Holmes Institute HA3042 Taxation Law Assignment: CGT and Deductions

VerifiedAdded on 2022/09/07

|12

|2579

|19

Homework Assignment

AI Summary

This assignment solution addresses key concepts in Australian Taxation Law, specifically focusing on Capital Gains Tax (CGT) and allowable deductions. The first part of the assignment analyzes a case involving the sale of various assets, including a block of land, shares, stamps, and a guitar, to determine the CGT implications for each. It meticulously examines the cost base of the land, the pre-CGT status of the shares, the treatment of collectables, and personal use assets. The second part delves into the deductibility of various expenses incurred by an individual, Ava, in relation to her employment as a hospital worker. It considers expenses such as travel costs, relocation costs, work-related clothing, childcare, phone calls, food, and fines, applying relevant legal principles and case law to determine which expenses qualify as allowable deductions. The analysis draws on specific sections of the Income Tax Assessment Act 1997 (ITAA 1997) and relevant case law to support the conclusions. The assignment provides a detailed understanding of tax law principles and their practical application in different scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Law:........................................................................................................................................7

Application:............................................................................................................................8

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Law:........................................................................................................................................7

Application:............................................................................................................................8

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Sale of block of land:

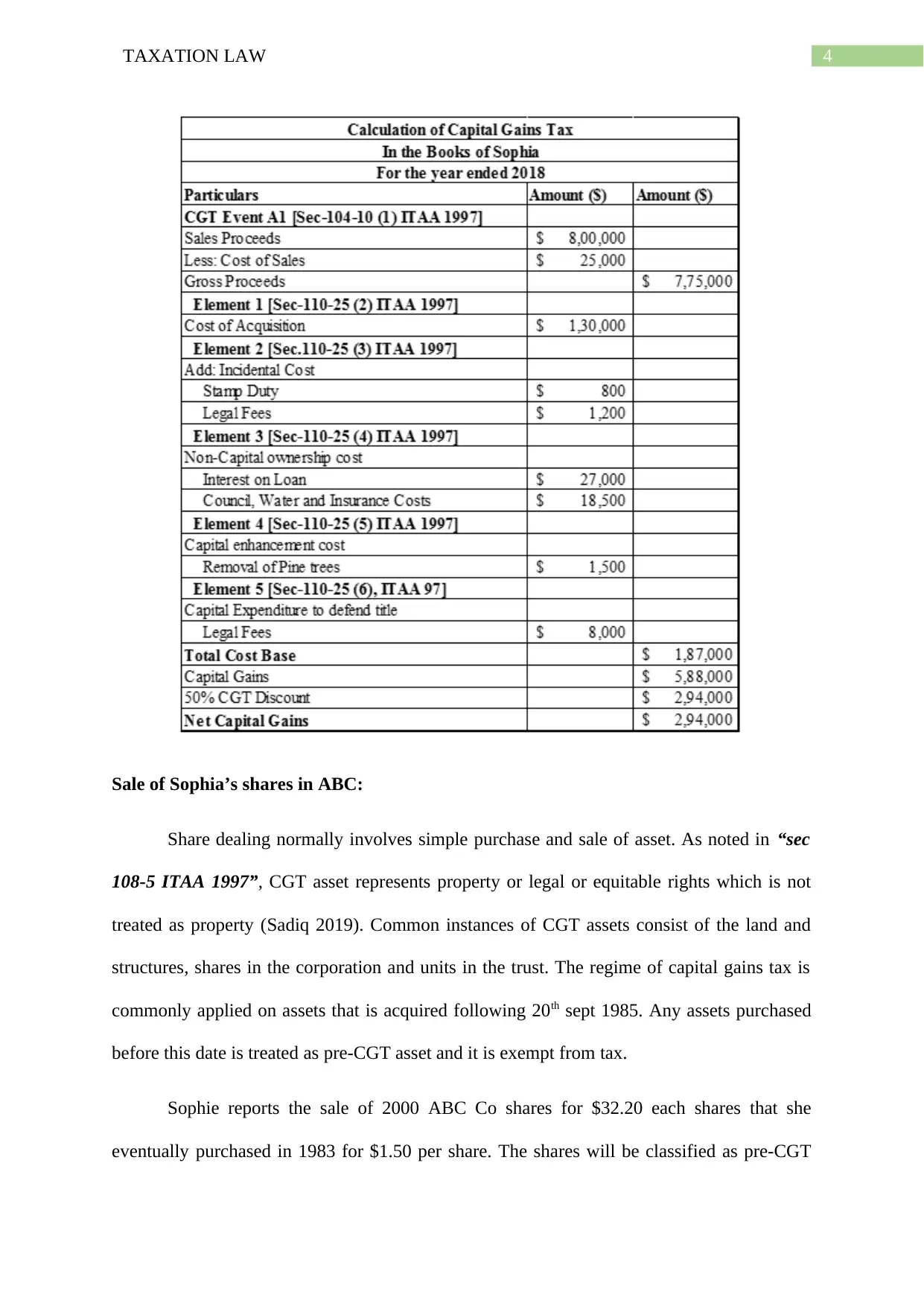

As noticed in “sec 110-25, ITAA 1997” there are commonly five elements of cost

base for CGT purpose of an asset. Under element one of “sec 110-25 (2), ITAA 1997” the

