Holmes Institute Faculty of Higher Education Taxation Law Assignment

VerifiedAdded on 2022/12/01

|14

|2777

|448

Homework Assignment

AI Summary

This assignment solution addresses key aspects of Australian taxation law, focusing on Capital Gains Tax (CGT) and capital allowance. The assignment begins with an introduction to CGT, explaining its implications and the importance of tax planning. The first part of the solution provides professional advice to an Australian resident, Jasmine, on the CGT consequences of selling assets before moving to the UK, covering CGT events, assets, exemptions, and residential status. The second part delves into capital allowance, specifically for a CNC machine acquired by John, detailing the calculation of the machine's cost and the start time for the decline in value. The analysis includes relevant legislation and rulings, providing a comprehensive overview of taxation liabilities and allowances. This assignment is a valuable resource for students studying taxation law, offering practical examples and insights into complex tax concepts.

Running head: - Taxation liabilities

1

AUSTRALIAN TAXATION LAW

CAPITAL GAINS TAX AND CAPITAL ALLOWANCE

Student’s Name:

ID:

Module:

Instructor:

Date of Submission:

Word Count:

1

AUSTRALIAN TAXATION LAW

CAPITAL GAINS TAX AND CAPITAL ALLOWANCE

Student’s Name:

ID:

Module:

Instructor:

Date of Submission:

Word Count:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation liabilities

2

Table of Contents

Introduction.................................................................................................................................................3

Answer to question no- 1............................................................................................................................3

Professional Advise to Jasmine, an Australian Resident, on CGT Consequences of Her Sale of Assets

before Leaving Australia for the UK.........................................................................................................3

Answer to question no- 2............................................................................................................................9

Capital Allowance for CNC Machine Acquired by John............................................................................9

Conclusion.................................................................................................................................................11

References.................................................................................................................................................11

2

Table of Contents

Introduction.................................................................................................................................................3

Answer to question no- 1............................................................................................................................3

Professional Advise to Jasmine, an Australian Resident, on CGT Consequences of Her Sale of Assets

before Leaving Australia for the UK.........................................................................................................3

Answer to question no- 2............................................................................................................................9

Capital Allowance for CNC Machine Acquired by John............................................................................9

Conclusion.................................................................................................................................................11

References.................................................................................................................................................11

Taxation liabilities

3

Introduction

With the changes in time, taxation rules and regulations have been changing. However, in

order to compute the proper taxation liabilities of the tax payer, there is need to implement the

proper tax planning as per the applicable taxation rules and regulations. It is considered that

capital gains tax (CGT) was introduced to the Australian taxation system in 1985. As such CGT

applies to any asset acquired after 20th September, 1985, subject to certain exemptions.

Australian Tax Office defines capital gain as the positive difference between the price that

assesse receives on disposal of the asset and the cost of the asset to the assesse. This report

reflects the key aspects of the taxation liabilities in the different situations.

Answer to question no- 1

Professional Advise to Jasmine, an Australian Resident, on CGT Consequences of Her

Sale of Assets before Leaving Australia for the UK

The assessee is required to report the capital gain or loss in the income tax return for the

purpose of paying CGT as part of income tax. As capital gain is added with the income, it might

significantly increase the income tax liability of the assessee. Since there is no provision in

Australian tax system for withholding CGT, the taxable capital gain needs to be worked out

earlier in order to make funds available to meet the tax obligation.

Australian taxation system has the provision of offsetting capital losses against capital

gains, and carrying forward the net capital loss for an indefinite period, but capital loss cannot be

offset against normal income of the assessee.

Capital Gains Tax (CGT) Event

According to Australian Tax Office (ATO) following are considered as CGT event

whether gain or loss (Australian Government, 2019):

i) An asset is sold or given away to someone else,

3

Introduction

With the changes in time, taxation rules and regulations have been changing. However, in

order to compute the proper taxation liabilities of the tax payer, there is need to implement the

proper tax planning as per the applicable taxation rules and regulations. It is considered that

capital gains tax (CGT) was introduced to the Australian taxation system in 1985. As such CGT

applies to any asset acquired after 20th September, 1985, subject to certain exemptions.

Australian Tax Office defines capital gain as the positive difference between the price that

assesse receives on disposal of the asset and the cost of the asset to the assesse. This report

reflects the key aspects of the taxation liabilities in the different situations.

