Taxation Law of Australia Assignment: Case Studies and Analysis

VerifiedAdded on 2020/02/18

|12

|3170

|44

Homework Assignment

AI Summary

This document presents a comprehensive solution to an Australian Taxation Law assignment. It addresses two key questions, providing detailed advice on the tax treatment of various items under Australian tax law, such as flyer points, property damage payments, holiday packages, and travel expenses. The assignment analyzes each scenario, referencing relevant Australian tax rulings and legislation to support the advice. Furthermore, the solution includes the calculation of an individual's taxable income for the 2016/17 financial year, incorporating gross salary, foreign income, and deductions. The analysis covers key concepts like taxable income, deductions, fringe benefits tax, and capital assets, offering practical insights into the application of Australian tax law. The document incorporates citations to relevant academic and professional sources.

Running head: TAXATION LAW OF AUSTRALIA

Taxation law of Australia

Name of the University:

Name of the Student:

Authors Note:

Taxation law of Australia

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW OF AUSTRALIA

Table of Contents

Question 1: Providing relevant advice to client for the following items, which could be

treated for tax purposes under Australian Tax Law...................................................................2

Answer to i) Receiving flyer point from Webjet.......................................................................2

Answer to ii) Received property damage payment from customer............................................2

Answer to iii) Nightclub manager receiving holiday package from alcohol supplier...............3

Answer to iv) Funds being returned to Canoe club members....................................................3

Answer to v) Payment received by footballer from television company...................................4

Answer to vi) Expenses related to building apprentices............................................................4

Answer to vii) Short course expenses conducted to become Art Director................................5

Answer to viii) Expenses conducted on makeup and dresses....................................................5

Answer to ix) Expenses conducted from travelling to office from home..................................6

Answer to x) Expenses conducted in travel between one employer to another.........................6

Question 2: Manpreet’s Taxable income for the year 2016/17 financial year...........................7

Reference and Bibliography:....................................................................................................10

TAXATION LAW OF AUSTRALIA

Table of Contents

Question 1: Providing relevant advice to client for the following items, which could be

treated for tax purposes under Australian Tax Law...................................................................2

Answer to i) Receiving flyer point from Webjet.......................................................................2

Answer to ii) Received property damage payment from customer............................................2

Answer to iii) Nightclub manager receiving holiday package from alcohol supplier...............3

Answer to iv) Funds being returned to Canoe club members....................................................3

Answer to v) Payment received by footballer from television company...................................4

Answer to vi) Expenses related to building apprentices............................................................4

Answer to vii) Short course expenses conducted to become Art Director................................5

Answer to viii) Expenses conducted on makeup and dresses....................................................5

Answer to ix) Expenses conducted from travelling to office from home..................................6

Answer to x) Expenses conducted in travel between one employer to another.........................6

Question 2: Manpreet’s Taxable income for the year 2016/17 financial year...........................7

Reference and Bibliography:....................................................................................................10

2

TAXATION LAW OF AUSTRALIA

Question 1: Providing relevant advice to client for the following items, which could be

treated for tax purposes under Australian Tax Law

Answer to i) Receiving flyer point from Webjet

The situation mainly defects that there is relevant benefits provided to a business

analyst flying regularly from Webjet. Under the normal circumstances these overall benefits

that are provided by airline companies are not considered under taxable income, as stated in

Taxation Ruling of TR 1999/6. However, the Australian taxation ruling also states that there

is some criteria’s, which needs to be met before allowing the expense as tax exemption. The

overall benefit that is provided by Webjet is not considered under taxable income or Fringe

benefit tax, until and unless these factors are proved (Bird and Zolt 2014.). There is a relation

between employer and employee when they could be considered as a family. In addition, if

the overall reward points is provided to the employee in terms of his/her employment

agreement. Lastly, the flight points provided by Webjet are under a particular arrangement.

However, evaluation of the scenario mainly states that there is no agreement between the

employee and Webjet or the employer and Webjet, which directly excludes the benefit from

taxable income.

