Taxation Law: Analysis of FBT and CGT for Income Year 2019

VerifiedAdded on 2023/03/23

|11

|2271

|73

Homework Assignment

AI Summary

This assignment provides a detailed analysis of Fringe Benefit Tax (FBT) and Capital Gains Tax (CGT) within the context of taxation law. It includes the computation of FBT liability for Spiceco Pty Ltd, considering the car fringe benefit provided to Lucinda, and explores different methods for calculating FBT. The assignment also determines the net CGT gain for Daniel Ray in the 2019 income year, addressing the treatment of CGT gains and losses, and includes a discussion on CGT events, assets, and exemptions, such as main residence and collectibles. The document concludes with detailed calculations and conclusions regarding both FBT and CGT scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Author Note

Taxation Law

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Question 1

Issue

The computation of the Fringe Benefit Tax liability pertaining to Spiceco Pty Ltd for the

car they have provided to Lucinda for being used in personal purposes in the FBT year

2018/19. Whether there are other methods available for calculating the FBT for the year

2018/19. Which method will be more apt for the assumption that Spiceco has been aiming to

minimise their FBT liability.

Rule

The word fringe benefit has been defined u/s 136 of the FBTAA 86. Any benefit that an

employer allows towards an employee employed with him or any person associated with him

or even a third party who needs to be extended with such benefit under an agreement between

the employer and employee. However this benefit extended needs to be used by the employee

or any other such person for a personal purpose. This may include any form of right as well

as interest with respect to a personal or real property. A facility or service may also be

extended by an employer under this system. The liability of paying the tax against such

benefit lies with the employer. The employer will be imposed with the tax liability for search

a benefit provided and it needs to be included in the assessable income of the employee. In

this context an employer include present, future or even past employer.

When an employer extend towards and employee employed with him with a car that is to

be used by the employee for serving his personal purpose is required to be treated as a car

fringe benefit u/s 7 of the FBTAA 86 and will be assessable in the hands of the employee in a

certain FBT year.

The FBTAA 86 provides for two methods for the purpose of computing the FBT liability.

These are the Statutory Method that has been provided under section 9(1) of the FBTAA 86.

Question 1

Issue

The computation of the Fringe Benefit Tax liability pertaining to Spiceco Pty Ltd for the

car they have provided to Lucinda for being used in personal purposes in the FBT year

2018/19. Whether there are other methods available for calculating the FBT for the year

2018/19. Which method will be more apt for the assumption that Spiceco has been aiming to

minimise their FBT liability.

Rule

The word fringe benefit has been defined u/s 136 of the FBTAA 86. Any benefit that an

employer allows towards an employee employed with him or any person associated with him

or even a third party who needs to be extended with such benefit under an agreement between

the employer and employee. However this benefit extended needs to be used by the employee

or any other such person for a personal purpose. This may include any form of right as well

as interest with respect to a personal or real property. A facility or service may also be

extended by an employer under this system. The liability of paying the tax against such

benefit lies with the employer. The employer will be imposed with the tax liability for search

a benefit provided and it needs to be included in the assessable income of the employee. In

this context an employer include present, future or even past employer.

When an employer extend towards and employee employed with him with a car that is to

be used by the employee for serving his personal purpose is required to be treated as a car

fringe benefit u/s 7 of the FBTAA 86 and will be assessable in the hands of the employee in a

certain FBT year.

The FBTAA 86 provides for two methods for the purpose of computing the FBT liability.

These are the Statutory Method that has been provided under section 9(1) of the FBTAA 86.

2TAXATION LAW

[0.2 * BV * (n/ tn)] - A

BV = Base value of the car

n = no. of days during the income tax year for which the car fringe benefit was provided

by the person providing

tn = no. of days in that income tax year

C = contribution of the recipient

The operating cost method that has been provided under section 10(2) of the FBTAA 86.

[C * ( 100% - BP)] – R

C = operating cost during the period of holding, which includes maintenance, insurance,

registration and fuel.

