Taxation Law Assignment - Problem Solving & Analysis

VerifiedAdded on 2020/03/23

|9

|2565

|38

Homework Assignment

AI Summary

This document presents a detailed analysis and solutions to a taxation law assignment, addressing various aspects of tax law through case studies. The assignment covers topics such as capital gains tax, analyzing the tax implications of asset sales, and the treatment of personal and collectible assets. It also explores loan fringe benefits, calculating taxable values, and considering statutory interest rates. Furthermore, the assignment delves into joint tenancy agreements, determining profit and loss sharing, and the impact of losses on individual tenants. The case of IRC v Duke of Westminster is discussed, examining the legality of tax minimization strategies. Finally, the document differentiates between revenue and capital receipts, particularly in the context of timber sales and lump-sum payments. The solutions provide a comprehensive understanding of the legal and financial implications of each scenario, offering insights into tax liabilities and accounting practices.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

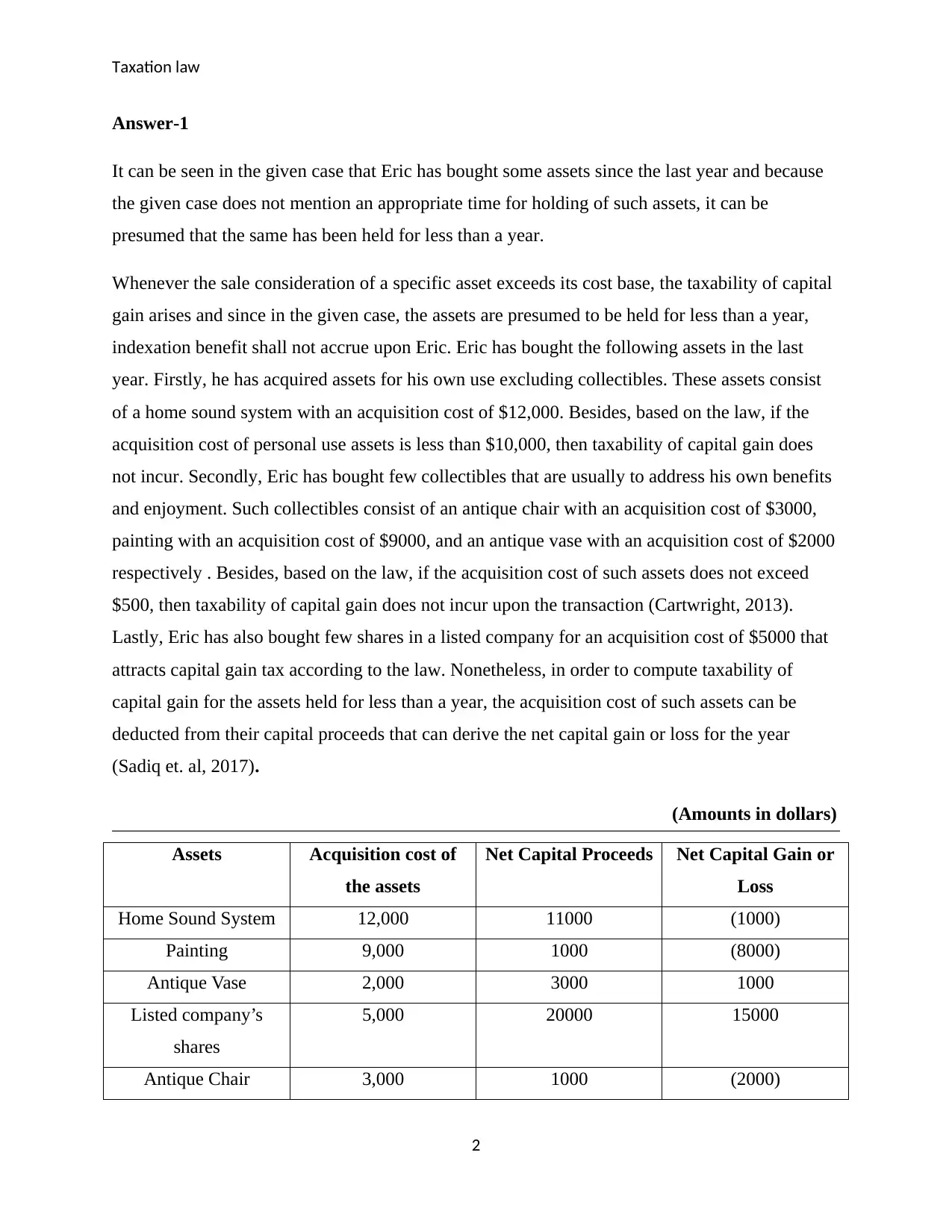

Answer-1

It can be seen in the given case that Eric has bought some assets since the last year and because

the given case does not mention an appropriate time for holding of such assets, it can be

presumed that the same has been held for less than a year.