Answer to ii) Received property damage payment from customer

The situation mainly states that relevant compensation is been received by the

company from a customer for damages conducted on its Capital Asset. According to the

Australian taxation law, the overall damage payment that is conducted on capital assets

cannot be considered under Taxable income. Furthermore there are certain criteria that need

to be followed by an organisation for not including the damage payment of capital assets as

their capital income (Lang 2014). Firstly, the assets should be used by the organisation

TAXATION LAW OF AUSTRALIA

Question 1: Providing relevant advice to client for the following items, which could be

treated for tax purposes under Australian Tax Law

Answer to i) Receiving flyer point from Webjet

The situation mainly defects that there is relevant benefits provided to a business

analyst flying regularly from Webjet. Under the normal circumstances these overall benefits

that are provided by airline companies are not considered under taxable income, as stated in

Taxation Ruling of TR 1999/6. However, the Australian taxation ruling also states that there

is some criteria’s, which needs to be met before allowing the expense as tax exemption. The

overall benefit that is provided by Webjet is not considered under taxable income or Fringe

benefit tax, until and unless these factors are proved (Bird and Zolt 2014.). There is a relation

between employer and employee when they could be considered as a family. In addition, if

the overall reward points is provided to the employee in terms of his/her employment

agreement. Lastly, the flight points provided by Webjet are under a particular arrangement.

However, evaluation of the scenario mainly states that there is no agreement between the

employee and Webjet or the employer and Webjet, which directly excludes the benefit from

taxable income.

Answer to ii) Received property damage payment from customer

The situation mainly states that relevant compensation is been received by the

company from a customer for damages conducted on its Capital Asset. According to the

Australian taxation law, the overall damage payment that is conducted on capital assets

cannot be considered under Taxable income. Furthermore there are certain criteria that need

to be followed by an organisation for not including the damage payment of capital assets as

their capital income (Lang 2014). Firstly, the assets should be used by the organisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW OF AUSTRALIA

thoroughly, which directly reduces the overall taxable income. The second measure mainly

states that the Capital Asset is adequately listed in the annual report where adequate

depreciation is been conducted. This measure is relevantly important, as it allows the

Australian taxation authority to understand that the Capital Asset has been used by the

organisation for more than one fiscal year.

Answer to iii) Nightclub manager receiving holiday package from alcohol supplier

The scenario mainly states that relevant holiday package is been provided to the

nightclub manager by the supplier of alcohol. This relevant Arrangement mainly states that

the benefit or gift provided by the alcohol supplier is relatively higher in value. According to

the Australian taxation authority, low budget gifts exempted from the taxable income,

whereas High Budget gifts are directly included into the taxable income. This mainly helps in

reducing the any kind of unethical measures that is conducted by employees and owners.

Moreover, the scenario mainly states that holiday package has higher value, where the night

club manager needs to add the benefit to its taxable income. in the Australian taxation office

the measure mainly states that any gift that could be considered as amount of cash paid to the

individual is considered under the taxable amount. Novikov, Ling and Kordzakhia (2014)

stated that individual employees getting benefit from their employers are mainly considered

as fringe benefit tax which is paid by the employer.

Answer to iv) Funds being returned to Canoe club members

The situation mainly states that relevant fund is being returned to the Canoe Club

Members, as excess money was being collected. This return of money from the Canoe Club

is mainly a refund and cannot be considered as an income of the members. As per the

Australian taxation law, any kind of expenses that are conducted on clubs for personal

entertainment are not deductible in nature (Davis et al. 2015). Therefore, the overall return of

TAXATION LAW OF AUSTRALIA

thoroughly, which directly reduces the overall taxable income. The second measure mainly

states that the Capital Asset is adequately listed in the annual report where adequate

depreciation is been conducted. This measure is relevantly important, as it allows the

Australian taxation authority to understand that the Capital Asset has been used by the

organisation for more than one fiscal year.

Answer to iii) Nightclub manager receiving holiday package from alcohol supplier

The scenario mainly states that relevant holiday package is been provided to the

nightclub manager by the supplier of alcohol. This relevant Arrangement mainly states that

the benefit or gift provided by the alcohol supplier is relatively higher in value. According to

the Australian taxation authority, low budget gifts exempted from the taxable income,

whereas High Budget gifts are directly included into the taxable income. This mainly helps in

reducing the any kind of unethical measures that is conducted by employees and owners.

Moreover, the scenario mainly states that holiday package has higher value, where the night

club manager needs to add the benefit to its taxable income. in the Australian taxation office

the measure mainly states that any gift that could be considered as amount of cash paid to the

individual is considered under the taxable amount. Novikov, Ling and Kordzakhia (2014)

stated that individual employees getting benefit from their employers are mainly considered

as fringe benefit tax which is paid by the employer.

Answer to iv) Funds being returned to Canoe club members

The situation mainly states that relevant fund is being returned to the Canoe Club

Members, as excess money was being collected. This return of money from the Canoe Club

is mainly a refund and cannot be considered as an income of the members. As per the

Australian taxation law, any kind of expenses that are conducted on clubs for personal

entertainment are not deductible in nature (Davis et al. 2015). Therefore, the overall return of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW OF AUSTRALIA

funds cannot be displayed as an additional income received by the members of Canoe Club.