BP = business percentage

C = contribution of the recipient.

Application

In the present instance, a car has been extended to Lucinda on 1st April 2018 by Spiceco

Pty Ltd by virtue of her employment with them for the purpose of being used in a personal

capacity and for personal purposes. This can be conceived as a fringe benefit that has been

extended towards Lucinda by Spiceco Pty Ltd as can be made evident u/s 136 of the FBTAA

86. On the other hand, the subject matter of the benefit is a car that has been extended

towards Lucinda for being used for personal purposes. Hence, this need to be treated as a car

fringe benefit and will be taxable in the hands of Spiceco Pty Ltd u/s 7 of the FBTAA 86.

The car that has been extended, has a cost of $18000, towards which Lucinda has made a

payment of $1000. There has been further expenses of $3300 for repairs, fuel for $990 as

[0.2 * BV * (n/ tn)] - A

BV = Base value of the car

n = no. of days during the income tax year for which the car fringe benefit was provided

by the person providing

tn = no. of days in that income tax year

C = contribution of the recipient

The operating cost method that has been provided under section 10(2) of the FBTAA 86.

[C * ( 100% - BP)] – R

C = operating cost during the period of holding, which includes maintenance, insurance,

registration and fuel.

BP = business percentage

C = contribution of the recipient.

Application

In the present instance, a car has been extended to Lucinda on 1st April 2018 by Spiceco

Pty Ltd by virtue of her employment with them for the purpose of being used in a personal

capacity and for personal purposes. This can be conceived as a fringe benefit that has been

extended towards Lucinda by Spiceco Pty Ltd as can be made evident u/s 136 of the FBTAA

86. On the other hand, the subject matter of the benefit is a car that has been extended

towards Lucinda for being used for personal purposes. Hence, this need to be treated as a car

fringe benefit and will be taxable in the hands of Spiceco Pty Ltd u/s 7 of the FBTAA 86.

The car that has been extended, has a cost of $18000, towards which Lucinda has made a

payment of $1000. There has been further expenses of $3300 for repairs, fuel for $990 as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

