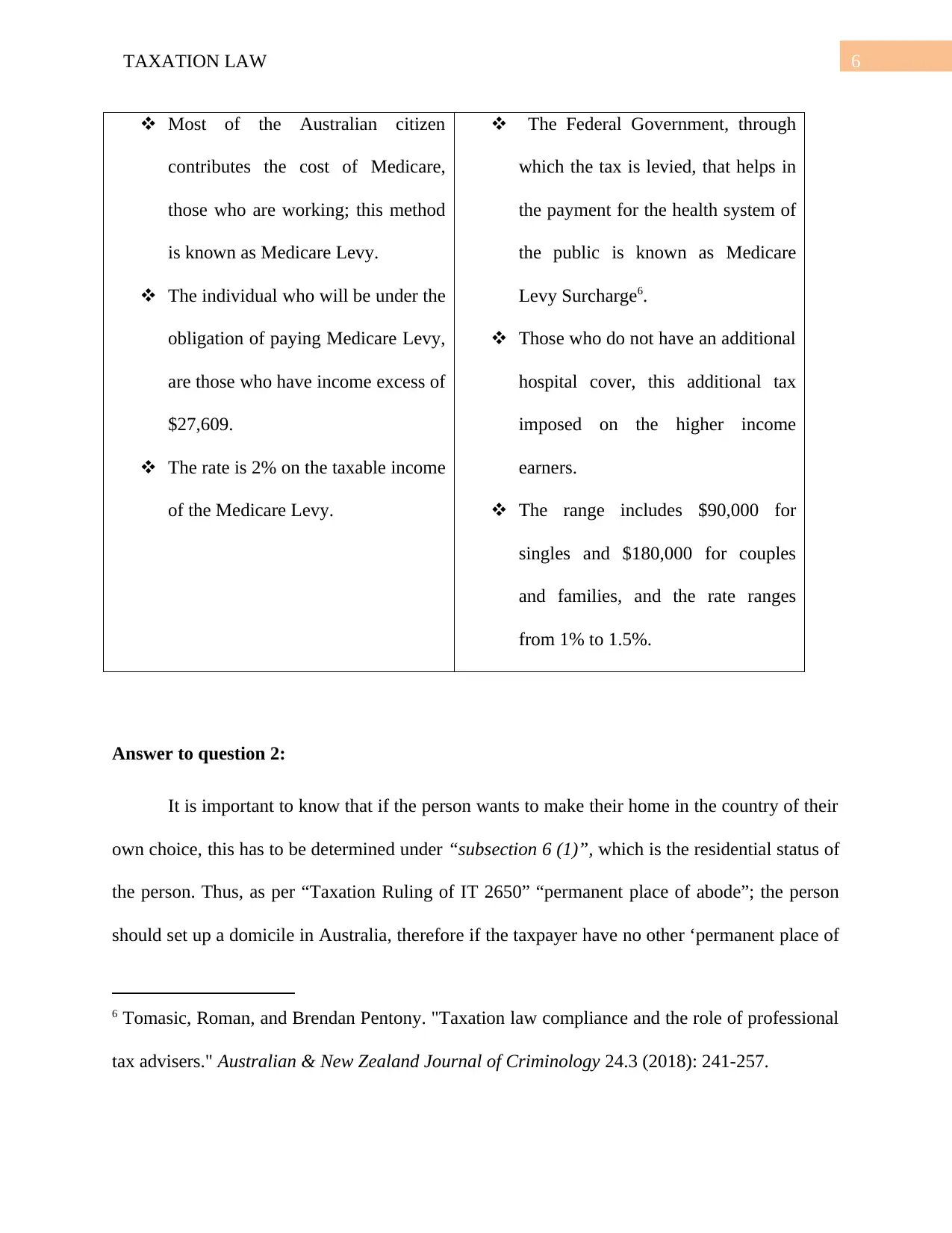

The differences of the Medicare Levy and Medicare Levy Surcharge are as follows:

Medicare Levy Medicare Levy Surcharge

5 Lymer, Andrew, and John Hasseldine, eds. The international taxation system. Springer Science

& Business Media, 2015.