Answer to question no- 1

Professional Advise to Jasmine, an Australian Resident, on CGT Consequences of Her

Sale of Assets before Leaving Australia for the UK

The assessee is required to report the capital gain or loss in the income tax return for the

purpose of paying CGT as part of income tax. As capital gain is added with the income, it might

significantly increase the income tax liability of the assessee. Since there is no provision in

Australian tax system for withholding CGT, the taxable capital gain needs to be worked out

earlier in order to make funds available to meet the tax obligation.

Australian taxation system has the provision of offsetting capital losses against capital

gains, and carrying forward the net capital loss for an indefinite period, but capital loss cannot be

offset against normal income of the assessee.

Capital Gains Tax (CGT) Event

According to Australian Tax Office (ATO) following are considered as CGT event

whether gain or loss (Australian Government, 2019):

i) An asset is sold or given away to someone else,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation liabilities

4

ii) An asset is lost or destroyed,

iii) Owned shares are cancelled, redeemed or surrendered,

iv) The taxpayer ceases to be an Australian resident,

v) As a shareholder the person receives payment, other than dividend, from the company.

Capital Gains Tax (CGT) Assets

All assets acquired by the taxpayer since the inception of CGT are subject to CGT, if not

exempted specifically (Australian Taxation Office, 2019). Following is a succinct list of CGT

assets:

Real estate: Most of the real estate assets are subject to CGT. This includes houses, vacant land,

rental properties, hobby farms, and holiday homes.

Shares and other investments: Company shares and units in a unit trust are subject to CGT,

unless those were acquired before 20 September, 1985. However gain on shares sold as part of

business activities is not subject to CGT, rather it is treated as ordinary income.

Crypto-currency: This is a digital asset, and gain on its sale is subject to CGT.

Leases, licenses, goodwill, contractual rights: Intangible assets are subject to CGT if they were

active assets.

Personal use assets: Personal use assets for CGT purpose includes furniture, electronic goods,

household items, and boats etc. which are kept for personal enjoyment.

Collectables: Collectables are items of personal enjoyment or enjoyment of associates of the

assessee. Section 108 of the Capital Gains Tax 1985 list certain items as collectables and subject

to CGT (Australian Taxation Office, 2019). These include. Sculptures, drawings, paintings,

engravings or photographs, reproductions of these items. or similar property, antiques, jewellery,

postage stamps or first day covers, rare manuscripts, books, folios.

Assets Exempted from CGT

4

ii) An asset is lost or destroyed,

iii) Owned shares are cancelled, redeemed or surrendered,

iv) The taxpayer ceases to be an Australian resident,

v) As a shareholder the person receives payment, other than dividend, from the company.

Capital Gains Tax (CGT) Assets

All assets acquired by the taxpayer since the inception of CGT are subject to CGT, if not

exempted specifically (Australian Taxation Office, 2019). Following is a succinct list of CGT

assets:

Real estate: Most of the real estate assets are subject to CGT. This includes houses, vacant land,

rental properties, hobby farms, and holiday homes.

Shares and other investments: Company shares and units in a unit trust are subject to CGT,

unless those were acquired before 20 September, 1985. However gain on shares sold as part of

business activities is not subject to CGT, rather it is treated as ordinary income.

Crypto-currency: This is a digital asset, and gain on its sale is subject to CGT.

Leases, licenses, goodwill, contractual rights: Intangible assets are subject to CGT if they were

active assets.

Personal use assets: Personal use assets for CGT purpose includes furniture, electronic goods,

household items, and boats etc. which are kept for personal enjoyment.

Collectables: Collectables are items of personal enjoyment or enjoyment of associates of the

assessee. Section 108 of the Capital Gains Tax 1985 list certain items as collectables and subject

to CGT (Australian Taxation Office, 2019). These include. Sculptures, drawings, paintings,

engravings or photographs, reproductions of these items. or similar property, antiques, jewellery,

postage stamps or first day covers, rare manuscripts, books, folios.

Assets Exempted from CGT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation liabilities

5

It is analyzed that some assets are exempt from CGT. Gain from such assets are not included in

the income, neither any loss from these assets are allowed to be used to offset against capital gain

to reduce taxable income.

Main home of the taxpayer: Main home of the assessee is exempt from CGT, if the taxpayer and

her family lived in the house, the address of the house is used as mailing address, the personal

belongings of the taxpayer are in that house, the address of the house is in electoral role, and the

house has gas and electricity connections. If the taxpayer was not a resident of Australia for CGT

purpose while living in the house, then this exemption cannot be availed.

Personal use assets: Any personal use asset acquired for less than $10,000 is exempt from CGT.

Collectibles: According to subsection 108 – 10(2) collectibles acquired for $500 or less are

disregarded for the purpose of CGT, nor any loss from sale of such items can be used to offset

against capital gain.