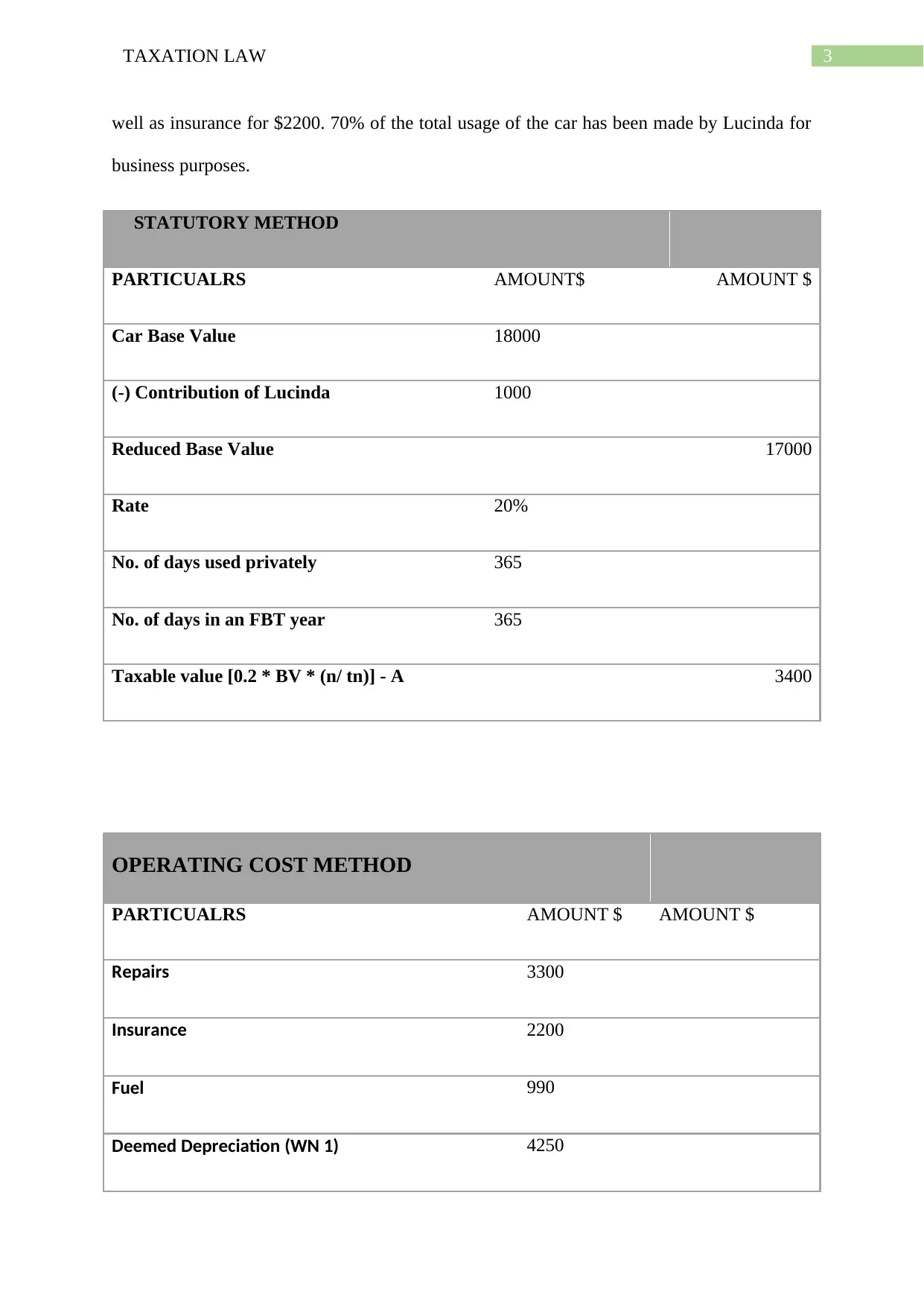

well as insurance for $2200. 70% of the total usage of the car has been made by Lucinda for

business purposes.

STATUTORY METHOD

PARTICUALRS AMOUNT$ AMOUNT $

Car Base Value 18000

(-) Contribution of Lucinda 1000

Reduced Base Value 17000

Rate 20%

No. of days used privately 365

No. of days in an FBT year 365

Taxable value [0.2 * BV * (n/ tn)] - A 3400

OPERATING COST METHOD

PARTICUALRS AMOUNT $ AMOUNT $

Repairs 3300

Insurance 2200

Fuel 990

Deemed Depreciation (WN 1) 4250

well as insurance for $2200. 70% of the total usage of the car has been made by Lucinda for

business purposes.

STATUTORY METHOD

PARTICUALRS AMOUNT$ AMOUNT $

Car Base Value 18000

(-) Contribution of Lucinda 1000

Reduced Base Value 17000

Rate 20%

No. of days used privately 365

No. of days in an FBT year 365

Taxable value [0.2 * BV * (n/ tn)] - A 3400

OPERATING COST METHOD

PARTICUALRS AMOUNT $ AMOUNT $

Repairs 3300

Insurance 2200

Fuel 990

Deemed Depreciation (WN 1) 4250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

