Taxation Law Case Study: Analysis of Deductions and Capital Gains

VerifiedAdded on 2023/06/11

|10

|2425

|484

Case Study

AI Summary

This case study examines two key aspects of Australian taxation law: deductions related to business repairs and improvements, and the calculation of capital gains. The first question addresses whether Ken Fong, the owner of a new restaurant, can claim deductions for various expenses, including repairs and replacements. It determines which expenses are deductible under Australian Taxation Law and which are not. The second question involves calculating Maurice's taxable income from capital gains, considering profits and losses from the sale of various assets like property, shares, furniture, a yacht, and vacant land. It explains the methods for calculating capital gains tax in Australia, including identifying capital gains or losses, calculating costs, and applying discounts where applicable. The report concludes that understanding tax obligations and claiming appropriate deductions are crucial for individuals and businesses.

Assessment 2 Case

Study

Study

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

Advice on the deductions that the business can get which are incurred on the repairs and

improvements..............................................................................................................................3

QUESTION 2..................................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

Advice on the deductions that the business can get which are incurred on the repairs and

improvements..............................................................................................................................3

QUESTION 2..................................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Taxation Law is formed for collecting the amount of tax payable by the individuals,

company and many other organisations. This law is formed under which the public

administration is regularised to claim the amount that the tax payers are required to pay on the

part of the property or income they hold. The tax is charged on the assessable income which

could be either, statutory, ordinary or non – statutory income (Williamson and Luke, 2021). In

this report, the case study consists of two questions. First question comprises of the deductions

related to the repair and maintenance incurred by the restaurant of Ken Fong. It consists of the

deductions and through that the taxable income will be computed. In question 2, the capital gain

for the long and short terms is computed.

QUESTION 1

Advice on the deductions that the business can get which are incurred on the repairs and

improvements.

Ken Fong acquired the new restaurant on 17 July, 2020, which be not be considered as the

deductible amount under the Taxation Law of Australia.

In August 2020, Ken spent $ 27000 on the repairing of the restaurant. This will be a part of

the replacement as the space which is acquired for the new business. For instance, the space

which has been acquired should be contain of the parts such as of construction. The amount of $

6400 is costing to ken for the replacement of the cracked tiles of kitchen. It will be allowed as the

deductible expense for the restaurant of Ken Fong (Maxwell, 2018).

In November 2020, the replacement of the cooking equipment was done voluntarily which cost $

30000. It will not be a deductible expense. As it will not be considered under the repairing of

machinery, it is the replacement costs when no hazardous situation was occurred in the

equipment’s of the kitchen. A deduction shall be made for the cost of restoring

corporate belongings, part of properties or a drop in the worth asset reserved for the drive of

creating a judgement income. If the properties are retained or only used in part for that goal, a

assumption may be made in so far as is suitable in the conditions. The assessment specialist

cannot force the proprietor to own the asset or the denigrating asset. It may also be retained by

another administration; though, if the expenditure is for upkeep and the proprietor retains or uses

the belongings or the denigrating asset from the year of revenue for the drive of generating

Taxation Law is formed for collecting the amount of tax payable by the individuals,

company and many other organisations. This law is formed under which the public

administration is regularised to claim the amount that the tax payers are required to pay on the

part of the property or income they hold. The tax is charged on the assessable income which

could be either, statutory, ordinary or non – statutory income (Williamson and Luke, 2021). In

this report, the case study consists of two questions. First question comprises of the deductions

related to the repair and maintenance incurred by the restaurant of Ken Fong. It consists of the

deductions and through that the taxable income will be computed. In question 2, the capital gain

for the long and short terms is computed.

QUESTION 1

Advice on the deductions that the business can get which are incurred on the repairs and

improvements.

Ken Fong acquired the new restaurant on 17 July, 2020, which be not be considered as the

deductible amount under the Taxation Law of Australia.

In August 2020, Ken spent $ 27000 on the repairing of the restaurant. This will be a part of

the replacement as the space which is acquired for the new business. For instance, the space

which has been acquired should be contain of the parts such as of construction. The amount of $

6400 is costing to ken for the replacement of the cracked tiles of kitchen. It will be allowed as the

deductible expense for the restaurant of Ken Fong (Maxwell, 2018).

