HA3042 Taxation Law T1 2018: Personal Exertion, Income & CGT

VerifiedAdded on 2023/06/12

|8

|1375

|335

Homework Assignment

AI Summary

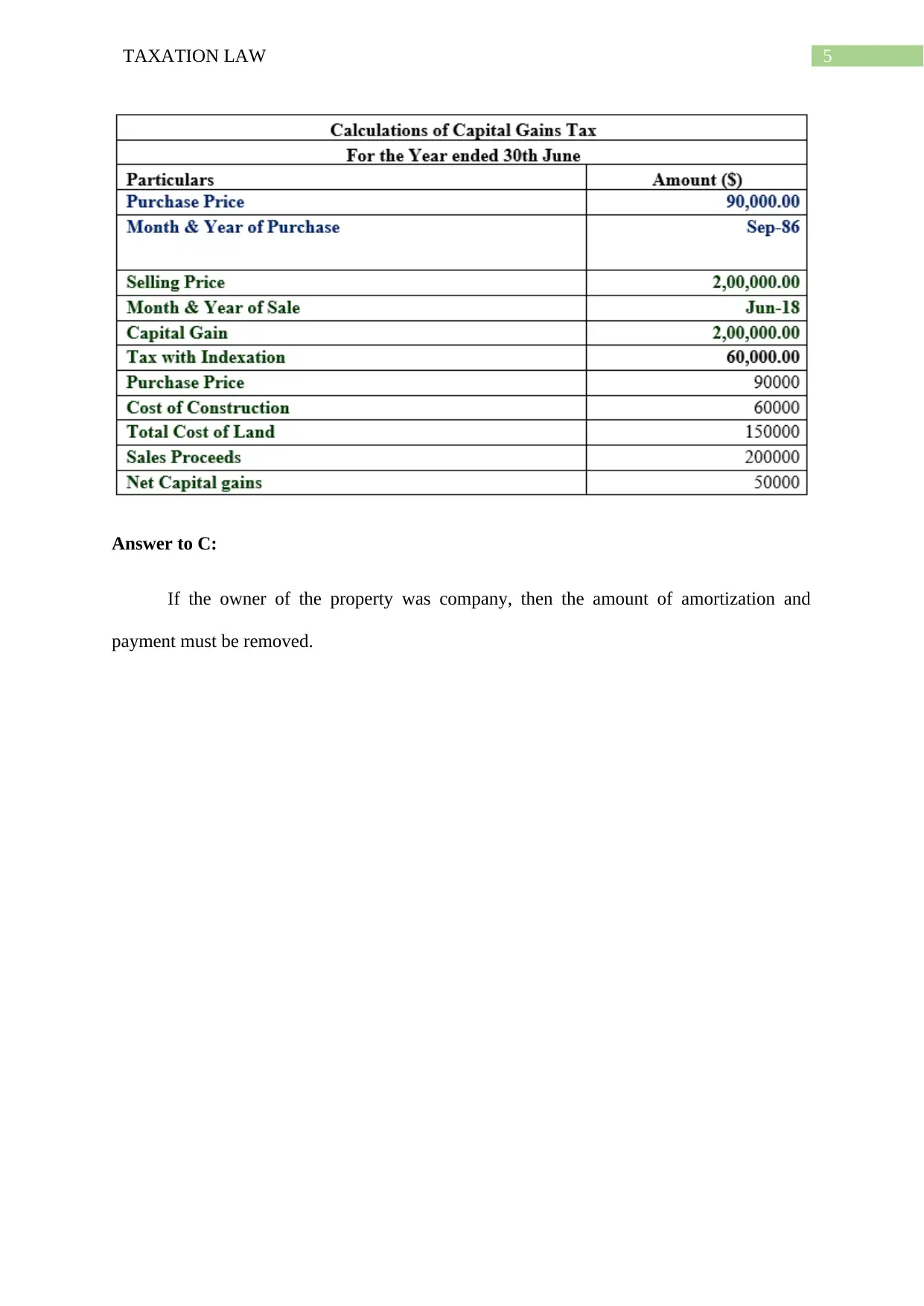

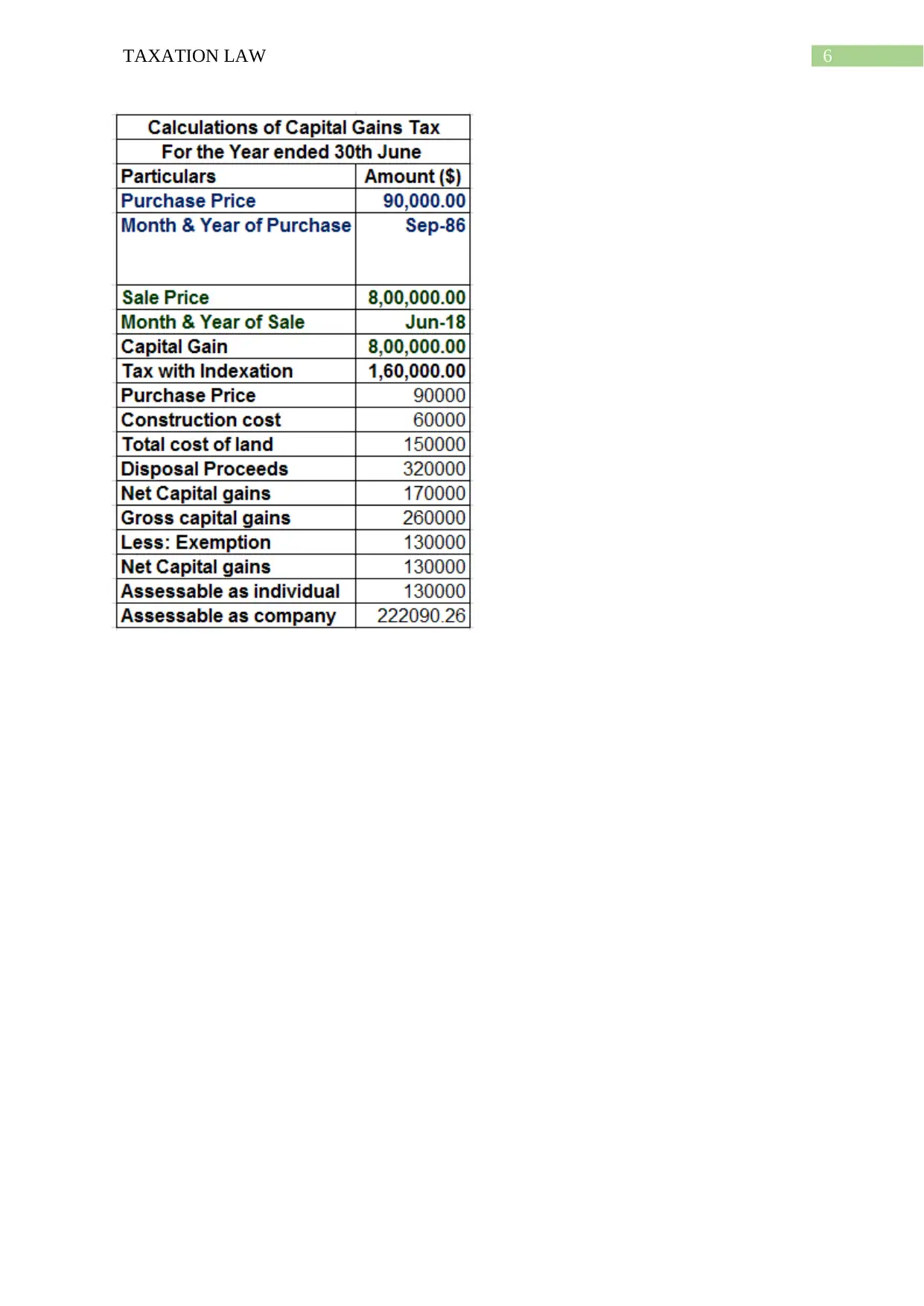

This assignment solution delves into various aspects of taxation law. It addresses whether payments received by Hilary, a mountain climber, for her life story, manuscript sales, and photographs constitute income from personal exertion. It references relevant sections of the ITAA 1997 and case law to support the analysis. Furthermore, the assignment explores the character of income in the context of a loan between a mother and son and discusses the implications of capital gains tax (CGT) on assets acquired before and after the introduction of the CGT regime, including the sale of property to a daughter. The solution also briefly touches upon the impact of company ownership on property amortization and payments.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.