Taxation Law Assignment - LAW505 - Charles Sturt University

VerifiedAdded on 2022/09/18

|16

|2944

|23

Homework Assignment

AI Summary

This taxation law assignment, prepared by a Charles Sturt University student, addresses two key questions concerning taxation principles. The first question delves into the assessability of various compensation receipts, including damages for loss of reputation, loss of income, and reimbursement of legal fees, for two clients, Sophie and Kate, under the ITAA 1997. It examines relevant rulings like TR 95/35 and case law such as FCT v Spedley Securities Ltd (1988) and Allsop v FC of T (1965), determining whether these receipts constitute assessable income or capital gains. The second question focuses on capital gains tax (CGT) implications related to an inherited main residence, analyzing whether a taxpayer is liable for CGT under section 118-195 of the ITAA 1997, considering the specific circumstances of Joe and Amy who inherited a property from their father. The assignment provides a detailed application of the law, citing ATO guidelines and relevant sections of the ITAA 1997 to support its conclusions.

Running head: TAXATION LAW

tAXATION lAW

tAXATION lAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

2TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Introduction:...........................................................................................................................3

Various Compensation Receipts:...........................................................................................3

Sophie Client:.........................................................................................................................3

2.1: Lump sum damages for potential loss of reputation.......................................................3

2.2: Compensation for the loss of income whilst the machine was being replaced:..............4

2.3: Reimbursement of Legal Fees:.......................................................................................5

3: Kate Client:............................................................................................................................6

3.1 A Lump sum payment for pain and suffering:.................................................................6

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................7

Conclusion:............................................................................................................................8

Answer to question 2:.................................................................................................................9

Introduction:...........................................................................................................................9

Rule:.......................................................................................................................................9

Client Joe and Amy:.............................................................................................................10

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................11

References:...............................................................................................................................13

Table of Contents

Answer to question 1:.................................................................................................................3

Introduction:...........................................................................................................................3

Various Compensation Receipts:...........................................................................................3

Sophie Client:.........................................................................................................................3

2.1: Lump sum damages for potential loss of reputation.......................................................3

2.2: Compensation for the loss of income whilst the machine was being replaced:..............4

2.3: Reimbursement of Legal Fees:.......................................................................................5

3: Kate Client:............................................................................................................................6

3.1 A Lump sum payment for pain and suffering:.................................................................6

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................7

Conclusion:............................................................................................................................8

Answer to question 2:.................................................................................................................9

Introduction:...........................................................................................................................9

Rule:.......................................................................................................................................9

Client Joe and Amy:.............................................................................................................10

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................11

References:...............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to question 1:

Introduction:

1.1. Is the lump sum damages, compensation for loss of earnings and reimbursement of

legal fees to Sophie and Kate for the general damages will be considered as assessable

pays under the “section 6-5, ITAA 1997”?

1.2. Whether any capital gains originating from the general damages payment ignored

within the jurisdictive provision of “section 118-37, ITAA 1997”?

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for probable loss of reputation

Rule:

Referring to “Taxation Ruling of TR 95/35” it provides guidelines relating to income

tax considerations of compensation incomes (Taxation Ruling of TR 95/35 ). The ruling is

generally applicable on those persons that receives any amount as compensation. It take into

the account the CGT consequences relating to the receipt of the compensation sum and

determines whether the sum must be counted for tax liability for the recipient under the “Part

IIIA of the ITAA 1936” (Part IIIA of the ITAA 1936).

If any amount that is obtained by the taxpayer is entirely for the sale of the underlying

asset or a portion of the underlying asset of an individual taxpayer then the compensation

constitute the consideration that is obtained upon the sale of the asset. Similarly the court in

“FC of T v Spedley Securities Ltd (1988)” held that the amount received included the

recompense for damage to the business goodwill which was agreed as the item of capital (FC

of T v Spedley Securities Ltd (1988) ).

Answer to question 1:

Introduction:

1.1. Is the lump sum damages, compensation for loss of earnings and reimbursement of

legal fees to Sophie and Kate for the general damages will be considered as assessable

pays under the “section 6-5, ITAA 1997”?

1.2. Whether any capital gains originating from the general damages payment ignored

within the jurisdictive provision of “section 118-37, ITAA 1997”?

