Taxation Law Assignment: Income Tax, Deductions, and GST Issues

VerifiedAdded on 2020/02/19

|13

|2572

|33

Homework Assignment

AI Summary

This document presents a detailed solution to a taxation law assignment, addressing several key issues. The assignment analyzes permissible income tax deductions related to the cost of moving machinery, revaluation of assets, and legal expenses incurred in business operations, referencing relevant case law like "British Insulated & Helsby Cables v. Atherton" and "Sun Newspapers Ltd v F C of T". It also examines the entitlement to input tax credits for advertising expenses under the GST Act 1999, referencing "GSTR 2006/3" and relevant case law. Furthermore, the document includes a computation of taxable income, providing a comprehensive overview of taxation principles and their practical application. The student's work offers valuable insights into various aspects of Australian taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer to question 1:

Issue:

The issue that has been illustrated in this case study is dealing with the cost of moving

the machine and gaining permissible income tax deductions.

Rule:

1. “British Insulated & Helsby Cables v. Atherton (1926)”

2. “Section 8 (1) of the ITAA 1997”

Applications:

The cost that has been generated in relocation of machine to the new place comprises

of capital expenditure under the context of “Section 8-1 of the ITAA 1997”. It is depicted that

the cost occurred from the shifting the machine to the new site representing a small change

which cannot be cannot be allowed for deductions and ultimately increases the depreciation

cost. Section 8-1 of the ITAA 1997 puts forward those allowable deductions for income tax

purpose is only permitted when the cost is incurred for every day trade functions (Manning,

Sciacca and Alford 2016.).

The judgement of “British Insulated & Helsby Cables v. Atherton (1926)” the fact

that there was the increase in the business benefits because of the shift of the depreciable

asset in the business (Coleman and Sadiq 2013). As depicted under the Taxation ruling of TD

93/123 charge involve in setting the machine and commencing the production procedure

represents revenue in nature and leads to an increase in the business benefit. Considerably,

Answer to question 1:

Issue:

The issue that has been illustrated in this case study is dealing with the cost of moving

the machine and gaining permissible income tax deductions.

Rule:

1. “British Insulated & Helsby Cables v. Atherton (1926)”

2. “Section 8 (1) of the ITAA 1997”

Applications:

The cost that has been generated in relocation of machine to the new place comprises

of capital expenditure under the context of “Section 8-1 of the ITAA 1997”. It is depicted that

the cost occurred from the shifting the machine to the new site representing a small change

which cannot be cannot be allowed for deductions and ultimately increases the depreciation

cost. Section 8-1 of the ITAA 1997 puts forward those allowable deductions for income tax

purpose is only permitted when the cost is incurred for every day trade functions (Manning,

Sciacca and Alford 2016.).

The judgement of “British Insulated & Helsby Cables v. Atherton (1926)” the fact

that there was the increase in the business benefits because of the shift of the depreciable

asset in the business (Coleman and Sadiq 2013). As depicted under the Taxation ruling of TD

93/123 charge involve in setting the machine and commencing the production procedure

represents revenue in nature and leads to an increase in the business benefit. Considerably,

2TAXATION LAW

understanding the proviso that has been explained under the “Section 8 (1) of the ITAA

1997” more specifically the expense that has been made by the person involved in the

problem statement for moving the machine to a new site would lead to a cost having the

features of capital. Because of this such cost under section 8 (1) of the ITAA 1997 are not

permitted for claiming deductions (Ismer 2016).

Conclusion:

The clarification stated above regarding the spending made on machine is not a

business related deductible cost. The cost has the nature of capital and they will not be treated

for deductions for income tax purpose.

Requirement 1.2:

Issue:

The problem that has been defined from the statement is matter of revaluation cost of

asset. Therefore, such can be considered for deductions that is allowed under “section 8 (1) of

the ITAA 1997” income tax deductions.

