HA3042 Taxation Law: Analyzing Income, Benefits, and Tax Avoidance

VerifiedAdded on 2023/06/04

|12

|3420

|217

Report

AI Summary

This report delves into various aspects of Australian taxation law through several case studies and scenarios. It addresses whether annual lottery commission payments constitute income, examines the calculation of taxable income for a pharmacy considering the Pharmaceutical Benefits Scheme (PBS), explains the principle applied in the IRC v Duke of Westminster case regarding tax avoidance, and analyzes the allocation of losses and capital gains for tax purposes. The report references relevant legislation such as the Income Tax Assessment Act and the National Health Act, providing a comprehensive overview of the legal and financial implications discussed. Desklib offers a wealth of similar resources for students seeking to enhance their understanding of complex legal and financial topics.

Running Head: TAXATION LAW

TAXATION LAW

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW 2

Table of Contents

Table of Contents.............................................................................................................................2

Introduction......................................................................................................................................3

Question 1: Explain with reason if annual payment of commission is income...............................3

Question 2: Calculate the taxable income of Corner Pharmacy and explain the Pharmaceuticals

benefit schemes................................................................................................................................5

Question 3: Explaining the Principle applied in IRC v Duke of Westminster [1936] AC 1...........7

Question 4: Explain how the loss incurred by Joseph is allocated for the purpose of the tax.

Evaluate its capital gain or loss.......................................................................................................9

References......................................................................................................................................11

Table of Contents

Table of Contents.............................................................................................................................2

Introduction......................................................................................................................................3

Question 1: Explain with reason if annual payment of commission is income...............................3

Question 2: Calculate the taxable income of Corner Pharmacy and explain the Pharmaceuticals

benefit schemes................................................................................................................................5

Question 3: Explaining the Principle applied in IRC v Duke of Westminster [1936] AC 1...........7

Question 4: Explain how the loss incurred by Joseph is allocated for the purpose of the tax.

Evaluate its capital gain or loss.......................................................................................................9

References......................................................................................................................................11

TAXATION LAW 3

Introduction

Taxation is the process of collecting contribution from the individual by the government. It is a

kind of charges imposed on service rendered or charging fine on breaches. The characteristics of

a tax are not linked directly with tax payment or provision of service. The case study is

emphasising the law of taxation in Australia based on the distinct scenario and determining the

rules that are applied in the significant case. In the first case, a taxation law of Income-tax

Assessment ACT of 1978 is applied to the treatment of lottery winning is determined. The

Pharmaceuticals Benefits Scheme is recognised for understanding the concept of taxable income

under the National Health Act 1953. This law is applied to income and expenditure by the

Australian Pharmacy. The issue of tax avoidance was raised in the case of IRC vs Duke of

Westminster which determined, whether the applicable principle is relevant or not.

Question 1: Explain with reason if annual payment of commission is income

Issue

A lottery commission conducted a lottery naming ‘Set for Life' and offered to pay $ 50000 each

year for consecutive 20 years to the winner who scratches three lotteries of ‘Set for Life'. The

first payment of $ 50000 is allowable when the winner is declared. A second payment is

allowable on the anniversary of initial payment. The issue arises in the instance when the

payment of the lottery would be made to the deceased estate after the death of winner. The issue

requires to be resolved if the annual payment to be paid to deceased estates accounts as income

or not.

Rule

Each of the lottery winners is taxable for such income by the Federal government. In a case when

the winner dies the tax is to be paid by the beneficiaries. As per the Rules of 2014 Registration

24 each of the lottery winnings is not taxable as sources like ordinary income1. The HM customs

does not consider the lottery prize as income and thus the amount is tax-free. According to the

Income Tax Assessment Act 1936, the beneficiary after the death of the winner receives a lump

1 classic.austlii.edu.au (2018), Legislation of commission on lottery. Available at: Retrieved on 22nd September

2018 from http://classic.austlii.edu.au/au/legis/wa/consol_reg/lcflr2014408/s24.html [Accessed on: 22nd September

2018]

Introduction

Taxation is the process of collecting contribution from the individual by the government. It is a

kind of charges imposed on service rendered or charging fine on breaches. The characteristics of

a tax are not linked directly with tax payment or provision of service. The case study is

emphasising the law of taxation in Australia based on the distinct scenario and determining the

rules that are applied in the significant case. In the first case, a taxation law of Income-tax

Assessment ACT of 1978 is applied to the treatment of lottery winning is determined. The

Pharmaceuticals Benefits Scheme is recognised for understanding the concept of taxable income

under the National Health Act 1953. This law is applied to income and expenditure by the

Australian Pharmacy. The issue of tax avoidance was raised in the case of IRC vs Duke of

Westminster which determined, whether the applicable principle is relevant or not.

Question 1: Explain with reason if annual payment of commission is income

Issue

A lottery commission conducted a lottery naming ‘Set for Life' and offered to pay $ 50000 each

year for consecutive 20 years to the winner who scratches three lotteries of ‘Set for Life'. The

first payment of $ 50000 is allowable when the winner is declared. A second payment is

allowable on the anniversary of initial payment. The issue arises in the instance when the

payment of the lottery would be made to the deceased estate after the death of winner. The issue

requires to be resolved if the annual payment to be paid to deceased estates accounts as income

or not.

