Holmes Institute HA3042 Taxation Law Individual Assignment T2 2019

VerifiedAdded on 2022/10/17

|12

|2864

|20

Homework Assignment

AI Summary

This taxation law assignment addresses key concepts in Australian taxation, focusing on Capital Gains Tax (CGT) and depreciation. The assignment analyzes different scenarios, including the sale of a main house, a car, a cleaning business, furniture, and paintings, to determine CGT implications. It also explores the tax deductions related to depreciating assets, specifically examining the case of a manufacturing business that purchased a CNC machine. The analysis covers relevant sections of the Income Tax Assessment Act 1997 (ITAA 97), including provisions related to personal use assets, small business entities, and the cost base of depreciating assets. The assignment applies legal principles to practical situations, providing detailed explanations and referencing relevant case law to support its conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Response A: Sale of main house:

The most common aspect of the CGT is that it is applicable on the assets that a

taxpayer has bought on or following 20/9/1985. While an exemption has been provided to the

taxpayer under “sec 104-10 (5) (a)” that assets which is purchased preceding the date of

20/9/1985 does not attracts tax liability (Dixon and Nassios 2016). These are called as pre-

CGT assets and falls out of the purview of CGT. There was an instance where Jasmine is

found to be selling her main house in the present tax year. The house was purchased by her

for $40,000 in 1981 and when Jasmine sold it fetched $650,000. The transaction clearly

shows that a capital gains has been made by her when the house was sold. However, the

house is falling under the pre-CGT asset because it was acquired in 1981 which is earlier to

the implementation of CGT regimes. Denoting “sec 104-10 (5) (a)” the capital gains are

exempted for Jasmine and no tax liability arises.

Response B: Sale of Car:

With respect to the “sec 108-20 (2)” the taxpayers should denote that the personal use

asset amounts to boats, electrical items, furniture, vehicles that is held by them for private

purpose and enjoyment (Burkhauser, Hahn and Wilkins 2015). Despite the fact “sec 108-20

(1)” requires the taxpayer to simply disregard the capital loss suffered from the personal use

asset. The liability to impose tax arises when the “CGT event A1” under “sec 104-10, ITA

Act 1997” happens.

