Taxation Law Assignment: Income, Deductions, CGT Analysis, UTS

VerifiedAdded on 2023/06/04

|10

|2353

|377

Report

AI Summary

This assignment provides a detailed analysis of taxation law, focusing on assessable income, allowable deductions, and capital gains tax (CGT) implications. It examines various scenarios related to an accountant's income, including salary, bonuses, awards, and business activities. The report applies relevant sections of the ITAA 1936 and ITAA 1997, along with case law, to determine the tax consequences of different income streams and expenses. Key issues addressed include the deductibility of clothing expenses, travel expenses, and the tax treatment of prizes and awards. Furthermore, the assignment explores the CGT implications of selling collectables and the destruction of a rental property, providing a comprehensive overview of the relevant tax principles and their application to real-world scenarios. Desklib offers this and many other solved assignments to aid students in their studies.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Introduction to Taxation Law.....................................................................................................2

Headings:....................................................................................................................................2

Issue:..........................................................................................................................................2

Rules:..........................................................................................................................................2

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Introduction to Taxation Law.....................................................................................................2

Headings:....................................................................................................................................2

Issue:..........................................................................................................................................2

Rules:..........................................................................................................................................2

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

2TAXATION LAW

Introduction to Taxation Law

Headings:

This is income tax problems relating to the tax consequences of assessable income

and allowable deductions.

Issue:

The issues involve: (1) whether the taxpayer be held assessable under the “section 6-

5 of the ITAA 1997”; and (2) whether the taxpayer be entitled to claim the allowable

deductions under “section 8-1 of the ITAA 1997”.

Rules:

As per “section 6, ITAA 1936” income from the personal exertion or income obtained

from the personal exertion implies income comprising of the wages, salaries, commission,

fees, allowance and gratuities received from carrying on of the business1. According to

“Section 6-5, ITAA 1997” commonly, most part of the income that comes into the taxpayer

is treated as income in terms of the ordinary concepts. In “Dean & Anor v FC of T (1997)

ATC 4762” retention payment that is given as the consideration to the key employees for

agreeing to remain employed for 12 months after buyout was treated as income.

The court stated that nexus is not effected by the lump sum or the one-off receipts for

performing the particular task. In “Brent v FCT (1971) 125 CLR 418” reward given to the

wife of train robber for the purpose of providing exclusive media rights of publishing her life

story would be treated as income2.

1 Barkoczy, Stephen, Foundations Of Taxation Law 2014

2 Brokelind, Cécile, Principles Of Law 2014.

Introduction to Taxation Law

Headings:

This is income tax problems relating to the tax consequences of assessable income

and allowable deductions.

Issue:

The issues involve: (1) whether the taxpayer be held assessable under the “section 6-

5 of the ITAA 1997”; and (2) whether the taxpayer be entitled to claim the allowable

deductions under “section 8-1 of the ITAA 1997”.

Rules:

As per “section 6, ITAA 1936” income from the personal exertion or income obtained

from the personal exertion implies income comprising of the wages, salaries, commission,

fees, allowance and gratuities received from carrying on of the business1. According to

“Section 6-5, ITAA 1997” commonly, most part of the income that comes into the taxpayer

is treated as income in terms of the ordinary concepts. In “Dean & Anor v FC of T (1997)

ATC 4762” retention payment that is given as the consideration to the key employees for

agreeing to remain employed for 12 months after buyout was treated as income.

The court stated that nexus is not effected by the lump sum or the one-off receipts for

performing the particular task. In “Brent v FCT (1971) 125 CLR 418” reward given to the

wife of train robber for the purpose of providing exclusive media rights of publishing her life

story would be treated as income2.

1 Barkoczy, Stephen, Foundations Of Taxation Law 2014

2 Brokelind, Cécile, Principles Of Law 2014.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

As per “section 15-2, ITAA 1997” the taxable income of the person should include

the value of the allowance, gratuities, compensation and benefits provided to the person in

relation to any employment or the services rendered by an individual.

According to “section 8-1, ITAA 1997” cost incurred for acquiring the ordinary items

of clothing such as suits are not regarded as deductible expenditure. As held in “Mansfield v

FC of T (1996) ATC 4001” the taxpayer was denied deduction on the ordinary articles of

apparel irrespective of fact that such expenses were necessary to make her appearance

suitable in a particular job or profession3.

