HA3042 Taxation Law: A Comprehensive Analysis of Tax Scenarios

VerifiedAdded on 2024/05/29

|7

|1450

|104

Homework Assignment

AI Summary

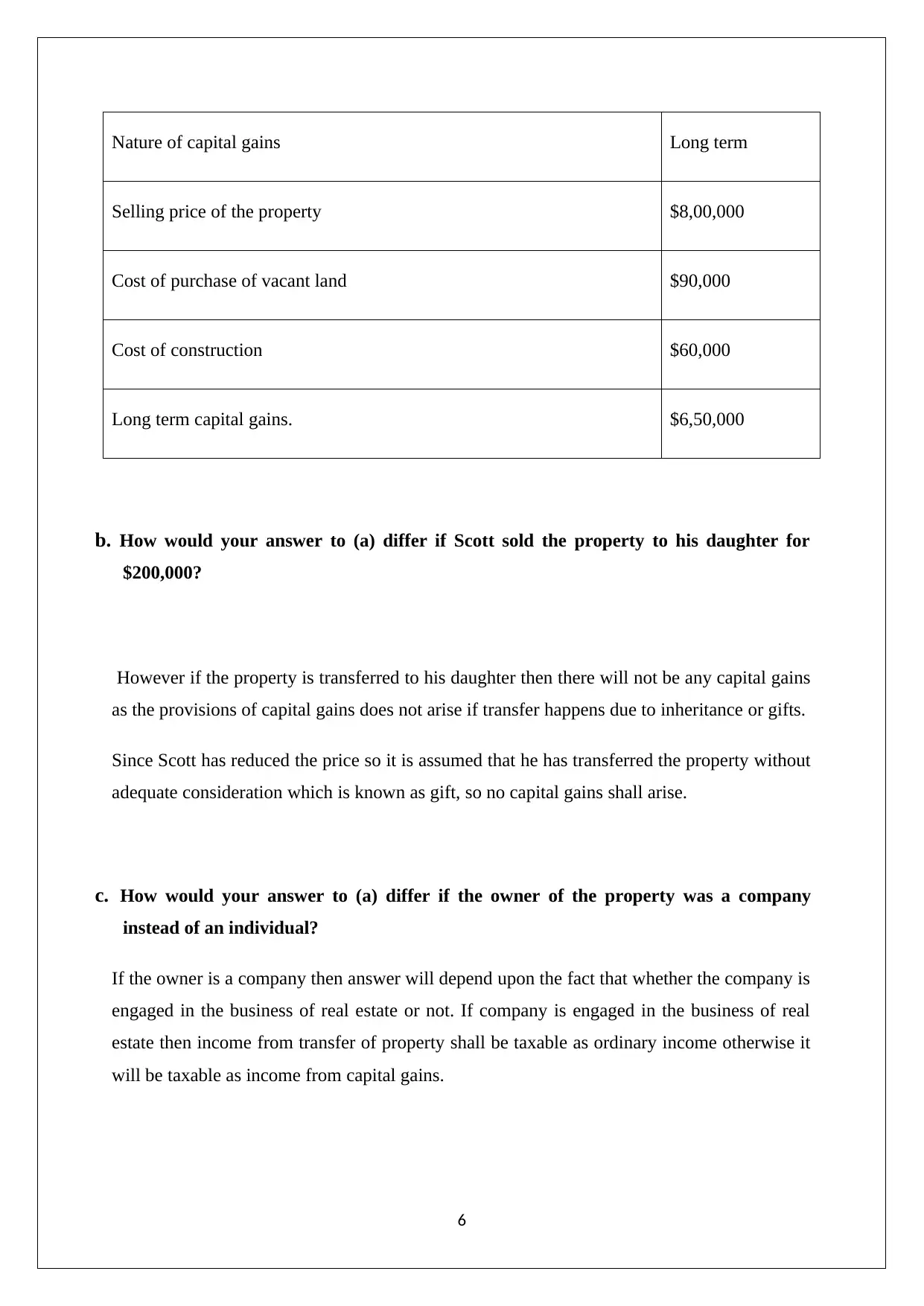

This assignment delves into various aspects of Australian taxation law, presenting solutions to hypothetical scenarios. It examines whether income from story writing and related activities qualifies as income from personal exertion or capital gains, referencing Section 8-1 of the Income Tax Assessment Act 1997. The assignment also addresses the tax implications of fringe benefits, specifically the use of a car for personal purposes, calculating its taxable value using the statutory formula. Furthermore, it analyzes a situation involving a loan between family members and the taxability of interest received. Finally, the assignment explores capital gains tax implications related to the sale of property, including scenarios involving sales to family members and different ownership structures (individual vs. company), providing a comprehensive overview of relevant tax principles and calculations. Desklib offers a wealth of similar solved assignments and resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.