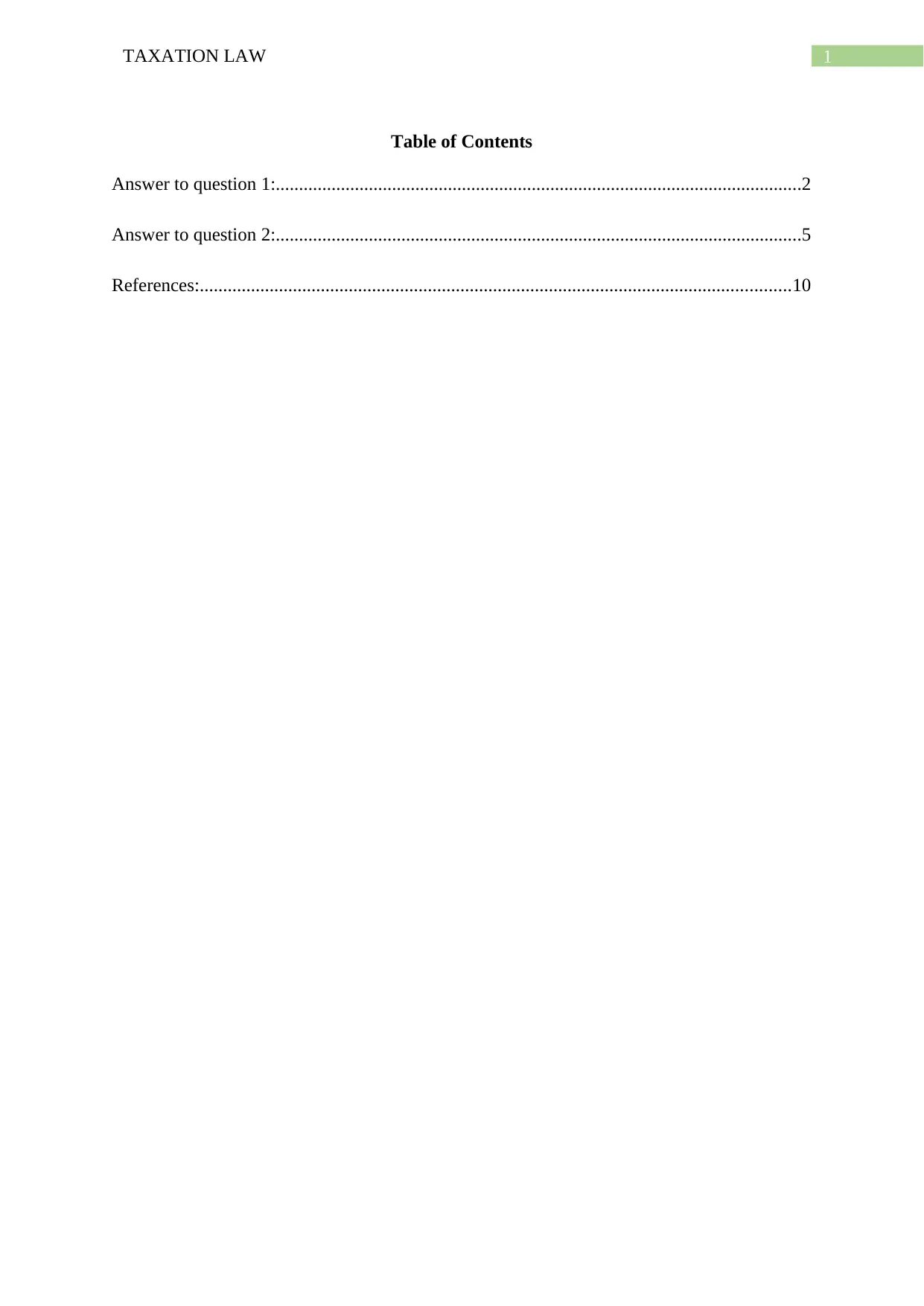

In continuance of Jasmine’s case facts, a car that she held from 2011 was sold in the

present year for $10,000. The car was actually purchased for $31,000. Citing “sec 108-20

(2)”, the car is a personal use asset and its sale has given rise to “CGT event A1” under “sec

Answer to question 1:

Response A: Sale of main house:

The most common aspect of the CGT is that it is applicable on the assets that a

taxpayer has bought on or following 20/9/1985. While an exemption has been provided to the

taxpayer under “sec 104-10 (5) (a)” that assets which is purchased preceding the date of

20/9/1985 does not attracts tax liability (Dixon and Nassios 2016). These are called as pre-

CGT assets and falls out of the purview of CGT. There was an instance where Jasmine is

found to be selling her main house in the present tax year. The house was purchased by her

for $40,000 in 1981 and when Jasmine sold it fetched $650,000. The transaction clearly

shows that a capital gains has been made by her when the house was sold. However, the

house is falling under the pre-CGT asset because it was acquired in 1981 which is earlier to

the implementation of CGT regimes. Denoting “sec 104-10 (5) (a)” the capital gains are

exempted for Jasmine and no tax liability arises.

Response B: Sale of Car:

With respect to the “sec 108-20 (2)” the taxpayers should denote that the personal use

asset amounts to boats, electrical items, furniture, vehicles that is held by them for private

purpose and enjoyment (Burkhauser, Hahn and Wilkins 2015). Despite the fact “sec 108-20

(1)” requires the taxpayer to simply disregard the capital loss suffered from the personal use

asset. The liability to impose tax arises when the “CGT event A1” under “sec 104-10, ITA

Act 1997” happens.

In continuance of Jasmine’s case facts, a car that she held from 2011 was sold in the

present year for $10,000. The car was actually purchased for $31,000. Citing “sec 108-20

(2)”, the car is a personal use asset and its sale has given rise to “CGT event A1” under “sec

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

104-10, ITA Act 1997” (Grudnoff 2015). However, as car is classified as personal use asset

the capital loss which is suffered by Jasmine must be disregarded under “sec 108-20 (1)”.

Response C: Sale of cleaning business:

There are some basic conditions that must be fulfilled under “Div 152” for the small

business entities (SBE) as upon fulfilling the conditions the SBE are allowed to get four types

of CGT concession (Feld et al. 2016). The concession are;

a. The business must have net value of asset not higher than $6 million or the revenues

should not go beyond $2 million to be classified as SBE.

b. The business must be having the active asset.

The four concessions for small business relief are as follows;

1. 15-year exemption: Under this the overall amount of capital gains which is earned

upon the sale of CGT asset owned for a minimum of 15 years is simply exempted.

The taxpayer should also be a minimum of 55 years older to get this benefit.

2. 50% reduction: A reduction by 50% following the application of general 50%

discount is available under this regime for taxpayers that qualifies for it (Evans, Minas

and Lim 2015).

3. Retirement concession: The capital gains are allowed for exemption when the

proceeds obtained from the disposal is used in the retirement of the taxpayers.

104-10, ITA Act 1997” (Grudnoff 2015). However, as car is classified as personal use asset

the capital loss which is suffered by Jasmine must be disregarded under “sec 108-20 (1)”.

Response C: Sale of cleaning business:

There are some basic conditions that must be fulfilled under “Div 152” for the small

business entities (SBE) as upon fulfilling the conditions the SBE are allowed to get four types

of CGT concession (Feld et al. 2016). The concession are;

a. The business must have net value of asset not higher than $6 million or the revenues

should not go beyond $2 million to be classified as SBE.

b. The business must be having the active asset.

The four concessions for small business relief are as follows;

1. 15-year exemption: Under this the overall amount of capital gains which is earned

upon the sale of CGT asset owned for a minimum of 15 years is simply exempted.

The taxpayer should also be a minimum of 55 years older to get this benefit.

