HI6028 Taxation Law: Partnership Income and Fringe Benefits T3 2018

VerifiedAdded on 2023/04/21

|13

|2244

|339

Homework Assignment

AI Summary

This assignment provides solutions to taxation law problems concerning partnership income and fringe benefits. It analyzes the calculation of partnership net income, considering ordinary income concepts, allowable deductions under the Income Tax Assessment Act 1997, and relevant case law. The assignment further examines the tax consequences of fringe benefits provided to an employee, focusing on expense payment fringe benefits and housing fringe benefits, referencing the FBT Assessment Act 1986. The solutions demonstrate the application of relevant legislative provisions to determine taxable values and employer tax liabilities.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1:................................................................................................................2

Partnership Net Income:.............................................................................................................4

Working Papers:.........................................................................................................................5

Answer to Question 2:................................................................................................................7

References:...............................................................................................................................10

Table of Contents

Answer to Question 1:................................................................................................................2

Partnership Net Income:.............................................................................................................4

Working Papers:.........................................................................................................................5

Answer to Question 2:................................................................................................................7

References:...............................................................................................................................10

2TAXATION LAW

Answer to Question 1:

Issues:

The common issue to the problems is to implement the general concepts of the

ordinary income and determine the total taxable income of the partnership business.

Laws:

The focus of the “sec 6-5, Income Tax Assessment Act 1997” is to understand the

general concepts ordinary income (Slemrod and Bakija 2017). Upon making the taxable

income, those incomes are considered into the taxable income on the basis of ordinary

concepts. A receipt cannot be categorized as the ordinary earnings until and unless it is

satisfying the standards of real gains and the cash or cash convertible. Given that both the

prerequisite has been met a gains would be treated as ordinary income if it meets the

periodical and flow concept.

An explanation has been made under the statutory provision of sec 90 that partnership

net income should be calculated after making some deductions. The net income or the loss

that is distributed among the partners that pay tax on the distribution (Dai et al. 2015). In

addition, sec 90 also makes the partners aware that the taxable income among the partners

should be decided after making the permissible deductions.

An essential depiction of the sec 8-1 also explains that the deduction is allowed for

the taxpayers under the general provisions given the outgoings is only occurred by the

taxpayer for the purpose of earning the taxable income (McLaren and Passant 2017). An

explanation is provided under the “sec 8-1 (1997)” that the taxpayer is given the permission

for being entitled for deduction only when the same is occurred for producing the chargeable

Answer to Question 1:

Issues:

The common issue to the problems is to implement the general concepts of the

ordinary income and determine the total taxable income of the partnership business.

Laws:

The focus of the “sec 6-5, Income Tax Assessment Act 1997” is to understand the

general concepts ordinary income (Slemrod and Bakija 2017). Upon making the taxable

income, those incomes are considered into the taxable income on the basis of ordinary

concepts. A receipt cannot be categorized as the ordinary earnings until and unless it is

satisfying the standards of real gains and the cash or cash convertible. Given that both the

prerequisite has been met a gains would be treated as ordinary income if it meets the

periodical and flow concept.

An explanation has been made under the statutory provision of sec 90 that partnership

net income should be calculated after making some deductions. The net income or the loss

that is distributed among the partners that pay tax on the distribution (Dai et al. 2015). In

addition, sec 90 also makes the partners aware that the taxable income among the partners

should be decided after making the permissible deductions.

An essential depiction of the sec 8-1 also explains that the deduction is allowed for

the taxpayers under the general provisions given the outgoings is only occurred by the

taxpayer for the purpose of earning the taxable income (McLaren and Passant 2017). An

explanation is provided under the “sec 8-1 (1997)” that the taxpayer is given the permission

for being entitled for deduction only when the same is occurred for producing the chargeable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

earnings. No deduction is permitted within the provision of “sec 8-1(2)” provided that they

are having the characteristics of capital, private or domestic.

It is of utmost important for the taxpayer under “sec 25-10” that items for repairs

occurred in the course of business is deductible. Most importantly under “sec 25-10 (3)” that

capital expenses of repairs are not permitted for deductions (Brandon 2015). As held in

“Shipping Co Ltd v Inland Revenue Commissioners (1923)” that repairs that is undertaken

at the time of acquisitions is a capital outgoings and non-deductible.