Whenever the sale consideration of a specific asset exceeds its cost base, the taxability of capital

gain arises and since in the given case, the assets are presumed to be held for less than a year,

indexation benefit shall not accrue upon Eric. Eric has bought the following assets in the last

year. Firstly, he has acquired assets for his own use excluding collectibles. These assets consist

of a home sound system with an acquisition cost of $12,000. Besides, based on the law, if the

acquisition cost of personal use assets is less than $10,000, then taxability of capital gain does

not incur. Secondly, Eric has bought few collectibles that are usually to address his own benefits

and enjoyment. Such collectibles consist of an antique chair with an acquisition cost of $3000,

painting with an acquisition cost of $9000, and an antique vase with an acquisition cost of $2000

respectively . Besides, based on the law, if the acquisition cost of such assets does not exceed

$500, then taxability of capital gain does not incur upon the transaction (Cartwright, 2013).

Lastly, Eric has also bought few shares in a listed company for an acquisition cost of $5000 that

attracts capital gain tax according to the law. Nonetheless, in order to compute taxability of

capital gain for the assets held for less than a year, the acquisition cost of such assets can be

deducted from their capital proceeds that can derive the net capital gain or loss for the year

(Sadiq et. al, 2017).

(Amounts in dollars)

Assets Acquisition cost of

the assets

Net Capital Proceeds Net Capital Gain or

Loss

Home Sound System 12,000 11000 (1000)

Painting 9,000 1000 (8000)

Antique Vase 2,000 3000 1000

Listed company’s

shares

5,000 20000 15000

Antique Chair 3,000 1000 (2000)

2

Answer-1

It can be seen in the given case that Eric has bought some assets since the last year and because

the given case does not mention an appropriate time for holding of such assets, it can be

presumed that the same has been held for less than a year.

Whenever the sale consideration of a specific asset exceeds its cost base, the taxability of capital

gain arises and since in the given case, the assets are presumed to be held for less than a year,

indexation benefit shall not accrue upon Eric. Eric has bought the following assets in the last

year. Firstly, he has acquired assets for his own use excluding collectibles. These assets consist

of a home sound system with an acquisition cost of $12,000. Besides, based on the law, if the

acquisition cost of personal use assets is less than $10,000, then taxability of capital gain does

not incur. Secondly, Eric has bought few collectibles that are usually to address his own benefits

and enjoyment. Such collectibles consist of an antique chair with an acquisition cost of $3000,

painting with an acquisition cost of $9000, and an antique vase with an acquisition cost of $2000

respectively . Besides, based on the law, if the acquisition cost of such assets does not exceed

$500, then taxability of capital gain does not incur upon the transaction (Cartwright, 2013).

Lastly, Eric has also bought few shares in a listed company for an acquisition cost of $5000 that

attracts capital gain tax according to the law. Nonetheless, in order to compute taxability of

capital gain for the assets held for less than a year, the acquisition cost of such assets can be

deducted from their capital proceeds that can derive the net capital gain or loss for the year

(Sadiq et. al, 2017).

(Amounts in dollars)

Assets Acquisition cost of

the assets

Net Capital Proceeds Net Capital Gain or

Loss

Home Sound System 12,000 11000 (1000)

Painting 9,000 1000 (8000)

Antique Vase 2,000 3000 1000

Listed company’s

shares

5,000 20000 15000

Antique Chair 3,000 1000 (2000)

2

Taxation law

Net Capital Gain 5000

Therefore, it can be seen from the above computation that the net capital gain in relation to Eric

comes to $5000 and the same is liable to be paid by him respectively.

In relation to the previously mentioned computation, many points must be taken into account.

Firstly, every personal asset bought by Eric have been purchased at an acquisition cost of more

than $10,000 and that is why they are applicable for taxability of capital gain. Secondly, the

collectibles bought by Eric have also been bought for an acquisition cost of more than $500 and

that is the reason why these are taken into account for computing net capital gain or loss for the

year (Sadiq et. al, 2017). Lastly, the net capital gain of $5000 has been derived by setting off the

capital losses from the capital gain in the particular year.