Mere prize is not treated as income however will be held as income if the prize holds

appropriate association with the income producing activities of the taxpayer. As held in

“Kelly v FCT (1985) 85 ATC 4283” award received by the professional footballer for being

the best and fairest player was treated as income. The sum was assessable as income since it

was relevant to his employment by the club and associated to the employee’s skill.

As per the legislative response of “section 25-100 ITAA 1997” permits the taxpayer

with the deductions relating to the cost of travel between the workplaces4. Travel should be

directly related between the income generating activities are performed and none of the place

is the assessor home. The court in “FCT v Wiener (1978) ATC 4006” allowed the taxpayer

with deduction for traveling between schools as the taxpayer was travelling in the

performance of her duties.

The legislative definition of business defined in section 995-1 refers to the profession,

trade, employment, vocation or calling but does not comprises of occupation in capacity of

3 Coleman, Cynthia and Kerrie Sadiq, Principles Of Taxation Law 2013

4 Graetz, Michael J, Deborah H Schenk and Anne Alstott, Federal Income Taxation 2015.

As per “section 15-2, ITAA 1997” the taxable income of the person should include

the value of the allowance, gratuities, compensation and benefits provided to the person in

relation to any employment or the services rendered by an individual.

According to “section 8-1, ITAA 1997” cost incurred for acquiring the ordinary items

of clothing such as suits are not regarded as deductible expenditure. As held in “Mansfield v

FC of T (1996) ATC 4001” the taxpayer was denied deduction on the ordinary articles of

apparel irrespective of fact that such expenses were necessary to make her appearance

suitable in a particular job or profession3.

Mere prize is not treated as income however will be held as income if the prize holds

appropriate association with the income producing activities of the taxpayer. As held in

“Kelly v FCT (1985) 85 ATC 4283” award received by the professional footballer for being

the best and fairest player was treated as income. The sum was assessable as income since it

was relevant to his employment by the club and associated to the employee’s skill.

As per the legislative response of “section 25-100 ITAA 1997” permits the taxpayer

with the deductions relating to the cost of travel between the workplaces4. Travel should be

directly related between the income generating activities are performed and none of the place

is the assessor home. The court in “FCT v Wiener (1978) ATC 4006” allowed the taxpayer

with deduction for traveling between schools as the taxpayer was travelling in the

performance of her duties.

The legislative definition of business defined in section 995-1 refers to the profession,

trade, employment, vocation or calling but does not comprises of occupation in capacity of

3 Coleman, Cynthia and Kerrie Sadiq, Principles Of Taxation Law 2013

4 Graetz, Michael J, Deborah H Schenk and Anne Alstott, Federal Income Taxation 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

employee. It becomes vital to ascertain when the hobby or recreational activities turns out to

be a business. Whether the profit making intention is present or not is not necessary to

preclude that there is a business activity. The court in “Thomas v FCT (1972) ATC 4094”

expressed that whether the commercial approach has been undertaken is greater than the

recreational activity5. In “FCT v JR Walker (1985)” small operations might be treated as

business if other sufficient characteristics are present.

Under “section 108-15 (1)” set of collectables are the one that is owned by the

taxpayer as the set and it is disposed ordinarily as the set6. As per “section 108-15 (2) of the

ITAA 1997” set of collectables are considered as the single collectable and each of the

disposal is treated as the part the collectables.

As per “section 110-25 of the ITAA 1997” the cost base of the property includes the

cost of ownership7. There is certain expenditure for which a taxpayer is not allowed to claim

deductions this includes the acquisition and costs of disposing the property. A taxpayer is not

allowed to claim deduction for the expenses that are occurred in acquiring or disposing the

rental property. However, these expenses would be treated as the part of the property cost

base for the purpose of CGT.

The court in “Adelaide Fruit and Produce Exchange Co Ltd v FCT (1932)” held

that rent refers to the price that is paid using another person’s property8. An individual

taxpayer must include the rental income in their assessable income rent since it constitutes an

5 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation

6 James, Simon, The Economics Of Taxation 2015

7 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

8 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

employee. It becomes vital to ascertain when the hobby or recreational activities turns out to

be a business. Whether the profit making intention is present or not is not necessary to

preclude that there is a business activity. The court in “Thomas v FCT (1972) ATC 4094”

expressed that whether the commercial approach has been undertaken is greater than the

recreational activity5. In “FCT v JR Walker (1985)” small operations might be treated as

business if other sufficient characteristics are present.