amount paid to get the asset is included. The second element involves the incidental cost

relating to purchase and sale of CGT asset under “sec 110-25, ITAA 1997” such as stamp

duty, fees of lawyer, commission etc. The third element includes the non-capital ownership

cost of asset such as the interest, repairs, land tax, interest (Woellner et al. 2016). This

element is commonly considered relevant when the taxpayer uses the asset for generating the

assessable earnings to deduct the non-capital ownership cost against it. The fourth element

under “sec 110-25 (5), ITAA 1997” involves the capital expenses which is occurred for

improving the asset which is reflected at the time of selling the asset. The final or fifth

element involves capital expenses that is occurred in establishing, defending the title or rights

associated to asset under “sec 110-25 (6) ITAA 1997”.

The current state of Sophia explains that she purchased a block of land that was

located in Ninety Mile Beach for $130,000 in 1991 for investment purpose. The land was

eventually sold by Sophia in 2018 for $800,000. The sale of land by Sophia has results in

“CGT event A1” within “section 104-10 ITAA 1997”. However to ascertain the CGT it is

vital to understand the cost base of the property (Barkoczy 2016). As per first element of cost

base under “sec 110-25 (2), ITAA 1997” comprises of the purchase price of $130,000 that

was paid by Sophia to acquire the land.

Sophia also reports incidental cost such as stamp duty and legal fees of $800 and

$1,200 individually. These cost forms the second element of cost base under “sec 110-25

(3)”. Sophia also reports an interest on loan that amounted to $27,000. She further reports

Answer to question 1:

Sale of block of land:

As noticed in “sec 110-25, ITAA 1997” there are commonly five elements of cost

base for CGT purpose of an asset. Under element one of “sec 110-25 (2), ITAA 1997” the

amount paid to get the asset is included. The second element involves the incidental cost

relating to purchase and sale of CGT asset under “sec 110-25, ITAA 1997” such as stamp

duty, fees of lawyer, commission etc. The third element includes the non-capital ownership

cost of asset such as the interest, repairs, land tax, interest (Woellner et al. 2016). This

element is commonly considered relevant when the taxpayer uses the asset for generating the

assessable earnings to deduct the non-capital ownership cost against it. The fourth element

under “sec 110-25 (5), ITAA 1997” involves the capital expenses which is occurred for

improving the asset which is reflected at the time of selling the asset. The final or fifth

element involves capital expenses that is occurred in establishing, defending the title or rights

associated to asset under “sec 110-25 (6) ITAA 1997”.

The current state of Sophia explains that she purchased a block of land that was

located in Ninety Mile Beach for $130,000 in 1991 for investment purpose. The land was

eventually sold by Sophia in 2018 for $800,000. The sale of land by Sophia has results in

“CGT event A1” within “section 104-10 ITAA 1997”. However to ascertain the CGT it is

vital to understand the cost base of the property (Barkoczy 2016). As per first element of cost

base under “sec 110-25 (2), ITAA 1997” comprises of the purchase price of $130,000 that

was paid by Sophia to acquire the land.

Sophia also reports incidental cost such as stamp duty and legal fees of $800 and

$1,200 individually. These cost forms the second element of cost base under “sec 110-25

(3)”. Sophia also reports an interest on loan that amounted to $27,000. She further reports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

council rates, water rates and insurance costs of $18,500 during her ownership period. The

interest on loan, council rates, water rates and insurance costs is a non-capital ownership cost

of land and will be contained inside the third element of cost base under “sec 110-25 (4),

ITAA 1997” for CGT purpose.

Sophia also reports occurrence of legal fees amounting to $8,000 for settling the

dispute with neighbour regarding the use of land. Under “sec 110-25 (6) ITAA 1997”, the

legal fees is a capital expenditures incurred by Sophia to defend her title on the investment

property. Hence, it must be counted under fifth element of cost base for CGT purpose

(Freudenberg et al. 2017). Sophia before selling the land spent $1,500 for removing the

hazardous pine trees on land. These expenses are capital expenses occurred to improve the

asset and it will be included under fourth element cost base of CGT asset under “sec 110-25

(5) ITAA 1997”.

council rates, water rates and insurance costs of $18,500 during her ownership period. The

interest on loan, council rates, water rates and insurance costs is a non-capital ownership cost

of land and will be contained inside the third element of cost base under “sec 110-25 (4),

ITAA 1997” for CGT purpose.

