Comprehensive Case Study on Capital Gains and Fringe Benefits Tax

VerifiedAdded on 2023/06/05

|12

|3033

|287

Case Study

AI Summary

This case study provides a detailed analysis of capital gains tax (CGT) and fringe benefits tax (FBT) implications under Australian taxation law. It examines various scenarios, including the sale of a vacant block of land, the loss of an antique bed, the sale of a painting and shares, and the sale of a violin, to determine CGT liabilities. Furthermore, the case study assesses FBT obligations related to an employee's use of a company car, car parking benefits, and a loan provided by the employer. The analysis references relevant sections of the ITAA 1997 and FBTAA 1986, as well as case law, to support its conclusions. This document is available on Desklib, a platform providing a wealth of study resources for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer 1:...................................................................................................................................2

Sale of vacant block of land:..................................................................................................2

Antique Bed:..........................................................................................................................3

Painting:.................................................................................................................................3

Shares:....................................................................................................................................4

Violin:....................................................................................................................................4

Answer 2:...................................................................................................................................6

Answer to A:..............................................................................................................................6

Issues:.....................................................................................................................................6

Rule:.......................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................8

Answer to B:..............................................................................................................................8

References................................................................................................................................10

Table of Contents

Answer 1:...................................................................................................................................2

Sale of vacant block of land:..................................................................................................2

Antique Bed:..........................................................................................................................3

Painting:.................................................................................................................................3

Shares:....................................................................................................................................4

Violin:....................................................................................................................................4

Answer 2:...................................................................................................................................6

Answer to A:..............................................................................................................................6

Issues:.....................................................................................................................................6

Rule:.......................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................8

Answer to B:..............................................................................................................................8

References................................................................................................................................10

2TAXATION LAW

Answer 1:

As per “section 102-20 of the ITAA 1997” it has been seen with the significance of

IT which is assessable only on the capital gains. This is directly in relation to any event of

loss pertaining to CGT excerpts. In some of the cases assessment of tax can occur pertaining

to any other event but CGT. The legislation of “section 104-10 (1) of the ITAA 1997” holds

true for disposal of asset which results in CGT event A1. The significance of “Sara Lee

Household v FC of T (2000)”, demonstrate that as soon as the tax bill enters into a contract it

is significant to consider CGT. Moreover, it should not be regarded as a separate IT

component as it was always included under the taxpayer’s obligations (Davidson 2016).

In addition to this, the discourse of “section 102-5, ITAA 1997”, entails that the

taxpayers are needed to contemplate with the net CG under the charge of the learnings for a

particular financial year. In order to do so, the taxpayer can quarantine the capital loss to the

established as per CG value. The CGT needs to be considered only on the assets which are

held for acquisition on or after the 20.09.1985. Furthermore, capital loss needs to be carried

forward rather than held for deductions. As discussed in the “Section 104-20(1)” C1 occurs

at the time of damage any CGT asset (Richardson 2016).

Sale of vacant block of land:

As per the given situation, the vacant land was acquired for either investment purpose

or private purpose. Which is already the case, CGT is applicable on capital asset at the time

of sales pertaining to the land. Based on the current contract the land was initially acquired

for $ 100k and also needed to pay land tax during the period of ownership.

As per the Australian taxation legislation as the vacant land was owned by the

taxpayer is treated as capital asset it is exposed to CGT and such a tax is not claimable under

deductions even if it did not generate any revenue. Therefore, the expenses pertaining to

Answer 1:

As per “section 102-20 of the ITAA 1997” it has been seen with the significance of

IT which is assessable only on the capital gains. This is directly in relation to any event of

loss pertaining to CGT excerpts. In some of the cases assessment of tax can occur pertaining

to any other event but CGT. The legislation of “section 104-10 (1) of the ITAA 1997” holds

true for disposal of asset which results in CGT event A1. The significance of “Sara Lee

Household v FC of T (2000)”, demonstrate that as soon as the tax bill enters into a contract it

is significant to consider CGT. Moreover, it should not be regarded as a separate IT

component as it was always included under the taxpayer’s obligations (Davidson 2016).

