Taxation Theory, Practice & Law: Capital Gains and Fringe Benefits Tax

VerifiedAdded on 2023/06/06

|12

|3144

|495

Homework Assignment

AI Summary

This assignment solution provides a detailed analysis of capital gains tax (CGT) and fringe benefits tax (FBT) implications based on a series of transactions and scenarios. It begins by defining key terms such as pre-CGT assets, CGT events, and cost base, outlining how capital gains and losses are computed and treated under Australian taxation law. The solution then examines five specific transactions involving the disposal of assets like land, antiques, paintings, shares, and a violin, determining the CGT implications for each. Furthermore, the assignment addresses fringe benefits provided to an employee, Jasmine, including a car and a concessional loan, calculating the FBT liability for the employer, Rapid Heat, in accordance with the Fringe Benefit Tax Assessment Act 1986. The analysis incorporates relevant tax rulings, legislation, and benchmark interest rates to provide a comprehensive assessment of the tax consequences.

Taxation Theory, Practice & Law

STUDENT ID

[Pick the date]

STUDENT ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The client given has conducted a host of transactions which involve asset disposal of different

types. Also, vital information has been presented based on which it is apparent that the disposal

of these assets is not as part of business activity by client. This implies that these transactions

would lead to generation of capital proceeds and not revenue proceeds. This has high relevance

with regards to taxation as capital proceeds do not attract any taxation unlike revenue proceeds.

However, a key aspect in relation to capital receipts is that Capital Gains Tax (CGT) may be

applicable on any capital gains tax that the taxpayer would have realised. Hence, the key focus of

the discussion with regards to the transactions would be on highlighting the capital gains

implications.

To assist in this regards, it is vital to introduce some of the key terms which would be relevant to

the discussion of the tax implications of the given transactions (Barkoczy, 2017).

Pre- CGT Asset

This concept has been introduced in s. 149(10) ITAA 1997 as per which all assets which the

taxpayer acquires on or before September 19, 1985 would be categorised as pre-CGT assets. The

reason for defining these assets can be linked to the fact that unlike the post CGT assets, these

assets do not attract CGT liability (Krever, 2017). The non-application of CGT on the capital

gains does not get influenced by the holding period and exact capital gains or losses generated on

sale.

CGT Event

The term CGT event has special relevance in the capital gains computation as the necessity to

determine the underlying capital gains/losses arise only when such an event takes place. The list

of all the CGT events has been presented as per s.104-5, ITAA 1997 (Gilders, et. al., 2015). A

particular event which is highly relevant to the given client is A1 event which transpires once

there has been disposal of the asset. Accordingly, the definition of capital gains computation

methodology may also be drawn from the A1 event. The capital gains would be arrived at by

deduction of the asset cost base from the price received on selling the asset (Krever, 2017).

Cost Base

1

The client given has conducted a host of transactions which involve asset disposal of different

types. Also, vital information has been presented based on which it is apparent that the disposal

of these assets is not as part of business activity by client. This implies that these transactions

would lead to generation of capital proceeds and not revenue proceeds. This has high relevance

with regards to taxation as capital proceeds do not attract any taxation unlike revenue proceeds.

However, a key aspect in relation to capital receipts is that Capital Gains Tax (CGT) may be

applicable on any capital gains tax that the taxpayer would have realised. Hence, the key focus of

the discussion with regards to the transactions would be on highlighting the capital gains

implications.

To assist in this regards, it is vital to introduce some of the key terms which would be relevant to

the discussion of the tax implications of the given transactions (Barkoczy, 2017).

Pre- CGT Asset

This concept has been introduced in s. 149(10) ITAA 1997 as per which all assets which the

taxpayer acquires on or before September 19, 1985 would be categorised as pre-CGT assets. The

reason for defining these assets can be linked to the fact that unlike the post CGT assets, these

assets do not attract CGT liability (Krever, 2017). The non-application of CGT on the capital

gains does not get influenced by the holding period and exact capital gains or losses generated on

sale.

CGT Event

The term CGT event has special relevance in the capital gains computation as the necessity to

determine the underlying capital gains/losses arise only when such an event takes place. The list

of all the CGT events has been presented as per s.104-5, ITAA 1997 (Gilders, et. al., 2015). A

particular event which is highly relevant to the given client is A1 event which transpires once

there has been disposal of the asset. Accordingly, the definition of capital gains computation

methodology may also be drawn from the A1 event. The capital gains would be arrived at by

deduction of the asset cost base from the price received on selling the asset (Krever, 2017).

Cost Base

1

In the computation of capital gains as per the formula provided by event A1, a key role is played

by the cost base of the asset (Reuters, 2017). The definition of this term has been provided in s.

110-25. In accordance with that definition s. 110-25(1) states that cost base is essentially the

amalgamation of five key components called as elements (Austlii, 2018 a).

Component 1: The price at which the asset was initially procured by the taxpayer.

Component 2: Any relevant costs (such as stamp duties, legal fees, agent fees) which the

taxpayer incurs which procuring the asset or disposing the same.

Component 3: Any relevant ownership costs (such as taxes, interest on capital investment in

asset) which are incurred as part of the ownership of asset.

Component 4: Any capital expenditure that is spent by taxpayer with the intention of preserving

asset value or appreciating the same.

Component 5: Any capital expenditure that is spent by taxpayer in relation to title maintenance

of the underlying asset (especially property) (Nethercott, Richardson and Devos, 2016).

