TAXATION LAW: Case Studies on Residency, Income, and Business Income

VerifiedAdded on 2022/09/17

|19

|3755

|60

Case Study

AI Summary

This assignment presents a detailed analysis of three case studies related to Australian taxation law. The first case study examines the residency status of an individual, Rachael, based on the 'resides test,' domicile test, and 183-day test, concluding that she is an Australian resident for tax purposes due to her physical presence and employment contract. The second part of the first case study addresses the tax implications of her income, determining the source of her income and the applicability of the Double Taxation Agreement. The second case study assesses the residency status of John who is working overseas and concludes he is a non-resident based on the same tests as the first case study. The third case study examines whether the receipts from the sale of paintings constitute ordinary income from a business activity or a hobby, concluding that it is a hobby and therefore not assessable income. The analysis incorporates relevant legislation, such as ITAA 1936 and ITAA 1997, and case law to support the conclusions on residency and income tax implications.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Case Study One – Residences....................................................................................................3

Part A:........................................................................................................................................3

Issues:.....................................................................................................................................3

Rule:.......................................................................................................................................3

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Part B:.......................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................8

Case Study 2: Part A:.................................................................................................................9

Issues:.....................................................................................................................................9

Rule:.......................................................................................................................................9

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................10

Case Study Three.....................................................................................................................11

Issues:...................................................................................................................................11

Rule:.....................................................................................................................................11

Application:..........................................................................................................................12

Table of Contents

Case Study One – Residences....................................................................................................3

Part A:........................................................................................................................................3

Issues:.....................................................................................................................................3

Rule:.......................................................................................................................................3

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Part B:.......................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................8

Case Study 2: Part A:.................................................................................................................9

Issues:.....................................................................................................................................9

Rule:.......................................................................................................................................9

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................10

Case Study Three.....................................................................................................................11

Issues:...................................................................................................................................11

Rule:.....................................................................................................................................11

Application:..........................................................................................................................12

2TAXATION LAW

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Case Study One – Residences

Part A:

Issues:

Is the Racheal an Australian occupant inside the denotation of “section 6 (1), ITAA

1936” for the relevant income year?

Rule:

According to the “taxation ruling of TR 98/17” the taxation official interprets the

ordinary sense of the expression “resides” inside the definition of resident given in

“subsection 6 (1), ITAA 1936” (Norbury 2019). The ruling is generally applicable to

individuals that enters Australia as a migrants, academics teaching or workers with

employment contracts.

For tax purpose, an Australian resident under “sec 6 (1), ITAA 1936” consist of an

individual that exist in Australia and take account of person who has their abode in Australia

unless the commissioner is content that an individual has their fixed dwelling place outside

Australia (Jones 2018). The definition includes four alternative tests namely;

1. Resides Test

2. Domicile Test

3. 183-Day Test

4. Commonwealth Superannuation test

Resides Test:

The expression “reside” implies dwelling on enduring basis or for the substantial

time. To determine whether an individual is living in Australia it is essential to look into the

character of the person’s actions while in Australia. As per the “taxation ruling of TR

Case Study One – Residences

Part A:

Issues:

Is the Racheal an Australian occupant inside the denotation of “section 6 (1), ITAA

1936” for the relevant income year?

Rule:

According to the “taxation ruling of TR 98/17” the taxation official interprets the

ordinary sense of the expression “resides” inside the definition of resident given in

“subsection 6 (1), ITAA 1936” (Norbury 2019). The ruling is generally applicable to

individuals that enters Australia as a migrants, academics teaching or workers with

employment contracts.