2. 50% reduction: A reduction by 50% following the application of general 50%

discount is available under this regime for taxpayers that qualifies for it (Evans, Minas

and Lim 2015).

3. Retirement concession: The capital gains are allowed for exemption when the

proceeds obtained from the disposal is used in the retirement of the taxpayers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

4. Roll-over relief: Under this a relief is given to SBE when the capital gains are used in

purchasing another replacement asset.

Jasmine in the current situation is noticed to be selling her small business of cleaning

and during the sale she has made $125,000 from the business equipment and goodwill. It can

be stated that Jasmine is allowed to obtain a concession from capital gains because her

cleaning business qualifies as SBE. Her net value of assets was not greater than $2 million

and all her business assets qualified as active asset. So she can avail the 15-year exemption

from the capital gains made under “Div 152, ITA Act 97” as she has owned the asset for 15

years and also ages more than the qualifying age of 55 years or more.

Response D: Sale of furniture:

The most important aspect regarding the personal use asset that is explained in the

“sec 118-10, ITA Act 97” says that when a capital gains is earned by the taxpayer from

selling any personal use asset then the gains that made is disregarded if the asset fails to meet

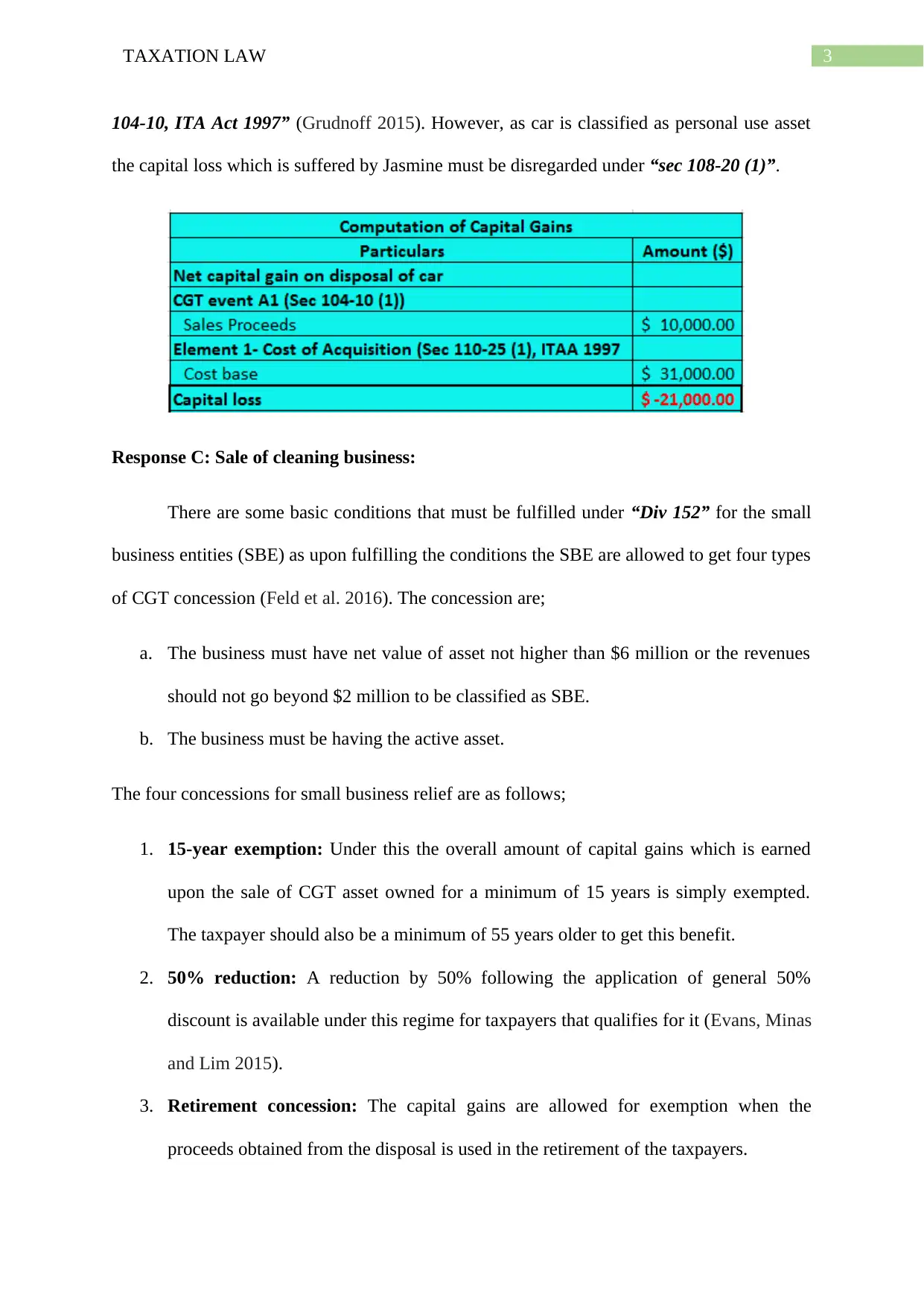

the first element cost of $10,000 (Chardon, Freudenberg and Brimble 2016). Jasmine in the

current case sold her furniture for $5000 which was purchased for $2,000. The capital gains

earned following the sale of furniture is disregarded in “sec 118-10, ITA Act 97” because its

cost base is lower than $10,000.

