Taxation Law Case Study

VerifiedAdded on 2020/02/24

|9

|1107

|49

Case Study

AI Summary

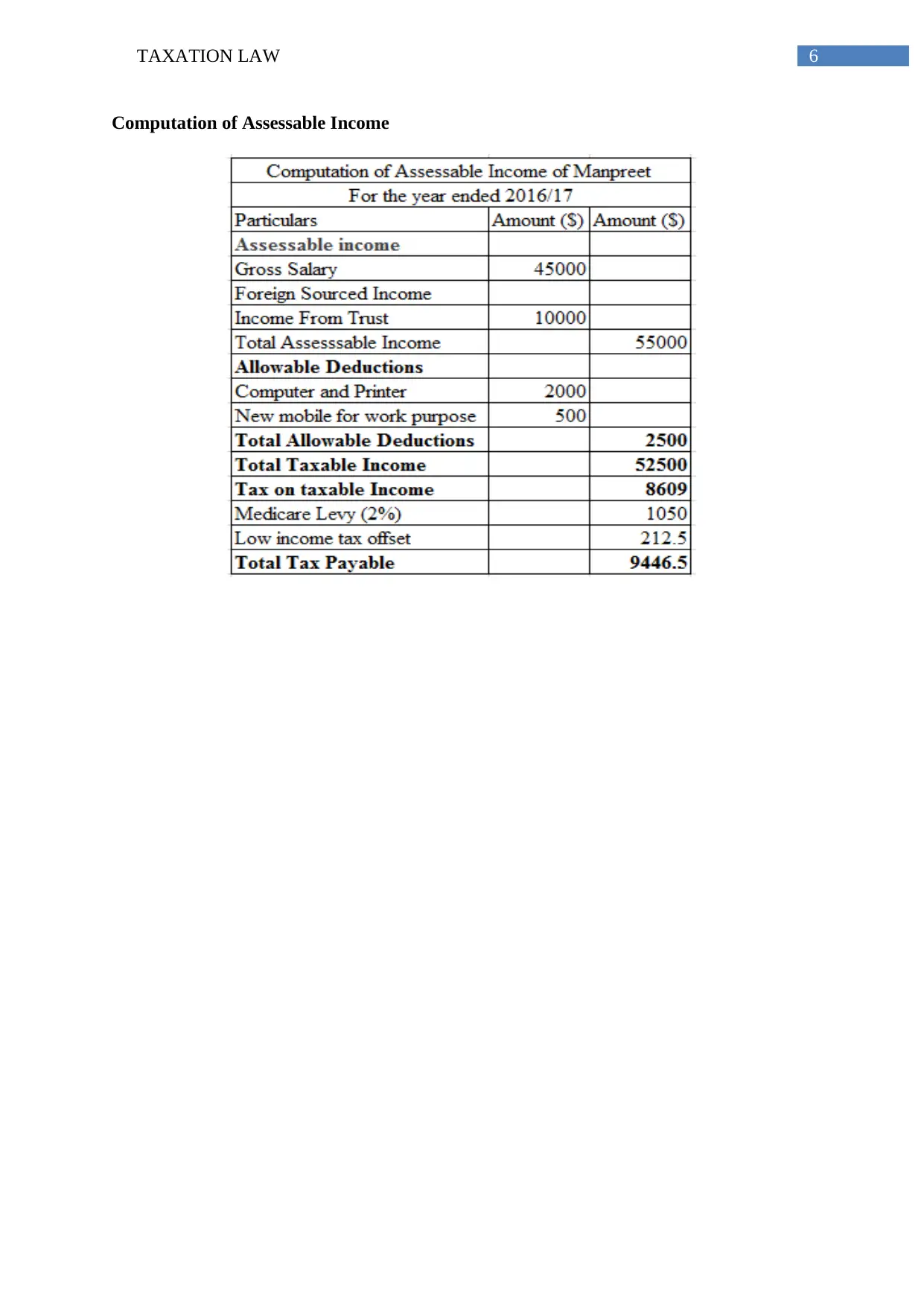

This case study examines the taxation implications for an overseas student, Manpreet, in Australia. It discusses his residential status, assessable income, and the deductibility of expenses related to his education. The analysis references relevant sections of the Income Tax Assessment Act 1997 and various case law to determine the allowable deductions and tax offsets applicable to Manpreet's situation. The study concludes with a computation of his assessable income and the tax implications thereof.

1 out of 9

Related Documents

![Taxation Law: Spriggs v Federal Commissioner of Taxation [2007]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fdocument%2Fpages%2Fspriggs-taxation-law-case-page-2.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.