Under “section 108-15 (1)” set of collectables are the one that is owned by the

taxpayer as the set and it is disposed ordinarily as the set6. As per “section 108-15 (2) of the

ITAA 1997” set of collectables are considered as the single collectable and each of the

disposal is treated as the part the collectables.

As per “section 110-25 of the ITAA 1997” the cost base of the property includes the

cost of ownership7. There is certain expenditure for which a taxpayer is not allowed to claim

deductions this includes the acquisition and costs of disposing the property. A taxpayer is not

allowed to claim deduction for the expenses that are occurred in acquiring or disposing the

rental property. However, these expenses would be treated as the part of the property cost

base for the purpose of CGT.

The court in “Adelaide Fruit and Produce Exchange Co Ltd v FCT (1932)” held

that rent refers to the price that is paid using another person’s property8. An individual

taxpayer must include the rental income in their assessable income rent since it constitutes an

5 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation

6 James, Simon, The Economics Of Taxation 2015

7 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

8 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

5TAXATION LAW

ordinary income under “section 6-5 of the ITAA 1997”. However, “section 8-1” allows the

taxpayer to claim deductions for the rental expenses incurred when the property is let out for

rent.

A CGT event C1 happens under “section 104-20 (1) of the ITAA 1997” if the CGT

asset that is owned by the taxpayer is lost or destroyed. It is necessary to determine the time

of the event when the compensation is first received by the taxpayer9. A taxpayer either

makes capital gains or loss from the receipt of such compensation.

Applications:

Jill is full time employed in the top tier accounting firm and received a salary of

$100,000 with the bonus of $80,000. Citing “section 6, ITAA 1936” the salary would be

treated as income from the personal exertion. With reference to “Dean & Anor v FC of T

(1997) ATC 4762” the salary income would be treated as ordinary income with in the

ordinary concepts of “Section 6-5, ITAA 1997”.

Jill received the bonus of $30,000 for helping the new graduates at the accounting

firm. Citing the case of “Brent v FCT (1971) 125 CLR 418” the sum of $30,000 constitutes

the reward for the services and holds the sufficient nexus with the income producing

activities. Therefore, the sum of $30,000 will be treated as assessable income under “section

6-5 of the ITAA 1997”.

On numerous occasion the employer of Jill pays her the taxi expenses for returning

home. Under “section 15-2, ITAA 1997” the expenses paid by her employer will treated as

fringe benefit which is paid to her in relation to employment or the services rendered by an

individual.

9 Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013)

ordinary income under “section 6-5 of the ITAA 1997”. However, “section 8-1” allows the

taxpayer to claim deductions for the rental expenses incurred when the property is let out for

rent.

A CGT event C1 happens under “section 104-20 (1) of the ITAA 1997” if the CGT

asset that is owned by the taxpayer is lost or destroyed. It is necessary to determine the time

of the event when the compensation is first received by the taxpayer9. A taxpayer either

makes capital gains or loss from the receipt of such compensation.

Applications:

Jill is full time employed in the top tier accounting firm and received a salary of

$100,000 with the bonus of $80,000. Citing “section 6, ITAA 1936” the salary would be

treated as income from the personal exertion. With reference to “Dean & Anor v FC of T

(1997) ATC 4762” the salary income would be treated as ordinary income with in the

ordinary concepts of “Section 6-5, ITAA 1997”.

Jill received the bonus of $30,000 for helping the new graduates at the accounting

firm. Citing the case of “Brent v FCT (1971) 125 CLR 418” the sum of $30,000 constitutes

the reward for the services and holds the sufficient nexus with the income producing

activities. Therefore, the sum of $30,000 will be treated as assessable income under “section

6-5 of the ITAA 1997”.

On numerous occasion the employer of Jill pays her the taxi expenses for returning

home. Under “section 15-2, ITAA 1997” the expenses paid by her employer will treated as

fringe benefit which is paid to her in relation to employment or the services rendered by an

individual.

