Taxation Law Assignment: HA3042 - T2 2019 Individual Assessment

VerifiedAdded on 2022/11/13

|12

|2713

|80

Homework Assignment

AI Summary

This taxation law assignment explores various aspects of Australian taxation. It begins by analyzing the tax implications of Jasmine's financial decisions, including the sale of her home (pre-CGT asset), car (personal use asset), small cleaning business, furniture, and paintings (collectables). The assignment then delves into the specifics of capital gains tax (CGT), small business concessions, and the treatment of personal use assets and collectables. The second part of the assignment focuses on depreciation, specifically examining John's claim for depreciation on a CNC machine used in his motor vehicle parts manufacturing company. The analysis considers relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997), including those related to depreciating assets, cost base determination, and taxable purpose. The assignment applies these legal principles to John's situation, determining the start time for depreciation and the calculation of the CNC machine's cost base for capital allowance purposes. Overall, the assignment demonstrates an understanding of tax law principles and their practical application in various scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

A: Sale of Home:

As a general note, the capital gains or loss happening to pre-CGT assets such as the

assets procured before 20/9/1985 is tax exempt from CGT. Other assets which is not

subjected to CGT is the main dwelling. Under “sec 118-110 (1)”, exemptions on main

residence is applied only when the dwelling qualifies as the main home where the taxpayer

lives (Mangioni 2015). The application of exemption on main dwelling is completely

dependent on the fact. There are some factors that is given by the tax commissioner this

includes;

a. The length of time lived in the dwelling by taxpayers

b. Place of residence of taxpayers family

As noted it is necessary that some degree of physical occupancy is needed to establish

the main exemption.

The situation here says that Jasmine an Australian resident is now deciding to move to

UK. She sells the home for $650,000 which was purchased 1981. During purchase she paid

$40,000 to acquire the house. The house of Jasmine qualifies as main residence exemption

under “sec 118-110 (1)” because she was using it for her dwelling purpose and under no

circumstances used for generating income (Becker, Reimer and Rust 2015). The capital gains

earned by Jasmine will be further exempted because her house is a pre-CGT asset because

she bought before 20/9/1985.

B: Sale of Car:

Capital gains or loss happens when the CGT event takes place. A CGT event A1

under “s 104-10 (1)” when capital gains or capital loss takes place.

Answer to question 1:

A: Sale of Home:

As a general note, the capital gains or loss happening to pre-CGT assets such as the

assets procured before 20/9/1985 is tax exempt from CGT. Other assets which is not

subjected to CGT is the main dwelling. Under “sec 118-110 (1)”, exemptions on main

residence is applied only when the dwelling qualifies as the main home where the taxpayer

lives (Mangioni 2015). The application of exemption on main dwelling is completely

dependent on the fact. There are some factors that is given by the tax commissioner this

includes;

a. The length of time lived in the dwelling by taxpayers

b. Place of residence of taxpayers family

As noted it is necessary that some degree of physical occupancy is needed to establish

the main exemption.

The situation here says that Jasmine an Australian resident is now deciding to move to

UK. She sells the home for $650,000 which was purchased 1981. During purchase she paid

$40,000 to acquire the house. The house of Jasmine qualifies as main residence exemption

under “sec 118-110 (1)” because she was using it for her dwelling purpose and under no

circumstances used for generating income (Becker, Reimer and Rust 2015). The capital gains

earned by Jasmine will be further exempted because her house is a pre-CGT asset because

she bought before 20/9/1985.

B: Sale of Car:

Capital gains or loss happens when the CGT event takes place. A CGT event A1

under “s 104-10 (1)” when capital gains or capital loss takes place.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Most notably in “subdivision 108-C” non-collectable assets or in other words

personal use asset refers to assets kept or used by taxpayer for private enjoyment purpose

(Braithwaite 2017). The example under “sec 108-20” includes the furniture, motor vehicle,

boat and household things. The most important aspect of the personal use asset is that under

“sec 118-10 (3)”, any kind of capital gains is ignored when assets has a base cost of $10k or

low. This implies that details must be kept by the taxpayer when they are purchasing assets

for a value greater than $10k. While “sec 108-20 (1)”, explains that capital loss from

disposing private use asset is not counted for tax purpose.