Response E: Sale of Painting:

4. Roll-over relief: Under this a relief is given to SBE when the capital gains are used in

purchasing another replacement asset.

Jasmine in the current situation is noticed to be selling her small business of cleaning

and during the sale she has made $125,000 from the business equipment and goodwill. It can

be stated that Jasmine is allowed to obtain a concession from capital gains because her

cleaning business qualifies as SBE. Her net value of assets was not greater than $2 million

and all her business assets qualified as active asset. So she can avail the 15-year exemption

from the capital gains made under “Div 152, ITA Act 97” as she has owned the asset for 15

years and also ages more than the qualifying age of 55 years or more.

Response D: Sale of furniture:

The most important aspect regarding the personal use asset that is explained in the

“sec 118-10, ITA Act 97” says that when a capital gains is earned by the taxpayer from

selling any personal use asset then the gains that made is disregarded if the asset fails to meet

the first element cost of $10,000 (Chardon, Freudenberg and Brimble 2016). Jasmine in the

current case sold her furniture for $5000 which was purchased for $2,000. The capital gains

earned following the sale of furniture is disregarded in “sec 118-10, ITA Act 97” because its

cost base is lower than $10,000.

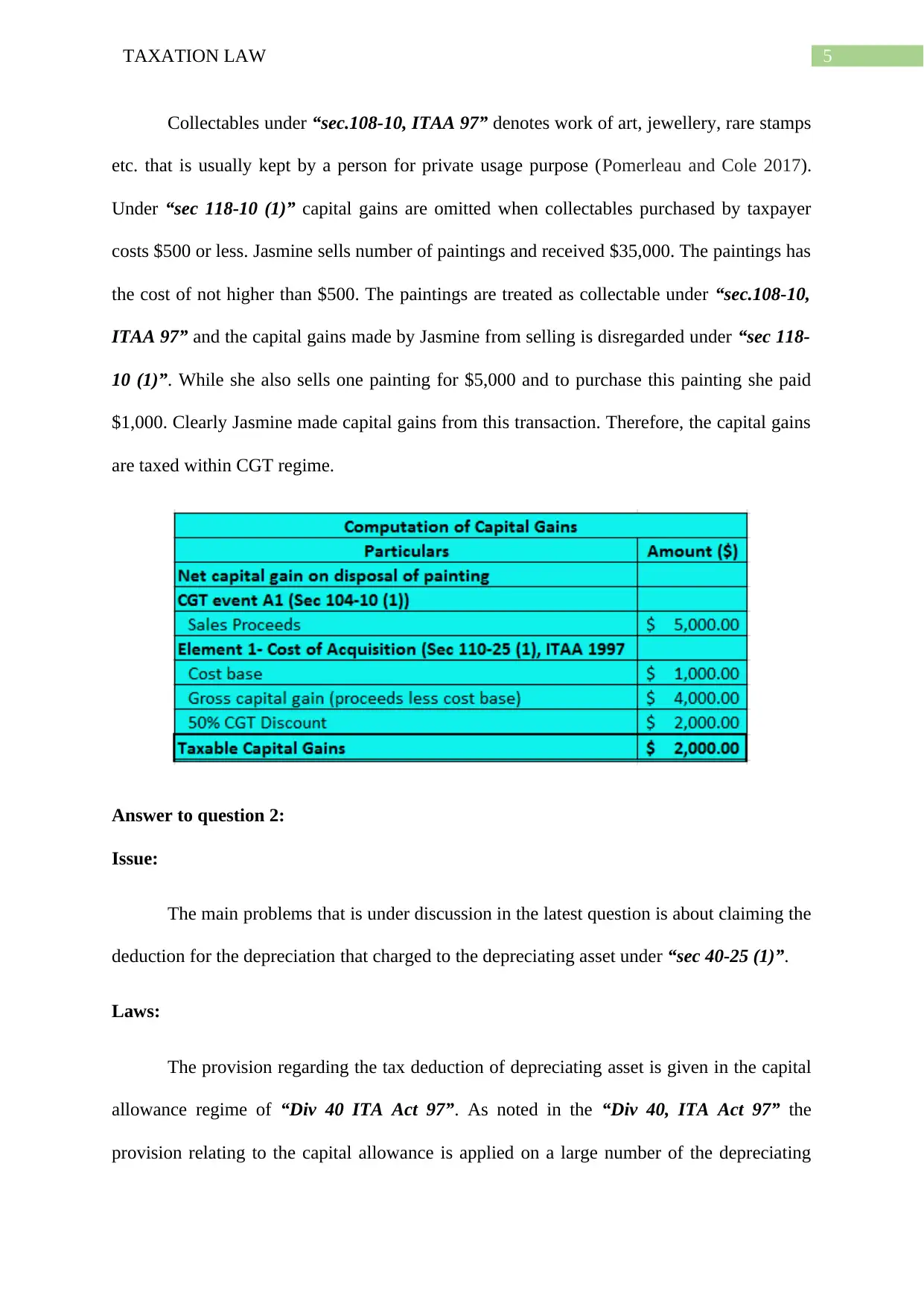

Response E: Sale of Painting:

5TAXATION LAW

Collectables under “sec.108-10, ITAA 97” denotes work of art, jewellery, rare stamps

etc. that is usually kept by a person for private usage purpose (Pomerleau and Cole 2017).