Thus, under the taxation law of Australia, the return of funds will not be considered under the

taxable income of the Canoe Club members.

Answer to v) Payment received by footballer from television company

Television Company has directly paid a sports person for participating in the sports

field honestly, under the circumstances the sportsperson is liable to add the money in its

taxable income. This situation is mainly stated under the Taxation Ruling TR 1999/17, where

it is depicted that any kind of benefits that is obtained by a sports person in Australia will

directly be considered as taxable income. Therefore according to the ruling the sport person

has to include the benefits provided by the television company in its taxable income and

relevant access to the Australian government. Petty et al. (2015) stated that taxation measure

is mainly used in reducing any kind of unethical measures conducted by an individual to

reduce taxable income.

Answer to vi) Expenses related to building apprentices

The situation many states that overall expenses are been conducted in the building,

where relevant expenses is been considered from the apprentice. In accordance with the

Australian taxation law, the situation mainly states that apprentice is directly considered

under the compensation of building labour. The measures that are used in identifying the

expenses of building are depicted under the taxation ruling of TR 95/22, where relevant

expenses and compensation are directly disclosed. According to the taxation rule relevant

expenses needs to be considered before identifying the apprentice as a building employee

(Ross, Walker and Walker 2017). The first measure mainly states that construction site is

considered when a supervisor work is being conducted on the premises. The second measure

states that labours were employed for building the premises is considered to be an employee.

TAXATION LAW OF AUSTRALIA

funds cannot be displayed as an additional income received by the members of Canoe Club.

Thus, under the taxation law of Australia, the return of funds will not be considered under the

taxable income of the Canoe Club members.

Answer to v) Payment received by footballer from television company

Television Company has directly paid a sports person for participating in the sports

field honestly, under the circumstances the sportsperson is liable to add the money in its

taxable income. This situation is mainly stated under the Taxation Ruling TR 1999/17, where

it is depicted that any kind of benefits that is obtained by a sports person in Australia will

directly be considered as taxable income. Therefore according to the ruling the sport person

has to include the benefits provided by the television company in its taxable income and

relevant access to the Australian government. Petty et al. (2015) stated that taxation measure

is mainly used in reducing any kind of unethical measures conducted by an individual to

reduce taxable income.

Answer to vi) Expenses related to building apprentices

The situation many states that overall expenses are been conducted in the building,

where relevant expenses is been considered from the apprentice. In accordance with the

Australian taxation law, the situation mainly states that apprentice is directly considered

under the compensation of building labour. The measures that are used in identifying the

expenses of building are depicted under the taxation ruling of TR 95/22, where relevant

expenses and compensation are directly disclosed. According to the taxation rule relevant

expenses needs to be considered before identifying the apprentice as a building employee

(Ross, Walker and Walker 2017). The first measure mainly states that construction site is

considered when a supervisor work is being conducted on the premises. The second measure

states that labours were employed for building the premises is considered to be an employee.

5

TAXATION LAW OF AUSTRALIA

The third measure states that relevant trainees, apprentice, and carpenters are considered

under the employed labours. Moreover, a construction site is also considered where project

manager is employed for completing and conducting relevant measures for the construction

of the building.

Thus, from the evaluation it could be understood that expenses conducted on

apprentice is considered as an labour compensation for the building and can be deducted in

the annual report.

Answer to vii) Short course expenses conducted to become Art Director

Expenses is been conducted on short term course for becoming an art director, which

has a relevant provisions in the Australian taxation office. Short course that is used by an

individual to enhance his career in the short time is mainly considered to be tax deductible

expense. This type of tax deductible expense is only considered when the study courses is

short, for long study courses there is no exceptions in the taxable income. Moreover relevant

measures as depicted by the Australian taxation office need to be evaluated by the taxable

person (Taylor and Richardson 2013). Then relevant education module and software for the

course needs to be used. In addition, fees for the course need to be for short duration have

relevant meals and travel expenses should be included. These measures are provided by

Australian taxation office needs to be evaluated before using the short term course, as a tax

deductible expense. Therefore, relevant tax deduction is conducted by the art director, which

helps in reducing the taxable income.

Answer to viii) Expenses conducted on makeup and dresses

There are relevant expenses conducted on both makeup and dresses on an individual,

which is a deductible in nature as mentioned by the Australian taxation office. However,

TAXATION LAW OF AUSTRALIA

The third measure states that relevant trainees, apprentice, and carpenters are considered

under the employed labours. Moreover, a construction site is also considered where project

manager is employed for completing and conducting relevant measures for the construction

of the building.