Sophia also reports occurrence of legal fees amounting to $8,000 for settling the

dispute with neighbour regarding the use of land. Under “sec 110-25 (6) ITAA 1997”, the

legal fees is a capital expenditures incurred by Sophia to defend her title on the investment

property. Hence, it must be counted under fifth element of cost base for CGT purpose

(Freudenberg et al. 2017). Sophia before selling the land spent $1,500 for removing the

hazardous pine trees on land. These expenses are capital expenses occurred to improve the

asset and it will be included under fourth element cost base of CGT asset under “sec 110-25

(5) ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Sale of Sophia’s shares in ABC:

Share dealing normally involves simple purchase and sale of asset. As noted in “sec

108-5 ITAA 1997”, CGT asset represents property or legal or equitable rights which is not

treated as property (Sadiq 2019). Common instances of CGT assets consist of the land and

structures, shares in the corporation and units in the trust. The regime of capital gains tax is

commonly applied on assets that is acquired following 20th sept 1985. Any assets purchased

before this date is treated as pre-CGT asset and it is exempt from tax.

Sophie reports the sale of 2000 ABC Co shares for $32.20 each shares that she

eventually purchased in 1983 for $1.50 per share. The shares will be classified as pre-CGT

Sale of Sophia’s shares in ABC:

Share dealing normally involves simple purchase and sale of asset. As noted in “sec

108-5 ITAA 1997”, CGT asset represents property or legal or equitable rights which is not

treated as property (Sadiq 2019). Common instances of CGT assets consist of the land and

structures, shares in the corporation and units in the trust. The regime of capital gains tax is

commonly applied on assets that is acquired following 20th sept 1985. Any assets purchased

before this date is treated as pre-CGT asset and it is exempt from tax.

Sophie reports the sale of 2000 ABC Co shares for $32.20 each shares that she

eventually purchased in 1983 for $1.50 per share. The shares will be classified as pre-CGT