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for probable loss of reputation

Rule:

Referring to “Taxation Ruling of TR 95/35” it provides guidelines relating to income

tax considerations of compensation incomes (Taxation Ruling of TR 95/35 ). The ruling is

generally applicable on those persons that receives any amount as compensation. It take into

the account the CGT consequences relating to the receipt of the compensation sum and

determines whether the sum must be counted for tax liability for the recipient under the “Part

IIIA of the ITAA 1936” (Part IIIA of the ITAA 1936).

If any amount that is obtained by the taxpayer is entirely for the sale of the underlying

asset or a portion of the underlying asset of an individual taxpayer then the compensation

constitute the consideration that is obtained upon the sale of the asset. Similarly the court in

“FC of T v Spedley Securities Ltd (1988)” held that the amount received included the

recompense for damage to the business goodwill which was agreed as the item of capital (FC

of T v Spedley Securities Ltd (1988) ).

5TAXATION LAW

Application:

The case study provides that Sophie sued FracPro for compensation after the faulty

calibration of laser machine leading to loss of income and business name. Sophie received a

lump sum of $100,000 damages for the probable loss of business status and reimbursement of

$7,000 for the legal fees. Referring to “FCT v Spedley Securities Ltd (1988)” the amount got

by Sophie included the compensation for injury to the business reputation which should be

agreed as the item of capital.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Rule:

According to the explanation given in “taxation determination ruling of TD 93/58”

certain types of compensation payment such as lump sum compensation or any form of

settlement payment received by taxpayer is considered taxable earnings. Compensation that a

taxpayer gets relating to the loss of income is characterised as the taxable earnings under

“subsection 25 (1) of the ITAA 1936”, given that; (Barkoczy, 2019).

a. The payment which is given to taxpayer as recompense is associated to the loss of

income or;

b. The lump sum imbursement can be recognized and measureable as income. This

happens when the parties agree whichever specifically or impliedly that some of

the imbursement recounts for the loss of earnings character.

Referring to “Allsop v FC of T (1965)” the verdict specified that payment given to taxpayer

also includes the lump sum payment which contains capital in character but the constituents

Application:

The case study provides that Sophie sued FracPro for compensation after the faulty

calibration of laser machine leading to loss of income and business name. Sophie received a

lump sum of $100,000 damages for the probable loss of business status and reimbursement of

$7,000 for the legal fees. Referring to “FCT v Spedley Securities Ltd (1988)” the amount got

by Sophie included the compensation for injury to the business reputation which should be

agreed as the item of capital.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Rule:

According to the explanation given in “taxation determination ruling of TD 93/58”

certain types of compensation payment such as lump sum compensation or any form of

settlement payment received by taxpayer is considered taxable earnings. Compensation that a

taxpayer gets relating to the loss of income is characterised as the taxable earnings under

“subsection 25 (1) of the ITAA 1936”, given that; (Barkoczy, 2019).

a. The payment which is given to taxpayer as recompense is associated to the loss of

income or;

b. The lump sum imbursement can be recognized and measureable as income. This

happens when the parties agree whichever specifically or impliedly that some of

the imbursement recounts for the loss of earnings character.

Referring to “Allsop v FC of T (1965)” the verdict specified that payment given to taxpayer

also includes the lump sum payment which contains capital in character but the constituents