Thus, from the evaluation it could be understood that expenses conducted on

apprentice is considered as an labour compensation for the building and can be deducted in

the annual report.

Answer to vii) Short course expenses conducted to become Art Director

Expenses is been conducted on short term course for becoming an art director, which

has a relevant provisions in the Australian taxation office. Short course that is used by an

individual to enhance his career in the short time is mainly considered to be tax deductible

expense. This type of tax deductible expense is only considered when the study courses is

short, for long study courses there is no exceptions in the taxable income. Moreover relevant

measures as depicted by the Australian taxation office need to be evaluated by the taxable

person (Taylor and Richardson 2013). Then relevant education module and software for the

course needs to be used. In addition, fees for the course need to be for short duration have

relevant meals and travel expenses should be included. These measures are provided by

Australian taxation office needs to be evaluated before using the short term course, as a tax

deductible expense. Therefore, relevant tax deduction is conducted by the art director, which

helps in reducing the taxable income.

Answer to viii) Expenses conducted on makeup and dresses

There are relevant expenses conducted on both makeup and dresses on an individual,

which is a deductible in nature as mentioned by the Australian taxation office. However,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW OF AUSTRALIA

there are certain criteria, which need to be satisfied before allowing the expenses to be tax

deductible. The expenses conducted on Makeup and dresses for the performing artist are

mainly deductible in nature (Saad 2014). Moreover, performing artist is considered to be a

magician, singer, actor, Circus performer, variety artist, and a dancer. Any kind of expenses

conducted on these individuals are considered to be a tax deduction expense. Therefore, the

scenario states that relevant expenses are conducted on makeup and dresses, but no disclosure

is provided regarding on whom the expenses are conducted. Hence, relevant assumptions are

made that the expenditure are conducted on performing artist, which could be deductible

from the taxable income and allow the individual to reduce the tax payable.

Answer to ix) Expenses conducted from travelling to office from home

Expenses conducted by the individual by travelling from home to workplace, Is

mainly considered to be an activity of work. However there is no clear evidence provided in

the scenario which could help in identifying the legality, where expenses are conducted for

office purposes. The Australian taxation office mainly states that any kind of expenses

conducted by an individual for the purpose of office is deductible in nature from its taxable

income. However, any kind of motive rather than office expenses is not deductible under the

taxation law in this particular scenario. Thus, the individual needs to identify actual expense

motive before using it as taxable deductions. Cao et al. (2015) argued that without adequate

monitoring there is no way where government could identify the expense conducted by

individuals in their income tax file. Hence, it could be stated that if the expenses conducted

for office purposes then it could be deducted from the taxable income. Nevertheless, this will

not reduce if the expenses are conducted for personal use.

TAXATION LAW OF AUSTRALIA

there are certain criteria, which need to be satisfied before allowing the expenses to be tax

deductible. The expenses conducted on Makeup and dresses for the performing artist are

mainly deductible in nature (Saad 2014). Moreover, performing artist is considered to be a

magician, singer, actor, Circus performer, variety artist, and a dancer. Any kind of expenses

conducted on these individuals are considered to be a tax deduction expense. Therefore, the

scenario states that relevant expenses are conducted on makeup and dresses, but no disclosure

is provided regarding on whom the expenses are conducted. Hence, relevant assumptions are

made that the expenditure are conducted on performing artist, which could be deductible

from the taxable income and allow the individual to reduce the tax payable.

Answer to ix) Expenses conducted from travelling to office from home

Expenses conducted by the individual by travelling from home to workplace, Is

mainly considered to be an activity of work. However there is no clear evidence provided in

the scenario which could help in identifying the legality, where expenses are conducted for

office purposes. The Australian taxation office mainly states that any kind of expenses

conducted by an individual for the purpose of office is deductible in nature from its taxable

income. However, any kind of motive rather than office expenses is not deductible under the

taxation law in this particular scenario. Thus, the individual needs to identify actual expense

motive before using it as taxable deductions. Cao et al. (2015) argued that without adequate

monitoring there is no way where government could identify the expense conducted by

individuals in their income tax file. Hence, it could be stated that if the expenses conducted

for office purposes then it could be deducted from the taxable income. Nevertheless, this will

not reduce if the expenses are conducted for personal use.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW OF AUSTRALIA

Answer to x) Expenses conducted in travel between one employer to another

The situation mainly states that relevant expenses are been conducted by an individual

from travelling to one employee to another. This mainly states that the individual is

conducting personal expense and travelling from one place to another in search of job, as one

individual cannot be employed by two companies. Therefore it could be understood that this

type of travel expense is a personal endeavour, which cannot be deducted from the taxable

income. According to the Australian taxation law, the individual cannot deduct the expenses

from its taxable income. Braithwaite (2017) mentioned that with the help of laws provided by

the Australian taxation authority, the Australian government is mainly able to reduce the

overall tax evasion conducted by individual. Therefore it could be understood that the

expenses conducted by the individual on travel from one employee to another is not

deductible in nature, which could not reduce its overall taxable income.