Rule

Each of the lottery winners is taxable for such income by the Federal government. In a case when

the winner dies the tax is to be paid by the beneficiaries. As per the Rules of 2014 Registration

24 each of the lottery winnings is not taxable as sources like ordinary income1. The HM customs

does not consider the lottery prize as income and thus the amount is tax-free. According to the

Income Tax Assessment Act 1936, the beneficiary after the death of the winner receives a lump

1 classic.austlii.edu.au (2018), Legislation of commission on lottery. Available at: Retrieved on 22nd September

2018 from http://classic.austlii.edu.au/au/legis/wa/consol_reg/lcflr2014408/s24.html [Accessed on: 22nd September

2018]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW 4

sum amount from a lottery winning. When the amount of lottery winning is banked then the

amount could be made taxable from source2. The beneficiary would be liable to pay tax on such

income at 40% as inheritance tax. A simple drafted agreement with a sign of beneficiaries would

save the lottery syndicates from the risk of non- payment of tax on lottery winning amount.

Analysis- the issue of lottery commission determines, whether to treat the lottery winnings as

income or not. As per the Australia Income-tax Rules, it is mentioned that cash received by a

beneficiary is a part of the estate3. The federal estate tax includes the received amount of lottery

winning amount after the death of the winner to be valued on a fair market rate. The HM

Revenue & Customs (HMRC) would tax the lottery winning amount in the scale of Inheritance

Tax (IHT). The scale of taxation is as follows

Reduction of tax by 20 % is the winner dies after gifting the amount in 3 to 4 years

Reduction of the tax rate by 40 % for year exceeding the death of 4 to 5 years after gifting

The whole matter of taxation on the winning amount depends on the assurance if the beneficiary

signed for paying the due tax as per agreement if the winner dies in 7 years4.

Conclusion- The above analysis on the treatment of lottery winning is concluded as annual

payment income of the beneficiaries if it is banked and liable for payment of tax on such amount

as Inheritance tax of 40%. It is concluded after the analysis that the beneficiaries would have to

sign an agreement before the winner dies for paying off the remaining tax after the death of

winner. The taxable rate on the lottery winning amount reduces as per the death tenure sectioned

under the rules of HM Revenue & Customs. The reduction on taxation rate is 20 % before 3 to 4

years and 40 % reduction if the deaths occur before 4 to 5 years of winning.

2 Kleven, H.J. and Schultz, E.A., 2014. Estimating taxable income responses using Danish tax reforms. American

Economic Journal: Economic Policy, 6(4), pp.271-301.

3theguardian.com (2018), Do you pay tax on lottery win. Available at:

https://www.theguardian.com/money/2012/sep/10/do-you-pay-tax-lottery-win [Accessed on: 22nd September 2018]

4 Koessler, A.K., Torgler, B., Feld, L.P. and Frey, B.S., 2016. Commitment to pay taxes: a field experiment on the

importance of promise.

sum amount from a lottery winning. When the amount of lottery winning is banked then the

amount could be made taxable from source2. The beneficiary would be liable to pay tax on such

income at 40% as inheritance tax. A simple drafted agreement with a sign of beneficiaries would

save the lottery syndicates from the risk of non- payment of tax on lottery winning amount.

Analysis- the issue of lottery commission determines, whether to treat the lottery winnings as

income or not. As per the Australia Income-tax Rules, it is mentioned that cash received by a

beneficiary is a part of the estate3. The federal estate tax includes the received amount of lottery

winning amount after the death of the winner to be valued on a fair market rate. The HM

Revenue & Customs (HMRC) would tax the lottery winning amount in the scale of Inheritance

Tax (IHT). The scale of taxation is as follows

Reduction of tax by 20 % is the winner dies after gifting the amount in 3 to 4 years

Reduction of the tax rate by 40 % for year exceeding the death of 4 to 5 years after gifting

The whole matter of taxation on the winning amount depends on the assurance if the beneficiary

signed for paying the due tax as per agreement if the winner dies in 7 years4.

Conclusion- The above analysis on the treatment of lottery winning is concluded as annual

payment income of the beneficiaries if it is banked and liable for payment of tax on such amount

as Inheritance tax of 40%. It is concluded after the analysis that the beneficiaries would have to

sign an agreement before the winner dies for paying off the remaining tax after the death of

winner. The taxable rate on the lottery winning amount reduces as per the death tenure sectioned

under the rules of HM Revenue & Customs. The reduction on taxation rate is 20 % before 3 to 4

years and 40 % reduction if the deaths occur before 4 to 5 years of winning.

2 Kleven, H.J. and Schultz, E.A., 2014. Estimating taxable income responses using Danish tax reforms. American

Economic Journal: Economic Policy, 6(4), pp.271-301.

