HI3042 Taxation Law T2 2017 Individual Assignment Analysis

VerifiedAdded on 2020/04/07

|11

|2646

|38

Homework Assignment

AI Summary

This assignment solution addresses several key areas of taxation law. Question 1 analyzes the deductibility of various business expenses, differentiating between capital and revenue expenditures, and applying relevant sections of the ITAA 1997. Question 2 focuses on GST credits, examining the eligibility of a bank for input tax credits on advertising campaigns. Question 3 delves into foreign tax offsets, outlining the calculation of Angelo's foreign tax offset based on different income sources and allowable deductions. Question 4 examines partnership taxation, determining taxable income, deductible expenses, and the treatment of partner salaries and other transactions within a partnership structure, including GST. The solution provides detailed explanations and references to relevant legal provisions and case studies.

HI3042 Taxation Law

T2 2017 Individual Assignment

T2 2017 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 1

Issue

In accordance with the provisions of sec 8-1 of ITAA 1997 expenses incurred

by business will be allowed for general deductions if conditions cited in it is satisfied.

Thus present case study deals with the analysis of given transaction to determine

whether they are deductible or not.

Description of legal provisions

A general deduction in business is supported by provisions of section 8-1 of

ITAA 97. Section 8-1(1) allows that an individual or business can subtract a loss to a

particular extent, if it can meet the direct requirement cited in provisions of both s 8-

1(1)(a) or s 8-1(1)(b) (Somers and Eynaud, 2015). While, taking a look at expense to

observe if it is deductible next to assessable income or not, one must first determine

whether they are allowable to a general deduction, or there is any exclusion

provisions been applicable to refuse the deduction.

S8-1(1) has two positive aspects from which minimum one must be confirmed

to be applicable before there is deduction in any of the amount, as a specific

deduction (Buchanan and Consett, 2016). Further; S8-1(2) has four negative aspects

which describe the circumstances in which deduction will not be provided if one of

the following aspects is satisfied (any of these) (Dunne, Mason and Patto, 2014).

NB:

While taking a look at a potential amount as a specific deduction, one must

assess the positive limbs and demonstrate one of them, further look after the

negative limbs to ensure none of the cited condition is satisfied (Liu, Huang and

Freudenberg, 2014). First prove that, if the company has any of the loss or outgoing

amount, it must be incurred in, next the expense must be valid and real and it must

relate to the income of taxpayer (Millar, 2016). After that the Assessable income is

not needed to be generated in the particular deductibility period, as it may be

subjected to Apportionment

Exclusion – s 8-1(2) ITAA 1997 as per s 8-1(2), if the positive limbs are

fulfilled according to the terms, a deduction will not be still entitled to the level, if the

loss or outgoing is capital nature or is of a personal or domestic nature or is incurred

Issue

In accordance with the provisions of sec 8-1 of ITAA 1997 expenses incurred

by business will be allowed for general deductions if conditions cited in it is satisfied.

Thus present case study deals with the analysis of given transaction to determine

whether they are deductible or not.

Description of legal provisions

A general deduction in business is supported by provisions of section 8-1 of

ITAA 97. Section 8-1(1) allows that an individual or business can subtract a loss to a

particular extent, if it can meet the direct requirement cited in provisions of both s 8-

1(1)(a) or s 8-1(1)(b) (Somers and Eynaud, 2015). While, taking a look at expense to

observe if it is deductible next to assessable income or not, one must first determine

whether they are allowable to a general deduction, or there is any exclusion

provisions been applicable to refuse the deduction.

S8-1(1) has two positive aspects from which minimum one must be confirmed

to be applicable before there is deduction in any of the amount, as a specific

deduction (Buchanan and Consett, 2016). Further; S8-1(2) has four negative aspects

which describe the circumstances in which deduction will not be provided if one of

the following aspects is satisfied (any of these) (Dunne, Mason and Patto, 2014).

NB:

While taking a look at a potential amount as a specific deduction, one must

assess the positive limbs and demonstrate one of them, further look after the

negative limbs to ensure none of the cited condition is satisfied (Liu, Huang and

Freudenberg, 2014). First prove that, if the company has any of the loss or outgoing

amount, it must be incurred in, next the expense must be valid and real and it must

relate to the income of taxpayer (Millar, 2016). After that the Assessable income is

not needed to be generated in the particular deductibility period, as it may be

subjected to Apportionment

Exclusion – s 8-1(2) ITAA 1997 as per s 8-1(2), if the positive limbs are

fulfilled according to the terms, a deduction will not be still entitled to the level, if the

loss or outgoing is capital nature or is of a personal or domestic nature or is incurred

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regarding earning or generating excused income or it prohibited from being deducted

from provision of the Act.

Application of cited provisions to determine allowance of expense

The cost of moving machinery into a new site; this expense is Non-

Deductible, it is because fixed asset’s shifting cost from place to place said to

be a capital expenditure, by which reduction will be done as per s 8-1 of

ITAA97 (Datt, Nienaber and Tran-Nam, 2017). While, this expense is allowed

to increase the item cost in regards to the transactions for depreciation

The cost of revaluing assets to effect insurance cover; this expense is

deductible, it is because in order to identify the expense deduction regarding

the fixation of assets, it is vital to identify either the subjected amount will

make increment in the earning capacity or are subjected just for the intention

to protect or preserve (Edmonds, Holle and Hartanti, 2015). According to this

case; it can be stated that the benefit are expected to be temporary or can be

habitual in nature therefore it is deductible as per s 8-1.

