Taxation Law: Calculating Income Tax, Medicare Levy, AY 2017

VerifiedAdded on 2024/04/26

|17

|2881

|196

Homework Assignment

AI Summary

This assignment provides detailed solutions for calculating income tax liabilities, Medicare levy, and Medicare levy surcharge under Australian taxation law for the year ended 30 June 2017. It covers various scenarios including resident and non-resident individuals, companies, and different income levels. The calculations take into account tax rates, income thresholds, franked dividends, PAYG tax, and applicable tax offsets. The assignment uses relevant sections of the ITAA 1997 and ITRA 1986 to determine taxable income and tax payable or refundable in each case study.

Taxation law

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................3

Question 1........................................................................................................................................4

Question 2........................................................................................................................................7

Question 3......................................................................................................................................10

Question 4......................................................................................................................................13

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

2

Introduction......................................................................................................................................3

Question 1........................................................................................................................................4

Question 2........................................................................................................................................7

Question 3......................................................................................................................................10

Question 4......................................................................................................................................13

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

2

Introduction

In the present report, various taxation norms that are related to calculation of income tax liability

that can be levied ion case of situation provide herein. The income tax and its ruling are herein

discussed. The medical levy and medical levy surcharge have been considered in respect of

income tax liability in case of various case studies. The law that deals with income tax valuation

has been effectively considered herein.

3

In the present report, various taxation norms that are related to calculation of income tax liability

that can be levied ion case of situation provide herein. The income tax and its ruling are herein

discussed. The medical levy and medical levy surcharge have been considered in respect of

income tax liability in case of various case studies. The law that deals with income tax valuation

has been effectively considered herein.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

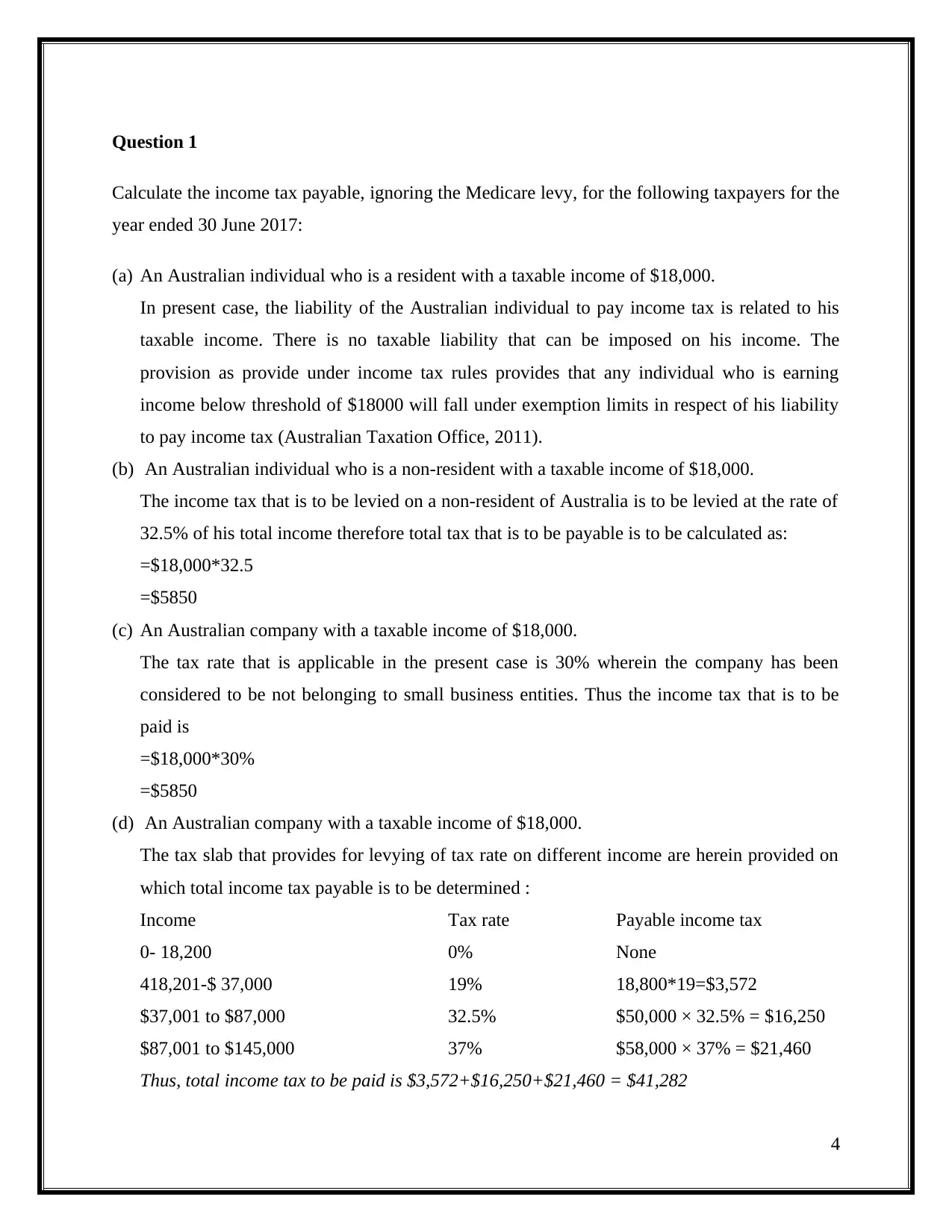

Question 1

Calculate the income tax payable, ignoring the Medicare levy, for the following taxpayers for the

year ended 30 June 2017:

(a) An Australian individual who is a resident with a taxable income of $18,000.