In November 2020, the replacement of the cooking equipment was done voluntarily which cost $

30000. It will not be a deductible expense. As it will not be considered under the repairing of

machinery, it is the replacement costs when no hazardous situation was occurred in the

equipment’s of the kitchen. A deduction shall be made for the cost of restoring

corporate belongings, part of properties or a drop in the worth asset reserved for the drive of

creating a judgement income. If the properties are retained or only used in part for that goal, a

assumption may be made in so far as is suitable in the conditions. The assessment specialist

cannot force the proprietor to own the asset or the denigrating asset. It may also be retained by

another administration; though, if the expenditure is for upkeep and the proprietor retains or uses

the belongings or the denigrating asset from the year of revenue for the drive of generating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a considerable income, the inference is allowable given that the imbursement is produced. There

are in total 3 cases which can be carried by the taxpayer in order to considers the deductions

available, it incurred in the same year when the deduction is incurred or it may regard to a

devaluing asset or a property.

The pest control is also not the deductible expense, as it is also done by the organization by

its voluntary wish for ensuring the health and safety standards of the employees. It will not be

counted in the assessable income (Nasution, Santi, Husaini, Fadli and Pirzada, 2020).

In January 2021, a casualty occurred due to which the roof of the restaurant got damaged. So

the replacement cost of roof which was $ 32000 will be used as a deductible expense form the

assessable income of the restaurant.

Deductions which can be claimed by the business for repair, replacement expenses and

maintenance expenses.

An individual whom have spent an amount for repair and maintenance of business can claim for

deduction for such business expenses which includes,

Conditioning gutters

Repairing electrical appliances

Replacing broken parts of fences or broken glass window

Mending leaks

Repairing machinery

Painting

Maintaining plumbing

Expenses those are incurred by the business but cannot be deducted from the income earned

by the organisation. These are the expenses which cannot be claimed by the organisation.

Repair of machinery, property and tool at the time of purchase.

Improvement for any machine or property (Brown, 2020).

Deduction for claim of deduction of capital expenses:

Capital work provisions

Depreciation provisions

Hence, the advice will be made that the improvement which are related to the equipment or

replacement of the machinery should be done by the organisation, in the case if it is required for

increasing the efficient of the company.

are in total 3 cases which can be carried by the taxpayer in order to considers the deductions

available, it incurred in the same year when the deduction is incurred or it may regard to a

devaluing asset or a property.

The pest control is also not the deductible expense, as it is also done by the organization by

its voluntary wish for ensuring the health and safety standards of the employees. It will not be

counted in the assessable income (Nasution, Santi, Husaini, Fadli and Pirzada, 2020).

In January 2021, a casualty occurred due to which the roof of the restaurant got damaged. So

the replacement cost of roof which was $ 32000 will be used as a deductible expense form the

assessable income of the restaurant.

Deductions which can be claimed by the business for repair, replacement expenses and

maintenance expenses.

An individual whom have spent an amount for repair and maintenance of business can claim for

deduction for such business expenses which includes,

Conditioning gutters

Repairing electrical appliances

Replacing broken parts of fences or broken glass window

Mending leaks

Repairing machinery

Painting

Maintaining plumbing

Expenses those are incurred by the business but cannot be deducted from the income earned

by the organisation. These are the expenses which cannot be claimed by the organisation.

Repair of machinery, property and tool at the time of purchase.

Improvement for any machine or property (Brown, 2020).

Deduction for claim of deduction of capital expenses:

Capital work provisions

Depreciation provisions

Hence, the advice will be made that the improvement which are related to the equipment or

replacement of the machinery should be done by the organisation, in the case if it is required for

