Taxation Law Assignment: Fringe Benefits, Capital Gains Tax Analysis

VerifiedAdded on 2020/05/16

|9

|2892

|105

Homework Assignment

AI Summary

This taxation law assignment explores two main areas: fringe benefits tax (FBT) and capital gains tax (CGT). The first part analyzes whether providing a car to an employee constitutes a fringe benefit under the Fringe Benefit Tax Assessment Act 1986 (FBTAA 1986). It examines the relevant rules, including the definitions of fringe benefits, car fringe benefits, and the application of statutory and cost basis formulas for calculating the taxable value. The assignment applies these rules to a case study involving an employer providing a car for an employee's private use, concluding that the employer is liable for car fringe benefit tax. The second part delves into capital gains tax, integrating it into income tax regimes. It examines the CGT implications of various asset sales, including a residential property, an artistic painting, a luxury yacht (personal use asset), and shares. The analysis considers relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997), such as CGT event H1, collectables, and personal use assets. The assignment concludes by summarizing the capital gains that can be used to fund retirement and the treatment of capital losses from personal-use assets. The document provides a comprehensive overview of both FBT and CGT, offering practical application of tax law principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.............................................................................................................2

Answer to question 2:.............................................................................................................5

Answer A:..............................................................................................................................5

Answer to B:.........................................................................................................................6

Answer to C:.........................................................................................................................6

References:..............................................................................................................................7

Table of Contents

Answer to question 1:.............................................................................................................2

Answer to question 2:.............................................................................................................5

Answer A:..............................................................................................................................5

Answer to B:.........................................................................................................................6

Answer to C:.........................................................................................................................6

References:..............................................................................................................................7

2TAXATION LAW

Answer to question 1:

Issues:

Is providing car to the employee in relation to the employment of the

employee amounts to fringe benefit for the employer under the “s-7 (1), FBTAA

1986”?

Rule:

The provision that are associated to the fringe benefit is given under the

Fringe benefit tax assessment act 1986 (Sowa et al. 2018). The fringe benefit tax is

different from that of the income tax. The employer should understand the difference

between the fringe benefit tax and the income tax. It includes the taxes that are

imposed on employer rather than taxes imposed on the employee based on the

provision of fringe benefits. The fringe benefit year starts from April 1 to March 31

and referred as the year of tax.

The taxpayers should denote that the fringe benefit tax regimes are

particularly the tax that is applied on large aspect of benefits that is given to the

employee by the employer (Young and Miles 2015). The fringe benefit tax is useful

tool in overcoming the inadequacies of the income tax regimes. This includes the

imposition of taxes on the non-cash benefits that were not easily cash convertible. It

is also takes into the account the application of benefits that is given to the

employee’s associate such as spouse.

The definition that is given in “S-136 (1), FBTAA 1986” explains that the

legislation of FBT is regarded as central in imposing tax (Harding 2014). A fringe tax

is existent where there is;

a. A benefit

b. Given in the year of tax

c. By the employer or the associates of the employer or the third party

d. To the associate or the employee

e. In regard to the service of the worker.

There are special rules that are applied by the “sec-136 (1), FBTAA 1986”.

This states that specific exclusion is applied on the salaries and wages derived by

the employee. As per the “S,136 (1), FBTAA 1986” the word benefit is inclusive of

the privilege, right, service or the amenities that is given to the employee under the

arrangement in respect of the performance of the work (Carney 2014). The definition

of fringe benefit tax is very wide and it is most likely to take into the consideration

majority of the benefits that also includes the non-cash benefits that is given to the

employee in respect of the employee.

The specific rules of the fringe benefit tax under “s-136 (1), FBTAA 1986”

explains that the benefit should be provided either by the employer or related parties

or under the arrangement with the employer. Under the definition of the “s, 136 (1),

FBTAA 1986” includes “employer” as the future employer, current employer and

the former employer (Edmonds 2015). While the word employee on the other hand

includes a person that is receiving salary and wages. The definition also covers the

future employee, current employee and the former employee.

Answer to question 1:

Issues:

Is providing car to the employee in relation to the employment of the

employee amounts to fringe benefit for the employer under the “s-7 (1), FBTAA

1986”?

