Tax Law Assignment: Fringe Benefits Tax and Capital Gains Tax Analysis

VerifiedAdded on 2023/03/20

|8

|2539

|29

Homework Assignment

AI Summary

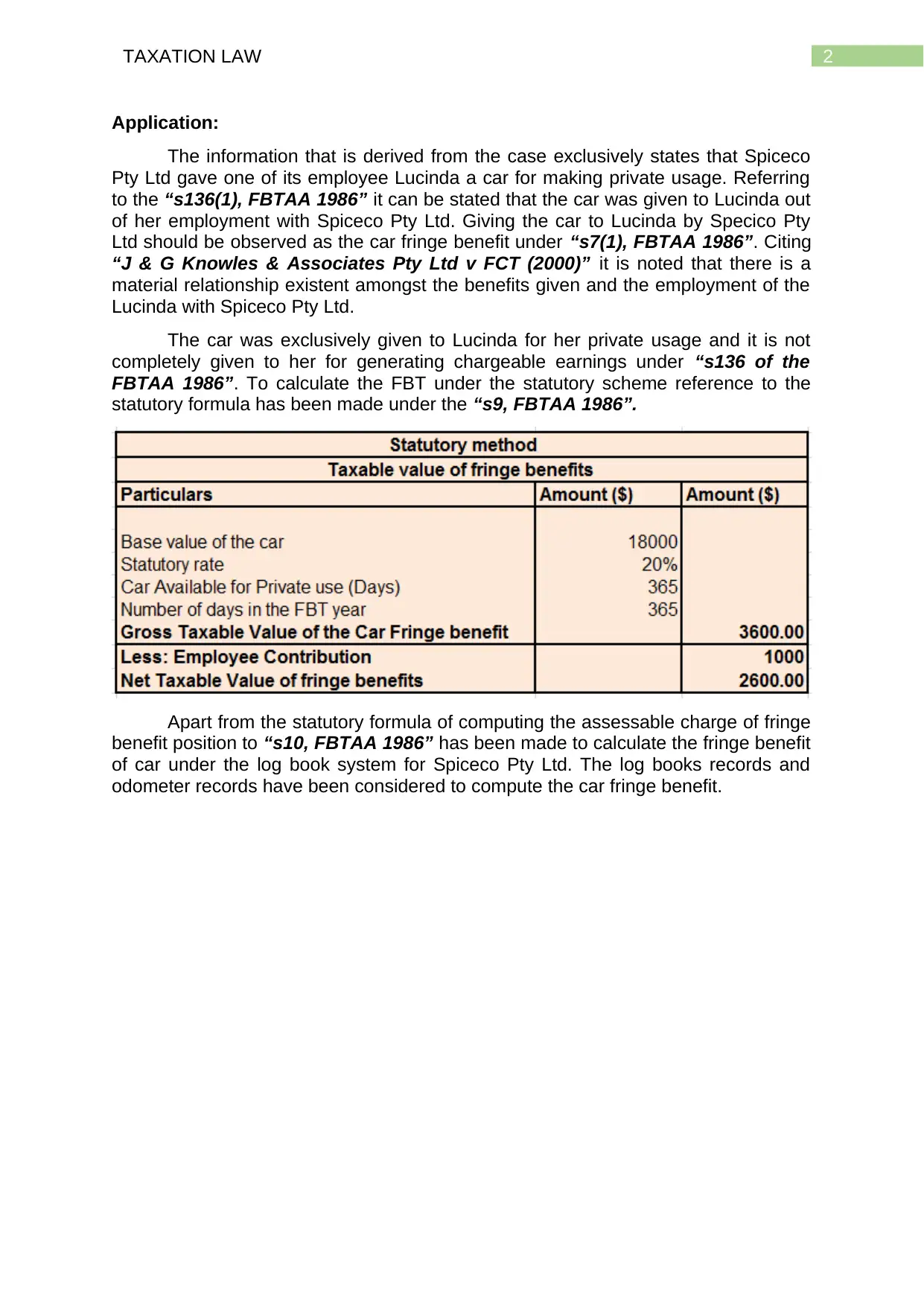

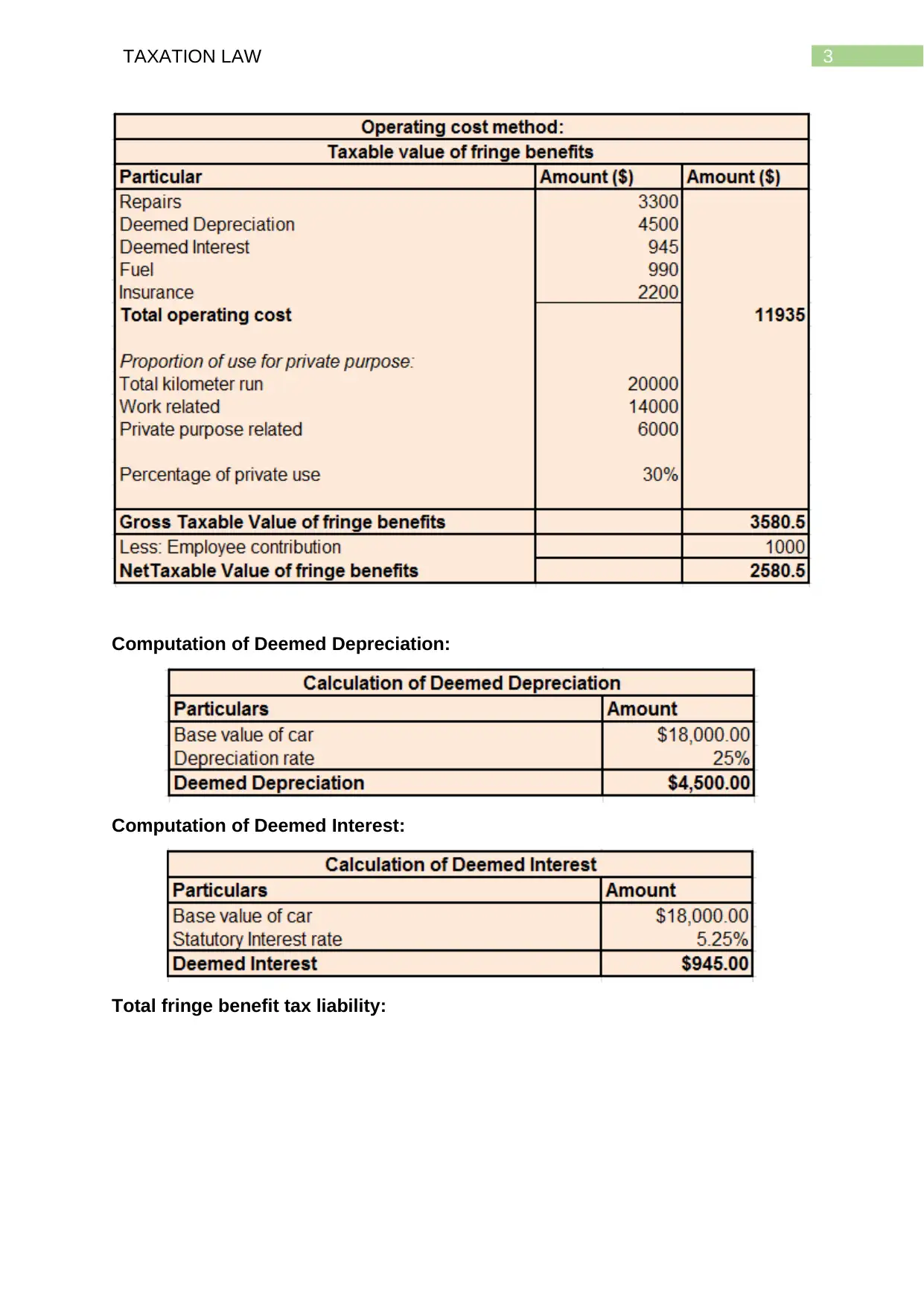

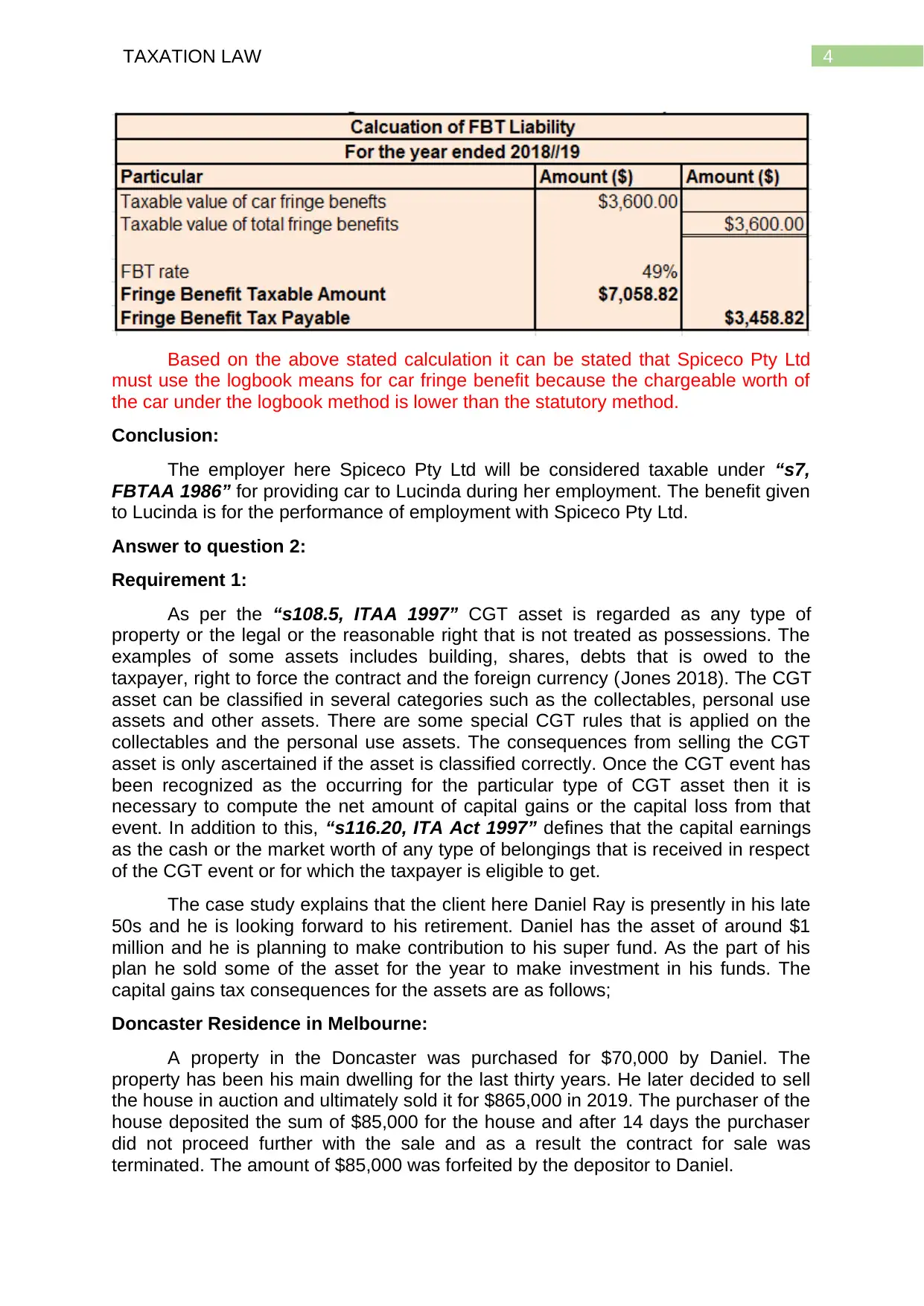

This document presents a comprehensive tax law assignment addressing two key areas: fringe benefits tax (FBT) and capital gains tax (CGT). The first part of the assignment examines the tax implications for Spiceco Pty Ltd, focusing on the provision of a car to an employee, Lucinda, and calculating the FBT liability using both the statutory and logbook methods. The analysis considers relevant legislation, including the FBTAA 1986, and case law to determine the appropriate tax treatment. The second part of the assignment deals with capital gains tax (CGT) for Daniel Ray, analyzing the CGT consequences of selling various assets, including a Doncaster residence, an artistic painting, a luxury yacht, and shares in BHP and AZJ. The analysis covers CGT events, the classification of assets (collectables, personal use assets), and the offsetting of capital losses against capital gains. The assignment concludes with recommendations for Daniel regarding investing capital gains and the treatment of capital losses, providing a detailed overview of the relevant tax principles and their application to the given scenarios.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.