Under “sec 118-10 (1)” capital gains are omitted when collectables purchased by taxpayer

costs $500 or less. Jasmine sells number of paintings and received $35,000. The paintings has

the cost of not higher than $500. The paintings are treated as collectable under “sec.108-10,

ITAA 97” and the capital gains made by Jasmine from selling is disregarded under “sec 118-

10 (1)”. While she also sells one painting for $5,000 and to purchase this painting she paid

$1,000. Clearly Jasmine made capital gains from this transaction. Therefore, the capital gains

are taxed within CGT regime.

Answer to question 2:

Issue:

The main problems that is under discussion in the latest question is about claiming the

deduction for the depreciation that charged to the depreciating asset under “sec 40-25 (1)”.

Laws:

The provision regarding the tax deduction of depreciating asset is given in the capital

allowance regime of “Div 40 ITA Act 97”. As noted in the “Div 40, ITA Act 97” the

provision relating to the capital allowance is applied on a large number of the depreciating

Collectables under “sec.108-10, ITAA 97” denotes work of art, jewellery, rare stamps

etc. that is usually kept by a person for private usage purpose (Pomerleau and Cole 2017).

Under “sec 118-10 (1)” capital gains are omitted when collectables purchased by taxpayer

costs $500 or less. Jasmine sells number of paintings and received $35,000. The paintings has

the cost of not higher than $500. The paintings are treated as collectable under “sec.108-10,

ITAA 97” and the capital gains made by Jasmine from selling is disregarded under “sec 118-

10 (1)”. While she also sells one painting for $5,000 and to purchase this painting she paid

$1,000. Clearly Jasmine made capital gains from this transaction. Therefore, the capital gains

are taxed within CGT regime.

Answer to question 2:

Issue:

The main problems that is under discussion in the latest question is about claiming the

deduction for the depreciation that charged to the depreciating asset under “sec 40-25 (1)”.

Laws:

The provision regarding the tax deduction of depreciating asset is given in the capital

allowance regime of “Div 40 ITA Act 97”. As noted in the “Div 40, ITA Act 97” the

provision relating to the capital allowance is applied on a large number of the depreciating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

assets under “sec.40-30 ITA Act 97”, as these expenses are not eligible for capital works

under “sec 40-50, ITA Act 97” (Kenny 2018). The taxpayers are required to denote that the

purchase of the depreciating asset is regarded as capital expenses and it is not allowed for

deduction under the “sec 8-1, ITAA 97”. The federal court passed its verdict in the case of

“Sun Newspapers v FCT (1938)” where the profit producing structure test represents that the

outlays with regard to the profit generating structure or the business entity amounts to a

capital expense.

The main focus of “Division 40” is that it mainly emphasizes on deduction for the

depreciation of the specific assets that are employed in generation of taxable earnings

(Mahar, Longridge and He 2016). A deduction associated to the “decline in value” for the

“depreciating asset” is allowed inside “sec.40-25 (1), ITA Act 97”. Depreciation should not

be viewed as the loss or outlays and the acquisition of asset is termed as capital, therefore

“sec 8-1” is not operative.

Depreciating asset is better defined in the “sec 40.30 (1), ITA Act 97”. It is termed as

the asset which only has very limited usable life. The depreciating asset is practically

projected to fall in their worth over the span of their usage (Black 2018). However, the

taxpayer should also denote that depreciating asset does not includes the trading stock or

land. The term asset usually does not has any definition and only has an ordinary meaning

which is considered under the definition of plant. As noted from the judgement of federal

court in “Wangaratta Woollen Mills Ltd v. FCT” 69 ATC 4095, a structure that was having

the shape of dye house was treated as plant, opposing to the normal situation with structures

in the form of building.

The taxpayers are required to denote that the “subsection 40.25 (1)” permits an

allowable deduction relating to the depreciating assets fall in value to those taxpayers that

assets under “sec.40-30 ITA Act 97”, as these expenses are not eligible for capital works

under “sec 40-50, ITA Act 97” (Kenny 2018). The taxpayers are required to denote that the

purchase of the depreciating asset is regarded as capital expenses and it is not allowed for

deduction under the “sec 8-1, ITAA 97”. The federal court passed its verdict in the case of

“Sun Newspapers v FCT (1938)” where the profit producing structure test represents that the

outlays with regard to the profit generating structure or the business entity amounts to a

capital expense.

