Taxation Law Assignment: TLAW603, Taxation Law, Semester 2, 2019

VerifiedAdded on 2022/10/13

|12

|2800

|21

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, likely for a university-level course (TLAW603), focusing on Australian taxation principles. The solution meticulously calculates income tax liabilities for two individuals, Piper and David, detailing assessable income, allowable deductions, and tax payable, referencing relevant sections of the ITAA 1936 and ITAA 1997. It addresses specific scenarios, such as foreign-sourced income, self-education expenses, and the tax implications of various income sources like salaries and gifts. The assignment further explores superannuation, discussing the tax treatment of foreign super funds and offering strategies like re-contribution to minimize tax liabilities. It concludes by examining deductible expenses related to seminars and self-education, providing a complete and practical guide to navigating complex tax scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the University

Name of the Student

Authors Note

Course ID

Taxation Law

Name of the University

Name of the Student

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................8

References:.................................................................................................................................9

2TAXATION LAW

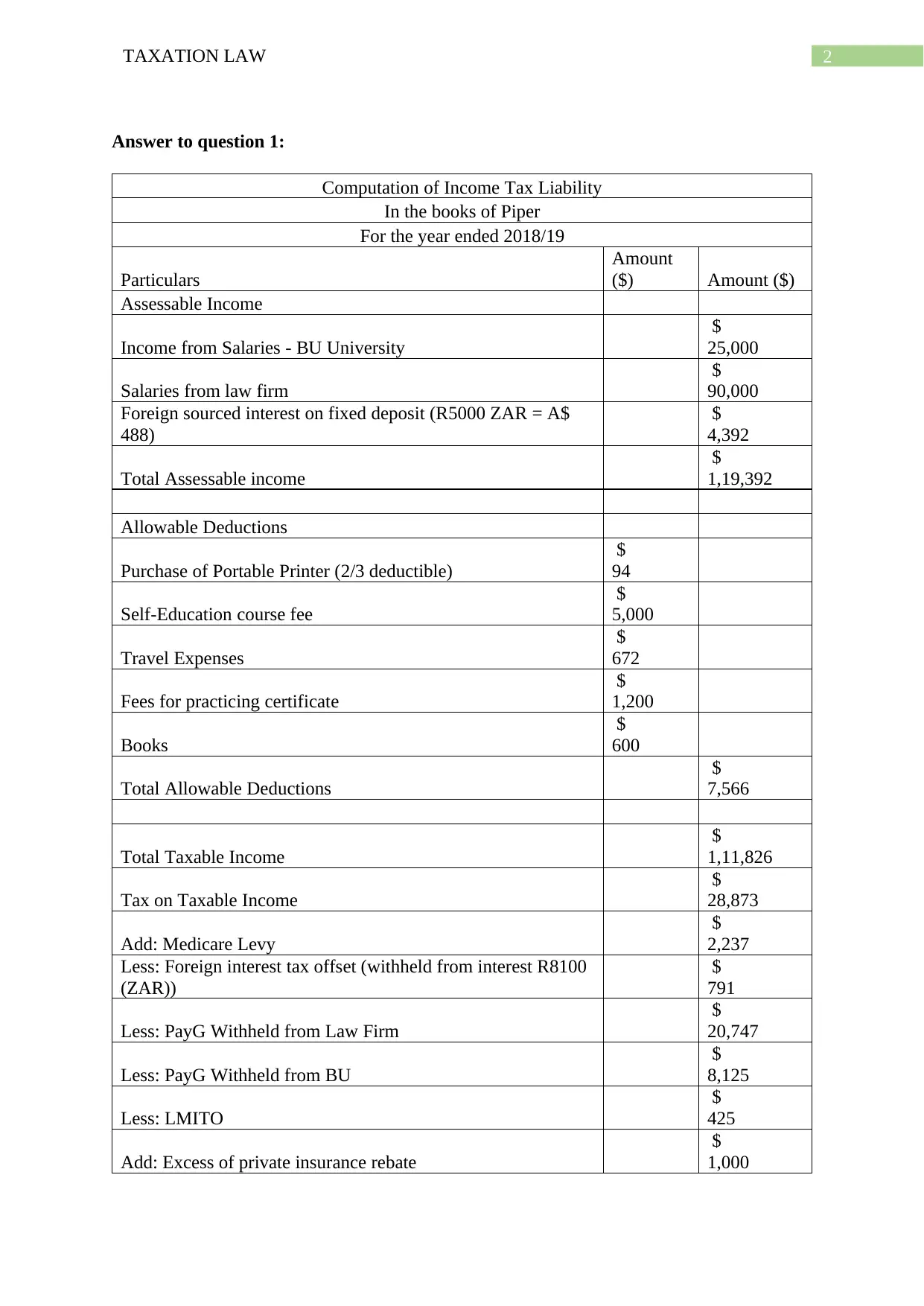

Answer to question 1:

Computation of Income Tax Liability

In the books of Piper

For the year ended 2018/19

Particulars

Amount