In present case, the liability of the Australian individual to pay income tax is related to his

taxable income. There is no taxable liability that can be imposed on his income. The

provision as provide under income tax rules provides that any individual who is earning

income below threshold of $18000 will fall under exemption limits in respect of his liability

to pay income tax (Australian Taxation Office, 2011).

(b) An Australian individual who is a non-resident with a taxable income of $18,000.

The income tax that is to be levied on a non-resident of Australia is to be levied at the rate of

32.5% of his total income therefore total tax that is to be payable is to be calculated as:

=$18,000*32.5

=$5850

(c) An Australian company with a taxable income of $18,000.

The tax rate that is applicable in the present case is 30% wherein the company has been

considered to be not belonging to small business entities. Thus the income tax that is to be

paid is

=$18,000*30%

=$5850

(d) An Australian company with a taxable income of $18,000.

The tax slab that provides for levying of tax rate on different income are herein provided on

which total income tax payable is to be determined :

Income Tax rate Payable income tax

0- 18,200 0% None

418,201-$ 37,000 19% 18,800*19=$3,572

$37,001 to $87,000 32.5% $50,000 × 32.5% = $16,250

$87,001 to $145,000 37% $58,000 × 37% = $21,460

Thus, total income tax to be paid is $3,572+$16,250+$21,460 = $41,282

4

Calculate the income tax payable, ignoring the Medicare levy, for the following taxpayers for the

year ended 30 June 2017:

(a) An Australian individual who is a resident with a taxable income of $18,000.

In present case, the liability of the Australian individual to pay income tax is related to his

taxable income. There is no taxable liability that can be imposed on his income. The

provision as provide under income tax rules provides that any individual who is earning

income below threshold of $18000 will fall under exemption limits in respect of his liability

to pay income tax (Australian Taxation Office, 2011).

(b) An Australian individual who is a non-resident with a taxable income of $18,000.

The income tax that is to be levied on a non-resident of Australia is to be levied at the rate of

32.5% of his total income therefore total tax that is to be payable is to be calculated as:

=$18,000*32.5

=$5850

(c) An Australian company with a taxable income of $18,000.

The tax rate that is applicable in the present case is 30% wherein the company has been

considered to be not belonging to small business entities. Thus the income tax that is to be

paid is

=$18,000*30%

=$5850

(d) An Australian company with a taxable income of $18,000.

The tax slab that provides for levying of tax rate on different income are herein provided on

which total income tax payable is to be determined :