3

Net Capital Gain 5000

Therefore, it can be seen from the above computation that the net capital gain in relation to Eric

comes to $5000 and the same is liable to be paid by him respectively.

In relation to the previously mentioned computation, many points must be taken into account.

Firstly, every personal asset bought by Eric have been purchased at an acquisition cost of more

than $10,000 and that is why they are applicable for taxability of capital gain. Secondly, the

collectibles bought by Eric have also been bought for an acquisition cost of more than $500 and

that is the reason why these are taken into account for computing net capital gain or loss for the

year (Sadiq et. al, 2017). Lastly, the net capital gain of $5000 has been derived by setting off the

capital losses from the capital gain in the particular year.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

Answer-2

It can be seen from the given case that the employer of Brian has granted him an opportunity to

avail a three-year loan amounting to $1 million at a special rate of interest that must be paid by

him in monthly installments. This criterion is also popularly known as loan fringe benefits

wherein an employer offers loan facility to his employee at a special rate of interest that is lesser

than the statutory interest rates of the market. Further, since the statutory interest is not known in

the given case, it can be presumed that the loan provided on April 1, 2016, with an interest rate

of 5.65% shall be the statutory interest rate of the given loan. Moreover, to compute the

taxability of such loan fringe benefit, various steps can be carried out.

Firstly, the taxable value of such benefit can be computed by excluding the deductible rule. In

relation to this, the actual interest rate of such loan must be subtracted from the statutory rate of

interest on such loan (Barcokzy, 2010). Therefore, the interest as per the actual rate of interest

shall amount to $1000000 * 1% = $10000. Similarly, the interest as per the statutory rate of

interest shall amount to $1000000 * 5.65% that is $56,500 respectively. Thus, the taxable value

shall amount to $56,500 - $10,000 = $46,500

Secondly, Brian must calculate the loan interest as per the statutory interest rate after assuming

that the same was payable in relation to the loan. Therefore, interest as per the statutory rate of

interest shall amount to $10,00,000 x 5.65% = $56,500

Thirdly, it can be observed that around forty percent of the loan has been utilized for settling the

future obligations and other purposes. Therefore, the imaginary amount of tax deductible interest

expense must amount to $56,500 x 40% = $22,600

Fourthly, just like the previously mentioned step, the actual interest amount of the tax deductible

interest expense must amount to $10,000 x 40% = $4000

Fifthly, the actual amount given in the fourth step shall be subtracted from the imaginary amount

in the third step. Therefore, it gives $22,600 - $4000 = $18,600

Lastly, after computing all the above-mentioned requirements, the final taxable figure can be

ascertained by subtracting $18,600 from $46,500 that gives $27,900 respectively.

4

Answer-2

It can be seen from the given case that the employer of Brian has granted him an opportunity to

avail a three-year loan amounting to $1 million at a special rate of interest that must be paid by

him in monthly installments. This criterion is also popularly known as loan fringe benefits

wherein an employer offers loan facility to his employee at a special rate of interest that is lesser

than the statutory interest rates of the market. Further, since the statutory interest is not known in

the given case, it can be presumed that the loan provided on April 1, 2016, with an interest rate

of 5.65% shall be the statutory interest rate of the given loan. Moreover, to compute the

taxability of such loan fringe benefit, various steps can be carried out.

Firstly, the taxable value of such benefit can be computed by excluding the deductible rule. In

relation to this, the actual interest rate of such loan must be subtracted from the statutory rate of

interest on such loan (Barcokzy, 2010). Therefore, the interest as per the actual rate of interest

shall amount to $1000000 * 1% = $10000. Similarly, the interest as per the statutory rate of

interest shall amount to $1000000 * 5.65% that is $56,500 respectively. Thus, the taxable value

shall amount to $56,500 - $10,000 = $46,500

Secondly, Brian must calculate the loan interest as per the statutory interest rate after assuming

that the same was payable in relation to the loan. Therefore, interest as per the statutory rate of

interest shall amount to $10,00,000 x 5.65% = $56,500

Thirdly, it can be observed that around forty percent of the loan has been utilized for settling the

future obligations and other purposes. Therefore, the imaginary amount of tax deductible interest

expense must amount to $56,500 x 40% = $22,600

Fourthly, just like the previously mentioned step, the actual interest amount of the tax deductible

interest expense must amount to $10,000 x 40% = $4000

Fifthly, the actual amount given in the fourth step shall be subtracted from the imaginary amount

in the third step. Therefore, it gives $22,600 - $4000 = $18,600

Lastly, after computing all the above-mentioned requirements, the final taxable figure can be

ascertained by subtracting $18,600 from $46,500 that gives $27,900 respectively.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