Rule:

1. “section 8 (1) of the ITAA 1997”

Application:

The situation provides that the expenditure has relations with the recurring cost.

Henceforth, at the time of ascertaining the sum of allowable business deductions it is

imperative for the business to ascertain the fact that the expense has incurred in the process of

revaluation of asset that increase the income of the business or the expense has just occurred

understanding the proviso that has been explained under the “Section 8 (1) of the ITAA

1997” more specifically the expense that has been made by the person involved in the

problem statement for moving the machine to a new site would lead to a cost having the

features of capital. Because of this such cost under section 8 (1) of the ITAA 1997 are not

permitted for claiming deductions (Ismer 2016).

Conclusion:

The clarification stated above regarding the spending made on machine is not a

business related deductible cost. The cost has the nature of capital and they will not be treated

for deductions for income tax purpose.

Requirement 1.2:

Issue:

The problem that has been defined from the statement is matter of revaluation cost of

asset. Therefore, such can be considered for deductions that is allowed under “section 8 (1) of

the ITAA 1997” income tax deductions.

Rule:

1. “section 8 (1) of the ITAA 1997”

Application:

The situation provides that the expenditure has relations with the recurring cost.

Henceforth, at the time of ascertaining the sum of allowable business deductions it is

imperative for the business to ascertain the fact that the expense has incurred in the process of

revaluation of asset that increase the income of the business or the expense has just occurred

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

in the process of protecting the asset. Perceiving down the above-defined argument related to

cost of revaluation of asset, such kind of cost are treated as periodic cost and it will be

measured as permissible deductions for the business under “section 8 (1) of the ITAA 1997”

(Nechaev 2014).

Conclusion:

The assessment that has been performed in the above context signifies that the cost

will be considered for the purpose of business deductions under “section 8 (1) of the ITAA

1997”. The chief reason for considering the cost for income tax deductions is because the

expenditure is possessing the characteristics of recurring nature.

Requirement 1.3:

Issue:

The issue that is mentioned in this case is dealing with the problems of legal expense

that is incurred in the process of opposing the winding up of business. The character of the

expense is evaluated under “section 8 (1) of the ITAA 1997”.

Rule:

a. “section 8 (1) of the ITAA 1997”

b. Sun Newspapers Ltd v F C of T (1938)

Applications:

The evaluation of the “section 8 (1) of the ITAA 1997” provides that expense that is

legal and incurred at the time of performing business activities will be viewed as business

deductions for taxation purpose (Gordon and Kopczuk 2014). Nevertheless it is imperative to

in the process of protecting the asset. Perceiving down the above-defined argument related to

cost of revaluation of asset, such kind of cost are treated as periodic cost and it will be

measured as permissible deductions for the business under “section 8 (1) of the ITAA 1997”

(Nechaev 2014).

Conclusion:

The assessment that has been performed in the above context signifies that the cost

will be considered for the purpose of business deductions under “section 8 (1) of the ITAA

1997”. The chief reason for considering the cost for income tax deductions is because the

expenditure is possessing the characteristics of recurring nature.

Requirement 1.3:

Issue:

The issue that is mentioned in this case is dealing with the problems of legal expense

that is incurred in the process of opposing the winding up of business. The character of the

expense is evaluated under “section 8 (1) of the ITAA 1997”.

Rule:

a. “section 8 (1) of the ITAA 1997”

b. Sun Newspapers Ltd v F C of T (1938)

Applications:

The evaluation of the “section 8 (1) of the ITAA 1997” provides that expense that is

legal and incurred at the time of performing business activities will be viewed as business

deductions for taxation purpose (Gordon and Kopczuk 2014). Nevertheless it is imperative to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

determine the characteristics of the legal expense upon claiming income tax deductions

(Zucman 2014). Noticing the explanation of the Taxation Ruling of ID 2004/367 a person

carrying on the business performance can put forward the entitlement of claiming legal cost

as the business related expense. In context of the “Sun Newspapers Ltd v F C of T (1938)”

the judgement stated that when the legal expenditure is committed in the direction of

structural purpose rather than for functional purpose then the outgoings or the expense will be

treated as capital expense. As a result of this such kind of expenditure would not be

considered deductible for income tax purpose (Mertens and Ravn 2013). Winding up of the

business represents a capital expenditure that is not directly related to the generation of the

business income. As the result of this the expenditure would be non allowable for income tax

purpose since it is not incurred from the operational activities of the business.

