Taxation Law Assignment: Analysis of Tax Deductions and GST

VerifiedAdded on 2020/04/01

|15

|1793

|186

Homework Assignment

AI Summary

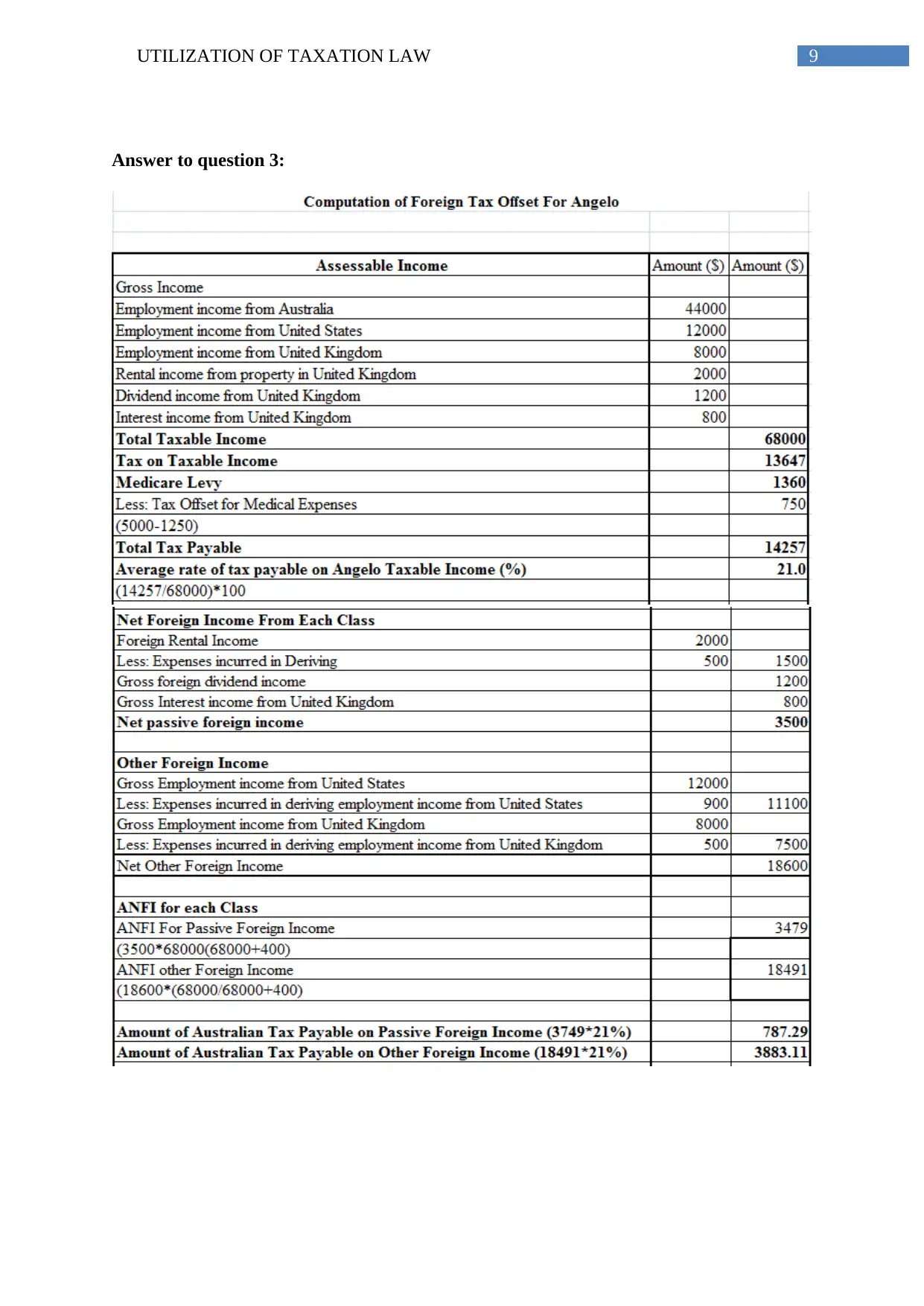

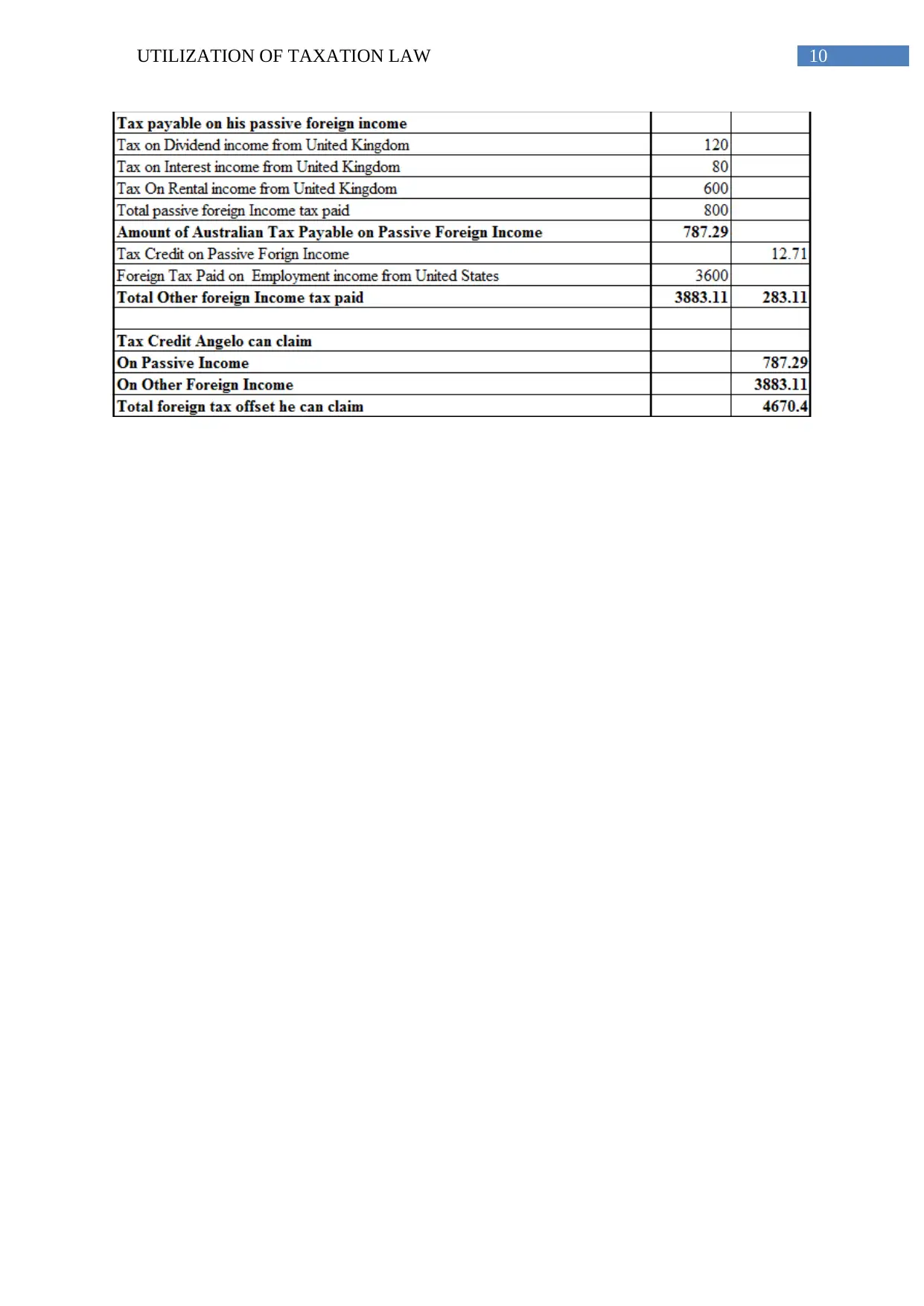

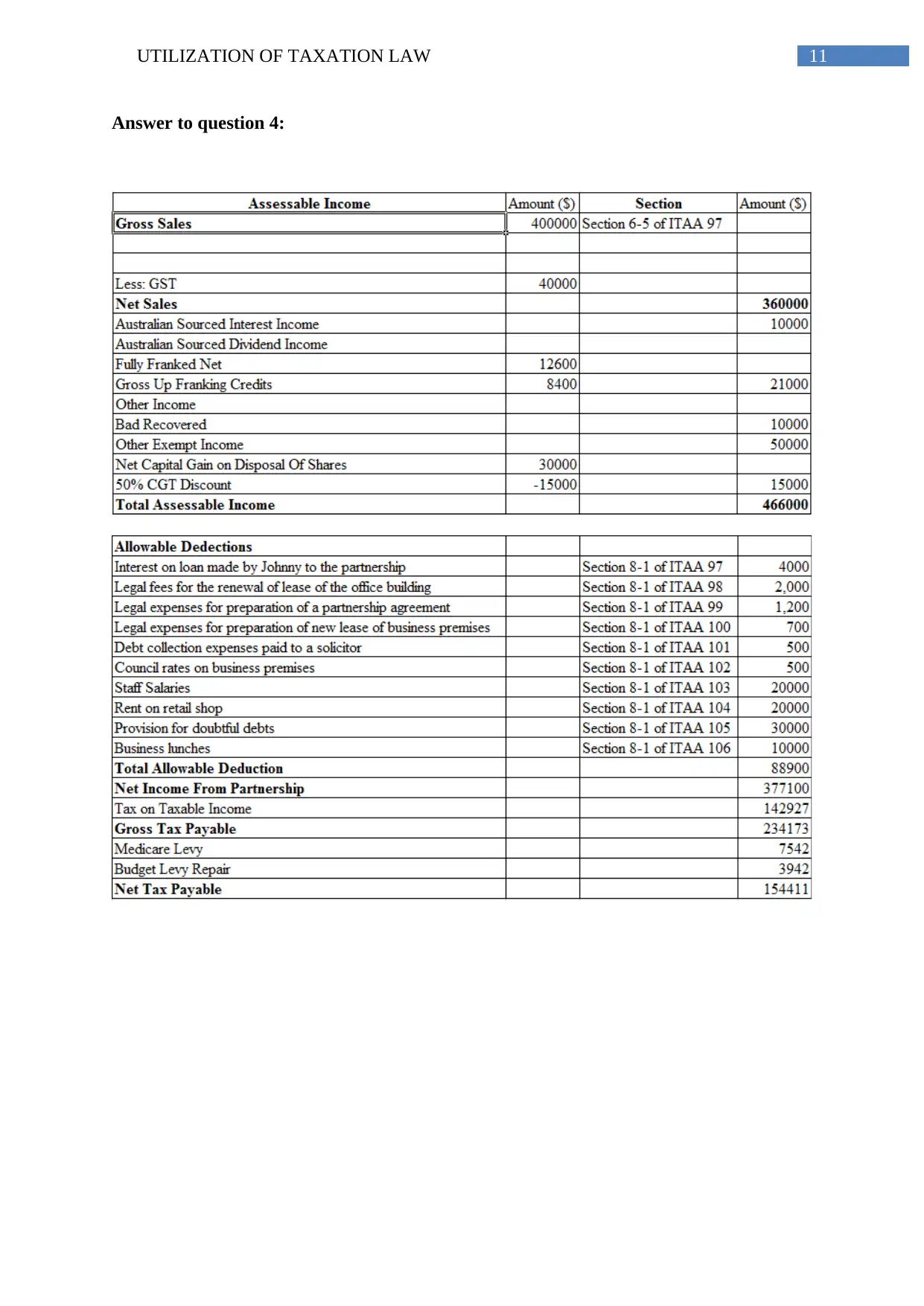

This assignment addresses several key issues in taxation law, providing detailed answers to four questions. The first question examines the deductibility of various expenses, including the cost of moving machinery, revaluation of assets for insurance purposes, legal expenses related to winding up a business, and legal expenditure for business operations. The second question focuses on the input tax credit for advertising expenditure under the GST Act, specifically concerning Big Bank Ltd. The assignment utilizes relevant sections of the Income Tax Assessment Act 1997 and the GST Act 1999, along with case law such as British Insulated & Helsby Cables and Ronpibon Tin NL v. FC of T, to support its arguments. The analysis considers capital expenditure, business operations, and creditable acquisitions. The assignment concludes with a comprehensive list of references, citing legal databases, textbooks, and journal articles related to taxation law.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.