3theguardian.com (2018), Do you pay tax on lottery win. Available at:

https://www.theguardian.com/money/2012/sep/10/do-you-pay-tax-lottery-win [Accessed on: 22nd September 2018]

4 Koessler, A.K., Torgler, B., Feld, L.P. and Frey, B.S., 2016. Commitment to pay taxes: a field experiment on the

importance of promise.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW 5

Question 2: Calculate the taxable income of Corner Pharmacy and explain the

Pharmaceuticals benefit schemes

Issue

The corner pharmacy is having a chemist shop which does not prefer to operate its business in

credit. However, it accepts credit cards for sales and fills up the prescriptions as per the schemes

mentioned under Pharmaceutical benefit schemes. The issues arise considering the taxable

income that is required is to be paid by Corner Pharmacy. The operational performance recorded

for sales or purchases, on stocks, salaries and rents charges made by a pharmacy for the financial

year is required to determine its taxable income. The taxable income of Corner pharmacy

considers that each transaction on accrual basis applies both costs of sales in cash and credit card

sales5.

Rules

The Pharmaceutical benefits claims consist of both original and the carbon copy of the claim for

reimbursement. The costs of medicines are subsidies as per the Australian government under

PBS. The antibiotics are available for Australian at free of cost which was introduced in 1944 by

Curtin Labour6. The Pharmaceutical benefits scheme is laid down under the National Health Act

1953 for positive results and proper use of medicines. The expenditure under PBS has remained

uncapped which could be increased by new drugs and increases the demands. A concession to

the patient under the PBS is provided to both the cardholder and general patients. Patient co-

payments provide a concession of $6.20 on the purchase of medicine and $ 38.20 for the general

patients7.

Analysis

5 Burns, S.K. and Ziliak, J.P., 2017. Identifying the elasticity of taxable income. The Economic Journal, 127(600),

pp.297-329.

6aph.gov.au (2018), Parliamentary Department of PBS. Available at:

https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/rp/rp1516/

Quick_Guides/PBS [Accessed on: 22nd September 2018]

7 Harris, C.A., Daniels, B., Ward, R.L. and Pearson, S.A., 2017. Retrospective comparison of Australia's

Pharmaceutical Benefits Scheme claims data with prescription data in HER2-positive early breast cancer patients,

2008-2012. Public Health Research and Practice, 27(5), pp.1-9.

Question 2: Calculate the taxable income of Corner Pharmacy and explain the

Pharmaceuticals benefit schemes

Issue

The corner pharmacy is having a chemist shop which does not prefer to operate its business in

credit. However, it accepts credit cards for sales and fills up the prescriptions as per the schemes

mentioned under Pharmaceutical benefit schemes. The issues arise considering the taxable

income that is required is to be paid by Corner Pharmacy. The operational performance recorded

for sales or purchases, on stocks, salaries and rents charges made by a pharmacy for the financial

year is required to determine its taxable income. The taxable income of Corner pharmacy

considers that each transaction on accrual basis applies both costs of sales in cash and credit card

sales5.

Rules

The Pharmaceutical benefits claims consist of both original and the carbon copy of the claim for

reimbursement. The costs of medicines are subsidies as per the Australian government under

PBS. The antibiotics are available for Australian at free of cost which was introduced in 1944 by

Curtin Labour6. The Pharmaceutical benefits scheme is laid down under the National Health Act

1953 for positive results and proper use of medicines. The expenditure under PBS has remained

uncapped which could be increased by new drugs and increases the demands. A concession to

the patient under the PBS is provided to both the cardholder and general patients. Patient co-

payments provide a concession of $6.20 on the purchase of medicine and $ 38.20 for the general

patients7.

Analysis

5 Burns, S.K. and Ziliak, J.P., 2017. Identifying the elasticity of taxable income. The Economic Journal, 127(600),

pp.297-329.

6aph.gov.au (2018), Parliamentary Department of PBS. Available at:

https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/rp/rp1516/

Quick_Guides/PBS [Accessed on: 22nd September 2018]

7 Harris, C.A., Daniels, B., Ward, R.L. and Pearson, S.A., 2017. Retrospective comparison of Australia's

Pharmaceutical Benefits Scheme claims data with prescription data in HER2-positive early breast cancer patients,

2008-2012. Public Health Research and Practice, 27(5), pp.1-9.