For tax purpose, an Australian resident under “sec 6 (1), ITAA 1936” consist of an

individual that exist in Australia and take account of person who has their abode in Australia

unless the commissioner is content that an individual has their fixed dwelling place outside

Australia (Jones 2018). The definition includes four alternative tests namely;

1. Resides Test

2. Domicile Test

3. 183-Day Test

4. Commonwealth Superannuation test

Resides Test:

The expression “reside” implies dwelling on enduring basis or for the substantial

time. To determine whether an individual is living in Australia it is essential to look into the

character of the person’s actions while in Australia. As per the “taxation ruling of TR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

98/17” it is necessary to recognise the taxpayer’s family and employment ties (Sharkey

2016). As held in “Miesageas v Commissioners of Inland Revenue (1957)” individuals that

comes to Australia for taking up the pre-arranged work prospects or academic course will be

considered residing here given their visit is regular with living in Australia.

Domicile Test:

As per “section 6 (1)(a)(i)” an individual is treated as Australian occupant if they

have a home in Australia. This includes the purpose and the real length of a person visit in

foreign state or any establishment of home out of Australia (Kenny, Blissenden and Villios

2015). Similarly, in “FCT v Applegate (1979)” the law court held that permanent do not

means forever and it is evaluated objectively each year.

183-Day Test:

An individual is regarded as tax occupant of Australia if they have actually been in

Australia either incessantly or in discontinuities for six months or 183 days of a year.

Commonwealth Superannuation Test:

This test is applicable on the participant of commonwealth superannuation fund and

they are deemed to be Australian occupant for tax purpose.

Source:

Determining the sources of income is a concrete material of fact. In “FCT v French

(1957)” the tax liability for the service income commonly arises where the services are done

(Barkoczy 2016).

98/17” it is necessary to recognise the taxpayer’s family and employment ties (Sharkey

2016). As held in “Miesageas v Commissioners of Inland Revenue (1957)” individuals that

comes to Australia for taking up the pre-arranged work prospects or academic course will be

considered residing here given their visit is regular with living in Australia.

Domicile Test:

As per “section 6 (1)(a)(i)” an individual is treated as Australian occupant if they

have a home in Australia. This includes the purpose and the real length of a person visit in

foreign state or any establishment of home out of Australia (Kenny, Blissenden and Villios

2015). Similarly, in “FCT v Applegate (1979)” the law court held that permanent do not

means forever and it is evaluated objectively each year.

183-Day Test:

An individual is regarded as tax occupant of Australia if they have actually been in

Australia either incessantly or in discontinuities for six months or 183 days of a year.

Commonwealth Superannuation Test:

This test is applicable on the participant of commonwealth superannuation fund and

they are deemed to be Australian occupant for tax purpose.

Source:

Determining the sources of income is a concrete material of fact. In “FCT v French

(1957)” the tax liability for the service income commonly arises where the services are done

(Barkoczy 2016).

5TAXATION LAW

Application:

The case facts suggest that Racheal arrived in Australia for a period of twelve months

to take up an employment contract that would keep her in Australia till 1st December 2019.

To decide the residency position of Racheal, four alternative residency checks are considered.

Reside Test:

Racheal will be viewed as Australian occupant if she is considered to “reside” in

Australia for the significant period of twelve months. Referring to the relevant factors given

under “TR 98/17” Racheal arrived Australia with an employment contract and lives in the

fully equipped flat given by her company. Referring to “Miesageas v Commissioners of

Inland Revenue (1957)” as Racheal is residence here for a substantial time although on her

employment contract she would be considered to be residing here (Braithwaite and Reinhart

2019). The factors which supports Racheal being an Australian resident during her twelve

month stay includes her physical existence, her children accompanying to Australia and the

preservation of house in Australia. Racheal will be considered Australian resident for tax

purpose as she “resides” here throughout the applicable period.

Domicile Test:

In terms of domicile test, Rachael has the permanent habitation of abode outside

Australia in UK. Referring to “FCT v Applegate (1979)” Racheal has the fixed house out of

Australia and she does not satisfies the “Domicile Test” (Freudenberg et al. 2017).

183-Day Test:

Irrespective whether Racheal is treated as an Australian occupant under the “Resides

Test”, she is surely an Australian dweller under the 183-day test. This is because she has been

in Australia ever since she arrived on 1st December 2018 and this is more than six months of

the applicable income year.