Income Tax rate Payable income tax

0- 18,200 0% None

418,201-$ 37,000 19% 18,800*19=$3,572

$37,001 to $87,000 32.5% $50,000 × 32.5% = $16,250

$87,001 to $145,000 37% $58,000 × 37% = $21,460

Thus, total income tax to be paid is $3,572+$16,250+$21,460 = $41,282

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

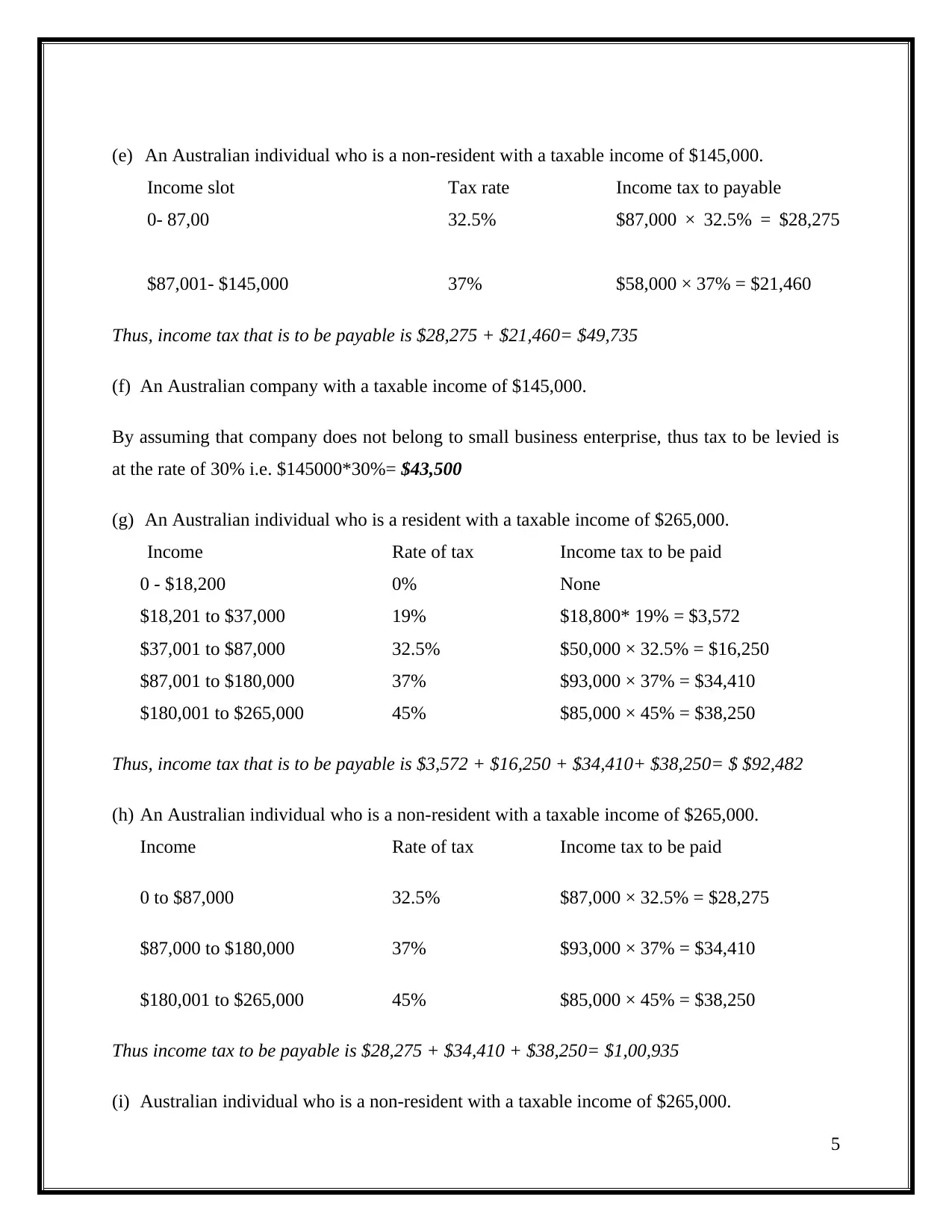

(e) An Australian individual who is a non-resident with a taxable income of $145,000.

Income slot Tax rate Income tax to payable

0- 87,00 32.5% $87,000 × 32.5% = $28,275

$87,001- $145,000 37% $58,000 × 37% = $21,460

Thus, income tax that is to be payable is $28,275 + $21,460= $49,735

(f) An Australian company with a taxable income of $145,000.

By assuming that company does not belong to small business enterprise, thus tax to be levied is

at the rate of 30% i.e. $145000*30%= $43,500

(g) An Australian individual who is a resident with a taxable income of $265,000.

Income Rate of tax Income tax to be paid

0 - $18,200 0% None

$18,201 to $37,000 19% $18,800* 19% = $3,572

$37,001 to $87,000 32.5% $50,000 × 32.5% = $16,250

$87,001 to $180,000 37% $93,000 × 37% = $34,410

$180,001 to $265,000 45% $85,000 × 45% = $38,250

Thus, income tax that is to be payable is $3,572 + $16,250 + $34,410+ $38,250= $ $92,482

(h) An Australian individual who is a non-resident with a taxable income of $265,000.

Income Rate of tax Income tax to be paid

0 to $87,000 32.5% $87,000 × 32.5% = $28,275

$87,000 to $180,000 37% $93,000 × 37% = $34,410

$180,001 to $265,000 45% $85,000 × 45% = $38,250

Thus income tax to be payable is $28,275 + $34,410 + $38,250= $1,00,935

(i) Australian individual who is a non-resident with a taxable income of $265,000.

5

Income slot Tax rate Income tax to payable

0- 87,00 32.5% $87,000 × 32.5% = $28,275

$87,001- $145,000 37% $58,000 × 37% = $21,460

Thus, income tax that is to be payable is $28,275 + $21,460= $49,735

(f) An Australian company with a taxable income of $145,000.

By assuming that company does not belong to small business enterprise, thus tax to be levied is

at the rate of 30% i.e. $145000*30%= $43,500

(g) An Australian individual who is a resident with a taxable income of $265,000.

Income Rate of tax Income tax to be paid

0 - $18,200 0% None

$18,201 to $37,000 19% $18,800* 19% = $3,572

$37,001 to $87,000 32.5% $50,000 × 32.5% = $16,250

$87,001 to $180,000 37% $93,000 × 37% = $34,410

$180,001 to $265,000 45% $85,000 × 45% = $38,250

Thus, income tax that is to be payable is $3,572 + $16,250 + $34,410+ $38,250= $ $92,482

(h) An Australian individual who is a non-resident with a taxable income of $265,000.

Income Rate of tax Income tax to be paid

0 to $87,000 32.5% $87,000 × 32.5% = $28,275

$87,000 to $180,000 37% $93,000 × 37% = $34,410

$180,001 to $265,000 45% $85,000 × 45% = $38,250

Thus income tax to be payable is $28,275 + $34,410 + $38,250= $1,00,935

(i) Australian individual who is a non-resident with a taxable income of $265,000.