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

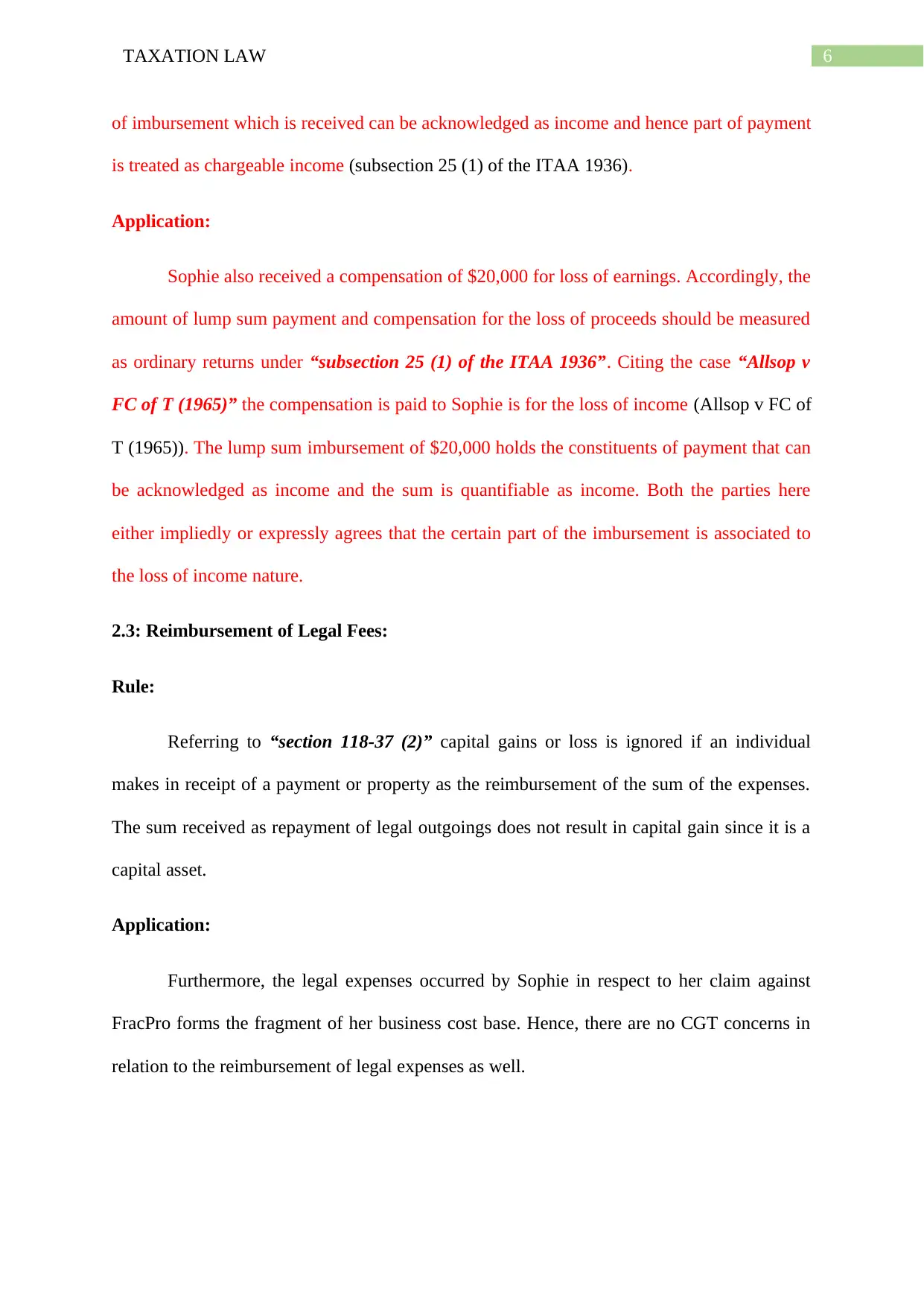

of imbursement which is received can be acknowledged as income and hence part of payment

is treated as chargeable income (subsection 25 (1) of the ITAA 1936).

Application:

Sophie also received a compensation of $20,000 for loss of earnings. Accordingly, the

amount of lump sum payment and compensation for the loss of proceeds should be measured

as ordinary returns under “subsection 25 (1) of the ITAA 1936”. Citing the case “Allsop v

FC of T (1965)” the compensation is paid to Sophie is for the loss of income (Allsop v FC of

T (1965)). The lump sum imbursement of $20,000 holds the constituents of payment that can

be acknowledged as income and the sum is quantifiable as income. Both the parties here

either impliedly or expressly agrees that the certain part of the imbursement is associated to

the loss of income nature.

2.3: Reimbursement of Legal Fees:

Rule:

Referring to “section 118-37 (2)” capital gains or loss is ignored if an individual

makes in receipt of a payment or property as the reimbursement of the sum of the expenses.

The sum received as repayment of legal outgoings does not result in capital gain since it is a

capital asset.