5TAXATION LAW

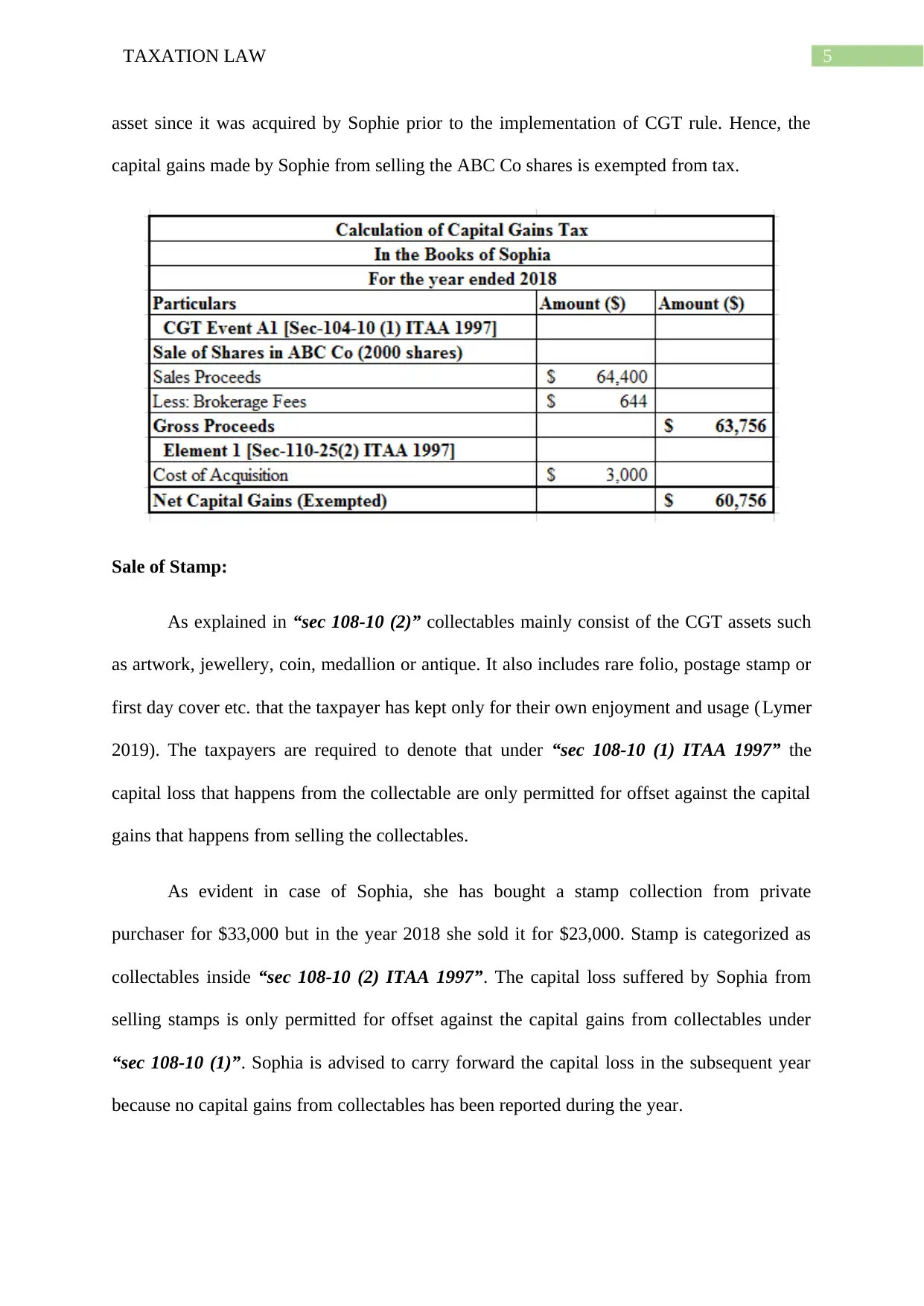

asset since it was acquired by Sophie prior to the implementation of CGT rule. Hence, the

capital gains made by Sophie from selling the ABC Co shares is exempted from tax.

Sale of Stamp:

As explained in “sec 108-10 (2)” collectables mainly consist of the CGT assets such

as artwork, jewellery, coin, medallion or antique. It also includes rare folio, postage stamp or

first day cover etc. that the taxpayer has kept only for their own enjoyment and usage (Lymer

2019). The taxpayers are required to denote that under “sec 108-10 (1) ITAA 1997” the

capital loss that happens from the collectable are only permitted for offset against the capital

gains that happens from selling the collectables.