5

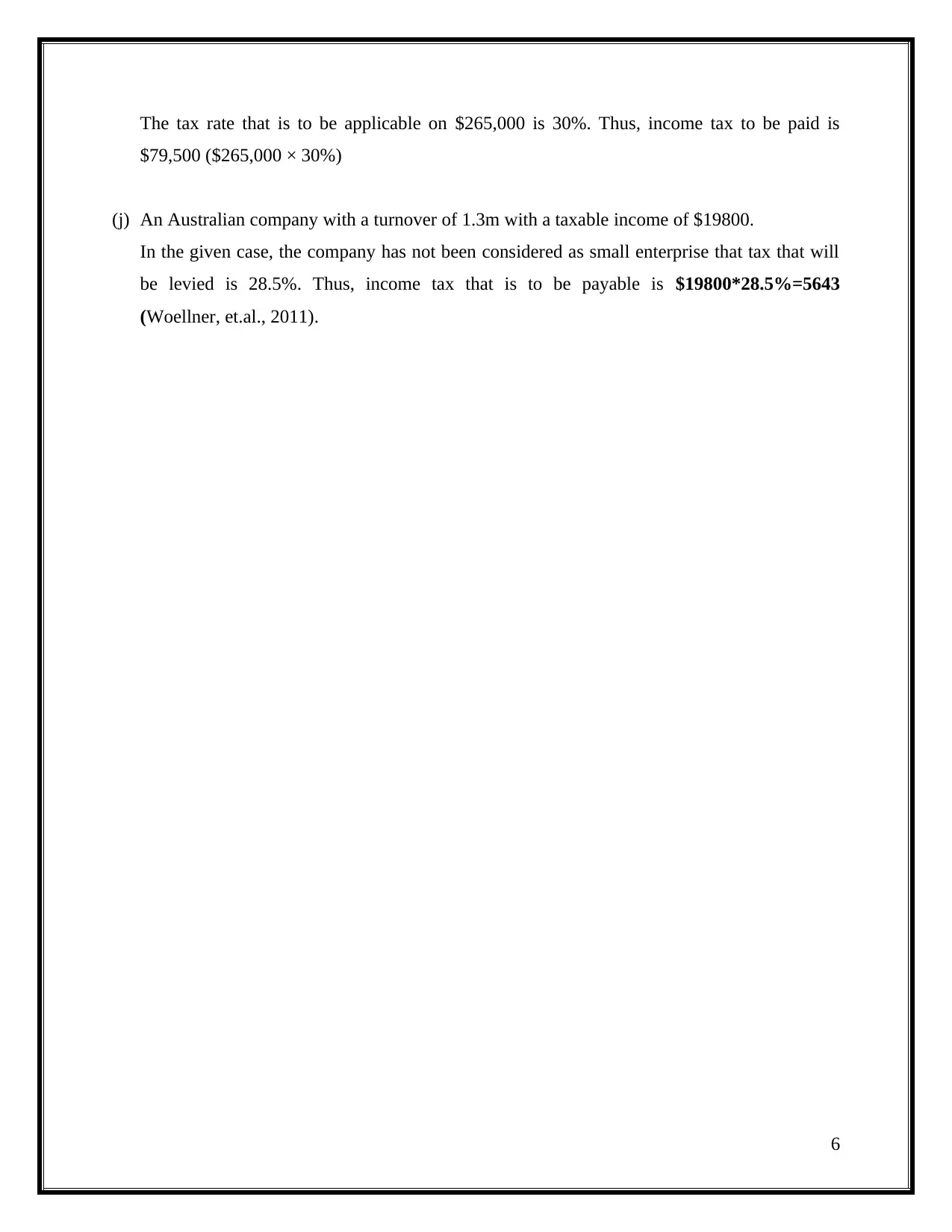

The tax rate that is to be applicable on $265,000 is 30%. Thus, income tax to be paid is

$79,500 ($265,000 × 30%)

(j) An Australian company with a turnover of 1.3m with a taxable income of $19800.

In the given case, the company has not been considered as small enterprise that tax that will

be levied is 28.5%. Thus, income tax that is to be payable is $19800*28.5%=5643

(Woellner, et.al., 2011).

6

$79,500 ($265,000 × 30%)

(j) An Australian company with a turnover of 1.3m with a taxable income of $19800.

In the given case, the company has not been considered as small enterprise that tax that will

be levied is 28.5%. Thus, income tax that is to be payable is $19800*28.5%=5643

(Woellner, et.al., 2011).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

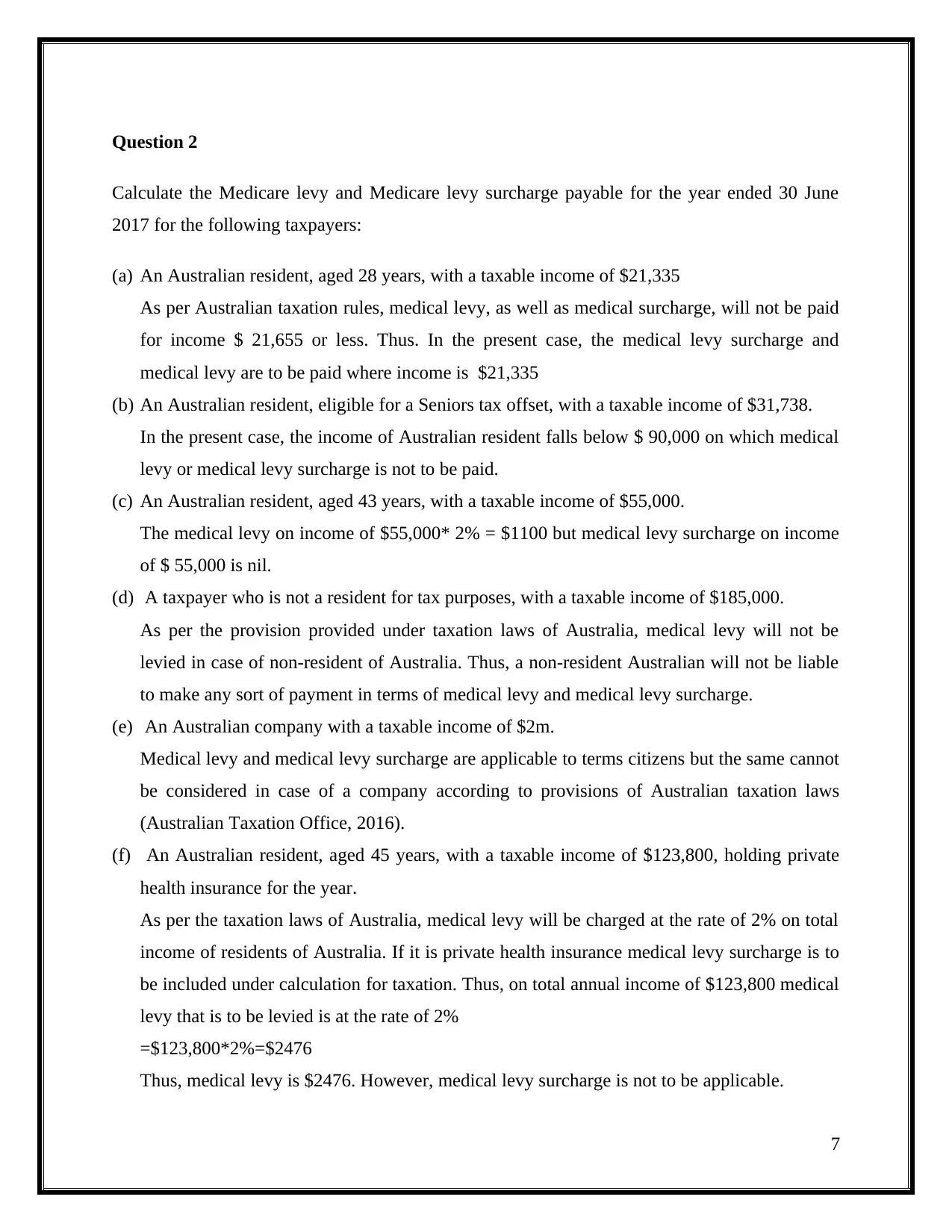

Question 2

Calculate the Medicare levy and Medicare levy surcharge payable for the year ended 30 June

