CLWM4100 Taxation Law Assessment: CGT Event Timing and Tax Advice

VerifiedAdded on 2022/08/21

|5

|429

|13

Case Study

AI Summary

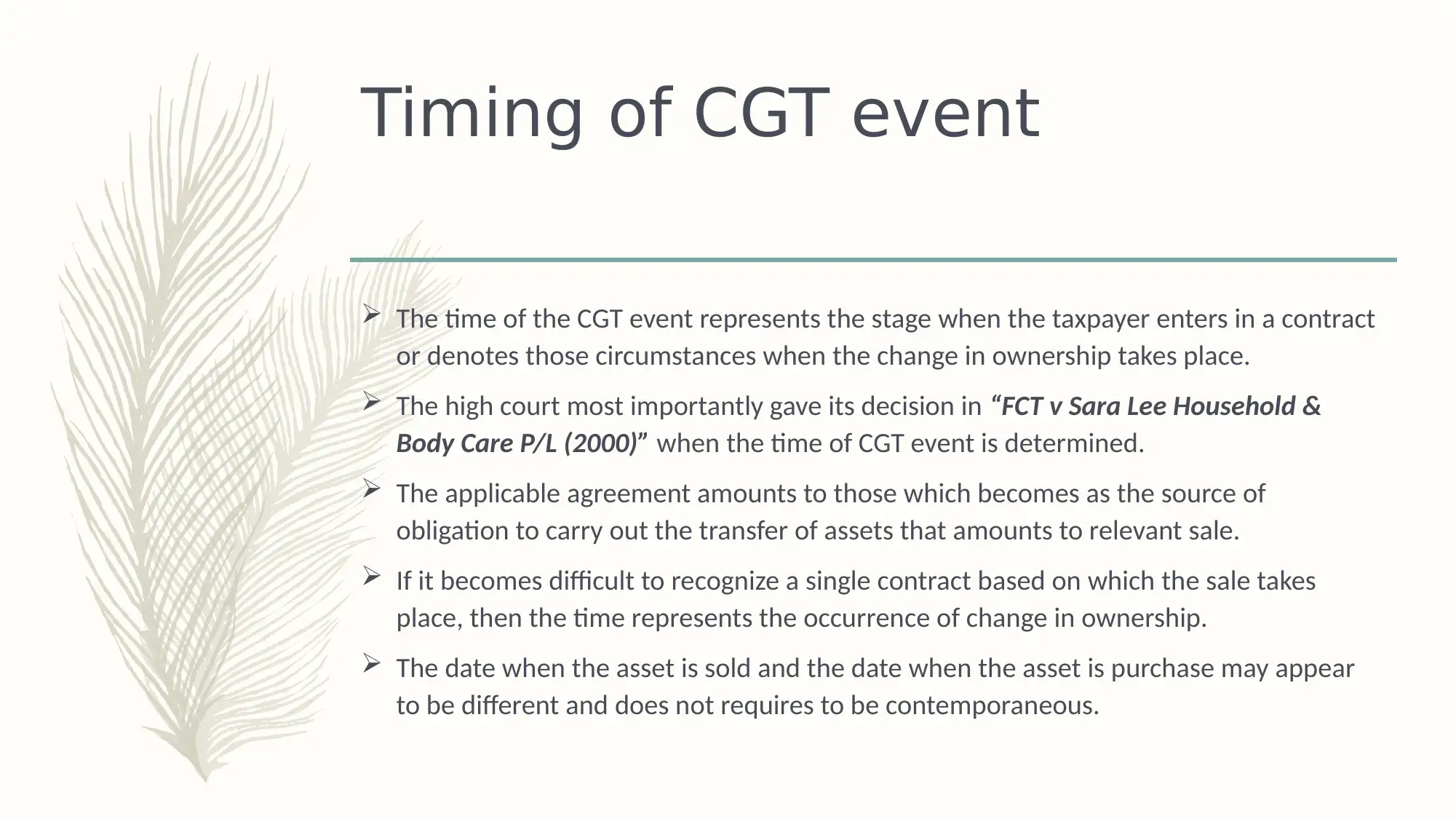

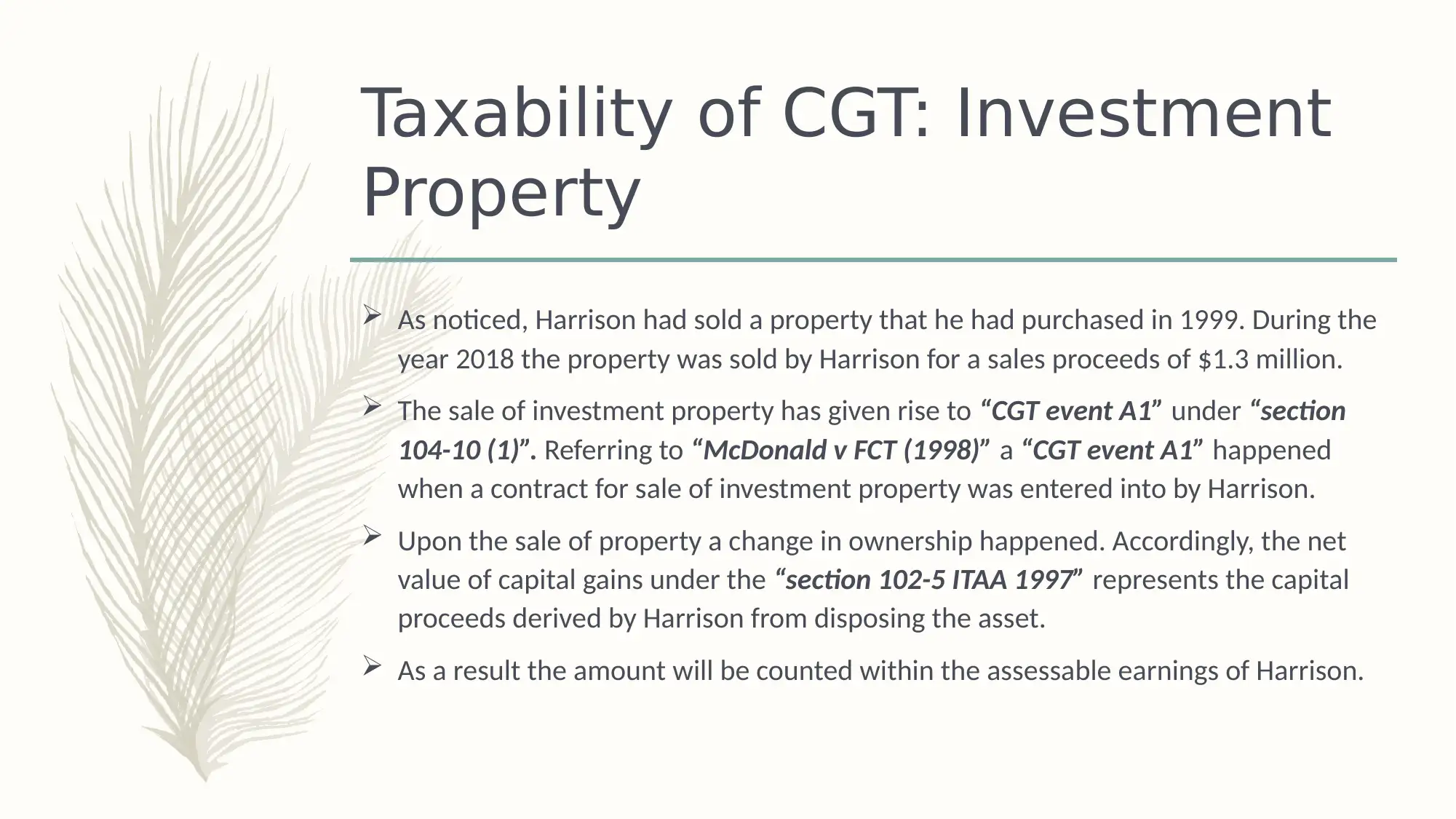

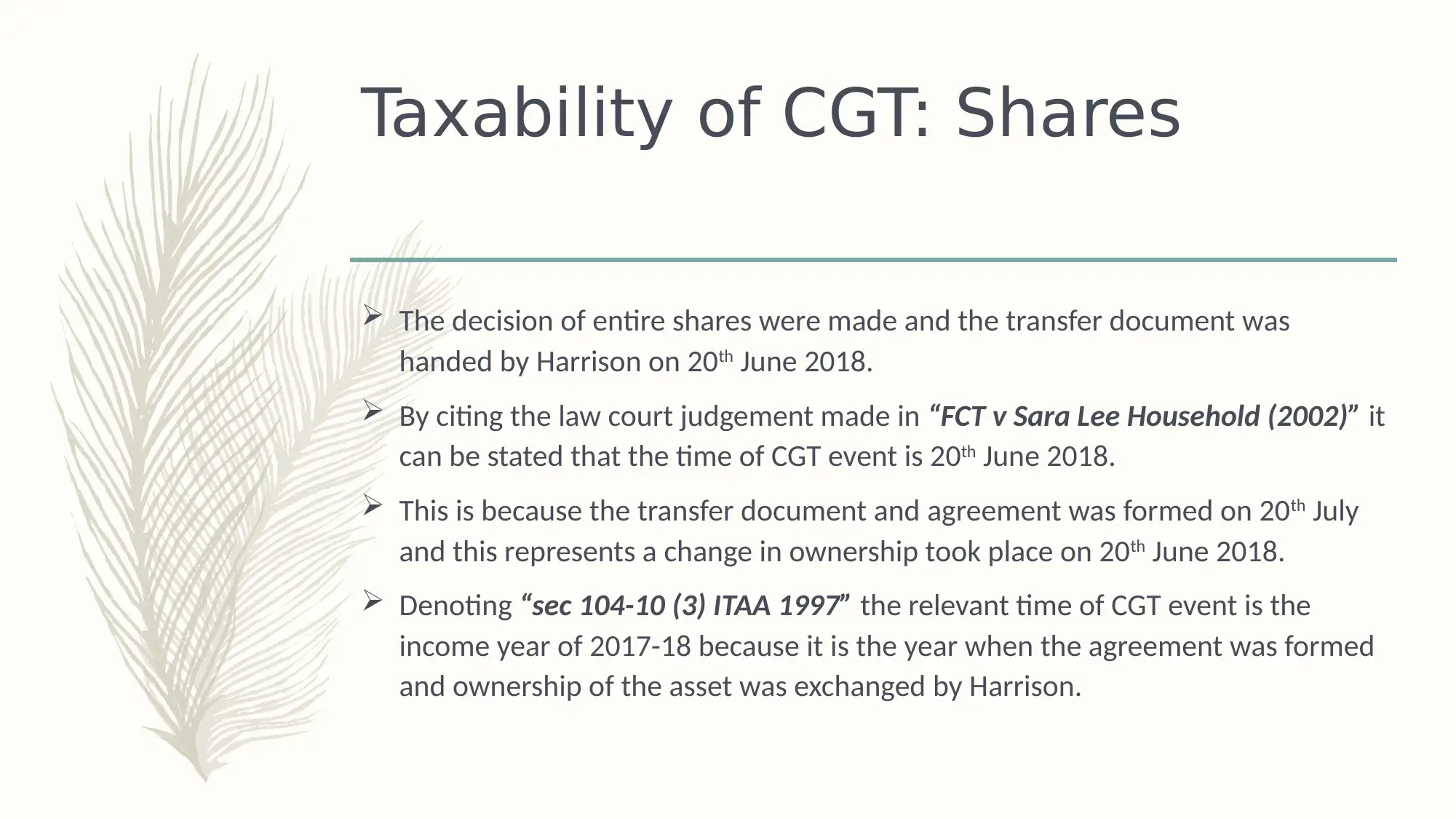

This case study analyzes the timing of Capital Gains Tax (CGT) events and the taxability of capital gains for Harrison Carter, an Australian resident. The analysis focuses on two key scenarios: the sale of an investment property and the sale of shares. The solution explains the determination of the CGT event timing, referencing relevant legal precedents like "FCT v Sara Lee Household & Body Care P/L (2000)" and "McDonald v FCT (1998)" and applicable sections of the ITAA 1997. The case study details how the sale of the investment property in 2018 triggered a CGT event A1, and the transfer of shares on June 20, 2018, also constituted a CGT event. It also provides an overview of how to calculate capital gains and losses to be included in Harrison Carter's tax return for the years ending 2018 and 2019, including all available methods for calculation. The document provides insights into how the timing of CGT events is determined and its implications on tax liability. The case study is designed to help students understand the practical application of CGT principles and the analysis of tax implications for various transactions.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.