The income which an individual

earns through various sources, which

can be direct or indirect, irrespective

of the location, then it is considered

as Ordinary income5.

Some of the examples which

indicates as ordinary income are

Salaries, wages, bonus, commissions

are.

The income which is earned and can

be considered as assessable income

based on certain rules as per the laws

of taxation is known as Statutory

income.

Some of the examples of statutory

Capital gains and dividends.

Answer I:

The differences of the Medicare Levy and Medicare Levy Surcharge are as follows:

Medicare Levy Medicare Levy Surcharge

5 Lymer, Andrew, and John Hasseldine, eds. The international taxation system. Springer Science

& Business Media, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Most of the Australian citizen

contributes the cost of Medicare,

those who are working; this method

is known as Medicare Levy.

The individual who will be under the

obligation of paying Medicare Levy,

are those who have income excess of

$27,609.

The rate is 2% on the taxable income

of the Medicare Levy.

The Federal Government, through

which the tax is levied, that helps in

the payment for the health system of

the public is known as Medicare

Levy Surcharge6.

Those who do not have an additional

hospital cover, this additional tax

imposed on the higher income

earners.

The range includes $90,000 for

singles and $180,000 for couples

and families, and the rate ranges

from 1% to 1.5%.

Answer to question 2:

It is important to know that if the person wants to make their home in the country of their

own choice, this has to be determined under “subsection 6 (1)”, which is the residential status of

the person. Thus, as per “Taxation Ruling of IT 2650” “permanent place of abode”; the person

should set up a domicile in Australia, therefore if the taxpayer have no other ‘permanent place of

6 Tomasic, Roman, and Brendan Pentony. "Taxation law compliance and the role of professional

tax advisers." Australian & New Zealand Journal of Criminology 24.3 (2018): 241-257.

Most of the Australian citizen

contributes the cost of Medicare,

those who are working; this method

is known as Medicare Levy.

The individual who will be under the

obligation of paying Medicare Levy,

are those who have income excess of

$27,609.

The rate is 2% on the taxable income

of the Medicare Levy.

The Federal Government, through

which the tax is levied, that helps in

the payment for the health system of

the public is known as Medicare

Levy Surcharge6.

Those who do not have an additional

hospital cover, this additional tax

imposed on the higher income

earners.

The range includes $90,000 for

singles and $180,000 for couples

and families, and the rate ranges

from 1% to 1.5%.

Answer to question 2:

It is important to know that if the person wants to make their home in the country of their

own choice, this has to be determined under “subsection 6 (1)”, which is the residential status of

the person. Thus, as per “Taxation Ruling of IT 2650” “permanent place of abode”; the person

should set up a domicile in Australia, therefore if the taxpayer have no other ‘permanent place of

6 Tomasic, Roman, and Brendan Pentony. "Taxation law compliance and the role of professional

tax advisers." Australian & New Zealand Journal of Criminology 24.3 (2018): 241-257.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

adobe” outside Australia, the taxation officer is satisfied7. The resident who lives with the family

in the state is usually expressed as “usual place of abode”. In “Levene v IRC (1928)” the “usual

place of abode” it signifies that the resident live with the physical surroundings.

In the meantime, “permanent place of abode” denoted that the residence have a fixed

home on the taxpayer’s dwelling. Sometimes, it is treated as abode or home of the tax payer so it

cannot be considered as their permanent residence8. Those who live as an ordinary residence, the

relationship between the particular places of abode, thus having their “usual place of abode”.

Time space, durability of relationship and continuity of presence are some of the factors which

should be considered.

As per the judgment of “FCT v Jenkins (1982)”, it was considered as “permanent place

of abode” out of Australia because the tax payer was setting up office for three years’ time after

transferred to New Hebrides. There was no development of the material intention, which is

remaining in overseas for indefinite time as per the taxpayer.

The movement of the tax payer would be fully temporary in nature if the individual will

keep on moving from on state to other. Thus, as per the statement there is no “usual place of

abode” in Australia or any “permanent place of abode”9.