Rule:

The provision that are associated to the fringe benefit is given under the

Fringe benefit tax assessment act 1986 (Sowa et al. 2018). The fringe benefit tax is

different from that of the income tax. The employer should understand the difference

between the fringe benefit tax and the income tax. It includes the taxes that are

imposed on employer rather than taxes imposed on the employee based on the

provision of fringe benefits. The fringe benefit year starts from April 1 to March 31

and referred as the year of tax.

The taxpayers should denote that the fringe benefit tax regimes are

particularly the tax that is applied on large aspect of benefits that is given to the

employee by the employer (Young and Miles 2015). The fringe benefit tax is useful

tool in overcoming the inadequacies of the income tax regimes. This includes the

imposition of taxes on the non-cash benefits that were not easily cash convertible. It

is also takes into the account the application of benefits that is given to the

employee’s associate such as spouse.

The definition that is given in “S-136 (1), FBTAA 1986” explains that the

legislation of FBT is regarded as central in imposing tax (Harding 2014). A fringe tax

is existent where there is;

a. A benefit

b. Given in the year of tax

c. By the employer or the associates of the employer or the third party

d. To the associate or the employee

e. In regard to the service of the worker.

There are special rules that are applied by the “sec-136 (1), FBTAA 1986”.

This states that specific exclusion is applied on the salaries and wages derived by

the employee. As per the “S,136 (1), FBTAA 1986” the word benefit is inclusive of

the privilege, right, service or the amenities that is given to the employee under the

arrangement in respect of the performance of the work (Carney 2014). The definition

of fringe benefit tax is very wide and it is most likely to take into the consideration

majority of the benefits that also includes the non-cash benefits that is given to the

employee in respect of the employee.

The specific rules of the fringe benefit tax under “s-136 (1), FBTAA 1986”

explains that the benefit should be provided either by the employer or related parties

or under the arrangement with the employer. Under the definition of the “s, 136 (1),

FBTAA 1986” includes “employer” as the future employer, current employer and

the former employer (Edmonds 2015). While the word employee on the other hand

includes a person that is receiving salary and wages. The definition also covers the

future employee, current employee and the former employee.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