Legal Expenses experienced by a company facing an appeal for winding

up; these expenses are Non-Deductible, as In this described situation

primary issues related to income generation effectiveness or are related to

operational activities (Dixon and Nassios, 2016). In the existing transaction, it

seems that these transactions will help company in winding up therefore this

will be considered as capital transaction as it is neither revenue in nature and

nor has recurring prospects.

Legal Expenses occurred for the services provided by the lawyer

regarding several matters; this expense is deductible. For the aspect of

determining additional deductibility, requirement of information is necessary

like expense nature, distribution or any other similar aspects. On the other

hand, these expenses appear to be revenue in nature, further it can be said

that it meets the term and conditions given as per s 8-1.

from provision of the Act.

Application of cited provisions to determine allowance of expense

The cost of moving machinery into a new site; this expense is Non-

Deductible, it is because fixed asset’s shifting cost from place to place said to

be a capital expenditure, by which reduction will be done as per s 8-1 of

ITAA97 (Datt, Nienaber and Tran-Nam, 2017). While, this expense is allowed

to increase the item cost in regards to the transactions for depreciation

The cost of revaluing assets to effect insurance cover; this expense is

deductible, it is because in order to identify the expense deduction regarding

the fixation of assets, it is vital to identify either the subjected amount will

make increment in the earning capacity or are subjected just for the intention

to protect or preserve (Edmonds, Holle and Hartanti, 2015). According to this

case; it can be stated that the benefit are expected to be temporary or can be

habitual in nature therefore it is deductible as per s 8-1.

Legal Expenses experienced by a company facing an appeal for winding

up; these expenses are Non-Deductible, as In this described situation

primary issues related to income generation effectiveness or are related to

operational activities (Dixon and Nassios, 2016). In the existing transaction, it

seems that these transactions will help company in winding up therefore this

will be considered as capital transaction as it is neither revenue in nature and

nor has recurring prospects.

Legal Expenses occurred for the services provided by the lawyer

regarding several matters; this expense is deductible. For the aspect of

determining additional deductibility, requirement of information is necessary

like expense nature, distribution or any other similar aspects. On the other

hand, these expenses appear to be revenue in nature, further it can be said

that it meets the term and conditions given as per s 8-1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 2

Issue

According to the cited case situation, Big Bank Ltd has its operations

nationwide, having over 50 branches and are authorized for the purpose of GST.

Bing bank has offered loan and deposits to Australian customers. Big bank has

spent over $1,650,000 for the promotional campaigns, in which amount of $550,000

was to be paid to advertising campaign of television. Another $1,100,000 was paid to

a common campaign of advertising which were inclusive of TV, media and radio.

During the launch of Big Bank home and contents insurance policies by the Big Bank

Ltd, it predicted that its business of home and contents insurance will comprise 2

percent of the total entity. Big bank prediction was proved to be correct, the

remaining 98% is comprised of conventional loans and deposit facilities businesses.

This case study is based on analysis of allowance of GST credit.

Description of legal provisions

Business can make claim for a credit for any of the GST inclusive in the price

of items that business pays to use them in its operations (King, 2016). This is known

as GST credit (or can also be known as input-tax credit, for the tax inclusive in the

business inputs price).

Business claims for GST credits in their activity statement if these below mentioned

four conditions are applicable:

Business purpose of purchases is exclusively or partially in running the

business and the purchased are not related to make up of input-taxed

supplies

Price of Purchases is inclusive of GST (Bankman and et.al, 2017)

Business offer, or are responsible to offer, item payment they purchased

Business contains a tax invoice from its suppliers (purchases of maximum

$82.5)

Application of cited provisions

By considering the cited provisions it can be said that Big Bank is entitled to

take input credit of advertisement as expenses as purchase of service is exclusively

related to running the business and price of Purchases is inclusive of GST. Further,

business is providing taxable services and they contains a tax invoice from its

suppliers.

Issue

According to the cited case situation, Big Bank Ltd has its operations

nationwide, having over 50 branches and are authorized for the purpose of GST.

Bing bank has offered loan and deposits to Australian customers. Big bank has

spent over $1,650,000 for the promotional campaigns, in which amount of $550,000

was to be paid to advertising campaign of television. Another $1,100,000 was paid to

a common campaign of advertising which were inclusive of TV, media and radio.

During the launch of Big Bank home and contents insurance policies by the Big Bank

Ltd, it predicted that its business of home and contents insurance will comprise 2

percent of the total entity. Big bank prediction was proved to be correct, the

remaining 98% is comprised of conventional loans and deposit facilities businesses.

This case study is based on analysis of allowance of GST credit.

Description of legal provisions

Business can make claim for a credit for any of the GST inclusive in the price

of items that business pays to use them in its operations (King, 2016). This is known

as GST credit (or can also be known as input-tax credit, for the tax inclusive in the

business inputs price).