Conclusion:

As noted from the above defined explanation and considering the reference of the

section 8-1 of the ITAA 1997 it can be stated that winding up expenditure would be

considered for non-allowable deductions.

Answer to requirement 1.4:

Issue:

The problem statement brings forward the issue that the payment of legal cost to

solicitor is accounted as the allowable deductions in the context of the section 8-1 of the

ITAA 1997.

Rule:

a. Herald and Weekly Times v F C of T (1962)

determine the characteristics of the legal expense upon claiming income tax deductions

(Zucman 2014). Noticing the explanation of the Taxation Ruling of ID 2004/367 a person

carrying on the business performance can put forward the entitlement of claiming legal cost

as the business related expense. In context of the “Sun Newspapers Ltd v F C of T (1938)”

the judgement stated that when the legal expenditure is committed in the direction of

structural purpose rather than for functional purpose then the outgoings or the expense will be

treated as capital expense. As a result of this such kind of expenditure would not be

considered deductible for income tax purpose (Mertens and Ravn 2013). Winding up of the

business represents a capital expenditure that is not directly related to the generation of the

business income. As the result of this the expenditure would be non allowable for income tax

purpose since it is not incurred from the operational activities of the business.

Conclusion:

As noted from the above defined explanation and considering the reference of the

section 8-1 of the ITAA 1997 it can be stated that winding up expenditure would be

considered for non-allowable deductions.

Answer to requirement 1.4:

Issue:

The problem statement brings forward the issue that the payment of legal cost to

solicitor is accounted as the allowable deductions in the context of the section 8-1 of the

ITAA 1997.

Rule:

a. Herald and Weekly Times v F C of T (1962)

5TAXATION LAW

b. Section 8-1 of the ITAA 1997

Applications:

As it has been rightly mentioned in the context of the section 8-1 of the ITAA 1997

legal expenditure that has occurred in discharge of the business operational functions that

forms the part of the day to day activities of the taxpayer are generally considered for

deductions (Tanzi 2014). There is also an exception to this fact is that if the expenses are

domestic or carrying the nature of the private expense or incurred for the production of the

non-exempt income then they are not regarded for income tax deductions. Considering the

decision that has been defined in the case of “Herald & Weekly Times v F C of T (1932)”

expenditure that are legal in the context of the section 8-1 of the ITAA 1997 and incurred

from daily business activities then it would be treated for income tax deductions (Auerbach

and Hassett 2015).

The evaluation conducted above evidently provides an understanding of “section 8 (1)

of the ITAA 1997” that legal expense relating to the service of solicitor for performance of

business activities is an admissible business deductions (Bodie 2013). The service of solicitor

represents cost that are directly related in the discharge of the business functions and hence it

would be treated as deductions for income tax purpose.

Conclusion:

The argumentative analysis has considered the vital explanation of the “section 8 (1)

of the ITAA 1997” to evidently reach at the conclusion that legal expense incurred for the

service of the solicitor is business expense. The solicitor service was taken for discharging

business functions that falls within the scope of business “section 8 (1) of the ITAA 1997” for

claiming allowable deductions.

b. Section 8-1 of the ITAA 1997

Applications:

As it has been rightly mentioned in the context of the section 8-1 of the ITAA 1997

legal expenditure that has occurred in discharge of the business operational functions that

forms the part of the day to day activities of the taxpayer are generally considered for

deductions (Tanzi 2014). There is also an exception to this fact is that if the expenses are

domestic or carrying the nature of the private expense or incurred for the production of the

non-exempt income then they are not regarded for income tax deductions. Considering the

decision that has been defined in the case of “Herald & Weekly Times v F C of T (1932)”

expenditure that are legal in the context of the section 8-1 of the ITAA 1997 and incurred

from daily business activities then it would be treated for income tax deductions (Auerbach

and Hassett 2015).