Application:

The case facts suggest that Racheal arrived in Australia for a period of twelve months

to take up an employment contract that would keep her in Australia till 1st December 2019.

To decide the residency position of Racheal, four alternative residency checks are considered.

Reside Test:

Racheal will be viewed as Australian occupant if she is considered to “reside” in

Australia for the significant period of twelve months. Referring to the relevant factors given

under “TR 98/17” Racheal arrived Australia with an employment contract and lives in the

fully equipped flat given by her company. Referring to “Miesageas v Commissioners of

Inland Revenue (1957)” as Racheal is residence here for a substantial time although on her

employment contract she would be considered to be residing here (Braithwaite and Reinhart

2019). The factors which supports Racheal being an Australian resident during her twelve

month stay includes her physical existence, her children accompanying to Australia and the

preservation of house in Australia. Racheal will be considered Australian resident for tax

purpose as she “resides” here throughout the applicable period.

Domicile Test:

In terms of domicile test, Rachael has the permanent habitation of abode outside

Australia in UK. Referring to “FCT v Applegate (1979)” Racheal has the fixed house out of

Australia and she does not satisfies the “Domicile Test” (Freudenberg et al. 2017).

183-Day Test:

Irrespective whether Racheal is treated as an Australian occupant under the “Resides

Test”, she is surely an Australian dweller under the 183-day test. This is because she has been

in Australia ever since she arrived on 1st December 2018 and this is more than six months of

the applicable income year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Commonwealth Superannuation Test:

This test is not applicable in case of Racheal.