9 Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Jill reported the expense of $5,000 on the contemporary suits. The expenses incurred

by Jill was for the ordinary items of clothing. Citing “Mansfield v FC of T (1996) ATC

4001” the clothing items is not a compulsory clothing and hence not deductible under

“section 8-1, ITAA 1997”10.

Jill later reports receipt of $3000 for being the best accountant with coffee machine of

$2,000. Citing the event of “Kelly v FCT (1985) 85 ATC 4283” the cash award will be

treated as taxable income since it was relevant to her employment by the club and associated

to the employee’s skill.

Later Jill reports the travel expense of $6,000 for commuting from Corp Co Ltd

premises to her accounting firm. Citing the legislative response of “section 25-100 ITAA

1997” the expenses incurred by Jill was for traveling between two work places with none of

the places being her home. Referring the court decision in “FCT v Wiener (1978) ATC

4006” Jill will be allowed to claim deductions since it was incurred in generating the taxable

income.

Later events suggest that Jill is talented in sewing curtains and considers sewing

custom made sewing curtains for the purpose of selling them to customers. Jill began sewing

curtains and puts it in her glossy catalogue. She fulfilled 4 orders of curtains and received the

sum of $10,000. Referring to “Thomas v FCT (1972) ATC 4094” Jill undertook the

commercial approach which is more than the recreational activity11. Citing the event of “FCT

v JR Walker (1985)” the activities of Jill constitute small operations of business since it

holds sufficient characteristics of carrying of business.

10 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation

Law (CCH Australia, 2013)

11 Sadiq, Kerrie, Principles Of Taxation Law 2014

Jill reported the expense of $5,000 on the contemporary suits. The expenses incurred

by Jill was for the ordinary items of clothing. Citing “Mansfield v FC of T (1996) ATC

4001” the clothing items is not a compulsory clothing and hence not deductible under

“section 8-1, ITAA 1997”10.

Jill later reports receipt of $3000 for being the best accountant with coffee machine of

$2,000. Citing the event of “Kelly v FCT (1985) 85 ATC 4283” the cash award will be

treated as taxable income since it was relevant to her employment by the club and associated

to the employee’s skill.

Later Jill reports the travel expense of $6,000 for commuting from Corp Co Ltd

premises to her accounting firm. Citing the legislative response of “section 25-100 ITAA

1997” the expenses incurred by Jill was for traveling between two work places with none of

the places being her home. Referring the court decision in “FCT v Wiener (1978) ATC

4006” Jill will be allowed to claim deductions since it was incurred in generating the taxable

income.

Later events suggest that Jill is talented in sewing curtains and considers sewing

custom made sewing curtains for the purpose of selling them to customers. Jill began sewing

curtains and puts it in her glossy catalogue. She fulfilled 4 orders of curtains and received the

sum of $10,000. Referring to “Thomas v FCT (1972) ATC 4094” Jill undertook the

commercial approach which is more than the recreational activity11. Citing the event of “FCT

v JR Walker (1985)” the activities of Jill constitute small operations of business since it

holds sufficient characteristics of carrying of business.

10 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation

Law (CCH Australia, 2013)

11 Sadiq, Kerrie, Principles Of Taxation Law 2014

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Jill reported the sale of three set of rare books for $900. Referring to “section 108-15

(2) of the ITAA 1997” the three set of books is an item of collectables. The disposal of

collectables under “section 108-15 (2) of the ITAA 1997” will be considered for capital gains

purpose with any capital gains shall be included in the assessable income.

Jill incurred an expense on stamp duty and legal fees while acquiring the investment

property. With reference to the “section 110-25 of the ITAA 1997” the legal expenses and

stamp duty forms the cost base of property which is non-deductible12. The expenses would be

treated as the part of the property cost base for the purpose of CGT.

The rental income received by Jill be will included for assessment under “section 6-5,

ITAA 1997” as income under ordinary concepts. However, Jill will be allowed to claim

deduction under “section 8-1” for insurance premiums, council and water rates because it

was incurred in the derivation of assessable income.

The rental property of Jill was however destroyed by bushfire. She received a

compensation of $500,000. The receipt compensation results in CGT event C1 under

“section 104-20 (1) of the ITAA 1997” since the asset was destroyed. The compensation

received was less than the cost base of rental property and hence results in loss.