In addition to this, the discourse of “section 102-5, ITAA 1997”, entails that the

taxpayers are needed to contemplate with the net CG under the charge of the learnings for a

particular financial year. In order to do so, the taxpayer can quarantine the capital loss to the

established as per CG value. The CGT needs to be considered only on the assets which are

held for acquisition on or after the 20.09.1985. Furthermore, capital loss needs to be carried

forward rather than held for deductions. As discussed in the “Section 104-20(1)” C1 occurs

at the time of damage any CGT asset (Richardson 2016).

Sale of vacant block of land:

As per the given situation, the vacant land was acquired for either investment purpose

or private purpose. Which is already the case, CGT is applicable on capital asset at the time

of sales pertaining to the land. Based on the current contract the land was initially acquired

for $ 100k and also needed to pay land tax during the period of ownership.

As per the Australian taxation legislation as the vacant land was owned by the

taxpayer is treated as capital asset it is exposed to CGT and such a tax is not claimable under

deductions even if it did not generate any revenue. Therefore, the expenses pertaining to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

water and sewage rates along with local council and water rates should be calculated for

assessment of CG during selling of the land (Graetz and Warren 2016).

Antique Bed:

The consideration of the several levels of information as per “section 108-10(2) of

the ITAA 1997”, clearly categorizes the duties of a taxpayer pertaining to quarantining of

capital losses. Moreover, based on this section the definition of collectables includes relics

such as medallion, artwork and antiques. However, as they are considered under rear

portfolio manuscript, the rules of taxation are different.

Any event of CL or CG should be excluded from the first element in case the cost

base of collectables is lesser than AUD 500. In addition to this, based on the given situation

the taxpayer declared that antique bed was taken away by thieves in a house. However, after a

thorough perusal of the case by the insurance Department, it was observed that the anti-Fed

was not included in her insurance policy. Henceforth, the insurance amount paid by the client

amounted to AUD 11,000 (McGregor-Lowndes 2016).

It needs to be also discerned that as per “section 104-20(1), ITAA 1997” expresses

the treatment for which that any case of damage or destruction of an asset which is owned by

the taxpayer leads to CGT C1. It is important to consider the time of CGT so as to specify the

compensation received for destruction or loss of property and in determination of CG or CL.

As the taxpayer did not include antique bed in her insurance policy, the compensation under

CGT event C1 was debarred (Berg, C. and Davidson 2015).

Painting:

The excerpt of “section 108-20(2), ITAA 1997”, has enumerated on the treatment of

personal use of asset. Moreover, “section 108-20(1), ITAA 1997” also enumerates that a

taxpayer should exclude CL pertaining to asset which was used as a personal property. The

water and sewage rates along with local council and water rates should be calculated for

assessment of CG during selling of the land (Graetz and Warren 2016).

Antique Bed:

The consideration of the several levels of information as per “section 108-10(2) of

the ITAA 1997”, clearly categorizes the duties of a taxpayer pertaining to quarantining of

capital losses. Moreover, based on this section the definition of collectables includes relics

such as medallion, artwork and antiques. However, as they are considered under rear

portfolio manuscript, the rules of taxation are different.

Any event of CL or CG should be excluded from the first element in case the cost

base of collectables is lesser than AUD 500. In addition to this, based on the given situation

the taxpayer declared that antique bed was taken away by thieves in a house. However, after a

thorough perusal of the case by the insurance Department, it was observed that the anti-Fed

was not included in her insurance policy. Henceforth, the insurance amount paid by the client

amounted to AUD 11,000 (McGregor-Lowndes 2016).

It needs to be also discerned that as per “section 104-20(1), ITAA 1997” expresses

the treatment for which that any case of damage or destruction of an asset which is owned by

the taxpayer leads to CGT C1. It is important to consider the time of CGT so as to specify the

compensation received for destruction or loss of property and in determination of CG or CL.

