HA3042 Taxation Law T2 2018: Income, Avoidance, and Property Ownership

VerifiedAdded on 2023/06/04

|12

|3274

|462

Report

AI Summary

This assignment provides a detailed analysis of various aspects of taxation law. It addresses the classification of annual payments as income, referencing relevant case law such as Scott v C of T (NSW) and Dixon v FCT. Furthermore, it examines the principle established in IRC v Duke of Westminster regarding tax avoidance schemes and its modern-day implications in Australia. The assignment also delves into the division of net income or loss from rental properties among joint owners, citing Taxation Ruling TR 93/32 and the McDonald v FCT case. The document offers a comprehensive overview of these key areas within taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer to question 1:

Issues:

The issue is related to the classification of yearly payments as having the nature of

income.

Rule:

The ordinary income does not has any definition in the taxation acts. The meaning of

the ordinary income is derived from the case law and is reliant on the principles that emerges

from the decisions. The taxation legislation role is to take into the account the value of

ordinary income in the taxable income given the amount meets the criteria ascertained by the

principles of case laws (Roberts 2017). The sum would be included into the taxable income

under “s 6-5 ITAA”. An individual taxable income comprises of the receipts obtained on the

basis of ordinary meaning that is known as ordinary income.

In “Scott v C of T (NSW) (1935)” the taxation commissioner held that income does

not signifies a term of art as receipts are comprehended inside it (Desai 2013). The court in

“Scott v FCT” stated that whether or not the receipts constitutes income is reliant on the

quality in the recipient’s hands (Baldry 2017). One should denote that there are some

noteworthy standards that demands the taxpayer to consider the receipts as earnings within

the meaning of section 6-5.

Majority of the amounts are easily categorized as ordinary income particularly the

salary and wages as they display the characteristics of recurrence, regularity and periodicity.

Nevertheless, these income should be viewed as the only general characteristics of certain

flow of income. As a matter of fact that the amount received in regular instalments does not

necessarily categorize such receipts as the ordinary income (Kakwani 2017). A receipt is not

categorized as ordinary income unless the receipts is a cash or real gain for the taxpayer. The

Answer to question 1:

Issues:

The issue is related to the classification of yearly payments as having the nature of

income.

Rule:

The ordinary income does not has any definition in the taxation acts. The meaning of

the ordinary income is derived from the case law and is reliant on the principles that emerges

from the decisions. The taxation legislation role is to take into the account the value of

ordinary income in the taxable income given the amount meets the criteria ascertained by the

principles of case laws (Roberts 2017). The sum would be included into the taxable income

under “s 6-5 ITAA”. An individual taxable income comprises of the receipts obtained on the

basis of ordinary meaning that is known as ordinary income.

In “Scott v C of T (NSW) (1935)” the taxation commissioner held that income does

not signifies a term of art as receipts are comprehended inside it (Desai 2013). The court in

“Scott v FCT” stated that whether or not the receipts constitutes income is reliant on the

quality in the recipient’s hands (Baldry 2017). One should denote that there are some

noteworthy standards that demands the taxpayer to consider the receipts as earnings within

the meaning of section 6-5.

Majority of the amounts are easily categorized as ordinary income particularly the

salary and wages as they display the characteristics of recurrence, regularity and periodicity.

Nevertheless, these income should be viewed as the only general characteristics of certain

flow of income. As a matter of fact that the amount received in regular instalments does not

necessarily categorize such receipts as the ordinary income (Kakwani 2017). A receipt is not

categorized as ordinary income unless the receipts is a cash or real gain for the taxpayer. The

2TAXATION LAW

taxpayer must assess any earnings that is received during the year depending upon the factors

relevant in the hands of those that receives it.

Given that both the prerequisites of the income are met, gains will be held as the

ordinary income if the payments holds the adequate characteristics of regular or periodical

receipt or possess the concept of regular flow (Mills, Newberry and Trautman 2015). A gain

that holds the necessary characteristics of regularity or periodicity is more likely regarded as

ordinary earnings than those payments that are paid as lump sum. The federal court in “Blake

v FCT (1984)” characterised regular receipts of payment as an income (Lambert 2015).