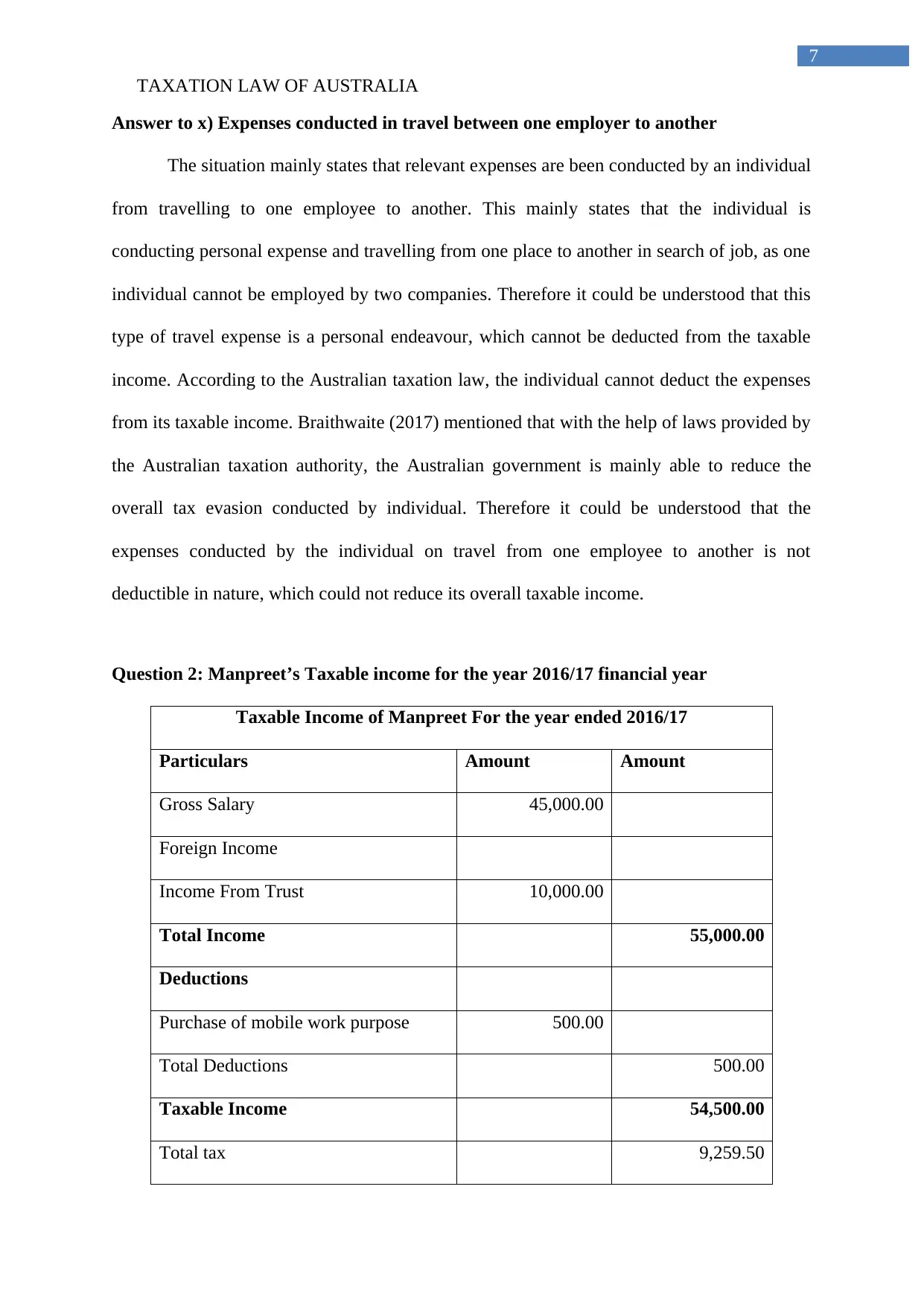

Question 2: Manpreet’s Taxable income for the year 2016/17 financial year

Taxable Income of Manpreet For the year ended 2016/17

Particulars Amount Amount

Gross Salary 45,000.00

Foreign Income

Income From Trust 10,000.00

Total Income 55,000.00

Deductions

Purchase of mobile work purpose 500.00

Total Deductions 500.00

Taxable Income 54,500.00

Total tax 9,259.50

TAXATION LAW OF AUSTRALIA

Answer to x) Expenses conducted in travel between one employer to another

The situation mainly states that relevant expenses are been conducted by an individual