Depreciating assets: Any depreciating asset used by the assessee solely for taxable purpose is not

subject to CGT. Business equipment, items in rental property are examples of depreciating asset.

Assets not in the depreciation pool however are subject to CGT, and any gain or loss from sale of

these assets is added with assessable income or deduction can be claimed as the case may be.

However, assets not treated for taxable purpose and used for private purpose are subject to CGT.

Pre-CGT assets: Assets acquired prior to 20 September, 1985 are exempted for computation of

CGT. As per Taxation Ruling TR 2004/18, exceptions to such exemption are pre-CGT shares in

private companies and interests in private trusts where CGT event arises due to combination of

more than one factors (Australian Taxation office, 2019). These assets are subject to CGT

(Woellner, et al. 2010).

Car and motor cycle: According to Section 118 – 5 of the Income Tax Assessment Act 1997, any

gain or loss arising from sale of cat, motor cycle or any other similar vehicle is to be disregarded

for the purpose of CGT. Subsection 995 – 1(1) of the Income Tax Assessment Act 1997 defines

car as a motor vehicle capable of carrying a load of less than 1 tonne and less than 9 passengers.

According to Section 108 – 10(2) a car is a CGT asset if it is antique. Taxation Determination

1999/40 defines an antique car which is at least 100 years old.

5

It is analyzed that some assets are exempt from CGT. Gain from such assets are not included in

the income, neither any loss from these assets are allowed to be used to offset against capital gain

to reduce taxable income.

Main home of the taxpayer: Main home of the assessee is exempt from CGT, if the taxpayer and

her family lived in the house, the address of the house is used as mailing address, the personal

belongings of the taxpayer are in that house, the address of the house is in electoral role, and the

house has gas and electricity connections. If the taxpayer was not a resident of Australia for CGT

purpose while living in the house, then this exemption cannot be availed.

Personal use assets: Any personal use asset acquired for less than $10,000 is exempt from CGT.

Collectibles: According to subsection 108 – 10(2) collectibles acquired for $500 or less are

disregarded for the purpose of CGT, nor any loss from sale of such items can be used to offset

against capital gain.

Depreciating assets: Any depreciating asset used by the assessee solely for taxable purpose is not

subject to CGT. Business equipment, items in rental property are examples of depreciating asset.

Assets not in the depreciation pool however are subject to CGT, and any gain or loss from sale of

these assets is added with assessable income or deduction can be claimed as the case may be.

However, assets not treated for taxable purpose and used for private purpose are subject to CGT.

Pre-CGT assets: Assets acquired prior to 20 September, 1985 are exempted for computation of

CGT. As per Taxation Ruling TR 2004/18, exceptions to such exemption are pre-CGT shares in

private companies and interests in private trusts where CGT event arises due to combination of

more than one factors (Australian Taxation office, 2019). These assets are subject to CGT

(Woellner, et al. 2010).

Car and motor cycle: According to Section 118 – 5 of the Income Tax Assessment Act 1997, any

gain or loss arising from sale of cat, motor cycle or any other similar vehicle is to be disregarded

for the purpose of CGT. Subsection 995 – 1(1) of the Income Tax Assessment Act 1997 defines

car as a motor vehicle capable of carrying a load of less than 1 tonne and less than 9 passengers.

According to Section 108 – 10(2) a car is a CGT asset if it is antique. Taxation Determination

1999/40 defines an antique car which is at least 100 years old.

Taxation liabilities

6

Resident for Tax Purpose

Residential status of an assessee is important for deciding upon how one would be taxed in

Australia. Australian Tax Office has set different standards to the Department of Immigration

and Border Protection for determining residential status for the purpose of tax. This ensures that

an Australian taxpayer pays tax in accordance with the set standards irrespective of the place of

residence of the taxpayer (Braithwaite, and Reinhart, 2019)

A taxpayer is considered a resident for tax purposes if any of the following conditions are met;

i) The person has always lived in Australia,

ii) The person has moved into Australia from overseas but intends to live in Australia for a

foreseeable future,

iii) The person stayed in Australia for half of the income year, provided s/he has no home abroad

and wants to live in Australia,

iv) The person is an overseas student enrolled in a study course in Australia which has more than

6 months duration (McBarnet, 2019).

On the basis of above findings the consequences of sale of assets are presented in the following

table (Symes, 2016).