In 2011 a car was purchased by Jasmine that cost her $31,000. While in current tax

year she sells the car that had the worth of $10,000. Therefore, selling of car has transpired a

CGT event A1 under “sec 104-10 (1), ITA Act 1997”. The car is characterized as the personal

use asset under sec 108-20. The capital loss from disposing the car by Jasmine under sec 108-

20 (1) is ought to be ignored.

C: Capital gain on sale of business:

As noted in “Div 152” basic concessions is given to help the small business. The basic

conditions includes the following;

a. The company should be categorized as small business with gross business revenue not

more than $2 million (Sterner 2017).

b. CGT asset should be actively used in business.

Four types of small business concessions is available;

1. 15-year capital gains from CGT asset

2. 50% reduction in capital gains after imposing general 50% discount

3. Retirement concessions of up to $500,000 on capital gains proceeds

4. Roll-over relief for using the capital gain to purchase replacement assets

Most notably in “subdivision 108-C” non-collectable assets or in other words

personal use asset refers to assets kept or used by taxpayer for private enjoyment purpose

(Braithwaite 2017). The example under “sec 108-20” includes the furniture, motor vehicle,

boat and household things. The most important aspect of the personal use asset is that under

“sec 118-10 (3)”, any kind of capital gains is ignored when assets has a base cost of $10k or

low. This implies that details must be kept by the taxpayer when they are purchasing assets

for a value greater than $10k. While “sec 108-20 (1)”, explains that capital loss from

disposing private use asset is not counted for tax purpose.

In 2011 a car was purchased by Jasmine that cost her $31,000. While in current tax

year she sells the car that had the worth of $10,000. Therefore, selling of car has transpired a

CGT event A1 under “sec 104-10 (1), ITA Act 1997”. The car is characterized as the personal

use asset under sec 108-20. The capital loss from disposing the car by Jasmine under sec 108-

20 (1) is ought to be ignored.

C: Capital gain on sale of business:

As noted in “Div 152” basic concessions is given to help the small business. The basic

conditions includes the following;

a. The company should be categorized as small business with gross business revenue not

more than $2 million (Sterner 2017).

b. CGT asset should be actively used in business.

Four types of small business concessions is available;

1. 15-year capital gains from CGT asset

2. 50% reduction in capital gains after imposing general 50% discount

3. Retirement concessions of up to $500,000 on capital gains proceeds

4. Roll-over relief for using the capital gain to purchase replacement assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

While for goodwill a “CGT event C1” is applied when upon the closure of business is

made by taxpayer for permanent basis. Business must be completely closed to trigger this

event.

Jasmine is moving permanently to UK and sells her small cleaning business. Her business

assets fetched her $65000 while her business goodwill fetched her $60,000. Jasmine qualifies

for the small business concessions. Her annual turnover of business is presumed to be not

more than $2 million. Her CGT assets are active assets. Therefore, Jasmine can get 15-year

exemption since she held the asset for greater than 15 years and Jasmine is more than 55

years old. While the goodwill disposal has led to “CGT event C1” (Spiro 2018). As her

business was permanently ceased and she is retiring from her business as well, Jasmine can

avail the retirement concessions and can disregard the capital related with her goodwill.

D: Sale of Furniture:

There are some very important special rules that are applicable on the taxpayers when

they decide the sell the private use asset held by them. The special rule is that under “sec

118-10 (3)”, when a taxpayer sells the private use asset which they have purchased it for

$10k or less then this provision requires the taxpayer to simply ignore those capital gains

(Frecknall-Hughes and Kirchler 2015).

As Jasmine is selling all her Australian assets she decides to sell her furniture as well

which she bought for $2.000. The sales fetched Jasmine with $5,000 in the present year. The

furniture is a private use asset under “sec 108-20”. The sale has transpired into CGT event

A1 under “sec 104-10 (1), ITA Act 1997”. The furniture also fails to meet the first element

cost base given under “sec 118-10 (3)” as it cost below $10,000. Therefore, capital gains

from painting is simply ignored for Jasmine.

While for goodwill a “CGT event C1” is applied when upon the closure of business is

made by taxpayer for permanent basis. Business must be completely closed to trigger this

event.

Jasmine is moving permanently to UK and sells her small cleaning business. Her business

assets fetched her $65000 while her business goodwill fetched her $60,000. Jasmine qualifies

for the small business concessions. Her annual turnover of business is presumed to be not

more than $2 million. Her CGT assets are active assets. Therefore, Jasmine can get 15-year

exemption since she held the asset for greater than 15 years and Jasmine is more than 55

years old. While the goodwill disposal has led to “CGT event C1” (Spiro 2018). As her

business was permanently ceased and she is retiring from her business as well, Jasmine can

avail the retirement concessions and can disregard the capital related with her goodwill.