As the taxpayer did not include antique bed in her insurance policy, the compensation under

CGT event C1 was debarred (Berg, C. and Davidson 2015).

Painting:

The excerpt of “section 108-20(2), ITAA 1997”, has enumerated on the treatment of

personal use of asset. Moreover, “section 108-20(1), ITAA 1997” also enumerates that a

taxpayer should exclude CL pertaining to asset which was used as a personal property. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

discourse under “section 108-20(2), ITAA 1997”, also elaborates that personal use of any

asset except for collectible needs to be considered under private use of taxpayer however,

such benefit is not applicable for land and building. Moreover, “section 118-10(3), ITAA

1997”, discusses that CG from personal use of any asset should be excluded when the price

of the asset is below $10,000 (Cao et al. 2015).

The information provided by the client suggests that obtaining of painting was done

with an amount of $2000 on 2.05.1985. In addition to this, such an item needs to be assessed

as pre-CGT. The rationale for such an evaluation is due to the fact that it was purchased

before 20th September 1985. Therefore, the taxpayer needs to exclude CG pertaining to sale

of the painting as it is pre-CGT in nature.

Shares:

The CGT imposition is applicable to securities similar to any other asset as prescribed

by the Australian legislation. At the time of CGT occurrence during the selling process, the

investors are seen to be making CG on the shares. Therefore, at this stage ordinary income is

generated as per the profits obtained pertaining to selling of the shares. As stated in the above

sentence, the reporting of CG was evident as a result of shares which were disposed for

Common Ltd, PHB Ltd and Build Ltd. The taxpayer can however claim for offsetting the CL

against CG as there was a certain loss incurred on disposing the shares of Young Kids

Learning Ltd (Hashimzade and Epifantseva 2017).

Violin:

The various excerpts stated under “Subdivision 108-C”, clearly defines the

jurisdictions for personal usage of an asset. The assets which are of personal use is to be

considered as a non-collectible entity. Such non-collectible assets comprise of the electrical

goods, furniture and boats. The discussions under “Section 108-20(2), ITAA 1997” also

discourse under “section 108-20(2), ITAA 1997”, also elaborates that personal use of any

asset except for collectible needs to be considered under private use of taxpayer however,

such benefit is not applicable for land and building. Moreover, “section 118-10(3), ITAA

1997”, discusses that CG from personal use of any asset should be excluded when the price

of the asset is below $10,000 (Cao et al. 2015).

The information provided by the client suggests that obtaining of painting was done

with an amount of $2000 on 2.05.1985. In addition to this, such an item needs to be assessed

as pre-CGT. The rationale for such an evaluation is due to the fact that it was purchased

before 20th September 1985. Therefore, the taxpayer needs to exclude CG pertaining to sale

of the painting as it is pre-CGT in nature.

Shares:

The CGT imposition is applicable to securities similar to any other asset as prescribed

by the Australian legislation. At the time of CGT occurrence during the selling process, the

investors are seen to be making CG on the shares. Therefore, at this stage ordinary income is

generated as per the profits obtained pertaining to selling of the shares. As stated in the above

sentence, the reporting of CG was evident as a result of shares which were disposed for

Common Ltd, PHB Ltd and Build Ltd. The taxpayer can however claim for offsetting the CL

against CG as there was a certain loss incurred on disposing the shares of Young Kids

Learning Ltd (Hashimzade and Epifantseva 2017).

Violin:

The various excerpts stated under “Subdivision 108-C”, clearly defines the

jurisdictions for personal usage of an asset. The assets which are of personal use is to be

considered as a non-collectible entity. Such non-collectible assets comprise of the electrical

goods, furniture and boats. The discussions under “Section 108-20(2), ITAA 1997” also

5TAXATION LAW

states that there are certain subdivisions which comprises of the rights and options in case a

taxpayer has used an asset for personal enjoyment. The CGT should not be included as the

purchase of the assets were less than $ 10,000. This is based on the statements under

“Section 118-10(3)”.