12 Woellner, R. H, Australian Taxation Law Select 2013 (CCH Australia, 2013)

Jill reported the sale of three set of rare books for $900. Referring to “section 108-15

(2) of the ITAA 1997” the three set of books is an item of collectables. The disposal of

collectables under “section 108-15 (2) of the ITAA 1997” will be considered for capital gains

purpose with any capital gains shall be included in the assessable income.

Jill incurred an expense on stamp duty and legal fees while acquiring the investment

property. With reference to the “section 110-25 of the ITAA 1997” the legal expenses and

stamp duty forms the cost base of property which is non-deductible12. The expenses would be

treated as the part of the property cost base for the purpose of CGT.

The rental income received by Jill be will included for assessment under “section 6-5,

ITAA 1997” as income under ordinary concepts. However, Jill will be allowed to claim

deduction under “section 8-1” for insurance premiums, council and water rates because it

was incurred in the derivation of assessable income.

The rental property of Jill was however destroyed by bushfire. She received a

compensation of $500,000. The receipt compensation results in CGT event C1 under

“section 104-20 (1) of the ITAA 1997” since the asset was destroyed. The compensation

received was less than the cost base of rental property and hence results in loss.

12 Woellner, R. H, Australian Taxation Law Select 2013 (CCH Australia, 2013)

8TAXATION LAW

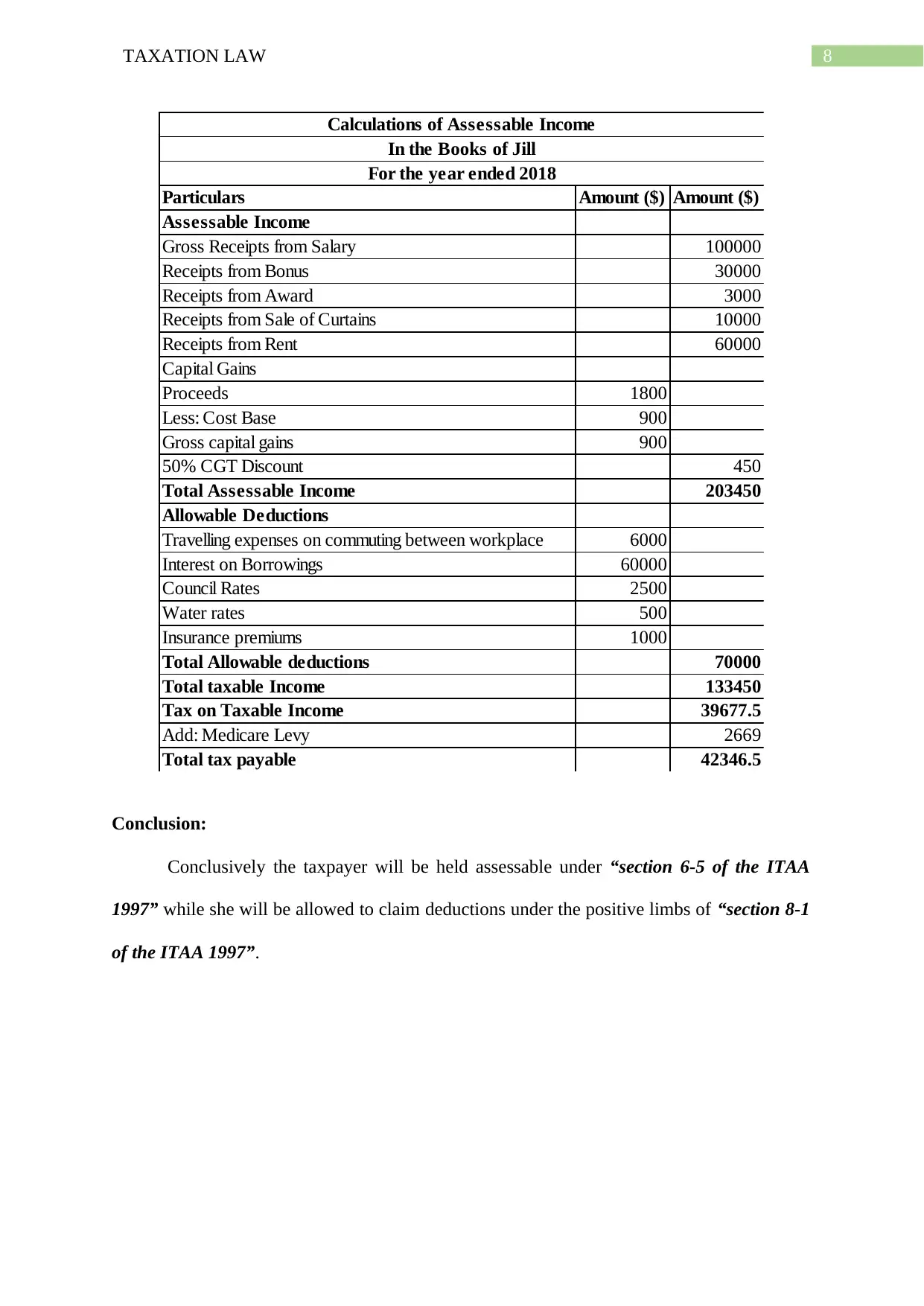

Particulars Amount ($) Amount ($)

Assessable Income

Gross Receipts from Salary 100000

Receipts from Bonus 30000

Receipts from Award 3000

Receipts from Sale of Curtains 10000

Receipts from Rent 60000

Capital Gains

Proceeds 1800

Less: Cost Base 900

Gross capital gains 900

50% CGT Discount 450

Total Assessable Income 203450

Allowable Deductions

Travelling expenses on commuting between workplace 6000

Interest on Borrowings 60000

Council Rates 2500

Water rates 500

Insurance premiums 1000

Total Allowable deductions 70000

Total taxable Income 133450

Tax on Taxable Income 39677.5

Add: Medicare Levy 2669

Total tax payable 42346.5

Calculations of Assessable Income

In the Books of Jill

For the year ended 2018

Conclusion:

Conclusively the taxpayer will be held assessable under “section 6-5 of the ITAA