The evaluation conducted above evidently provides an understanding of “section 8 (1)

of the ITAA 1997” that legal expense relating to the service of solicitor for performance of

business activities is an admissible business deductions (Bodie 2013). The service of solicitor

represents cost that are directly related in the discharge of the business functions and hence it

would be treated as deductions for income tax purpose.

Conclusion:

The argumentative analysis has considered the vital explanation of the “section 8 (1)

of the ITAA 1997” to evidently reach at the conclusion that legal expense incurred for the

service of the solicitor is business expense. The solicitor service was taken for discharging

business functions that falls within the scope of business “section 8 (1) of the ITAA 1997” for

claiming allowable deductions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issue:

The problem statement of the case study is based with the ascertainment of the

entitlement of the advertisement expense that has been incurred by the Big Bank Ltd under

the legislation of GSTR Act 1999.

Rule:

a. “Goods and Service Tax Ruling of GSTR 2006/3”

b. “GST Act 1999”

c. paragraphs 11-5 and 15-5

d. subsection 15-25

e. “Ronpibon Tin NL v F C of T”

Application:

The problem statement of the Big Bank Ltd deals with the ascertainment of the input

tax credit by applying the taxation ruling of GSTR 2006/3. The GSTR 2006/3 is concerned

with the procedure that should be applied in the present context of Big Bank to ascertain the

amount of the input tax credit for the amount of the financial supplies that is made by Big

Bank along with the included amount of GST Act 1999. It is noteworthy to denote that for the

purpose of assessing the creditable purpose section 11-15 and 129 under the scope of GST is

implemented (Coleman and Sadiq 2013). The taxable entities should be registered or they are

required to get the registration under GST Act 1999 that have ultimately surpassed the

financial acquisition limit. The “Goods and Service Tax Ruling of GSTR 2006/3”specifically

lay down that business entities are should obtain the registration under the GST Act 1997 for

Answer to question 2:

Issue:

The problem statement of the case study is based with the ascertainment of the

entitlement of the advertisement expense that has been incurred by the Big Bank Ltd under

the legislation of GSTR Act 1999.

Rule:

a. “Goods and Service Tax Ruling of GSTR 2006/3”

b. “GST Act 1999”

c. paragraphs 11-5 and 15-5

d. subsection 15-25

e. “Ronpibon Tin NL v F C of T”

Application:

The problem statement of the Big Bank Ltd deals with the ascertainment of the input

tax credit by applying the taxation ruling of GSTR 2006/3. The GSTR 2006/3 is concerned

with the procedure that should be applied in the present context of Big Bank to ascertain the

amount of the input tax credit for the amount of the financial supplies that is made by Big

Bank along with the included amount of GST Act 1999. It is noteworthy to denote that for the

purpose of assessing the creditable purpose section 11-15 and 129 under the scope of GST is

implemented (Coleman and Sadiq 2013). The taxable entities should be registered or they are

required to get the registration under GST Act 1999 that have ultimately surpassed the

financial acquisition limit. The “Goods and Service Tax Ruling of GSTR 2006/3”specifically

lay down that business entities are should obtain the registration under the GST Act 1997 for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

the amount of GST included in the financial supplies made (Graetz and Schenk 2013).

Therefore as the result this those business registered will be able to claim input tax credit.