Business claims for GST credits in their activity statement if these below mentioned

four conditions are applicable:

Business purpose of purchases is exclusively or partially in running the

business and the purchased are not related to make up of input-taxed

supplies

Price of Purchases is inclusive of GST (Bankman and et.al, 2017)

Business offer, or are responsible to offer, item payment they purchased

Business contains a tax invoice from its suppliers (purchases of maximum

$82.5)

Application of cited provisions

By considering the cited provisions it can be said that Big Bank is entitled to

take input credit of advertisement as expenses as purchase of service is exclusively

related to running the business and price of Purchases is inclusive of GST. Further,

business is providing taxable services and they contains a tax invoice from its

suppliers.

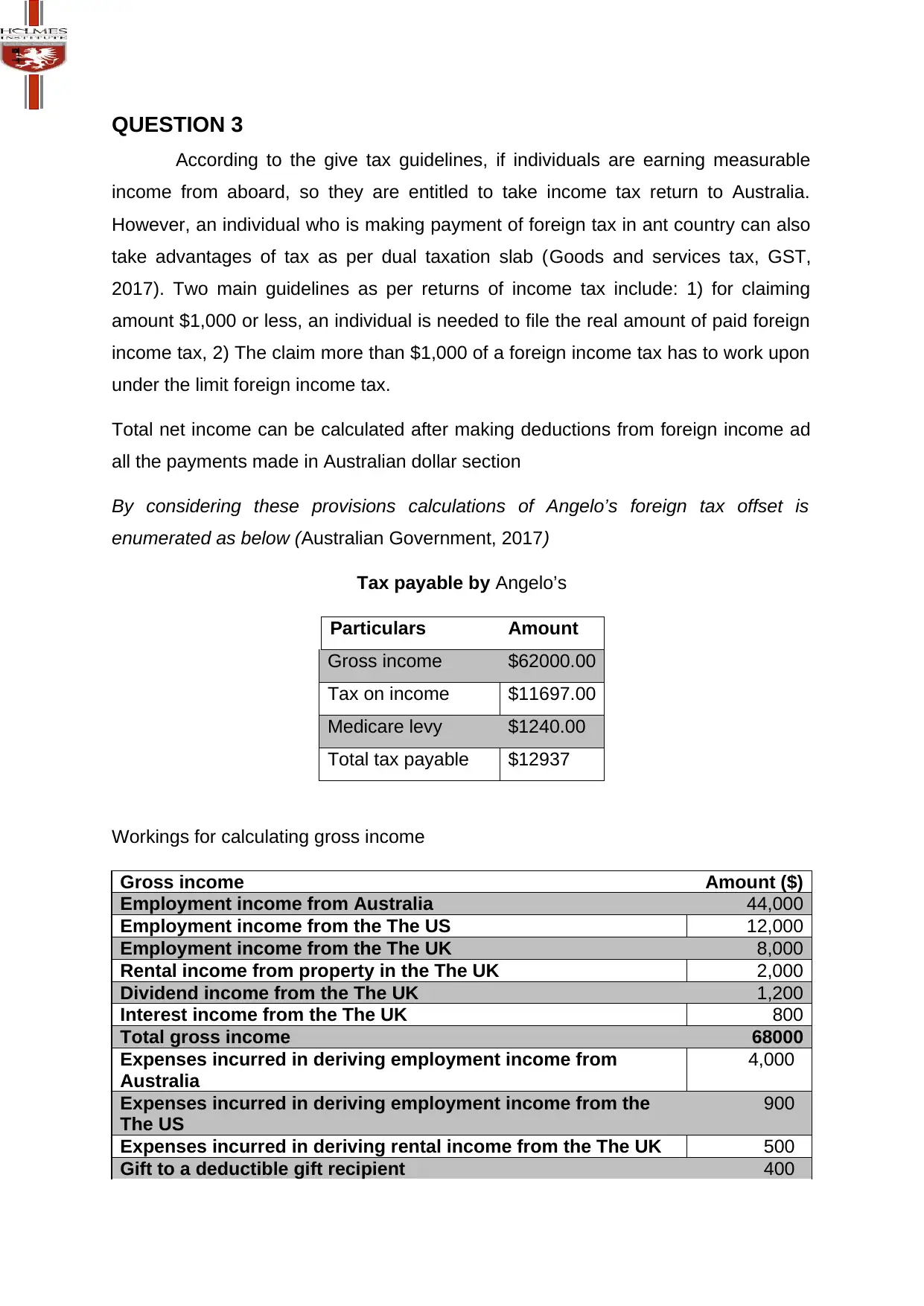

QUESTION 3

According to the give tax guidelines, if individuals are earning measurable

income from aboard, so they are entitled to take income tax return to Australia.

However, an individual who is making payment of foreign tax in ant country can also

take advantages of tax as per dual taxation slab (Goods and services tax, GST,

2017). Two main guidelines as per returns of income tax include: 1) for claiming

amount $1,000 or less, an individual is needed to file the real amount of paid foreign

income tax, 2) The claim more than $1,000 of a foreign income tax has to work upon

under the limit foreign income tax.