Concessions in Capital Gains

It is pivotal to note that CGT is not applied to the capital gains derived after applying the relevant

formula listed in A1 event. Instead there are two methods which can help with the objective of

lowering CGT liability. These are indexation method and discount method. The indexation asset

has limited usage considering it is useful only for assets purchased before September 1999. This

is not the case with discount method as per which a rebate of 50% in the capital gains is provided

which then yields taxable capital gains. However, as per s. 115-25(1) ITAA 1997, a crucial

condition is that the underlying gains must be long term gains. The gains arising from those

assets where the taxpayers’ holding period exceeds a year would be termed as long term capital

gains.

Subject of Capital Losses

When the formula stated in A1 event is applied, at times capital losses are generated. The big

question thus emerges as to how to deal with these. The first pivotal point to make note is that

capital losses cannot be used to negate taxable income (Barkoczy, 2017). These can only be

2

by the cost base of the asset (Reuters, 2017). The definition of this term has been provided in s.

110-25. In accordance with that definition s. 110-25(1) states that cost base is essentially the

amalgamation of five key components called as elements (Austlii, 2018 a).

Component 1: The price at which the asset was initially procured by the taxpayer.

Component 2: Any relevant costs (such as stamp duties, legal fees, agent fees) which the

taxpayer incurs which procuring the asset or disposing the same.

Component 3: Any relevant ownership costs (such as taxes, interest on capital investment in

asset) which are incurred as part of the ownership of asset.

Component 4: Any capital expenditure that is spent by taxpayer with the intention of preserving

asset value or appreciating the same.

Component 5: Any capital expenditure that is spent by taxpayer in relation to title maintenance

of the underlying asset (especially property) (Nethercott, Richardson and Devos, 2016).

Concessions in Capital Gains

It is pivotal to note that CGT is not applied to the capital gains derived after applying the relevant

formula listed in A1 event. Instead there are two methods which can help with the objective of

lowering CGT liability. These are indexation method and discount method. The indexation asset

has limited usage considering it is useful only for assets purchased before September 1999. This

is not the case with discount method as per which a rebate of 50% in the capital gains is provided

which then yields taxable capital gains. However, as per s. 115-25(1) ITAA 1997, a crucial

condition is that the underlying gains must be long term gains. The gains arising from those

assets where the taxpayers’ holding period exceeds a year would be termed as long term capital

gains.

Subject of Capital Losses

When the formula stated in A1 event is applied, at times capital losses are generated. The big

question thus emerges as to how to deal with these. The first pivotal point to make note is that

capital losses cannot be used to negate taxable income (Barkoczy, 2017). These can only be

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

adjusted against capital gains, thereby reducing the capital gains to the extent of capital losses.

However, if no capital gains exist against which the capital loss may be adjusted, then this capital

loss is carried forward to the next tax year and this process can be continued for a period of five

years for a given capital loss (Nethercott, Richardson and Devos, 2016).