The main focus of “Division 40” is that it mainly emphasizes on deduction for the

depreciation of the specific assets that are employed in generation of taxable earnings

(Mahar, Longridge and He 2016). A deduction associated to the “decline in value” for the

“depreciating asset” is allowed inside “sec.40-25 (1), ITA Act 97”. Depreciation should not

be viewed as the loss or outlays and the acquisition of asset is termed as capital, therefore

“sec 8-1” is not operative.

Depreciating asset is better defined in the “sec 40.30 (1), ITA Act 97”. It is termed as

the asset which only has very limited usable life. The depreciating asset is practically

projected to fall in their worth over the span of their usage (Black 2018). However, the

taxpayer should also denote that depreciating asset does not includes the trading stock or

land. The term asset usually does not has any definition and only has an ordinary meaning

which is considered under the definition of plant. As noted from the judgement of federal

court in “Wangaratta Woollen Mills Ltd v. FCT” 69 ATC 4095, a structure that was having

the shape of dye house was treated as plant, opposing to the normal situation with structures

in the form of building.

The taxpayers are required to denote that the “subsection 40.25 (1)” permits an

allowable deduction relating to the depreciating assets fall in value to those taxpayers that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

holds the asset (Killaly 2017). While “sec 40.40” is generally associated with holding the

asset. Usually, sec 40.40 is operative on the legal owner that holds the asset and they will be

viewed as rightfully entitled to a deduction.

The relevant dates for claiming depreciation is also considered important. When a

taxpayer holds the “depreciating asset” it begins to decline in terms of its value when the

start time of the asset inaugurates (Paull 2016). In other words, under “sec 40-60 (1), ITA

Act 97” the start time of the depreciating assets inaugurates when it is first utilized or

installed by the taxpayer as ready for commercial usage or for any other purpose.

“Subdivision 40-C” says that depreciation is allowed for calculations based on the

cost of depreciating asset. The cost under “sec 40-175” comprises of the two important

elements. These are;

1st Element Cost Base: This includes the consideration that is paid by taxpayer to

ultimately acquire the asset. Under “sec 40.180” the first element cost base involves

the purchase price together with the incidental expenses occurred while purchasing

the asset such as the stamp duty.

2nd Element Cost Base: This element of the depreciating asset involves the

consideration that is given by the taxpayer to finally bring the asset to its current state

and location from time to time (Ingles and Stewart 2018). The examples of the cost

under “sec 40.190, ITA Act 97” includes the transportation cost, insurance, capital

improvements, installation cost.

Application:

The application of the overhead cited laws is executed in the circumstance of John

who in the present case is operating a business of manufacturing company. John as found in

the present situation is the producer of certified BMW parts. An instance that was reported by

holds the asset (Killaly 2017). While “sec 40.40” is generally associated with holding the

asset. Usually, sec 40.40 is operative on the legal owner that holds the asset and they will be

viewed as rightfully entitled to a deduction.

The relevant dates for claiming depreciation is also considered important. When a

taxpayer holds the “depreciating asset” it begins to decline in terms of its value when the

start time of the asset inaugurates (Paull 2016). In other words, under “sec 40-60 (1), ITA

Act 97” the start time of the depreciating assets inaugurates when it is first utilized or

installed by the taxpayer as ready for commercial usage or for any other purpose.

“Subdivision 40-C” says that depreciation is allowed for calculations based on the

cost of depreciating asset. The cost under “sec 40-175” comprises of the two important

elements. These are;

1st Element Cost Base: This includes the consideration that is paid by taxpayer to

ultimately acquire the asset. Under “sec 40.180” the first element cost base involves

the purchase price together with the incidental expenses occurred while purchasing

the asset such as the stamp duty.

2nd Element Cost Base: This element of the depreciating asset involves the

consideration that is given by the taxpayer to finally bring the asset to its current state

and location from time to time (Ingles and Stewart 2018). The examples of the cost

under “sec 40.190, ITA Act 97” includes the transportation cost, insurance, capital

improvements, installation cost.

Application:

The application of the overhead cited laws is executed in the circumstance of John

who in the present case is operating a business of manufacturing company. John as found in

the present situation is the producer of certified BMW parts. An instance that was reported by

8TAXATION LAW

him includes a visit to CNC machine factory in Germany. The machine was ultimately

acquired by John in consideration of $300,000. The CNC machine which John has purchased

is regarded as the depreciating capital asset and hence the cost paid is not allowed for

deduction under operative provision of “sec 8-1, ITA Act 97”. Citing “Sun Newspaper v

FCT (1938)” the CNC machine is a profit yielding structure and the expenses incurred by

John is capital in nature.

All the same, John must refer to the “Division 40, ITA Act 97” that deals with capital

allowance of depreciating assed used in generation of taxable earnings. A deduction for

decline in value of CNC machine under “sec 40.25 (1)” will be permitted to John since

depreciation cannot be termed as loss or outlays. Also under “sec 40.30 (1)” the CNC

machine is described as the depreciating asset (Evans and Razeed 2018). Referring to

“Wangaratta Woollen Mills Ltd v. FCT” 69 ATC 4095 the CNC machine meets the ordinary

definition of plant because it is having a limited active life and with the passage of time the

CNC machine is projected to fall in its value. A deduction will be usually entitled to John

under “sec 40.40” since he is holding the asset legally.