2017 for the following taxpayers:

(a) An Australian resident, aged 28 years, with a taxable income of $21,335

As per Australian taxation rules, medical levy, as well as medical surcharge, will not be paid

for income $ 21,655 or less. Thus. In the present case, the medical levy surcharge and

medical levy are to be paid where income is $21,335

(b) An Australian resident, eligible for a Seniors tax offset, with a taxable income of $31,738.

In the present case, the income of Australian resident falls below $ 90,000 on which medical

levy or medical levy surcharge is not to be paid.

(c) An Australian resident, aged 43 years, with a taxable income of $55,000.

The medical levy on income of $55,000* 2% = $1100 but medical levy surcharge on income

of $ 55,000 is nil.

(d) A taxpayer who is not a resident for tax purposes, with a taxable income of $185,000.

As per the provision provided under taxation laws of Australia, medical levy will not be

levied in case of non-resident of Australia. Thus, a non-resident Australian will not be liable

to make any sort of payment in terms of medical levy and medical levy surcharge.

(e) An Australian company with a taxable income of $2m.

Medical levy and medical levy surcharge are applicable to terms citizens but the same cannot

be considered in case of a company according to provisions of Australian taxation laws

(Australian Taxation Office, 2016).

(f) An Australian resident, aged 45 years, with a taxable income of $123,800, holding private

health insurance for the year.

As per the taxation laws of Australia, medical levy will be charged at the rate of 2% on total

income of residents of Australia. If it is private health insurance medical levy surcharge is to

be included under calculation for taxation. Thus, on total annual income of $123,800 medical

levy that is to be levied is at the rate of 2%

=$123,800*2%=$2476

Thus, medical levy is $2476. However, medical levy surcharge is not to be applicable.

7

Calculate the Medicare levy and Medicare levy surcharge payable for the year ended 30 June

2017 for the following taxpayers:

(a) An Australian resident, aged 28 years, with a taxable income of $21,335

As per Australian taxation rules, medical levy, as well as medical surcharge, will not be paid

for income $ 21,655 or less. Thus. In the present case, the medical levy surcharge and

medical levy are to be paid where income is $21,335

(b) An Australian resident, eligible for a Seniors tax offset, with a taxable income of $31,738.

In the present case, the income of Australian resident falls below $ 90,000 on which medical

levy or medical levy surcharge is not to be paid.

(c) An Australian resident, aged 43 years, with a taxable income of $55,000.

The medical levy on income of $55,000* 2% = $1100 but medical levy surcharge on income

of $ 55,000 is nil.

(d) A taxpayer who is not a resident for tax purposes, with a taxable income of $185,000.

As per the provision provided under taxation laws of Australia, medical levy will not be

levied in case of non-resident of Australia. Thus, a non-resident Australian will not be liable

to make any sort of payment in terms of medical levy and medical levy surcharge.

(e) An Australian company with a taxable income of $2m.

Medical levy and medical levy surcharge are applicable to terms citizens but the same cannot

be considered in case of a company according to provisions of Australian taxation laws

(Australian Taxation Office, 2016).

(f) An Australian resident, aged 45 years, with a taxable income of $123,800, holding private

health insurance for the year.

As per the taxation laws of Australia, medical levy will be charged at the rate of 2% on total

income of residents of Australia. If it is private health insurance medical levy surcharge is to

be included under calculation for taxation. Thus, on total annual income of $123,800 medical

levy that is to be levied is at the rate of 2%

=$123,800*2%=$2476

Thus, medical levy is $2476. However, medical levy surcharge is not to be applicable.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