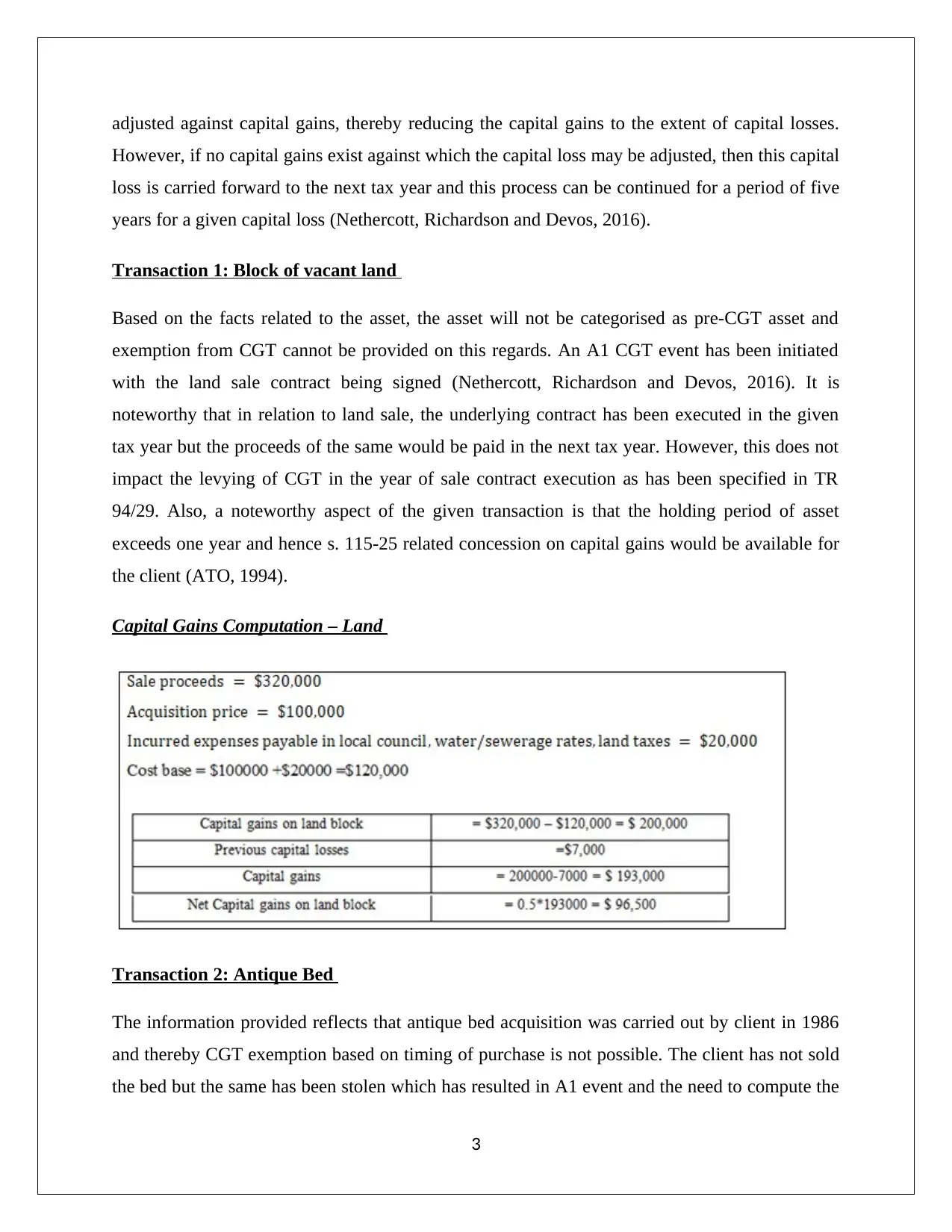

Transaction 1: Block of vacant land

Based on the facts related to the asset, the asset will not be categorised as pre-CGT asset and

exemption from CGT cannot be provided on this regards. An A1 CGT event has been initiated

with the land sale contract being signed (Nethercott, Richardson and Devos, 2016). It is

noteworthy that in relation to land sale, the underlying contract has been executed in the given

tax year but the proceeds of the same would be paid in the next tax year. However, this does not

impact the levying of CGT in the year of sale contract execution as has been specified in TR

94/29. Also, a noteworthy aspect of the given transaction is that the holding period of asset

exceeds one year and hence s. 115-25 related concession on capital gains would be available for

the client (ATO, 1994).

Capital Gains Computation – Land

Transaction 2: Antique Bed

The information provided reflects that antique bed acquisition was carried out by client in 1986

and thereby CGT exemption based on timing of purchase is not possible. The client has not sold

the bed but the same has been stolen which has resulted in A1 event and the need to compute the

3

However, if no capital gains exist against which the capital loss may be adjusted, then this capital

loss is carried forward to the next tax year and this process can be continued for a period of five

years for a given capital loss (Nethercott, Richardson and Devos, 2016).

Transaction 1: Block of vacant land

Based on the facts related to the asset, the asset will not be categorised as pre-CGT asset and

exemption from CGT cannot be provided on this regards. An A1 CGT event has been initiated

with the land sale contract being signed (Nethercott, Richardson and Devos, 2016). It is

noteworthy that in relation to land sale, the underlying contract has been executed in the given

tax year but the proceeds of the same would be paid in the next tax year. However, this does not

impact the levying of CGT in the year of sale contract execution as has been specified in TR

94/29. Also, a noteworthy aspect of the given transaction is that the holding period of asset

exceeds one year and hence s. 115-25 related concession on capital gains would be available for

the client (ATO, 1994).

Capital Gains Computation – Land

Transaction 2: Antique Bed

The information provided reflects that antique bed acquisition was carried out by client in 1986

and thereby CGT exemption based on timing of purchase is not possible. The client has not sold

the bed but the same has been stolen which has resulted in A1 event and the need to compute the