The conclusive statement provided in the case study Big Bank Ltd, it is assumed from

the business transaction that the bank has acquired an outflow of $1,650,000 that is

interrelated with the cost of advertisement spending that take account of the sum of GST in

the value of commercial supplies of financial nature made. In context of the Big Bank Ltd it

can be put forward that the bank qualifies for the entitlement of the input tax credit or

lowered input tax credit (Grange et al. 2014). As depicted under the GSTR ruling of 2006/3

an organisation that is registered under the GST Act or required to obtain registration then the

company would be required to pay the amount of GST included in the price of the financial

supplies (James 2014). The legislation of the GST defines that business firms that is required

to pay GST relating to the financial supplies made or imported by the company.

The primary principles of to the degree and the to the certain degree has already been

explained under the legislative case of Ronpibon Tin NL v. FC of T with the objective of

assessing the GST Act (Sadiq et al. 2014). The verdict defined under this case effectively lay

down the appropriate methods of apportionment that practically needs to be adopted by the

organization. In order to make a financial acquisition to the meet the eligibility of the

creditable purpose they must be absolutely or in fragments should be of creditable purpose

and the same has been enumerated in para 11-5 and 15-5 of the GST Act 1999. From the

current case study of Big Bank, it has been found that financial supply that has been made by

Big Bank Ltd has surpassed the financial acquisition threshold limit (Schreiber 2013). As a

result to of this to qualify for the input tax credit the bank can partially claim for the financial

made by it. A company that is making financial acquisition is authorised to make an

entitlement of putting forward the claim of input tax credit under the section 11-5 and 15-10

of the GSTR ruling of 2006/3.

the amount of GST included in the financial supplies made (Graetz and Schenk 2013).

Therefore as the result this those business registered will be able to claim input tax credit.

The conclusive statement provided in the case study Big Bank Ltd, it is assumed from

the business transaction that the bank has acquired an outflow of $1,650,000 that is

interrelated with the cost of advertisement spending that take account of the sum of GST in

the value of commercial supplies of financial nature made. In context of the Big Bank Ltd it

can be put forward that the bank qualifies for the entitlement of the input tax credit or

lowered input tax credit (Grange et al. 2014). As depicted under the GSTR ruling of 2006/3

an organisation that is registered under the GST Act or required to obtain registration then the

company would be required to pay the amount of GST included in the price of the financial

supplies (James 2014). The legislation of the GST defines that business firms that is required

to pay GST relating to the financial supplies made or imported by the company.

The primary principles of to the degree and the to the certain degree has already been

explained under the legislative case of Ronpibon Tin NL v. FC of T with the objective of

assessing the GST Act (Sadiq et al. 2014). The verdict defined under this case effectively lay

down the appropriate methods of apportionment that practically needs to be adopted by the

organization. In order to make a financial acquisition to the meet the eligibility of the

creditable purpose they must be absolutely or in fragments should be of creditable purpose

and the same has been enumerated in para 11-5 and 15-5 of the GST Act 1999. From the

current case study of Big Bank, it has been found that financial supply that has been made by

Big Bank Ltd has surpassed the financial acquisition threshold limit (Schreiber 2013). As a

result to of this to qualify for the input tax credit the bank can partially claim for the financial

made by it. A company that is making financial acquisition is authorised to make an

entitlement of putting forward the claim of input tax credit under the section 11-5 and 15-10

of the GSTR ruling of 2006/3.

8TAXATION LAW

As depicted in the current context of Big Bank the outlay or the advertisement

expenditure that has occurred by the bank in the creditable purpose will be eligible for

claiming input tax credit (Weltman 2013). Concerning the assessment ruling of the “GSTR

2006/3” an evidence can be bought forward that Big Bank meet the requirements for the

entitlement of the claiming input tax credit involving the fiscal supplies in the present context

made by the bank.

Conclusion:

As defined from the above stated analysis of the Big Bank Ltd it can be stated that the

Big Bank Ltd shall be entitlement of putting forward the claim of getting the input tax credit.