D: Sale of Furniture:

There are some very important special rules that are applicable on the taxpayers when

they decide the sell the private use asset held by them. The special rule is that under “sec

118-10 (3)”, when a taxpayer sells the private use asset which they have purchased it for

$10k or less then this provision requires the taxpayer to simply ignore those capital gains

(Frecknall-Hughes and Kirchler 2015).

As Jasmine is selling all her Australian assets she decides to sell her furniture as well

which she bought for $2.000. The sales fetched Jasmine with $5,000 in the present year. The

furniture is a private use asset under “sec 108-20”. The sale has transpired into CGT event

A1 under “sec 104-10 (1), ITA Act 1997”. The furniture also fails to meet the first element

cost base given under “sec 118-10 (3)” as it cost below $10,000. Therefore, capital gains

from painting is simply ignored for Jasmine.

5TAXATION LAW

E: Sale of paintings:

“Sec 108-10, ITA Act 1997” says collectables means asset that the taxpayer uses for their

private amusement (McCluskey and Franzsen 2017). The list under “sec 108-10 (2)”,

includes;

a. Antiques and Jewels

b. Art works such as paintings

c. Rare stamps

“Sec 118-10 (1)” says that capital gains are disregarded when collectable is acquired for

below $500.

Jasmine here sells all of her paintings for $35,000 that she had bought from a second

hand shop for $500. The painting held by Jasmine is categorized under “sec 108-10 (2)” as

collectables. The capital gains made from selling paintings should be ignored by Jasmine

under “sec 118-10 (1)” because the painting has failed to meet the first element cost base as

not a single painting has cost of $500 or more.