TAXATION LAW 6

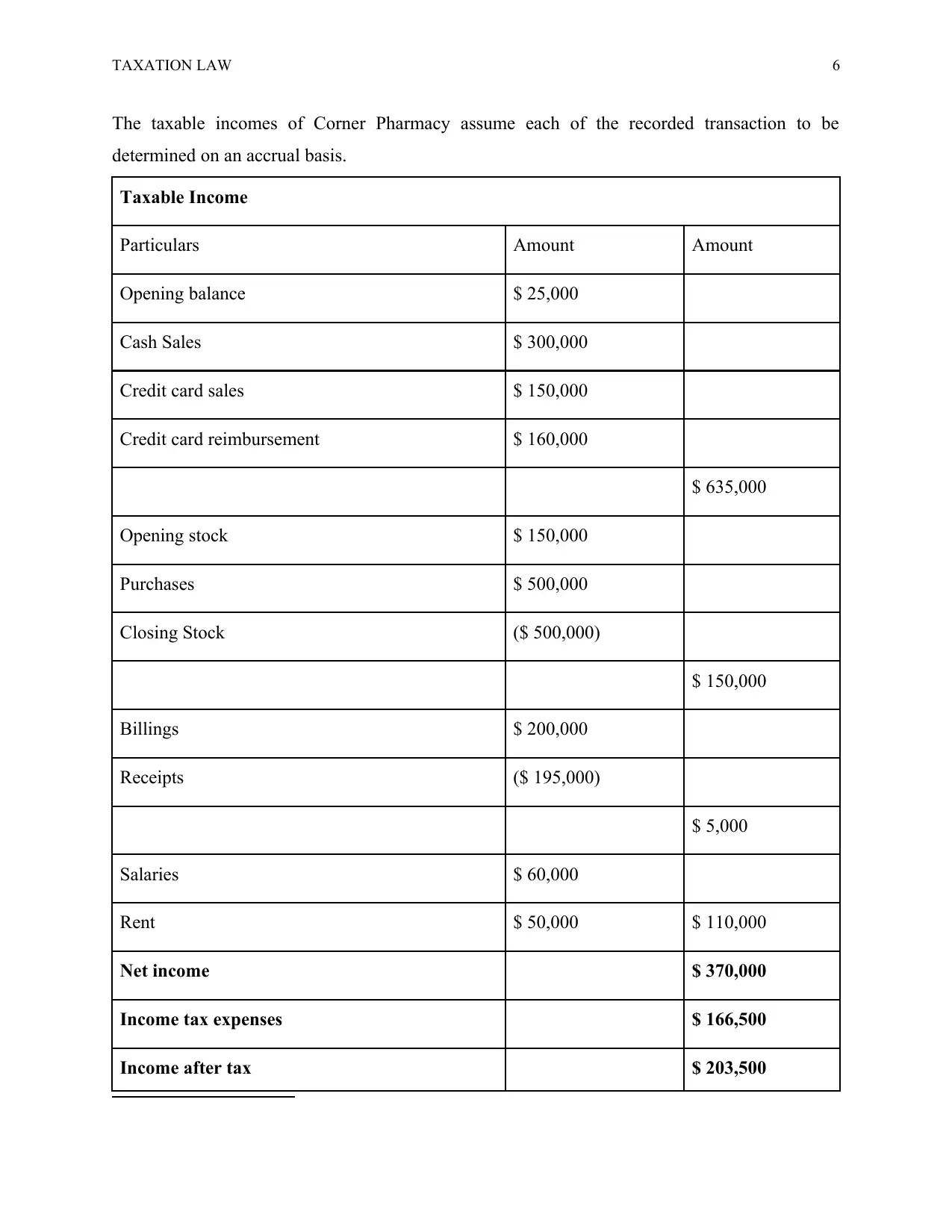

The taxable incomes of Corner Pharmacy assume each of the recorded transaction to be

determined on an accrual basis.

Taxable Income

Particulars Amount Amount

Opening balance $ 25,000

Cash Sales $ 300,000

Credit card sales $ 150,000

Credit card reimbursement $ 160,000

$ 635,000

Opening stock $ 150,000

Purchases $ 500,000

Closing Stock ($ 500,000)

$ 150,000

Billings $ 200,000

Receipts ($ 195,000)

$ 5,000

Salaries $ 60,000

Rent $ 50,000 $ 110,000

Net income $ 370,000

Income tax expenses $ 166,500

Income after tax $ 203,500

The taxable incomes of Corner Pharmacy assume each of the recorded transaction to be

determined on an accrual basis.

Taxable Income

Particulars Amount Amount

Opening balance $ 25,000

Cash Sales $ 300,000

Credit card sales $ 150,000

Credit card reimbursement $ 160,000

$ 635,000

Opening stock $ 150,000

Purchases $ 500,000

Closing Stock ($ 500,000)

$ 150,000

Billings $ 200,000

Receipts ($ 195,000)

$ 5,000

Salaries $ 60,000

Rent $ 50,000 $ 110,000

Net income $ 370,000

Income tax expenses $ 166,500

Income after tax $ 203,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW 7

Table 1: Taxable Income of Corner Pharmacy

(Source: Created by Author)

Under Pharmaceutical schemes, the Corner Pharmacy provides medicine to the patient on both

cash sales and accept credit card. It also attempts to provide accurate prescription on the

purchase. As per the PBS rules the patients would be provided a concession by Corner Pharmacy

which is not mentioned in the record of a financial statement. The net Income approached by

Corner Pharmacy in the financial year is $ 370000. As per the income tax slab of Australia, the

net income of Corner Pharmacy is taxable at the rate of 45 %. The amount of income tax paid by

Corner pharmacy is $ 166500 the net income after tax amounted to $ 203500.