As explained by the ATO that whenever an ongoing business makes the acquisition of

business purpose assets that has the cost base of lower than ATO limit of AUD$ 20,000 then

there is a permission allowed to provide the taxpayer with immediate deductions (Kyle 2015).

Applications:

The above stated laws can be applied here for the purpose of explaining that Olivia

along with Daniel are operating the partnership business in terms of the sec 90, of the

partnership act. When they conducted the business activities there was the cash receipts from

the ordinary business process and debtor’s payment that was received by them. These are

classified as the ordinary earnings in relation to the provision of the ordinary concepts under

“sec 6-5, ITA Act”. The main reason is that they are meeting the regular concepts of flow and

will be assessed for tax purpose.

While there are business outgoings which is reported by Olivia and Daniel. As a

result, these includes the rates expenses on the council, Union fees, ANZ bank account

charges etc. is held for deductions. The reference of positive limbs under “sec 8-1” is

implemented for obtaining deductions for the above stated expenses (Halpern 2018). While

certain expenses such as drawings which is reported by Daniel and Olivia is not allowed for

earnings. No deduction is permitted within the provision of “sec 8-1(2)” provided that they

are having the characteristics of capital, private or domestic.

It is of utmost important for the taxpayer under “sec 25-10” that items for repairs

occurred in the course of business is deductible. Most importantly under “sec 25-10 (3)” that

capital expenses of repairs are not permitted for deductions (Brandon 2015). As held in

“Shipping Co Ltd v Inland Revenue Commissioners (1923)” that repairs that is undertaken

at the time of acquisitions is a capital outgoings and non-deductible.

As explained by the ATO that whenever an ongoing business makes the acquisition of

business purpose assets that has the cost base of lower than ATO limit of AUD$ 20,000 then

there is a permission allowed to provide the taxpayer with immediate deductions (Kyle 2015).

Applications:

The above stated laws can be applied here for the purpose of explaining that Olivia

along with Daniel are operating the partnership business in terms of the sec 90, of the

partnership act. When they conducted the business activities there was the cash receipts from

the ordinary business process and debtor’s payment that was received by them. These are

classified as the ordinary earnings in relation to the provision of the ordinary concepts under

“sec 6-5, ITA Act”. The main reason is that they are meeting the regular concepts of flow and

will be assessed for tax purpose.

While there are business outgoings which is reported by Olivia and Daniel. As a

result, these includes the rates expenses on the council, Union fees, ANZ bank account

charges etc. is held for deductions. The reference of positive limbs under “sec 8-1” is

implemented for obtaining deductions for the above stated expenses (Halpern 2018). While

certain expenses such as drawings which is reported by Daniel and Olivia is not allowed for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