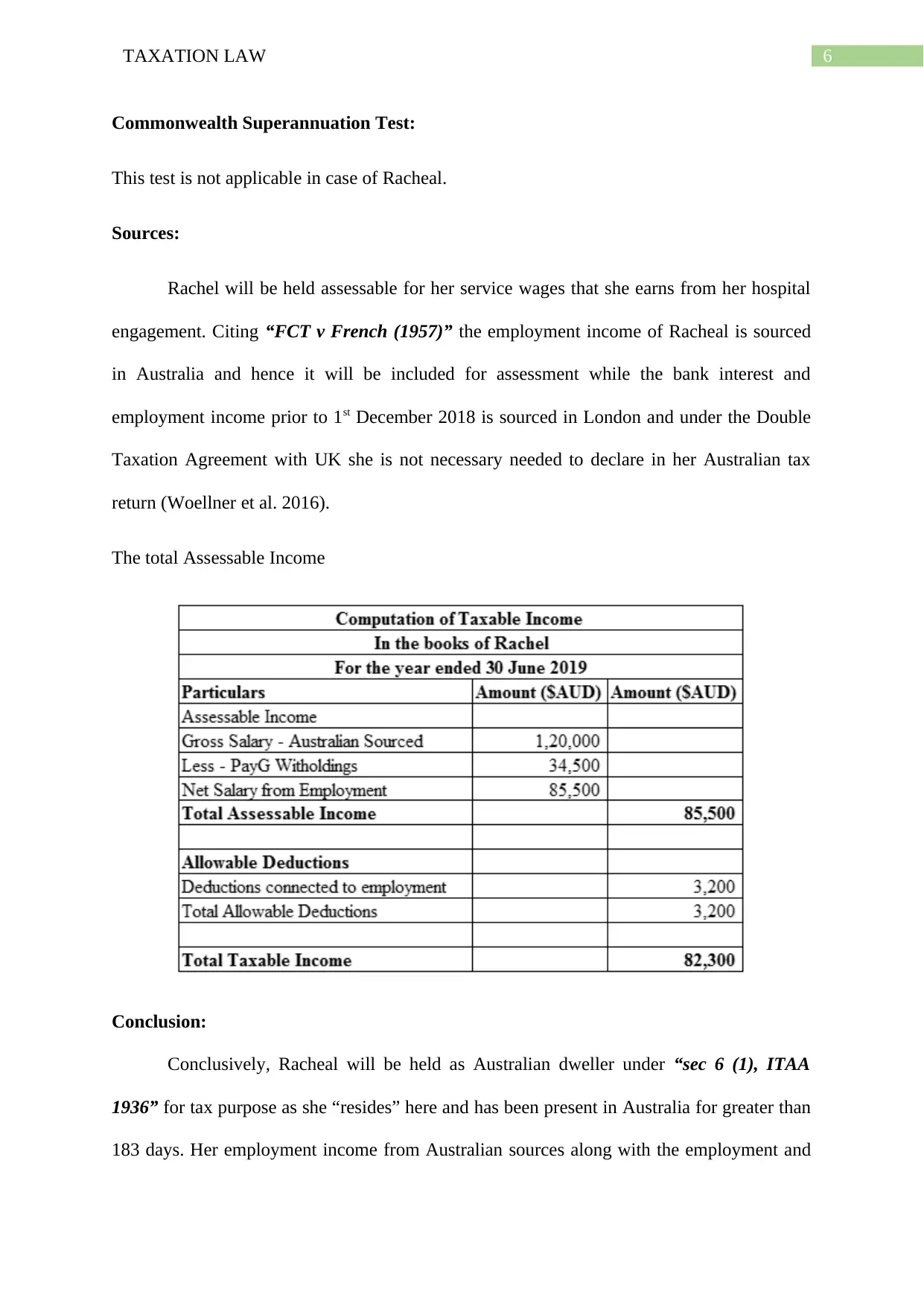

Sources:

Rachel will be held assessable for her service wages that she earns from her hospital

engagement. Citing “FCT v French (1957)” the employment income of Racheal is sourced

in Australia and hence it will be included for assessment while the bank interest and

employment income prior to 1st December 2018 is sourced in London and under the Double

Taxation Agreement with UK she is not necessary needed to declare in her Australian tax

return (Woellner et al. 2016).

The total Assessable Income

Conclusion:

Conclusively, Racheal will be held as Australian dweller under “sec 6 (1), ITAA

1936” for tax purpose as she “resides” here and has been present in Australia for greater than

183 days. Her employment income from Australian sources along with the employment and

Commonwealth Superannuation Test:

This test is not applicable in case of Racheal.

Sources:

Rachel will be held assessable for her service wages that she earns from her hospital

engagement. Citing “FCT v French (1957)” the employment income of Racheal is sourced

in Australia and hence it will be included for assessment while the bank interest and

employment income prior to 1st December 2018 is sourced in London and under the Double

Taxation Agreement with UK she is not necessary needed to declare in her Australian tax

return (Woellner et al. 2016).

The total Assessable Income

Conclusion:

Conclusively, Racheal will be held as Australian dweller under “sec 6 (1), ITAA

1936” for tax purpose as she “resides” here and has been present in Australia for greater than

183 days. Her employment income from Australian sources along with the employment and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

interest income from London bank account will be held for taxation. Any issues relating to

double taxation can be resolved and Racheal can claim a tax offset on foreign income for the

taxes paid in London.

Answer to Part B:

Issues:

Will John be treated as occupant of Australia under the description of inhabitant given

in “subsection 6 (1), ITAA 1936”.

Rule:

Resides Test:

An individual is held as tax inhabitant of Australia given they really live in Australia

unrelatedly of their nationality and site of permanent house. As held in “Dempsey v FCT

(2014)” a taxpayer working in Saudi Arabia was held as non-residence of Australia based on

taxpayer’s intention of residing in overseas (Sadiq 2019).

Domicile Test:

In “sec 6 (1)”, a person is tax occupant of Australia if they have residence in Australia

if not the taxpayer can prove that they have set up perpetual home outside Australia. In

“Harding v FCT (2019)” the taxpayer was held as non-resident of Australia (Butler 2019).