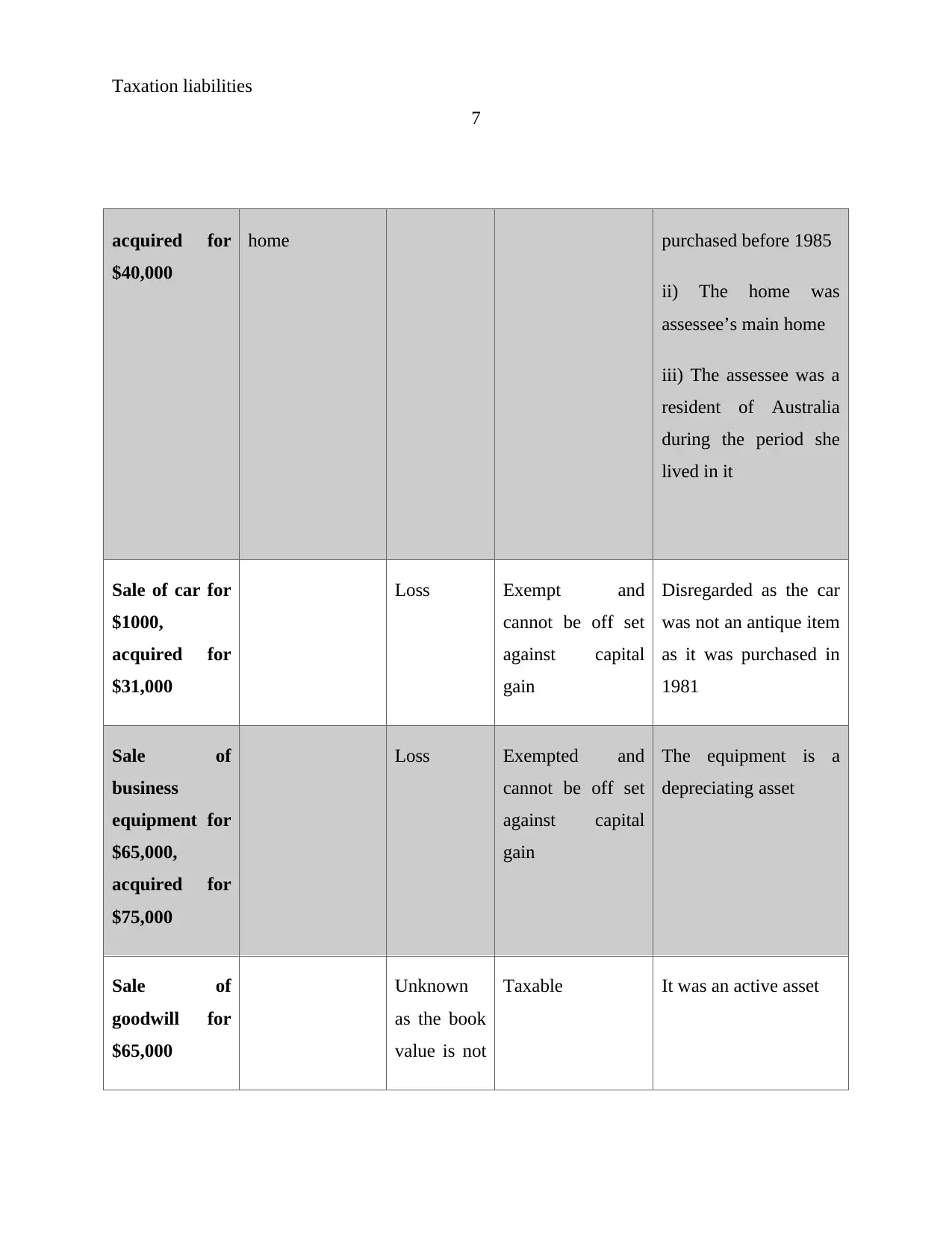

Table showing CGT consequences of sale of assets by Jasmine

CGT Event Residential

Status

Gain/Loss CGT

Consequence

Reason/Explanation

Sale of home

for $650,000,

Resident while

living in the

Gain Excluded i) The asset was

6

Resident for Tax Purpose

Residential status of an assessee is important for deciding upon how one would be taxed in

Australia. Australian Tax Office has set different standards to the Department of Immigration

and Border Protection for determining residential status for the purpose of tax. This ensures that

an Australian taxpayer pays tax in accordance with the set standards irrespective of the place of

residence of the taxpayer (Braithwaite, and Reinhart, 2019)

A taxpayer is considered a resident for tax purposes if any of the following conditions are met;

i) The person has always lived in Australia,

ii) The person has moved into Australia from overseas but intends to live in Australia for a

foreseeable future,

iii) The person stayed in Australia for half of the income year, provided s/he has no home abroad

and wants to live in Australia,

iv) The person is an overseas student enrolled in a study course in Australia which has more than

6 months duration (McBarnet, 2019).