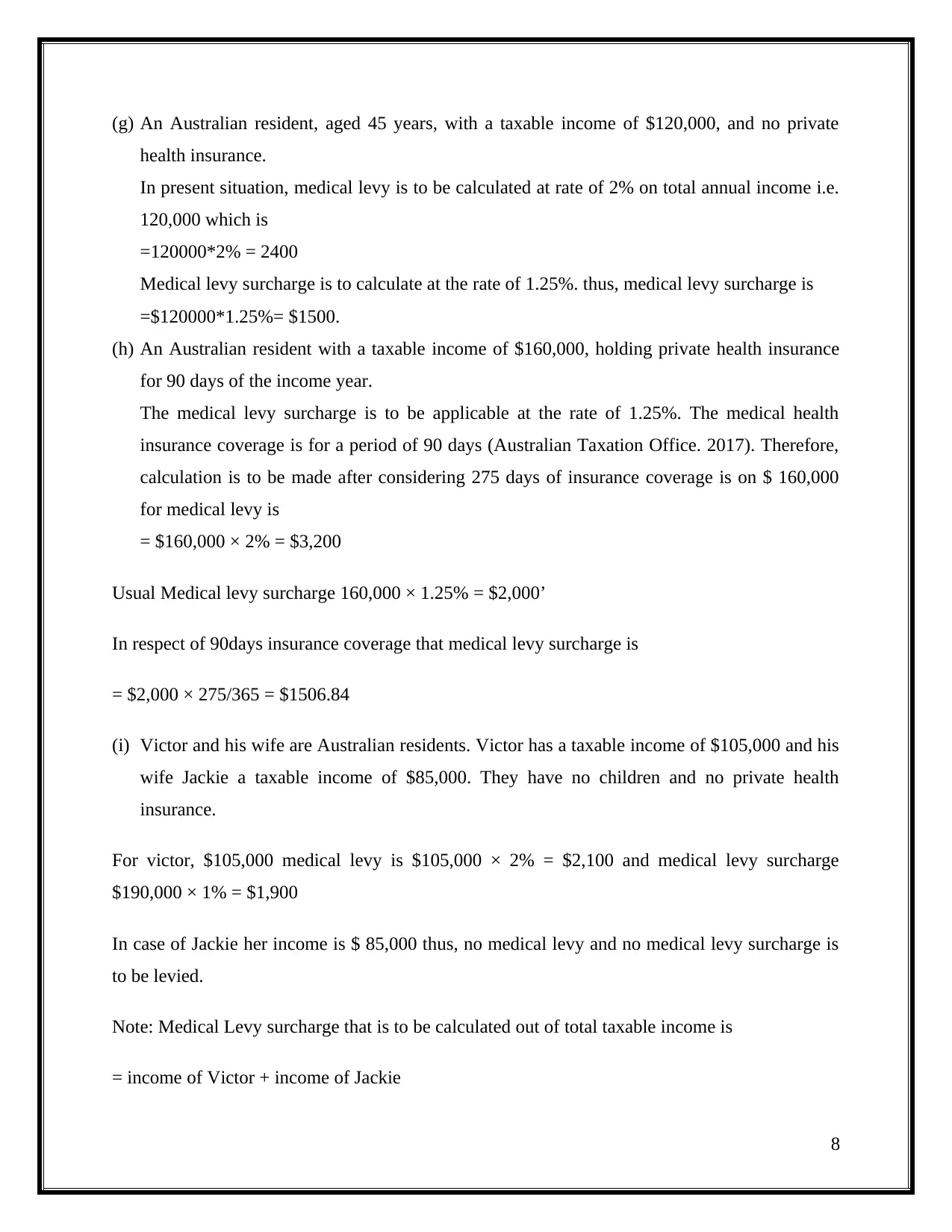

(g) An Australian resident, aged 45 years, with a taxable income of $120,000, and no private

health insurance.

In present situation, medical levy is to be calculated at rate of 2% on total annual income i.e.

120,000 which is

=120000*2% = 2400

Medical levy surcharge is to calculate at the rate of 1.25%. thus, medical levy surcharge is

=$120000*1.25%= $1500.

(h) An Australian resident with a taxable income of $160,000, holding private health insurance

for 90 days of the income year.

The medical levy surcharge is to be applicable at the rate of 1.25%. The medical health

insurance coverage is for a period of 90 days (Australian Taxation Office. 2017). Therefore,

calculation is to be made after considering 275 days of insurance coverage is on $ 160,000

for medical levy is

= $160,000 × 2% = $3,200

Usual Medical levy surcharge 160,000 × 1.25% = $2,000’

In respect of 90days insurance coverage that medical levy surcharge is

= $2,000 × 275/365 = $1506.84

(i) Victor and his wife are Australian residents. Victor has a taxable income of $105,000 and his

wife Jackie a taxable income of $85,000. They have no children and no private health

insurance.

For victor, $105,000 medical levy is $105,000 × 2% = $2,100 and medical levy surcharge

$190,000 × 1% = $1,900

In case of Jackie her income is $ 85,000 thus, no medical levy and no medical levy surcharge is

to be levied.

Note: Medical Levy surcharge that is to be calculated out of total taxable income is

= income of Victor + income of Jackie

8

health insurance.

In present situation, medical levy is to be calculated at rate of 2% on total annual income i.e.

120,000 which is

=120000*2% = 2400

Medical levy surcharge is to calculate at the rate of 1.25%. thus, medical levy surcharge is

=$120000*1.25%= $1500.

(h) An Australian resident with a taxable income of $160,000, holding private health insurance

for 90 days of the income year.

The medical levy surcharge is to be applicable at the rate of 1.25%. The medical health

insurance coverage is for a period of 90 days (Australian Taxation Office. 2017). Therefore,

calculation is to be made after considering 275 days of insurance coverage is on $ 160,000

for medical levy is

= $160,000 × 2% = $3,200

Usual Medical levy surcharge 160,000 × 1.25% = $2,000’

In respect of 90days insurance coverage that medical levy surcharge is

= $2,000 × 275/365 = $1506.84

(i) Victor and his wife are Australian residents. Victor has a taxable income of $105,000 and his

wife Jackie a taxable income of $85,000. They have no children and no private health

insurance.

For victor, $105,000 medical levy is $105,000 × 2% = $2,100 and medical levy surcharge

$190,000 × 1% = $1,900

In case of Jackie her income is $ 85,000 thus, no medical levy and no medical levy surcharge is

to be levied.

Note: Medical Levy surcharge that is to be calculated out of total taxable income is

= income of Victor + income of Jackie

8

=$105000+85000=$190000

Thus, medical levy and medical levy surcharge are to be calculated on income of Victor.

(j) An Australian couple has four children and no private hospital health insurance. What would

be the family's minimum Medicare levy surcharge threshold?

The medical levy surcharge threshold limit is

=180,000

For every child, after first child, the family threshold is increased by 1,500

Thus, in present case,

=1,500* (4-1) = 1,500*3= $4,500

Thus, minimum Medicare levy surcharge threshold is 180,000 + 4500= $184,500.