The financial supplies made are within the framework of the “Goods and Service Tax Ruling

of GSTR 2006/3” relating to the amount that has been included in the price of the financial

supplies made by the bank.

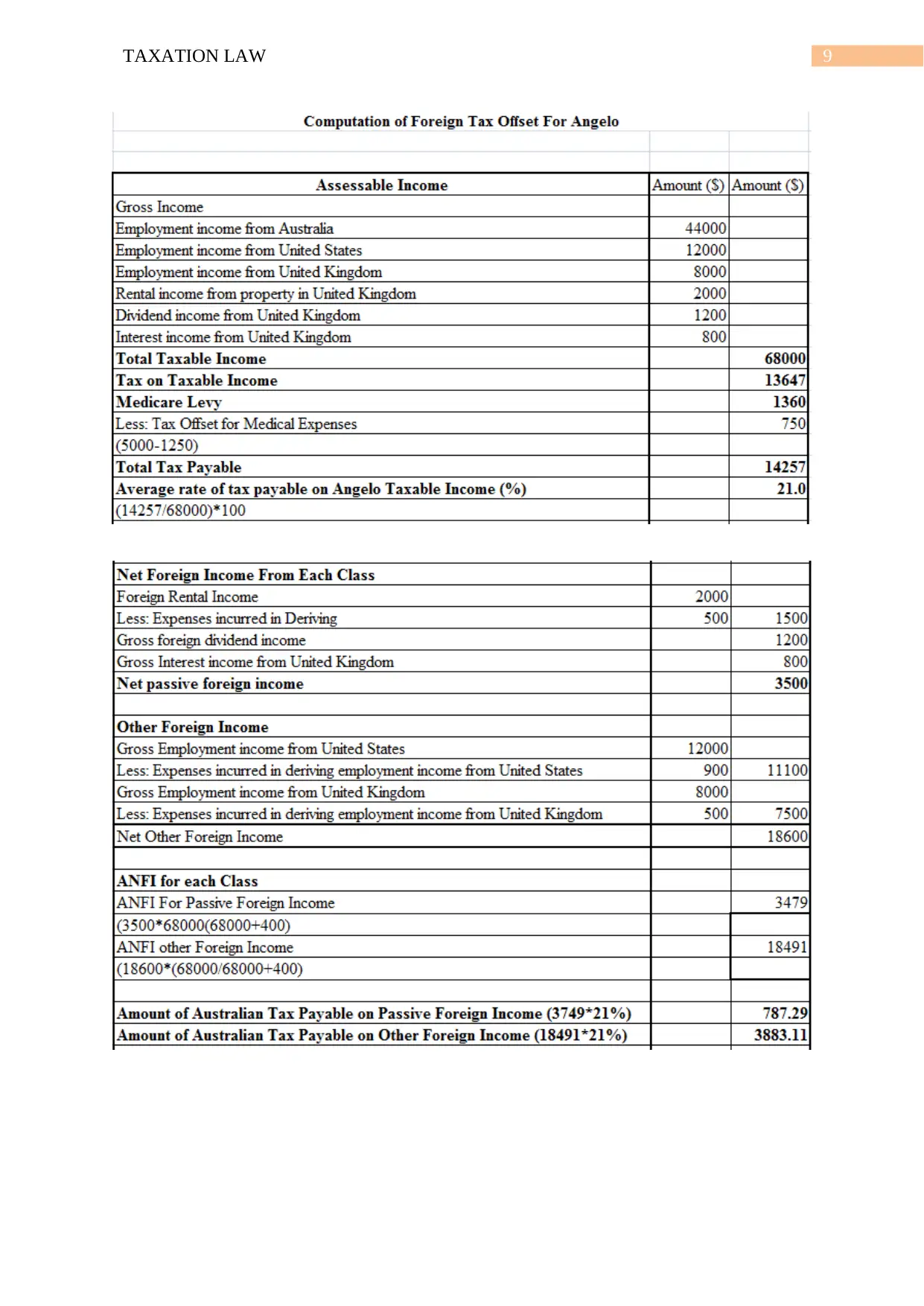

Answer to question 3:

Computation of Taxable Income of Angelo

As depicted in the current context of Big Bank the outlay or the advertisement

expenditure that has occurred by the bank in the creditable purpose will be eligible for

claiming input tax credit (Weltman 2013). Concerning the assessment ruling of the “GSTR

2006/3” an evidence can be bought forward that Big Bank meet the requirements for the

entitlement of the claiming input tax credit involving the fiscal supplies in the present context

made by the bank.

Conclusion:

As defined from the above stated analysis of the Big Bank Ltd it can be stated that the

Big Bank Ltd shall be entitlement of putting forward the claim of getting the input tax credit.

The financial supplies made are within the framework of the “Goods and Service Tax Ruling

of GSTR 2006/3” relating to the amount that has been included in the price of the financial

supplies made by the bank.

Answer to question 3:

Computation of Taxable Income of Angelo

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

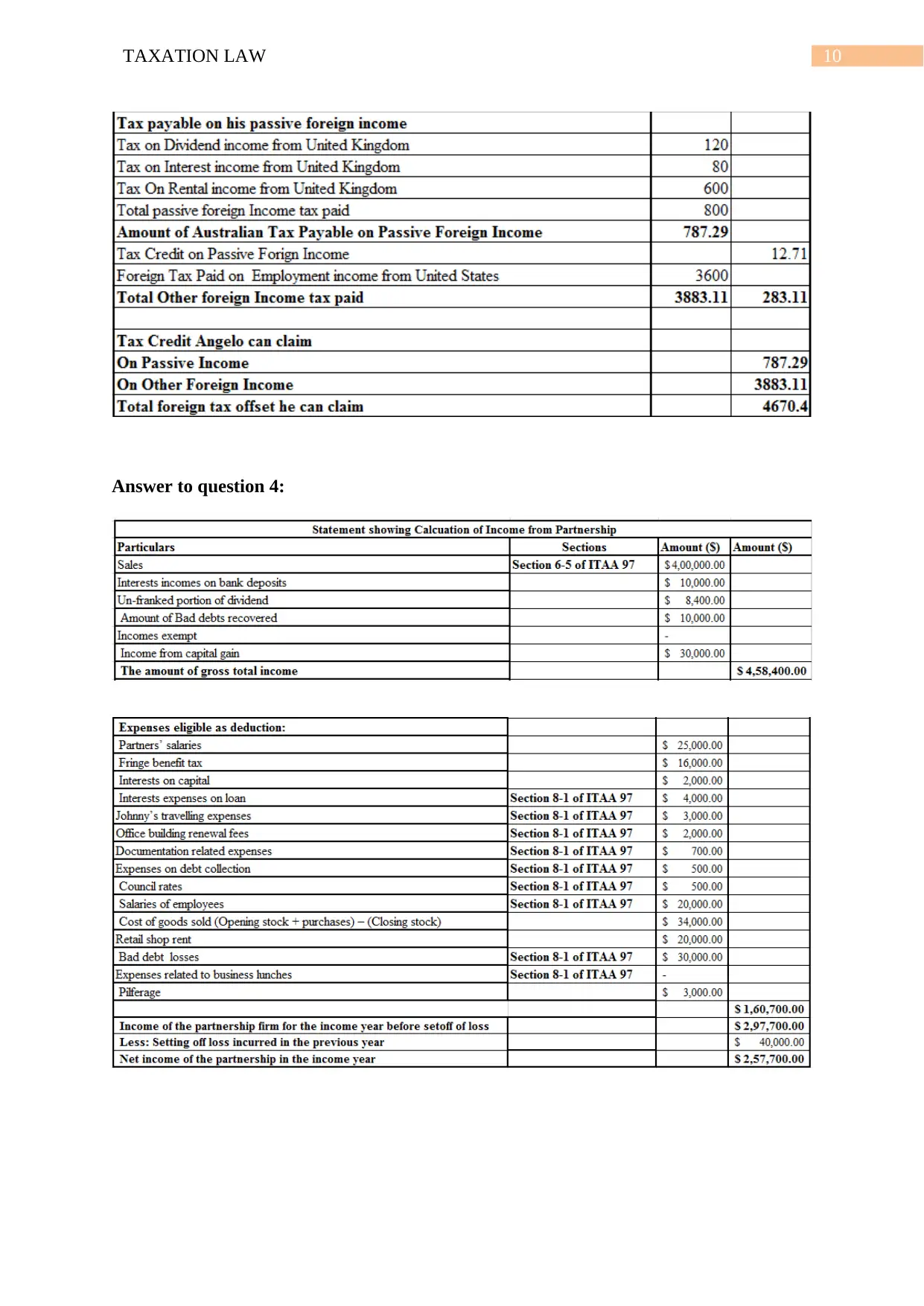

Answer to question 4:

Answer to question 4:

11TAXATION LAW

Reference list:

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The

American Economic Review, 105(5), pp.38-42.

Bodie, Z., 2013. Investments. McGraw-Hill.

Coleman, C. and Sadiq, K. (n.d.). Principles of taxation law 2013.

Gordon, R.H. and Kopczuk, W., 2014. The choice of the personal income tax base. Journal

of Public Economics, 118, pp.97-110.

Graetz, M. and Schenk, D. (n.d.). Federal income taxation.

Grange, J., Jover-Ledesma, G. and Maydew, G. (n.d.). 2014 principles of business taxation.

Ismer, R., 2016. Judicial Review of Tax Laws: The Coherence Requirement

(Folgerichtigkeitsgebot). In Rational Lawmaking under Review (pp. 209-232). Springer

International Publishing.

James, S. (n.d.). The economics of taxation.