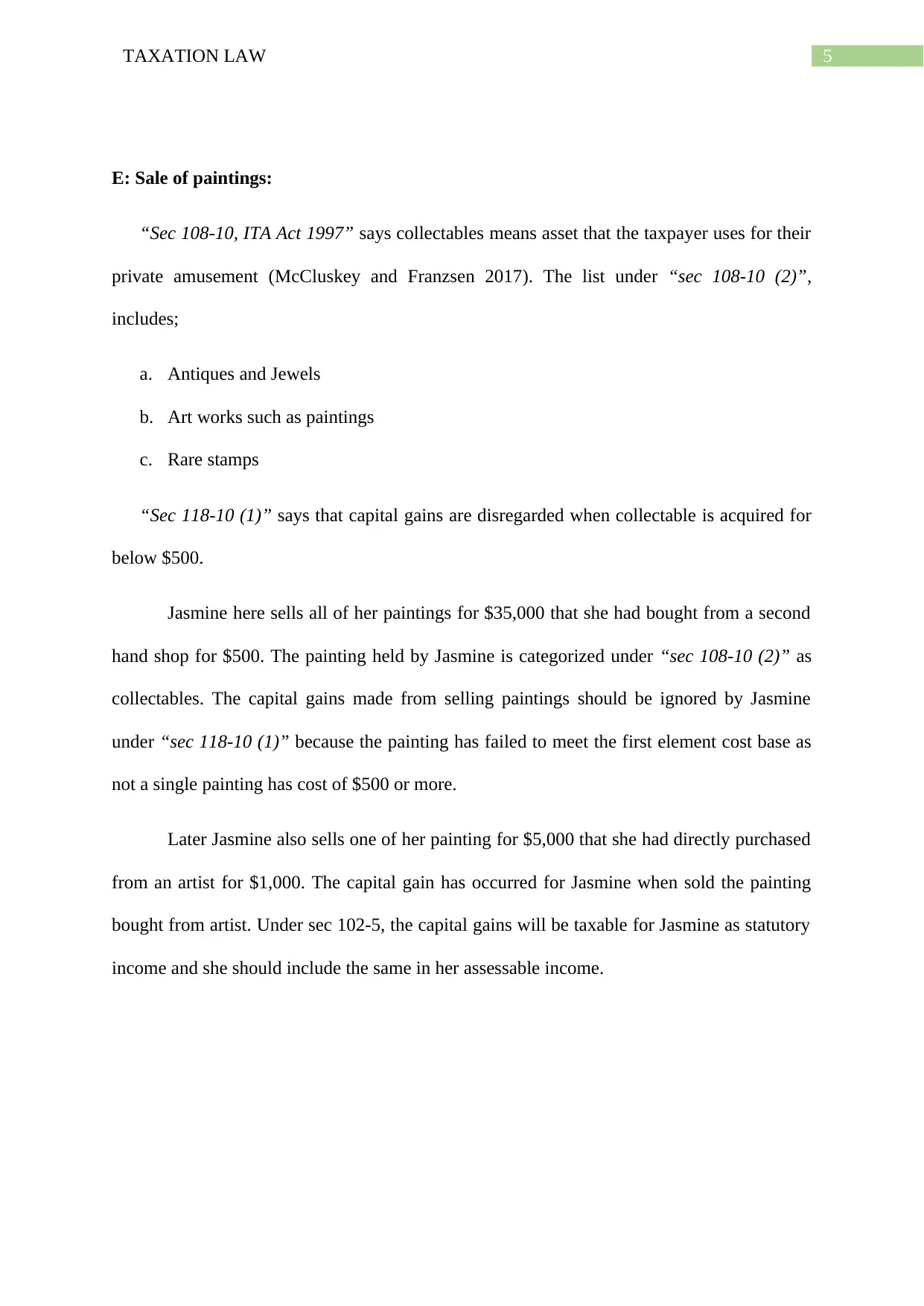

Later Jasmine also sells one of her painting for $5,000 that she had directly purchased

from an artist for $1,000. The capital gain has occurred for Jasmine when sold the painting

bought from artist. Under sec 102-5, the capital gains will be taxable for Jasmine as statutory

income and she should include the same in her assessable income.

E: Sale of paintings:

“Sec 108-10, ITA Act 1997” says collectables means asset that the taxpayer uses for their

private amusement (McCluskey and Franzsen 2017). The list under “sec 108-10 (2)”,

includes;

a. Antiques and Jewels

b. Art works such as paintings

c. Rare stamps

“Sec 118-10 (1)” says that capital gains are disregarded when collectable is acquired for

below $500.

Jasmine here sells all of her paintings for $35,000 that she had bought from a second

hand shop for $500. The painting held by Jasmine is categorized under “sec 108-10 (2)” as

collectables. The capital gains made from selling paintings should be ignored by Jasmine

under “sec 118-10 (1)” because the painting has failed to meet the first element cost base as

not a single painting has cost of $500 or more.

Later Jasmine also sells one of her painting for $5,000 that she had directly purchased

from an artist for $1,000. The capital gain has occurred for Jasmine when sold the painting

bought from artist. Under sec 102-5, the capital gains will be taxable for Jasmine as statutory

income and she should include the same in her assessable income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issues:

The case involves the claims of depreciation that is occurred by the taxpayer

regarding the depreciating asset equivalent to the fall in value under “s40.25, ITA Act 1997”.

Laws:

Under the income tax, a taxpayer is given the permission of obtaining the deduction

for the outgoings that is occurred at the time of making business income or incurred in

carrying the business. Generally, the value of assets which gives the benefit to business for

large number of years and simultaneously falls over its effective life is allowed as deduction.

The capital allowances cost such as depreciation under “s 40.25, ITA Act 1997” is allowed

for deduction to taxpayer equal to assets fall in value (Schenk, Thuronyi and Ciu 2016). The

taxpayers must denote that the deduction is permitted based on the projected useful life of

asset.

As noted in “s 40.30 (1), ITA Act 1997” assets that are depreciating in nature and it is

anticipated to fall in terms of value based on its use is known as depreciating assets

(McCluskey 2018). The taxpayer must denote that to claim the deduction under “sec 40-25,

ITA Act 1997” it is necessary to ascertain when the assets is held and when the decline in

value of assets commences for the taxable purpose. Generally the asset holder is permitted

deduction for the depreciating asset fall in value under “s 40.25” (Barkoczy 2016). The

Answer to question 2:

Issues:

The case involves the claims of depreciation that is occurred by the taxpayer

regarding the depreciating asset equivalent to the fall in value under “s40.25, ITA Act 1997”.

Laws:

Under the income tax, a taxpayer is given the permission of obtaining the deduction

for the outgoings that is occurred at the time of making business income or incurred in

carrying the business. Generally, the value of assets which gives the benefit to business for

large number of years and simultaneously falls over its effective life is allowed as deduction.