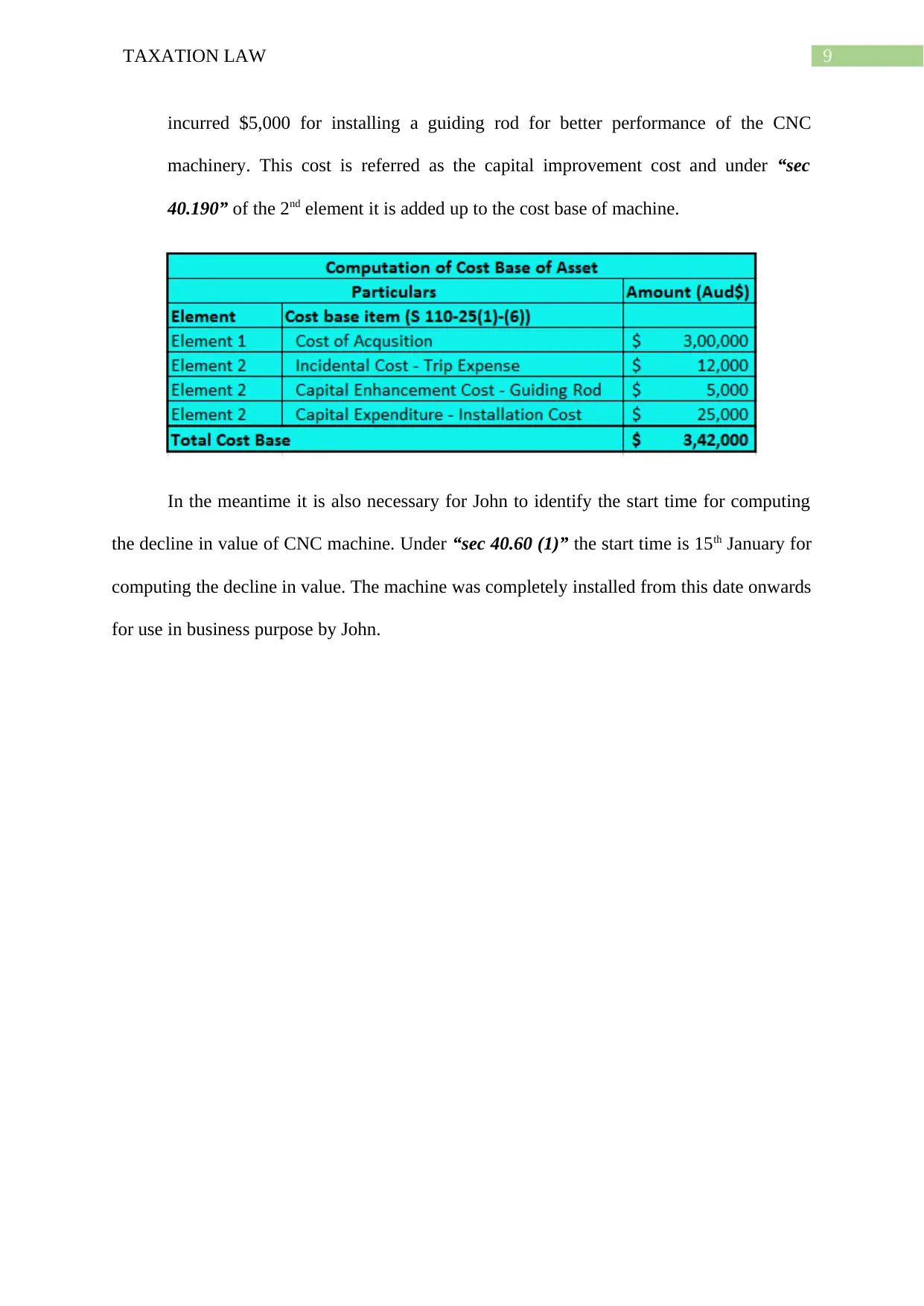

Prior to computing the decline in value of the CNC machine it is important to identify its

cost. Noting “sec 40.175” a depreciation for CNC machine can be computed on the basis of

its cost that is divided below in two elements.

1st Element cost base: Under the first element the consideration that is paid by John

to hold the CNC machine has been included. Referring to “sec 40.180” the purchase

price forms the acquisition cost of the machine.

2nd Element cost base: John is found to have reported travel expenses of $12,000 for

inspecting the machine and also reported an installation cost of $25,000 for installing

the machine. These costs are included in the 2nd element cost base. While he further

him includes a visit to CNC machine factory in Germany. The machine was ultimately

acquired by John in consideration of $300,000. The CNC machine which John has purchased

is regarded as the depreciating capital asset and hence the cost paid is not allowed for

deduction under operative provision of “sec 8-1, ITA Act 97”. Citing “Sun Newspaper v

FCT (1938)” the CNC machine is a profit yielding structure and the expenses incurred by

John is capital in nature.