($) Amount ($)

Assessable Income

Income from Salaries - BU University

$

25,000

Salaries from law firm

$

90,000

Foreign sourced interest on fixed deposit (R5000 ZAR = A$

488)

$

4,392

Total Assessable income

$

1,19,392

Allowable Deductions

Purchase of Portable Printer (2/3 deductible)

$

94

Self-Education course fee

$

5,000

Travel Expenses

$

672

Fees for practicing certificate

$

1,200

Books

$

600

Total Allowable Deductions

$

7,566

Total Taxable Income

$

1,11,826

Tax on Taxable Income

$

28,873

Add: Medicare Levy

$

2,237

Less: Foreign interest tax offset (withheld from interest R8100

(ZAR))

$

791

Less: PayG Withheld from Law Firm

$

20,747

Less: PayG Withheld from BU

$

8,125

Less: LMITO

$

425

Add: Excess of private insurance rebate

$

1,000

Answer to question 1:

Computation of Income Tax Liability

In the books of Piper

For the year ended 2018/19

Particulars

Amount

($) Amount ($)

Assessable Income

Income from Salaries - BU University

$

25,000

Salaries from law firm

$

90,000

Foreign sourced interest on fixed deposit (R5000 ZAR = A$

488)

$

4,392

Total Assessable income

$

1,19,392

Allowable Deductions

Purchase of Portable Printer (2/3 deductible)

$

94

Self-Education course fee

$

5,000

Travel Expenses

$

672

Fees for practicing certificate

$

1,200

Books

$

600

Total Allowable Deductions

$

7,566

Total Taxable Income

$

1,11,826

Tax on Taxable Income

$

28,873

Add: Medicare Levy

$

2,237

Less: Foreign interest tax offset (withheld from interest R8100

(ZAR))

