Taxation Law: Comprehensive Analysis of Bruce Lee's Income Tax, TAX305

VerifiedAdded on 2023/06/07

|10

|2559

|364

Case Study

AI Summary

This case study provides a comprehensive analysis of Bruce Lee's income tax situation for the year ended 30 June 2018. It identifies and assesses various sources of assessable income, including professional legal fees, salary from part-time lecturing, interest income, rental income, and dividend income. The study also examines allowable deductions such as office rent, cleaning contractor payments, employee salary, and expenses related to the investment property, along with specific deductions like tax agent fees and the cost of replacing storm-damaged roof tiles. Ultimately, the study computes Bruce Lee's taxable income, tax liability, Medicare levy, and any applicable surcharges, while also considering carry-forward losses and franking credits, leading to a final determination of the total tax payable for the year. Desklib offers similar solved assignments and past papers for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Assessment 2:.............................................................................................................................2

Answer to question 1:.................................................................................................................2

References:.................................................................................................................................8

Table of Contents

Assessment 2:.............................................................................................................................2

Answer to question 1:.................................................................................................................2

References:.................................................................................................................................8

2TAXATION LAW

Assessment 2:

Answer to question 1:

An individual’s assessable income is subjected to income tax since it is added into the

taxable income. Income according to the ordinary concepts is taxable under “section 6-5

ITAA 1997”. The court in “Scott v CT (1935)” held that income should be interpreted in

terms of the ordinary concepts of mankind. Gains originating from business is an ordinary

income under “section 6-5” (Bankman et al. 2017). The case study of Bruce provides that he

carries on the profession of lawyer and receipts a total sum of $340,000 during the year from

his profession. “Section 995-1” provides the legislative definition of business which includes

the profession, trade or employment. With respect to “section 995-1” receipts of legal fees

from the practice of professional lawyer constitutes business receipts. The receipts are

assessable according to the ordinary concepts of “section 6-5 ITAA 1997”.

“Section 6-20 of the ITAA 1997” explains that there is certain income that are

exempted from taxation (Murphy and Higgins 2016). A receipt of $8,000 was reported by

Bruce. The sum is a non-taxable exempted income under “section 6-20”.

The description given in “Section 44 (1)” held that dividends obtained by taxpayer

from the listed companies are required to be declared in taxable income (Buenker 2018).

Bruce earned a fully franked dividend income of $7,000 from the Australian resident

company. Denoting the description of “section 44 (1)” Bruce must include the dividend

income in his assessment for taxable purpose while the franking credits that is attached to it

can be allowed for claiming tax offset.

An item having the character of income which is derived will be regarded as income

up to the amount of the realisable value. The Australian taxation office requires a taxpayer to

include in their taxable earnings the interest obtained from the financial institutions such as

Assessment 2:

Answer to question 1:

An individual’s assessable income is subjected to income tax since it is added into the

taxable income. Income according to the ordinary concepts is taxable under “section 6-5

ITAA 1997”. The court in “Scott v CT (1935)” held that income should be interpreted in

terms of the ordinary concepts of mankind. Gains originating from business is an ordinary

income under “section 6-5” (Bankman et al. 2017). The case study of Bruce provides that he

carries on the profession of lawyer and receipts a total sum of $340,000 during the year from

his profession. “Section 995-1” provides the legislative definition of business which includes

the profession, trade or employment. With respect to “section 995-1” receipts of legal fees

from the practice of professional lawyer constitutes business receipts. The receipts are

assessable according to the ordinary concepts of “section 6-5 ITAA 1997”.

“Section 6-20 of the ITAA 1997” explains that there is certain income that are

exempted from taxation (Murphy and Higgins 2016). A receipt of $8,000 was reported by

Bruce. The sum is a non-taxable exempted income under “section 6-20”.

The description given in “Section 44 (1)” held that dividends obtained by taxpayer

from the listed companies are required to be declared in taxable income (Buenker 2018).

Bruce earned a fully franked dividend income of $7,000 from the Australian resident

company. Denoting the description of “section 44 (1)” Bruce must include the dividend

income in his assessment for taxable purpose while the franking credits that is attached to it

can be allowed for claiming tax offset.

An item having the character of income which is derived will be regarded as income

up to the amount of the realisable value. The Australian taxation office requires a taxpayer to

include in their taxable earnings the interest obtained from the financial institutions such as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

bank deposits or term deposits (Woellner et al. 2016). Those interest receipts constitute

ordinary income under “section 6-5” and attracts tax liability. The receipt of $5,000 as the

interest income from bank deposits by Bruce would be treated as ordinary income and would

be considered liable for taxation.