Likewise, in “Dixon v FCT (1952)” held that periodical type of payments paid at least

annually in question holds the character of income stream and are regarded as income.

Application:

The lotteries commissioner performs the instant lottery where commission provides

the winner with a payment of $50,000 each every year for 20 years’ time. The first $50,000

was paid soon the notification to the winner is sent while the later the amounts are paid every

year following the first instalment. Mentioning the decision in “Scott v C of T (NSW)

(1935)” it is necessary to determine the nature of annual payment received in the hands of

recipient (Burman, Geissler and Toder 2018). Citing the event of “Scott v FCT” the annual

payment of $50,000 can be easily categorized as ordinary income. This is because the annual

payment of $50,000 involves the characteristics of recurrence, regularity and periodicity. The

payment is made every year to the winner even on the conditions that the outstanding amount

can be paid to the deceased estate if the winner dies.

The annual payment of $50,000 can be categorized as income because the payment is

a real gain for the taxpayer. Denting the event of “Blake v FCT (1984)” the annual payment

of $50,000 meets both the prerequisites of the income as the payments holds the adequate

taxpayer must assess any earnings that is received during the year depending upon the factors

relevant in the hands of those that receives it.

Given that both the prerequisites of the income are met, gains will be held as the

ordinary income if the payments holds the adequate characteristics of regular or periodical

receipt or possess the concept of regular flow (Mills, Newberry and Trautman 2015). A gain

that holds the necessary characteristics of regularity or periodicity is more likely regarded as

ordinary earnings than those payments that are paid as lump sum. The federal court in “Blake

v FCT (1984)” characterised regular receipts of payment as an income (Lambert 2015).

Likewise, in “Dixon v FCT (1952)” held that periodical type of payments paid at least

annually in question holds the character of income stream and are regarded as income.

Application:

The lotteries commissioner performs the instant lottery where commission provides

the winner with a payment of $50,000 each every year for 20 years’ time. The first $50,000

was paid soon the notification to the winner is sent while the later the amounts are paid every

year following the first instalment. Mentioning the decision in “Scott v C of T (NSW)

(1935)” it is necessary to determine the nature of annual payment received in the hands of

recipient (Burman, Geissler and Toder 2018). Citing the event of “Scott v FCT” the annual

payment of $50,000 can be easily categorized as ordinary income. This is because the annual

payment of $50,000 involves the characteristics of recurrence, regularity and periodicity. The

payment is made every year to the winner even on the conditions that the outstanding amount

can be paid to the deceased estate if the winner dies.

The annual payment of $50,000 can be categorized as income because the payment is

a real gain for the taxpayer. Denting the event of “Blake v FCT (1984)” the annual payment

of $50,000 meets both the prerequisites of the income as the payments holds the adequate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

characteristics of regular, periodical receipt and owns the concept of regular flow (Allingham

and Sandmo 2013). Henceforth, quoting the event of “Dixon v FCT (1952)” the annual

payment of $50,000 is periodical type of payments which is paid at least annually in question.

The payment holds the character of income stream and should observed as income.

Conclusion:

Annual payment that is paid at each of the 12 months period to the taxpayer is holding

the feature of income. It is necessary to settle that the sum is an income in the hands of the

recipient.