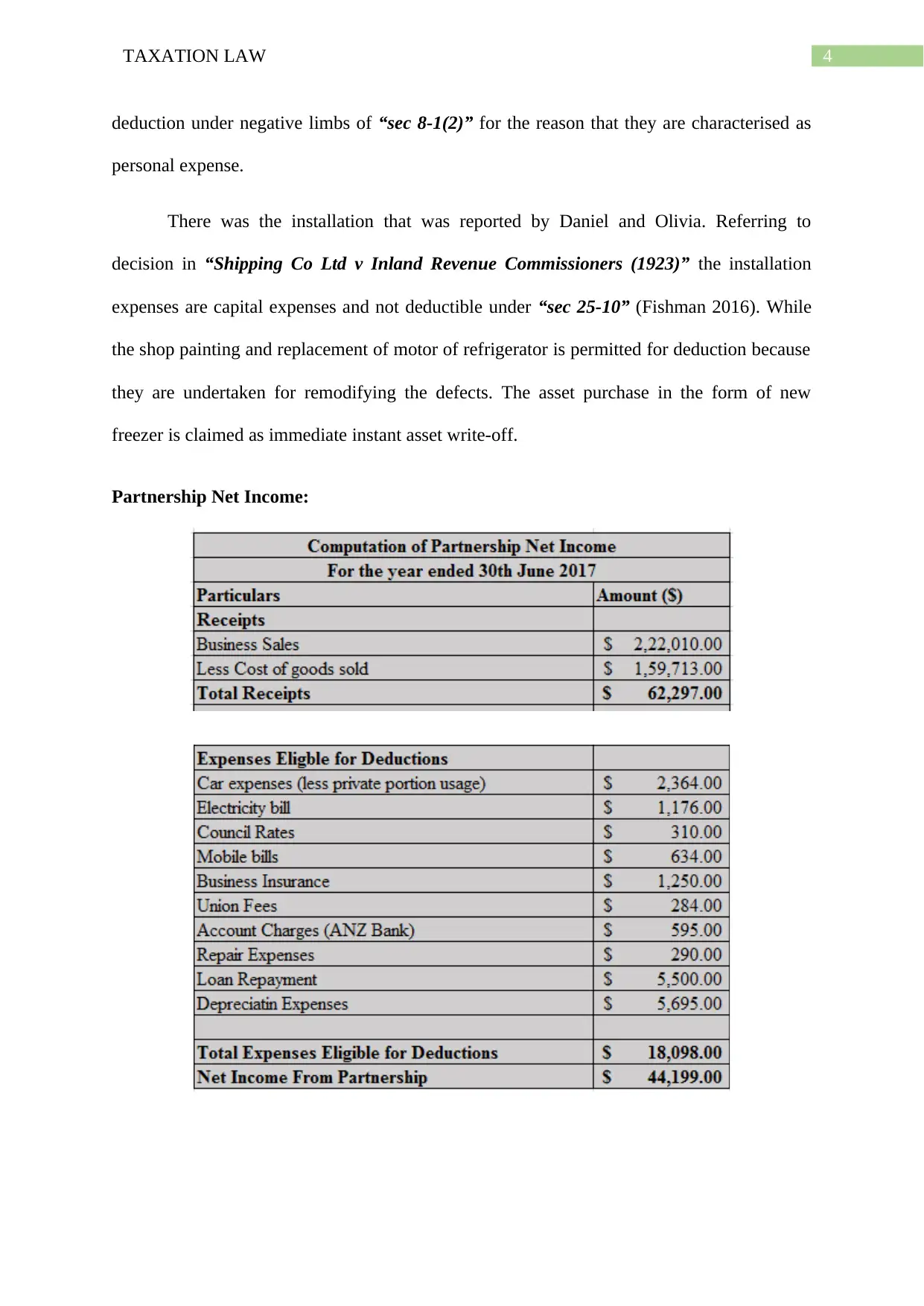

deduction under negative limbs of “sec 8-1(2)” for the reason that they are characterised as

personal expense.

There was the installation that was reported by Daniel and Olivia. Referring to

decision in “Shipping Co Ltd v Inland Revenue Commissioners (1923)” the installation

expenses are capital expenses and not deductible under “sec 25-10” (Fishman 2016). While

the shop painting and replacement of motor of refrigerator is permitted for deduction because

they are undertaken for remodifying the defects. The asset purchase in the form of new

freezer is claimed as immediate instant asset write-off.

Partnership Net Income:

deduction under negative limbs of “sec 8-1(2)” for the reason that they are characterised as

personal expense.

There was the installation that was reported by Daniel and Olivia. Referring to

decision in “Shipping Co Ltd v Inland Revenue Commissioners (1923)” the installation

expenses are capital expenses and not deductible under “sec 25-10” (Fishman 2016). While

the shop painting and replacement of motor of refrigerator is permitted for deduction because

they are undertaken for remodifying the defects. The asset purchase in the form of new

freezer is claimed as immediate instant asset write-off.