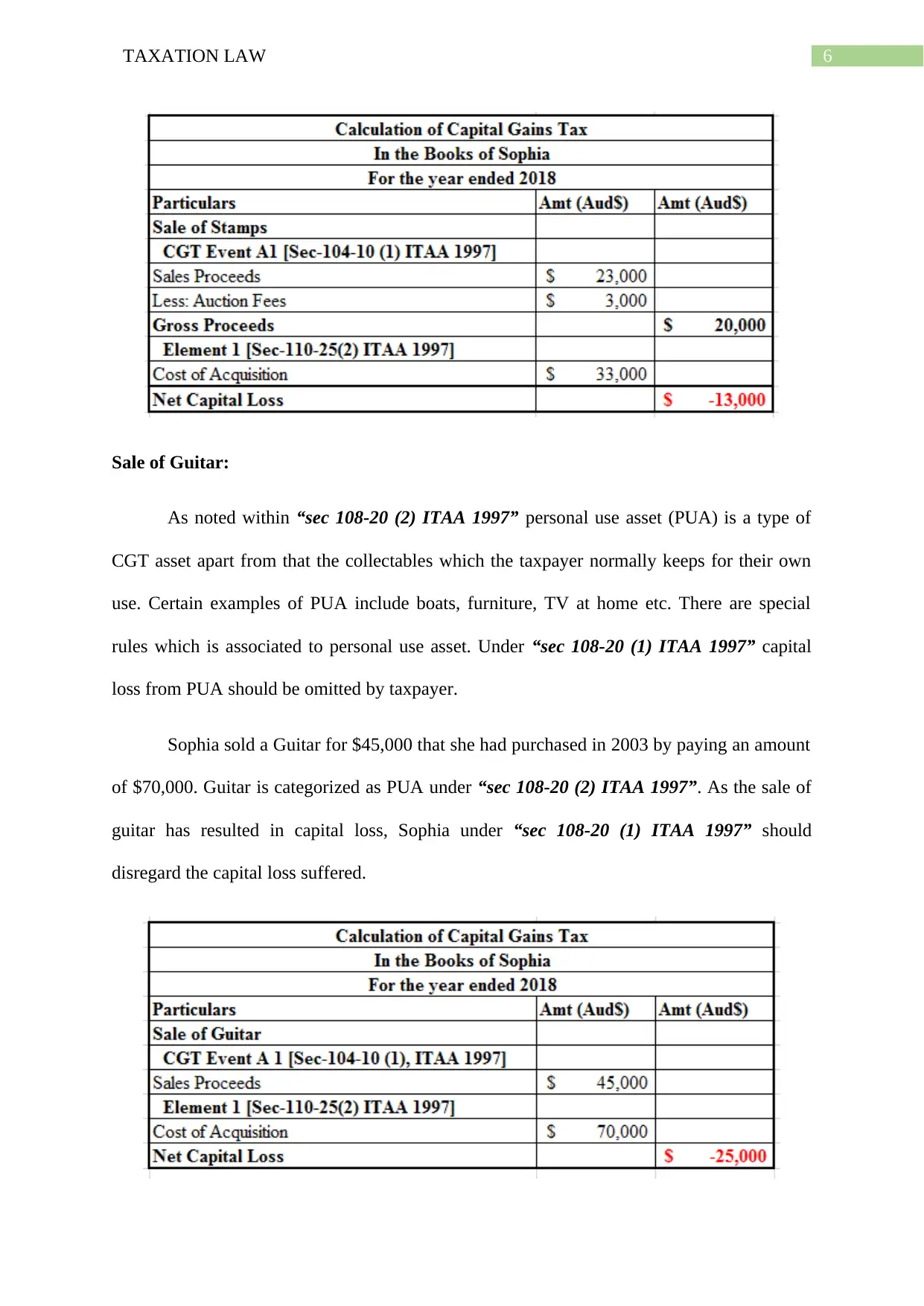

As evident in case of Sophia, she has bought a stamp collection from private

purchaser for $33,000 but in the year 2018 she sold it for $23,000. Stamp is categorized as

collectables inside “sec 108-10 (2) ITAA 1997”. The capital loss suffered by Sophia from

selling stamps is only permitted for offset against the capital gains from collectables under

“sec 108-10 (1)”. Sophia is advised to carry forward the capital loss in the subsequent year

because no capital gains from collectables has been reported during the year.

asset since it was acquired by Sophie prior to the implementation of CGT rule. Hence, the

capital gains made by Sophie from selling the ABC Co shares is exempted from tax.

Sale of Stamp:

As explained in “sec 108-10 (2)” collectables mainly consist of the CGT assets such

as artwork, jewellery, coin, medallion or antique. It also includes rare folio, postage stamp or

first day cover etc. that the taxpayer has kept only for their own enjoyment and usage (Lymer

2019). The taxpayers are required to denote that under “sec 108-10 (1) ITAA 1997” the

capital loss that happens from the collectable are only permitted for offset against the capital

gains that happens from selling the collectables.

As evident in case of Sophia, she has bought a stamp collection from private

purchaser for $33,000 but in the year 2018 she sold it for $23,000. Stamp is categorized as

collectables inside “sec 108-10 (2) ITAA 1997”. The capital loss suffered by Sophia from

selling stamps is only permitted for offset against the capital gains from collectables under

“sec 108-10 (1)”. Sophia is advised to carry forward the capital loss in the subsequent year

because no capital gains from collectables has been reported during the year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