Total net income can be calculated after making deductions from foreign income ad

all the payments made in Australian dollar section

By considering these provisions calculations of Angelo’s foreign tax offset is

enumerated as below (Australian Government, 2017)

Tax payable by Angelo’s

Particulars Amount

Gross income $62000.00

Tax on income $11697.00

Medicare levy $1240.00

Total tax payable $12937

Workings for calculating gross income

Gross income Amount ($)

Employment income from Australia 44,000

Employment income from the The US 12,000

Employment income from the The UK 8,000

Rental income from property in the The UK 2,000

Dividend income from the The UK 1,200

Interest income from the The UK 800

Total gross income 68000

Expenses incurred in deriving employment income from

Australia

4,000

Expenses incurred in deriving employment income from the

The US

900

Expenses incurred in deriving rental income from the The UK 500

Gift to a deductible gift recipient 400

According to the give tax guidelines, if individuals are earning measurable

income from aboard, so they are entitled to take income tax return to Australia.

However, an individual who is making payment of foreign tax in ant country can also

take advantages of tax as per dual taxation slab (Goods and services tax, GST,

2017). Two main guidelines as per returns of income tax include: 1) for claiming

amount $1,000 or less, an individual is needed to file the real amount of paid foreign

income tax, 2) The claim more than $1,000 of a foreign income tax has to work upon

under the limit foreign income tax.

Total net income can be calculated after making deductions from foreign income ad

all the payments made in Australian dollar section

By considering these provisions calculations of Angelo’s foreign tax offset is

enumerated as below (Australian Government, 2017)

Tax payable by Angelo’s

Particulars Amount

Gross income $62000.00

Tax on income $11697.00

Medicare levy $1240.00

Total tax payable $12937

Workings for calculating gross income

Gross income Amount ($)

Employment income from Australia 44,000

Employment income from the The US 12,000

Employment income from the The UK 8,000

Rental income from property in the The UK 2,000

Dividend income from the The UK 1,200

Interest income from the The UK 800

Total gross income 68000

Expenses incurred in deriving employment income from

Australia

4,000

Expenses incurred in deriving employment income from the

The US

900

Expenses incurred in deriving rental income from the The UK 500

Gift to a deductible gift recipient 400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