The court stated that “permanent place of abode” must be interpreted to consider whether an

individual is permanently living in particular “state or country”.

183 Day Test:

An individual is held to be Australia occupant if they are present in Australia for

greater than 183 days or six months of an income year (Murray et al. 2018).

Commonwealth Superannuation test:

interest income from London bank account will be held for taxation. Any issues relating to

double taxation can be resolved and Racheal can claim a tax offset on foreign income for the

taxes paid in London.

Answer to Part B:

Issues:

Will John be treated as occupant of Australia under the description of inhabitant given

in “subsection 6 (1), ITAA 1936”.

Rule:

Resides Test:

An individual is held as tax inhabitant of Australia given they really live in Australia

unrelatedly of their nationality and site of permanent house. As held in “Dempsey v FCT

(2014)” a taxpayer working in Saudi Arabia was held as non-residence of Australia based on

taxpayer’s intention of residing in overseas (Sadiq 2019).

Domicile Test:

In “sec 6 (1)”, a person is tax occupant of Australia if they have residence in Australia

if not the taxpayer can prove that they have set up perpetual home outside Australia. In

“Harding v FCT (2019)” the taxpayer was held as non-resident of Australia (Butler 2019).

The court stated that “permanent place of abode” must be interpreted to consider whether an

individual is permanently living in particular “state or country”.

183 Day Test:

An individual is held to be Australia occupant if they are present in Australia for

greater than 183 days or six months of an income year (Murray et al. 2018).

Commonwealth Superannuation test:

8TAXATION LAW

This test is useful on the members of a specific commonwealth superannuation fund.

Application:

To determine the residency position of John the four alternative tests are applied.

Residency Test:

Under resides test, John has physically not been present in Australia for a very long

time following and has organized all his personal belongings to Brunei. He has no intent of

coming back to Australia. Referring to “Dempsey v FCT (2014)” John is non-resident under

this test.

Domicile Test:

After moving to Brunei, John has conclusively stated his choice of domicile is in

Brunei when he further renewed his house lease for additional twelve months. John’s actions

indicate that he choose to stay far away from Australia for unspecified period. Citing

“Harding v FCT (2019)” John’s fixed domicile is in Brunei and he is non-resident under this

test.

183-Day Test:

John was physically not existent in Australia for 2017/18 and 2018/19. Consequently,

he is non-resident under this test.

Commonwealth Superannuation Test:

This test is not applicable in case of John.

Conclusion:

John will be treated as non-resident of Australia under the meaning of “sec 6 (1),

ITAA 1936” he has successfully passed all the four alternative test.

This test is useful on the members of a specific commonwealth superannuation fund.

Application:

To determine the residency position of John the four alternative tests are applied.

Residency Test:

Under resides test, John has physically not been present in Australia for a very long

time following and has organized all his personal belongings to Brunei. He has no intent of

coming back to Australia. Referring to “Dempsey v FCT (2014)” John is non-resident under

this test.

Domicile Test:

After moving to Brunei, John has conclusively stated his choice of domicile is in

Brunei when he further renewed his house lease for additional twelve months. John’s actions

indicate that he choose to stay far away from Australia for unspecified period. Citing

“Harding v FCT (2019)” John’s fixed domicile is in Brunei and he is non-resident under this

test.

183-Day Test:

John was physically not existent in Australia for 2017/18 and 2018/19. Consequently,

he is non-resident under this test.

Commonwealth Superannuation Test:

This test is not applicable in case of John.

Conclusion:

John will be treated as non-resident of Australia under the meaning of “sec 6 (1),

ITAA 1936” he has successfully passed all the four alternative test.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Case Study 2: Part A:

Issues:

Is the receipts from the sale of painting landscape undertaken during leisure amounts

to ordinary earnings from the commercial activity or a simple hobby under “section 995-1,

ITAA 1997”?