increasing the efficient of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

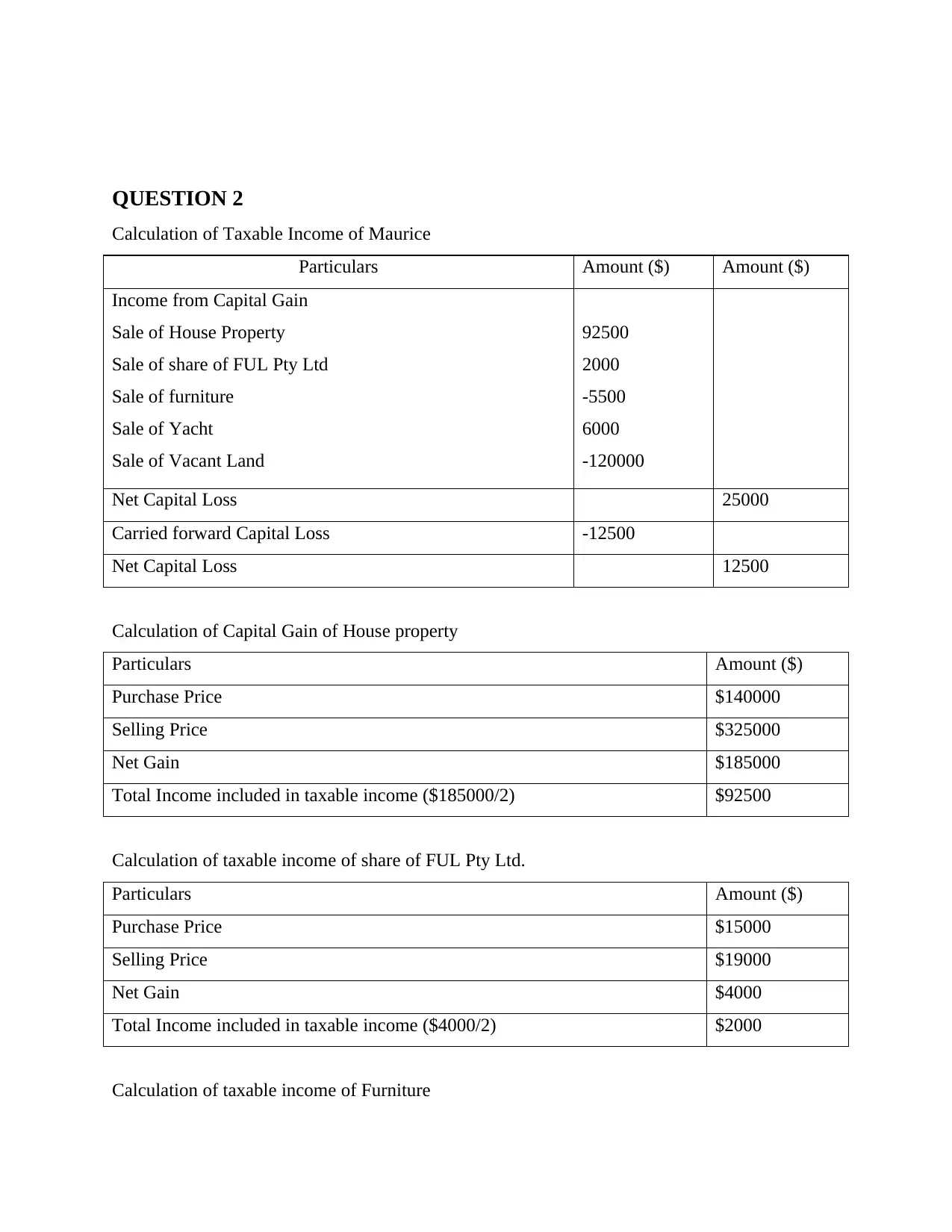

QUESTION 2

Calculation of Taxable Income of Maurice

Particulars Amount ($) Amount ($)

Income from Capital Gain

Sale of House Property

Sale of share of FUL Pty Ltd

Sale of furniture

Sale of Yacht

Sale of Vacant Land

92500

2000

-5500

6000

-120000

Net Capital Loss 25000

Carried forward Capital Loss -12500

Net Capital Loss 12500

Calculation of Capital Gain of House property

Particulars Amount ($)

Purchase Price $140000

Selling Price $325000

Net Gain $185000

Total Income included in taxable income ($185000/2) $92500

Calculation of taxable income of share of FUL Pty Ltd.

Particulars Amount ($)

Purchase Price $15000

Selling Price $19000

Net Gain $4000

Total Income included in taxable income ($4000/2) $2000

Calculation of taxable income of Furniture

Calculation of Taxable Income of Maurice

Particulars Amount ($) Amount ($)

Income from Capital Gain

Sale of House Property

Sale of share of FUL Pty Ltd

Sale of furniture

Sale of Yacht

Sale of Vacant Land

92500

2000

-5500

6000

-120000

Net Capital Loss 25000

Carried forward Capital Loss -12500

Net Capital Loss 12500

Calculation of Capital Gain of House property

Particulars Amount ($)

Purchase Price $140000

Selling Price $325000

Net Gain $185000

Total Income included in taxable income ($185000/2) $92500

Calculation of taxable income of share of FUL Pty Ltd.