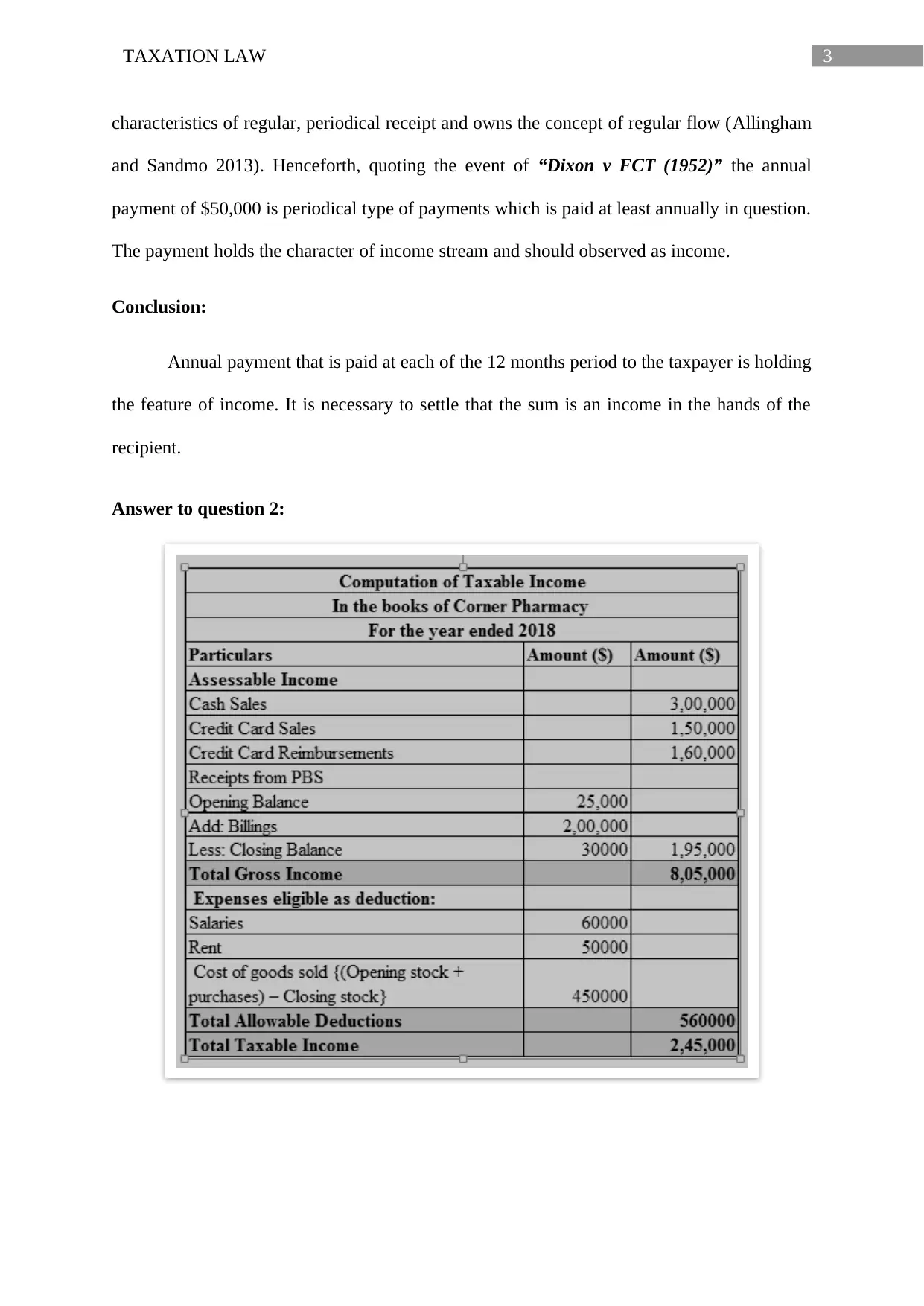

Answer to question 2:

characteristics of regular, periodical receipt and owns the concept of regular flow (Allingham

and Sandmo 2013). Henceforth, quoting the event of “Dixon v FCT (1952)” the annual

payment of $50,000 is periodical type of payments which is paid at least annually in question.

The payment holds the character of income stream and should observed as income.

Conclusion:

Annual payment that is paid at each of the 12 months period to the taxpayer is holding

the feature of income. It is necessary to settle that the sum is an income in the hands of the

recipient.

Answer to question 2:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to question 3:

IRC v Duke of Westminster [1936]

In this case there is an event of avoidance of tax that occurred when the duke made a

false covenant. The duke recruited the gardener to pay from his after tax profits having

substantial in nature.

In the attempt of reducing the tax, the “Duke of the Westminster” stopped paying the

wage of the gardener and rather drew up a solemn promise of paying the equal sum of

amount following the end of the specified period (Fox and Campbell 2014). With respect to

the tax laws of that time, this enabled the duke in reducing the income tax liability by

claiming a deduction for the expenses. This ultimately helped the Duke in reducing his

liability for the purpose of income tax and surtax (Christiansen 2014). The department of

Inland Revenue however challenged the case by stating that arrangement was

“tantamounting” towards the evasion of taxation and ultimately took the “Duke of the

Westminster” to the court. They department of Inland Revenue eventually lost their case.