Receipts that are obtained from employment and offering personal services might be

subjected to income tax for an employee. Employment income may be paid directly in the

bank account of an individual or in any alternative way. Notwithstanding of the fact that

whether a person has one or greater than one employment or whether the person is employed

in the full or part time employment (Robin 2017). Income received from the employment

would be considered for taxation. “Section 6-1 of the ITAA 1936” held that amount that are

obtained from the personal exertion might be considered for assessment as either statutory or

ordinary income. The receipt of salary by Bruce from the part time lecture in the university

would be considered for assessment under “section 6-1” as the income from the employment.

Receipts of rent is regarded as ordinary income since under the flow concept, the rent

flows from the investment in the property. The judgment of court in “FC of T v Blake

(1984)” held that regular receipts are held as income in nature. Bruce earned a rental income

of $10,000 from the investment property (Maley 2018). Under the ordinary concepts of

“section 6-5” the rental income from investment property would be held taxable.

The two positive limbs of “section 8-1” allow the taxpayer to deduct from their

taxable income the losses or outgoings till the extent that it is occurred in producing the

taxable income or it is incurred necessarily in performing business activities for gaining the

taxable income (Blakelock and King 2017). While the negative limbs of “section 8-1 (2)”

disallows a person to deduct outgoings if they are capital in nature or the expenses are private

or domestic in nature.

bank deposits or term deposits (Woellner et al. 2016). Those interest receipts constitute

ordinary income under “section 6-5” and attracts tax liability. The receipt of $5,000 as the

interest income from bank deposits by Bruce would be treated as ordinary income and would

be considered liable for taxation.

Receipts that are obtained from employment and offering personal services might be

subjected to income tax for an employee. Employment income may be paid directly in the

bank account of an individual or in any alternative way. Notwithstanding of the fact that

whether a person has one or greater than one employment or whether the person is employed

in the full or part time employment (Robin 2017). Income received from the employment

would be considered for taxation. “Section 6-1 of the ITAA 1936” held that amount that are

obtained from the personal exertion might be considered for assessment as either statutory or

ordinary income. The receipt of salary by Bruce from the part time lecture in the university

would be considered for assessment under “section 6-1” as the income from the employment.

Receipts of rent is regarded as ordinary income since under the flow concept, the rent

flows from the investment in the property. The judgment of court in “FC of T v Blake

(1984)” held that regular receipts are held as income in nature. Bruce earned a rental income

of $10,000 from the investment property (Maley 2018). Under the ordinary concepts of

“section 6-5” the rental income from investment property would be held taxable.

The two positive limbs of “section 8-1” allow the taxpayer to deduct from their

taxable income the losses or outgoings till the extent that it is occurred in producing the

taxable income or it is incurred necessarily in performing business activities for gaining the

taxable income (Blakelock and King 2017). While the negative limbs of “section 8-1 (2)”

disallows a person to deduct outgoings if they are capital in nature or the expenses are private

or domestic in nature.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Bruce reported an expenditure of office rent, cleaning contractor and salary of

employee during the year. According to judgment noted in “Amalgamated Zinc (De

Bavay’s) Ltd v FCT (1935)” expenditure occurred for gaining or producing the taxable

income or in the course of producing the taxable income will be considered allowable

deduction under the general provision of “section 8-1” (Miller and Oats 2016). Cost of office

rent, cleaning contractor and payment of employee salary would be held as allowable as

general deduction. This is because these expenses are incurred in course of producing the

taxable income for Bruce and qualifies under the positive limbs of “section 8-1 of the ITAA

1997”.

The description of Australian Taxation Office includes that purchase of business

tools, equipment or any alternative assets for obtaining business income will be allowed as

deductions for the entire costs of the tool or the partial cost. The form of deduction that is

allowed to a taxpayer is reliant on the asset cost (Lang 2014). Where any tools or equipment

that does not forms the part of the any set or cost base of the asset is less than $300 then a

deduction for the same can be claimed for the same immediately. A calculator was purchased

by Bruce for business purpose having a cost base of $290. Since the cost of asset is less than

$300, Bruce can immediately claim deduction for the calculator.