There is more evidence which suggests that despite of selling the violin at a profit, it

was mainly used by the taxpayer for his personal enjoyment. Therefore, the cost base of the

purchaser of asset of less than $ 10,000 is still applicable even if the violin was sold for

$12,000. This is directly under the legislations of “section 118-10 (3), ITAA 1997”, which

states that such a CG should be excluded from IT assessment (Burton and Karlinsky 2016).

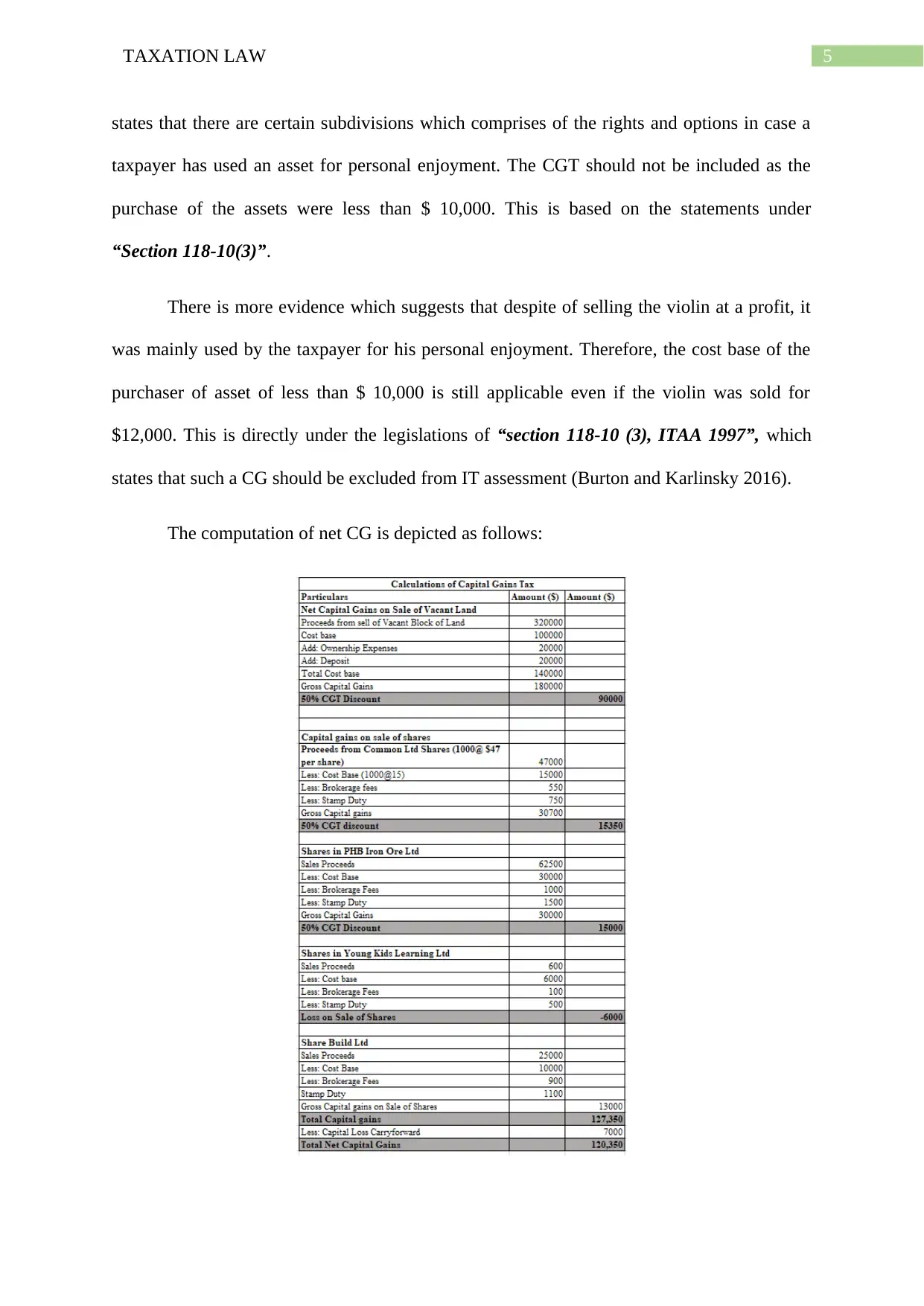

The computation of net CG is depicted as follows:

states that there are certain subdivisions which comprises of the rights and options in case a

taxpayer has used an asset for personal enjoyment. The CGT should not be included as the

purchase of the assets were less than $ 10,000. This is based on the statements under

“Section 118-10(3)”.

There is more evidence which suggests that despite of selling the violin at a profit, it

was mainly used by the taxpayer for his personal enjoyment. Therefore, the cost base of the

purchaser of asset of less than $ 10,000 is still applicable even if the violin was sold for

$12,000. This is directly under the legislations of “section 118-10 (3), ITAA 1997”, which

states that such a CG should be excluded from IT assessment (Burton and Karlinsky 2016).

The computation of net CG is depicted as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer 2:

Answer to A:

Issues:

The important concerns for consideration of FBT are seen as per “FBTAA 1986”.

The consideration of significant issues under “section 7, FBTAA 1986” shows if the car used

for personal use needs to be regarded for FBT. The consequence of “subdivision A of

FBTAA, 1986” for loan FB. This is to be considered directly for assertion.

Rule:

The legislations of FBT presents that tax should be considered in case benefit is

obtained is as a result of payments made by the employee from their salary. The legislation

for that constitutes that the advantages provided to the employee may considering the

employment status. This significantly shows that fund is provided to someone just as they are

employed (Lang et al. 2018).

The inclusion of excerpts from “sub-section 136 (1), FBTAA 1986” applies to the car

used by employee in the course of his employment is related to the availability of use and it

shall be treated under FBT. Moreover, there was no instance of gaining access of income by