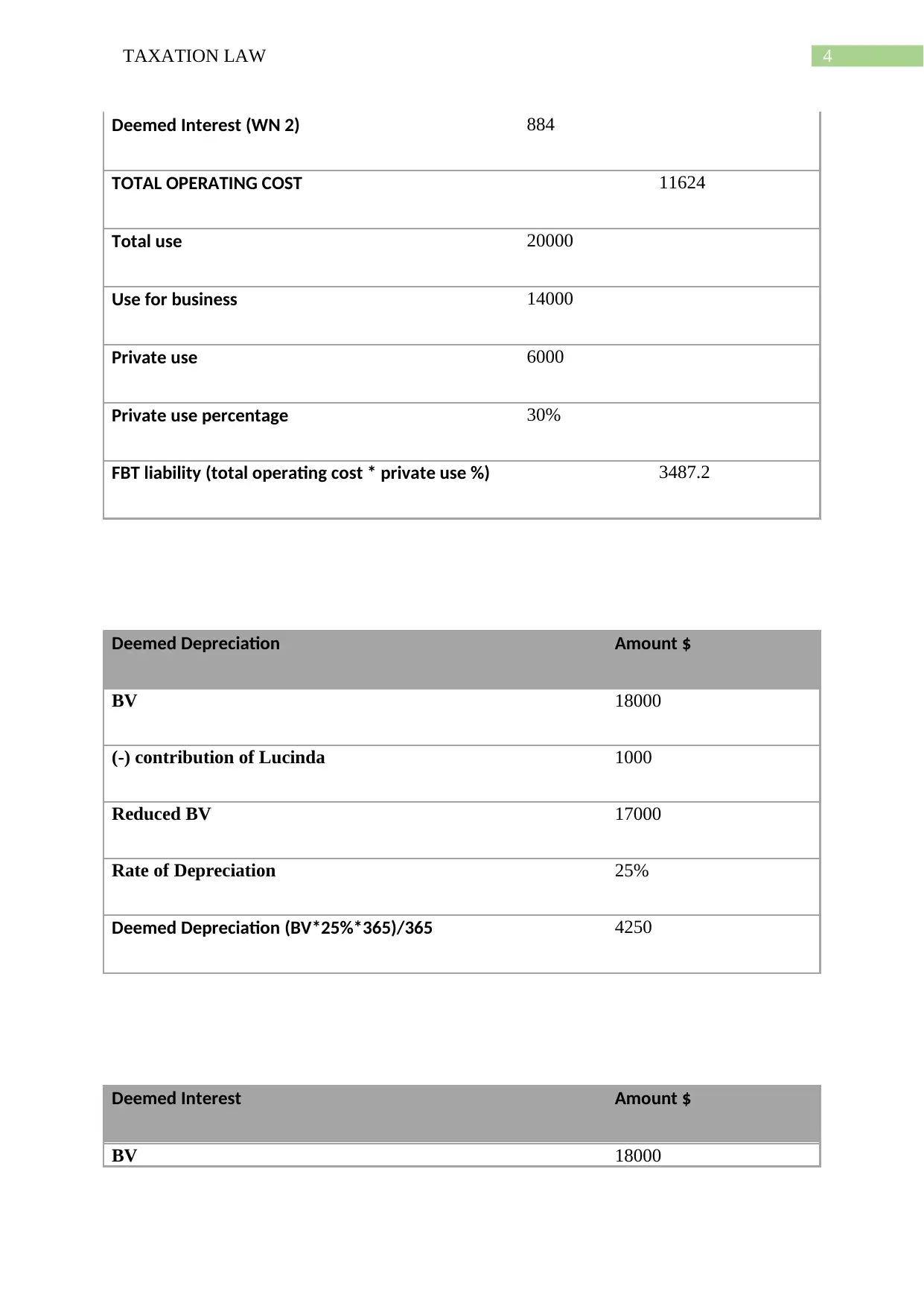

Deemed Interest (WN 2) 884

TOTAL OPERATING COST 11624

Total use 20000

Use for business 14000

Private use 6000

Private use percentage 30%

FBT liability (total operating cost * private use %) 3487.2

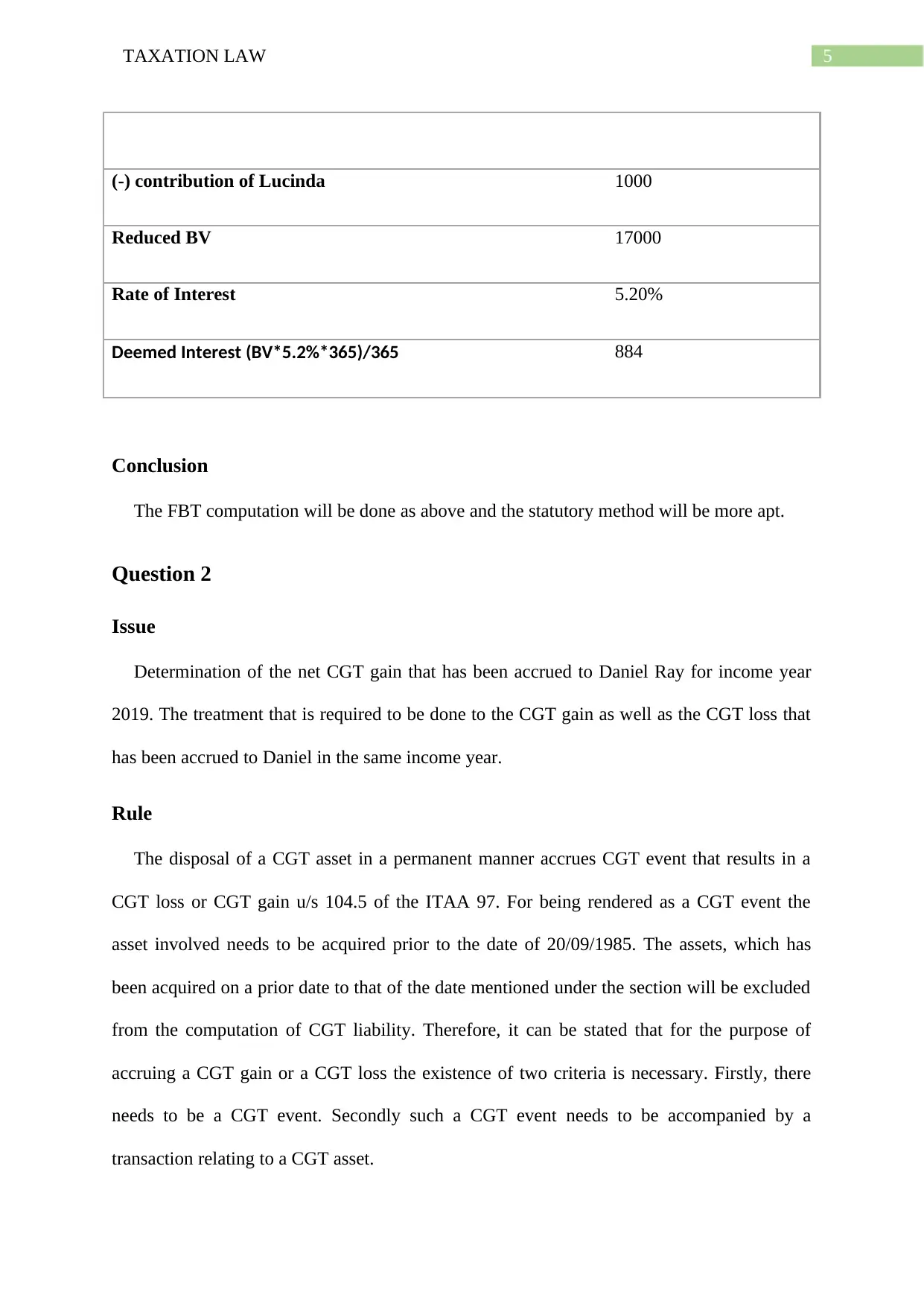

Deemed Depreciation Amount $

BV 18000

(-) contribution of Lucinda 1000

Reduced BV 17000

Rate of Depreciation 25%

Deemed Depreciation (BV*25%*365)/365 4250

Deemed Interest Amount $

BV 18000

Deemed Interest (WN 2) 884

TOTAL OPERATING COST 11624

Total use 20000

Use for business 14000

Private use 6000

Private use percentage 30%

FBT liability (total operating cost * private use %) 3487.2

Deemed Depreciation Amount $

BV 18000

(-) contribution of Lucinda 1000

Reduced BV 17000

Rate of Depreciation 25%

Deemed Depreciation (BV*25%*365)/365 4250

Deemed Interest Amount $

BV 18000

5TAXATION LAW

(-) contribution of Lucinda 1000

Reduced BV 17000

Rate of Interest 5.20%

Deemed Interest (BV*5.2%*365)/365 884

Conclusion

The FBT computation will be done as above and the statutory method will be more apt.