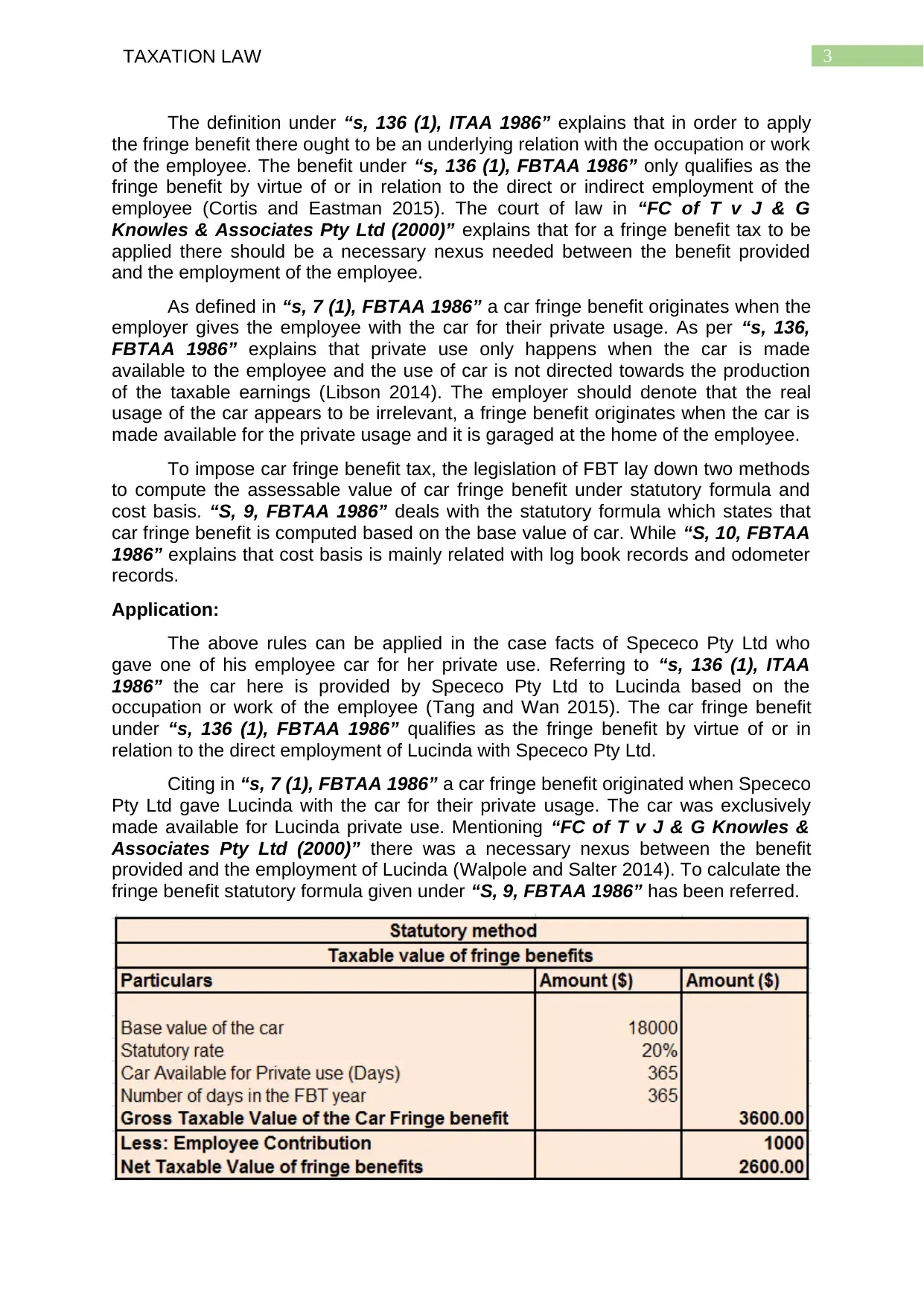

The definition under “s, 136 (1), ITAA 1986” explains that in order to apply

the fringe benefit there ought to be an underlying relation with the occupation or work

of the employee. The benefit under “s, 136 (1), FBTAA 1986” only qualifies as the

fringe benefit by virtue of or in relation to the direct or indirect employment of the

employee (Cortis and Eastman 2015). The court of law in “FC of T v J & G

Knowles & Associates Pty Ltd (2000)” explains that for a fringe benefit tax to be

applied there should be a necessary nexus needed between the benefit provided

and the employment of the employee.

As defined in “s, 7 (1), FBTAA 1986” a car fringe benefit originates when the

employer gives the employee with the car for their private usage. As per “s, 136,

FBTAA 1986” explains that private use only happens when the car is made

available to the employee and the use of car is not directed towards the production

of the taxable earnings (Libson 2014). The employer should denote that the real

usage of the car appears to be irrelevant, a fringe benefit originates when the car is

made available for the private usage and it is garaged at the home of the employee.

To impose car fringe benefit tax, the legislation of FBT lay down two methods

to compute the assessable value of car fringe benefit under statutory formula and

cost basis. “S, 9, FBTAA 1986” deals with the statutory formula which states that

car fringe benefit is computed based on the base value of car. While “S, 10, FBTAA

1986” explains that cost basis is mainly related with log book records and odometer

records.

Application:

The above rules can be applied in the case facts of Spececo Pty Ltd who

gave one of his employee car for her private use. Referring to “s, 136 (1), ITAA

1986” the car here is provided by Spececo Pty Ltd to Lucinda based on the

occupation or work of the employee (Tang and Wan 2015). The car fringe benefit

under “s, 136 (1), FBTAA 1986” qualifies as the fringe benefit by virtue of or in

relation to the direct employment of Lucinda with Spececo Pty Ltd.

Citing in “s, 7 (1), FBTAA 1986” a car fringe benefit originated when Spececo

Pty Ltd gave Lucinda with the car for their private usage. The car was exclusively

made available for Lucinda private use. Mentioning “FC of T v J & G Knowles &

Associates Pty Ltd (2000)” there was a necessary nexus between the benefit

provided and the employment of Lucinda (Walpole and Salter 2014). To calculate the

fringe benefit statutory formula given under “S, 9, FBTAA 1986” has been referred.

The definition under “s, 136 (1), ITAA 1986” explains that in order to apply

the fringe benefit there ought to be an underlying relation with the occupation or work

of the employee. The benefit under “s, 136 (1), FBTAA 1986” only qualifies as the

fringe benefit by virtue of or in relation to the direct or indirect employment of the

employee (Cortis and Eastman 2015). The court of law in “FC of T v J & G

Knowles & Associates Pty Ltd (2000)” explains that for a fringe benefit tax to be

applied there should be a necessary nexus needed between the benefit provided

and the employment of the employee.