$

791

Less: PayG Withheld from Law Firm

$

20,747

Less: PayG Withheld from BU

$

8,125

Less: LMITO

$

425

Add: Excess of private insurance rebate

$

1,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

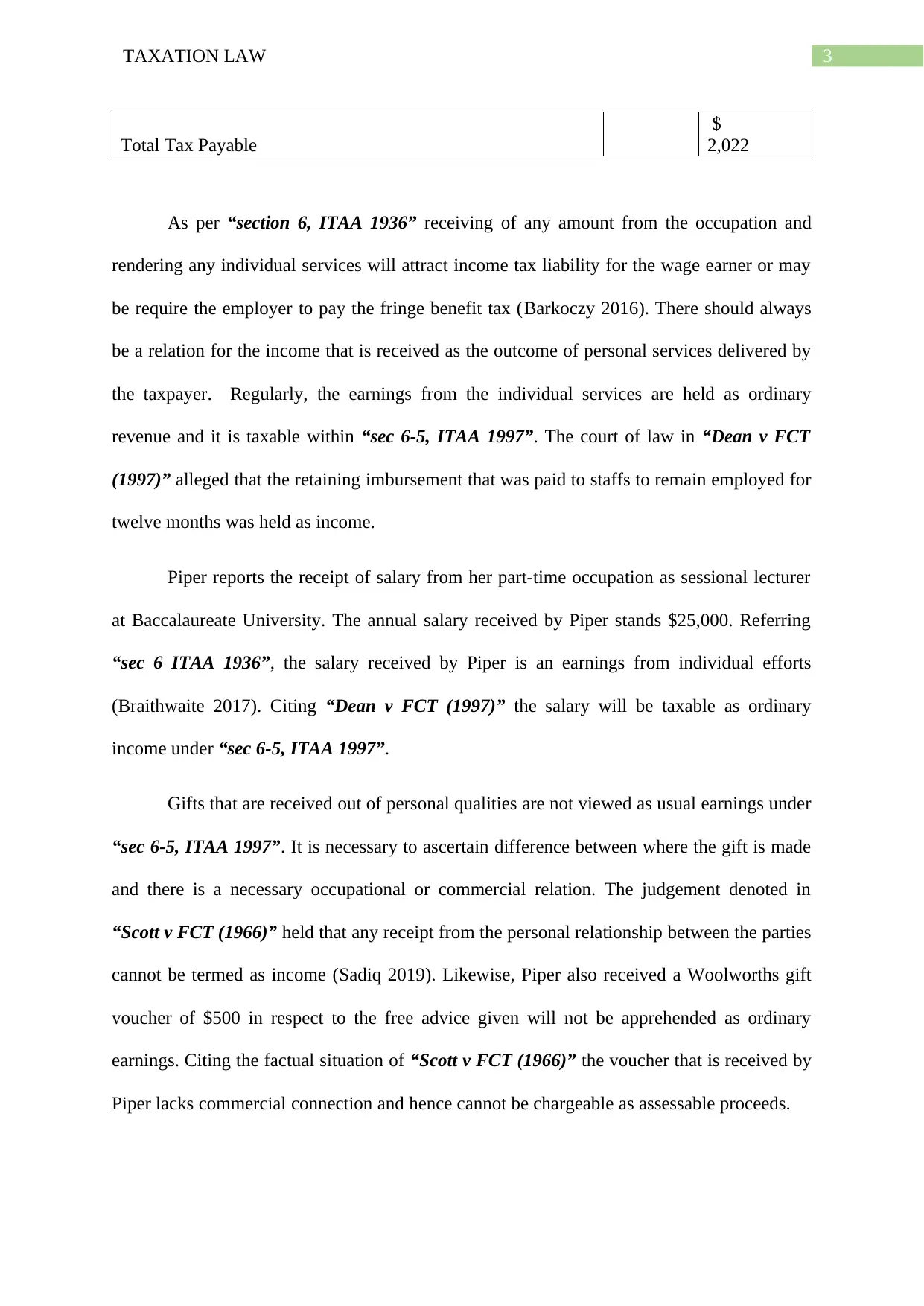

Total Tax Payable

$

2,022

As per “section 6, ITAA 1936” receiving of any amount from the occupation and

rendering any individual services will attract income tax liability for the wage earner or may

be require the employer to pay the fringe benefit tax (Barkoczy 2016). There should always

be a relation for the income that is received as the outcome of personal services delivered by

the taxpayer. Regularly, the earnings from the individual services are held as ordinary

revenue and it is taxable within “sec 6-5, ITAA 1997”. The court of law in “Dean v FCT

(1997)” alleged that the retaining imbursement that was paid to staffs to remain employed for

twelve months was held as income.

Piper reports the receipt of salary from her part-time occupation as sessional lecturer

at Baccalaureate University. The annual salary received by Piper stands $25,000. Referring

“sec 6 ITAA 1936”, the salary received by Piper is an earnings from individual efforts

(Braithwaite 2017). Citing “Dean v FCT (1997)” the salary will be taxable as ordinary

income under “sec 6-5, ITAA 1997”.

Gifts that are received out of personal qualities are not viewed as usual earnings under

“sec 6-5, ITAA 1997”. It is necessary to ascertain difference between where the gift is made

and there is a necessary occupational or commercial relation. The judgement denoted in

“Scott v FCT (1966)” held that any receipt from the personal relationship between the parties

cannot be termed as income (Sadiq 2019). Likewise, Piper also received a Woolworths gift

voucher of $500 in respect to the free advice given will not be apprehended as ordinary

earnings. Citing the factual situation of “Scott v FCT (1966)” the voucher that is received by

Piper lacks commercial connection and hence cannot be chargeable as assessable proceeds.