Particulars Amount ($)

Purchase Price $15000

Selling Price $19000

Net Gain $4000

Total Income included in taxable income ($4000/2) $2000

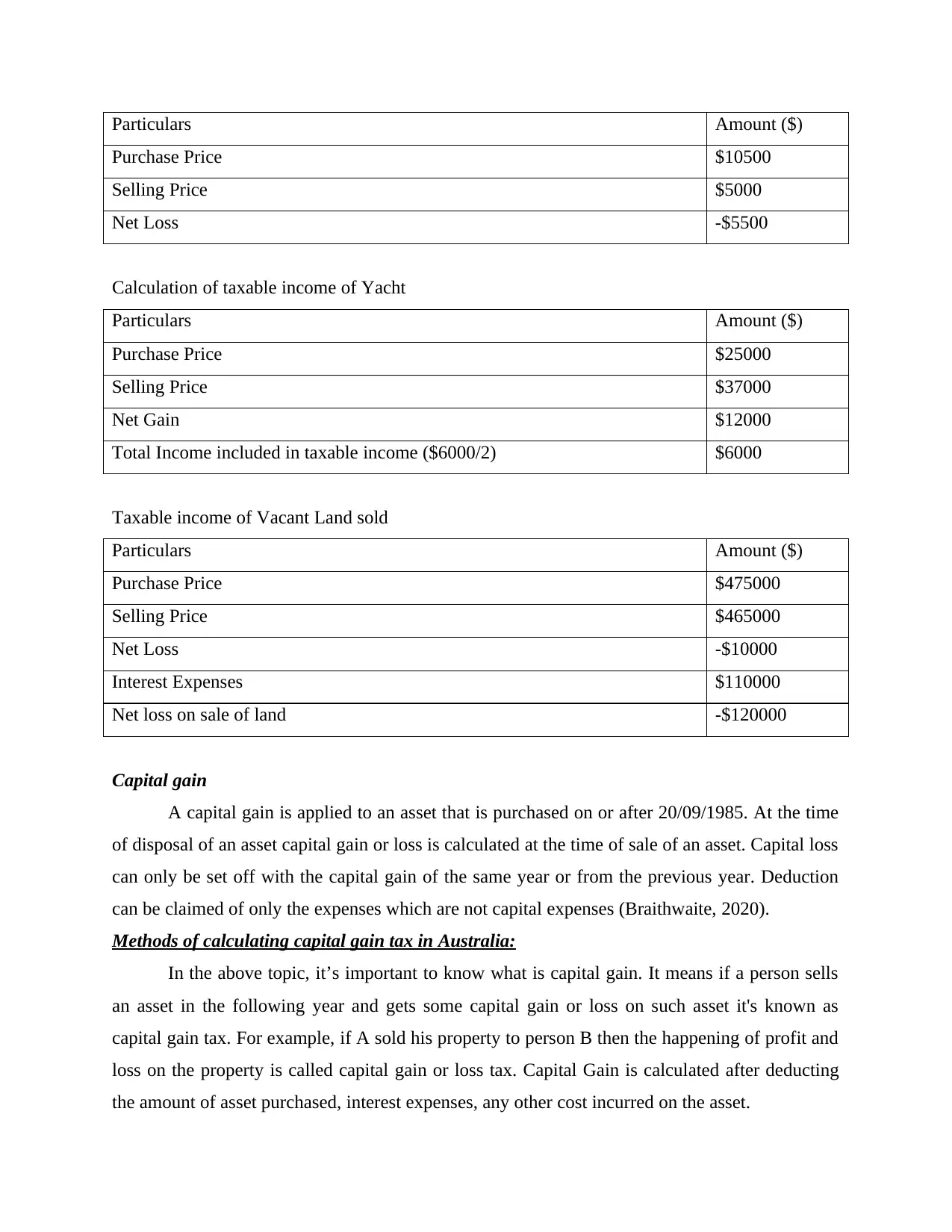

Calculation of taxable income of Furniture

Particulars Amount ($)

Purchase Price $10500

Selling Price $5000

Net Loss -$5500

Calculation of taxable income of Yacht

Particulars Amount ($)

Purchase Price $25000

Selling Price $37000

Net Gain $12000

Total Income included in taxable income ($6000/2) $6000

Taxable income of Vacant Land sold

Particulars Amount ($)

Purchase Price $475000

Selling Price $465000

Net Loss -$10000

Interest Expenses $110000

Net loss on sale of land -$120000

Capital gain

A capital gain is applied to an asset that is purchased on or after 20/09/1985. At the time

of disposal of an asset capital gain or loss is calculated at the time of sale of an asset. Capital loss

can only be set off with the capital gain of the same year or from the previous year. Deduction

can be claimed of only the expenses which are not capital expenses (Braithwaite, 2020).

Methods of calculating capital gain tax in Australia:

In the above topic, it’s important to know what is capital gain. It means if a person sells

an asset in the following year and gets some capital gain or loss on such asset it's known as

capital gain tax. For example, if A sold his property to person B then the happening of profit and

loss on the property is called capital gain or loss tax. Capital Gain is calculated after deducting

the amount of asset purchased, interest expenses, any other cost incurred on the asset.