Question 2

Issue

Determination of the net CGT gain that has been accrued to Daniel Ray for income year

2019. The treatment that is required to be done to the CGT gain as well as the CGT loss that

has been accrued to Daniel in the same income year.

Rule

The disposal of a CGT asset in a permanent manner accrues CGT event that results in a

CGT loss or CGT gain u/s 104.5 of the ITAA 97. For being rendered as a CGT event the

asset involved needs to be acquired prior to the date of 20/09/1985. The assets, which has

been acquired on a prior date to that of the date mentioned under the section will be excluded

from the computation of CGT liability. Therefore, it can be stated that for the purpose of

accruing a CGT gain or a CGT loss the existence of two criteria is necessary. Firstly, there

needs to be a CGT event. Secondly such a CGT event needs to be accompanied by a

transaction relating to a CGT asset.

(-) contribution of Lucinda 1000

Reduced BV 17000

Rate of Interest 5.20%

Deemed Interest (BV*5.2%*365)/365 884

Conclusion

The FBT computation will be done as above and the statutory method will be more apt.

Question 2

Issue

Determination of the net CGT gain that has been accrued to Daniel Ray for income year

2019. The treatment that is required to be done to the CGT gain as well as the CGT loss that

has been accrued to Daniel in the same income year.

Rule

The disposal of a CGT asset in a permanent manner accrues CGT event that results in a

CGT loss or CGT gain u/s 104.5 of the ITAA 97. For being rendered as a CGT event the

asset involved needs to be acquired prior to the date of 20/09/1985. The assets, which has

been acquired on a prior date to that of the date mentioned under the section will be excluded

from the computation of CGT liability. Therefore, it can be stated that for the purpose of

accruing a CGT gain or a CGT loss the existence of two criteria is necessary. Firstly, there

needs to be a CGT event. Secondly such a CGT event needs to be accompanied by a

transaction relating to a CGT asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

When a CGT asset is disposed off permanently in the form of sale, it is generally brought

under the A1 category of CGT event u/s 104.10 of the ITAA 97. In case of such a category of

CGT event the lower of the cost proceed or the cost base is required to be subtracted from the

other one for calculating the CGT gain or CGT loss accrued. It is evident from this section

that for the incurring a CGT gain or a CGT loss, the presence of a GTT event is necessary.

For the purpose of occurrence of such a CGT event A1 category, the formation of a contract,

which effects the transfer of ownership or the actual transfer of ownership is needed to be

established or effected for the purpose of bringing an event under the purview of this section.

The proceeds from the sale of a residential property or a property being used for

residential purposes is required to be considered as an exemption while computing a CGT

liability of a person u/s 118.10 of the ITAA 97.

Collectible implies any commodity that has been owned and possessed by a person for

being used personally or for the purpose of personal enjoyment and is construed to be a CGT

asset as per section 108.10 of the ITAA 97. These commodities may include artwork,

jewellery, antique objects and other objects of similar kind.

Collectible is generally treated as a CGT asset if the same can be proved worth more than

$500. Any collectible which is worth less than the prescribed amount will be treated as an

exemption from being permitted as a component in the CGT computation u/s 110.10 of the

ITAA 97.

As per section 108.5 of the ITAA 97, an equitable right or a legal right can also be treated

as or CGT asset. This form of asset include shares, buildings, foreign currency, contractual

rights, recoverable debts and options. Any such asset when disposed off permanently will

give rise to A1 category CGT event.

When a CGT asset is disposed off permanently in the form of sale, it is generally brought

under the A1 category of CGT event u/s 104.10 of the ITAA 97. In case of such a category of

CGT event the lower of the cost proceed or the cost base is required to be subtracted from the

other one for calculating the CGT gain or CGT loss accrued. It is evident from this section

that for the incurring a CGT gain or a CGT loss, the presence of a GTT event is necessary.