Total Tax Payable

$

2,022

As per “section 6, ITAA 1936” receiving of any amount from the occupation and

rendering any individual services will attract income tax liability for the wage earner or may

be require the employer to pay the fringe benefit tax (Barkoczy 2016). There should always

be a relation for the income that is received as the outcome of personal services delivered by

the taxpayer. Regularly, the earnings from the individual services are held as ordinary

revenue and it is taxable within “sec 6-5, ITAA 1997”. The court of law in “Dean v FCT

(1997)” alleged that the retaining imbursement that was paid to staffs to remain employed for

twelve months was held as income.

Piper reports the receipt of salary from her part-time occupation as sessional lecturer

at Baccalaureate University. The annual salary received by Piper stands $25,000. Referring

“sec 6 ITAA 1936”, the salary received by Piper is an earnings from individual efforts

(Braithwaite 2017). Citing “Dean v FCT (1997)” the salary will be taxable as ordinary

income under “sec 6-5, ITAA 1997”.

Gifts that are received out of personal qualities are not viewed as usual earnings under

“sec 6-5, ITAA 1997”. It is necessary to ascertain difference between where the gift is made

and there is a necessary occupational or commercial relation. The judgement denoted in

“Scott v FCT (1966)” held that any receipt from the personal relationship between the parties

cannot be termed as income (Sadiq 2019). Likewise, Piper also received a Woolworths gift

voucher of $500 in respect to the free advice given will not be apprehended as ordinary

earnings. Citing the factual situation of “Scott v FCT (1966)” the voucher that is received by

Piper lacks commercial connection and hence cannot be chargeable as assessable proceeds.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The entertainment expenditure are commonly not allowable as permissible tax

deduction under “sec.8-1, ITAA 1997” unless there is any application of exception. The

definition of entertainment under “sec 32-10, ITAA 1997” widely consist of the food, drink

or recreation (Morgan, Mortimer and Pinto 2018). Piper reports expenses on meal and soft

drink bought from the nearby café that cost her $360. The expenses can be termed as self-

entertainment expenses and hence no permissible income tax deduction is allowed under “sec

8-1, ITAA 1997”.

As noted in “sec.8-1, ITAA 1997” outlays occurred in conventional clothing is not

considered as deductible expenditure because it carries the characteristics of domestic or

personal expenditure. These expenses are considered as the day-to-day living outgoings and

does not has any relation with the process of producing the taxable earnings (Morgan and

Castelyn 2018). As held in “Westcott v FCT (1997)” deduction for clothing is only

acceptable when the clothes are used in the production of income. Piper reports expenses of

$5000 on clothes to maintain a professional image at work. Denoting the factual situation of

“Westcott v FCT (1997)” the expenses occurred on clothing is having the characteristics of

domestic or personal expenditure and no deduction will be permitted under general rules of

“sec.8-1, ITAA 1997”.

Gains that initiates from executing any commercial actions are treated as ordinary

revenues under “sec 6-5, ITAA 1997” while gains originating from non-business activities

are commonly termed as hobby or pleasure activities (Woellner et al. 2016). Such income are

not treated taxable. The most frequent business indicators that are considered by the courts is

the extent of events combined with the type and form of capital or the level of turnover. The

federal court in “JR Walker v FCT (1985)” believed that the small processes might be

treated as commercial business if there are satisfactory other character.

The entertainment expenditure are commonly not allowable as permissible tax

deduction under “sec.8-1, ITAA 1997” unless there is any application of exception. The

definition of entertainment under “sec 32-10, ITAA 1997” widely consist of the food, drink

or recreation (Morgan, Mortimer and Pinto 2018). Piper reports expenses on meal and soft

drink bought from the nearby café that cost her $360. The expenses can be termed as self-

entertainment expenses and hence no permissible income tax deduction is allowed under “sec

8-1, ITAA 1997”.