The Australian taxation office explains that cost that is occurred on the food and

entertainment of business clients are held as business expenditure and deduction for the same

can be claimed by the taxpayer (Burton 2017). Bruce incurs cost on food and meal for one of

his business client. Since the expenses are for business purpose therefore, a deduction can be

claimed in this respect. Conversely, Bruce reported the expenses on food and meal for

himself as well. Referring to “section 8-1 of the ITAA 1997” Bruce will not be allowed

claim deduction for food and drinks expenses upon himself as this constitute a private

expense.

Bruce reported an expenditure of office rent, cleaning contractor and salary of

employee during the year. According to judgment noted in “Amalgamated Zinc (De

Bavay’s) Ltd v FCT (1935)” expenditure occurred for gaining or producing the taxable

income or in the course of producing the taxable income will be considered allowable

deduction under the general provision of “section 8-1” (Miller and Oats 2016). Cost of office

rent, cleaning contractor and payment of employee salary would be held as allowable as

general deduction. This is because these expenses are incurred in course of producing the

taxable income for Bruce and qualifies under the positive limbs of “section 8-1 of the ITAA

1997”.

The description of Australian Taxation Office includes that purchase of business

tools, equipment or any alternative assets for obtaining business income will be allowed as

deductions for the entire costs of the tool or the partial cost. The form of deduction that is

allowed to a taxpayer is reliant on the asset cost (Lang 2014). Where any tools or equipment

that does not forms the part of the any set or cost base of the asset is less than $300 then a

deduction for the same can be claimed for the same immediately. A calculator was purchased

by Bruce for business purpose having a cost base of $290. Since the cost of asset is less than

$300, Bruce can immediately claim deduction for the calculator.

The Australian taxation office explains that cost that is occurred on the food and

entertainment of business clients are held as business expenditure and deduction for the same

can be claimed by the taxpayer (Burton 2017). Bruce incurs cost on food and meal for one of

his business client. Since the expenses are for business purpose therefore, a deduction can be

claimed in this respect. Conversely, Bruce reported the expenses on food and meal for

himself as well. Referring to “section 8-1 of the ITAA 1997” Bruce will not be allowed

claim deduction for food and drinks expenses upon himself as this constitute a private

expense.

5TAXATION LAW

The court in “Lunney v FCT (1958)” held that the travel between home and an

individual workplace is usually not allowed for deductions. A taxpayer is allowed deduction

under “section 25-100 of the ITAA 1997” for the travelling costs between the workplace.

The court in “Payne v FCT (2001)” disallowed the taxpayer to claim deduction for the cost

incurred in travelling between his home and workplace (Jones 2017). Travel between two

unrelated workplaces is non-deductible under “section 8-1”. The travelling cost of $1,200

would not be allowed for deduction under “section 8-1” since it constitute travel amid two

unrelated workplaces by Bruce.

Any loss or outgoing that are private or domestic in character might not be held as

deductible expenditure because these expenses does not meet the principles of positive limbs

or the same is not allowed as deduction under the second negative limb of “section 8-1 (2)

(b)” (Somers and Eynaud 2015). An expense of 2,200 on family home and 900 for electricity

was incurred by Bruce during the year. Bruce cannot claim an allowable deduction since

these expenses are private or domestic in nature and the same is not permissible as deduction

under the second negative limb of “section 8-1 (2) (b)”.

“Section 8-5” states that a taxpayer is allowed to claim deduction of specific nature

when the specific provision of the legislation permits the deduction to the taxpayer. “Section

25-5” enable an individual taxpayer to claim deduction for certain costs together with the

expenditure incurred in managing the tax affairs (Barrett and Elsayed 2014). A tax agent fee

of $1,000 for preparing the tax return was reported by Bruce during the year. Bruce can claim

deduction for the same under “section 25-5 of the ITAA 1997”.

When a taxpayer sub-lets the rental property for deriving assessable income, expenses

incurred in gaining the taxable income from that property would be allowed for deductions.

Nevertheless, expenditure of private or capital nature is non-deductible. Citing the case of

The court in “Lunney v FCT (1958)” held that the travel between home and an

individual workplace is usually not allowed for deductions. A taxpayer is allowed deduction

under “section 25-100 of the ITAA 1997” for the travelling costs between the workplace.

The court in “Payne v FCT (2001)” disallowed the taxpayer to claim deduction for the cost

incurred in travelling between his home and workplace (Jones 2017). Travel between two

unrelated workplaces is non-deductible under “section 8-1”. The travelling cost of $1,200

would not be allowed for deduction under “section 8-1” since it constitute travel amid two

unrelated workplaces by Bruce.