7 Braithwaite, Valerie, and Monika Reinhart. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University, 2019.

8 Oats, Lynne, ed. Taxation: A fieldwork research handbook. Routledge, 2014.

adobe” outside Australia, the taxation officer is satisfied7. The resident who lives with the family

in the state is usually expressed as “usual place of abode”. In “Levene v IRC (1928)” the “usual

place of abode” it signifies that the resident live with the physical surroundings.

In the meantime, “permanent place of abode” denoted that the residence have a fixed

home on the taxpayer’s dwelling. Sometimes, it is treated as abode or home of the tax payer so it

cannot be considered as their permanent residence8. Those who live as an ordinary residence, the

relationship between the particular places of abode, thus having their “usual place of abode”.

Time space, durability of relationship and continuity of presence are some of the factors which

should be considered.

As per the judgment of “FCT v Jenkins (1982)”, it was considered as “permanent place

of abode” out of Australia because the tax payer was setting up office for three years’ time after

transferred to New Hebrides. There was no development of the material intention, which is

remaining in overseas for indefinite time as per the taxpayer.

The movement of the tax payer would be fully temporary in nature if the individual will

keep on moving from on state to other. Thus, as per the statement there is no “usual place of

abode” in Australia or any “permanent place of abode”9.

7 Braithwaite, Valerie, and Monika Reinhart. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University, 2019.

8 Oats, Lynne, ed. Taxation: A fieldwork research handbook. Routledge, 2014.

8TAXATION LAW

The tax payers maintain a family and financial bond in Australia, those who use to work

overseas; it is seen as per the case of “Harding v FC of T (2019)”. Thus, there is a judgment

which is passed by the federal court which states that under “section 6 (1), ITAA 1997”, the

resident of Australia is not the taxpayer10. Through a proper investigation it can found that

“permanent place of abode”, the residential status cannot be determined that whether the person

is living permanently or not.

In the above discussion, it is explained that the person cannot be from outside of

Australia “usual place of abode”. For the individuals there should be a test where there is

“permanent place of abode” is outside Australia.

Answer to Question – 3

HECS-HELP: $850

It has stated as per “Sec 26-20 ITAA 1997”, if a person makes any contribution towards

the Australian Government then he/she will not be liable to get any deduction of an Income tax.

While seeing the fact in the case it has noticed that the trainee accountant has made expenses of

$850 while contributing towards the HECS_HELP. Therefore, it is not an appropriate link fir

getting income tax deduction11.

9 Braithwaite, Valerie, Kristina Murphy, and Monika Reinhart. "Taxation threat, motivational

postures, and responsive regulation." Law & Policy 29.1 (2017): 137-158.

10 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

11 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

The tax payers maintain a family and financial bond in Australia, those who use to work

overseas; it is seen as per the case of “Harding v FC of T (2019)”. Thus, there is a judgment

which is passed by the federal court which states that under “section 6 (1), ITAA 1997”, the

resident of Australia is not the taxpayer10. Through a proper investigation it can found that

“permanent place of abode”, the residential status cannot be determined that whether the person

is living permanently or not.

In the above discussion, it is explained that the person cannot be from outside of

Australia “usual place of abode”. For the individuals there should be a test where there is

“permanent place of abode” is outside Australia.

Answer to Question – 3

HECS-HELP: $850

It has stated as per “Sec 26-20 ITAA 1997”, if a person makes any contribution towards

the Australian Government then he/she will not be liable to get any deduction of an Income tax.

While seeing the fact in the case it has noticed that the trainee accountant has made expenses of

$850 while contributing towards the HECS_HELP. Therefore, it is not an appropriate link fir

getting income tax deduction11.

9 Braithwaite, Valerie, Kristina Murphy, and Monika Reinhart. "Taxation threat, motivational

postures, and responsive regulation." Law & Policy 29.1 (2017): 137-158.