The principle stated that an individual is entitled within the legislation to organize

their affairs of taxation in a manner so that they can reduce their liability of taxation. The

government and the ministers have criticized publicly with the help of well-known

entertainers and larger multinational corporations that acted completely within the law as the

attempt of reducing their liability of taxation (Yi and Haifeng 2014). The principles

established in the case of “Duke of the Westminster” is no longer inviolable. The court of

law has increasingly implemented the purposive interpretation to defeat the tax avoidance

scheme of artificial arrangement.

The attempt of Duke in reducing his tax surtax bill will now be treated by several as

the unacceptable and morally objectionable. The judicial interpretation of this case states that

Answer to question 3:

IRC v Duke of Westminster [1936]

In this case there is an event of avoidance of tax that occurred when the duke made a

false covenant. The duke recruited the gardener to pay from his after tax profits having

substantial in nature.

In the attempt of reducing the tax, the “Duke of the Westminster” stopped paying the

wage of the gardener and rather drew up a solemn promise of paying the equal sum of

amount following the end of the specified period (Fox and Campbell 2014). With respect to

the tax laws of that time, this enabled the duke in reducing the income tax liability by

claiming a deduction for the expenses. This ultimately helped the Duke in reducing his

liability for the purpose of income tax and surtax (Christiansen 2014). The department of

Inland Revenue however challenged the case by stating that arrangement was

“tantamounting” towards the evasion of taxation and ultimately took the “Duke of the

Westminster” to the court. They department of Inland Revenue eventually lost their case.

The principle stated that an individual is entitled within the legislation to organize

their affairs of taxation in a manner so that they can reduce their liability of taxation. The

government and the ministers have criticized publicly with the help of well-known

entertainers and larger multinational corporations that acted completely within the law as the

attempt of reducing their liability of taxation (Yi and Haifeng 2014). The principles

established in the case of “Duke of the Westminster” is no longer inviolable. The court of

law has increasingly implemented the purposive interpretation to defeat the tax avoidance

scheme of artificial arrangement.

The attempt of Duke in reducing his tax surtax bill will now be treated by several as

the unacceptable and morally objectionable. The judicial interpretation of this case states that

5TAXATION LAW

if the legislation seems to be ambiguous the court of law might look at the record of the

parliamentary proceedings for the clear indication by the legislation promoter as its intended

meaning (Boortz and Linder 2015). As the matter of fact, the court of law has regularly

casted a sceptical view over the contrived tax avoidance scheme. The court has since then not

hesitated to scrutinise the facts to understand whether they stand up or implement the

purposive interpretation.

In the case of “Duke of the Westminster” the problem was prevalent on whether the

solemn promise or in other words the deed of covenant may be viewed or treated as the

employment contract (Perotti 2013). Furthermore, the “Duke of the Westminster” was

neither paying the gardeners and the servants a weekly wage nor did the Duke paid any

monthly salary based on the employment contract which the Duke intended to pay. Although

the principles that was established in the case of Duke was attractive for others in seeking tax

avoidance lawfully by establishing complex structures, but since then it has been weakened

by the subsequent cases where the court of law have viewed into the overall effect of the

transactions.

The “Duke of the Westminster” case provides the readers with the suggestion that tax

avoidance may be treated as the allowable until it adheres with the statute law that is

established (Mills 2018). In the case of Duke, the basic principles of the deed of covenant

was the format of the deed that can lower down the liability of the taxation.

Taking into the account the relevancy of principle that was established in the case of

Duke in the modern age of Australia the principle is not any more inviolable (Stiglitz 2015).

The government of Australian have increasingly implemented the purposive interpretation

with the objective of defeating the schemes of artificial tax avoidance. The measures of tax

if the legislation seems to be ambiguous the court of law might look at the record of the

parliamentary proceedings for the clear indication by the legislation promoter as its intended

meaning (Boortz and Linder 2015). As the matter of fact, the court of law has regularly

casted a sceptical view over the contrived tax avoidance scheme. The court has since then not

hesitated to scrutinise the facts to understand whether they stand up or implement the

purposive interpretation.

