Tax Law Exam Practice Questions and Solutions - Taxation Law Exam

VerifiedAdded on 2022/11/25

|8

|1128

|394

Homework Assignment

AI Summary

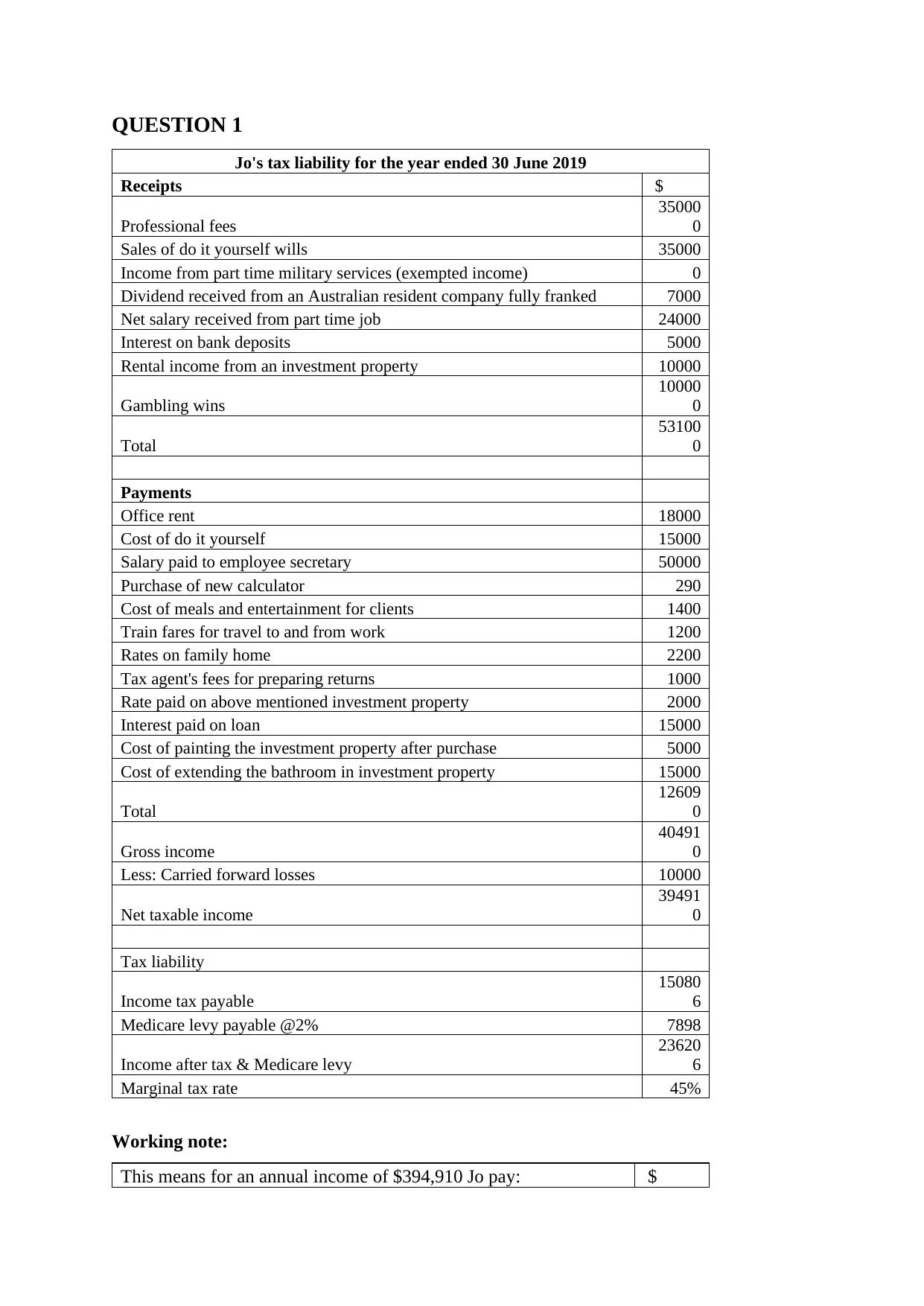

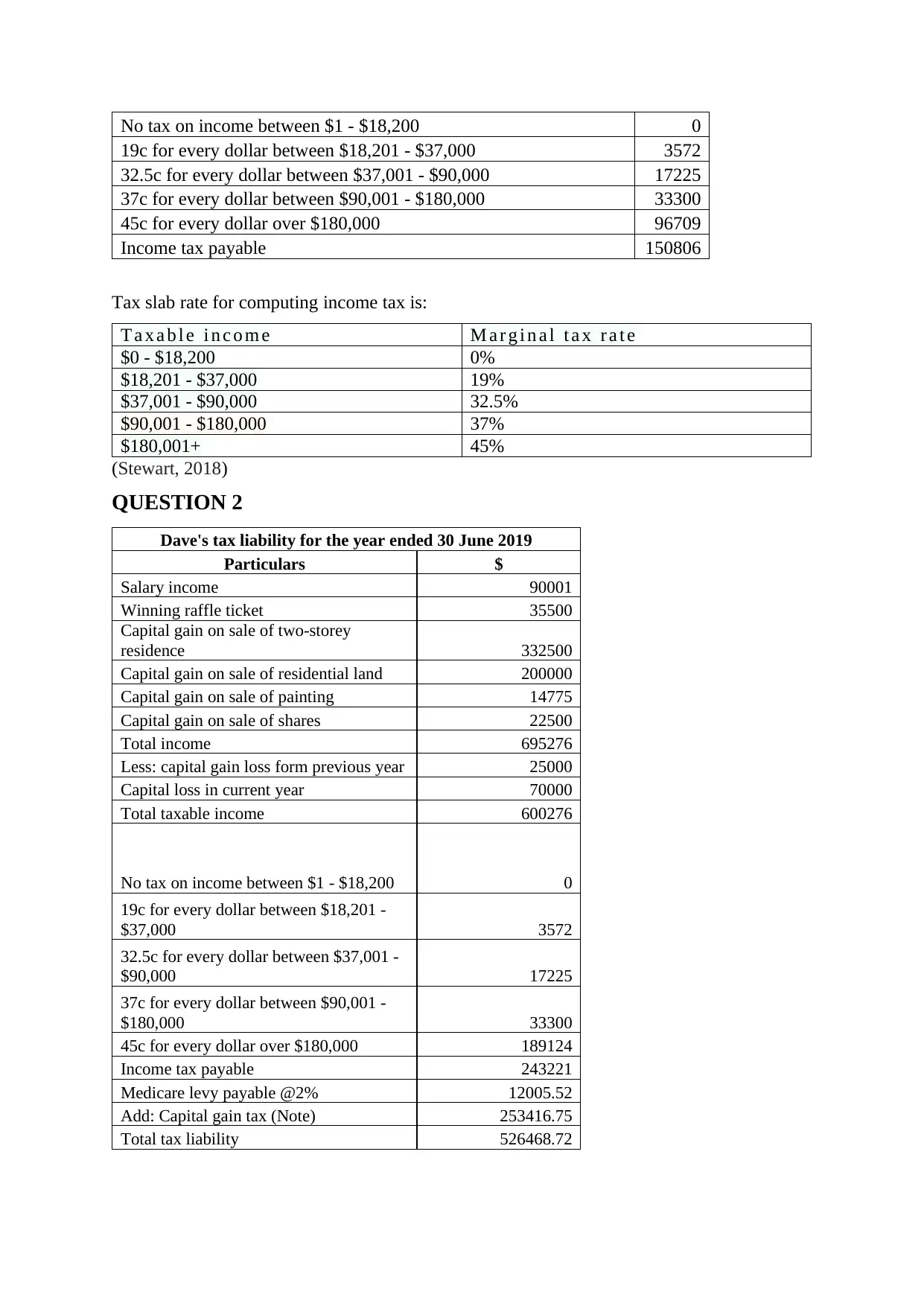

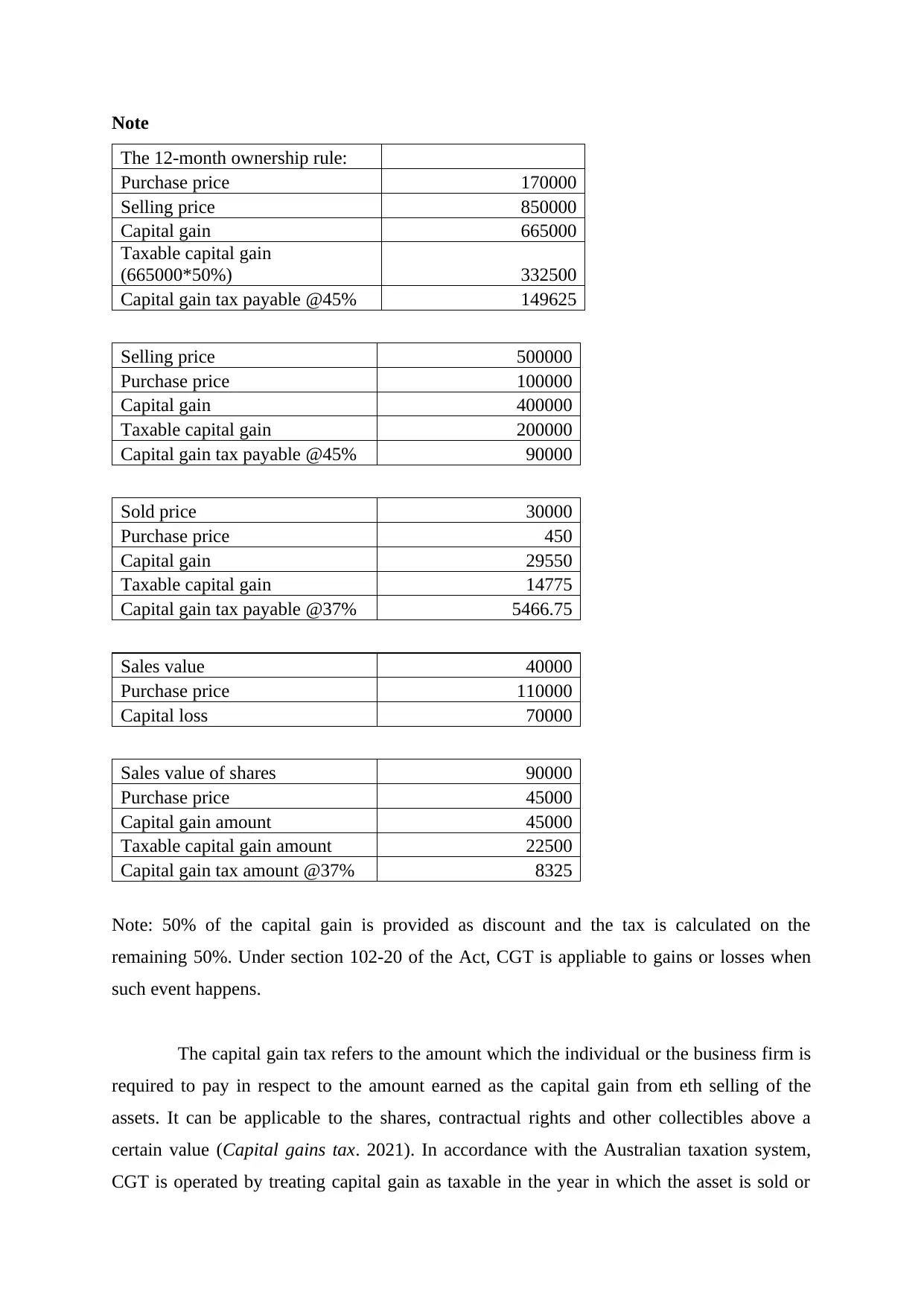

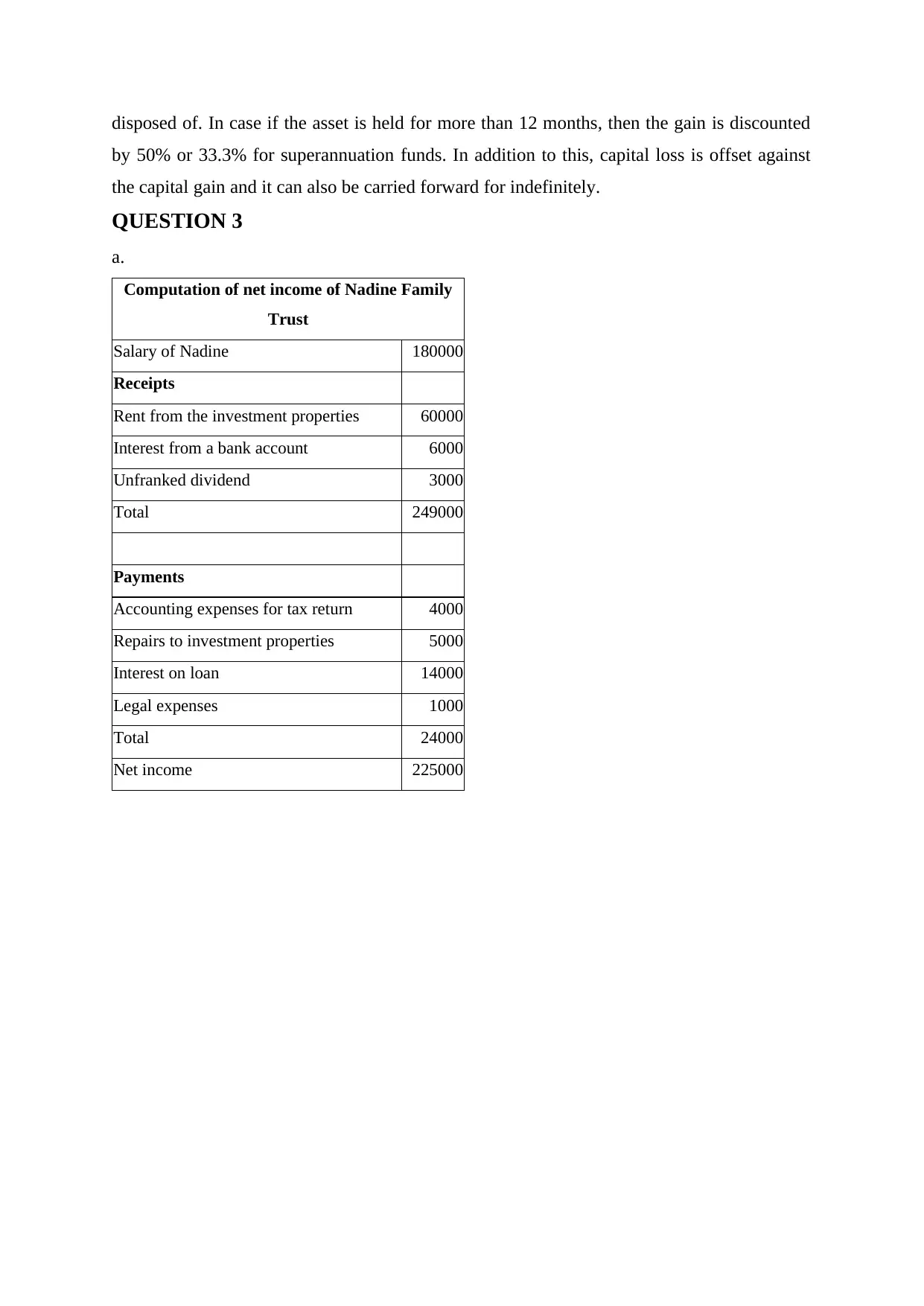

This document presents a set of practice questions and detailed solutions designed to aid in the preparation for a Taxation Law exam. The content covers the calculation of tax liabilities for individuals, including the computation of taxable income, income tax payable, and Medicare levy. The first question focuses on Jo's tax liability for the year ended 30 June 2019, involving various income sources and deductions. The second question addresses Dave's tax liability, incorporating capital gains from the sale of assets and capital loss. The solutions include working notes that explain the tax slab rates and marginal tax rates. The third question delves into the computation of net income for the Nadine Family Trust and discusses the distribution of distributable net income to beneficiaries to minimize tax liability. The assignment concludes with a reference list.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.