As defined in “s, 7 (1), FBTAA 1986” a car fringe benefit originates when the

employer gives the employee with the car for their private usage. As per “s, 136,

FBTAA 1986” explains that private use only happens when the car is made

available to the employee and the use of car is not directed towards the production

of the taxable earnings (Libson 2014). The employer should denote that the real

usage of the car appears to be irrelevant, a fringe benefit originates when the car is

made available for the private usage and it is garaged at the home of the employee.

To impose car fringe benefit tax, the legislation of FBT lay down two methods

to compute the assessable value of car fringe benefit under statutory formula and

cost basis. “S, 9, FBTAA 1986” deals with the statutory formula which states that

car fringe benefit is computed based on the base value of car. While “S, 10, FBTAA

1986” explains that cost basis is mainly related with log book records and odometer

records.

Application:

The above rules can be applied in the case facts of Spececo Pty Ltd who

gave one of his employee car for her private use. Referring to “s, 136 (1), ITAA

1986” the car here is provided by Spececo Pty Ltd to Lucinda based on the

occupation or work of the employee (Tang and Wan 2015). The car fringe benefit

under “s, 136 (1), FBTAA 1986” qualifies as the fringe benefit by virtue of or in

relation to the direct employment of Lucinda with Spececo Pty Ltd.

Citing in “s, 7 (1), FBTAA 1986” a car fringe benefit originated when Spececo

Pty Ltd gave Lucinda with the car for their private usage. The car was exclusively

made available for Lucinda private use. Mentioning “FC of T v J & G Knowles &

Associates Pty Ltd (2000)” there was a necessary nexus between the benefit

provided and the employment of Lucinda (Walpole and Salter 2014). To calculate the

fringe benefit statutory formula given under “S, 9, FBTAA 1986” has been referred.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