Application:

Furthermore, the legal expenses occurred by Sophie in respect to her claim against

FracPro forms the fragment of her business cost base. Hence, there are no CGT concerns in

relation to the reimbursement of legal expenses as well.

of imbursement which is received can be acknowledged as income and hence part of payment

is treated as chargeable income (subsection 25 (1) of the ITAA 1936).

Application:

Sophie also received a compensation of $20,000 for loss of earnings. Accordingly, the

amount of lump sum payment and compensation for the loss of proceeds should be measured

as ordinary returns under “subsection 25 (1) of the ITAA 1936”. Citing the case “Allsop v

FC of T (1965)” the compensation is paid to Sophie is for the loss of income (Allsop v FC of

T (1965)). The lump sum imbursement of $20,000 holds the constituents of payment that can

be acknowledged as income and the sum is quantifiable as income. Both the parties here

either impliedly or expressly agrees that the certain part of the imbursement is associated to

the loss of income nature.

2.3: Reimbursement of Legal Fees:

Rule:

Referring to “section 118-37 (2)” capital gains or loss is ignored if an individual

makes in receipt of a payment or property as the reimbursement of the sum of the expenses.

The sum received as repayment of legal outgoings does not result in capital gain since it is a

capital asset.

Application:

Furthermore, the legal expenses occurred by Sophie in respect to her claim against

FracPro forms the fragment of her business cost base. Hence, there are no CGT concerns in

relation to the reimbursement of legal expenses as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Rule:

As explained in the “paragraph 118-37 (1)(a), ITAA 1997” a person must overlook

the capital gains that is derived from the CGT event when it is noticed that the money

received is allied to the reward that is received for any wrong or injury sustained. The capital

gains derived from the right of seeking compensation is ignored under “paragraph 118-37

(1)(a), ITAA 1997” since it is capital amount.

Application:

Meanwhile under the current situation of Kate, the lump sum payment for pain and

distress as well as medical costs cannot be treated as proceeds from render any individual

services, revenue from property or revenue derived from conducting any business. The

imbursement was not earned by her since it does not have relation to any performance of

services. Instead, it was a one-off payment for Kate which do not contain any component of

consistency or repetition.

Even though the payment was anticipated and relied upon by Kate, the anticipated

only originated from the pain and suffering out of alleged hurt and general damages instead

of from any kind of relationship to personal services performed.

The entire settlement amount for damages is regarded as capital profits from the

“CGT event C2” occurring to her right of seeking compensation. Therefore, capital gains

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Rule:

As explained in the “paragraph 118-37 (1)(a), ITAA 1997” a person must overlook

the capital gains that is derived from the CGT event when it is noticed that the money

received is allied to the reward that is received for any wrong or injury sustained. The capital

gains derived from the right of seeking compensation is ignored under “paragraph 118-37

(1)(a), ITAA 1997” since it is capital amount.

Application:

Meanwhile under the current situation of Kate, the lump sum payment for pain and

distress as well as medical costs cannot be treated as proceeds from render any individual

services, revenue from property or revenue derived from conducting any business. The

imbursement was not earned by her since it does not have relation to any performance of

services. Instead, it was a one-off payment for Kate which do not contain any component of

consistency or repetition.

Even though the payment was anticipated and relied upon by Kate, the anticipated

only originated from the pain and suffering out of alleged hurt and general damages instead

of from any kind of relationship to personal services performed.

The entire settlement amount for damages is regarded as capital profits from the

“CGT event C2” occurring to her right of seeking compensation. Therefore, capital gains

8TAXATION LAW

derived from the CGT event occurring out of Kate’s right to seek compensation should be

ignored under the paragraph “sec 118-37(1)(b), ITAA 1997”.

3.2 Payment of ongoing medical and cosmetic surgery costs

Rule:

Receipt of lump sum imbursement may result in capital gain. The net sum of capital

gains derived by the taxpayer is later included into their assessable earnings under the

“section 102-5, ITAA 1997” unless any exemption is applicable. The exempted transaction

under “Division 118, ITAA 1997” includes the payment received by the taxpayer as

compensation for wrong doings or injury that is suffered by the taxpayer in relation to their

occupation or by the taxpayer personally, such as compensation for discrimination or

harassment at work place then it is exempted under “section 118-37 (1) (a), ITAA 1997”

(Division 118, ITAA 1997). While exemption also applies under “sec 118-37 (1) (b), ITAA

1997” where the payment received by the taxpayer as the compensation is for wrong, illness

or injury sustained by taxpayer or their relatives.