Conclusion

The case scenario of Corner Pharmacy concluded that the taxable rate incurred on the financial

expenditure and income is 45%. The pharmacy was liable to pay the taxable value of $ 166500 at

the end of the financial year. The credit card sales and cash sales are the income of the income of

the Corner pharmacy; therefore the amount is added for determining the taxable income.

Question 3: Explaining the Principle applied in IRC v Duke of Westminster [1936] AC 1

Issue

The case of IRC v Duke of Westminster raised an issue of tax avoidance. The Duke used to

appoint gardener and make payment to them out of the income of Post-tax. Which was essential

according to the Duke of Westminster for reducing the burden of the tax? The Duke drew a

covenant for paying the entire salary to the gardener at the end of a period8.

Duke claimed for deduction of expenses and reduction of tax on income. The Inland Revenue

department challenged Duke for tantamounting the arrangement for evasion of tax.

Rule

According to Income Tax Act 1936 (Cth), the provision of tax avoidance is complicated which is

found in Part IVA of the ITA 1936. The law provides a power to the taxation Commissioner for

cancellation of a tax laid under Part IVA. The Commissioner is involved in making an

assessment if the taxable income and determine the amount after cancelling the tax benefit. The

8 oxfordindex.oup.com (2018), IRC v Duke of Westminster [1936] AC 1, Available at:

http://oxfordindex.oup.com/view/10.1093/oi/authority.20110803121911242 [Accessed on: 22nd September 2018]

Table 1: Taxable Income of Corner Pharmacy

(Source: Created by Author)

Under Pharmaceutical schemes, the Corner Pharmacy provides medicine to the patient on both

cash sales and accept credit card. It also attempts to provide accurate prescription on the

purchase. As per the PBS rules the patients would be provided a concession by Corner Pharmacy

which is not mentioned in the record of a financial statement. The net Income approached by

Corner Pharmacy in the financial year is $ 370000. As per the income tax slab of Australia, the

net income of Corner Pharmacy is taxable at the rate of 45 %. The amount of income tax paid by

Corner pharmacy is $ 166500 the net income after tax amounted to $ 203500.

Conclusion

The case scenario of Corner Pharmacy concluded that the taxable rate incurred on the financial

expenditure and income is 45%. The pharmacy was liable to pay the taxable value of $ 166500 at

the end of the financial year. The credit card sales and cash sales are the income of the income of

the Corner pharmacy; therefore the amount is added for determining the taxable income.

Question 3: Explaining the Principle applied in IRC v Duke of Westminster [1936] AC 1

Issue

The case of IRC v Duke of Westminster raised an issue of tax avoidance. The Duke used to

appoint gardener and make payment to them out of the income of Post-tax. Which was essential

according to the Duke of Westminster for reducing the burden of the tax? The Duke drew a

covenant for paying the entire salary to the gardener at the end of a period8.

Duke claimed for deduction of expenses and reduction of tax on income. The Inland Revenue

department challenged Duke for tantamounting the arrangement for evasion of tax.

Rule

According to Income Tax Act 1936 (Cth), the provision of tax avoidance is complicated which is

found in Part IVA of the ITA 1936. The law provides a power to the taxation Commissioner for

cancellation of a tax laid under Part IVA. The Commissioner is involved in making an

assessment if the taxable income and determine the amount after cancelling the tax benefit. The

8 oxfordindex.oup.com (2018), IRC v Duke of Westminster [1936] AC 1, Available at:

http://oxfordindex.oup.com/view/10.1093/oi/authority.20110803121911242 [Accessed on: 22nd September 2018]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW 8

principles that are applied in the IRC v Duke Westminster 1936 ac 1 was that person is liable to

arrange its affairs lawfully in the purpose of reducing the burden of tax liability9. The rules

mentioned by Lord Tomlin that every individual is liable to arrange the affairs in order to avoid

tax. As per the case scenario, the unappreciative Commissioner is not liable to enforce Duke for

payment of extended tax for such arrangement for his ingenuity.

Analysis

The case studies of IRC vs Duke of Westminster determine the issue of how the Duke appointed

a new gardener every year and makes payment to them from the income of pos-tax. The similar

issue is observed in the case of (THE BRAIN DISORDERS RESEARCH LTD

PARTNERSHIP AND ANOTHER V REVENUE AND CUSTOMS (INCOME TAX – TAX

AVOIDANCE SCHEME): UTTC 8 MAY 2017 10). This arrangement is a kind of principle

applied by Duke for the purpose of avoiding tax. Later the Duke signed a covenant with the

gardener for paying the entire amount after the completion of mentioned period. The Inland

Revenue Commissioner accused Duke of avoiding the payment of tax. However, after attending

the court, Lord Tomlin sentenced lastly that any individual is liable for arranging the affairs of

taxable income for reduction of tax payment. Hence the principle applied by the Duke of

Westminster is observed to be relevant.

Conclusion

The case scenario of IRC v Duke of Westminster concluded that the applicable principle of tax

avoidance by arranging the income and expenditure issue by itself is relevant in the case. The

principle is relevant as per the Income Tax Act 1936 (Cth). The case is thus closed by Lord

Tomlin with a sentence that the accuser could not enforce the accused individual for its

arrangement of affairs for tax evasion.