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

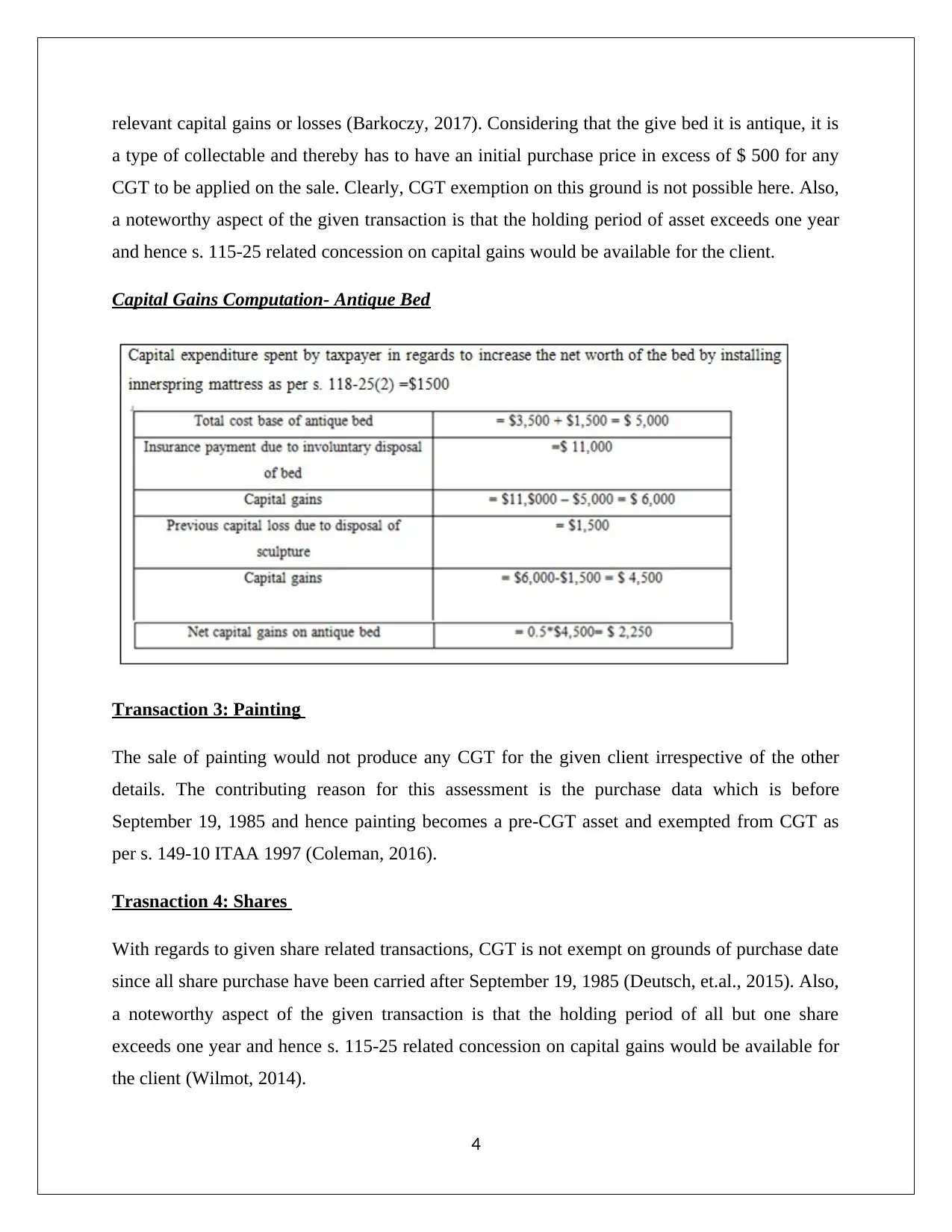

relevant capital gains or losses (Barkoczy, 2017). Considering that the give bed it is antique, it is

a type of collectable and thereby has to have an initial purchase price in excess of $ 500 for any

CGT to be applied on the sale. Clearly, CGT exemption on this ground is not possible here. Also,

a noteworthy aspect of the given transaction is that the holding period of asset exceeds one year

and hence s. 115-25 related concession on capital gains would be available for the client.

Capital Gains Computation- Antique Bed

Transaction 3: Painting

The sale of painting would not produce any CGT for the given client irrespective of the other

details. The contributing reason for this assessment is the purchase data which is before

September 19, 1985 and hence painting becomes a pre-CGT asset and exempted from CGT as

per s. 149-10 ITAA 1997 (Coleman, 2016).

Trasnaction 4: Shares

With regards to given share related transactions, CGT is not exempt on grounds of purchase date

since all share purchase have been carried after September 19, 1985 (Deutsch, et.al., 2015). Also,

a noteworthy aspect of the given transaction is that the holding period of all but one share

exceeds one year and hence s. 115-25 related concession on capital gains would be available for

the client (Wilmot, 2014).

4

a type of collectable and thereby has to have an initial purchase price in excess of $ 500 for any

CGT to be applied on the sale. Clearly, CGT exemption on this ground is not possible here. Also,

a noteworthy aspect of the given transaction is that the holding period of asset exceeds one year

and hence s. 115-25 related concession on capital gains would be available for the client.

Capital Gains Computation- Antique Bed

Transaction 3: Painting

The sale of painting would not produce any CGT for the given client irrespective of the other

details. The contributing reason for this assessment is the purchase data which is before

September 19, 1985 and hence painting becomes a pre-CGT asset and exempted from CGT as

per s. 149-10 ITAA 1997 (Coleman, 2016).

Trasnaction 4: Shares

With regards to given share related transactions, CGT is not exempt on grounds of purchase date

since all share purchase have been carried after September 19, 1985 (Deutsch, et.al., 2015). Also,

a noteworthy aspect of the given transaction is that the holding period of all but one share

exceeds one year and hence s. 115-25 related concession on capital gains would be available for

the client (Wilmot, 2014).