Application:

The payment received by Kate for her medical and cosmetic surgery is a single

payment that do not carry any element of repetition. The imbursement cannot be considered

as earnings from rendering any personal services rather it amounts to capital asset under

“paragraph 118-37(1)(a), ITAA 1997” since the amount is associated to her personal injury.

The entire settlement amount for damages is regarded as capital profits from the “CGT event

C2” occurring to her right of seeking compensation.

3.3 Interest on the lump sum payment

Rule:

derived from the CGT event occurring out of Kate’s right to seek compensation should be

ignored under the paragraph “sec 118-37(1)(b), ITAA 1997”.

3.2 Payment of ongoing medical and cosmetic surgery costs

Rule:

Receipt of lump sum imbursement may result in capital gain. The net sum of capital

gains derived by the taxpayer is later included into their assessable earnings under the

“section 102-5, ITAA 1997” unless any exemption is applicable. The exempted transaction

under “Division 118, ITAA 1997” includes the payment received by the taxpayer as

compensation for wrong doings or injury that is suffered by the taxpayer in relation to their

occupation or by the taxpayer personally, such as compensation for discrimination or

harassment at work place then it is exempted under “section 118-37 (1) (a), ITAA 1997”

(Division 118, ITAA 1997). While exemption also applies under “sec 118-37 (1) (b), ITAA

1997” where the payment received by the taxpayer as the compensation is for wrong, illness

or injury sustained by taxpayer or their relatives.

Application:

The payment received by Kate for her medical and cosmetic surgery is a single

payment that do not carry any element of repetition. The imbursement cannot be considered

as earnings from rendering any personal services rather it amounts to capital asset under

“paragraph 118-37(1)(a), ITAA 1997” since the amount is associated to her personal injury.

The entire settlement amount for damages is regarded as capital profits from the “CGT event

C2” occurring to her right of seeking compensation.