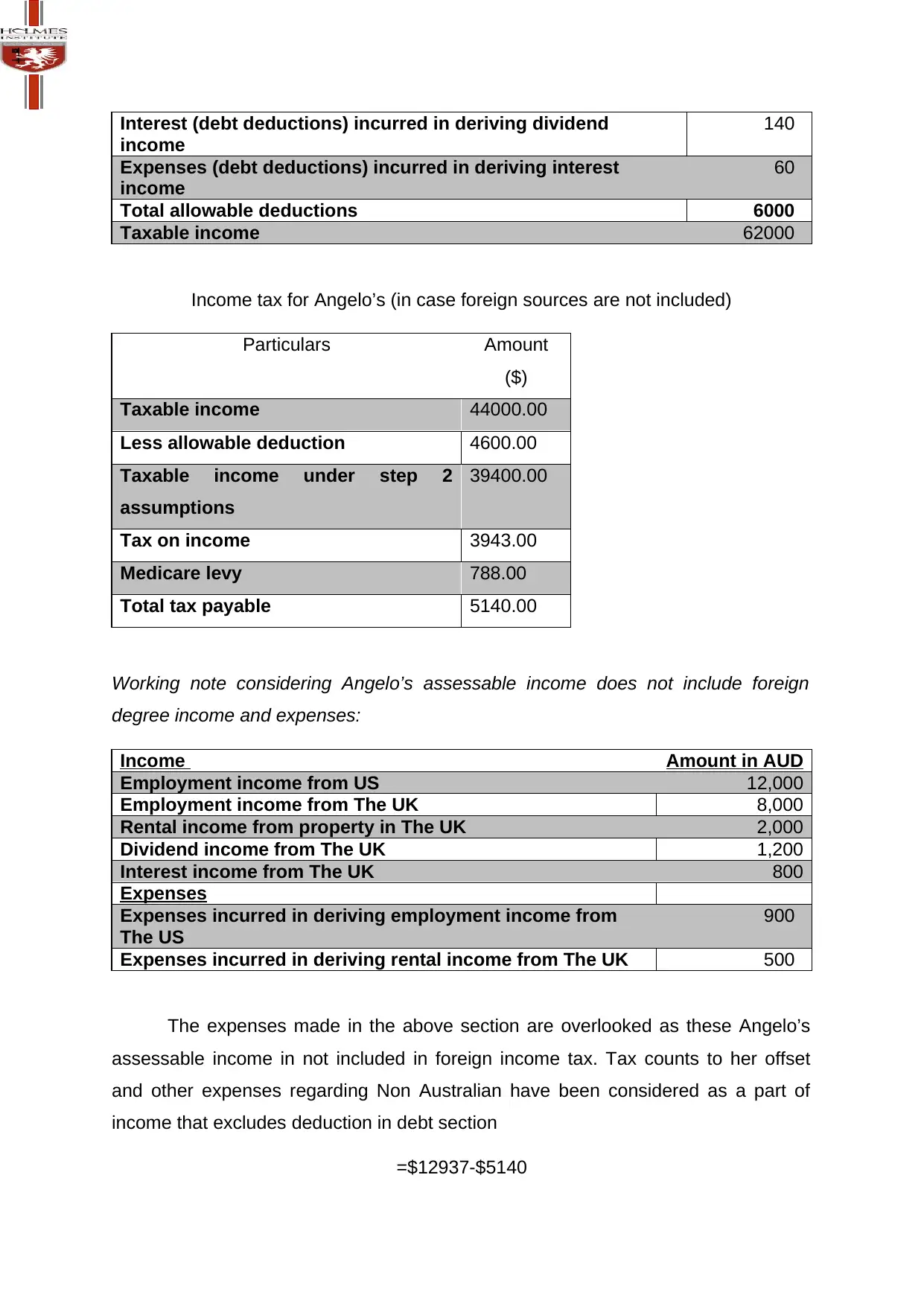

Interest (debt deductions) incurred in deriving dividend

income

140

Expenses (debt deductions) incurred in deriving interest

income

60

Total allowable deductions 6000

Taxable income 62000

Income tax for Angelo’s (in case foreign sources are not included)

Particulars Amount

($)

Taxable income 44000.00

Less allowable deduction 4600.00

Taxable income under step 2

assumptions

39400.00

Tax on income 3943.00

Medicare levy 788.00

Total tax payable 5140.00

Working note considering Angelo’s assessable income does not include foreign

degree income and expenses:

Income Amount in AUD

Employment income from US 12,000

Employment income from The UK 8,000

Rental income from property in The UK 2,000

Dividend income from The UK 1,200

Interest income from The UK 800

Expenses

Expenses incurred in deriving employment income from

The US

900

Expenses incurred in deriving rental income from The UK 500

The expenses made in the above section are overlooked as these Angelo’s

assessable income in not included in foreign income tax. Tax counts to her offset

and other expenses regarding Non Australian have been considered as a part of

income that excludes deduction in debt section

=$12937-$5140

income

140

Expenses (debt deductions) incurred in deriving interest

income

60

Total allowable deductions 6000

Taxable income 62000

Income tax for Angelo’s (in case foreign sources are not included)

Particulars Amount

($)

Taxable income 44000.00

Less allowable deduction 4600.00

Taxable income under step 2

assumptions

39400.00

Tax on income 3943.00

Medicare levy 788.00

Total tax payable 5140.00

Working note considering Angelo’s assessable income does not include foreign

degree income and expenses:

Income Amount in AUD

Employment income from US 12,000

Employment income from The UK 8,000

Rental income from property in The UK 2,000

Dividend income from The UK 1,200

Interest income from The UK 800

Expenses

Expenses incurred in deriving employment income from

The US

900

Expenses incurred in deriving rental income from The UK 500

The expenses made in the above section are overlooked as these Angelo’s

assessable income in not included in foreign income tax. Tax counts to her offset

and other expenses regarding Non Australian have been considered as a part of

income that excludes deduction in debt section

=$12937-$5140

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=$7797

The amount paid of $4,400 in not included as Angelo’s foreign income tax and

a difference amount between the offset limit and paid amount is carried in the

upcoming year.