In the case of “Duke of the Westminster” the problem was prevalent on whether the

solemn promise or in other words the deed of covenant may be viewed or treated as the

employment contract (Perotti 2013). Furthermore, the “Duke of the Westminster” was

neither paying the gardeners and the servants a weekly wage nor did the Duke paid any

monthly salary based on the employment contract which the Duke intended to pay. Although

the principles that was established in the case of Duke was attractive for others in seeking tax

avoidance lawfully by establishing complex structures, but since then it has been weakened

by the subsequent cases where the court of law have viewed into the overall effect of the

transactions.

The “Duke of the Westminster” case provides the readers with the suggestion that tax

avoidance may be treated as the allowable until it adheres with the statute law that is

established (Mills 2018). In the case of Duke, the basic principles of the deed of covenant

was the format of the deed that can lower down the liability of the taxation.

Taking into the account the relevancy of principle that was established in the case of

Duke in the modern age of Australia the principle is not any more inviolable (Stiglitz 2015).

The government of Australian have increasingly implemented the purposive interpretation

with the objective of defeating the schemes of artificial tax avoidance. The measures of tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

avoidance can be viewed as the measure of avoiding a person’s duty towards the general

public by simply not lending support to the government.

Presently in Australia, the taxpayers that holds the intention of mitigating tax are

walking on the thin ice. This is because there is only a thin line present between the tax

avoidance and tax evasion (Hellerstein 2013). The taxpayers presently in Australia should be

careful at the time of drafting the tax mitigation plans as the government of Australia

currently making an attempt of linking the tax avoidance and the tax evasion together.

Answer to question 4:

Issue:

The issue here will take into the consideration for the purpose of income tax, dividing

of net income or the loss made from the rental property amid the joint owners of that rental

property.

Rule:

A noteworthy explanation has been provided in “Taxation Ruling TR 93/32”

regarding the dividing of rental property net income and net loss between the joint owners

(Lambert and Pfähler 2015). An explanation has been provided under this ruling on the basis

of which the commissioner accepts dividing of rental property net profit and loss for the

purpose of taxation between the joint owners of the rental property.

A husband and wife that are holding the property of rental nature will be accountable

for income tax purpose only but are not viewed as the partners under the common law (Pfahle

2017). Where it is noticed that the joint-ownership amounts to partnership for the purpose of

income tax solely, the profits and loss obtained from the rental property is obtained from the

avoidance can be viewed as the measure of avoiding a person’s duty towards the general

public by simply not lending support to the government.

Presently in Australia, the taxpayers that holds the intention of mitigating tax are

walking on the thin ice. This is because there is only a thin line present between the tax

avoidance and tax evasion (Hellerstein 2013). The taxpayers presently in Australia should be

careful at the time of drafting the tax mitigation plans as the government of Australia

currently making an attempt of linking the tax avoidance and the tax evasion together.

Answer to question 4:

Issue:

The issue here will take into the consideration for the purpose of income tax, dividing

of net income or the loss made from the rental property amid the joint owners of that rental

property.

Rule:

A noteworthy explanation has been provided in “Taxation Ruling TR 93/32”

regarding the dividing of rental property net income and net loss between the joint owners

(Lambert and Pfähler 2015). An explanation has been provided under this ruling on the basis

of which the commissioner accepts dividing of rental property net profit and loss for the

purpose of taxation between the joint owners of the rental property.

A husband and wife that are holding the property of rental nature will be accountable

for income tax purpose only but are not viewed as the partners under the common law (Pfahle

2017). Where it is noticed that the joint-ownership amounts to partnership for the purpose of

income tax solely, the profits and loss obtained from the rental property is obtained from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

joint ownership of the property and does not amounts to distributing of partnership profit and

loss.

As co-owners are not the partners under the common law they must share the rental

income in respect to the income tax purpose. Instead, any partnership settlement either oral or

writing it does not have any influence on the distribution of the rental profit net loss and net

loss (Hemming and Keen 2013). Accordingly, the income or loss obtained from the rental

property should be shared based on the legal interest of the owners particularly in those

situations where an adequate evidence is available to establish that the equitable interest is

different from the lawful interest.

As per the paragraph 9 of the “Taxation Ruling TR 93/32” the rental property joint

owners would usually hold the property as the joint owners or tenants in common.