For the purpose of occurrence of such a CGT event A1 category, the formation of a contract,

which effects the transfer of ownership or the actual transfer of ownership is needed to be

established or effected for the purpose of bringing an event under the purview of this section.

The proceeds from the sale of a residential property or a property being used for

residential purposes is required to be considered as an exemption while computing a CGT

liability of a person u/s 118.10 of the ITAA 97.

Collectible implies any commodity that has been owned and possessed by a person for

being used personally or for the purpose of personal enjoyment and is construed to be a CGT

asset as per section 108.10 of the ITAA 97. These commodities may include artwork,

jewellery, antique objects and other objects of similar kind.

Collectible is generally treated as a CGT asset if the same can be proved worth more than

$500. Any collectible which is worth less than the prescribed amount will be treated as an

exemption from being permitted as a component in the CGT computation u/s 110.10 of the

ITAA 97.

As per section 108.5 of the ITAA 97, an equitable right or a legal right can also be treated

as or CGT asset. This form of asset include shares, buildings, foreign currency, contractual

rights, recoverable debts and options. Any such asset when disposed off permanently will

give rise to A1 category CGT event.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Shares of treated as CGT assets and proceeds of the sale of such shares is a component

while computing the CGT liability u/s 110.55 of the ITAA 97. However, if the cost base has

been reduced by virtue of any loan availed or any interest thereto accrued is required to be

excluded with the third element that is the owning cost while computing the CGT liability.

Application

In the present case, the sale of the house by Daniel, which has been used by him as a main

residence for 30 years will required to be treated as an exemption. This is because The

proceeds from the sale of a residential property or a property being used for residential

purposes is required to be considered as an exemption while computing a CGT liability of a

person u/s 118.10 of the ITAA 97. However, this cannot be treated as a CGT event in the first

place as there has not been any formation of a contract that effects the actual transfer of the

property. After 14 days of that proposed sale, the buyer has decided to terminate the contract

of sale. This needs to be excluded from the CGT computation.

The sale of the painting by Margaret Preston earning a proceed of $125000 actually being

acquired for a price of 15000 dollars on the date of 20/09/1985 is required to be treated as a

CGT event, as it has been acquired on the prescribed date and not prior to the prescribed date.

This is because for being rendered as a CGT event the asset involved needs to be acquired

prior to the date of 20/09/1985. The assets, which has been acquired on a prior date to that of

the date mentioned under the section will be excluded from the computation of CGT liability.

A discount of 50% will also allowed under div 115. CGT gain accrued will be $(125000 –

15000) * 50% = $55000

The sale of the luxury yacht for a price of $60,000, which has actually been acquired for

$110000 is required to be treated as a CGT loss. This is because, in this case, the cost proceed

that has been earned with the transaction was less than the cost base that is the acquisition

cost of the yacht. CGT loss that accrued $110000 - $60000 = $50000. CGT loss on personal

assets are disregarded.

Shares of treated as CGT assets and proceeds of the sale of such shares is a component

while computing the CGT liability u/s 110.55 of the ITAA 97. However, if the cost base has

been reduced by virtue of any loan availed or any interest thereto accrued is required to be

excluded with the third element that is the owning cost while computing the CGT liability.

Application

In the present case, the sale of the house by Daniel, which has been used by him as a main

residence for 30 years will required to be treated as an exemption. This is because The

proceeds from the sale of a residential property or a property being used for residential

purposes is required to be considered as an exemption while computing a CGT liability of a

person u/s 118.10 of the ITAA 97. However, this cannot be treated as a CGT event in the first

place as there has not been any formation of a contract that effects the actual transfer of the

property. After 14 days of that proposed sale, the buyer has decided to terminate the contract

of sale. This needs to be excluded from the CGT computation.

