Taxation Law: Small Business Concession - Analysis and Recommendations

VerifiedAdded on 2021/05/30

|16

|902

|27

Report

AI Summary

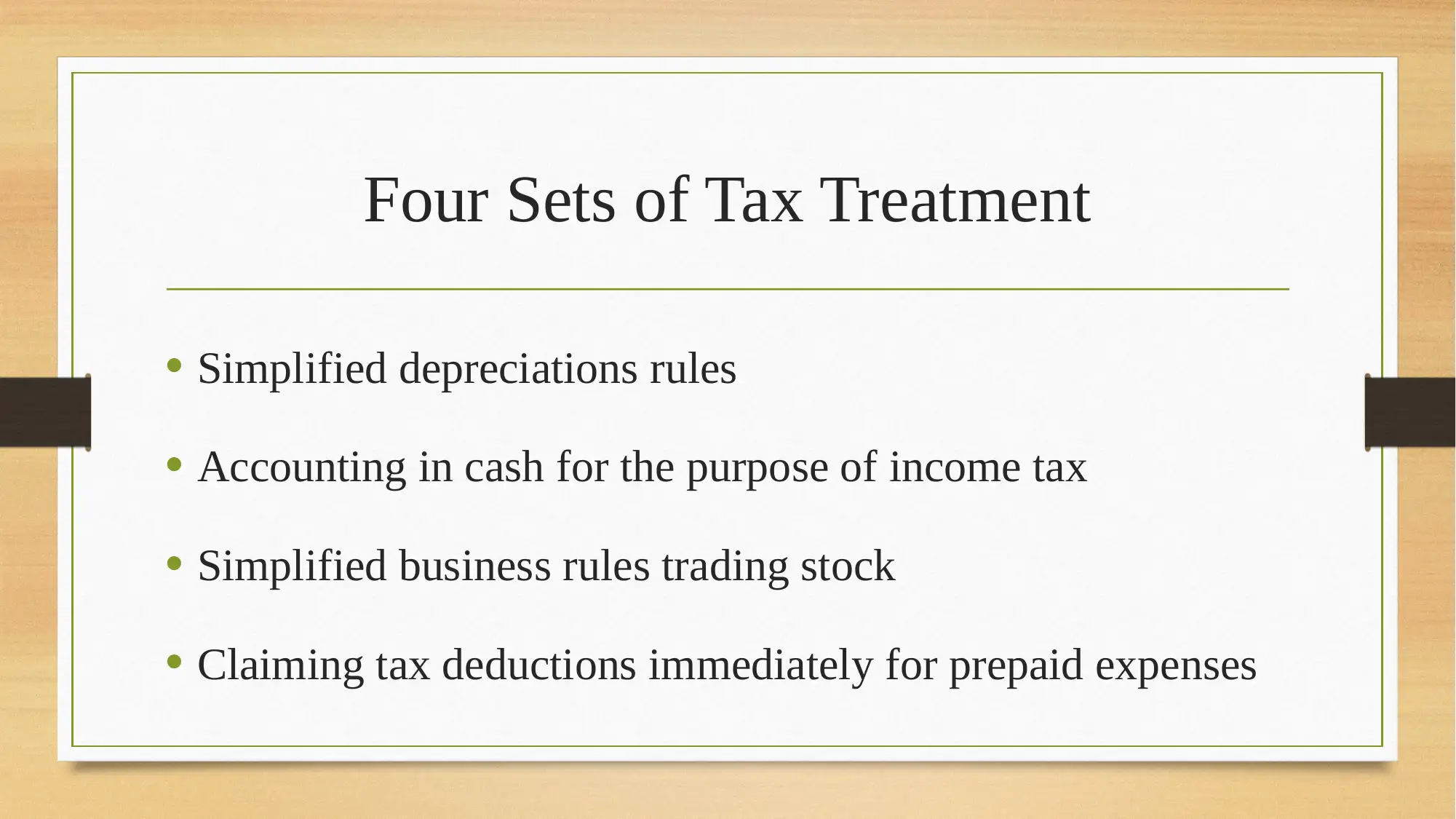

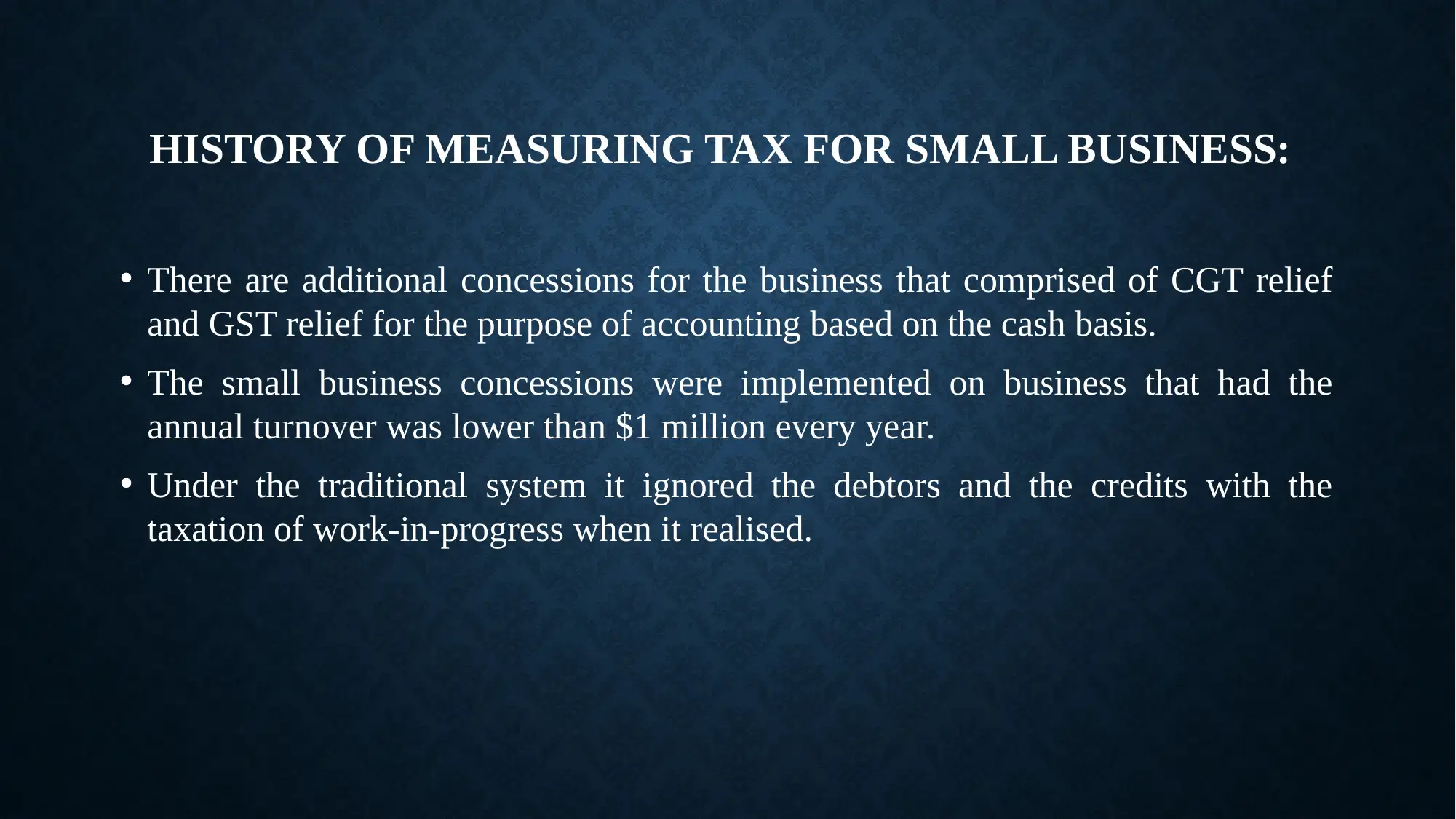

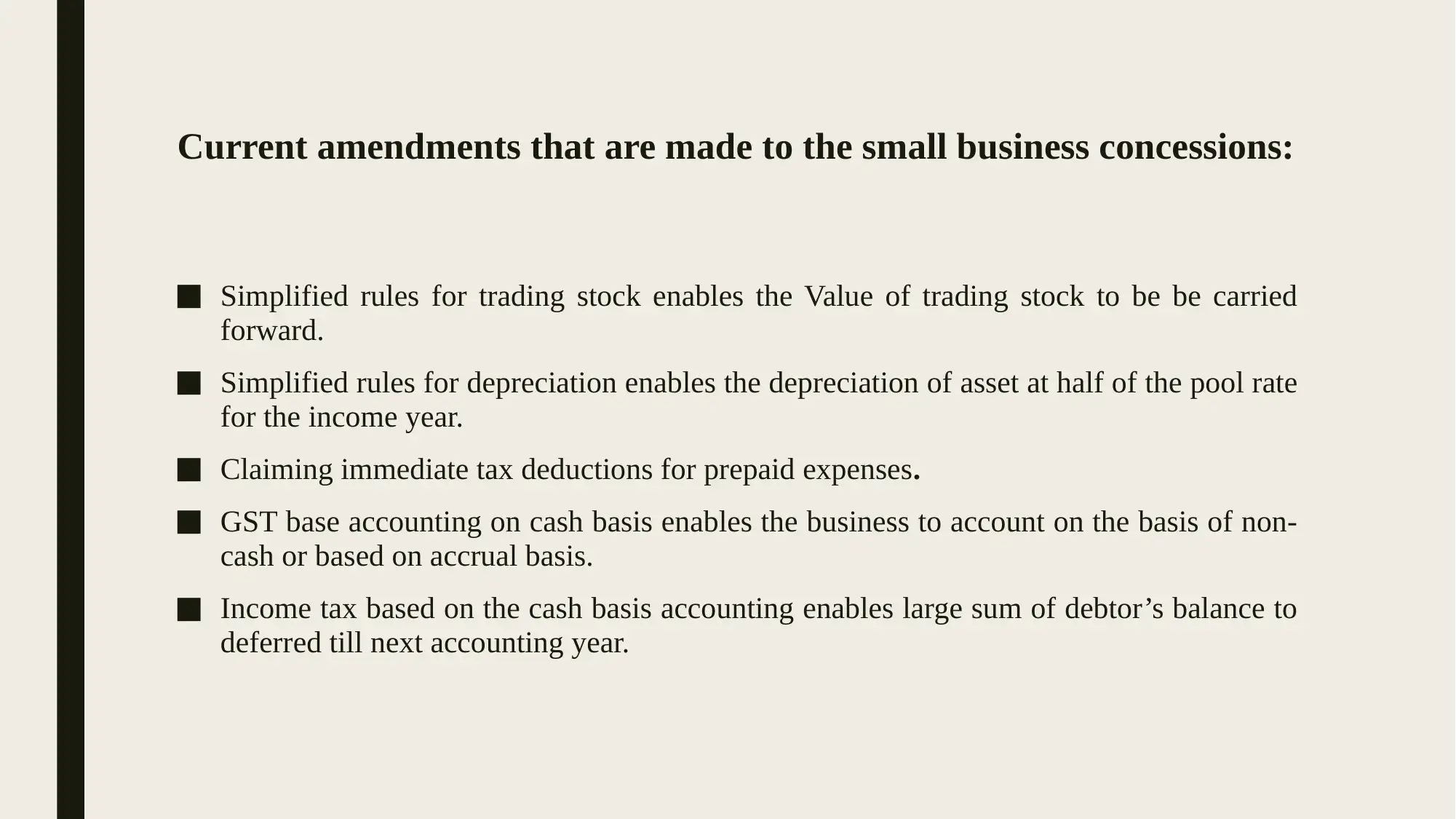

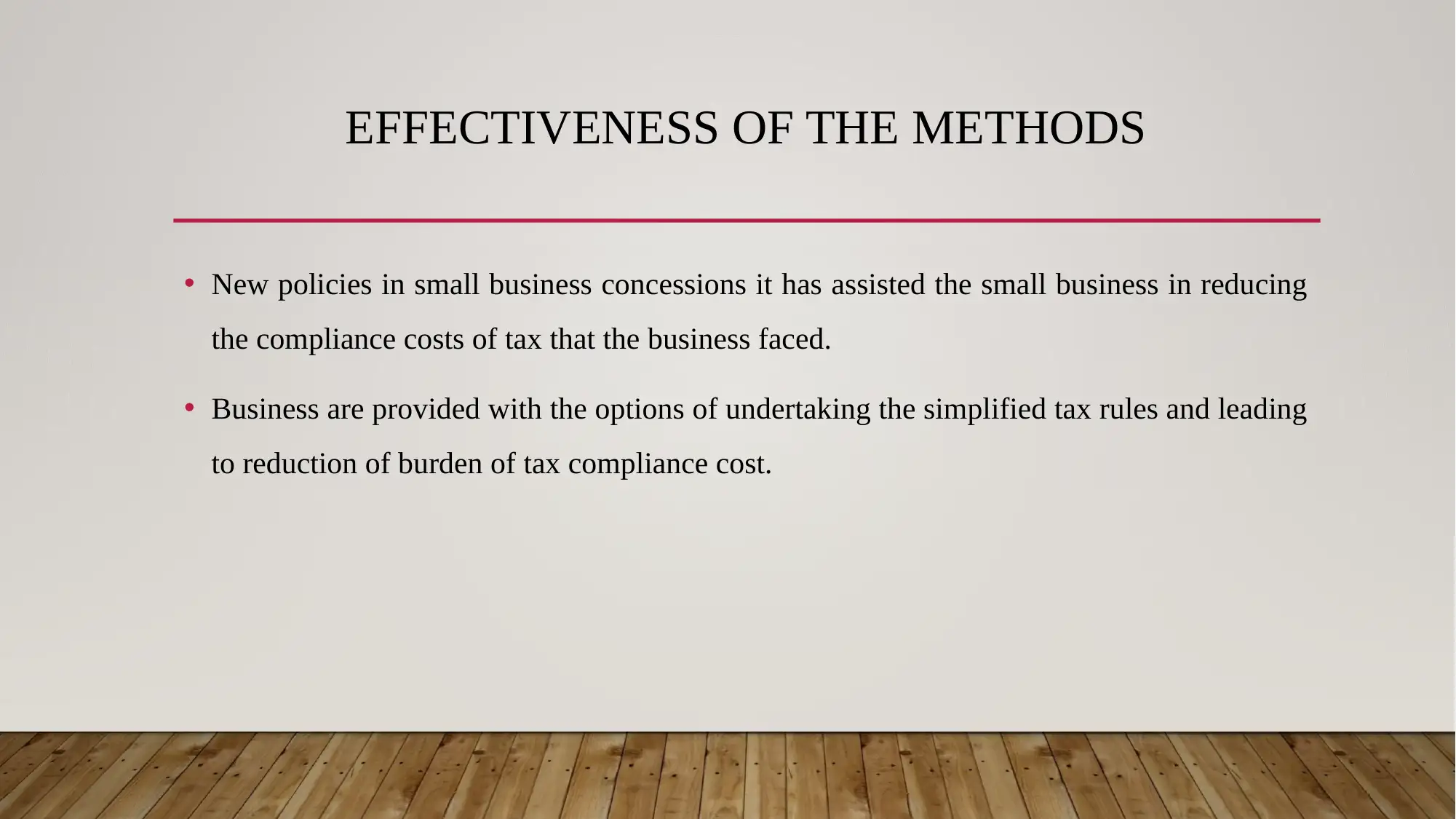

This report provides an overview of small business tax concessions in Australia. It discusses the importance of small businesses and the revenue they generate. The report outlines different types of concessions, including those related to active assets, retirement, and rollovers, as well as the criteria for eligibility. It explores the objectives of these concessions, such as simplifying tax measures and reducing compliance costs. The report also covers the history of small business tax, current amendments, and the effectiveness of new policies like simplified depreciation rules, immediate tax deductions for prepaid expenses, and GST and income tax accounting based on cash basis. Recommendations are made to improve eligibility criteria and aggregate turnover. The conclusion emphasizes the increasing adoption of these concessions and their positive impact on reducing tax compliance costs. References to relevant literature are also included.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.