using the car. Therefore, the taxpayer should be treated with the travelling from his place of

employment to business under “Federal Commissioner of Taxation v Lunney (1958)”.

The discussions under “Subdivision B 22A of the FBTAA 1986”, additionally relates

to FBP associated expenses. The origination of such an expense payment is held at the time

employer is seen to reimburse an employee with expense which they incur. This sort of cost

may be both business or private in nature or a combination. In this case, the general rule is

applicable which shows that no expense had taken place at the time then there was consistent

Answer 2:

Answer to A:

Issues:

The important concerns for consideration of FBT are seen as per “FBTAA 1986”.

The consideration of significant issues under “section 7, FBTAA 1986” shows if the car used

for personal use needs to be regarded for FBT. The consequence of “subdivision A of

FBTAA, 1986” for loan FB. This is to be considered directly for assertion.

Rule:

The legislations of FBT presents that tax should be considered in case benefit is

obtained is as a result of payments made by the employee from their salary. The legislation

for that constitutes that the advantages provided to the employee may considering the

employment status. This significantly shows that fund is provided to someone just as they are

employed (Lang et al. 2018).

The inclusion of excerpts from “sub-section 136 (1), FBTAA 1986” applies to the car

used by employee in the course of his employment is related to the availability of use and it

shall be treated under FBT. Moreover, there was no instance of gaining access of income by

using the car. Therefore, the taxpayer should be treated with the travelling from his place of

employment to business under “Federal Commissioner of Taxation v Lunney (1958)”.

The discussions under “Subdivision B 22A of the FBTAA 1986”, additionally relates

to FBP associated expenses. The origination of such an expense payment is held at the time

employer is seen to reimburse an employee with expense which they incur. This sort of cost

may be both business or private in nature or a combination. In this case, the general rule is

applicable which shows that no expense had taken place at the time then there was consistent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

reimbursement of expenses of fringe benefit in nature. Therefore, this value is to reimburse

the employee (Anderson 2015).