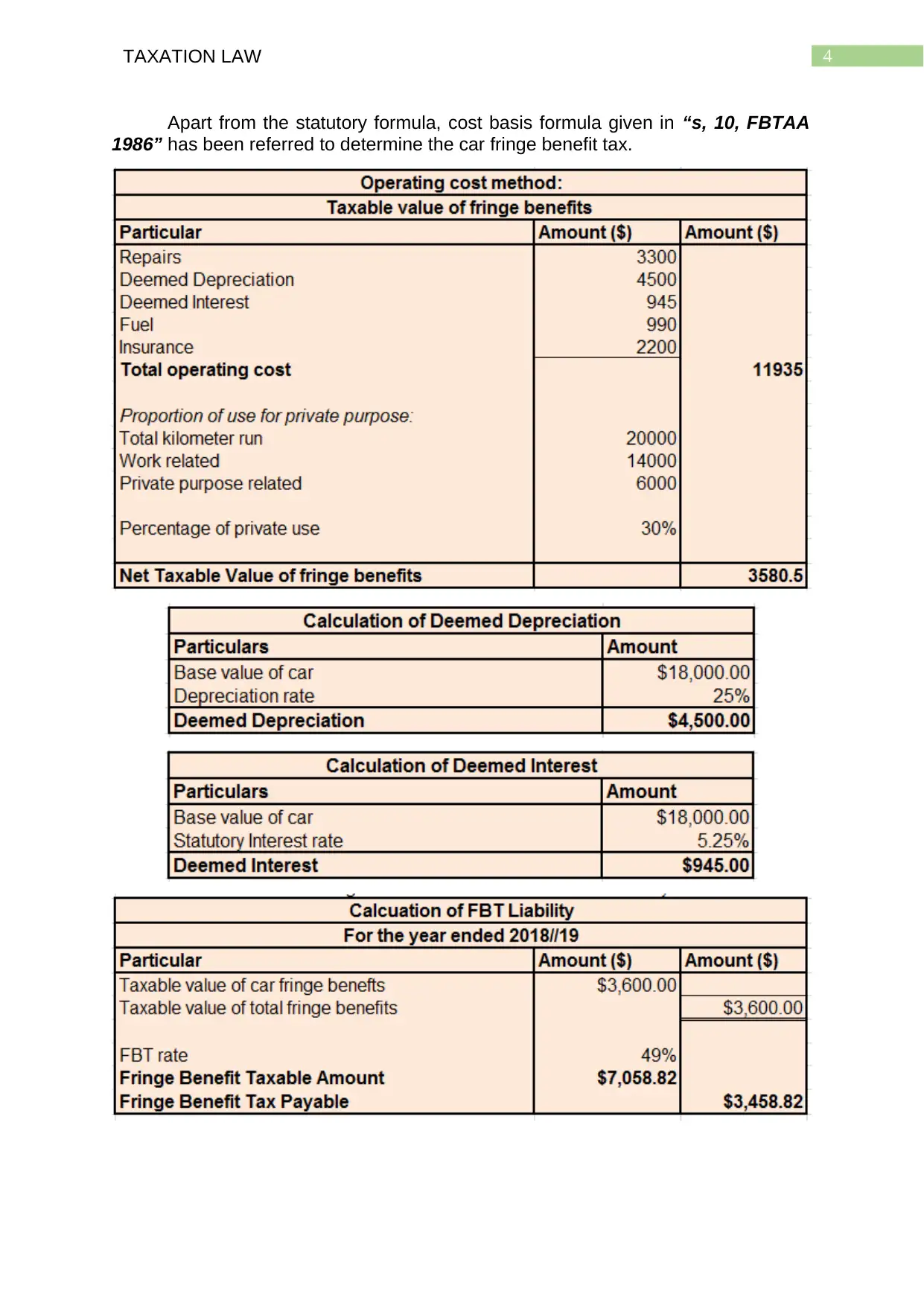

Apart from the statutory formula, cost basis formula given in “s, 10, FBTAA

1986” has been referred to determine the car fringe benefit tax.

Apart from the statutory formula, cost basis formula given in “s, 10, FBTAA

1986” has been referred to determine the car fringe benefit tax.

5TAXATION LAW

The taxable value of fringe benefit that is calculated under the statutory

method appears to be lower. It is recommended that the Spececo Pty Ltd should use

the statutory formula as the net taxable value under the statutory formula is $2,600.

Conclusion:

On arriving at the conclusion, it can be stated that the car was provided to the

Lucinda was out of the employer and employee relationship with Spececo Pty Ltd.

With respect to the “s, 7 (1), FBTAA 1986” the employer here will be liable for the

car fringe benefit tax.

Answer to question 2:

Answer A:

Capital gains tax cannot be considered as the separate tax. It is integrated

into income tax regimes. As explained in the “section 102-5, ITAA 1997” the net

capital gains are included into the assessable income of the taxpayer during the year

of income (Maples and Karlinsky 2014). Capital losses are required to be

quarantined and only it is permitted to be offset from the capital gains that are made.

The taxpayer should denote that the net capital gains are not permitted for

deductions and net losses are required to be carried forward. The case study

provides that Daniel is presently in his late 50’s and wants to make investment for his

retirement. He is looking forward to contribute in his superannuation fund and as the

plan of collecting $1 million for retirement some of the assets are sold. The capital

gains tax treatment for the assets sold is given below;

Doncaster House:

Daniel resided in the Doncaster property for last 30 years. The property was

eventually purchased for $70,000 and a contract for sale has been entered by Daniel

for $865,000. A buyer decided to purchase the property and deposited $85,000. The

contract was however cancelled by the purchaser because of insufficient fund and

forfeited the sum deposit to Daniel on 1st May 2019.

“Sec-104-150, ITAA 1997” explains regarded the CGT event H1 that

originates because of the forfeiture of deposit. The event generally happens when a

purchaser makes the deposit on the potential sale and forfeits the transactions upon

the cancellation of sales (Dabner 2015). Similarly, in the situation of Daniel the

forfeited amount that is received by Daniel for his Doncaster property would be

treated as CGT event H1 under “sec 104-150, ITAA 1997”. The sum of $85,000 is a

capital gain less the cost that was paid to the property agent for the cancelled

transaction.

Artistic Painting:

Daniel had purchased the artistic painting on September 20 1985 that had the

purchase value of $15,000. The painting was sold by Daniel at $125,000 at auction.

As discussed above the capital gains tax is applied on the assets which is acquired

after the 20 sept 1985. Furthermore, the disposal of CGT asset to another person

amounts to CGT event A1 under “s104-10 (1), ITAA 1997” (Arnold et al. 2014). The

definition given in “s108-10 (2), ITAA 1997” entails that collectables mainly involve

The taxable value of fringe benefit that is calculated under the statutory

method appears to be lower. It is recommended that the Spececo Pty Ltd should use

the statutory formula as the net taxable value under the statutory formula is $2,600.