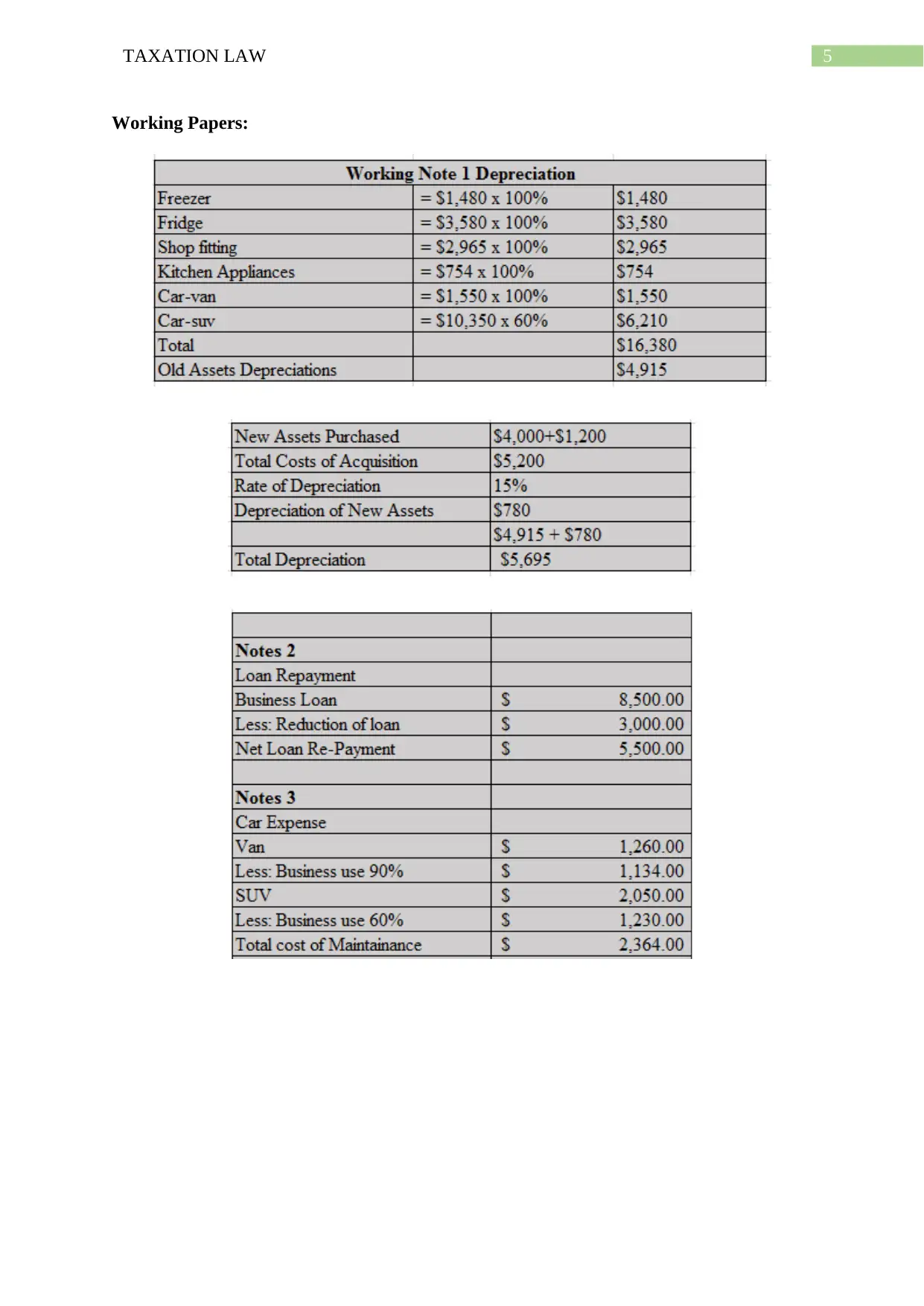

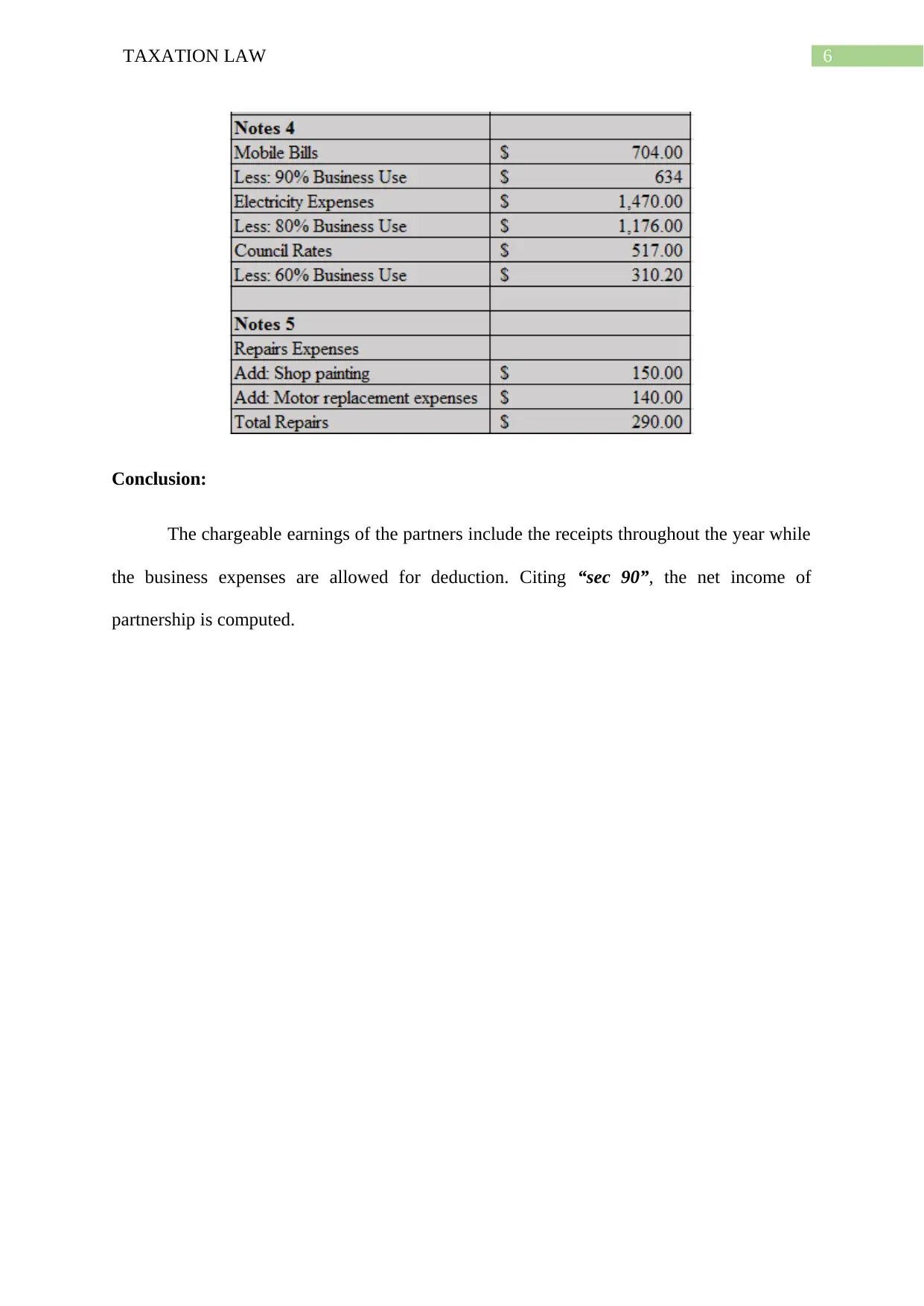

Partnership Net Income:

5TAXATION LAW

Working Papers:

Working Papers:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Conclusion:

The chargeable earnings of the partners include the receipts throughout the year while

the business expenses are allowed for deduction. Citing “sec 90”, the net income of

partnership is computed.

Conclusion:

The chargeable earnings of the partners include the receipts throughout the year while

the business expenses are allowed for deduction. Citing “sec 90”, the net income of

partnership is computed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to Question 2:

Issues:

The common issue to the problems is the tax consequences for the worker and the

employer. The tax consequences issues here include the housing fringe benefit issues and the

payment of the expense by the employer for the worker under the legislation of “FBT

Assessment Act 1986”.

Laws:

An important law that relates to the expense payment fringe benefit is the “section 20

of the FBT Assessment Act 1986” which is applicable to the expenditure that is occurred by

the worker and the same is reimbursed back to the worker or paid by the employer. The

legislation explains that the law is not applicable to the purchase of goods and services

directly or given to the employee (Pope, Fayle and Chen 2013). Under the sec 20, of this

fringe benefit provision the employer is held liable for levy only when the expense payment

fringe benefit is reimbursed to the worker that they have occurred or the same is paid as the

satisfaction to the third party that is occurred by the employee.

On the other hand, there is a legislative standing of “sec 23 of FBT Assessment Act

1986” that deals with the chargeable value of expenditure that have been occurred by

employer or the expenses is subsequently reimbursed by the employer (Pope 2013). The

standing provision of “sec 23, FBT Assessment Act 1986” makes the employer aware that

chargeable sum of the expense payment fringe benefit constitutes the value that the employer

gives or reimburses the employees.

During the course of employment, the employer often provides the employee with the

housing fringe benefit as the right granted for using the accommodation as the worker’s

Answer to Question 2:

Issues:

The common issue to the problems is the tax consequences for the worker and the

employer. The tax consequences issues here include the housing fringe benefit issues and the

payment of the expense by the employer for the worker under the legislation of “FBT

Assessment Act 1986”.