1997” while she will be allowed to claim deductions under the positive limbs of “section 8-1

of the ITAA 1997”.

Particulars Amount ($) Amount ($)

Assessable Income

Gross Receipts from Salary 100000

Receipts from Bonus 30000

Receipts from Award 3000

Receipts from Sale of Curtains 10000

Receipts from Rent 60000

Capital Gains

Proceeds 1800

Less: Cost Base 900

Gross capital gains 900

50% CGT Discount 450

Total Assessable Income 203450

Allowable Deductions

Travelling expenses on commuting between workplace 6000

Interest on Borrowings 60000

Council Rates 2500

Water rates 500

Insurance premiums 1000

Total Allowable deductions 70000

Total taxable Income 133450

Tax on Taxable Income 39677.5

Add: Medicare Levy 2669

Total tax payable 42346.5

Calculations of Assessable Income

In the Books of Jill

For the year ended 2018

Conclusion:

Conclusively the taxpayer will be held assessable under “section 6-5 of the ITAA

1997” while she will be allowed to claim deductions under the positive limbs of “section 8-1

of the ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Barkoczy, Stephen, Foundations Of Taxation Law 2014

Brokelind, Cécile, Principles Of Law 2014.

Coleman, Cynthia and Kerrie Sadiq, Principles Of Taxation Law 2013

Graetz, Michael J, Deborah H Schenk and Anne Alstott, Federal Income Taxation 2015.

Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation

James, Simon, The Economics Of Taxation 2015

Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013)

Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013)

Sadiq, Kerrie, Principles Of Taxation Law 2014

Woellner, R. H, Australian Taxation Law Select 2013 (CCH Australia, 2013)

References:

Barkoczy, Stephen, Foundations Of Taxation Law 2014

Brokelind, Cécile, Principles Of Law 2014.

Coleman, Cynthia and Kerrie Sadiq, Principles Of Taxation Law 2013

Graetz, Michael J, Deborah H Schenk and Anne Alstott, Federal Income Taxation 2015.

Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation

James, Simon, The Economics Of Taxation 2015

Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013)

Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013)

Sadiq, Kerrie, Principles Of Taxation Law 2014

Woellner, R. H, Australian Taxation Law Select 2013 (CCH Australia, 2013)

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.