9

Thus, medical levy and medical levy surcharge are to be calculated on income of Victor.

(j) An Australian couple has four children and no private hospital health insurance. What would

be the family's minimum Medicare levy surcharge threshold?

The medical levy surcharge threshold limit is

=180,000

For every child, after first child, the family threshold is increased by 1,500

Thus, in present case,

=1,500* (4-1) = 1,500*3= $4,500

Thus, minimum Medicare levy surcharge threshold is 180,000 + 4500= $184,500.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 3

You client, Rob, has the following income and deductions for the financial year ended 30 June

2017: salary, $32,000; bank interest received, $150; and allowable deductions for special work

clothing, $450. Rob’s employer has deducted $2600 as PAYG tax from his salary during the

year.

Calculate Rob’s income tax payable or refundable.

Solution

Section 4-15 of ITAA, 1997 provides for taxable income:

I- Taxable income for Rob for 30 June 2017

Particulars Amount

Salary $32,000

Bank

Interest

(+) $150

Clothing

Allowable

deductions

(-) $450

Income to be

taxed

$31,700

II- Taxable liability of Rob as provided under ITRA 1986

10

You client, Rob, has the following income and deductions for the financial year ended 30 June

2017: salary, $32,000; bank interest received, $150; and allowable deductions for special work

clothing, $450. Rob’s employer has deducted $2600 as PAYG tax from his salary during the

year.

Calculate Rob’s income tax payable or refundable.

Solution

Section 4-15 of ITAA, 1997 provides for taxable income:

I- Taxable income for Rob for 30 June 2017

Particulars Amount

Salary $32,000

Bank

Interest

(+) $150

Clothing

Allowable

deductions

(-) $450

Income to be

taxed

$31,700

II- Taxable liability of Rob as provided under ITRA 1986

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

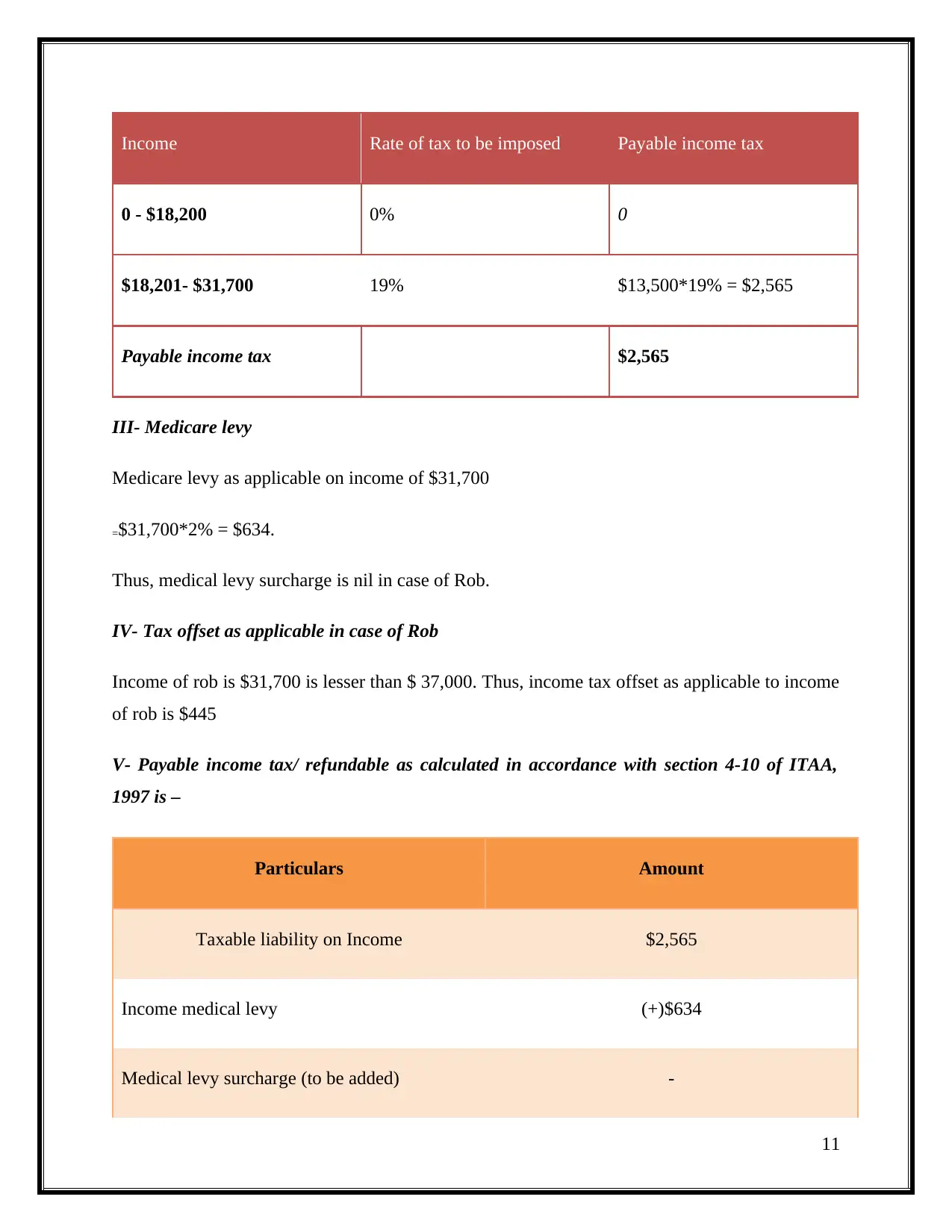

Income Rate of tax to be imposed Payable income tax

0 - $18,200 0% 0

$18,201- $31,700 19% $13,500*19% = $2,565

Payable income tax $2,565

III- Medicare levy

Medicare levy as applicable on income of $31,700

=$31,700*2% = $634.