Conclusion:

On arriving at the conclusion, it can be stated that the car was provided to the

Lucinda was out of the employer and employee relationship with Spececo Pty Ltd.

With respect to the “s, 7 (1), FBTAA 1986” the employer here will be liable for the

car fringe benefit tax.

Answer to question 2:

Answer A:

Capital gains tax cannot be considered as the separate tax. It is integrated

into income tax regimes. As explained in the “section 102-5, ITAA 1997” the net

capital gains are included into the assessable income of the taxpayer during the year

of income (Maples and Karlinsky 2014). Capital losses are required to be

quarantined and only it is permitted to be offset from the capital gains that are made.

The taxpayer should denote that the net capital gains are not permitted for

deductions and net losses are required to be carried forward. The case study

provides that Daniel is presently in his late 50’s and wants to make investment for his

retirement. He is looking forward to contribute in his superannuation fund and as the

plan of collecting $1 million for retirement some of the assets are sold. The capital

gains tax treatment for the assets sold is given below;

Doncaster House:

Daniel resided in the Doncaster property for last 30 years. The property was

eventually purchased for $70,000 and a contract for sale has been entered by Daniel

for $865,000. A buyer decided to purchase the property and deposited $85,000. The

contract was however cancelled by the purchaser because of insufficient fund and

forfeited the sum deposit to Daniel on 1st May 2019.

“Sec-104-150, ITAA 1997” explains regarded the CGT event H1 that

originates because of the forfeiture of deposit. The event generally happens when a

purchaser makes the deposit on the potential sale and forfeits the transactions upon

the cancellation of sales (Dabner 2015). Similarly, in the situation of Daniel the

forfeited amount that is received by Daniel for his Doncaster property would be

treated as CGT event H1 under “sec 104-150, ITAA 1997”. The sum of $85,000 is a

capital gain less the cost that was paid to the property agent for the cancelled

transaction.

Artistic Painting:

Daniel had purchased the artistic painting on September 20 1985 that had the

purchase value of $15,000. The painting was sold by Daniel at $125,000 at auction.

As discussed above the capital gains tax is applied on the assets which is acquired

after the 20 sept 1985. Furthermore, the disposal of CGT asset to another person

amounts to CGT event A1 under “s104-10 (1), ITAA 1997” (Arnold et al. 2014). The

definition given in “s108-10 (2), ITAA 1997” entails that collectables mainly involve

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

artworks, rare stamps, antiques, coins etc. which is exclusively for taxpayer’s

personal enjoyment.

In the current case of Daniel, the painting will be considered post-CGT asset.

The painting was purchased after the CGT regime was integrated into the tax

system. The artistic painting is classified as collectables under “s-108-10 (1), ITAA

1997”. When the painting was sold by Daniel a CGT event A1 happened under

“s104-10 (1), ITAA 1997” (Antoniades 2015). The gains that is made from the sale

of painting will be included into the Daniels taxable income as the statutory income

under “section 102-5, ITAA 1997” during the year of income.

Luxury Yacht:

In a bid to fund for retirement Daniel also sold the yacht that was purchased

during November 2004. The purchase value of the yacht was $110,000. But in the in

the current tax year the yacht Daniel sold the yacht for $60,000. The definition of

personal use asset is given under the “s-108-10 (2), ITA Act 1997”. Under this

definition the personal use asset involves the boats, yacht, vehicles, electronic items

etc. that are under the ownership of taxpayer for their personal enjoyment purpose

(Sadiq and Sawyer 2018). The rule of the personal use asset is that under “s-118-

10 (3), ITA Act 1997” the taxpayer should ignore the capital gains when the cost

base of the asset is lower than $10,000. While the “s-108-20 (1), ITAA 1997” says

that if there is any capital loss suffered from the sale of personal use asset then it is

to be disregarded by the taxpayer.

The case study explains that Daniel reports the capital loss from selling the

yacht. Daniel should note that the yacht is the personal use asset under “s-108-10

(2), ITA Act 1997” (Lawrence 2019). The capital loss that is suffered by Daniel from

selling the yacht must be ignored by him under legislation of “s-108-20 (1), ITAA

1997”.