All the same, John must refer to the “Division 40, ITA Act 97” that deals with capital

allowance of depreciating assed used in generation of taxable earnings. A deduction for

decline in value of CNC machine under “sec 40.25 (1)” will be permitted to John since

depreciation cannot be termed as loss or outlays. Also under “sec 40.30 (1)” the CNC

machine is described as the depreciating asset (Evans and Razeed 2018). Referring to

“Wangaratta Woollen Mills Ltd v. FCT” 69 ATC 4095 the CNC machine meets the ordinary

definition of plant because it is having a limited active life and with the passage of time the

CNC machine is projected to fall in its value. A deduction will be usually entitled to John

under “sec 40.40” since he is holding the asset legally.

Prior to computing the decline in value of the CNC machine it is important to identify its

cost. Noting “sec 40.175” a depreciation for CNC machine can be computed on the basis of

its cost that is divided below in two elements.

1st Element cost base: Under the first element the consideration that is paid by John

to hold the CNC machine has been included. Referring to “sec 40.180” the purchase

price forms the acquisition cost of the machine.

2nd Element cost base: John is found to have reported travel expenses of $12,000 for

inspecting the machine and also reported an installation cost of $25,000 for installing

the machine. These costs are included in the 2nd element cost base. While he further

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

incurred $5,000 for installing a guiding rod for better performance of the CNC

machinery. This cost is referred as the capital improvement cost and under “sec

40.190” of the 2nd element it is added up to the cost base of machine.

In the meantime it is also necessary for John to identify the start time for computing

the decline in value of CNC machine. Under “sec 40.60 (1)” the start time is 15th January for

computing the decline in value. The machine was completely installed from this date onwards

for use in business purpose by John.

incurred $5,000 for installing a guiding rod for better performance of the CNC

machinery. This cost is referred as the capital improvement cost and under “sec

40.190” of the 2nd element it is added up to the cost base of machine.

In the meantime it is also necessary for John to identify the start time for computing

the decline in value of CNC machine. Under “sec 40.60 (1)” the start time is 15th January for

computing the decline in value. The machine was completely installed from this date onwards

for use in business purpose by John.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax Treaties",

IBFD: Amsterdam.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Evans, J.R. and Razeed, A., 2018. An Analysis of Household Retirement Adequacy In

Australia. Available at SSRN 3302331.

Feld, L.P., Ruf, M., Schreiber, U., Todtenhaupt, M. and Voget, J., 2016. Taxing away M&A:

The effect of corporate capital gains taxes on acquisition activity.

Grudnoff, M., 2015. Top gears: how negative gearing and the capital gains tax discount

benefit the top 10 per cent and drive up house prices.

Ingles, D. and Stewart, M., 2018, October. Australia's company tax: Options for fiscally

sustainable reform. In Australian Tax Forum (Vol. 33, No. 1).

Kenny, P., 2018. Small business capital allowances.

References:

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax Treaties",

IBFD: Amsterdam.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Evans, J.R. and Razeed, A., 2018. An Analysis of Household Retirement Adequacy In

Australia. Available at SSRN 3302331.

Feld, L.P., Ruf, M., Schreiber, U., Todtenhaupt, M. and Voget, J., 2016. Taxing away M&A:

The effect of corporate capital gains taxes on acquisition activity.

Grudnoff, M., 2015. Top gears: how negative gearing and the capital gains tax discount

benefit the top 10 per cent and drive up house prices.

Ingles, D. and Stewart, M., 2018, October. Australia's company tax: Options for fiscally

sustainable reform. In Australian Tax Forum (Vol. 33, No. 1).

Kenny, P., 2018. Small business capital allowances.

11TAXATION LAW

Killaly, J., 2017. A systemic approach to tax policy to best position Australia. Journal of

Australian Taxation, 19(3), p.11.

Mahar, F., Longridge, J. and He, J.L., 2016. The economic impact of a corporate tax rate cut

in Australia. Taxation in Australia, 51(3), p.141.

Paull, C., 2016. Alternative assets insights: Fixed assets-a case for further

inspection. Taxation in Australia, 51(6), p.325.

Pomerleau, K. and Cole, A., 2017. International tax competitiveness index

2015. Washington, DC: Tax Foundation.

Killaly, J., 2017. A systemic approach to tax policy to best position Australia. Journal of

Australian Taxation, 19(3), p.11.

Mahar, F., Longridge, J. and He, J.L., 2016. The economic impact of a corporate tax rate cut

in Australia. Taxation in Australia, 51(3), p.141.

Paull, C., 2016. Alternative assets insights: Fixed assets-a case for further

inspection. Taxation in Australia, 51(6), p.325.

Pomerleau, K. and Cole, A., 2017. International tax competitiveness index

2015. Washington, DC: Tax Foundation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.