Purchase Price $10500

Selling Price $5000

Net Loss -$5500

Calculation of taxable income of Yacht

Particulars Amount ($)

Purchase Price $25000

Selling Price $37000

Net Gain $12000

Total Income included in taxable income ($6000/2) $6000

Taxable income of Vacant Land sold

Particulars Amount ($)

Purchase Price $475000

Selling Price $465000

Net Loss -$10000

Interest Expenses $110000

Net loss on sale of land -$120000

Capital gain

A capital gain is applied to an asset that is purchased on or after 20/09/1985. At the time

of disposal of an asset capital gain or loss is calculated at the time of sale of an asset. Capital loss

can only be set off with the capital gain of the same year or from the previous year. Deduction

can be claimed of only the expenses which are not capital expenses (Braithwaite, 2020).

Methods of calculating capital gain tax in Australia:

In the above topic, it’s important to know what is capital gain. It means if a person sells

an asset in the following year and gets some capital gain or loss on such asset it's known as

capital gain tax. For example, if A sold his property to person B then the happening of profit and

loss on the property is called capital gain or loss tax. Capital Gain is calculated after deducting

the amount of asset purchased, interest expenses, any other cost incurred on the asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

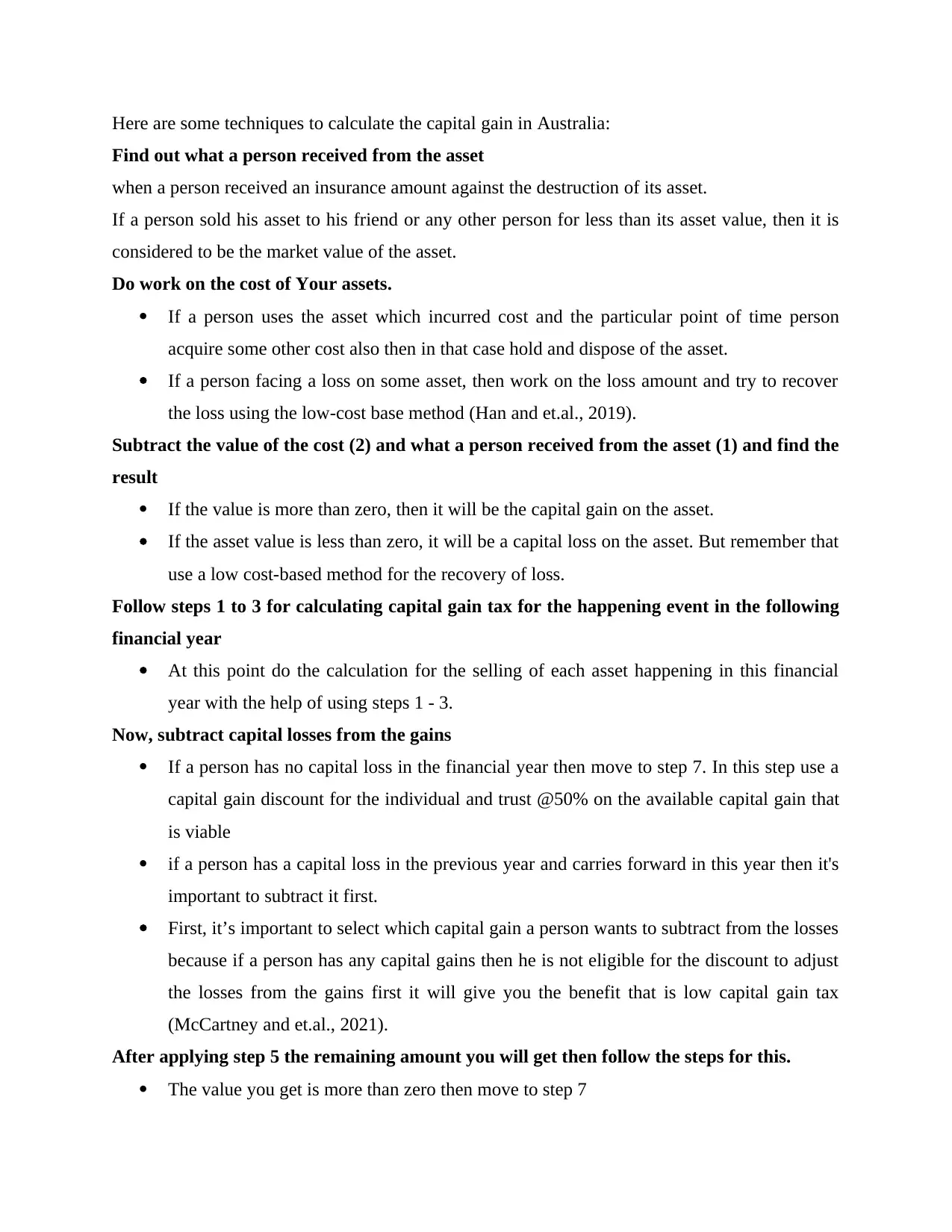

Here are some techniques to calculate the capital gain in Australia:

Find out what a person received from the asset

when a person received an insurance amount against the destruction of its asset.