Any loss or outgoing that are private or domestic in character might not be held as

deductible expenditure because these expenses does not meet the principles of positive limbs

or the same is not allowed as deduction under the second negative limb of “section 8-1 (2)

(b)” (Somers and Eynaud 2015). An expense of 2,200 on family home and 900 for electricity

was incurred by Bruce during the year. Bruce cannot claim an allowable deduction since

these expenses are private or domestic in nature and the same is not permissible as deduction

under the second negative limb of “section 8-1 (2) (b)”.

“Section 8-5” states that a taxpayer is allowed to claim deduction of specific nature

when the specific provision of the legislation permits the deduction to the taxpayer. “Section

25-5” enable an individual taxpayer to claim deduction for certain costs together with the

expenditure incurred in managing the tax affairs (Barrett and Elsayed 2014). A tax agent fee

of $1,000 for preparing the tax return was reported by Bruce during the year. Bruce can claim

deduction for the same under “section 25-5 of the ITAA 1997”.

When a taxpayer sub-lets the rental property for deriving assessable income, expenses

incurred in gaining the taxable income from that property would be allowed for deductions.

Nevertheless, expenditure of private or capital nature is non-deductible. Citing the case of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

“Amalgamated Zinc Ltd v FCT (1935)” expenditure that carries adequate relation between

the outgoings and losses or occurred in producing the taxable income is allowed for

deductions (Walsh 2018). The loan interest expense and rates on rental property would be

allowed for deduction under “section 8-1” since it was occurred in producing rental income.

While acquiring investment property notional repairs of capital nature are not allowed

for deduction under “section 25-10 (3)”. The court in “Inland Revenue Commissioners v

Shipping Co Ltd (1923)” disallowed the taxpayer from claiming initial repair deduction on

the investment property since it was capital in nature (Woellner et al. 2016). Bruce reports a

cost of $5,000 for repainting the property soon after acquisition and the same is non-

allowable deduction under “section 25-10 (3)”.

A deduction is allowed to taxpayer under “section 25-10” for damage on the

investment property originating from storm. Bruce incurs an expense of $1,000 for replacing

the tiles of roof on investment property that was damaged by storm. Under “section 25-10”

the expense is eligible for deductions.

Improvement that surpasses the repair such as changes in the character of original

item are capital in nature. In “FCT v Western Suburbs Cinemas Ltd (1952)” a deduction was

denied to taxpayer for repairing the ceiling with new material since it was not a repair (Robin

2017). Similarly, the expenses incurred by Bruce in extending the bathroom of investment

property is work carried on of significant nature and not allowed for deduction under

“section 25-10”.

“Amalgamated Zinc Ltd v FCT (1935)” expenditure that carries adequate relation between

the outgoings and losses or occurred in producing the taxable income is allowed for

deductions (Walsh 2018). The loan interest expense and rates on rental property would be

allowed for deduction under “section 8-1” since it was occurred in producing rental income.

While acquiring investment property notional repairs of capital nature are not allowed

for deduction under “section 25-10 (3)”. The court in “Inland Revenue Commissioners v

Shipping Co Ltd (1923)” disallowed the taxpayer from claiming initial repair deduction on

the investment property since it was capital in nature (Woellner et al. 2016). Bruce reports a

cost of $5,000 for repainting the property soon after acquisition and the same is non-

allowable deduction under “section 25-10 (3)”.

A deduction is allowed to taxpayer under “section 25-10” for damage on the

investment property originating from storm. Bruce incurs an expense of $1,000 for replacing

the tiles of roof on investment property that was damaged by storm. Under “section 25-10”

the expense is eligible for deductions.

Improvement that surpasses the repair such as changes in the character of original

item are capital in nature. In “FCT v Western Suburbs Cinemas Ltd (1952)” a deduction was

denied to taxpayer for repairing the ceiling with new material since it was not a repair (Robin

2017). Similarly, the expenses incurred by Bruce in extending the bathroom of investment

property is work carried on of significant nature and not allowed for deduction under