As noted in “sec.8-1, ITAA 1997” outlays occurred in conventional clothing is not

considered as deductible expenditure because it carries the characteristics of domestic or

personal expenditure. These expenses are considered as the day-to-day living outgoings and

does not has any relation with the process of producing the taxable earnings (Morgan and

Castelyn 2018). As held in “Westcott v FCT (1997)” deduction for clothing is only

acceptable when the clothes are used in the production of income. Piper reports expenses of

$5000 on clothes to maintain a professional image at work. Denoting the factual situation of

“Westcott v FCT (1997)” the expenses occurred on clothing is having the characteristics of

domestic or personal expenditure and no deduction will be permitted under general rules of

“sec.8-1, ITAA 1997”.

Gains that initiates from executing any commercial actions are treated as ordinary

revenues under “sec 6-5, ITAA 1997” while gains originating from non-business activities

are commonly termed as hobby or pleasure activities (Woellner et al. 2016). Such income are

not treated taxable. The most frequent business indicators that are considered by the courts is

the extent of events combined with the type and form of capital or the level of turnover. The

federal court in “JR Walker v FCT (1985)” believed that the small processes might be

treated as commercial business if there are satisfactory other character.

5TAXATION LAW

Piper reports receipts from providing meal during odd occasion to her neighbour for

which she received $25 per meal. The activities were conducted by Piper on four different

occasions during the year. Citing “JR Walker v FCT (1985)” the activities of Piper cannot be

treated as business activity since it does not involve any regularity nor does she employed

any capital (Robin and Barkoczy 2019). Therefore, the receipts can be termed as purely a

hobby or pleasure and it is non-taxable as ordinary income. A deduction relating to the

depreciating asset is usually allowed under “sec 40.25 (2)” up to its attributable use for a

purpose apart from taxable purpose. Similarly, Piper can claim the deduction under “sec

40.25 (2)” for depreciation of printer up to two-third portion that is attributable to her taxable

purpose.

Deductions are available under “sec 8-1” for the common outgoings experienced in

self-education purpose that relates to the present career of the taxpayer (Bankman et al.

2018). There should also be an adequate connection associated to the making of the

taxpayer’s chargeable proceeds when the self-education costs are experienced. The decision

of the federal court in “FCT v Hatchett (1971)” outgoings incurred for self-education

purpose to earn higher income in the existent occupation of the taxpayer was allowed for

deduction. Similarly, the self-education outlays sustained on course fee of master degree in

law will be permitted deduction. She also reported payment of fees in respect of her

practicing certificate. Citing the “FCT v Hatchett (1971)” the expenses incurred by Piper is

mainly to improve her earnings in the current career and hence it will be allowable as

deduction with “sec 8-1, ITAA 1997”.

The travel payments that is associated to the self-education may be considered as

deductible expenditure when the travel is associated to the source of chargeable revenues The

verdict cited in “FCT v Finn (1961)” held that travel expense incurred in self-education is

permitted for deduction when the travel was completely devoted to the improvement of future

Piper reports receipts from providing meal during odd occasion to her neighbour for

which she received $25 per meal. The activities were conducted by Piper on four different

occasions during the year. Citing “JR Walker v FCT (1985)” the activities of Piper cannot be

treated as business activity since it does not involve any regularity nor does she employed

any capital (Robin and Barkoczy 2019). Therefore, the receipts can be termed as purely a

hobby or pleasure and it is non-taxable as ordinary income. A deduction relating to the

depreciating asset is usually allowed under “sec 40.25 (2)” up to its attributable use for a

purpose apart from taxable purpose. Similarly, Piper can claim the deduction under “sec

40.25 (2)” for depreciation of printer up to two-third portion that is attributable to her taxable

purpose.

Deductions are available under “sec 8-1” for the common outgoings experienced in

self-education purpose that relates to the present career of the taxpayer (Bankman et al.