The capital allowances cost such as depreciation under “s 40.25, ITA Act 1997” is allowed

for deduction to taxpayer equal to assets fall in value (Schenk, Thuronyi and Ciu 2016). The

taxpayers must denote that the deduction is permitted based on the projected useful life of

asset.

As noted in “s 40.30 (1), ITA Act 1997” assets that are depreciating in nature and it is

anticipated to fall in terms of value based on its use is known as depreciating assets

(McCluskey 2018). The taxpayer must denote that to claim the deduction under “sec 40-25,

ITA Act 1997” it is necessary to ascertain when the assets is held and when the decline in

value of assets commences for the taxable purpose. Generally the asset holder is permitted

deduction for the depreciating asset fall in value under “s 40.25” (Barkoczy 2016). The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

taxpayer should note down that a decline in value of depreciating asset is only allowed up to

the extent of taxable purpose under “s 40.25 (2)”. In other words under “sec 40.25 (7)”, the

taxable purpose usually implies that the asset is used in generation of chargeable business

revenues.

The holder of the depreciating assets is permitted to claim the depreciation from the

phase when the start time happens under “s 40.60 (1), ITAA 1997” (Braithwaite 2017). The

holder of the asset is permitted to obtain the deduction for assets decline in value when they

make the first use for earning taxable income or for carrying on the business.

The holder of depreciating asset should understand that depreciation is completely

based on assets cost and “Subdiv 40-C” assists the taxpayer with certain rules regarding the

determination of assets cost. Usually the assets takes into account the acquisition price which

is paid for getting the asset but on certain occasions other incidental costs of delivery and

installation are also included into the cost base (Thuronyi and Brooks 2016). In “Broken Hill

Pty Co Ltd v. FCT (1969)” certain small expenses such as expenditure for rearranging and

removing the asset is also included in cost base.

The legislature of “s 40-175, ITA Act 1997” says that depreciating asset cost is

classified in two elements. “Sec 40.180” says that first element of cost base must be worked

out to know the assets cost base. “Subsec 40.180 (1)” says that the cost base of first element

should be determined when the taxpayer beings holding the asset (Sadiq 2019). The first

element comprises of the purchase price which the taxpayer pays for the acquisition of the

asset. While “sec 40.190, ITA Act 1997” explains the second element cost base of

depreciating asset. Under this the assets deliver cost, installation and capital improvement

that is made to asset is included in the cost base.

Application:

taxpayer should note down that a decline in value of depreciating asset is only allowed up to

the extent of taxable purpose under “s 40.25 (2)”. In other words under “sec 40.25 (7)”, the

taxable purpose usually implies that the asset is used in generation of chargeable business

revenues.

The holder of the depreciating assets is permitted to claim the depreciation from the

phase when the start time happens under “s 40.60 (1), ITAA 1997” (Braithwaite 2017). The

holder of the asset is permitted to obtain the deduction for assets decline in value when they

make the first use for earning taxable income or for carrying on the business.

The holder of depreciating asset should understand that depreciation is completely

based on assets cost and “Subdiv 40-C” assists the taxpayer with certain rules regarding the

determination of assets cost. Usually the assets takes into account the acquisition price which

is paid for getting the asset but on certain occasions other incidental costs of delivery and

installation are also included into the cost base (Thuronyi and Brooks 2016). In “Broken Hill

Pty Co Ltd v. FCT (1969)” certain small expenses such as expenditure for rearranging and

removing the asset is also included in cost base.

The legislature of “s 40-175, ITA Act 1997” says that depreciating asset cost is

classified in two elements. “Sec 40.180” says that first element of cost base must be worked

out to know the assets cost base. “Subsec 40.180 (1)” says that the cost base of first element

should be determined when the taxpayer beings holding the asset (Sadiq 2019). The first

element comprises of the purchase price which the taxpayer pays for the acquisition of the

asset. While “sec 40.190, ITA Act 1997” explains the second element cost base of

depreciating asset. Under this the assets deliver cost, installation and capital improvement

that is made to asset is included in the cost base.

Application:

8TAXATION LAW

Evidences from the case reading shows that John is the owner of motor vehicle parts

manufacturing company. He engages himself in the production of BMW parts. John when to

Germany to inspect about the CNC machine. After the successful inspection he decided to

purchase it for $300,000 on 1st November 2014. He installed the machine in his factory on 15

January. The CNC machine purchased by John satisifies the meaning of depreciating asset

under “s 40.30 (1), ITA Act 1997” (Butler 2019). This is because the CNC has the some

degree of effective life and the machine is projected to fall in terms of value in regard to its

usage.