9 Christians, A., 2014. Avoidance, evasion, and taxpayer morality. Wash. UJL & Pol'y, 44, p.39.

10 fedcourt.gov.au (2018), THE BRAIN DISORDERS RESEARCH LTD PARTNERSHIP AND ANOTHER V

REVENUE AND CUSTOMS (INCOME TAX – TAX AVOIDANCE SCHEME): UTTC 8 MAY 2017), Available

at: http://www.fedcourt.gov.au/digital-law-library/judges-speeches/speeches-former-judges/justice-pagone/201706

[Accessed on: 22nd September 2018]

principles that are applied in the IRC v Duke Westminster 1936 ac 1 was that person is liable to

arrange its affairs lawfully in the purpose of reducing the burden of tax liability9. The rules

mentioned by Lord Tomlin that every individual is liable to arrange the affairs in order to avoid

tax. As per the case scenario, the unappreciative Commissioner is not liable to enforce Duke for

payment of extended tax for such arrangement for his ingenuity.

Analysis

The case studies of IRC vs Duke of Westminster determine the issue of how the Duke appointed

a new gardener every year and makes payment to them from the income of pos-tax. The similar

issue is observed in the case of (THE BRAIN DISORDERS RESEARCH LTD

PARTNERSHIP AND ANOTHER V REVENUE AND CUSTOMS (INCOME TAX – TAX

AVOIDANCE SCHEME): UTTC 8 MAY 2017 10). This arrangement is a kind of principle

applied by Duke for the purpose of avoiding tax. Later the Duke signed a covenant with the

gardener for paying the entire amount after the completion of mentioned period. The Inland

Revenue Commissioner accused Duke of avoiding the payment of tax. However, after attending

the court, Lord Tomlin sentenced lastly that any individual is liable for arranging the affairs of

taxable income for reduction of tax payment. Hence the principle applied by the Duke of

Westminster is observed to be relevant.

Conclusion

The case scenario of IRC v Duke of Westminster concluded that the applicable principle of tax

avoidance by arranging the income and expenditure issue by itself is relevant in the case. The

principle is relevant as per the Income Tax Act 1936 (Cth). The case is thus closed by Lord

Tomlin with a sentence that the accuser could not enforce the accused individual for its

arrangement of affairs for tax evasion.

9 Christians, A., 2014. Avoidance, evasion, and taxpayer morality. Wash. UJL & Pol'y, 44, p.39.

10 fedcourt.gov.au (2018), THE BRAIN DISORDERS RESEARCH LTD PARTNERSHIP AND ANOTHER V

REVENUE AND CUSTOMS (INCOME TAX – TAX AVOIDANCE SCHEME): UTTC 8 MAY 2017), Available

at: http://www.fedcourt.gov.au/digital-law-library/judges-speeches/speeches-former-judges/justice-pagone/201706

[Accessed on: 22nd September 2018]

TAXATION LAW 9

Question 4: Explain how the loss incurred by Joseph is allocated for the purpose of the tax.

Evaluate its capital gain or loss

Issue

Joseph is an accountant who initiated for acquiring rental house as a joint tenant with his wife

Jane. Joseph is entitled to a profit of 20 % whereas Jane would be profited by 80 % from the

rental house property. The issues arise that any loss incurred by the rental house property would

be carried by Joseph of 100 % or not. Joseph decided to sell off the property for capital gain or

loss.

Rule

The joint tenant who has borrowed the rental house property is partners for business or spouse is

to be recognised for understanding the applicable law. As per the Australian Taxation law, the

division of property income among the joint tenant (excluding the business carrier joint tenants)

is, liable for payment of 20 % and 80 % interest11. If a case arises that division of interest in the

agreement is divided in proportion apart from the equal division would have no effect on the

purpose of the tax. The issues arise that the loss of 100 % would be carried by Joseph, which is

not applicable according to the Australian Taxation Law. The decision of selling off the property

by Joseph for eliminating capital loss of 100 % is required to offset the capital gain at the initial

stage.

Analysis

In case scenario of Joseph, the rental house is borrowed in joint tenancy by Joseph and his wife,

which share the profit by a percent of 20% and 80% as per Australian Taxation Rules. However,

the loss of $ 40000 was fully incurred by Joseph, which is not relevant to the case. As per Capital

gain tax acquisition of property after 19th September 1985 and selling would incur a capital gain

or loss on the property. The gain of the property is calculated by deducting the cost of capital and

additional capital expenses with sales cost. However, the capital loss is incurred by the joint

tenants in the case is required to be allocated equally as per the Australian Taxation law

Conclusion

11 rjsanderson.com.au (2018) Joint tenant borrowing of house, Available at: http://www.rjsanderson.com.au/wp-

content/uploads/2016/08/Rental-Property-Guide-2017.pdf [Accessed on: 22nd September 2018]

Question 4: Explain how the loss incurred by Joseph is allocated for the purpose of the tax.