Laws:

An important law that relates to the expense payment fringe benefit is the “section 20

of the FBT Assessment Act 1986” which is applicable to the expenditure that is occurred by

the worker and the same is reimbursed back to the worker or paid by the employer. The

legislation explains that the law is not applicable to the purchase of goods and services

directly or given to the employee (Pope, Fayle and Chen 2013). Under the sec 20, of this

fringe benefit provision the employer is held liable for levy only when the expense payment

fringe benefit is reimbursed to the worker that they have occurred or the same is paid as the

satisfaction to the third party that is occurred by the employee.

On the other hand, there is a legislative standing of “sec 23 of FBT Assessment Act

1986” that deals with the chargeable value of expenditure that have been occurred by

employer or the expenses is subsequently reimbursed by the employer (Pope 2013). The

standing provision of “sec 23, FBT Assessment Act 1986” makes the employer aware that

chargeable sum of the expense payment fringe benefit constitutes the value that the employer

gives or reimburses the employees.

During the course of employment, the employer often provides the employee with the

housing fringe benefit as the right granted for using the accommodation as the worker’s

8TAXATION LAW

normal place for living (Tran-Nam 2016). The statutory standing of “sec 25, FBT

Assessment Act 1986” clarifies notably that when during the whole or in part of the FBT year

the employer is giving an accommodation for the purpose of employee living or residence

then such accommodation shall be taken as housing fringe benefit for the employer.

Most importantly, the legislative standing of “sec 27, FBT Assessment Act 1986”

provides the basis on which taxes are imposed on the employer (Long, Campbell and

Kelshaw 2016). The legal provision of “sec 27, FBT Assessment Act 1986” elucidates that

taxes are imposed for the housing fringe benefit by making a reference to the market value of

the right for occupying the residence which can be further lowered down in respect of the

contribution of rent paid by employee as the rental payments.

Application:

The application of the above stated legislative provision can be made in the case of

John who is working in capacity of the employee and has received several fringe benefit

during the course of the employment from his employer. As the practical matter there was a

payment that was made by the employer of printing company for the schooling fees in which

the child of John is currently enrolled. The amount that was paid stands $15,000 and this is

the arrangement of salary package for John.

Upon paying the schooling fees of the worker’s child here the employer of John

within the legislative standing of “section 20”, has given rise to the expense payment fringe

benefit (Cooper 2018). The amount that was paid by the employer here was made to John in

capacity of the employee as the means of satisfying the expenses of the third party that is

occurred by the employee. The expenses hold the combination of private and domestic

arrangement for John.

normal place for living (Tran-Nam 2016). The statutory standing of “sec 25, FBT

Assessment Act 1986” clarifies notably that when during the whole or in part of the FBT year

the employer is giving an accommodation for the purpose of employee living or residence

then such accommodation shall be taken as housing fringe benefit for the employer.

Most importantly, the legislative standing of “sec 27, FBT Assessment Act 1986”

provides the basis on which taxes are imposed on the employer (Long, Campbell and

Kelshaw 2016). The legal provision of “sec 27, FBT Assessment Act 1986” elucidates that

taxes are imposed for the housing fringe benefit by making a reference to the market value of

the right for occupying the residence which can be further lowered down in respect of the

contribution of rent paid by employee as the rental payments.

Application:

The application of the above stated legislative provision can be made in the case of

John who is working in capacity of the employee and has received several fringe benefit

during the course of the employment from his employer. As the practical matter there was a

payment that was made by the employer of printing company for the schooling fees in which

the child of John is currently enrolled. The amount that was paid stands $15,000 and this is

the arrangement of salary package for John.

Upon paying the schooling fees of the worker’s child here the employer of John

within the legislative standing of “section 20”, has given rise to the expense payment fringe

benefit (Cooper 2018). The amount that was paid by the employer here was made to John in

capacity of the employee as the means of satisfying the expenses of the third party that is

occurred by the employee. The expenses hold the combination of private and domestic