2018). There should also be an adequate connection associated to the making of the

taxpayer’s chargeable proceeds when the self-education costs are experienced. The decision

of the federal court in “FCT v Hatchett (1971)” outgoings incurred for self-education

purpose to earn higher income in the existent occupation of the taxpayer was allowed for

deduction. Similarly, the self-education outlays sustained on course fee of master degree in

law will be permitted deduction. She also reported payment of fees in respect of her

practicing certificate. Citing the “FCT v Hatchett (1971)” the expenses incurred by Piper is

mainly to improve her earnings in the current career and hence it will be allowable as

deduction with “sec 8-1, ITAA 1997”.

The travel payments that is associated to the self-education may be considered as

deductible expenditure when the travel is associated to the source of chargeable revenues The

verdict cited in “FCT v Finn (1961)” held that travel expense incurred in self-education is

permitted for deduction when the travel was completely devoted to the improvement of future

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

earnings and career opportunities (Kenny, Blissenden and Villios 2018). The travel expenses

of $672 is viewed as an admissible deduction in case of Piper. Citing “FCT v Finn (1961)”

the travel was completely devoted to the improvement of future earnings and career

opportunities of Piper. While the expenses on books incurred by Piper are permitted as tax

deduction under “sec 8-1, ITAA 1997”.

Answer to question 2:

Computation of Income Tax Liability

In the books of David

For the year ended 2018/19

Particulars Amount ($) Amount ($)

Assessable Income

Income from Salaries - BU University $ 60,000

Total Assessable Income $ 60,000

Allowable deductions Nil

Total Taxable Income $ 60,000

Tax on Taxable income 11047

Add: Medicare Levy $ 1,200

Less: PayG Withheld from BU $ 10,500

Less: LIMO 100

Less: LMITO 1080

Add: Excess of private insurance rebate $ 1,000

Total Tax Payable $ 1,567

Answer to question 3:

Superannuation is regarded as the money a person puts aside during their working life

for use by them during retirement period. Under the Australian taxation law, any amounts

that is withdrawn from the foreign super funds may be considered as the subject of tax. A

taxpayer may also be subjected to other obligations in the foreign nation (McCouat, 2018).

Based on the rules of the overseas super fund, a taxpayer might be allowed to transfer the

earnings and career opportunities (Kenny, Blissenden and Villios 2018). The travel expenses

of $672 is viewed as an admissible deduction in case of Piper. Citing “FCT v Finn (1961)”

the travel was completely devoted to the improvement of future earnings and career

opportunities of Piper. While the expenses on books incurred by Piper are permitted as tax

deduction under “sec 8-1, ITAA 1997”.

Answer to question 2:

Computation of Income Tax Liability

In the books of David

For the year ended 2018/19

Particulars Amount ($) Amount ($)

Assessable Income

Income from Salaries - BU University $ 60,000

Total Assessable Income $ 60,000

Allowable deductions Nil

Total Taxable Income $ 60,000

Tax on Taxable income 11047

Add: Medicare Levy $ 1,200

Less: PayG Withheld from BU $ 10,500

Less: LIMO 100

Less: LMITO 1080

Add: Excess of private insurance rebate $ 1,000

Total Tax Payable $ 1,567

Answer to question 3:

Superannuation is regarded as the money a person puts aside during their working life

for use by them during retirement period. Under the Australian taxation law, any amounts

that is withdrawn from the foreign super funds may be considered as the subject of tax. A

taxpayer may also be subjected to other obligations in the foreign nation (McCouat, 2018).

Based on the rules of the overseas super fund, a taxpayer might be allowed to transfer the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

amount to either the complying Australian super fund or to themselves. Either the taxpayer or

their super fund might have to pay the income tax on some or all the amount.

If an individual taxpayer transfers the amount to the complying Australian super fund,

the amount would usually be included either or both the contribution caps and the taxpayer

will be required to pay the excess amount of contribution tax. As held in the case of

“Moneymen Pty Ltd v FCT (1991)” the fixed gross amount received by the taxpayer was

considered as assessable annuity.