Sale of Shares:

Daniel has purchased the shares during the year on 10 January 2019 for

$75,000. But the shares were sold for $80,000. An additional cost of stamp duty was

incurred while purchasing the shares and a brokerage fees of $750 was paid while

selling the shares. With respect to “sec 110-35, ITAA 1997” the stamp duty paid for

acquiring the shares were included into the cost base of asset as the incidental cost

(Allerdice 2014). Daniel reports a capital gain from sale of BHP shares. On the other

hand, a carried forward capital loss from previous year of AZJ shares were reported.

The carried forward capital loss is offset against the capital gains from BHP shares.

The leftover loss is carried forward to the subsequent year.

Answer to B:

As evident from the above stated computation it is understood that the capital

gains that were reported by Daniel from the sale of several assets during the year

can be used to fund the retirement fund.

Answer to C:

On the other hand, Daniel also has the loss from disposing the personal use

asset. In other words, loss made from the sale of yacht must be disregarded by

Daniel as it is not allowed for offset. While the AZJ shares left over capital loss

artworks, rare stamps, antiques, coins etc. which is exclusively for taxpayer’s

personal enjoyment.

In the current case of Daniel, the painting will be considered post-CGT asset.

The painting was purchased after the CGT regime was integrated into the tax

system. The artistic painting is classified as collectables under “s-108-10 (1), ITAA

1997”. When the painting was sold by Daniel a CGT event A1 happened under

“s104-10 (1), ITAA 1997” (Antoniades 2015). The gains that is made from the sale

of painting will be included into the Daniels taxable income as the statutory income

under “section 102-5, ITAA 1997” during the year of income.

Luxury Yacht:

In a bid to fund for retirement Daniel also sold the yacht that was purchased

during November 2004. The purchase value of the yacht was $110,000. But in the in

the current tax year the yacht Daniel sold the yacht for $60,000. The definition of

personal use asset is given under the “s-108-10 (2), ITA Act 1997”. Under this

definition the personal use asset involves the boats, yacht, vehicles, electronic items

etc. that are under the ownership of taxpayer for their personal enjoyment purpose

(Sadiq and Sawyer 2018). The rule of the personal use asset is that under “s-118-

10 (3), ITA Act 1997” the taxpayer should ignore the capital gains when the cost

base of the asset is lower than $10,000. While the “s-108-20 (1), ITAA 1997” says

that if there is any capital loss suffered from the sale of personal use asset then it is

to be disregarded by the taxpayer.

The case study explains that Daniel reports the capital loss from selling the

yacht. Daniel should note that the yacht is the personal use asset under “s-108-10

(2), ITA Act 1997” (Lawrence 2019). The capital loss that is suffered by Daniel from

selling the yacht must be ignored by him under legislation of “s-108-20 (1), ITAA

1997”.

Sale of Shares:

Daniel has purchased the shares during the year on 10 January 2019 for

$75,000. But the shares were sold for $80,000. An additional cost of stamp duty was

incurred while purchasing the shares and a brokerage fees of $750 was paid while

selling the shares. With respect to “sec 110-35, ITAA 1997” the stamp duty paid for

acquiring the shares were included into the cost base of asset as the incidental cost

(Allerdice 2014). Daniel reports a capital gain from sale of BHP shares. On the other

hand, a carried forward capital loss from previous year of AZJ shares were reported.

The carried forward capital loss is offset against the capital gains from BHP shares.

The leftover loss is carried forward to the subsequent year.

Answer to B:

As evident from the above stated computation it is understood that the capital

gains that were reported by Daniel from the sale of several assets during the year

can be used to fund the retirement fund.

Answer to C:

On the other hand, Daniel also has the loss from disposing the personal use

asset. In other words, loss made from the sale of yacht must be disregarded by

Daniel as it is not allowed for offset. While the AZJ shares left over capital loss

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

should be carried forward to next year and can be only offset against the capital

gains from shares.

should be carried forward to next year and can be only offset against the capital

gains from shares.

8TAXATION LAW

References:

Allerdice, R., 2014. Beneficiary and third party capital dealings. Marks' Trusts &

Estates: Taxation and Practice, p.624.

Antoniades, H., 2015, December. Capital Gains Tax for Real Property: Why is this

tax system so complicated?. In Asian Real Estate Society Conference. AsRES2016.

Arnold, B.R., Bateman, H., Ferguson, A. and Raftery, A., 2014. The size, cost and

asset allocation of Australian self-managed superannuation funds. CIFR Paper,

(033).