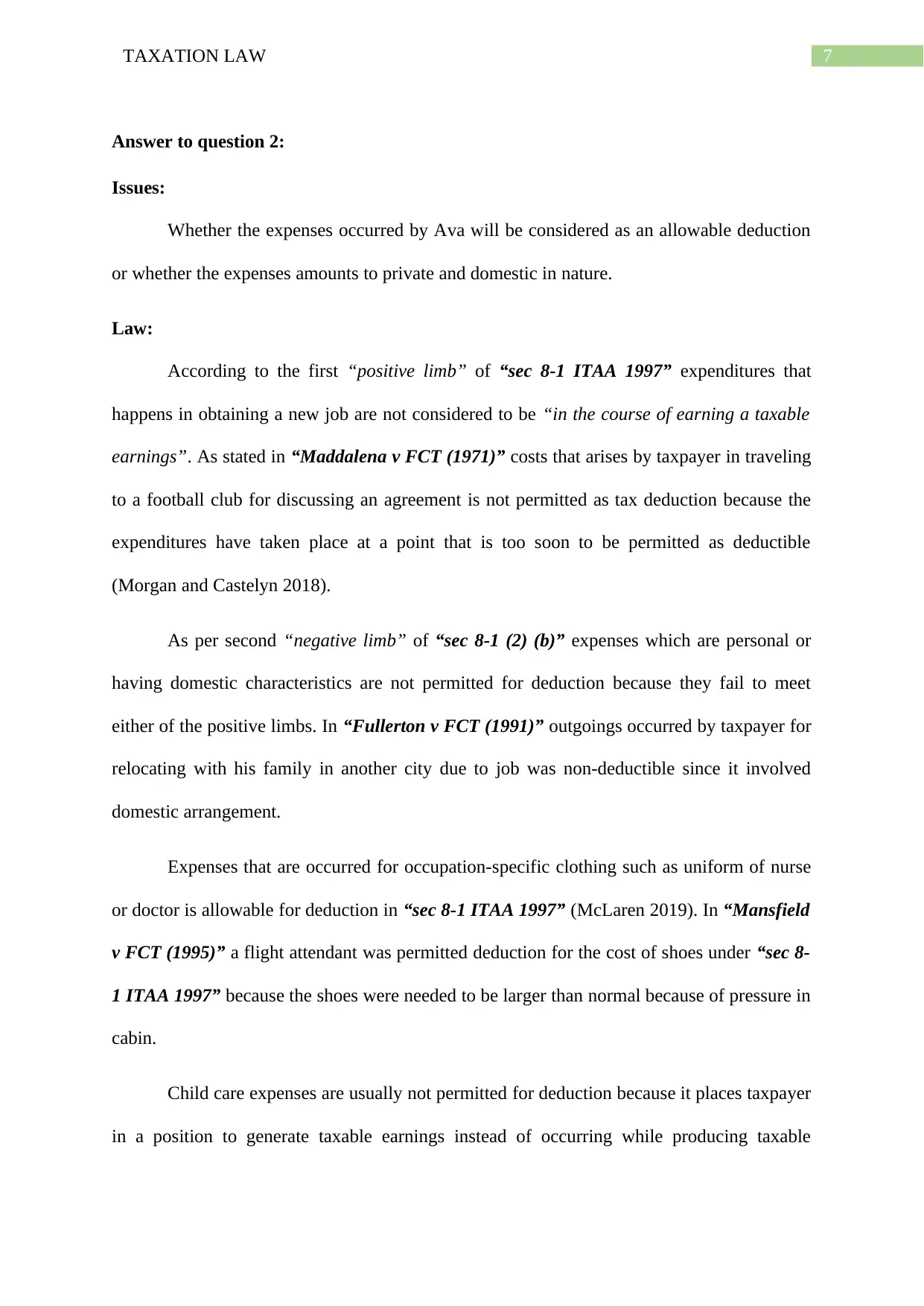

Sale of Guitar:

As noted within “sec 108-20 (2) ITAA 1997” personal use asset (PUA) is a type of

CGT asset apart from that the collectables which the taxpayer normally keeps for their own

use. Certain examples of PUA include boats, furniture, TV at home etc. There are special

rules which is associated to personal use asset. Under “sec 108-20 (1) ITAA 1997” capital

loss from PUA should be omitted by taxpayer.

Sophia sold a Guitar for $45,000 that she had purchased in 2003 by paying an amount

of $70,000. Guitar is categorized as PUA under “sec 108-20 (2) ITAA 1997”. As the sale of

guitar has resulted in capital loss, Sophia under “sec 108-20 (1) ITAA 1997” should

disregard the capital loss suffered.

Sale of Guitar:

As noted within “sec 108-20 (2) ITAA 1997” personal use asset (PUA) is a type of

CGT asset apart from that the collectables which the taxpayer normally keeps for their own

use. Certain examples of PUA include boats, furniture, TV at home etc. There are special

rules which is associated to personal use asset. Under “sec 108-20 (1) ITAA 1997” capital

loss from PUA should be omitted by taxpayer.

Sophia sold a Guitar for $45,000 that she had purchased in 2003 by paying an amount

of $70,000. Guitar is categorized as PUA under “sec 108-20 (2) ITAA 1997”. As the sale of

guitar has resulted in capital loss, Sophia under “sec 108-20 (1) ITAA 1997” should

disregard the capital loss suffered.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

Whether the expenses occurred by Ava will be considered as an allowable deduction

or whether the expenses amounts to private and domestic in nature.

Law:

According to the first “positive limb” of “sec 8-1 ITAA 1997” expenditures that

happens in obtaining a new job are not considered to be “in the course of earning a taxable

earnings”. As stated in “Maddalena v FCT (1971)” costs that arises by taxpayer in traveling

to a football club for discussing an agreement is not permitted as tax deduction because the

expenditures have taken place at a point that is too soon to be permitted as deductible

(Morgan and Castelyn 2018).

As per second “negative limb” of “sec 8-1 (2) (b)” expenses which are personal or

having domestic characteristics are not permitted for deduction because they fail to meet

either of the positive limbs. In “Fullerton v FCT (1991)” outgoings occurred by taxpayer for

relocating with his family in another city due to job was non-deductible since it involved

domestic arrangement.

Expenses that are occurred for occupation-specific clothing such as uniform of nurse

or doctor is allowable for deduction in “sec 8-1 ITAA 1997” (McLaren 2019). In “Mansfield

v FCT (1995)” a flight attendant was permitted deduction for the cost of shoes under “sec 8-

1 ITAA 1997” because the shoes were needed to be larger than normal because of pressure in

cabin.

Child care expenses are usually not permitted for deduction because it places taxpayer

in a position to generate taxable earnings instead of occurring while producing taxable

Answer to question 2:

Issues:

Whether the expenses occurred by Ava will be considered as an allowable deduction

or whether the expenses amounts to private and domestic in nature.

Law:

According to the first “positive limb” of “sec 8-1 ITAA 1997” expenditures that

happens in obtaining a new job are not considered to be “in the course of earning a taxable

earnings”. As stated in “Maddalena v FCT (1971)” costs that arises by taxpayer in traveling

to a football club for discussing an agreement is not permitted as tax deduction because the

expenditures have taken place at a point that is too soon to be permitted as deductible

(Morgan and Castelyn 2018).

