Taxation Law: A Comprehensive Analysis of Income and Fringe Benefits

VerifiedAdded on 2023/04/24

|11

|2231

|395

Case Study

AI Summary

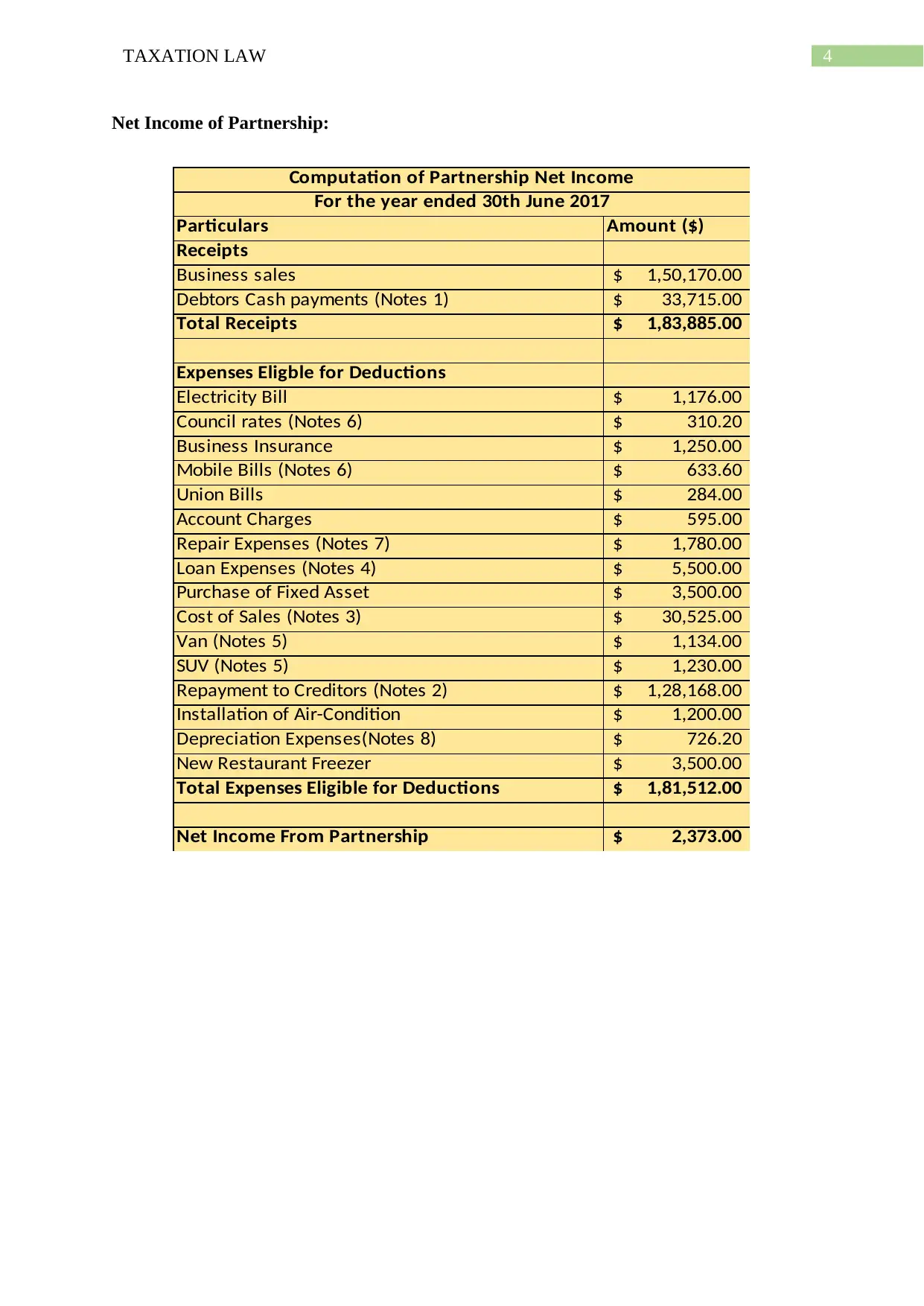

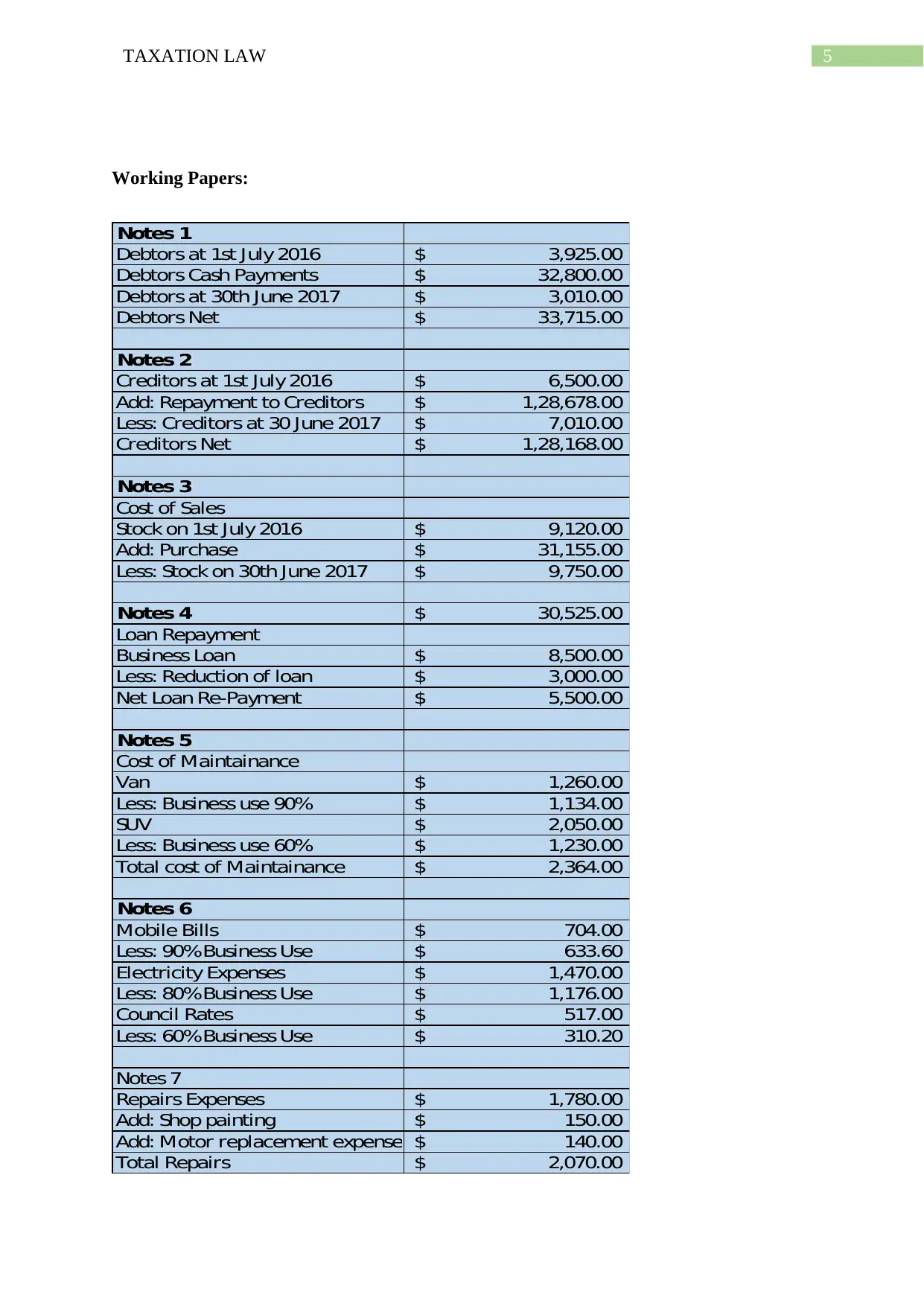

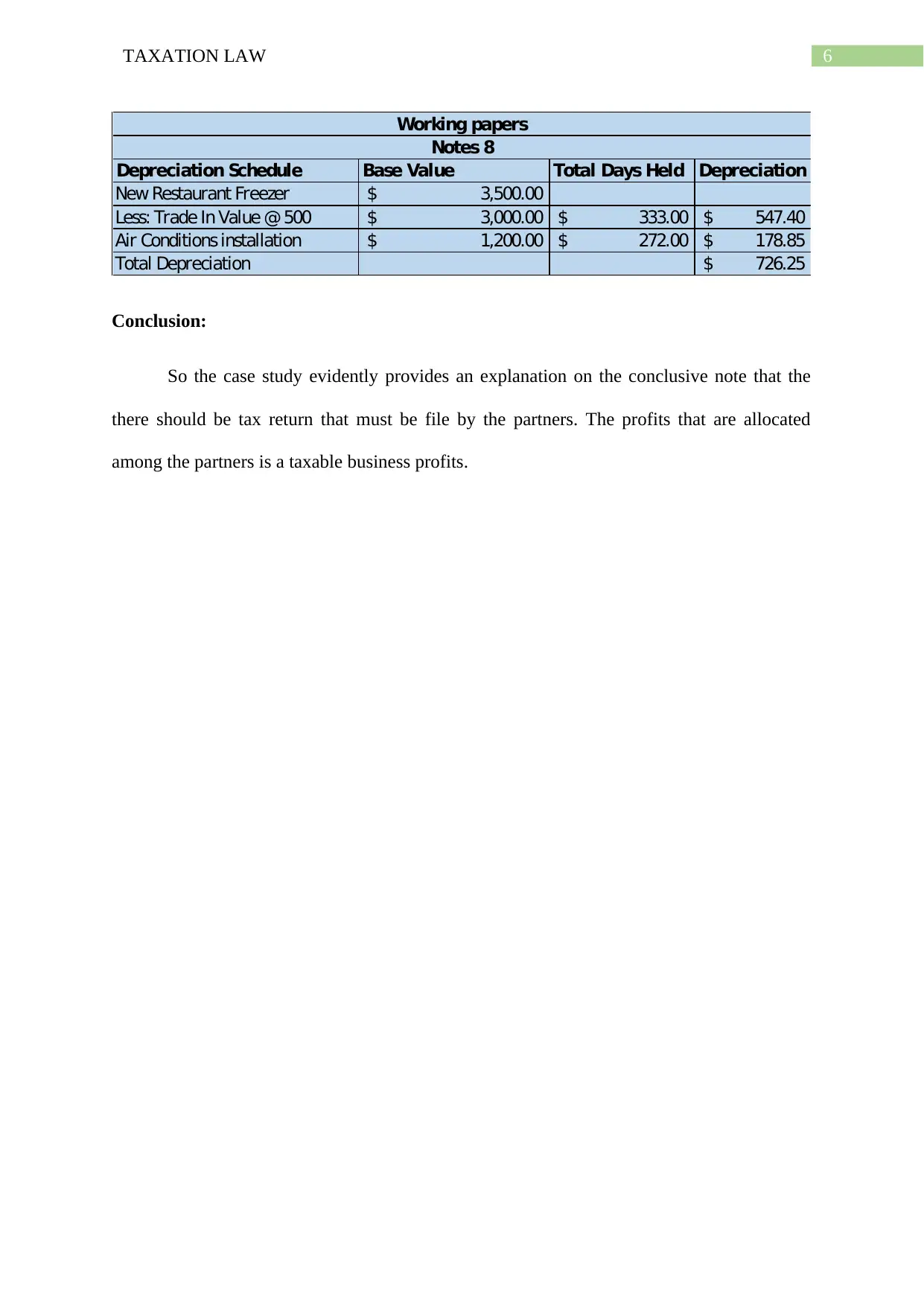

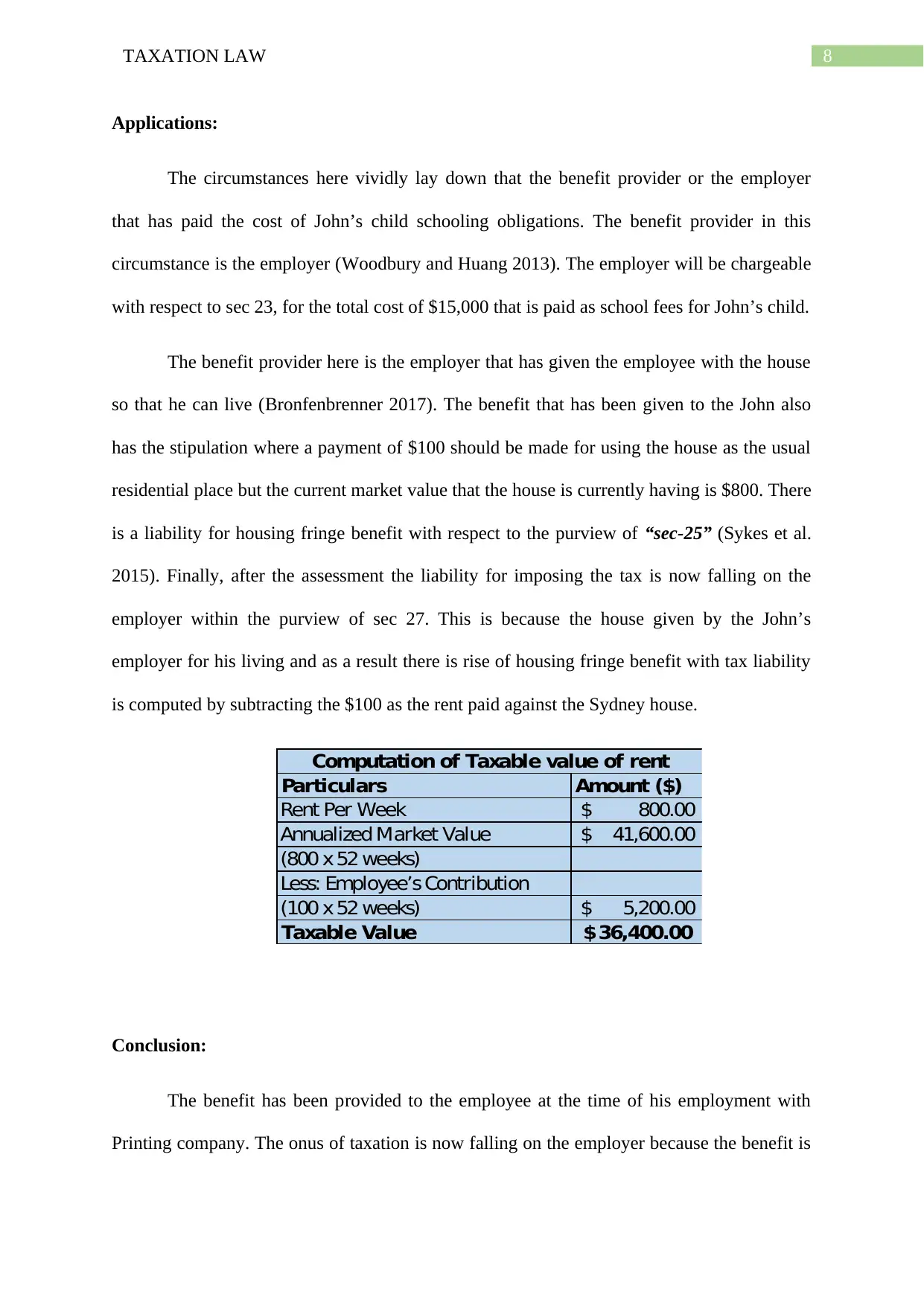

This case study examines taxation law principles related to partnership income and fringe benefits. It analyzes a scenario involving Olivia and Daniel's partnership, focusing on the taxability of their business income and the deductibility of various expenses. The study computes the partnership's net income, considering factors like business sales, debtors, cash payments, and eligible deductions such as electricity bills, council rates, and repair expenses. It also addresses the tax implications of drawings made by the partners. Furthermore, the case study delves into fringe benefits tax (FBT) concerning an employee, John, focusing on the employer's obligations regarding school fees and housing benefits. The analysis calculates the taxable value of the housing benefit, considering market rent and employee contributions. The study concludes that the employer is liable for FBT on the provided benefits, with the value of these benefits eligible for tax rebates. Desklib offers a range of study tools and resources, including similar solved assignments, to aid students in understanding complex legal and financial concepts.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.