John here is permitted under “s 40-25, ITA Act 1997” to claim the deduction for

depreciation or the “decline in value” of CNC machine which he has held during the year.

The asset has been duly held by John under “sec 40.25 (2), ITA Act 1997” for the purpose of

taxable purpose. This is because under “s 40.25 (7)”, John has held CNC machine for

generating chargeable business proceeds during the ordinary business course (Murray et al.

2018). Therefore, the machine was installed on 15th January as ready for use and John began

using the asset from that time onwards. Hence under “sec 40.60 (1)” the start time for

computing the decline in value of CNC machine is 15 January onwards.

To compute the CNC machine cost for capital allowance purpose rules of “Sub-Div

40-C” must be considered. Referring to “Broken Hill Pty Co Ltd v. FCT (1969)” certain

small expenses such as expenditure for rearranging the CNC machine is also included in cost

base in case of John. Under “Sec 40.180”, the first element of CNC machine cost base, the

purchase price paid by John to acquire it has been included (Liu 2018). While under the

second element cost base installation cost and the additional cost of adding a guiding rod to

make the CNC machine is also included with respect to the legislative provision of “sec

40.190, ITA Act 1997”.

Evidences from the case reading shows that John is the owner of motor vehicle parts

manufacturing company. He engages himself in the production of BMW parts. John when to

Germany to inspect about the CNC machine. After the successful inspection he decided to

purchase it for $300,000 on 1st November 2014. He installed the machine in his factory on 15

January. The CNC machine purchased by John satisifies the meaning of depreciating asset

under “s 40.30 (1), ITA Act 1997” (Butler 2019). This is because the CNC has the some

degree of effective life and the machine is projected to fall in terms of value in regard to its

usage.

John here is permitted under “s 40-25, ITA Act 1997” to claim the deduction for

depreciation or the “decline in value” of CNC machine which he has held during the year.

The asset has been duly held by John under “sec 40.25 (2), ITA Act 1997” for the purpose of

taxable purpose. This is because under “s 40.25 (7)”, John has held CNC machine for

generating chargeable business proceeds during the ordinary business course (Murray et al.

2018). Therefore, the machine was installed on 15th January as ready for use and John began

using the asset from that time onwards. Hence under “sec 40.60 (1)” the start time for

computing the decline in value of CNC machine is 15 January onwards.

To compute the CNC machine cost for capital allowance purpose rules of “Sub-Div

40-C” must be considered. Referring to “Broken Hill Pty Co Ltd v. FCT (1969)” certain

small expenses such as expenditure for rearranging the CNC machine is also included in cost

base in case of John. Under “Sec 40.180”, the first element of CNC machine cost base, the

purchase price paid by John to acquire it has been included (Liu 2018). While under the

second element cost base installation cost and the additional cost of adding a guiding rod to

make the CNC machine is also included with respect to the legislative provision of “sec