“section 25-10”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

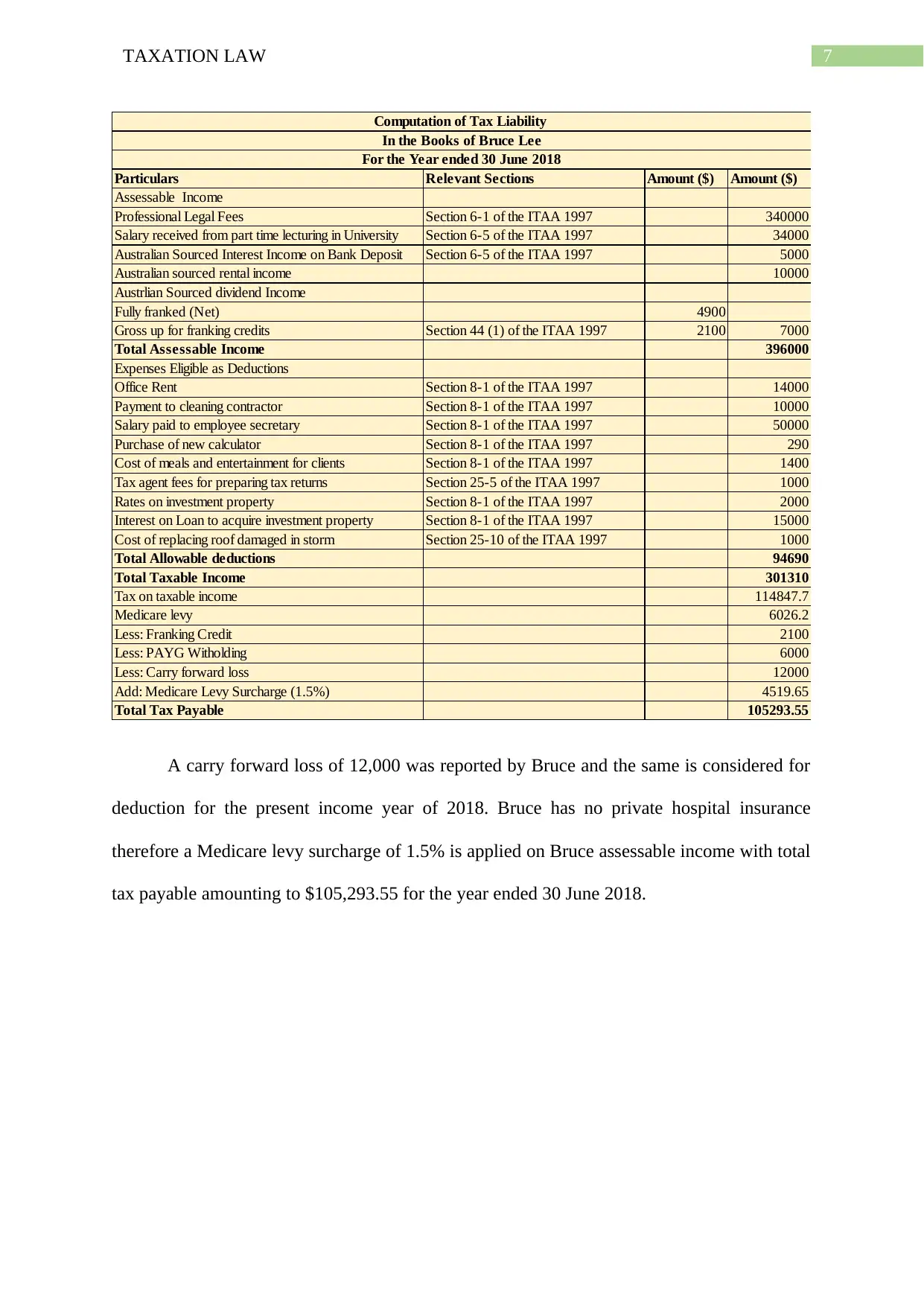

Particulars Relevant Sections Amount ($) Amount ($)

Assessable Income

Professional Legal Fees Section 6-1 of the ITAA 1997 340000

Salary received from part time lecturing in University Section 6-5 of the ITAA 1997 34000

Australian Sourced Interest Income on Bank Deposit Section 6-5 of the ITAA 1997 5000

Australian sourced rental income 10000

Austrlian Sourced dividend Income

Fully franked (Net) 4900

Gross up for franking credits Section 44 (1) of the ITAA 1997 2100 7000

Total Assessable Income 396000

Expenses Eligible as Deductions

Office Rent Section 8-1 of the ITAA 1997 14000

Payment to cleaning contractor Section 8-1 of the ITAA 1997 10000

Salary paid to employee secretary Section 8-1 of the ITAA 1997 50000

Purchase of new calculator Section 8-1 of the ITAA 1997 290

Cost of meals and entertainment for clients Section 8-1 of the ITAA 1997 1400

Tax agent fees for preparing tax returns Section 25-5 of the ITAA 1997 1000

Rates on investment property Section 8-1 of the ITAA 1997 2000

Interest on Loan to acquire investment property Section 8-1 of the ITAA 1997 15000