Furthermore, paragraph 11 of the “Taxation Ruling TR 93/32” states that the feature of joint

tenants and tenants in common represents the legal interest of the tenant (Mills and Newberry

2015). Nevertheless, the legal interest ultimately ascertains between the joint owners the

dividing of net income and loss obtained from the property. These occupancies falls under the

definition of the joint owners. There is a lawful interest of legal type to share the equitable

interest between the property holders. The holders of the tenancies properties are under the

definition held as the co-owners where the allocation of the tenancies profits should equal

among both the partners.

The McDonald’s Case provides an explanation regarding the joint owners of the

rental property that falls within the definition of partnership for income tax purpose. In the

case of “McDonald v FCT”, Mr McDonald and his wife jointly owned the two units which

the couple rented out (Pfahle 2017). The agreement of sharing the net profit is based on the

ratio of 25:75. In other words, Mr McDonald would be entitled to 25% of the share whereas

joint ownership of the property and does not amounts to distributing of partnership profit and

loss.

As co-owners are not the partners under the common law they must share the rental

income in respect to the income tax purpose. Instead, any partnership settlement either oral or

writing it does not have any influence on the distribution of the rental profit net loss and net

loss (Hemming and Keen 2013). Accordingly, the income or loss obtained from the rental

property should be shared based on the legal interest of the owners particularly in those

situations where an adequate evidence is available to establish that the equitable interest is

different from the lawful interest.

As per the paragraph 9 of the “Taxation Ruling TR 93/32” the rental property joint

owners would usually hold the property as the joint owners or tenants in common.

Furthermore, paragraph 11 of the “Taxation Ruling TR 93/32” states that the feature of joint

tenants and tenants in common represents the legal interest of the tenant (Mills and Newberry

2015). Nevertheless, the legal interest ultimately ascertains between the joint owners the

dividing of net income and loss obtained from the property. These occupancies falls under the

definition of the joint owners. There is a lawful interest of legal type to share the equitable

interest between the property holders. The holders of the tenancies properties are under the

definition held as the co-owners where the allocation of the tenancies profits should equal

among both the partners.

The McDonald’s Case provides an explanation regarding the joint owners of the

rental property that falls within the definition of partnership for income tax purpose. In the

case of “McDonald v FCT”, Mr McDonald and his wife jointly owned the two units which

the couple rented out (Pfahle 2017). The agreement of sharing the net profit is based on the

ratio of 25:75. In other words, Mr McDonald would be entitled to 25% of the share whereas

8TAXATION LAW

Mrs McDonald takes 75% of the share of profits. Further conditions included that Mr

McDonald would bear the 100% of the rental property loss. The court of law contented that

both Mr and Mrs McDonald cannot be treated as partners under the general law since they

were simply the joint owners and the losses must be shared on equal basis.

Applications:

The evidences noted from this case states that Joseph was the accountant while his

wife Jane a housewife borrowed a sum of money to purchase the rental property. The

agreement between Joseph and Jane included that they would be sharing the profit at a ratio

of 20:80. In other words Joseph would be sharing only 20% of the net profit and 80% of the

rental profits would be kept by Jane.

The tenancies of the rental possession that is held by the couple in the present case

represents the co-owners. They are only partners for the purpose of the taxation but cannot be

regarded as the partners as per the partnership act. As an alternative, any partnership

settlement either oral and in writing does not have any influence on the distribution of the

rental profit net loss and net loss between Joseph and Jane.

Accordingly, the income or loss obtained from the rental property should be shared

based on the legal interest of Joseph and Jane. Citing paragraph 9 of the Taxation Ruling TR

93/32 both Joseph and Jane would should be viewed as the joint owners or tenants in

common. Such kind of tenancies between Joseph and Jane are in addition classified as the co-

owner’s interest.

Citing the reference of “McDonald v FCT” the partnership between Joseph and Jane

constituted partnership under the income tax purpose and not under the general law (Mills

and Newberry 2015). The analysis clearly explains that there was no partnership between

Mrs McDonald takes 75% of the share of profits. Further conditions included that Mr

McDonald would bear the 100% of the rental property loss. The court of law contented that

both Mr and Mrs McDonald cannot be treated as partners under the general law since they

were simply the joint owners and the losses must be shared on equal basis.