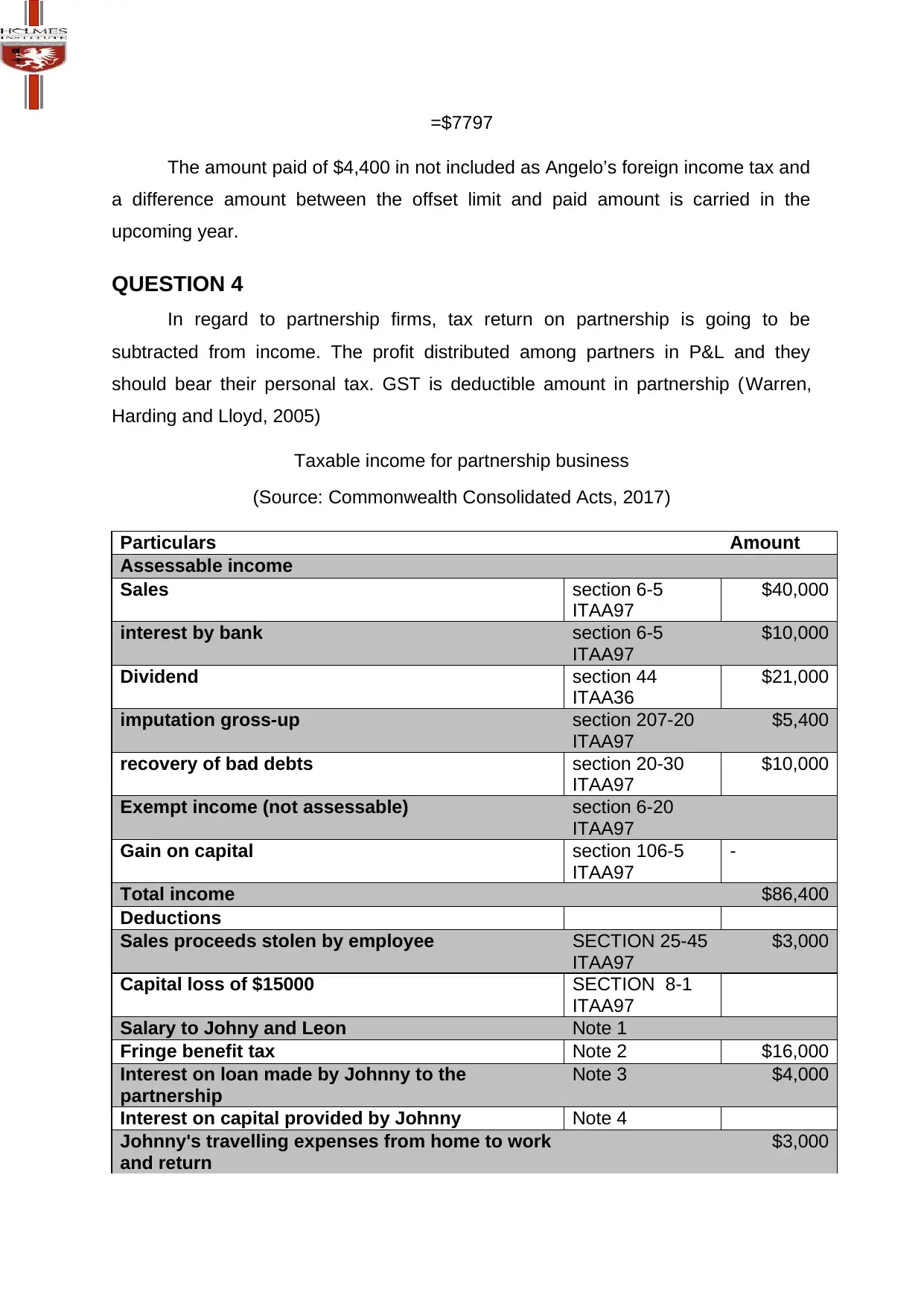

QUESTION 4

In regard to partnership firms, tax return on partnership is going to be

subtracted from income. The profit distributed among partners in P&L and they

should bear their personal tax. GST is deductible amount in partnership (Warren,

Harding and Lloyd, 2005)

Taxable income for partnership business

(Source: Commonwealth Consolidated Acts, 2017)

Particulars Amount

Assessable income

Sales section 6-5

ITAA97

$40,000

interest by bank section 6-5

ITAA97

$10,000

Dividend section 44

ITAA36

$21,000

imputation gross-up section 207-20

ITAA97

$5,400

recovery of bad debts section 20-30

ITAA97

$10,000

Exempt income (not assessable) section 6-20

ITAA97

Gain on capital section 106-5

ITAA97

-

Total income $86,400

Deductions

Sales proceeds stolen by employee SECTION 25-45

ITAA97

$3,000

Capital loss of $15000 SECTION 8-1

ITAA97

Salary to Johny and Leon Note 1

Fringe benefit tax Note 2 $16,000

Interest on loan made by Johnny to the

partnership

Note 3 $4,000

Interest on capital provided by Johnny Note 4

Johnny's travelling expenses from home to work

and return

$3,000

The amount paid of $4,400 in not included as Angelo’s foreign income tax and

a difference amount between the offset limit and paid amount is carried in the

upcoming year.

QUESTION 4

In regard to partnership firms, tax return on partnership is going to be

subtracted from income. The profit distributed among partners in P&L and they

should bear their personal tax. GST is deductible amount in partnership (Warren,

Harding and Lloyd, 2005)

Taxable income for partnership business

(Source: Commonwealth Consolidated Acts, 2017)