The taxable value of car parking FBT stated under “Sub-Division B 39C of the

FBTAA 1986”. The fringe benefit pertaining to car parking can be identified with following

list

a) Utilization of the car from place of abode to the place of work at least once

b) Car parked in the employer’s properties

c) Parking is done within one-kilometre range

d) Facilitation of the car during the course of employment

e) Crossing the time limit of 4 hours of parking

As briefed under “Division 4 of the FBTAA 1986”, the occurrence of loan fringe

benefit is evident when the terms of loan are agreed between the employer and employee.

This is also depicted with the purpose of “subsection 136 (1), FBTAA 1986” which is

designated to signify the repayment of the tax sum to another person. The reduced rate of

return for interest often shows that taxpayer is maintaining lesser than statutory taxation rate

(Eccleston and Krever 2017).

Application:

Based on the current case of Rapid Heat Pty Ltd it needs to be identified that Jasmine

is an employer of this organisation. Since her joining, she has been provided with a vehicle as

her job role involves lot of travelling for the purpose of employment. In addition to this, she

has used the car not only to restrict its use is only for work but also private activities as well.

The excerpt of “sub-section 136 (1), FBTAA 1986”, has been able to identify that the car

fringe benefit was provided to as a repercussion of her employment. Therefore, “FC of T v

reimbursement of expenses of fringe benefit in nature. Therefore, this value is to reimburse

the employee (Anderson 2015).

The taxable value of car parking FBT stated under “Sub-Division B 39C of the

FBTAA 1986”. The fringe benefit pertaining to car parking can be identified with following

list

a) Utilization of the car from place of abode to the place of work at least once

b) Car parked in the employer’s properties

c) Parking is done within one-kilometre range

d) Facilitation of the car during the course of employment

e) Crossing the time limit of 4 hours of parking

As briefed under “Division 4 of the FBTAA 1986”, the occurrence of loan fringe

benefit is evident when the terms of loan are agreed between the employer and employee.

This is also depicted with the purpose of “subsection 136 (1), FBTAA 1986” which is

designated to signify the repayment of the tax sum to another person. The reduced rate of

return for interest often shows that taxpayer is maintaining lesser than statutory taxation rate

(Eccleston and Krever 2017).

Application:

Based on the current case of Rapid Heat Pty Ltd it needs to be identified that Jasmine

is an employer of this organisation. Since her joining, she has been provided with a vehicle as

her job role involves lot of travelling for the purpose of employment. In addition to this, she

has used the car not only to restrict its use is only for work but also private activities as well.

The excerpt of “sub-section 136 (1), FBTAA 1986”, has been able to identify that the car

fringe benefit was provided to as a repercussion of her employment. Therefore, “FC of T v

8TAXATION LAW

Lunney (1958)”, held the usage of car beyond the scope of work and it shall be treated as

FBT as per “FBTAA, 1986” (Daniel et al. 2016).

During the later stages it was found that she used the expense of $ 550 for trivial

repairing jobs. However, Jasmine compensated these expenditures for Rapid Heat Pty Ltd.

the car repair needs to be assessed as per “subdivision B 22A of the FBTAA 1986”. It also

identified that during the end of the financial period, she parked the vehicle in the premises of

commercial airport. Therefore, she did not use the car for a tenure of 10 days after it first part.

Such a situation will not be considered for FBT as neither the car was parked at the company

nor it was situated within the 1 km radius of parking place in commercial property (Parker

2018).

Rapid Heat Pty Ltd offered Jasmine the total amount of $500,000 for the statutory

interest rate. The total sum was held as a loan which was to be disbursed to Jasmine. This

needs to be taken into account as per the various types of the important considerations related

to the statutory interest rate. The application of “Division 4 of the FBTAA 1986”, will be

also applicable for assessment of value to loan benefit of FBT (Picard et al. 2016).