Rule:

As per “sec 6-5, ITAA 1997”, gains that arises from carrying the business is regarded as

ordinary earnings while gains arising from non-business activities are considered as hobby

and not held as taxable income (Morgan, Mortimer and Pinto 2018). To treat the receipts as

the ordinary earnings from the business activity there are two steps involved in it. Namely;

1. Establishing whether or not the taxpayer is conducting any business activities

2. Defining whether or not the receipts are obtained from the usual proceeds of that

commercial activity.

The legislative definition of business given in “sec 995-1, ITAA 1997” comprises of

any kind of business, trade, service, vocation or occupation but does not comprises of

occupation as the employee (Morgan and Castelyn 2018). It is vital to ascertain when a

pleasure activity or hobby turns into business. Common pointers that are measured by the

courts is whether an individual has any profit making intention. Likewise in “Stone v FCT

(2005)” lack of profit deriving intention generally do not prevent there is a business. The

scale of events combined with the nature or type of capital and turnover are some of the

common indicators of business activities.

The court in “FCT v Thomas (1972)” held that whether or not any commercial

approach undertaken by the taxpayer amounts to more than a frivolous activity is a common

indicators of business activity (Robin and Barkoczy 2019).

Case Study 2: Part A:

Issues:

Is the receipts from the sale of painting landscape undertaken during leisure amounts

to ordinary earnings from the commercial activity or a simple hobby under “section 995-1,

ITAA 1997”?

Rule:

As per “sec 6-5, ITAA 1997”, gains that arises from carrying the business is regarded as

ordinary earnings while gains arising from non-business activities are considered as hobby

and not held as taxable income (Morgan, Mortimer and Pinto 2018). To treat the receipts as

the ordinary earnings from the business activity there are two steps involved in it. Namely;

1. Establishing whether or not the taxpayer is conducting any business activities

2. Defining whether or not the receipts are obtained from the usual proceeds of that

commercial activity.

The legislative definition of business given in “sec 995-1, ITAA 1997” comprises of

any kind of business, trade, service, vocation or occupation but does not comprises of

occupation as the employee (Morgan and Castelyn 2018). It is vital to ascertain when a

pleasure activity or hobby turns into business. Common pointers that are measured by the

courts is whether an individual has any profit making intention. Likewise in “Stone v FCT

(2005)” lack of profit deriving intention generally do not prevent there is a business. The

scale of events combined with the nature or type of capital and turnover are some of the

common indicators of business activities.

The court in “FCT v Thomas (1972)” held that whether or not any commercial

approach undertaken by the taxpayer amounts to more than a frivolous activity is a common

indicators of business activity (Robin and Barkoczy 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Application:

Nadine during her leisure time paints landscape in order to relieve stress from her

accountant work. After a suggestion by one of Nadine’s friend she displays three pieces of

painting in the market. She receive a total of $4,500 from her painting sales excluding the

material cost of $800.

The receipts of $4,500 from the sale of artwork by Nadine cannot be treated as

carrying on the business activities. This is because Nadine’s artwork is purely to relieve her

stress and it is undertaken for recreational purpose. Referring to “Stone v FCT (2005)” there

is a clear lack of profit making intention by Nadine since it does not involve any degree of

planning and neither she invest any significant amount of time.

To support further, no such commercial approach or effort was taken by Nadine to

sell her paintings and she only attends the market stall when she has a painting to sell. The

purpose of her painting is only to reduce her stress instead of any actual profit making

intention. Citing “FCT v Thomas (1972)” it can be stated that Nadine’s receipts constitute

gains from non-business activities (Bankman et al. 2018). It is simply hobby or pleasure and

it is non-assessable income under “sec 6-5, ITAA 1997”.

Conclusion:

Conclusively, the receipts from sale of painting by Nadine is gains from hobby or

non-business activities and it is non-assessable income.