3.3 Interest on the lump sum payment

Rule:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

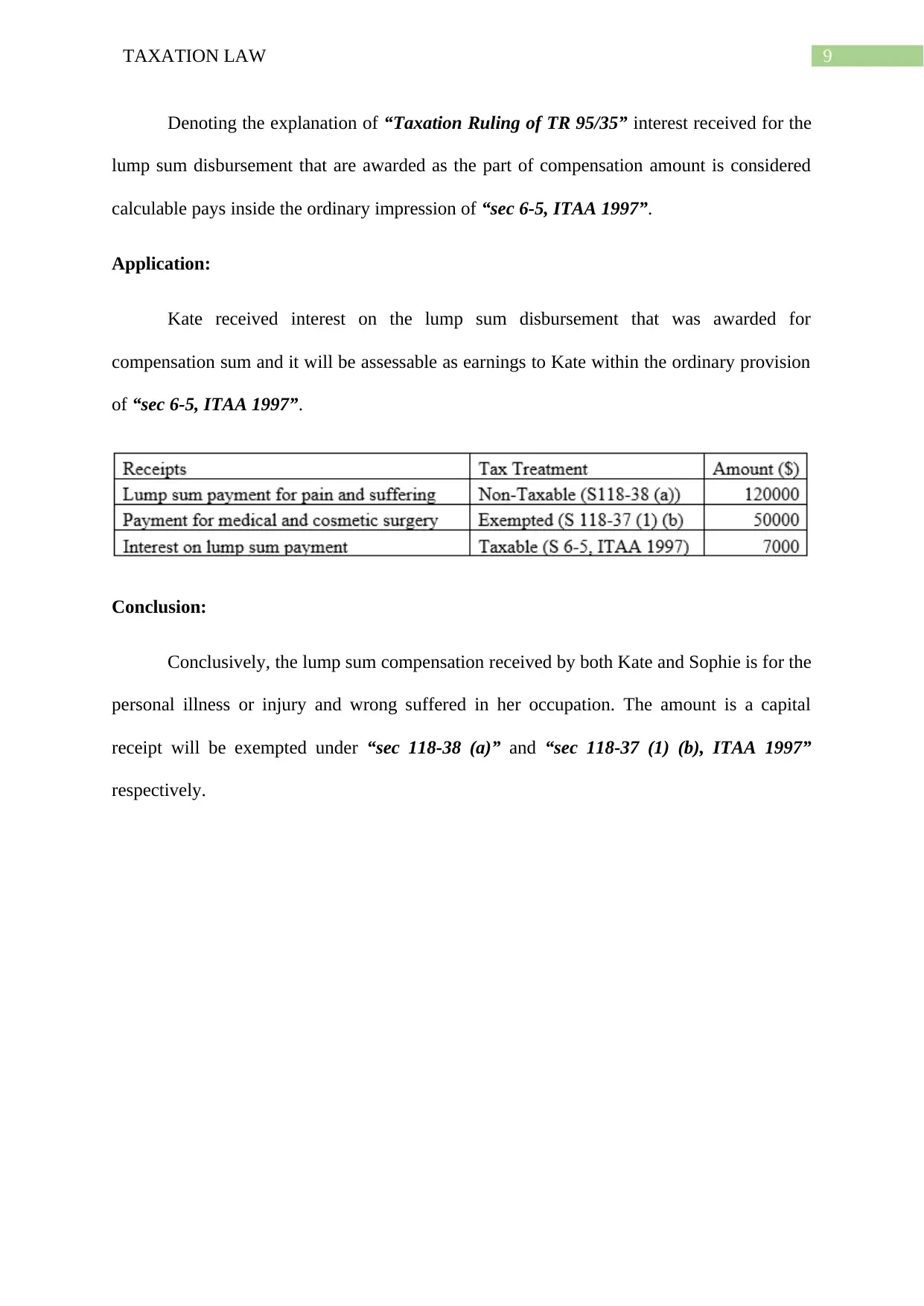

Denoting the explanation of “Taxation Ruling of TR 95/35” interest received for the

lump sum disbursement that are awarded as the part of compensation amount is considered

calculable pays inside the ordinary impression of “sec 6-5, ITAA 1997”.

Application:

Kate received interest on the lump sum disbursement that was awarded for

compensation sum and it will be assessable as earnings to Kate within the ordinary provision

of “sec 6-5, ITAA 1997”.

Conclusion:

Conclusively, the lump sum compensation received by both Kate and Sophie is for the

personal illness or injury and wrong suffered in her occupation. The amount is a capital

receipt will be exempted under “sec 118-38 (a)” and “sec 118-37 (1) (b), ITAA 1997”

respectively.

Denoting the explanation of “Taxation Ruling of TR 95/35” interest received for the

lump sum disbursement that are awarded as the part of compensation amount is considered

calculable pays inside the ordinary impression of “sec 6-5, ITAA 1997”.

Application:

Kate received interest on the lump sum disbursement that was awarded for

compensation sum and it will be assessable as earnings to Kate within the ordinary provision

of “sec 6-5, ITAA 1997”.

Conclusion:

Conclusively, the lump sum compensation received by both Kate and Sophie is for the

personal illness or injury and wrong suffered in her occupation. The amount is a capital

receipt will be exempted under “sec 118-38 (a)” and “sec 118-37 (1) (b), ITAA 1997”

respectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Answer to question 2:

Introduction:

1.1. Will the taxpayer be liable for CGT from the CGT event that takes place in respect to

an inherited main residence under the “section 118-195, ITAA 1997”?

Rule:

As stated by the ATO, an individual taxpayer’s main dwelling is normally exempted

from the CGT. However, in order to gain the exception on the property, it ought to have a

lodging on the property and the taxpayer should have to live on the property. Customarily, a

dwelling is held to be main dwelling if;

a. The taxpayer and their family lived on the property

b. The personal belongings of the taxpayer belonged in it.

c. It forms the address of the taxpayers mail

d. It forms the address of the taxpayer’s electric roll.