from travelling to one employee to another. This mainly states that the individual is

conducting personal expense and travelling from one place to another in search of job, as one

individual cannot be employed by two companies. Therefore it could be understood that this

type of travel expense is a personal endeavour, which cannot be deducted from the taxable

income. According to the Australian taxation law, the individual cannot deduct the expenses

from its taxable income. Braithwaite (2017) mentioned that with the help of laws provided by

the Australian taxation authority, the Australian government is mainly able to reduce the

overall tax evasion conducted by individual. Therefore it could be understood that the

expenses conducted by the individual on travel from one employee to another is not

deductible in nature, which could not reduce its overall taxable income.

Question 2: Manpreet’s Taxable income for the year 2016/17 financial year

Taxable Income of Manpreet For the year ended 2016/17

Particulars Amount Amount

Gross Salary 45,000.00

Foreign Income

Income From Trust 10,000.00

Total Income 55,000.00

Deductions

Purchase of mobile work purpose 500.00

Total Deductions 500.00

Taxable Income 54,500.00

Total tax 9,259.50

8

TAXATION LAW OF AUSTRALIA

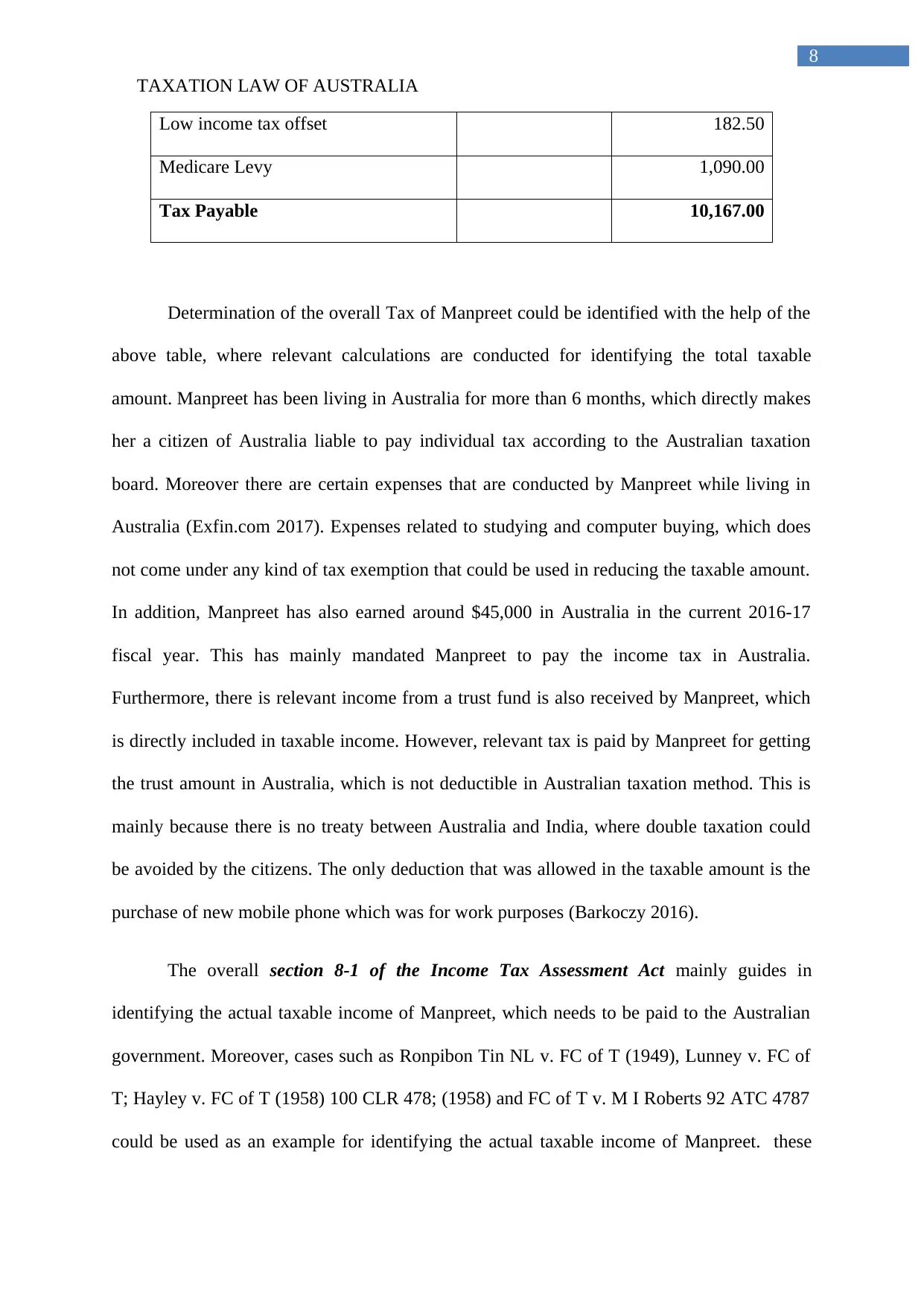

Low income tax offset 182.50

Medicare Levy 1,090.00

Tax Payable 10,167.00

Determination of the overall Tax of Manpreet could be identified with the help of the

above table, where relevant calculations are conducted for identifying the total taxable

amount. Manpreet has been living in Australia for more than 6 months, which directly makes

her a citizen of Australia liable to pay individual tax according to the Australian taxation

board. Moreover there are certain expenses that are conducted by Manpreet while living in

Australia (Exfin.com 2017). Expenses related to studying and computer buying, which does

not come under any kind of tax exemption that could be used in reducing the taxable amount.

In addition, Manpreet has also earned around $45,000 in Australia in the current 2016-17

fiscal year. This has mainly mandated Manpreet to pay the income tax in Australia.

Furthermore, there is relevant income from a trust fund is also received by Manpreet, which

is directly included in taxable income. However, relevant tax is paid by Manpreet for getting

the trust amount in Australia, which is not deductible in Australian taxation method. This is

mainly because there is no treaty between Australia and India, where double taxation could

be avoided by the citizens. The only deduction that was allowed in the taxable amount is the

purchase of new mobile phone which was for work purposes (Barkoczy 2016).

The overall section 8-1 of the Income Tax Assessment Act mainly guides in

identifying the actual taxable income of Manpreet, which needs to be paid to the Australian