The sale of the painting by Margaret Preston earning a proceed of $125000 actually being

acquired for a price of 15000 dollars on the date of 20/09/1985 is required to be treated as a

CGT event, as it has been acquired on the prescribed date and not prior to the prescribed date.

This is because for being rendered as a CGT event the asset involved needs to be acquired

prior to the date of 20/09/1985. The assets, which has been acquired on a prior date to that of

the date mentioned under the section will be excluded from the computation of CGT liability.

A discount of 50% will also allowed under div 115. CGT gain accrued will be $(125000 –

15000) * 50% = $55000

The sale of the luxury yacht for a price of $60,000, which has actually been acquired for

$110000 is required to be treated as a CGT loss. This is because, in this case, the cost proceed

that has been earned with the transaction was less than the cost base that is the acquisition

cost of the yacht. CGT loss that accrued $110000 - $60000 = $50000. CGT loss on personal

assets are disregarded.

8TAXATION LAW

In this case the shares that has been acquired by Daniel was worth $75,000 and acquisition

has been affected on 10th January of the year 2019. The shares has been sold for a price of

$80,000 and the sale has been affected on 5th of June 2019. This sale has been rendered a

CGT event of A1 category, but it will not be permitted to avail a discount of 50% as the

shares were not held by Daniel for a period, which exceeds 12 months. Daniel has taken a

loan of $70000 for acquiring such shares and he has been subjected to an interest of $5000

upon that loan. In addition to this an expense of 750 dollars of brokerage fee as well as 250

dollars of stamp duty has also been incurred by Daniel for the acquisition of such shares.

Again, shares are treated as CGT assets and proceeds of the sale of such shares is a

component while computing the CGT liability u/s 110.55 of the ITAA 97. However, if the

cost base has been reduced by virtue of any loan availed or any interest thereto accrued is

required to be excluded with the third element that is the owning cost while computing the

CGT liability. In this case, as a loan has been availed for the purpose of acquiring the shares,

the interest will form the third element of the reduced cost base and hence will required to be

e excluded while computing the CGT liability. CGT loss incurred will be $ [(75000+250) –

(80000 – 750)] = $ 4000.

CGT gain is:

House – 0

Painting – 55000

Yacht – 50000 (disregarded)

Shares – 4000

Loss from previous year – 10000

Total capital gain is – 49000

In this case the shares that has been acquired by Daniel was worth $75,000 and acquisition

has been affected on 10th January of the year 2019. The shares has been sold for a price of

$80,000 and the sale has been affected on 5th of June 2019. This sale has been rendered a

CGT event of A1 category, but it will not be permitted to avail a discount of 50% as the

shares were not held by Daniel for a period, which exceeds 12 months. Daniel has taken a

loan of $70000 for acquiring such shares and he has been subjected to an interest of $5000

upon that loan. In addition to this an expense of 750 dollars of brokerage fee as well as 250

dollars of stamp duty has also been incurred by Daniel for the acquisition of such shares.

Again, shares are treated as CGT assets and proceeds of the sale of such shares is a

component while computing the CGT liability u/s 110.55 of the ITAA 97. However, if the

cost base has been reduced by virtue of any loan availed or any interest thereto accrued is

required to be excluded with the third element that is the owning cost while computing the

CGT liability. In this case, as a loan has been availed for the purpose of acquiring the shares,

the interest will form the third element of the reduced cost base and hence will required to be

e excluded while computing the CGT liability. CGT loss incurred will be $ [(75000+250) –

(80000 – 750)] = $ 4000.

CGT gain is:

House – 0

Painting – 55000

Yacht – 50000 (disregarded)

Shares – 4000

Loss from previous year – 10000

Total capital gain is – 49000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Conclusion

The net CGT computation is as above.

Conclusion

The net CGT computation is as above.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

The Fringe Benefits Tax Assessment Act 1986 (Cth)

The Income Tax Assessment Act 1997 (Cth)

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Reference

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

The Fringe Benefits Tax Assessment Act 1986 (Cth)

The Income Tax Assessment Act 1997 (Cth)

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.