Applications:

The evidences noted from this case states that Joseph was the accountant while his

wife Jane a housewife borrowed a sum of money to purchase the rental property. The

agreement between Joseph and Jane included that they would be sharing the profit at a ratio

of 20:80. In other words Joseph would be sharing only 20% of the net profit and 80% of the

rental profits would be kept by Jane.

The tenancies of the rental possession that is held by the couple in the present case

represents the co-owners. They are only partners for the purpose of the taxation but cannot be

regarded as the partners as per the partnership act. As an alternative, any partnership

settlement either oral and in writing does not have any influence on the distribution of the

rental profit net loss and net loss between Joseph and Jane.

Accordingly, the income or loss obtained from the rental property should be shared

based on the legal interest of Joseph and Jane. Citing paragraph 9 of the Taxation Ruling TR

93/32 both Joseph and Jane would should be viewed as the joint owners or tenants in

common. Such kind of tenancies between Joseph and Jane are in addition classified as the co-

owner’s interest.

Citing the reference of “McDonald v FCT” the partnership between Joseph and Jane

constituted partnership under the income tax purpose and not under the general law (Mills

and Newberry 2015). The analysis clearly explains that there was no partnership between

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Joseph and Jane at the general law because they are simply the joint owners and their loss of

$40,000 must be shared in the equal basis.

As the alternative to the situation, if Joseph and Jane makes the decision of selling

rental property any capital gains or loss made from such sale should be divided in their legal

equitable interest (Pfahle 2017). It is noteworthy to denote that the personal arrangement

between Joseph and his spouse as to their distribution of net capital gains or loss, do not have

any influence for their respective entitlements for the purpose of income tax. In other words

the profits and losses should be shares on equal basis.

Conclusion:

The analysis supports the conclusion that any agreement between Joseph and Jane for

the division of income and loss in proportion apart from their equal share does not has any

impact for the purpose of income tax.

Joseph and Jane at the general law because they are simply the joint owners and their loss of

$40,000 must be shared in the equal basis.

As the alternative to the situation, if Joseph and Jane makes the decision of selling

rental property any capital gains or loss made from such sale should be divided in their legal

equitable interest (Pfahle 2017). It is noteworthy to denote that the personal arrangement

between Joseph and his spouse as to their distribution of net capital gains or loss, do not have

any influence for their respective entitlements for the purpose of income tax. In other words

the profits and losses should be shares on equal basis.

Conclusion:

The analysis supports the conclusion that any agreement between Joseph and Jane for

the division of income and loss in proportion apart from their equal share does not has any

impact for the purpose of income tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Allingham, M.G. and Sandmo, A., 2013. Income tax evasion: A.

Baldry, J.C., 2017. Income tax evasion and the tax schedule: Some experimental

results. Public Finance= Finances publiques, 42(3), pp.357-383.

Boortz, N. and Linder, J., 2015. The FairTax Book: Saying Goodbye to the Income Tax and

the IRS. New York: Regan Books.

Burman, L.E., Geissler, C. and Toder, E.J., 2018. How big are total individual income tax

expenditures, and who benefits from them?. American Economic Review, 98(2), pp.79-83.

Christiansen, V., 2014. Two comments on tax evasion. Journal of Public Economics, 13(3),

pp.389-393.

Desai, M.A., 2013. The divergence between book income and tax income. Tax policy and the

economy, 17, pp.169-206.

Fox, W.F. and Campbell, C., 2014. Stability of the state sales tax income elasticity. National

Tax Journal, pp.201-212.

Hellerstein, W., 2013. Jurisdiction to Tax Income and Consumption in the New Economy: A

Theoretical and Comparative Perspective. Ga. L. Rev., 38, p.1.

Hemming, R. and Keen, M.J., 2013. Single-crossing conditions in comparisons of tax

progressivity. Journal of Public Economics, 20(3), pp.373-380.

Kakwani, N.C., 2017. Measurement of tax progressivity: an international comparison. The

Economic Journal, 87(345), pp.71-80.

Lambert, P. and Pfähler, W., 2015. Income tax progression and redistributive effect.

References:

Allingham, M.G. and Sandmo, A., 2013. Income tax evasion: A.