There are general rule relating to the CGT and Death where upon the death of the

taxpayer, a CGT event associated to the CGT asset is usually disregarded under the “section

128, ITAA 1997”. Upon the death of the taxpayer, the beneficiary or the heir is believed to

have got the assets on the day of demise. Where the property forms the pre-CGT asset of the

deceased, the new beneficiary is believed to have got the property based on the present

market worth on the day of the demise. While “section 128-15, ITAA 1997” also stated

where the properties is the post-CGT asset of the departed, the beneficiary here is believed to

have got the property on the day of demise based on the assets cost base (Section 128, ITAA

1997).

Answer to question 2:

Introduction:

1.1. Will the taxpayer be liable for CGT from the CGT event that takes place in respect to

an inherited main residence under the “section 118-195, ITAA 1997”?

Rule:

As stated by the ATO, an individual taxpayer’s main dwelling is normally exempted

from the CGT. However, in order to gain the exception on the property, it ought to have a

lodging on the property and the taxpayer should have to live on the property. Customarily, a

dwelling is held to be main dwelling if;

a. The taxpayer and their family lived on the property

b. The personal belongings of the taxpayer belonged in it.

c. It forms the address of the taxpayers mail

d. It forms the address of the taxpayer’s electric roll.

There are general rule relating to the CGT and Death where upon the death of the

taxpayer, a CGT event associated to the CGT asset is usually disregarded under the “section

128, ITAA 1997”. Upon the death of the taxpayer, the beneficiary or the heir is believed to

have got the assets on the day of demise. Where the property forms the pre-CGT asset of the

deceased, the new beneficiary is believed to have got the property based on the present

market worth on the day of the demise. While “section 128-15, ITAA 1997” also stated

where the properties is the post-CGT asset of the departed, the beneficiary here is believed to

have got the property on the day of demise based on the assets cost base (Section 128, ITAA

1997).

11TAXATION LAW

If the properties forms the main home of the deceased and was never utilized for the

purpose of generating income then cost base to the recipient is the market worth on the time

of demise (Kenny et al., 2016). If the asset formed the central abode of the deceased and

never make use of it for generating income, the beneficiary might inherit the exemption of

main residence when the certain conditions given under “section 118-195, ITAA 1997” are

met (section 118-195).

According to the “section 118-195, ITAA 1997” an individual beneficiary is permitted to

disregard any form of capital gain or loss concerning the previous residence of the deceased

person if either of the following conditions are applied.

1. The beneficiary disposed their ownership interest within the time span of two years of

the death of deceased or within the long time period as permitted by the

commissioner;

2. If beneficiary does not sold their ownership inside the span of two years, the house

was, from the stage of deceased demise till the end of possession interest of

beneficiary formed the chief dwelling of one or more of;

a. The wife of deceased during the time of death, or;

b. An individual that has the right of occupying the home under the will of deceased,

or

c. As the recipient of the estate

Client Joe and Amy:

Application:

The case study provides that Joe and Amy inherited the property from their father

after the death of the deceased on 23 May 2015. Joe dwelt on that the property to look after

his father by acting as his full-time care-taker prior to the passing away of the deceased. The

If the properties forms the main home of the deceased and was never utilized for the

purpose of generating income then cost base to the recipient is the market worth on the time

of demise (Kenny et al., 2016). If the asset formed the central abode of the deceased and

never make use of it for generating income, the beneficiary might inherit the exemption of

main residence when the certain conditions given under “section 118-195, ITAA 1997” are

met (section 118-195).

According to the “section 118-195, ITAA 1997” an individual beneficiary is permitted to

disregard any form of capital gain or loss concerning the previous residence of the deceased

person if either of the following conditions are applied.

1. The beneficiary disposed their ownership interest within the time span of two years of

the death of deceased or within the long time period as permitted by the

commissioner;

2. If beneficiary does not sold their ownership inside the span of two years, the house

was, from the stage of deceased demise till the end of possession interest of

beneficiary formed the chief dwelling of one or more of;

a. The wife of deceased during the time of death, or;

b. An individual that has the right of occupying the home under the will of deceased,

or

c. As the recipient of the estate

Client Joe and Amy:

Application:

The case study provides that Joe and Amy inherited the property from their father

after the death of the deceased on 23 May 2015. Joe dwelt on that the property to look after

his father by acting as his full-time care-taker prior to the passing away of the deceased. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.