Conclusion:

The study can be concluded by observing the various types of advantages for Jasmine

as per “section 7 of the FBTAA 1986”. Furthermore, the vehicle used by Jasmine needs to be

considered for FBT as per the rulings of “sub-section 136 (1), FBTAA 1986”. The collection

of facts about other benefits may be observed with reimbursement of loan and repairing

expenses as suitable with “FBTAA 1986”.

Answer to B:

The extraction of evidences as per “section 8-1 of the ITAA 1997”, recommends that

the paye of tax is entitled to deductions which are permissible with the expenditures

Lunney (1958)”, held the usage of car beyond the scope of work and it shall be treated as

FBT as per “FBTAA, 1986” (Daniel et al. 2016).

During the later stages it was found that she used the expense of $ 550 for trivial

repairing jobs. However, Jasmine compensated these expenditures for Rapid Heat Pty Ltd.

the car repair needs to be assessed as per “subdivision B 22A of the FBTAA 1986”. It also

identified that during the end of the financial period, she parked the vehicle in the premises of

commercial airport. Therefore, she did not use the car for a tenure of 10 days after it first part.

Such a situation will not be considered for FBT as neither the car was parked at the company

nor it was situated within the 1 km radius of parking place in commercial property (Parker

2018).

Rapid Heat Pty Ltd offered Jasmine the total amount of $500,000 for the statutory

interest rate. The total sum was held as a loan which was to be disbursed to Jasmine. This

needs to be taken into account as per the various types of the important considerations related

to the statutory interest rate. The application of “Division 4 of the FBTAA 1986”, will be

also applicable for assessment of value to loan benefit of FBT (Picard et al. 2016).

Conclusion:

The study can be concluded by observing the various types of advantages for Jasmine

as per “section 7 of the FBTAA 1986”. Furthermore, the vehicle used by Jasmine needs to be

considered for FBT as per the rulings of “sub-section 136 (1), FBTAA 1986”. The collection

of facts about other benefits may be observed with reimbursement of loan and repairing

expenses as suitable with “FBTAA 1986”.

Answer to B:

The extraction of evidences as per “section 8-1 of the ITAA 1997”, recommends that

the paye of tax is entitled to deductions which are permissible with the expenditures

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

involving to cohort of assessable income. Moreover, deductions can be claimed by the

taxpayer during the publishing process of as a double income.

In case, Jasmine had considered the left-out part of the loan amount ($ 50,000) then

she could have claimed for the deductions as prescribed in “section 8-1, ITAA 1997”.

Therefore, as it is evident that the left-out part was borrowed by her husband for purchasing

shares, she is not authorised to claim for deductions associated to interest present in the loan.

This could have been otherwise considered for exemption as per “section 8-1, ITAA 1997”.

involving to cohort of assessable income. Moreover, deductions can be claimed by the

taxpayer during the publishing process of as a double income.

In case, Jasmine had considered the left-out part of the loan amount ($ 50,000) then

she could have claimed for the deductions as prescribed in “section 8-1, ITAA 1997”.

Therefore, as it is evident that the left-out part was borrowed by her husband for purchasing

shares, she is not authorised to claim for deductions associated to interest present in the loan.

This could have been otherwise considered for exemption as per “section 8-1, ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References

Anderson, H.L., O'Connell, A., Ramsay, I., Welsh, M.A. and Withers, H., 2015. Profiling

Phoenix Activity: A New Taxonomy.

Berg, C. and Davidson, S., 2015. Submission to Treasury Consultation Into Exposure Draft

of Tax Laws Amendment (Tax Integrity Multinational Anti-Avoidance Law) Bill 2015.

Institute of Public Affairs (Melbourne). Institute of Public Affairs.

Burton, H.A. and Karlinsky, S., 2016. Tax professionals’ perception of large and mid-size

business US tax law complexity. eJournal of Tax Research, 14(1).