On the basis of above findings the consequences of sale of assets are presented in the following

table (Symes, 2016).

Table showing CGT consequences of sale of assets by Jasmine

CGT Event Residential

Status

Gain/Loss CGT

Consequence

Reason/Explanation

Sale of home

for $650,000,

Resident while

living in the

Gain Excluded i) The asset was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation liabilities

7

acquired for

$40,000

home purchased before 1985

ii) The home was

assessee’s main home

iii) The assessee was a

resident of Australia

during the period she

lived in it

Sale of car for

$1000,

acquired for

$31,000

Loss Exempt and

cannot be off set

against capital

gain

Disregarded as the car

was not an antique item

as it was purchased in

1981

Sale of

business

equipment for

$65,000,

acquired for

$75,000

Loss Exempted and

cannot be off set

against capital

gain

The equipment is a

depreciating asset

Sale of

goodwill for

$65,000

Unknown

as the book

value is not

Taxable It was an active asset

7

acquired for

$40,000

home purchased before 1985

ii) The home was

assessee’s main home

iii) The assessee was a

resident of Australia

during the period she

lived in it

Sale of car for

$1000,

acquired for

$31,000

Loss Exempt and

cannot be off set

against capital

gain

Disregarded as the car

was not an antique item

as it was purchased in

1981

Sale of

business

equipment for

$65,000,

acquired for

$75,000

Loss Exempted and

cannot be off set

against capital

gain

The equipment is a

depreciating asset

Sale of

goodwill for

$65,000

Unknown

as the book

value is not

Taxable It was an active asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation liabilities