If the lump sum amount of foreign super fund is paid to the taxpayer, then the taxable

range of the imbursement and any kind of related funds should be contained within in the

taxable proceeds of the taxpayer and will be considered taxable based on the marginal rate of

tax. While the remaining part of the transfer would not be considered subjected to income

tax. Any kind of the foreign fund transfer which surpasses the sum that was invested during

the time of transfer might be contained within in their personal taxable income (Sadiq et al.

2018). Additionally, the applicable funds earnings represent the income on the taxpayer

foreign super interest that has accrued from the time when the taxpayer became the

Australian resident.

As evident in the current situation, if the Piper realises the investment of the

retirement annuity and transfers the cash in her Australian bank account then the lump sum

from the foreign super fund will be considered taxable as income relating to the payment. By

denoting the judgement made in “Moneymen Pty Ltd v FCT (1991)” the applicable amount

of funds earnings will be included in Piper’s taxable income and will be taxed based on the

marginal rate.

amount to either the complying Australian super fund or to themselves. Either the taxpayer or

their super fund might have to pay the income tax on some or all the amount.

If an individual taxpayer transfers the amount to the complying Australian super fund,

the amount would usually be included either or both the contribution caps and the taxpayer

will be required to pay the excess amount of contribution tax. As held in the case of

“Moneymen Pty Ltd v FCT (1991)” the fixed gross amount received by the taxpayer was

considered as assessable annuity.

If the lump sum amount of foreign super fund is paid to the taxpayer, then the taxable

range of the imbursement and any kind of related funds should be contained within in the

taxable proceeds of the taxpayer and will be considered taxable based on the marginal rate of

tax. While the remaining part of the transfer would not be considered subjected to income

tax. Any kind of the foreign fund transfer which surpasses the sum that was invested during

the time of transfer might be contained within in their personal taxable income (Sadiq et al.

2018). Additionally, the applicable funds earnings represent the income on the taxpayer

foreign super interest that has accrued from the time when the taxpayer became the

Australian resident.

As evident in the current situation, if the Piper realises the investment of the

retirement annuity and transfers the cash in her Australian bank account then the lump sum

from the foreign super fund will be considered taxable as income relating to the payment. By

denoting the judgement made in “Moneymen Pty Ltd v FCT (1991)” the applicable amount

of funds earnings will be included in Piper’s taxable income and will be taxed based on the

marginal rate.

8TAXATION LAW

To lower the tax liability of Piper from the retirement fund withdrawal, piper can use

the re-contribution strategy which can be useful in lowering the tax. The number of areas

where the strategy of re-contribution can be employed in case of Piper is given below;

Estate planning:

Piper can use the re-distribution strategy to lower her assessable component of their

retirement fund benefit by considering a non-tax dependent. This can be done by vesting the

funds on non-dependents that are below the age of 18 as they do not have to pay tax.

Tax Planning:

As piper is below the age of 60 years she can start making the use of money in her

super account to pay the income stream when she retires, the chargeable component of the

income stream would be taxed on the basis of marginal tax rate less a 15% tax offset (Taylor

et al. 2018). The tax free portion will be paid to her and by using the re-contribution strategy

the can simply convert their chargeable component in the tax free component as this will help

in lowering her tax bill.

Answer to question 4:

Commonly a person is allowed with the entitlement to obtain the deduction for the

cost of attending the seminars, sessions and education related workshops which has adequate

relation with an individual taxpayers working activities. This can also take into the account

the recognised training course expenses that is provided by the specialised associations. If

attending a conferences consist of travel, a taxpayer may is under obligation of showing that

they have lowered their claim to eliminate the personal part of expenses for any tour (Sadiq et

al. 2018). An individual taxpayer is permitted to claim the deduction for the self-education

expenditure if their self-education is connected to their present work activities as the

employee or if they get a taxable bonded scholarship. The decision handed in “FCT v

To lower the tax liability of Piper from the retirement fund withdrawal, piper can use

the re-contribution strategy which can be useful in lowering the tax. The number of areas

where the strategy of re-contribution can be employed in case of Piper is given below;

Estate planning:

Piper can use the re-distribution strategy to lower her assessable component of their

retirement fund benefit by considering a non-tax dependent. This can be done by vesting the

funds on non-dependents that are below the age of 18 as they do not have to pay tax.