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Daniel, P., Keen, M., Świstak, A. and Thuronyi, V. eds., 2016. International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Davidson, S.R., 2016. Submission to Parliamentary Joint Committee on Law Enforcement

Inquiry into Illicit Tobacco.

Eccleston, R. and Krever, R. eds., 2017. The Future of Federalism: Intergovernmental

Financial Relations in an Age of Austerity. Edward Elgar Publishing.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder taxes.

Hashimzade, N. and Epifantseva, Y. eds., 2017. The Routledge Companion to Tax Avoidance

Research. Routledge.

References

Anderson, H.L., O'Connell, A., Ramsay, I., Welsh, M.A. and Withers, H., 2015. Profiling

Phoenix Activity: A New Taxonomy.

Berg, C. and Davidson, S., 2015. Submission to Treasury Consultation Into Exposure Draft

of Tax Laws Amendment (Tax Integrity Multinational Anti-Avoidance Law) Bill 2015.

Institute of Public Affairs (Melbourne). Institute of Public Affairs.

Burton, H.A. and Karlinsky, S., 2016. Tax professionals’ perception of large and mid-size

business US tax law complexity. eJournal of Tax Research, 14(1).

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Daniel, P., Keen, M., Świstak, A. and Thuronyi, V. eds., 2016. International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Davidson, S.R., 2016. Submission to Parliamentary Joint Committee on Law Enforcement

Inquiry into Illicit Tobacco.

Eccleston, R. and Krever, R. eds., 2017. The Future of Federalism: Intergovernmental

Financial Relations in an Age of Austerity. Edward Elgar Publishing.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder taxes.

Hashimzade, N. and Epifantseva, Y. eds., 2017. The Routledge Companion to Tax Avoidance

Research. Routledge.

11TAXATION LAW

Lang, M., Rust, A., Owens, J., Pistone, P., Schuch, J., Staringer, C., Storck, A., ESSERS, P.,

Smit, D. and Kemmeren, E. eds., 2018. Tax Treaty Case Law around the Globe 2017:

Schriftenreihe IStR Band 108 (Vol. 108). Linde Verlag GmbH.

McGregor-Lowndes, M., 2016. Lawyers, reform and regulation in the Australian third

sector. Third Sector Review, 22(2), p.33.

Parker, H., 2018. Instead of the Dole: an enquiry into integration of the tax and benefit

systems. Routledge.

Picard, R., Belair-Gagnon, V., Ranchordás, S., Aptowitzer, A., Flynn, R., Papandrea, F. and

Townend, J., 2016. The impact of charity and tax law and regulation on not-for-profit news

organizations.

Richardson, G., 2016. The Determinants of Tax Evasion: A Cross-Country Study.

In Financial Crimes: Psychological, Technological, and Ethical Issues (pp. 33-57). Springer,

Cham.

Lang, M., Rust, A., Owens, J., Pistone, P., Schuch, J., Staringer, C., Storck, A., ESSERS, P.,

Smit, D. and Kemmeren, E. eds., 2018. Tax Treaty Case Law around the Globe 2017:

Schriftenreihe IStR Band 108 (Vol. 108). Linde Verlag GmbH.

McGregor-Lowndes, M., 2016. Lawyers, reform and regulation in the Australian third

sector. Third Sector Review, 22(2), p.33.

Parker, H., 2018. Instead of the Dole: an enquiry into integration of the tax and benefit

systems. Routledge.

Picard, R., Belair-Gagnon, V., Ranchordás, S., Aptowitzer, A., Flynn, R., Papandrea, F. and

Townend, J., 2016. The impact of charity and tax law and regulation on not-for-profit news

organizations.

Richardson, G., 2016. The Determinants of Tax Evasion: A Cross-Country Study.

In Financial Crimes: Psychological, Technological, and Ethical Issues (pp. 33-57). Springer,

Cham.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.