Thus, medical levy surcharge is nil in case of Rob.

IV- Tax offset as applicable in case of Rob

Income of rob is $31,700 is lesser than $ 37,000. Thus, income tax offset as applicable to income

of rob is $445

V- Payable income tax/ refundable as calculated in accordance with section 4-10 of ITAA,

1997 is –

Particulars Amount

Taxable liability on Income $2,565

Income medical levy (+)$634

Medical levy surcharge (to be added) -

11

0 - $18,200 0% 0

$18,201- $31,700 19% $13,500*19% = $2,565

Payable income tax $2,565

III- Medicare levy

Medicare levy as applicable on income of $31,700

=$31,700*2% = $634.

Thus, medical levy surcharge is nil in case of Rob.

IV- Tax offset as applicable in case of Rob

Income of rob is $31,700 is lesser than $ 37,000. Thus, income tax offset as applicable to income

of rob is $445

V- Payable income tax/ refundable as calculated in accordance with section 4-10 of ITAA,

1997 is –

Particulars Amount

Taxable liability on Income $2,565

Income medical levy (+)$634

Medical levy surcharge (to be added) -

11

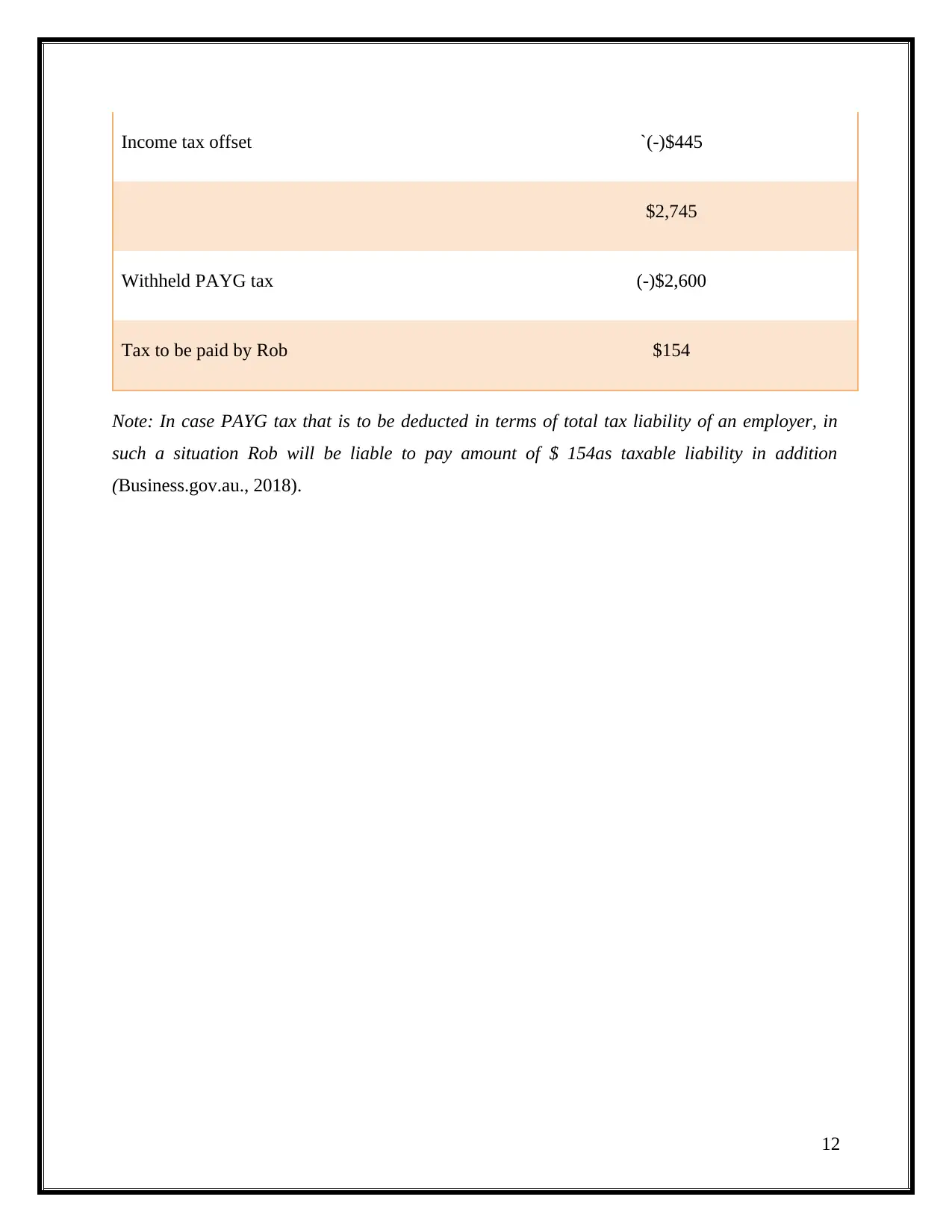

Income tax offset `(-)$445

$2,745

Withheld PAYG tax (-)$2,600

Tax to be paid by Rob $154

Note: In case PAYG tax that is to be deducted in terms of total tax liability of an employer, in

such a situation Rob will be liable to pay amount of $ 154as taxable liability in addition

(Business.gov.au., 2018).

12

$2,745

Withheld PAYG tax (-)$2,600

Tax to be paid by Rob $154

Note: In case PAYG tax that is to be deducted in terms of total tax liability of an employer, in

such a situation Rob will be liable to pay amount of $ 154as taxable liability in addition

(Business.gov.au., 2018).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.