4

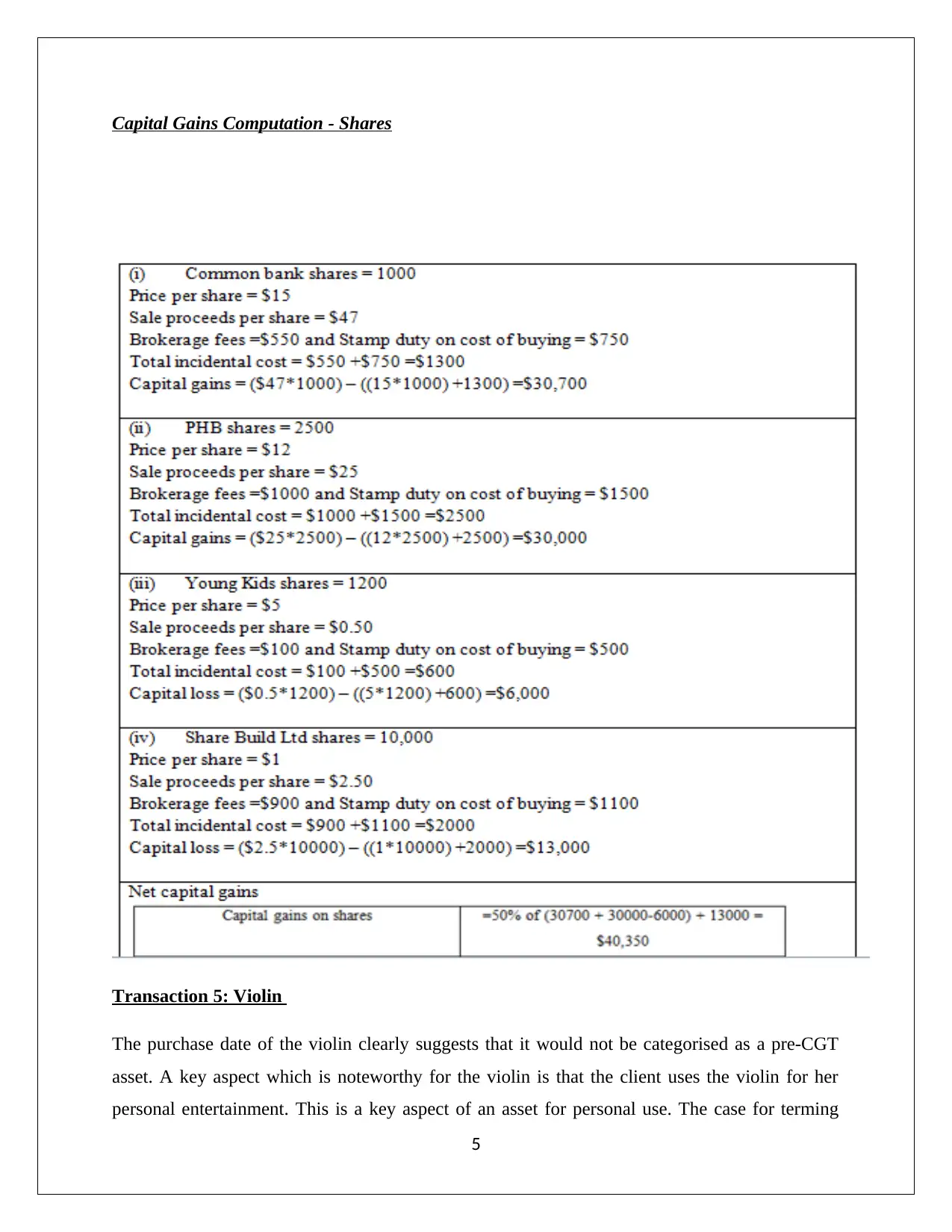

Capital Gains Computation - Shares

Transaction 5: Violin

The purchase date of the violin clearly suggests that it would not be categorised as a pre-CGT

asset. A key aspect which is noteworthy for the violin is that the client uses the violin for her

personal entertainment. This is a key aspect of an asset for personal use. The case for terming

5

Transaction 5: Violin

The purchase date of the violin clearly suggests that it would not be categorised as a pre-CGT

asset. A key aspect which is noteworthy for the violin is that the client uses the violin for her

personal entertainment. This is a key aspect of an asset for personal use. The case for terming

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

violin as an asset of personal use is strengthened considering taxpayer has skill in playing the

instrument and has a host of violins which are played quite often (Deutsch, et.al., 2015).

Therefore, violin instead of being recognised as a collectable would be instead personal use

asset. With regards to these assets, CGT applicability is linked to purchase price which has to be

in excess of $ 10,000. Clearly, the given transaction does not satisfy this minimum condition

with the result that CGT exemption would be available for violin.

Capital gains (Cumulative)

Question 2

(a) Certain benefits provided to employees by employer are of personal nature and provided in

non-cash form and these are referred to as fringe benefits. The taxation of the fringe benefits

is dictated by the appropriate clauses mentioned in “Fringe Benefit Tax Assessment Act

(FBTAA) 1986”. A key feature of the FBT (Fringe Benefit Tax) regime is that the complete

tax burden falls on the employer and employee despite being the recipient of these benefits

do not have to pay any tax. The discussion in the context of key fringe benefits that Rapid

Heat has provided to Jasmine is carried out below.

Car Fringe Benefit

This is explained in s. 7 FBTAA 1986 which hints that a necessary condition for extension of car

fringe benefit is that the employer owned car should be available to the employee for usage of

personal nature. Extension of car by the employer along does not amount to car fringe benefit as

the employee would get benefit on account of car when employer has allowed the car for

personal use of employee and relevant associates (Woellner, 2017).

In the presented circumstances, Rapid Heat (in the capacity of employer) has given a Jaguar car

to Jasmine (in the capacity of employee). The employer has provided consent for personal usage

of the car by the employee. As a result of this decision, FBT liability would arise for Rapid Heat

6

instrument and has a host of violins which are played quite often (Deutsch, et.al., 2015).

Therefore, violin instead of being recognised as a collectable would be instead personal use

asset. With regards to these assets, CGT applicability is linked to purchase price which has to be

in excess of $ 10,000. Clearly, the given transaction does not satisfy this minimum condition

with the result that CGT exemption would be available for violin.

Capital gains (Cumulative)

Question 2

(a) Certain benefits provided to employees by employer are of personal nature and provided in

non-cash form and these are referred to as fringe benefits. The taxation of the fringe benefits

is dictated by the appropriate clauses mentioned in “Fringe Benefit Tax Assessment Act

(FBTAA) 1986”. A key feature of the FBT (Fringe Benefit Tax) regime is that the complete

tax burden falls on the employer and employee despite being the recipient of these benefits

do not have to pay any tax. The discussion in the context of key fringe benefits that Rapid

Heat has provided to Jasmine is carried out below.