Baldry, J.C., 2017. Income tax evasion and the tax schedule: Some experimental

results. Public Finance= Finances publiques, 42(3), pp.357-383.

Boortz, N. and Linder, J., 2015. The FairTax Book: Saying Goodbye to the Income Tax and

the IRS. New York: Regan Books.

Burman, L.E., Geissler, C. and Toder, E.J., 2018. How big are total individual income tax

expenditures, and who benefits from them?. American Economic Review, 98(2), pp.79-83.

Christiansen, V., 2014. Two comments on tax evasion. Journal of Public Economics, 13(3),

pp.389-393.

Desai, M.A., 2013. The divergence between book income and tax income. Tax policy and the

economy, 17, pp.169-206.

Fox, W.F. and Campbell, C., 2014. Stability of the state sales tax income elasticity. National

Tax Journal, pp.201-212.

Hellerstein, W., 2013. Jurisdiction to Tax Income and Consumption in the New Economy: A

Theoretical and Comparative Perspective. Ga. L. Rev., 38, p.1.

Hemming, R. and Keen, M.J., 2013. Single-crossing conditions in comparisons of tax

progressivity. Journal of Public Economics, 20(3), pp.373-380.

Kakwani, N.C., 2017. Measurement of tax progressivity: an international comparison. The

Economic Journal, 87(345), pp.71-80.

Lambert, P. and Pfähler, W., 2015. Income tax progression and redistributive effect.

11TAXATION LAW

Lambert, P.J., 2015. The distribution and redistribution of income. In Current issues in

public sector economics (pp. 200-226). Palgrave, London.

Mills, L., Newberry, K. and Trautman, W., 2015. Trends in book-tax income and balance

sheet differences.

Mills, L.F. and Newberry, K.J., 2015. The influence of tax and nontax costs on book-tax

reporting differences: Public and private firms. Journal of the American Taxation

Association, 23(1), pp.1-19.

Mills, L.F., 2018. Book-tax differences and Internal Revenue Service adjustments. Journal of

Accounting research, 36(2), pp.343-356.

Perotti, R., 2013. Political equilibrium, income distribution, and growth. The Review of

Economic Studies, 60(4), pp.755-776.

Pfahler, W., 2017. Redistributive effects of tax progressivity: evaluating a general class of

aggregate measures. Public Finance= Finances publiques, 42(1), pp.1-31.

Roberts, K.W., 2017. Voting over income tax schedules. Journal of public Economics, 8(3),

pp.329-340.

Stiglitz, J.E., 2015. The effects of income, wealth, and capital gains taxation on risk-taking.

In Stochastic Optimization Models in Finance (pp. 291-311).

Yi, L. and Haifeng, N., 2014. The Effect of Indirect Tax Incidence on Income Distribution

[J]. Economic Research Journal, 5, p.002.

Lambert, P.J., 2015. The distribution and redistribution of income. In Current issues in

public sector economics (pp. 200-226). Palgrave, London.

Mills, L., Newberry, K. and Trautman, W., 2015. Trends in book-tax income and balance

sheet differences.

Mills, L.F. and Newberry, K.J., 2015. The influence of tax and nontax costs on book-tax

reporting differences: Public and private firms. Journal of the American Taxation

Association, 23(1), pp.1-19.

Mills, L.F., 2018. Book-tax differences and Internal Revenue Service adjustments. Journal of

Accounting research, 36(2), pp.343-356.

Perotti, R., 2013. Political equilibrium, income distribution, and growth. The Review of

Economic Studies, 60(4), pp.755-776.

Pfahler, W., 2017. Redistributive effects of tax progressivity: evaluating a general class of

aggregate measures. Public Finance= Finances publiques, 42(1), pp.1-31.

Roberts, K.W., 2017. Voting over income tax schedules. Journal of public Economics, 8(3),

pp.329-340.

Stiglitz, J.E., 2015. The effects of income, wealth, and capital gains taxation on risk-taking.

In Stochastic Optimization Models in Finance (pp. 291-311).

Yi, L. and Haifeng, N., 2014. The Effect of Indirect Tax Incidence on Income Distribution

[J]. Economic Research Journal, 5, p.002.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.