Application:

Nadine during her leisure time paints landscape in order to relieve stress from her

accountant work. After a suggestion by one of Nadine’s friend she displays three pieces of

painting in the market. She receive a total of $4,500 from her painting sales excluding the

material cost of $800.

The receipts of $4,500 from the sale of artwork by Nadine cannot be treated as

carrying on the business activities. This is because Nadine’s artwork is purely to relieve her

stress and it is undertaken for recreational purpose. Referring to “Stone v FCT (2005)” there

is a clear lack of profit making intention by Nadine since it does not involve any degree of

planning and neither she invest any significant amount of time.

To support further, no such commercial approach or effort was taken by Nadine to

sell her paintings and she only attends the market stall when she has a painting to sell. The

purpose of her painting is only to reduce her stress instead of any actual profit making

intention. Citing “FCT v Thomas (1972)” it can be stated that Nadine’s receipts constitute

gains from non-business activities (Bankman et al. 2018). It is simply hobby or pleasure and

it is non-assessable income under “sec 6-5, ITAA 1997”.

Conclusion:

Conclusively, the receipts from sale of painting by Nadine is gains from hobby or

non-business activities and it is non-assessable income.

11TAXATION LAW

Case Study Three

Issues:

Is the receipts derived from the ordinary business course and employment services

amounts to earnings under the ordinary perception of “section 6-5, ITAA 1997”.

Rule:

A receipt that is received from the usual earnings of the business is treated as ordinary

income under “section 6-5, ITAA 1997”. To characterize the receipt as the portion of usual

business profits requires determining whether the receipts has relation with the recognized

business activities (Schmalbeck, Zelenak and Lawsky 2015). A receipt is generally treated as

usual profits of business when it is earned as the portion of ordinary commercial activity.

Gifts that is received for the personal qualities is not viewed as ordinary income. The

law court in “Scott v FCT (1966)” explained that a mere gift received out of individual

relationship amongst the parties is not viewed as income.

A receipt that is received by an employee from the service and providing individual

services will attract income tax under ordinary perception of “section 6-5, ITAA 1997”. As

held in “Dean v FCT (1997)” remuneration from employment was considered as income

under ordinary concept (Miller and Oats 2016).

When an individual receives interest it is deemed taxable under the “section 15-35”.

While prizes and casual winnings are considered as non-taxable windfall gains when it is

derived by fluke. The court in “Moore v Griffiths (1972)” held that mere prizes are not

considered income.

The potential of “section 8-1, ITAA 1997” is valid to everyone. A taxpayer is

permitted to obtain deduction from their calculable earnings an expense or loss till the extent

Case Study Three

Issues:

Is the receipts derived from the ordinary business course and employment services

amounts to earnings under the ordinary perception of “section 6-5, ITAA 1997”.

Rule:

A receipt that is received from the usual earnings of the business is treated as ordinary

income under “section 6-5, ITAA 1997”. To characterize the receipt as the portion of usual

business profits requires determining whether the receipts has relation with the recognized

business activities (Schmalbeck, Zelenak and Lawsky 2015). A receipt is generally treated as

usual profits of business when it is earned as the portion of ordinary commercial activity.

Gifts that is received for the personal qualities is not viewed as ordinary income. The

law court in “Scott v FCT (1966)” explained that a mere gift received out of individual

relationship amongst the parties is not viewed as income.

A receipt that is received by an employee from the service and providing individual

services will attract income tax under ordinary perception of “section 6-5, ITAA 1997”. As

held in “Dean v FCT (1997)” remuneration from employment was considered as income

under ordinary concept (Miller and Oats 2016).

When an individual receives interest it is deemed taxable under the “section 15-35”.

While prizes and casual winnings are considered as non-taxable windfall gains when it is

derived by fluke. The court in “Moore v Griffiths (1972)” held that mere prizes are not

considered income.

The potential of “section 8-1, ITAA 1997” is valid to everyone. A taxpayer is

permitted to obtain deduction from their calculable earnings an expense or loss till the extent

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.