8

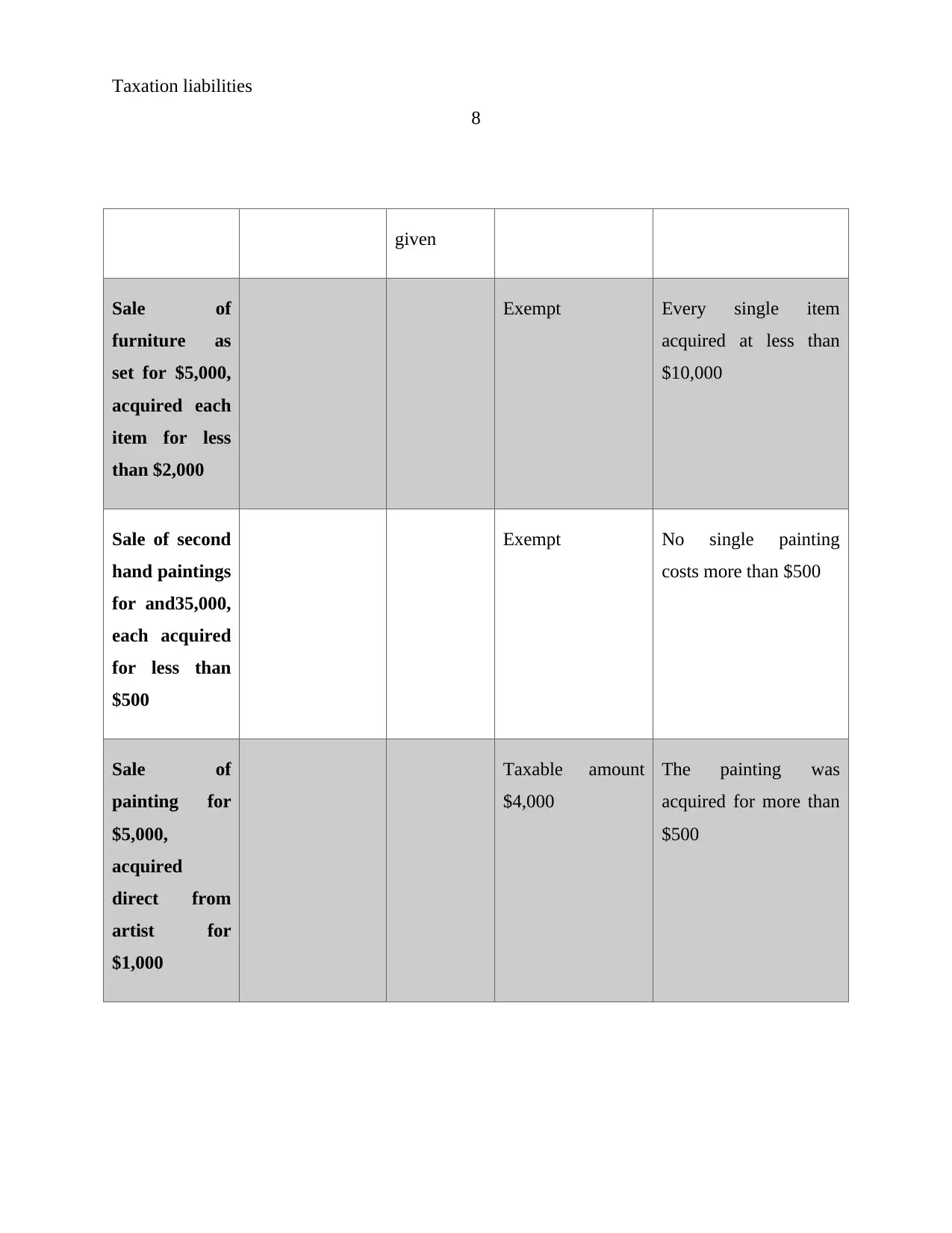

given

Sale of

furniture as

set for $5,000,

acquired each

item for less

than $2,000

Exempt Every single item

acquired at less than

$10,000

Sale of second

hand paintings

for and35,000,

each acquired

for less than

$500

Exempt No single painting

costs more than $500

Sale of

painting for

$5,000,

acquired

direct from

artist for

$1,000

Taxable amount

$4,000

The painting was

acquired for more than

$500

8

given

Sale of

furniture as

set for $5,000,

acquired each

item for less

than $2,000

Exempt Every single item

acquired at less than

$10,000

Sale of second

hand paintings

for and35,000,

each acquired

for less than

$500

Exempt No single painting

costs more than $500

Sale of

painting for

$5,000,

acquired

direct from

artist for

$1,000

Taxable amount

$4,000

The painting was

acquired for more than

$500

Taxation liabilities

9

Answer to question no- 2

Capital Allowance for CNC Machine Acquired by John

Capital Allowance

Capital allowance, also called tax depreciation, is a deduction available for decline in the value

of an asset (Capital Claims, 2019). It is a tax relief for certain capital expenditures. The entire

cost of an asset cannot be deducted in one single year as per taxation and accounting rules.

Capital allowances are available to assets for which annual investment allowance (AIA) is not

applicable (Australian Taxation Office, 2019). Capital allowance can be claimed for an asset up

to 40 years (Barkoczy, 2016).

Australian Taxation Office has adopted Uniform Capital Allowance Rules on 1 July 2001 for all

kinds of depreciating assets (Australian Taxation Office, 2019). The UCA incorporates a range

of capital allowance provisions that existed earlier in relation to plant and equipment. A set of

general rules is provided by UCA for calculation of deduction for decline in value of

depreciating assets. Some concessions are provided in the rule for primary production

depreciating assets (Australian Taxation Office, 2019). The UCA rule also provides for

deductions for certain capital expenditures which was not available before implementation of the

rule (Braithwaite, and Reinhart, 2019).

Cost of the CNC Machine for the Purpose of Capital Allowance

In order to determine the capital allowance pertaining to a depreciating asset, it is imperative to

determine the cost of the asset. For the purpose of UCA there are two elements for calculating

the cost (McBarnet, 2019). The first element of cost includes the price directly associated with

holding of the asset. Examples of such expenses are purchase price of the asset, travelling cost,

and other costs that are directly related to holding the asset. The second element of cost includes

any cost incurred after the first element for bringing the asset into present condition, location,

9

Answer to question no- 2

Capital Allowance for CNC Machine Acquired by John

Capital Allowance

Capital allowance, also called tax depreciation, is a deduction available for decline in the value

of an asset (Capital Claims, 2019). It is a tax relief for certain capital expenditures. The entire

cost of an asset cannot be deducted in one single year as per taxation and accounting rules.

Capital allowances are available to assets for which annual investment allowance (AIA) is not

applicable (Australian Taxation Office, 2019). Capital allowance can be claimed for an asset up

to 40 years (Barkoczy, 2016).

Australian Taxation Office has adopted Uniform Capital Allowance Rules on 1 July 2001 for all

kinds of depreciating assets (Australian Taxation Office, 2019). The UCA incorporates a range

of capital allowance provisions that existed earlier in relation to plant and equipment. A set of

general rules is provided by UCA for calculation of deduction for decline in value of

depreciating assets. Some concessions are provided in the rule for primary production

depreciating assets (Australian Taxation Office, 2019). The UCA rule also provides for

deductions for certain capital expenditures which was not available before implementation of the

rule (Braithwaite, and Reinhart, 2019).