Evaluate its capital gain or loss

Issue

Joseph is an accountant who initiated for acquiring rental house as a joint tenant with his wife

Jane. Joseph is entitled to a profit of 20 % whereas Jane would be profited by 80 % from the

rental house property. The issues arise that any loss incurred by the rental house property would

be carried by Joseph of 100 % or not. Joseph decided to sell off the property for capital gain or

loss.

Rule

The joint tenant who has borrowed the rental house property is partners for business or spouse is

to be recognised for understanding the applicable law. As per the Australian Taxation law, the

division of property income among the joint tenant (excluding the business carrier joint tenants)

is, liable for payment of 20 % and 80 % interest11. If a case arises that division of interest in the

agreement is divided in proportion apart from the equal division would have no effect on the

purpose of the tax. The issues arise that the loss of 100 % would be carried by Joseph, which is

not applicable according to the Australian Taxation Law. The decision of selling off the property

by Joseph for eliminating capital loss of 100 % is required to offset the capital gain at the initial

stage.

Analysis

In case scenario of Joseph, the rental house is borrowed in joint tenancy by Joseph and his wife,

which share the profit by a percent of 20% and 80% as per Australian Taxation Rules. However,

the loss of $ 40000 was fully incurred by Joseph, which is not relevant to the case. As per Capital

gain tax acquisition of property after 19th September 1985 and selling would incur a capital gain

or loss on the property. The gain of the property is calculated by deducting the cost of capital and

additional capital expenses with sales cost. However, the capital loss is incurred by the joint

tenants in the case is required to be allocated equally as per the Australian Taxation law

Conclusion

11 rjsanderson.com.au (2018) Joint tenant borrowing of house, Available at: http://www.rjsanderson.com.au/wp-

content/uploads/2016/08/Rental-Property-Guide-2017.pdf [Accessed on: 22nd September 2018]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW 10

The case scenario concluded that if the profits are allocated as per the Australian Taxation law in

the proportion of 80 % to Jane and 20 % to Joseph. Then the loss incurred by the Property should

be allocated proportionally. The capital loss of $ 40000 incurred by selling of the rental property

should be accounted for after the offset of Initial capital gain.

Conclusion and overall synopsis

The different case scenario describes the different types of taxation laws applicable in the district

situation. As per the case study, the annual payment by lottery commission to the descendant

after the death of winner. The descendant is liable for payment of remaining tax after receiving

the winning lottery. The second case scenario determines that Corner Pharmacy is liable for

payment of a tax of $ 166500 under the Pharmaceutical Benefits Scheme and provides

concession to the patient at a specific percentage. The Corner Pharmacy is required to keep a

record of every transaction and provide a prescription to the patient for both cash sales and credit

card sales. The second case scenario concluded that IRC lost the accused case imposed on the

Duke of Westminster. The principle applied by Duke for tax evasion was proved to be relevant.

In the last case studies, it is concluded that the loss incurred by property should be treated

equally if the profit on the property is allocated in a proportion.

The case scenario concluded that if the profits are allocated as per the Australian Taxation law in

the proportion of 80 % to Jane and 20 % to Joseph. Then the loss incurred by the Property should

be allocated proportionally. The capital loss of $ 40000 incurred by selling of the rental property

should be accounted for after the offset of Initial capital gain.

Conclusion and overall synopsis

The different case scenario describes the different types of taxation laws applicable in the district

situation. As per the case study, the annual payment by lottery commission to the descendant

after the death of winner. The descendant is liable for payment of remaining tax after receiving

the winning lottery. The second case scenario determines that Corner Pharmacy is liable for

payment of a tax of $ 166500 under the Pharmaceutical Benefits Scheme and provides

concession to the patient at a specific percentage. The Corner Pharmacy is required to keep a

record of every transaction and provide a prescription to the patient for both cash sales and credit

card sales. The second case scenario concluded that IRC lost the accused case imposed on the

Duke of Westminster. The principle applied by Duke for tax evasion was proved to be relevant.

In the last case studies, it is concluded that the loss incurred by property should be treated

equally if the profit on the property is allocated in a proportion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW 11

References

aph.gov.au (2018), Parliamentary Department of PBS. Available at:

https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/

pubs/rp/rp1516/Quick_Guides/PBS [Accessed on: 22nd September 2018]

Behagg, C., 2016. Tax Inversions: Time to Take a Look in the Mirror Reflections on the

Inversion Phenomenon. Intertax, 44(2), pp.130-145.

Burns, S.K. and Ziliak, J.P., 2017. Identifying the elasticity of taxable income. The Economic

Journal, 127(600), pp.297-329.