Car Fringe Benefit

This is explained in s. 7 FBTAA 1986 which hints that a necessary condition for extension of car

fringe benefit is that the employer owned car should be available to the employee for usage of

personal nature. Extension of car by the employer along does not amount to car fringe benefit as

the employee would get benefit on account of car when employer has allowed the car for

personal use of employee and relevant associates (Woellner, 2017).

In the presented circumstances, Rapid Heat (in the capacity of employer) has given a Jaguar car

to Jasmine (in the capacity of employee). The employer has provided consent for personal usage

of the car by the employee. As a result of this decision, FBT liability would arise for Rapid Heat

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

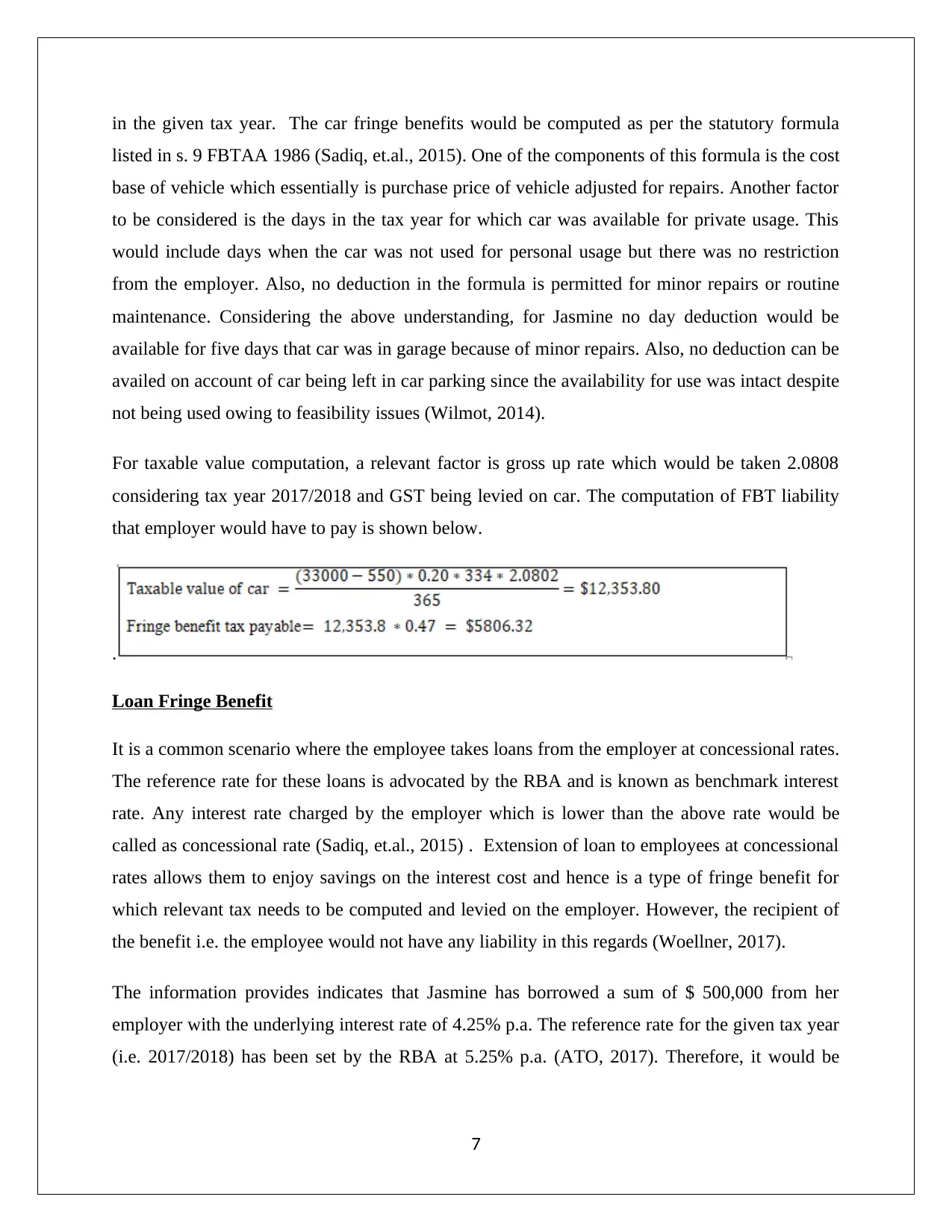

in the given tax year. The car fringe benefits would be computed as per the statutory formula

listed in s. 9 FBTAA 1986 (Sadiq, et.al., 2015). One of the components of this formula is the cost

base of vehicle which essentially is purchase price of vehicle adjusted for repairs. Another factor

to be considered is the days in the tax year for which car was available for private usage. This

would include days when the car was not used for personal usage but there was no restriction

from the employer. Also, no deduction in the formula is permitted for minor repairs or routine

maintenance. Considering the above understanding, for Jasmine no day deduction would be

available for five days that car was in garage because of minor repairs. Also, no deduction can be

availed on account of car being left in car parking since the availability for use was intact despite

not being used owing to feasibility issues (Wilmot, 2014).