As per second “negative limb” of “sec 8-1 (2) (b)” expenses which are personal or

having domestic characteristics are not permitted for deduction because they fail to meet

either of the positive limbs. In “Fullerton v FCT (1991)” outgoings occurred by taxpayer for

relocating with his family in another city due to job was non-deductible since it involved

domestic arrangement.

Expenses that are occurred for occupation-specific clothing such as uniform of nurse

or doctor is allowable for deduction in “sec 8-1 ITAA 1997” (McLaren 2019). In “Mansfield

v FCT (1995)” a flight attendant was permitted deduction for the cost of shoes under “sec 8-

1 ITAA 1997” because the shoes were needed to be larger than normal because of pressure in

cabin.

Child care expenses are usually not permitted for deduction because it places taxpayer

in a position to generate taxable earnings instead of occurring while producing taxable

8TAXATION LAW

earnings. In “Lodge v FCT (1972)” deductions were denied to law clerk for occurring

childcare expenses because it was not relevant to income making activities of taxpayer.

Phone calls related to work are permitted for deduction if a taxpayer has the

documented evidence of being on call with clients or employer while they are away from

their workplace (Payne 2018). As held in “Ronpibon Tin No Liability v FCT (1949)”

expenses that are occurred for work-related phone calls are permitted for deduction if it

satisfies either of “positive limbs” under “section 8-1 ITAA 1997”.

Normally there are disbursement which is related to being human and being the part

of social society. Hence, expenditures such as food, housing, clothing of common type are

not permitted for deduction. In “FCT v Cooper (1991)” expenses incurred by professional

rugby player on consuming additional food was not allowable for income tax deduction in

“positive limbs” of “sec 8-1 ITAA 1997” because it was not falling inside the first limb.

As per “section 26-5 ITAA 1997” certain types of fines that are imposed by

Australian laws such as speeding fines, parking fines etc. are not permissible for deduction

(Morgan, Mortimer and Pinto 2018). Travel costs occurred by taxpayer between home and

place of work is not acceptable for deduction under “sec 8-1 ITAA 1997”. In “Lunney v

FCT (1958)” travel amid the taxpayer’s home and work is non-deductible.

Application:

Ava in the current situation is working in Sunshine Hospital. With respect to the

applicability of the above laws the tax treatment of each expenses are given below

(A): The travel costs incurred to Sunshine Hospital for job interview is a private outgoings.

Referring to “Maddalena v FCT (1971)” outlays occurred in traveling to job interview is not

permitted for deduction since the expenditures have taken place at a stage that is too soon to

be permitted as deductible.

earnings. In “Lodge v FCT (1972)” deductions were denied to law clerk for occurring

childcare expenses because it was not relevant to income making activities of taxpayer.

Phone calls related to work are permitted for deduction if a taxpayer has the

documented evidence of being on call with clients or employer while they are away from

their workplace (Payne 2018). As held in “Ronpibon Tin No Liability v FCT (1949)”

expenses that are occurred for work-related phone calls are permitted for deduction if it

satisfies either of “positive limbs” under “section 8-1 ITAA 1997”.

Normally there are disbursement which is related to being human and being the part

of social society. Hence, expenditures such as food, housing, clothing of common type are

not permitted for deduction. In “FCT v Cooper (1991)” expenses incurred by professional

rugby player on consuming additional food was not allowable for income tax deduction in

“positive limbs” of “sec 8-1 ITAA 1997” because it was not falling inside the first limb.

As per “section 26-5 ITAA 1997” certain types of fines that are imposed by

Australian laws such as speeding fines, parking fines etc. are not permissible for deduction

(Morgan, Mortimer and Pinto 2018). Travel costs occurred by taxpayer between home and

place of work is not acceptable for deduction under “sec 8-1 ITAA 1997”. In “Lunney v

FCT (1958)” travel amid the taxpayer’s home and work is non-deductible.

Application:

Ava in the current situation is working in Sunshine Hospital. With respect to the

applicability of the above laws the tax treatment of each expenses are given below

(A): The travel costs incurred to Sunshine Hospital for job interview is a private outgoings.

Referring to “Maddalena v FCT (1971)” outlays occurred in traveling to job interview is not

permitted for deduction since the expenditures have taken place at a stage that is too soon to

be permitted as deductible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

(B): Ava later relocated to Victoria and incurred relocation cost of $1,800. Citing “Fullerton

v FCT (1991)” outgoings occurred by Ava for relocating to Victoria due to job was not

permitted for deduction under “second negative limb” of “sec 8-1 (2) (b)” since it involved

domestic arrangement.

(C): Ava occurred work related clothing outlays of $200. Mentioning to the verdict given in

“Mansfield v FCT (1995)” Ava will be permitted tax deduction under “sec 8-1 ITAA 1997”

since it is an occupation-specific clothing and related to his income producing activity.