Manning, R., Sciacca, R. and Alford, A., 2016. Tax Inversions: A Preliminary Review of

Company Financial Data. Bates White, January, 12.

Mertens, K. and Ravn, M.O., 2013. The dynamic effects of personal and corporate income

tax changes in the Australia. The American Economic Review, 103(4), pp.1212-1247.

Nechaev, A., 2014. Taxation as an instrument of stimulation of innovation-active business

entities. arXiv preprint arXiv:1412.2746.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W. and Ting, A.

(n.d.). Principles of taxation law 2014.

Reference list:

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The

American Economic Review, 105(5), pp.38-42.

Bodie, Z., 2013. Investments. McGraw-Hill.

Coleman, C. and Sadiq, K. (n.d.). Principles of taxation law 2013.

Gordon, R.H. and Kopczuk, W., 2014. The choice of the personal income tax base. Journal

of Public Economics, 118, pp.97-110.

Graetz, M. and Schenk, D. (n.d.). Federal income taxation.

Grange, J., Jover-Ledesma, G. and Maydew, G. (n.d.). 2014 principles of business taxation.

Ismer, R., 2016. Judicial Review of Tax Laws: The Coherence Requirement

(Folgerichtigkeitsgebot). In Rational Lawmaking under Review (pp. 209-232). Springer

International Publishing.

James, S. (n.d.). The economics of taxation.

Manning, R., Sciacca, R. and Alford, A., 2016. Tax Inversions: A Preliminary Review of

Company Financial Data. Bates White, January, 12.

Mertens, K. and Ravn, M.O., 2013. The dynamic effects of personal and corporate income

tax changes in the Australia. The American Economic Review, 103(4), pp.1212-1247.

Nechaev, A., 2014. Taxation as an instrument of stimulation of innovation-active business

entities. arXiv preprint arXiv:1412.2746.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W. and Ting, A.

(n.d.). Principles of taxation law 2014.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.