10 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

11 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

TRAVEL: $110

Australian Taxation Officer (ATO) has stated that if an employee or a person who is

working somewhere and for the improvement or increasing their skills and production in that

field if he/she is taking any formal course then it will be allow as deduction. For getting the

benefit of deduction, the employee must satisfy the given conditions:

The course that the person is taking must be for increasing the skills and knowledge in

respect to the current work

He/she must proof that the course leads to increasing their income from the activities

related to the current job

The deduction is allowing on the expenses of $110 made from a person while travelling

from the work place to home. The trainee accountant travels from university to home. Under

“S8-1, ITTA 1997” the general deduction is allowing to the taxpayer as the course undertaken

is to enhance the skills and knowledge and the taxpayer is travelling regarding that from

University to home place12.

BOOKS- $200

The “Taxation Ruling of TR 98/9” states that the expenses incurred on the self-

education that includes the book cost or the study materials like calculators, stationary and many

more13. Such expenses have been allowing for deduction under “S8-1, ITAA 1997”. The

12 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

13 Keyzer, Patrick, Christopher Goff, and Asaf Fisher. Principles of Australian constitutional

law. LexisNexis Butterworths, 2017.

TRAVEL: $110

Australian Taxation Officer (ATO) has stated that if an employee or a person who is

working somewhere and for the improvement or increasing their skills and production in that

field if he/she is taking any formal course then it will be allow as deduction. For getting the

benefit of deduction, the employee must satisfy the given conditions:

The course that the person is taking must be for increasing the skills and knowledge in

respect to the current work

He/she must proof that the course leads to increasing their income from the activities

related to the current job

The deduction is allowing on the expenses of $110 made from a person while travelling

from the work place to home. The trainee accountant travels from university to home. Under

“S8-1, ITTA 1997” the general deduction is allowing to the taxpayer as the course undertaken

is to enhance the skills and knowledge and the taxpayer is travelling regarding that from

University to home place12.

BOOKS- $200

The “Taxation Ruling of TR 98/9” states that the expenses incurred on the self-

education that includes the book cost or the study materials like calculators, stationary and many

more13. Such expenses have been allowing for deduction under “S8-1, ITAA 1997”. The

12 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

13 Keyzer, Patrick, Christopher Goff, and Asaf Fisher. Principles of Australian constitutional

law. LexisNexis Butterworths, 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

taxpayer will get the deduction for the expenses done in living and travelling within “FCT v

Studert (1982) ATC 4463” that relates to the scope of increase income in the current work.

Therefore, the trainee accountant within “S8-1, ITAA 1997” has allowed to claim

deduction as the cost incurred of $200 was in the books for the purpose of self-deduction as these

expense helps in increase in the income in the current job.

CHILDCARE DURING COURSE: $80

Within “sec8-1 (2) (b), ITAA 1997” negative limbs does not allow for any deduction for

the expenses made in the childcare. In the case of “Lodge v FCT (1972), the court has rejected

the claim of the taxpayer for the deduction of childcare expenses as the fact is not linked with the

origin of assessable income14. Therefore, the expenses of $80 for the childcare during the

evening classes will not be allow for deduction under “s8-1(2)(b), ITAA 1997” as the fact of the

taxpayer does not meet the criteria for the origin of assessable income.

FRIDGE REPAIRED FOR HOME: $250

The expenses related to the repairs of any depreciating asset that is not for the creation of

an assessable income will not be allow for deduction within the “sec25-10, ITAA 1997”15. In the

fact here, the taxpayer has made an expense of $250 on repairing of the fridge for home as

14 Burton, Hughlene A., and Stewart Karlinsky. "Tax professionals' perception of large and mid-

size business US tax law complexity." eJTR 14 (2016): 61.

15 Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

taxpayer will get the deduction for the expenses done in living and travelling within “FCT v

Studert (1982) ATC 4463” that relates to the scope of increase income in the current work.

Therefore, the trainee accountant within “S8-1, ITAA 1997” has allowed to claim

deduction as the cost incurred of $200 was in the books for the purpose of self-deduction as these

expense helps in increase in the income in the current job.