Cost of the CNC Machine for the Purpose of Capital Allowance

In order to determine the capital allowance pertaining to a depreciating asset, it is imperative to

determine the cost of the asset. For the purpose of UCA there are two elements for calculating

the cost (McBarnet, 2019). The first element of cost includes the price directly associated with

holding of the asset. Examples of such expenses are purchase price of the asset, travelling cost,

and other costs that are directly related to holding the asset. The second element of cost includes

any cost incurred after the first element for bringing the asset into present condition, location,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation liabilities

10

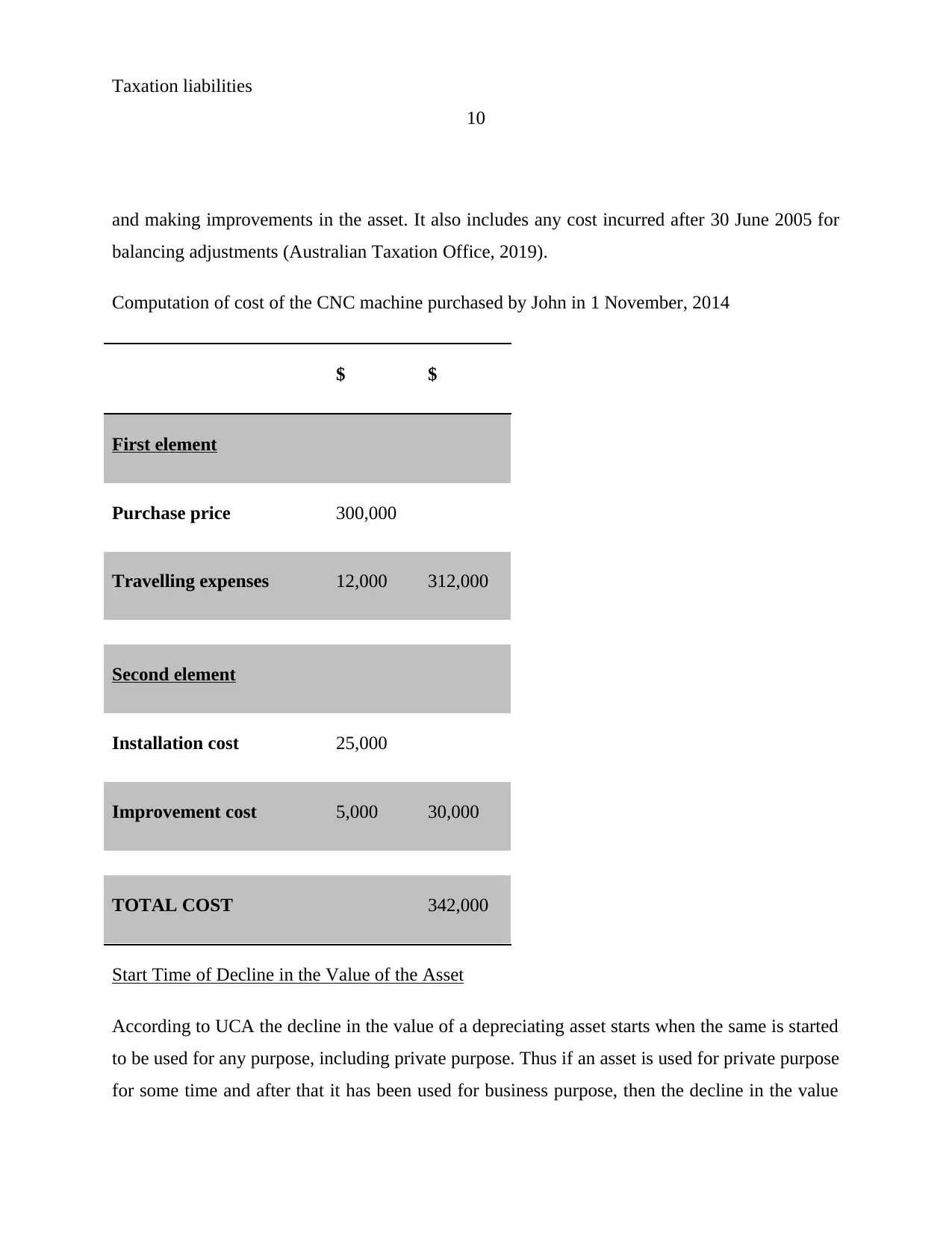

and making improvements in the asset. It also includes any cost incurred after 30 June 2005 for

balancing adjustments (Australian Taxation Office, 2019).