government. Moreover, cases such as Ronpibon Tin NL v. FC of T (1949), Lunney v. FC of

T; Hayley v. FC of T (1958) 100 CLR 478; (1958) and FC of T v. M I Roberts 92 ATC 4787

could be used as an example for identifying the actual taxable income of Manpreet. these

TAXATION LAW OF AUSTRALIA

Low income tax offset 182.50

Medicare Levy 1,090.00

Tax Payable 10,167.00

Determination of the overall Tax of Manpreet could be identified with the help of the

above table, where relevant calculations are conducted for identifying the total taxable

amount. Manpreet has been living in Australia for more than 6 months, which directly makes

her a citizen of Australia liable to pay individual tax according to the Australian taxation

board. Moreover there are certain expenses that are conducted by Manpreet while living in

Australia (Exfin.com 2017). Expenses related to studying and computer buying, which does

not come under any kind of tax exemption that could be used in reducing the taxable amount.

In addition, Manpreet has also earned around $45,000 in Australia in the current 2016-17

fiscal year. This has mainly mandated Manpreet to pay the income tax in Australia.

Furthermore, there is relevant income from a trust fund is also received by Manpreet, which

is directly included in taxable income. However, relevant tax is paid by Manpreet for getting

the trust amount in Australia, which is not deductible in Australian taxation method. This is

mainly because there is no treaty between Australia and India, where double taxation could

be avoided by the citizens. The only deduction that was allowed in the taxable amount is the

purchase of new mobile phone which was for work purposes (Barkoczy 2016).

The overall section 8-1 of the Income Tax Assessment Act mainly guides in

identifying the actual taxable income of Manpreet, which needs to be paid to the Australian

government. Moreover, cases such as Ronpibon Tin NL v. FC of T (1949), Lunney v. FC of

T; Hayley v. FC of T (1958) 100 CLR 478; (1958) and FC of T v. M I Roberts 92 ATC 4787

could be used as an example for identifying the actual taxable income of Manpreet. these

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW OF AUSTRALIA

cases also help in gauging into the overall taxation rules that is followed in Australia and the

relevant amendments that needs to be conducted in the taxable amount. Moreover medical

navy and low income tax for state is also used in the calculation of total tax payable of

Manpreet, which is promptly disclosed in the Australian taxation Office website (Ato.gov.au

2017). Therefore medical leave is mainly added to the income tax amount, while the low

income tax offset is deducted from the taxable amount. This mainly allows the individual to

identify the actual tax payable in Australia, in accordance with the rules and regulations laid

down by ATO (Snape and De 2016).