CHILDCARE DURING COURSE: $80

Within “sec8-1 (2) (b), ITAA 1997” negative limbs does not allow for any deduction for

the expenses made in the childcare. In the case of “Lodge v FCT (1972), the court has rejected

the claim of the taxpayer for the deduction of childcare expenses as the fact is not linked with the

origin of assessable income14. Therefore, the expenses of $80 for the childcare during the

evening classes will not be allow for deduction under “s8-1(2)(b), ITAA 1997” as the fact of the

taxpayer does not meet the criteria for the origin of assessable income.

FRIDGE REPAIRED FOR HOME: $250

The expenses related to the repairs of any depreciating asset that is not for the creation of

an assessable income will not be allow for deduction within the “sec25-10, ITAA 1997”15. In the

fact here, the taxpayer has made an expense of $250 on repairing of the fridge for home as

14 Burton, Hughlene A., and Stewart Karlinsky. "Tax professionals' perception of large and mid-

size business US tax law complexity." eJTR 14 (2016): 61.

15 Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

11TAXATION LAW

private purpose and the asset has not repaired for generating an assessable income thus, not allow

for deduction.

BLACK TROUSERS AND SHIRT FOR OFFICE: $145

As per “sec 8-1, ITAA 1997” on the apparels for the office purpose will not be allow for

deduction. In the case of “Westcott v FCT (1997)” for the purchase of the apparels for the

office purpose, the deduction has not allowed by the court, as it was not for the origin of income.

Hence, considered as an Ordinary article of clothing. The taxpayer has made the expense of $145

in cloth such as black trousers and shirts for use in the office. Hence, it has nondeductible within

“sec 8-1, ITAA 1997” as it has treated as Ordinary Article of apparel

LEGAL EXPENSES FOR NEW EMPLOYMENT: $300

As it has mentioned within the positive limb of “sec 8-1, ITAA 1997” that expenses

made for getting new employment is not the way of generating an income. The case of a

footballer while negotiating contract within Maddalena v FCT (1971)” has not get deduction16.

The trainee has made a legal expense of $300 for writing up a new employment with a new

employer that is treated as non-deductible as it has not made for generating income and soon

within “sec 8-1, ITAA 1997” of positive limbs.

Answer to Question – 4

Answer (a)

On the lease of land, several capital tax gains are existing to be applicable on it. If a

taxpayer has allowed lease to any person or in the case of renewing the earlier permitted lease

16 Butler, Daniel. "Who can provide taxation advice?." Taxation in Australia 53.7 (2019): 381.

private purpose and the asset has not repaired for generating an assessable income thus, not allow

for deduction.

BLACK TROUSERS AND SHIRT FOR OFFICE: $145

As per “sec 8-1, ITAA 1997” on the apparels for the office purpose will not be allow for

deduction. In the case of “Westcott v FCT (1997)” for the purchase of the apparels for the

office purpose, the deduction has not allowed by the court, as it was not for the origin of income.

Hence, considered as an Ordinary article of clothing. The taxpayer has made the expense of $145

in cloth such as black trousers and shirts for use in the office. Hence, it has nondeductible within

“sec 8-1, ITAA 1997” as it has treated as Ordinary Article of apparel

LEGAL EXPENSES FOR NEW EMPLOYMENT: $300

As it has mentioned within the positive limb of “sec 8-1, ITAA 1997” that expenses

made for getting new employment is not the way of generating an income. The case of a

footballer while negotiating contract within Maddalena v FCT (1971)” has not get deduction16.

The trainee has made a legal expense of $300 for writing up a new employment with a new

employer that is treated as non-deductible as it has not made for generating income and soon

within “sec 8-1, ITAA 1997” of positive limbs.

Answer to Question – 4

Answer (a)

On the lease of land, several capital tax gains are existing to be applicable on it. If a

taxpayer has allowed lease to any person or in the case of renewing the earlier permitted lease

16 Butler, Daniel. "Who can provide taxation advice?." Taxation in Australia 53.7 (2019): 381.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.