40.190, ITA Act 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

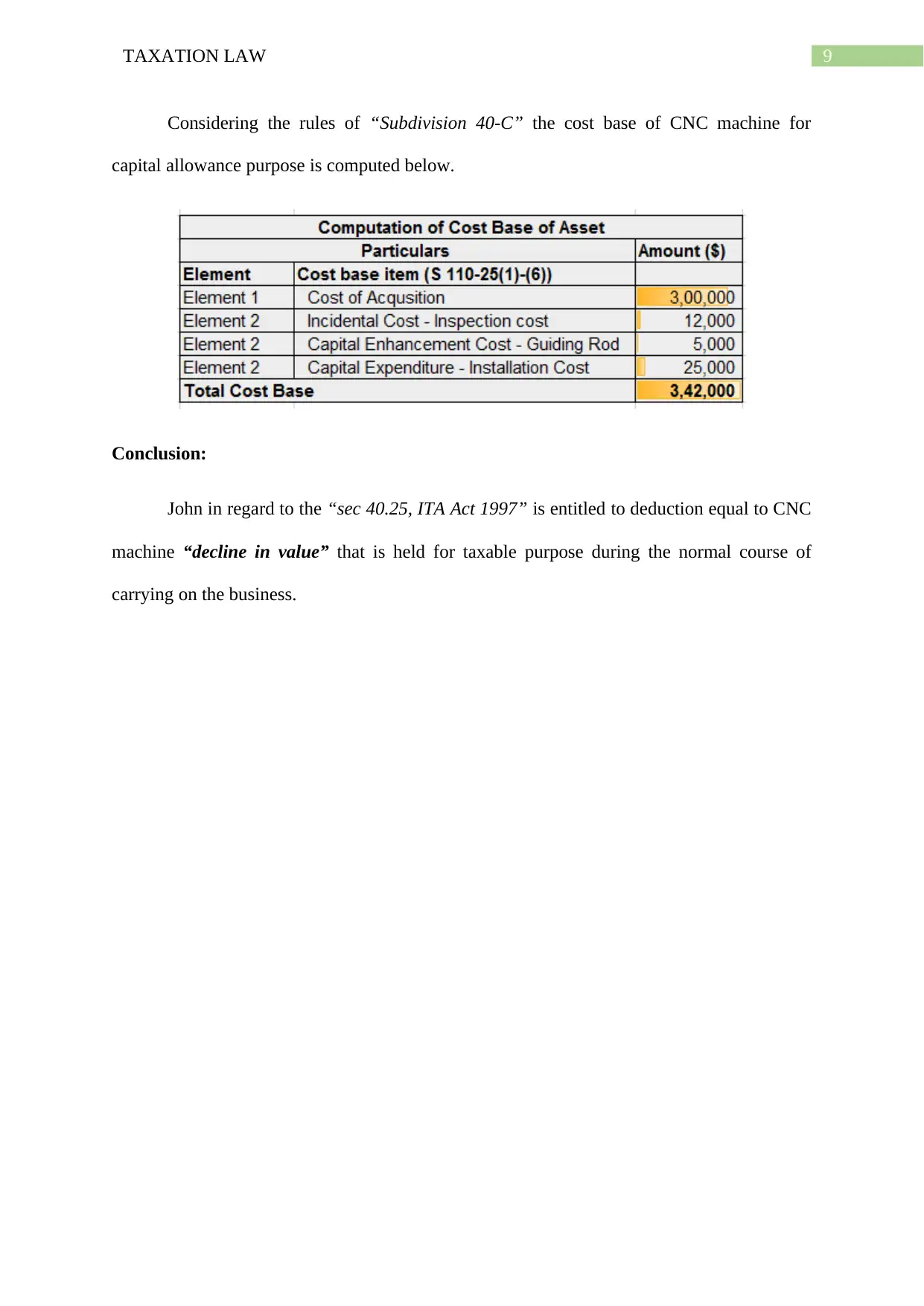

Considering the rules of “Subdivision 40-C” the cost base of CNC machine for

capital allowance purpose is computed below.

Conclusion:

John in regard to the “sec 40.25, ITA Act 1997” is entitled to deduction equal to CNC

machine “decline in value” that is held for taxable purpose during the normal course of

carrying on the business.

Considering the rules of “Subdivision 40-C” the cost base of CNC machine for

capital allowance purpose is computed below.

Conclusion:

John in regard to the “sec 40.25, ITA Act 1997” is entitled to deduction equal to CNC

machine “decline in value” that is held for taxable purpose during the normal course of

carrying on the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

Liu, J., 2018. Understanding Australian commercial law. Taxation in Australia, 53(6), p.300.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Murray, I., Taylor, J., Walpole, M., Burton, M. and Ciro, T., 2018. Understanding Taxation

Law 2019.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Schenk, A., THURONYI, V. and CUI, W., 2016. Value added tax: a comparative approach.

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

Liu, J., 2018. Understanding Australian commercial law. Taxation in Australia, 53(6), p.300.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Murray, I., Taylor, J., Walpole, M., Burton, M. and Ciro, T., 2018. Understanding Taxation

Law 2019.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Schenk, A., THURONYI, V. and CUI, W., 2016. Value added tax: a comparative approach.

11TAXATION LAW

Spiro, P.S., 2018. Tax policy and the underground economy. In Size, causes and

consequences of the underground economy (pp. 179-201). Routledge.

Sterner, T., 2017. Environmental taxation in practice. Routledge.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Spiro, P.S., 2018. Tax policy and the underground economy. In Size, causes and

consequences of the underground economy (pp. 179-201). Routledge.

Sterner, T., 2017. Environmental taxation in practice. Routledge.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.