For taxable value computation, a relevant factor is gross up rate which would be taken 2.0808

considering tax year 2017/2018 and GST being levied on car. The computation of FBT liability

that employer would have to pay is shown below.

.

Loan Fringe Benefit

It is a common scenario where the employee takes loans from the employer at concessional rates.

The reference rate for these loans is advocated by the RBA and is known as benchmark interest

rate. Any interest rate charged by the employer which is lower than the above rate would be

called as concessional rate (Sadiq, et.al., 2015) . Extension of loan to employees at concessional

rates allows them to enjoy savings on the interest cost and hence is a type of fringe benefit for

which relevant tax needs to be computed and levied on the employer. However, the recipient of

the benefit i.e. the employee would not have any liability in this regards (Woellner, 2017).

The information provides indicates that Jasmine has borrowed a sum of $ 500,000 from her

employer with the underlying interest rate of 4.25% p.a. The reference rate for the given tax year

(i.e. 2017/2018) has been set by the RBA at 5.25% p.a. (ATO, 2017). Therefore, it would be

7

listed in s. 9 FBTAA 1986 (Sadiq, et.al., 2015). One of the components of this formula is the cost

base of vehicle which essentially is purchase price of vehicle adjusted for repairs. Another factor

to be considered is the days in the tax year for which car was available for private usage. This

would include days when the car was not used for personal usage but there was no restriction

from the employer. Also, no deduction in the formula is permitted for minor repairs or routine

maintenance. Considering the above understanding, for Jasmine no day deduction would be

available for five days that car was in garage because of minor repairs. Also, no deduction can be

availed on account of car being left in car parking since the availability for use was intact despite

not being used owing to feasibility issues (Wilmot, 2014).

For taxable value computation, a relevant factor is gross up rate which would be taken 2.0808

considering tax year 2017/2018 and GST being levied on car. The computation of FBT liability

that employer would have to pay is shown below.

.

Loan Fringe Benefit

It is a common scenario where the employee takes loans from the employer at concessional rates.

The reference rate for these loans is advocated by the RBA and is known as benchmark interest

rate. Any interest rate charged by the employer which is lower than the above rate would be

called as concessional rate (Sadiq, et.al., 2015) . Extension of loan to employees at concessional

rates allows them to enjoy savings on the interest cost and hence is a type of fringe benefit for

which relevant tax needs to be computed and levied on the employer. However, the recipient of

the benefit i.e. the employee would not have any liability in this regards (Woellner, 2017).

The information provides indicates that Jasmine has borrowed a sum of $ 500,000 from her

employer with the underlying interest rate of 4.25% p.a. The reference rate for the given tax year

(i.e. 2017/2018) has been set by the RBA at 5.25% p.a. (ATO, 2017). Therefore, it would be

7

correct to conclude that loan given to Jasmine has been extended at the concessional rate and

therefore would attract FBT liability.

For taxable value computation, a relevant factor is gross up rate which would be taken 1.8868

considering tax year 2017/2018 and GST not being levied on loan. The computation of FBT

liability that employer would have to pay is shown below.

With regards to loan utilisation, it can be done by employee or any associate. However, for the

employer, this usage pattern has special significance. This is because FBTAA 1986 allows

deduction for the employer on the loan amount to the extent that it is used for income generation

by the employee. A crucial point to note is that if the loan proceeds are used by an associate of

employee for income generation, then tax deduction are not available to the employer

(Hodgson,Mortimer and Butler, 2016). Applying this understanding to the given circumstance,

Rapid Heat may be able to avail deduction to the extent of interest saving enjoyed by Jasmine on

the $ 450,000 loan utilised for buying holiday house if it starts producing assessable income.

However, the remaining amount of $ 50,000 would not yield any deduction since it is used by

her husband.

Internal Expense Fringe Benefit

Any benefit that employer provides which seeks the cash outflow of employee in relation to

private expense is referred to as expense fringe benefit. This can be illustrated using the given

scenario. Jasmine wanted to purchase a heater made by Rapid Heat (Gilders, et. al., 2015). In

order buy the same for her consumption, she would have to spend $ 2,600. However, the

employer provided her for half the amount, thereby paying the remainder half by itself. As a

result, the private expense cash outflow of Jasmine lowered by $ 1,300 and therefore FBT would

be levied on employer for the same.

8

therefore would attract FBT liability.

For taxable value computation, a relevant factor is gross up rate which would be taken 1.8868

considering tax year 2017/2018 and GST not being levied on loan. The computation of FBT

liability that employer would have to pay is shown below.

With regards to loan utilisation, it can be done by employee or any associate. However, for the

employer, this usage pattern has special significance. This is because FBTAA 1986 allows

deduction for the employer on the loan amount to the extent that it is used for income generation

by the employee. A crucial point to note is that if the loan proceeds are used by an associate of

employee for income generation, then tax deduction are not available to the employer

(Hodgson,Mortimer and Butler, 2016). Applying this understanding to the given circumstance,

Rapid Heat may be able to avail deduction to the extent of interest saving enjoyed by Jasmine on

the $ 450,000 loan utilised for buying holiday house if it starts producing assessable income.

However, the remaining amount of $ 50,000 would not yield any deduction since it is used by

her husband.