Particulars Amount

Assessable income

Sales section 6-5

ITAA97

$40,000

interest by bank section 6-5

ITAA97

$10,000

Dividend section 44

ITAA36

$21,000

imputation gross-up section 207-20

ITAA97

$5,400

recovery of bad debts section 20-30

ITAA97

$10,000

Exempt income (not assessable) section 6-20

ITAA97

Gain on capital section 106-5

ITAA97

-

Total income $86,400

Deductions

Sales proceeds stolen by employee SECTION 25-45

ITAA97

$3,000

Capital loss of $15000 SECTION 8-1

ITAA97

Salary to Johny and Leon Note 1

Fringe benefit tax Note 2 $16,000

Interest on loan made by Johnny to the

partnership

Note 3 $4,000

Interest on capital provided by Johnny Note 4

Johnny's travelling expenses from home to work

and return

$3,000

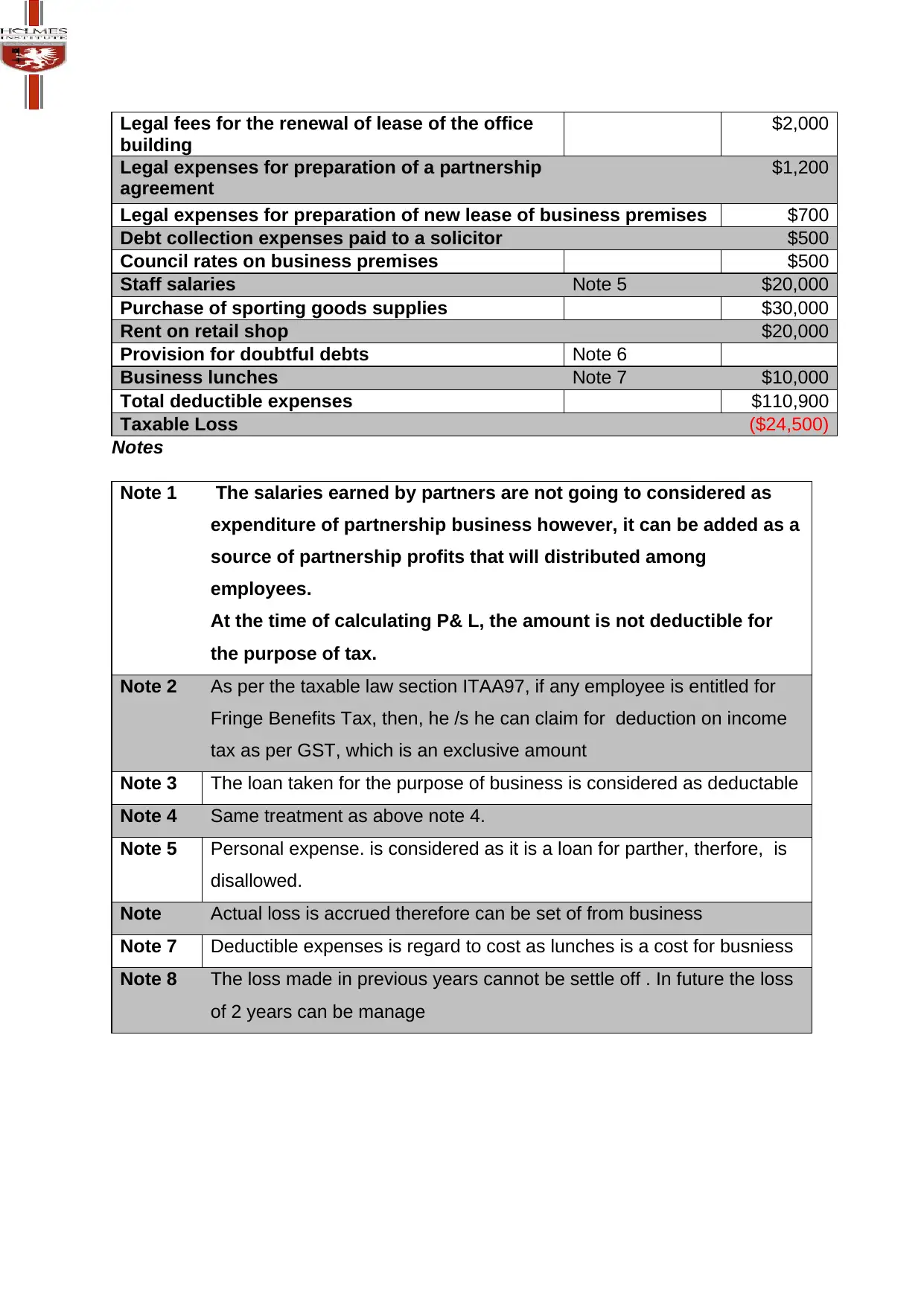

Legal fees for the renewal of lease of the office

building

$2,000

Legal expenses for preparation of a partnership

agreement

$1,200

Legal expenses for preparation of new lease of business premises $700

Debt collection expenses paid to a solicitor $500

Council rates on business premises $500

Staff salaries Note 5 $20,000

Purchase of sporting goods supplies $30,000

Rent on retail shop $20,000

Provision for doubtful debts Note 6

Business lunches Note 7 $10,000

Total deductible expenses $110,900

Taxable Loss ($24,500)

Notes

Note 1 The salaries earned by partners are not going to considered as

expenditure of partnership business however, it can be added as a

source of partnership profits that will distributed among

employees.

At the time of calculating P& L, the amount is not deductible for

the purpose of tax.

Note 2 As per the taxable law section ITAA97, if any employee is entitled for

Fringe Benefits Tax, then, he /s he can claim for deduction on income

tax as per GST, which is an exclusive amount

Note 3 The loan taken for the purpose of business is considered as deductable

Note 4 Same treatment as above note 4.

Note 5 Personal expense. is considered as it is a loan for parther, therfore, is

disallowed.

Note Actual loss is accrued therefore can be set of from business

Note 7 Deductible expenses is regard to cost as lunches is a cost for busniess

Note 8 The loss made in previous years cannot be settle off . In future the loss

of 2 years can be manage

building

$2,000

Legal expenses for preparation of a partnership

agreement

$1,200

Legal expenses for preparation of new lease of business premises $700

Debt collection expenses paid to a solicitor $500

Council rates on business premises $500

Staff salaries Note 5 $20,000

Purchase of sporting goods supplies $30,000

Rent on retail shop $20,000

Provision for doubtful debts Note 6

Business lunches Note 7 $10,000

Total deductible expenses $110,900

Taxable Loss ($24,500)

Notes

Note 1 The salaries earned by partners are not going to considered as

expenditure of partnership business however, it can be added as a

source of partnership profits that will distributed among

employees.