After evaluating the previously mentioned steps, it can be stated that if the interest was payable

after termination of the loan in place of payment through monthly installment basis, then the

deemed time of such loan would have been considered from the time when such interest became

payable or would have been paid.

5

After evaluating the previously mentioned steps, it can be stated that if the interest was payable

after termination of the loan in place of payment through monthly installment basis, then the

deemed time of such loan would have been considered from the time when such interest became

payable or would have been paid.

5

Taxation law

Answer-3

An agreement has been entered into between Jack and Jill for the purpose of renting a property,

and they are liable to share the property as joint tenants with no other disputes. Further, Jill is

entitled to 90% share of the profits in relation to the sale of property whereas Jack will be liable

to the remaining amount. Besides, in the event of losses, every loss must be borne by Jack alone

and Jill does not take any responsibility for the same.

Nonetheless, in the given case, it can be observed that a loss of $10,000 had taken place and

based on the agreement, Jack alone is responsible to bear the same. However, he has full right to

set off such losses with his other income so that the net income or loss for the year can be

determined. Similarly, if no gains have accrued to him, he can also carry forward such losses for

the upcoming years (Adams, 2011). Therefore, if Jack and Jill sell the mentioned property in the

given case, it is assured that either gain or loss may incur. In the case of profit from the sale of

such property, the same must be borne by both the tenants in the ratio of 90:10 wherein Jill shall

attain 90% of the profits and Jack shall attain the rest. Besides, Jack can also set off the loss of

$10,000 that have accrued last year in contrast to the profits that may arise from the sale of such

property. Moreover, if there is a loss, Jill will not participate in the same, and Jack shall take

responsibility for the entire amount wherein he can set off the same with other income or carry

forward it to subsequent years.

On a whole, the net outcome is that Jack has the right to set off his past losses with the profits of

the current period so that net income or loss can be determined. Similarly, if by selling the

property, losses are incurred, Jack is entirely responsible for the same and he can utilize his right

to set off or carry forward the same (Thorpe, 2012). Therefore, Jill cannot be affected by any tax

treatment in the provided case.

6

Answer-3

An agreement has been entered into between Jack and Jill for the purpose of renting a property,

and they are liable to share the property as joint tenants with no other disputes. Further, Jill is

entitled to 90% share of the profits in relation to the sale of property whereas Jack will be liable

to the remaining amount. Besides, in the event of losses, every loss must be borne by Jack alone

and Jill does not take any responsibility for the same.

Nonetheless, in the given case, it can be observed that a loss of $10,000 had taken place and

based on the agreement, Jack alone is responsible to bear the same. However, he has full right to

set off such losses with his other income so that the net income or loss for the year can be

determined. Similarly, if no gains have accrued to him, he can also carry forward such losses for

the upcoming years (Adams, 2011). Therefore, if Jack and Jill sell the mentioned property in the

given case, it is assured that either gain or loss may incur. In the case of profit from the sale of

such property, the same must be borne by both the tenants in the ratio of 90:10 wherein Jill shall

attain 90% of the profits and Jack shall attain the rest. Besides, Jack can also set off the loss of

$10,000 that have accrued last year in contrast to the profits that may arise from the sale of such

property. Moreover, if there is a loss, Jill will not participate in the same, and Jack shall take

responsibility for the entire amount wherein he can set off the same with other income or carry

forward it to subsequent years.

On a whole, the net outcome is that Jack has the right to set off his past losses with the profits of

the current period so that net income or loss can be determined. Similarly, if by selling the

property, losses are incurred, Jack is entirely responsible for the same and he can utilize his right

to set off or carry forward the same (Thorpe, 2012). Therefore, Jill cannot be affected by any tax

treatment in the provided case.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

Answer-4

It can be observed from the case of IRC v Duke of Westminster [1936] that an individual has full

right to make use of legal methods in a manner that can allow him or her to minimize his total

income or total tax payable as a whole. Besides, no superior authority has jurisdiction in

restricting him from doing so. However, if lawful methods are not adopted to manage the

accounts, then the authorities have complete jurisdiction to restrict the same and ask for an

increased amount of tax payable by him. Further, the prevalence of authenticated documents in

relation to managing the books of accounts is sufficient to prove that the methods adopted for

decreasing total tax are genuine in nature (Adams, 2011).