Tax Planning:

As piper is below the age of 60 years she can start making the use of money in her

super account to pay the income stream when she retires, the chargeable component of the

income stream would be taxed on the basis of marginal tax rate less a 15% tax offset (Taylor

et al. 2018). The tax free portion will be paid to her and by using the re-contribution strategy

the can simply convert their chargeable component in the tax free component as this will help

in lowering her tax bill.

Answer to question 4:

Commonly a person is allowed with the entitlement to obtain the deduction for the

cost of attending the seminars, sessions and education related workshops which has adequate

relation with an individual taxpayers working activities. This can also take into the account

the recognised training course expenses that is provided by the specialised associations. If

attending a conferences consist of travel, a taxpayer may is under obligation of showing that

they have lowered their claim to eliminate the personal part of expenses for any tour (Sadiq et

al. 2018). An individual taxpayer is permitted to claim the deduction for the self-education

expenditure if their self-education is connected to their present work activities as the

employee or if they get a taxable bonded scholarship. The decision handed in “FCT v

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Hatchett (1971)” stated that a taxpayer was given the permission of claiming the self-

education expenditure that were incurred in earning the higher income that were incurred in

the current career.

Deductions can be permitted by the taxpayer throughout the financial year in which

the expenses are occurred. Usually, a taxpayer is permitted to obtain entitlement relating to

the tax deductions for the seminars, sessions and training workshops that is associated to their

work (Kenny et al. 2018). The taxpayer must have incurred the expenses by themselves and

were not reimbursed, it should also directly relate to the revenue making activities of the

taxpayer and the taxpayer is also required to have the records to prove it.

As obvious in the existing situation of Piper is planning to attend the conference in

relation to her studies. Citing the example of “FCT v Hatchett (1971)” the self-education

expenses that Piper is looking forward to claim is associated to her current career in which

she is presently employed. The conference will be held in the 1st September 2019 in Berlin.

As piper is planning to claim the expenses in the current year it can be stated she is only

allowed to claim the expenses in the year in which the expenses will occur. Therefore, in the

current income year this expenses cannot be claimed by Piper but can be subsequently

permissible to claim in the next income year of 2019-20.

Hatchett (1971)” stated that a taxpayer was given the permission of claiming the self-

education expenditure that were incurred in earning the higher income that were incurred in

the current career.

Deductions can be permitted by the taxpayer throughout the financial year in which

the expenses are occurred. Usually, a taxpayer is permitted to obtain entitlement relating to

the tax deductions for the seminars, sessions and training workshops that is associated to their

work (Kenny et al. 2018). The taxpayer must have incurred the expenses by themselves and

were not reimbursed, it should also directly relate to the revenue making activities of the

taxpayer and the taxpayer is also required to have the records to prove it.

As obvious in the existing situation of Piper is planning to attend the conference in

relation to her studies. Citing the example of “FCT v Hatchett (1971)” the self-education

expenses that Piper is looking forward to claim is associated to her current career in which

she is presently employed. The conference will be held in the 1st September 2019 in Berlin.

As piper is planning to claim the expenses in the current year it can be stated she is only

allowed to claim the expenses in the year in which the expenses will occur. Therefore, in the

current income year this expenses cannot be claimed by Piper but can be subsequently

permissible to claim in the next income year of 2019-20.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

McCouat, P. (2018). Australian master GST guide 2018. North Ryde: CCH Australia,

Limited.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Robin and Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.), 2019. Australian

Taxation Law Select 2019: Legislation And Commentary. Oxford University Press.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Taylor, C., Walpole, M., Burton, M., Ciro, T. and Murray, I. 2018. Understanding taxation

law.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

McCouat, P. (2018). Australian master GST guide 2018. North Ryde: CCH Australia,

Limited.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Robin and Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.), 2019. Australian

Taxation Law Select 2019: Legislation And Commentary. Oxford University Press.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Taylor, C., Walpole, M., Burton, M., Ciro, T. and Murray, I. 2018. Understanding taxation

law.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

11TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.