Computation of cost of the CNC machine purchased by John in 1 November, 2014

$ $

First element

Purchase price 300,000

Travelling expenses 12,000 312,000

Second element

Installation cost 25,000

Improvement cost 5,000 30,000

TOTAL COST 342,000

Start Time of Decline in the Value of the Asset

According to UCA the decline in the value of a depreciating asset starts when the same is started

to be used for any purpose, including private purpose. Thus if an asset is used for private purpose

for some time and after that it has been used for business purpose, then the decline in the value

10

and making improvements in the asset. It also includes any cost incurred after 30 June 2005 for

balancing adjustments (Australian Taxation Office, 2019).

Computation of cost of the CNC machine purchased by John in 1 November, 2014

$ $

First element

Purchase price 300,000

Travelling expenses 12,000 312,000

Second element

Installation cost 25,000

Improvement cost 5,000 30,000

TOTAL COST 342,000

Start Time of Decline in the Value of the Asset

According to UCA the decline in the value of a depreciating asset starts when the same is started

to be used for any purpose, including private purpose. Thus if an asset is used for private purpose

for some time and after that it has been used for business purpose, then the decline in the value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation liabilities

11

would start when the asset was first installed for private purpose (Australian Taxation Office,

2019).

John purchased the machine on 1 November 2014, and the machine was installed on 1 January

2015. Installation was complete only after a guiding rod was installed on 15 February 2015.

Hence the decline in the value of the CNC machine would start from 15 February 2015.

Conclusion

After assessing the income tax of assess, it is found that If the cost of acquisition of the

assets exceeds the price at which it is disposed of, the result is capital loss. Capital gain tax is not

separately payable in Australia but it is added with the income of the assessee in the same year

when the capital gain for the assessee takes place. However, if capital gain arises out of sale of

an asset which was held by the assessee for at least 1 year, then the capital gain is discounted by

50% for individual taxpayers, and by 33.3% for superannuation funds.

11

would start when the asset was first installed for private purpose (Australian Taxation Office,

2019).

John purchased the machine on 1 November 2014, and the machine was installed on 1 January

2015. Installation was complete only after a guiding rod was installed on 15 February 2015.

Hence the decline in the value of the CNC machine would start from 15 February 2015.

Conclusion

After assessing the income tax of assess, it is found that If the cost of acquisition of the

assets exceeds the price at which it is disposed of, the result is capital loss. Capital gain tax is not

separately payable in Australia but it is added with the income of the assessee in the same year

when the capital gain for the assessee takes place. However, if capital gain arises out of sale of

an asset which was held by the assessee for at least 1 year, then the capital gain is discounted by

50% for individual taxpayers, and by 33.3% for superannuation funds.

Taxation liabilities

12

References

Australian Government (2019). Capital Gains Tax (CGT). [online] accessed on 21st September

2019 available at https://www.business.gov.au/finance/taxation/capital-gains-tax

Australian Taxation Office (2019). CGT assets and exemptions. [online] accessed on 21st

September, available at https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-

exemptions/#Exemptions1

Australian Taxation Office (2019). Other capital assets and expense deductions. [online]

retrieved from https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-

allowances/other-capital-asset-and-expense-deductions/ on 21 September 2019

Australian Taxation Office (2019). Uniform capital allowance system: calculating the decline in

value of depreciating assets. . [online] accessed on 21st September, available at

https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/In-detail/

Depreciating-assets/Uniform-capital-allowance-system--calculating-the-decline-in-value-of-a-

depreciating-asset/

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V., and Reinhart, M. (2019). The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Braithwaite, V., and Reinhart, M. (2019). The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

12

References

Australian Government (2019). Capital Gains Tax (CGT). [online] accessed on 21st September

2019 available at https://www.business.gov.au/finance/taxation/capital-gains-tax

Australian Taxation Office (2019). CGT assets and exemptions. [online] accessed on 21st

September, available at https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-

exemptions/#Exemptions1

Australian Taxation Office (2019). Other capital assets and expense deductions. [online]

retrieved from https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-

allowances/other-capital-asset-and-expense-deductions/ on 21 September 2019

Australian Taxation Office (2019). Uniform capital allowance system: calculating the decline in

value of depreciating assets. . [online] accessed on 21st September, available at

https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/In-detail/

Depreciating-assets/Uniform-capital-allowance-system--calculating-the-decline-in-value-of-a-

depreciating-asset/

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V., and Reinhart, M. (2019). The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Braithwaite, V., and Reinhart, M. (2019). The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.