Nonetheless, the given case has proved to be of utmost significance until the emergence of other

case laws in relation to accounting and taxation policies. As a result, the perception of people

regarding the previously mentioned case has become distinct in nature. In relation to the current

situation, this case has been of significant importance because it plays a key role in preventing

organizations from influencing relevant details from their books of accounts and allows them to

proceed only with genuine means (Kenny, 2016). This can be illustrated through an example

wherein a business ‘X’ suffering from major losses owing to high debts in the business can make

use of the case law to change its details in the balance sheet or write off its fixed assets to their

carrying values. In simple words, the organization ‘X’ can alter its financials if it is facing major

losses and even if authenticated documents are not shown, the mere transaction of writing off

fixed assets will be enough to validate the same (Goldberg, 2017). Furthermore, if such business

attempts to make use of fraudulent methods to do the same, then the case law plays a vital role in

preventing the same from happening. On a whole, if any transaction or event that can assist an

organization in doing a business efficiently and in a lawful manner, then it is appropriate for the

business and not immoral or illegal.

7

Answer-4

It can be observed from the case of IRC v Duke of Westminster [1936] that an individual has full

right to make use of legal methods in a manner that can allow him or her to minimize his total

income or total tax payable as a whole. Besides, no superior authority has jurisdiction in

restricting him from doing so. However, if lawful methods are not adopted to manage the

accounts, then the authorities have complete jurisdiction to restrict the same and ask for an

increased amount of tax payable by him. Further, the prevalence of authenticated documents in

relation to managing the books of accounts is sufficient to prove that the methods adopted for

decreasing total tax are genuine in nature (Adams, 2011).

Nonetheless, the given case has proved to be of utmost significance until the emergence of other

case laws in relation to accounting and taxation policies. As a result, the perception of people

regarding the previously mentioned case has become distinct in nature. In relation to the current

situation, this case has been of significant importance because it plays a key role in preventing

organizations from influencing relevant details from their books of accounts and allows them to

proceed only with genuine means (Kenny, 2016). This can be illustrated through an example

wherein a business ‘X’ suffering from major losses owing to high debts in the business can make

use of the case law to change its details in the balance sheet or write off its fixed assets to their

carrying values. In simple words, the organization ‘X’ can alter its financials if it is facing major

losses and even if authenticated documents are not shown, the mere transaction of writing off

fixed assets will be enough to validate the same (Goldberg, 2017). Furthermore, if such business

attempts to make use of fraudulent methods to do the same, then the case law plays a vital role in

preventing the same from happening. On a whole, if any transaction or event that can assist an

organization in doing a business efficiently and in a lawful manner, then it is appropriate for the

business and not immoral or illegal.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

Answer-5

It can be seen from the given case that there are various pine trees in a land that is owned by Bill

and in order to graze sheep in the land, Bill has no other option than to cut the trees. If he hires a

logging company to the same, he shall receive $1000 for every 100 meters of timber provided to

them. Since, the given case does not provide relevant information about the total amount of

receipts attained by Bill from the logging company, the same can be regarded as a revenue

receipt, and capital gain tax must not incur upon the same (Barkoczy, 2014).

Further, if Bill attains a lump sum amount of $50,000 for providing the right to such logging

company for clearing out the timber trees from his land, the same receipt cannot be regarded as a

revenue receipt. This is because it is a non-recurring receipt and is associated with a lump sum

payment that is received only after giving the right to perform the required task (Hopewell,

2012). Nonetheless, this receipt must be considered as a capital receipt and the same must be

taxable under the heading capital gain tax for the year.

On a whole, it can be seen in both the cases that Bill receiving some amount of money. However,

the major difference in both the cases is that in the first case, it is a recurring receipt and is not a

lump sum payment that has been received after provision of the right to perform the required

task. In contrast to this, it can be witnessed in the second case that the lump sum amount of

$50,000 is a non-recurring figure because, after removal of timber from the land, it will surely

take some time to grow again (Patterson, 2009). Therefore, since Bill has offered a right to the

logging company for clearing the timber from the land, and in exchange, he has received a lump

sum amount, the same cannot be considered as a revenue receipt and instead, it must be regarded

as a capital receipt. This is because it is mainly associated with the selling of an asset to the

logging company and hence, taxable under capital gains (Cane & Conaghan, 2009). Similarly,

the first case shall be taxable under the normal rate of taxes.