arrangement for John.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

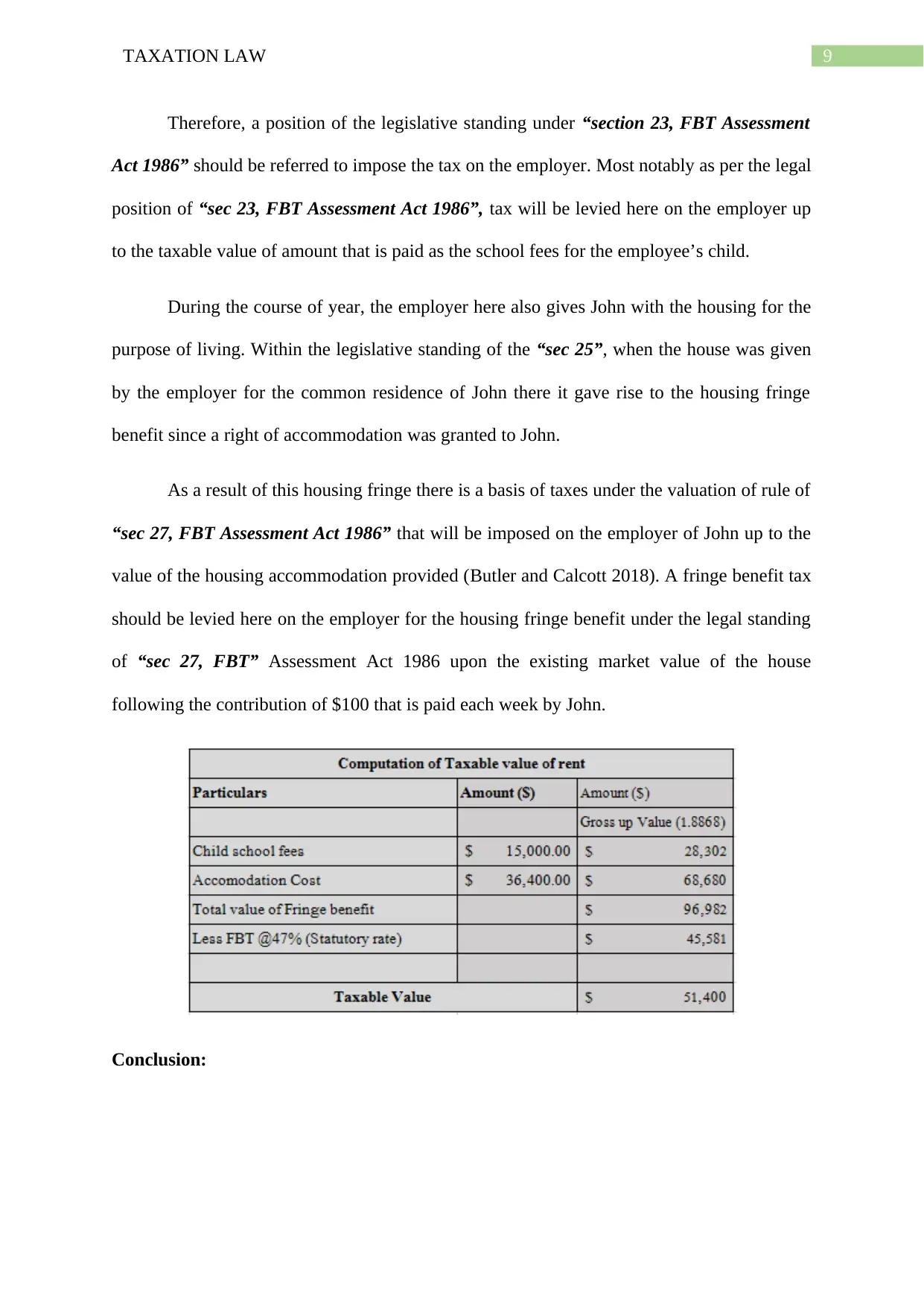

Therefore, a position of the legislative standing under “section 23, FBT Assessment

Act 1986” should be referred to impose the tax on the employer. Most notably as per the legal

position of “sec 23, FBT Assessment Act 1986”, tax will be levied here on the employer up

to the taxable value of amount that is paid as the school fees for the employee’s child.

During the course of year, the employer here also gives John with the housing for the

purpose of living. Within the legislative standing of the “sec 25”, when the house was given

by the employer for the common residence of John there it gave rise to the housing fringe

benefit since a right of accommodation was granted to John.

As a result of this housing fringe there is a basis of taxes under the valuation of rule of

“sec 27, FBT Assessment Act 1986” that will be imposed on the employer of John up to the

value of the housing accommodation provided (Butler and Calcott 2018). A fringe benefit tax

should be levied here on the employer for the housing fringe benefit under the legal standing

of “sec 27, FBT” Assessment Act 1986 upon the existing market value of the house

following the contribution of $100 that is paid each week by John.