Internal Expense Fringe Benefit

Any benefit that employer provides which seeks the cash outflow of employee in relation to

private expense is referred to as expense fringe benefit. This can be illustrated using the given

scenario. Jasmine wanted to purchase a heater made by Rapid Heat (Gilders, et. al., 2015). In

order buy the same for her consumption, she would have to spend $ 2,600. However, the

employer provided her for half the amount, thereby paying the remainder half by itself. As a

result, the private expense cash outflow of Jasmine lowered by $ 1,300 and therefore FBT would

be levied on employer for the same.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For taxable value computation, a relevant factor is gross up rate which would be taken 2.0808

considering tax year 2017/2018 and GST being levied on heater. The computation of FBT

liability that employer would have to pay is shown below.

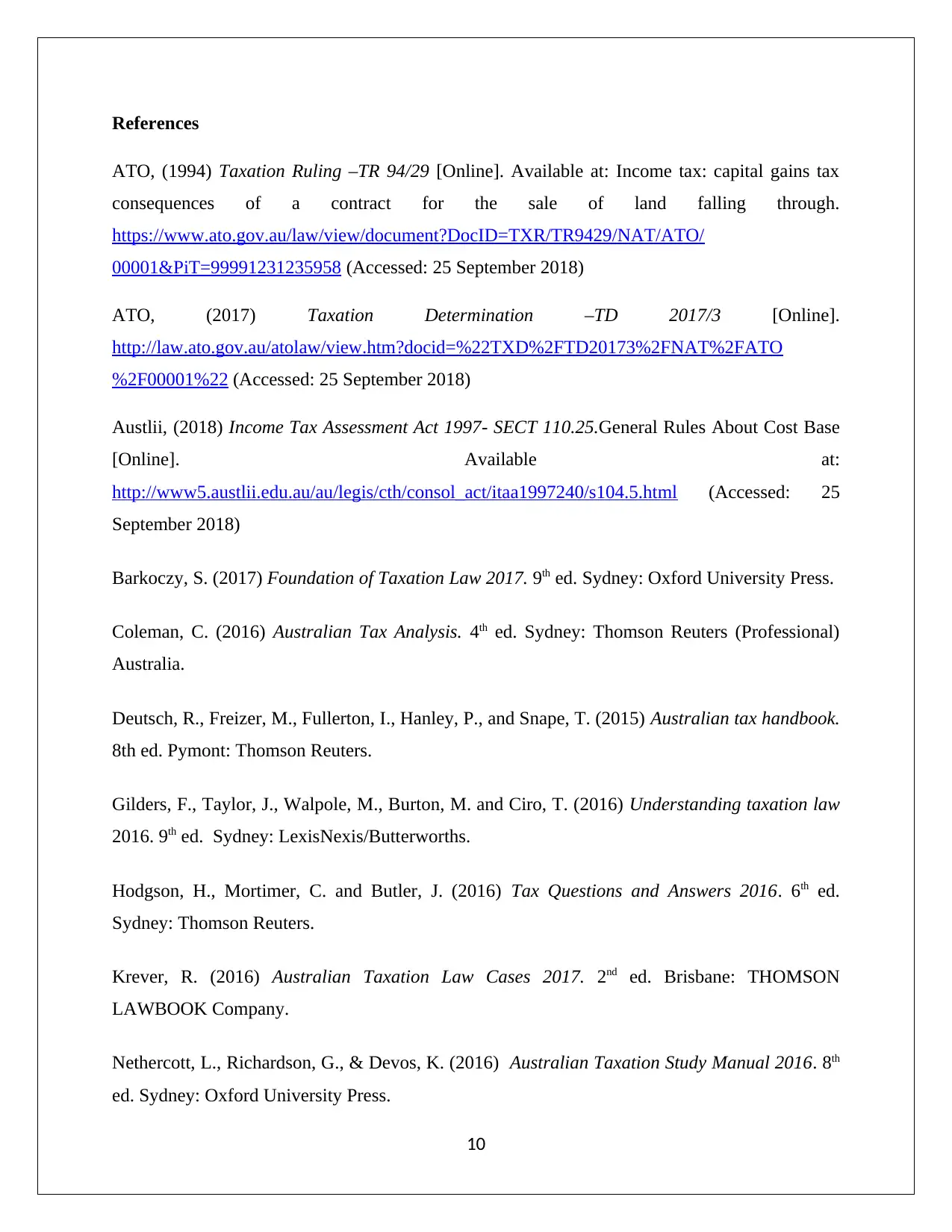

(b) As per the information provided, the $ 50,000 amount which earlier was extended to husband

now is being used by Jasmine herself for buying shares of Telstra. Considering the company

that the shares are being invested in, Jasmine is reasonably expected to receive dividend

income and hence this would be eligible for providing deduction to the employer which is

can be computed in the manner exhibited follows.

9

considering tax year 2017/2018 and GST being levied on heater. The computation of FBT

liability that employer would have to pay is shown below.

(b) As per the information provided, the $ 50,000 amount which earlier was extended to husband

now is being used by Jasmine herself for buying shares of Telstra. Considering the company

that the shares are being invested in, Jasmine is reasonably expected to receive dividend

income and hence this would be eligible for providing deduction to the employer which is

can be computed in the manner exhibited follows.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 25 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 25 September 2018)

Austlii, (2018) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost Base

[Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 25

September 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

10

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 25 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 25 September 2018)

Austlii, (2018) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost Base

[Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 25

September 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

10

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.