Cost of replacing roof damaged in storm Section 25-10 of the ITAA 1997 1000

Total Allowable deductions 94690

Total Taxable Income 301310

Tax on taxable income 114847.7

Medicare levy 6026.2

Less: Franking Credit 2100

Less: PAYG Witholding 6000

Less: Carry forward loss 12000

Add: Medicare Levy Surcharge (1.5%) 4519.65

Total Tax Payable 105293.55

Computation of Tax Liability

In the Books of Bruce Lee

For the Year ended 30 June 2018

A carry forward loss of 12,000 was reported by Bruce and the same is considered for

deduction for the present income year of 2018. Bruce has no private hospital insurance

therefore a Medicare levy surcharge of 1.5% is applied on Bruce assessable income with total

tax payable amounting to $105,293.55 for the year ended 30 June 2018.

Particulars Relevant Sections Amount ($) Amount ($)

Assessable Income

Professional Legal Fees Section 6-1 of the ITAA 1997 340000

Salary received from part time lecturing in University Section 6-5 of the ITAA 1997 34000

Australian Sourced Interest Income on Bank Deposit Section 6-5 of the ITAA 1997 5000

Australian sourced rental income 10000

Austrlian Sourced dividend Income

Fully franked (Net) 4900

Gross up for franking credits Section 44 (1) of the ITAA 1997 2100 7000

Total Assessable Income 396000

Expenses Eligible as Deductions

Office Rent Section 8-1 of the ITAA 1997 14000

Payment to cleaning contractor Section 8-1 of the ITAA 1997 10000

Salary paid to employee secretary Section 8-1 of the ITAA 1997 50000

Purchase of new calculator Section 8-1 of the ITAA 1997 290

Cost of meals and entertainment for clients Section 8-1 of the ITAA 1997 1400

Tax agent fees for preparing tax returns Section 25-5 of the ITAA 1997 1000

Rates on investment property Section 8-1 of the ITAA 1997 2000

Interest on Loan to acquire investment property Section 8-1 of the ITAA 1997 15000

Cost of replacing roof damaged in storm Section 25-10 of the ITAA 1997 1000

Total Allowable deductions 94690

Total Taxable Income 301310

Tax on taxable income 114847.7

Medicare levy 6026.2

Less: Franking Credit 2100

Less: PAYG Witholding 6000

Less: Carry forward loss 12000

Add: Medicare Levy Surcharge (1.5%) 4519.65

Total Tax Payable 105293.55

Computation of Tax Liability

In the Books of Bruce Lee

For the Year ended 30 June 2018

A carry forward loss of 12,000 was reported by Bruce and the same is considered for

deduction for the present income year of 2018. Bruce has no private hospital insurance

therefore a Medicare levy surcharge of 1.5% is applied on Bruce assessable income with total

tax payable amounting to $105,293.55 for the year ended 30 June 2018.

8TAXATION LAW

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Barrett, J. and Elsayed, A., 2014. Deductibility of employer contributions to employee

remuneration trusts-where are we at?. Governance Directions, 66(5), p.307.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Jones, D., 2017. Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Maley, M.N., 2018. Australian Taxation Office Guidance on the Diverted Profits Tax.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

Somers, R. and Eynaud, A., 2015. A matter of trusts: The ATO's proposed treatment of

unpaid present entitlements: Part 1. Taxation in Australia, 50(2), p.90.

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Barrett, J. and Elsayed, A., 2014. Deductibility of employer contributions to employee

remuneration trusts-where are we at?. Governance Directions, 66(5), p.307.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Jones, D., 2017. Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Maley, M.N., 2018. Australian Taxation Office Guidance on the Diverted Profits Tax.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

Somers, R. and Eynaud, A., 2015. A matter of trusts: The ATO's proposed treatment of

unpaid present entitlements: Part 1. Taxation in Australia, 50(2), p.90.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Walsh, M., 2018. Tax deeds. Tax Specialist, 21(5), p.211.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Walsh, M., 2018. Tax deeds. Tax Specialist, 21(5), p.211.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.