If a person sold his asset to his friend or any other person for less than its asset value, then it is

considered to be the market value of the asset.

Do work on the cost of Your assets.

If a person uses the asset which incurred cost and the particular point of time person

acquire some other cost also then in that case hold and dispose of the asset.

If a person facing a loss on some asset, then work on the loss amount and try to recover

the loss using the low-cost base method (Han and et.al., 2019).

Subtract the value of the cost (2) and what a person received from the asset (1) and find the

result

If the value is more than zero, then it will be the capital gain on the asset.

If the asset value is less than zero, it will be a capital loss on the asset. But remember that

use a low cost-based method for the recovery of loss.

Follow steps 1 to 3 for calculating capital gain tax for the happening event in the following

financial year

At this point do the calculation for the selling of each asset happening in this financial

year with the help of using steps 1 - 3.

Now, subtract capital losses from the gains

If a person has no capital loss in the financial year then move to step 7. In this step use a

capital gain discount for the individual and trust @50% on the available capital gain that

is viable

if a person has a capital loss in the previous year and carries forward in this year then it's

important to subtract it first.

First, it’s important to select which capital gain a person wants to subtract from the losses

because if a person has any capital gains then he is not eligible for the discount to adjust

the losses from the gains first it will give you the benefit that is low capital gain tax

(McCartney and et.al., 2021).

After applying step 5 the remaining amount you will get then follow the steps for this.

The value you get is more than zero then move to step 7

Find out what a person received from the asset

when a person received an insurance amount against the destruction of its asset.

If a person sold his asset to his friend or any other person for less than its asset value, then it is

considered to be the market value of the asset.

Do work on the cost of Your assets.

If a person uses the asset which incurred cost and the particular point of time person

acquire some other cost also then in that case hold and dispose of the asset.

If a person facing a loss on some asset, then work on the loss amount and try to recover

the loss using the low-cost base method (Han and et.al., 2019).

Subtract the value of the cost (2) and what a person received from the asset (1) and find the

result

If the value is more than zero, then it will be the capital gain on the asset.

If the asset value is less than zero, it will be a capital loss on the asset. But remember that

use a low cost-based method for the recovery of loss.

Follow steps 1 to 3 for calculating capital gain tax for the happening event in the following

financial year

At this point do the calculation for the selling of each asset happening in this financial

year with the help of using steps 1 - 3.

Now, subtract capital losses from the gains

If a person has no capital loss in the financial year then move to step 7. In this step use a

capital gain discount for the individual and trust @50% on the available capital gain that

is viable

if a person has a capital loss in the previous year and carries forward in this year then it's

important to subtract it first.

First, it’s important to select which capital gain a person wants to subtract from the losses

because if a person has any capital gains then he is not eligible for the discount to adjust

the losses from the gains first it will give you the benefit that is low capital gain tax

(McCartney and et.al., 2021).

After applying step 5 the remaining amount you will get then follow the steps for this.

The value you get is more than zero then move to step 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