8

Answer-5

It can be seen from the given case that there are various pine trees in a land that is owned by Bill

and in order to graze sheep in the land, Bill has no other option than to cut the trees. If he hires a

logging company to the same, he shall receive $1000 for every 100 meters of timber provided to

them. Since, the given case does not provide relevant information about the total amount of

receipts attained by Bill from the logging company, the same can be regarded as a revenue

receipt, and capital gain tax must not incur upon the same (Barkoczy, 2014).

Further, if Bill attains a lump sum amount of $50,000 for providing the right to such logging

company for clearing out the timber trees from his land, the same receipt cannot be regarded as a

revenue receipt. This is because it is a non-recurring receipt and is associated with a lump sum

payment that is received only after giving the right to perform the required task (Hopewell,

2012). Nonetheless, this receipt must be considered as a capital receipt and the same must be

taxable under the heading capital gain tax for the year.

On a whole, it can be seen in both the cases that Bill receiving some amount of money. However,

the major difference in both the cases is that in the first case, it is a recurring receipt and is not a

lump sum payment that has been received after provision of the right to perform the required

task. In contrast to this, it can be witnessed in the second case that the lump sum amount of

$50,000 is a non-recurring figure because, after removal of timber from the land, it will surely

take some time to grow again (Patterson, 2009). Therefore, since Bill has offered a right to the

logging company for clearing the timber from the land, and in exchange, he has received a lump

sum amount, the same cannot be considered as a revenue receipt and instead, it must be regarded

as a capital receipt. This is because it is mainly associated with the selling of an asset to the

logging company and hence, taxable under capital gains (Cane & Conaghan, 2009). Similarly,

the first case shall be taxable under the normal rate of taxes.

8

Taxation law

References

Adams, J 2011, What is The Difference Between Tax Avoidance and Tax Evasion?, viewed 19

September 2017 https://www.taxinsider.co.uk/680-

What_is_The_Difference_Between_Tax_Avoidance_and_Tax_Evasion.html

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Barkoczy, S, 2014, Australian Tax, 12th Edition, Adobe Digital Editions

Cane, P & Conaghan, J 2009, The new oxford companion to law, Oxford university Press.

Cartwright, M 2013, Death to the Australia Tax?, viewed 18 September 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

Goldberg, S.G 2017, The Death of the Income Tax: A Progressive Consumption Tax and the

Path to Fiscal Reform, Oxford Press.

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 18 September 2017,

www.zdnet.com.au.

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Patterson, D 2009, Cancellation Fees - The ATO Rulings, viewed 19 September 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2009,_Sound_Education_in_GST,_Cancellation_Fees___The_ATO_Rulings.html

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

Thorpe, C 2012, Tax Pack dumped online returns encouraged ABC News, viewed 18 September

2017 http://www.abc.net.au/news/2012-07-09/tax-pack-dumped-online-returns-encouraged/

4117784

9

References

Adams, J 2011, What is The Difference Between Tax Avoidance and Tax Evasion?, viewed 19

September 2017 https://www.taxinsider.co.uk/680-

What_is_The_Difference_Between_Tax_Avoidance_and_Tax_Evasion.html

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Barkoczy, S, 2014, Australian Tax, 12th Edition, Adobe Digital Editions

Cane, P & Conaghan, J 2009, The new oxford companion to law, Oxford university Press.

Cartwright, M 2013, Death to the Australia Tax?, viewed 18 September 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

Goldberg, S.G 2017, The Death of the Income Tax: A Progressive Consumption Tax and the

Path to Fiscal Reform, Oxford Press.

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 18 September 2017,

www.zdnet.com.au.

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Patterson, D 2009, Cancellation Fees - The ATO Rulings, viewed 19 September 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2009,_Sound_Education_in_GST,_Cancellation_Fees___The_ATO_Rulings.html

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

Thorpe, C 2012, Tax Pack dumped online returns encouraged ABC News, viewed 18 September

2017 http://www.abc.net.au/news/2012-07-09/tax-pack-dumped-online-returns-encouraged/

4117784

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.