TAXATION LAW OF AUSTRALIA

cases also help in gauging into the overall taxation rules that is followed in Australia and the

relevant amendments that needs to be conducted in the taxable amount. Moreover medical

navy and low income tax for state is also used in the calculation of total tax payable of

Manpreet, which is promptly disclosed in the Australian taxation Office website (Ato.gov.au

2017). Therefore medical leave is mainly added to the income tax amount, while the low

income tax offset is deducted from the taxable amount. This mainly allows the individual to

identify the actual tax payable in Australia, in accordance with the rules and regulations laid

down by ATO (Snape and De 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW OF AUSTRALIA

Reference and Bibliography:

Ali, M., Sales, A.B.I.C.L., Barwick, J., Digirolamo, L., Australia, C.R., Officer, D.R., Do,

T.N., Supply, I.W.W., El Boustani, P., Sales, S.H.B.B.H. and Khalid, A., 2017. School of

Business.

Ato.gov.au. (2017). Low income earners. [online] Available at:

https://www.ato.gov.au/Individuals/Income-and-deductions/Offsets-and-rebates/Low-

income-earners/ [Accessed 3 Sep. 2017].

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Bird, R.M. and Zolt, E.M., 2014. Redistribution via taxation: the limited role of the personal

income tax in developing countries. Annals of Economics and Finance, 15(2), pp.625-683.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burton, H.A. and Karlinsky, S., 2016. Tax professionals' perception of large and mid-size

business US tax law complexity. eJournal of Tax Research, 14(1), p.61.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Davison, M., Monotti, A. and Wiseman, L., 2015. Australian intellectual property law.

Cambridge University Press.

TAXATION LAW OF AUSTRALIA

Reference and Bibliography:

Ali, M., Sales, A.B.I.C.L., Barwick, J., Digirolamo, L., Australia, C.R., Officer, D.R., Do,

T.N., Supply, I.W.W., El Boustani, P., Sales, S.H.B.B.H. and Khalid, A., 2017. School of

Business.

Ato.gov.au. (2017). Low income earners. [online] Available at:

https://www.ato.gov.au/Individuals/Income-and-deductions/Offsets-and-rebates/Low-

income-earners/ [Accessed 3 Sep. 2017].

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Bird, R.M. and Zolt, E.M., 2014. Redistribution via taxation: the limited role of the personal

income tax in developing countries. Annals of Economics and Finance, 15(2), pp.625-683.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burton, H.A. and Karlinsky, S., 2016. Tax professionals' perception of large and mid-size

business US tax law complexity. eJournal of Tax Research, 14(1), p.61.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Davison, M., Monotti, A. and Wiseman, L., 2015. Australian intellectual property law.

Cambridge University Press.

11

TAXATION LAW OF AUSTRALIA

Douglas, H., Bartlett, F., Luker, T. and Hunter, R. eds., 2014. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Exfin.com. (2017). Current Australian IncomeTax Rates - Resident and Non-Resident | Exfin

- The Australian Expatriate's Gateway. [online] Available at:

https://www.exfin.com/australian-tax-rates [Accessed 3 Sep. 2017].

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Novikov, A.A., Ling, T.G. and Kordzakhia, N., 2014. Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp. 461-

474). Springer International Publishing.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M.,

2015. Financial management: Principles and applications. Pearson Higher Education AU.

Ross, M., Walker, J. and Walker, J., 2017. Multinationals targeted down under. Taxation in

Australia, 52(1), p.22.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing

and Taxation, 22(1), pp.12-25.

TAXATION LAW OF AUSTRALIA

Douglas, H., Bartlett, F., Luker, T. and Hunter, R. eds., 2014. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Exfin.com. (2017). Current Australian IncomeTax Rates - Resident and Non-Resident | Exfin

- The Australian Expatriate's Gateway. [online] Available at:

https://www.exfin.com/australian-tax-rates [Accessed 3 Sep. 2017].

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Novikov, A.A., Ling, T.G. and Kordzakhia, N., 2014. Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp. 461-

474). Springer International Publishing.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M.,

2015. Financial management: Principles and applications. Pearson Higher Education AU.

Ross, M., Walker, J. and Walker, J., 2017. Multinationals targeted down under. Taxation in

Australia, 52(1), p.22.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing

and Taxation, 22(1), pp.12-25.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.