Carney, T., 2014. Australia 2013: Heralding Collaborative Welfare & Simplification.

Cortis, N. and Eastman, C., 2015. Salary sacrificing in A ustralia: are patterns of

uptake and benefit different in the not‐for‐profit sector?. Asia Pacific Journal of

Human Resources, 53(3), pp.311-330.

Dabner, J., 2015. Tax Simplification–An Accident Looking for a Place to

Happen?. Available at SSRN 2707910.

Edmonds, R., 2015. Structural tax reform: What should be brought to the

table. Austl. Tax F., 30, p.393.

Harding, M., 2014. Personal tax treatment of company cars and commuting

expenses.

Lawrence, S., 2019. Separate SMSFs for collectables. Taxation in Australia, 53(9),

p.480.

Libson, A., 2014. Taxing Status: Tax Treatment of Mixed Business and Personal

Expenses. U. Pa. J. Bus. L., 17, p.1139.

Maples, A. and Karlinsky, S., 2014. The Australian capital gains tax regime and the

proposed New Zealand CGT: Through Adam Smith's lens. Journal of Australian

Taxation, 16(2), p.156.

Sadiq, K. and Sawyer, A., 2018. New Zealand's Experience with Capital Gains

Taxation and Policy Choice Lessons from Australia. eJTR, 16, p.362.

Sowa, P.M., Kault, S., Byrnes, J., Ng, S.K., Comans, T. and Scuffham, P.A., 2018.

Private health insurance incentives in Australia: in search of cost-effective

adjustments. Applied health economics and health policy, 16(1), pp.31-41.

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation. Australian Resources and

Energy Law Journal, 34(1), p.17.

Walpole, M. and Salter, D., 2014. Regulation of tax agents in Australia. eJTR, 12,

p.335.

Young, W. and Miles, C.F., 2015. A spatial study of parking policy and usage in

Melbourne, Australia. Case Studies on Transport Policy, 3(1), pp.23-32.

References:

Allerdice, R., 2014. Beneficiary and third party capital dealings. Marks' Trusts &

Estates: Taxation and Practice, p.624.

Antoniades, H., 2015, December. Capital Gains Tax for Real Property: Why is this

tax system so complicated?. In Asian Real Estate Society Conference. AsRES2016.

Arnold, B.R., Bateman, H., Ferguson, A. and Raftery, A., 2014. The size, cost and

asset allocation of Australian self-managed superannuation funds. CIFR Paper,

(033).

Carney, T., 2014. Australia 2013: Heralding Collaborative Welfare & Simplification.

Cortis, N. and Eastman, C., 2015. Salary sacrificing in A ustralia: are patterns of

uptake and benefit different in the not‐for‐profit sector?. Asia Pacific Journal of

Human Resources, 53(3), pp.311-330.

Dabner, J., 2015. Tax Simplification–An Accident Looking for a Place to

Happen?. Available at SSRN 2707910.

Edmonds, R., 2015. Structural tax reform: What should be brought to the

table. Austl. Tax F., 30, p.393.

Harding, M., 2014. Personal tax treatment of company cars and commuting

expenses.

Lawrence, S., 2019. Separate SMSFs for collectables. Taxation in Australia, 53(9),

p.480.

Libson, A., 2014. Taxing Status: Tax Treatment of Mixed Business and Personal

Expenses. U. Pa. J. Bus. L., 17, p.1139.

Maples, A. and Karlinsky, S., 2014. The Australian capital gains tax regime and the

proposed New Zealand CGT: Through Adam Smith's lens. Journal of Australian

Taxation, 16(2), p.156.

Sadiq, K. and Sawyer, A., 2018. New Zealand's Experience with Capital Gains

Taxation and Policy Choice Lessons from Australia. eJTR, 16, p.362.

Sowa, P.M., Kault, S., Byrnes, J., Ng, S.K., Comans, T. and Scuffham, P.A., 2018.

Private health insurance incentives in Australia: in search of cost-effective

adjustments. Applied health economics and health policy, 16(1), pp.31-41.

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation. Australian Resources and

Energy Law Journal, 34(1), p.17.

Walpole, M. and Salter, D., 2014. Regulation of tax agents in Australia. eJTR, 12,

p.335.

Young, W. and Miles, C.F., 2015. A spatial study of parking policy and usage in

Melbourne, Australia. Case Studies on Transport Policy, 3(1), pp.23-32.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.