At the time of calculating P& L, the amount is not deductible for

the purpose of tax.

Note 2 As per the taxable law section ITAA97, if any employee is entitled for

Fringe Benefits Tax, then, he /s he can claim for deduction on income

tax as per GST, which is an exclusive amount

Note 3 The loan taken for the purpose of business is considered as deductable

Note 4 Same treatment as above note 4.

Note 5 Personal expense. is considered as it is a loan for parther, therfore, is

disallowed.

Note Actual loss is accrued therefore can be set of from business

Note 7 Deductible expenses is regard to cost as lunches is a cost for busniess

Note 8 The loss made in previous years cannot be settle off . In future the loss

of 2 years can be manage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Buchanan, R. and Consett, E., 2016. Section 974-80 ITAA97: The current state of

play. Tax Specialist, 19(5), p.217.

Datt, K., Nienaber, G. and Tran-Nam, B., 2017. GST/VAT general anti-avoidance

approaches: Some preliminary findings from a comparative study of Australia and

South Africa. In Australian Tax Forum (Vol. 32, No. 2, p. 377). Tax Institute.

Dixon, J.M. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in

Australia. Centre for Policy Studies, Victoria University.

Dunne, J., Mason, J. and Patto, J., 2014. 2013 cases show high ATO success

rate. Taxation in Australia, 48(8), p.429.

Edmonds, M., Holle, C. and Hartanti, W., 2015. Alternative assets insights: Super

funds-tax impediments to going global. Taxation in Australia, 49(7), p.413.

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part

2. Taxation in Australia, 51(1), p.12.

Liu, B., Huang, A. and Freudenberg, B., 2014. The impact of the GST on mortgage

pricing of Australian credit unions: An empirical analysis. Accounting Research

Journal, 27(1), pp.37-51.

Millar, R., 2016. Limitations on the right to credit input tax: Rio Tinto Services Limited

v Commissioner of Taxation [2015] FCAFC 117. World Journal of VAT/GST

Law, 5(1), pp.42-47.

Somers, R. and Eynaud, A., 2015. A matter of trusts: The ATO's proposed treatment

of unpaid present entitlements: Part 1. Taxation in Australia, 50(2), p.90.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed

companies in Australia?. Browser Download This Paper.

Goods and services tax (GST), 2017. Available at

<https://www.ato.gov.au/Business/Business-activity-statements-(BAS)/Goods-and-

services-tax-(GST)/ > [Accessed from 11th September 2017]

Commonwealth Consolidated Acts, 2017. INCOME TAX ASSESSMENT ACT 1997 -

SECT 8.1 General deductionsection Available at <http://www6.austlii.edu.au/cgi-

Buchanan, R. and Consett, E., 2016. Section 974-80 ITAA97: The current state of

play. Tax Specialist, 19(5), p.217.

Datt, K., Nienaber, G. and Tran-Nam, B., 2017. GST/VAT general anti-avoidance

approaches: Some preliminary findings from a comparative study of Australia and

South Africa. In Australian Tax Forum (Vol. 32, No. 2, p. 377). Tax Institute.

Dixon, J.M. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in

Australia. Centre for Policy Studies, Victoria University.

Dunne, J., Mason, J. and Patto, J., 2014. 2013 cases show high ATO success

rate. Taxation in Australia, 48(8), p.429.

Edmonds, M., Holle, C. and Hartanti, W., 2015. Alternative assets insights: Super

funds-tax impediments to going global. Taxation in Australia, 49(7), p.413.

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part

2. Taxation in Australia, 51(1), p.12.

Liu, B., Huang, A. and Freudenberg, B., 2014. The impact of the GST on mortgage

pricing of Australian credit unions: An empirical analysis. Accounting Research

Journal, 27(1), pp.37-51.

Millar, R., 2016. Limitations on the right to credit input tax: Rio Tinto Services Limited

v Commissioner of Taxation [2015] FCAFC 117. World Journal of VAT/GST

Law, 5(1), pp.42-47.

Somers, R. and Eynaud, A., 2015. A matter of trusts: The ATO's proposed treatment

of unpaid present entitlements: Part 1. Taxation in Australia, 50(2), p.90.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed

companies in Australia?. Browser Download This Paper.

Goods and services tax (GST), 2017. Available at

<https://www.ato.gov.au/Business/Business-activity-statements-(BAS)/Goods-and-

services-tax-(GST)/ > [Accessed from 11th September 2017]

Commonwealth Consolidated Acts, 2017. INCOME TAX ASSESSMENT ACT 1997 -

SECT 8.1 General deductionsection Available at <http://www6.austlii.edu.au/cgi-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.1.html>. [Accessed on 9th

September 2017]

Warren, N., Harding, A. and Lloyd, R., 2005. GST and the changing incidence of

Australian taxes: 1994-95 to 2001-02. eJournal of Tax Research, 3(1), pp.114-45.

September 2017]

Warren, N., Harding, A. and Lloyd, R., 2005. GST and the changing incidence of

Australian taxes: 1994-95 to 2001-02. eJournal of Tax Research, 3(1), pp.114-45.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.