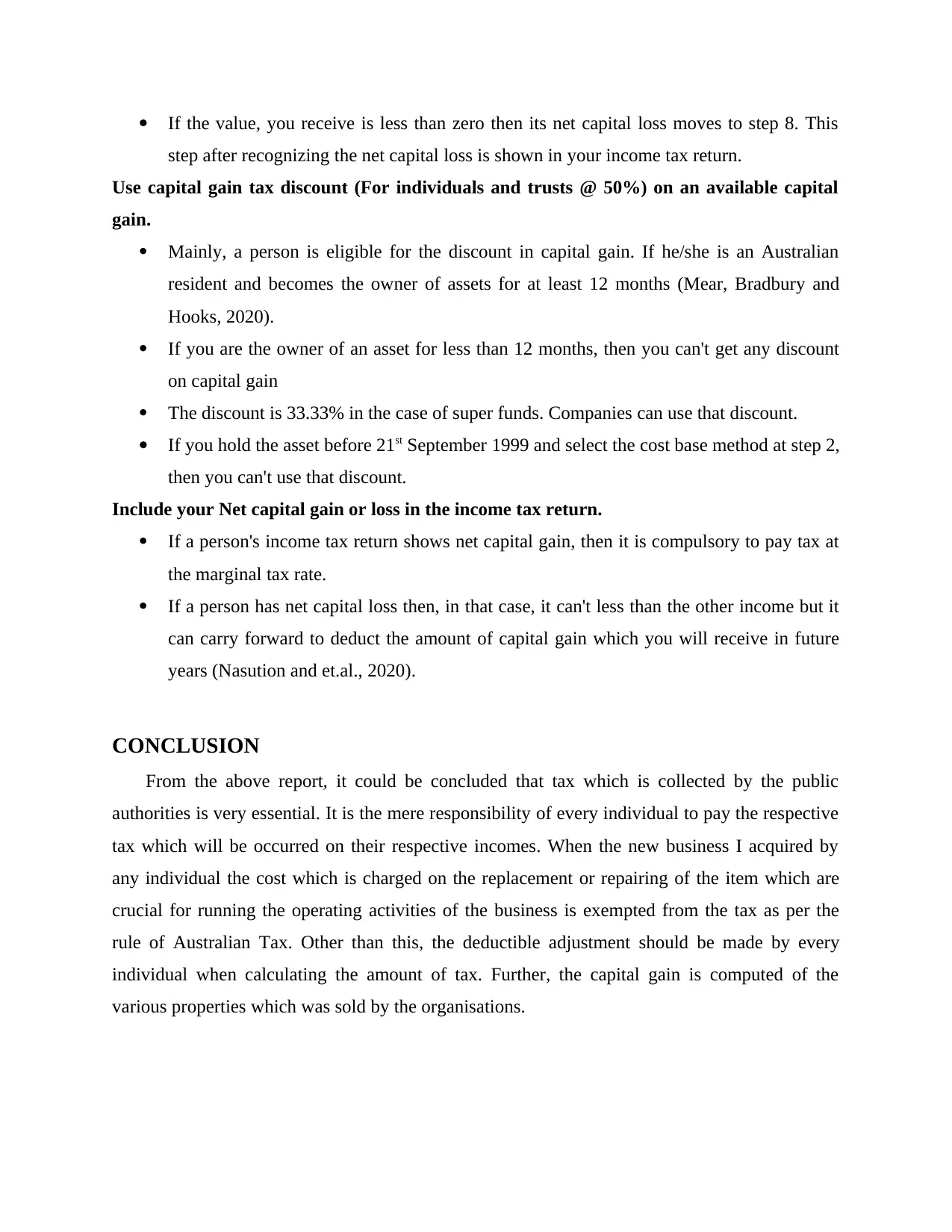

If the value, you receive is less than zero then its net capital loss moves to step 8. This

step after recognizing the net capital loss is shown in your income tax return.

Use capital gain tax discount (For individuals and trusts @ 50%) on an available capital

gain.

Mainly, a person is eligible for the discount in capital gain. If he/she is an Australian

resident and becomes the owner of assets for at least 12 months (Mear, Bradbury and

Hooks, 2020).

If you are the owner of an asset for less than 12 months, then you can't get any discount

on capital gain

The discount is 33.33% in the case of super funds. Companies can use that discount.

If you hold the asset before 21st September 1999 and select the cost base method at step 2,

then you can't use that discount.

Include your Net capital gain or loss in the income tax return.

If a person's income tax return shows net capital gain, then it is compulsory to pay tax at

the marginal tax rate.

If a person has net capital loss then, in that case, it can't less than the other income but it

can carry forward to deduct the amount of capital gain which you will receive in future

years (Nasution and et.al., 2020).

CONCLUSION

From the above report, it could be concluded that tax which is collected by the public

authorities is very essential. It is the mere responsibility of every individual to pay the respective

tax which will be occurred on their respective incomes. When the new business I acquired by

any individual the cost which is charged on the replacement or repairing of the item which are

crucial for running the operating activities of the business is exempted from the tax as per the

rule of Australian Tax. Other than this, the deductible adjustment should be made by every

individual when calculating the amount of tax. Further, the capital gain is computed of the

various properties which was sold by the organisations.

step after recognizing the net capital loss is shown in your income tax return.

Use capital gain tax discount (For individuals and trusts @ 50%) on an available capital

gain.

Mainly, a person is eligible for the discount in capital gain. If he/she is an Australian

resident and becomes the owner of assets for at least 12 months (Mear, Bradbury and

Hooks, 2020).