Christians, A., 2014. Avoidance, evasion, and taxpayer morality. Wash. UJL & Pol'y, 44, p.39.

classic.austlii.edu.au (2018), Legislation of commission on lottery. Available at: Retrieved on

22nd September 2018 from http://classic.austlii.edu.au/au/legis/wa/consol_reg/lcflr2014408/

s24.html [Accessed on: 22nd September 2018]

Doerrenberg, P., Peichl, A. and Siegloch, S., 2017. The elasticity of taxable income in the

presence of deduction possibilities. Journal of Public Economics, 151, pp.41-55.

fedcourt.gov.au (2018), THE BRAIN DISORDERS RESEARCH LTD PARTNERSHIP AND

ANOTHER V REVENUE AND CUSTOMS (INCOME TAX – TAX AVOIDANCE

SCHEME): UTTC 8 MAY 2017), Available at: http://www.fedcourt.gov.au/digital-law-

library/judges-speeches/speeches-former-judges/justice-pagone/201706 [Accessed on: 22nd

September 2018]

Harris, C.A., Daniels, B., Ward, R.L. and Pearson, S.A., 2017. Retrospective comparison of

Australia's Pharmaceutical Benefits Scheme claims data with prescription data in HER2-positive

early breast cancer patients, 2008-2012. Public Health Research and Practice, 27(5), pp.1-9.

Kleven, H.J. and Schultz, E.A., 2014. Estimating taxable income responses using Danish tax

reforms. American Economic Journal: Economic Policy, 6(4), pp.271-301.

References

aph.gov.au (2018), Parliamentary Department of PBS. Available at:

https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/

pubs/rp/rp1516/Quick_Guides/PBS [Accessed on: 22nd September 2018]

Behagg, C., 2016. Tax Inversions: Time to Take a Look in the Mirror Reflections on the

Inversion Phenomenon. Intertax, 44(2), pp.130-145.

Burns, S.K. and Ziliak, J.P., 2017. Identifying the elasticity of taxable income. The Economic

Journal, 127(600), pp.297-329.

Christians, A., 2014. Avoidance, evasion, and taxpayer morality. Wash. UJL & Pol'y, 44, p.39.

classic.austlii.edu.au (2018), Legislation of commission on lottery. Available at: Retrieved on

22nd September 2018 from http://classic.austlii.edu.au/au/legis/wa/consol_reg/lcflr2014408/

s24.html [Accessed on: 22nd September 2018]

Doerrenberg, P., Peichl, A. and Siegloch, S., 2017. The elasticity of taxable income in the

presence of deduction possibilities. Journal of Public Economics, 151, pp.41-55.

fedcourt.gov.au (2018), THE BRAIN DISORDERS RESEARCH LTD PARTNERSHIP AND

ANOTHER V REVENUE AND CUSTOMS (INCOME TAX – TAX AVOIDANCE

SCHEME): UTTC 8 MAY 2017), Available at: http://www.fedcourt.gov.au/digital-law-

library/judges-speeches/speeches-former-judges/justice-pagone/201706 [Accessed on: 22nd

September 2018]

Harris, C.A., Daniels, B., Ward, R.L. and Pearson, S.A., 2017. Retrospective comparison of

Australia's Pharmaceutical Benefits Scheme claims data with prescription data in HER2-positive

early breast cancer patients, 2008-2012. Public Health Research and Practice, 27(5), pp.1-9.

Kleven, H.J. and Schultz, E.A., 2014. Estimating taxable income responses using Danish tax

reforms. American Economic Journal: Economic Policy, 6(4), pp.271-301.

TAXATION LAW 12

Koessler, A.K., Torgler, B., Feld, L.P. and Frey, B.S., 2016. Commitment to pay taxes: a field

experiment on the importance of promise.

Okamura, J.Y., 2014. Filipino Hometown Associations in Hawaii 1. In Asian American Family

Life and Community (pp. 89-101). Abingdon: Routledge.

oxfordindex.oup.com (2018), IRC v Duke of Westminster [1936] AC 1, Available at:

http://oxfordindex.oup.com/view/10.1093/oi/authority.20110803121911242 [Accessed on: 22nd

September 2018]

rjsanderson.com.au (2018) Joint tenant borrowing of house Retrieved on 22nd September 2018

from http://www.rjsanderson.com.au/wp-content/uploads/2016/08/Rental-Property-Guide-

2017.pdf

theguardian.com (2018), Do you pay tax on lottery win. Available at:

https://www.theguardian.com/money/2012/sep/10/do-you-pay-tax-lottery-win [Accessed on:

22nd September 2018]

Koessler, A.K., Torgler, B., Feld, L.P. and Frey, B.S., 2016. Commitment to pay taxes: a field

experiment on the importance of promise.

Okamura, J.Y., 2014. Filipino Hometown Associations in Hawaii 1. In Asian American Family

Life and Community (pp. 89-101). Abingdon: Routledge.

oxfordindex.oup.com (2018), IRC v Duke of Westminster [1936] AC 1, Available at:

http://oxfordindex.oup.com/view/10.1093/oi/authority.20110803121911242 [Accessed on: 22nd

September 2018]

rjsanderson.com.au (2018) Joint tenant borrowing of house Retrieved on 22nd September 2018

from http://www.rjsanderson.com.au/wp-content/uploads/2016/08/Rental-Property-Guide-

2017.pdf

theguardian.com (2018), Do you pay tax on lottery win. Available at:

https://www.theguardian.com/money/2012/sep/10/do-you-pay-tax-lottery-win [Accessed on:

22nd September 2018]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.