Conclusion:

Therefore, a position of the legislative standing under “section 23, FBT Assessment

Act 1986” should be referred to impose the tax on the employer. Most notably as per the legal

position of “sec 23, FBT Assessment Act 1986”, tax will be levied here on the employer up

to the taxable value of amount that is paid as the school fees for the employee’s child.

During the course of year, the employer here also gives John with the housing for the

purpose of living. Within the legislative standing of the “sec 25”, when the house was given

by the employer for the common residence of John there it gave rise to the housing fringe

benefit since a right of accommodation was granted to John.

As a result of this housing fringe there is a basis of taxes under the valuation of rule of

“sec 27, FBT Assessment Act 1986” that will be imposed on the employer of John up to the

value of the housing accommodation provided (Butler and Calcott 2018). A fringe benefit tax

should be levied here on the employer for the housing fringe benefit under the legal standing

of “sec 27, FBT” Assessment Act 1986 upon the existing market value of the house

following the contribution of $100 that is paid each week by John.

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

As per the legislative provision of the FBT Assessment Act 1986 a statutory rate of

47% has been applied on the overall amount of fringe benefit that is given by the employer

and the employer is held taxation purpose upon the taxable value of $51,400.

As per the legislative provision of the FBT Assessment Act 1986 a statutory rate of

47% has been applied on the overall amount of fringe benefit that is given by the employer

and the employer is held taxation purpose upon the taxable value of $51,400.

11TAXATION LAW

References:

Brandon, G., 2015. Taxation and crowdfunding-the start. Taxation in Australia, 49(8), p.446.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Dai, M., Liu, H., Yang, C. and Zhong, Y., 2015. Optimal tax timing with asymmetric long-

term/short-term capital gains tax. The Review of Financial Studies, 28(9), pp.2687-2721.

Fishman, S., 2016. Every Landlord's Tax Deduction Guide. Nolo.

Halpern, J., 2018. WHEN EQUIPMENT REPAIRS ARE ORDINARY AND NECESSARY:

New regulations provide some help in determining whether equipment repairs and

improvements should be capitalized or expensed. Strategic Finance, 99(7), pp.18-20.

Kyle, T., 2015. Practical application of the new Pt IVA. Tax Specialist, 18(3), p.104.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

McLaren, J. and Passant, J., 2017. Leasehold property and the deductibiIity of stamp

duty. Australian Tax Law Bulletin, 4(3), pp.44-46.

Pope, J., 2013. The compliance costs of taxation in Australia and tax simplification: The

issues. Australian Journal of Management, 18(1), pp.69-89.

Pope, J., Fayle, R. and Chen, D.L., 2013. The compliance costs of employment-related

taxation in Australia: employers' pay-as-you-earn, fringe benefits tax, prescribed payments

system and payroll tax. Australian Tax Research Foundation Research Studies, p.viii.

References:

Brandon, G., 2015. Taxation and crowdfunding-the start. Taxation in Australia, 49(8), p.446.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Dai, M., Liu, H., Yang, C. and Zhong, Y., 2015. Optimal tax timing with asymmetric long-

term/short-term capital gains tax. The Review of Financial Studies, 28(9), pp.2687-2721.

Fishman, S., 2016. Every Landlord's Tax Deduction Guide. Nolo.

Halpern, J., 2018. WHEN EQUIPMENT REPAIRS ARE ORDINARY AND NECESSARY:

New regulations provide some help in determining whether equipment repairs and

improvements should be capitalized or expensed. Strategic Finance, 99(7), pp.18-20.

Kyle, T., 2015. Practical application of the new Pt IVA. Tax Specialist, 18(3), p.104.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

McLaren, J. and Passant, J., 2017. Leasehold property and the deductibiIity of stamp

duty. Australian Tax Law Bulletin, 4(3), pp.44-46.

Pope, J., 2013. The compliance costs of taxation in Australia and tax simplification: The

issues. Australian Journal of Management, 18(1), pp.69-89.

Pope, J., Fayle, R. and Chen, D.L., 2013. The compliance costs of employment-related

taxation in Australia: employers' pay-as-you-earn, fringe benefits tax, prescribed payments

system and payroll tax. Australian Tax Research Foundation Research Studies, p.viii.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.