If you are the owner of an asset for less than 12 months, then you can't get any discount

on capital gain

The discount is 33.33% in the case of super funds. Companies can use that discount.

If you hold the asset before 21st September 1999 and select the cost base method at step 2,

then you can't use that discount.

Include your Net capital gain or loss in the income tax return.

If a person's income tax return shows net capital gain, then it is compulsory to pay tax at

the marginal tax rate.

If a person has net capital loss then, in that case, it can't less than the other income but it

can carry forward to deduct the amount of capital gain which you will receive in future

years (Nasution and et.al., 2020).

CONCLUSION

From the above report, it could be concluded that tax which is collected by the public

authorities is very essential. It is the mere responsibility of every individual to pay the respective

tax which will be occurred on their respective incomes. When the new business I acquired by

any individual the cost which is charged on the replacement or repairing of the item which are

crucial for running the operating activities of the business is exempted from the tax as per the

rule of Australian Tax. Other than this, the deductible adjustment should be made by every

individual when calculating the amount of tax. Further, the capital gain is computed of the

various properties which was sold by the organisations.

REFERENCES

Books and Journals

Braithwaite, V., 2020. Beyond the bubble that is Robodebt: How governments that lose integrity

threaten democracy. Australian Journal of Social Issues, 55(3), pp.242-259.

Brown, R.J., 2020, September. Voluntary tax disclosures and corporate tax avoidance: Evidence

from Australia. In Australian Tax Forum (Vol. 35, No. 3, pp. 391-429).

Evans, V., 2021. Caring for Traumatic Brain Injury Patients: Australian Nursing

Perspectives. Critical Care Nursing Clinics, 33(1), pp.21-36.

Han, J., and et.al., 2019. The wealth effects of the announcement of the Australian carbon

pricing scheme. Pacific-Basin Finance Journal, 53, pp.399-409.

Koong, K.S., and et.al., 2019. Advancements and forecasts of electronic tax return and

informational filings in the US. International Journal of Accounting & Information

Management.

Maxwell, P., 2018. The end of the mining boom? A Western Australian perspective. Mineral

Economics, 31(1), pp.153-170.

McCartney, D., and et.al.,2021. Analysis of dietary intake, diet cost and food group expenditure

from a 24‐hour food record collected in a sample of Australian university

students. Nutrition & Dietetics, 78(2), pp.174-182.

Mear, K., Bradbury, M. and Hooks, J., 2020. Is the balance sheet method of deferred tax

informative?. Pacific Accounting Review.

Nasution, M.K. and et.al., 2020. Determinants of tax compliance: a study on individual taxpayers

in Indonesia. Entrepreneurship and Sustainability Issues, 8(2), p.1401.

Williamson, A.K. and Luke, B.G., 2021. Mapping the field of public ancillary funds. Australian

Journal of Public Administration.

Books and Journals

Braithwaite, V., 2020. Beyond the bubble that is Robodebt: How governments that lose integrity

threaten democracy. Australian Journal of Social Issues, 55(3), pp.242-259.

Brown, R.J., 2020, September. Voluntary tax disclosures and corporate tax avoidance: Evidence

from Australia. In Australian Tax Forum (Vol. 35, No. 3, pp. 391-429).

Evans, V., 2021. Caring for Traumatic Brain Injury Patients: Australian Nursing

Perspectives. Critical Care Nursing Clinics, 33(1), pp.21-36.

Han, J., and et.al., 2019. The wealth effects of the announcement of the Australian carbon

pricing scheme. Pacific-Basin Finance Journal, 53, pp.399-409.

Koong, K.S., and et.al., 2019. Advancements and forecasts of electronic tax return and

informational filings in the US. International Journal of Accounting & Information

Management.

Maxwell, P., 2018. The end of the mining boom? A Western Australian perspective. Mineral

Economics, 31(1), pp.153-170.

McCartney, D., and et.al.,2021. Analysis of dietary intake, diet cost and food group expenditure

from a 24‐hour food record collected in a sample of Australian university

students. Nutrition & Dietetics, 78(2), pp.174-182.

Mear, K., Bradbury, M. and Hooks, J., 2020. Is the balance sheet method of deferred tax

informative?. Pacific Accounting Review.

Nasution, M.K. and et.al., 2020. Determinants of tax compliance: a study on individual taxpayers

in Indonesia. Entrepreneurship and Sustainability Issues, 8(2), p.1401.

Williamson, A.K. and Luke, B.G., 2021. Mapping the field of public ancillary funds. Australian

Journal of Public Administration.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.