(D): Ava reported child care outlays of $18,200 for her daughter. Noting the elucidation

made in “Lodge v FCT (1972)” child care costs are not allowable for tax deduction to Ava

for the reason that it was not related to making income.

(E): Ava further reports outlays on making phone calls to Sunshine Hospital to check on

patients after her working hours. Referring to “Ronpibon Tin No Liability v FCT (1949)” the

phone call cost paid by Ava is linked to work and deduction will be permitted since it fulfils

the “positive limbs” of “section 8-1 ITAA 1997” (Trad and Freudenberg 2018).

(F): Ava also incurs expenditures on food while working in evening shift. Citing “FCT v

Cooper (1991)” payments made by Ava on food is not allowed for deduction under “sec 8-1

ITAA 1997” for the reason that it was not falling inside the first limb. The outlays relates to

being the part of human society.

(G): Ava incurs speeding fine of $207 while running late for her hospital. Referring to

“section 26-5 ITAA 1997” speeding fines imposed by Australian laws is not allowed for

deduction to Ava.

(F): Ava reports travel cost of $330 from her home and work. Referring to “Lunney v FCT

(1958)” travel outlays incurred by Ava from home and work is not permitted for deduction

(B): Ava later relocated to Victoria and incurred relocation cost of $1,800. Citing “Fullerton

v FCT (1991)” outgoings occurred by Ava for relocating to Victoria due to job was not

permitted for deduction under “second negative limb” of “sec 8-1 (2) (b)” since it involved

domestic arrangement.

(C): Ava occurred work related clothing outlays of $200. Mentioning to the verdict given in

“Mansfield v FCT (1995)” Ava will be permitted tax deduction under “sec 8-1 ITAA 1997”

since it is an occupation-specific clothing and related to his income producing activity.

(D): Ava reported child care outlays of $18,200 for her daughter. Noting the elucidation

made in “Lodge v FCT (1972)” child care costs are not allowable for tax deduction to Ava

for the reason that it was not related to making income.

(E): Ava further reports outlays on making phone calls to Sunshine Hospital to check on

patients after her working hours. Referring to “Ronpibon Tin No Liability v FCT (1949)” the

phone call cost paid by Ava is linked to work and deduction will be permitted since it fulfils

the “positive limbs” of “section 8-1 ITAA 1997” (Trad and Freudenberg 2018).

(F): Ava also incurs expenditures on food while working in evening shift. Citing “FCT v

Cooper (1991)” payments made by Ava on food is not allowed for deduction under “sec 8-1

ITAA 1997” for the reason that it was not falling inside the first limb. The outlays relates to

being the part of human society.

(G): Ava incurs speeding fine of $207 while running late for her hospital. Referring to

“section 26-5 ITAA 1997” speeding fines imposed by Australian laws is not allowed for

deduction to Ava.

(F): Ava reports travel cost of $330 from her home and work. Referring to “Lunney v FCT

(1958)” travel outlays incurred by Ava from home and work is not permitted for deduction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

under “sec 8-1 ITAA 1997” since it is private outgoings and not experienced in creating

chargeable returns.

Conclusion:

Ava is only entitled to deduction for her compulsory uniform, work related phone

calls under “section 8-1 ITAA 1997”. While the remaining expenditures are personal in type

and not permitted for deduction under “negative limbs” of “sec 8-1 (2) ITAA 1997”.

under “sec 8-1 ITAA 1997” since it is private outgoings and not experienced in creating

chargeable returns.

Conclusion:

Ava is only entitled to deduction for her compulsory uniform, work related phone

calls under “section 8-1 ITAA 1997”. While the remaining expenditures are personal in type

and not permitted for deduction under “negative limbs” of “sec 8-1 (2) ITAA 1997”.

11TAXATION LAW

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Lymer, A., 2019. Contemporary issues in taxation research. Routledge.

McLaren, J., 2019. Laws to protect tax whistleblowing in Australia: what does this mean for

taxpayers and the taxation profession. Australian Tax Review, 48, pp.24-41.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Payne, K., 2018. Taxation: Fix it up or trade up?. Company Director, 34(6), p.52.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Trad, B. and Freudenberg, B., 2018. A Dual Income Tax System for Australian Small

Business: Achieving Greater Tax Neutrality. J. Austl. Tax'n, 20, p.93.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Lymer, A., 2019. Contemporary issues in taxation research. Routledge.

McLaren, J., 2019. Laws to protect tax whistleblowing in Australia: what does this mean for

taxpayers and the taxation profession. Australian Tax Review, 48, pp.24-41.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Payne, K., 2018. Taxation: Fix it up or trade up?. Company Director, 34(6), p.52.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Trad, B. and Freudenberg, B., 2018. A Dual Income Tax System for Australian Small

Business: Achieving Greater Tax Neutrality. J. Austl. Tax'n, 20, p.93.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.