Taxation Law of Australia Individual Assignment - Term 2 2019

VerifiedAdded on 2022/09/15

|11

|2952

|38

Homework Assignment

AI Summary

This assignment solution addresses several key areas of Australian taxation law, including the determination of business activity, deductibility of gifts and contributions, and the application of income tax rates. It covers topics such as capital gains tax (CGT) implications, assessable income thresholds, and the taxability of earnings from previous employment. The assignment further explores the distinction between ordinary and statutory income, the calculation of Medicare levies and surcharges, and the residency and domicile tests for individuals. It also delves into the deductibility of various outgoings, including HECS-HELP payments, work-related travel expenses, and the purchase of professional books, while also addressing CGT events, including those related to leased property and share transactions. Finally, the assignment examines the CGT implications of a main residence and the tax treatment of partially used properties.

Running head: TAXATION

Taxation

Name of the Student

Name of the University

Author Note

Taxation

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

1)

a) The TR 2019/11, regulates the determination with respect to the instance at which any business

activity is being effected by a company.

b) the contention of the fact that gifts plus contributions can be given dealt as a deduction is

necessary to be assessed as per principle in div 30, ITAA972.

c) the uppermost rate relating to income tax that needs to be applied for the taxation year 2019-20

would be a sum of $54097 to be paid along with 45% for every dollar beyond $180,0003.

d) Both the vehicles namely a motorcycle or even a car needs to be made eligible to be counted as

an exempt from being exposed to CGT implications in accordance with s 118.5, ITAA974.

e) The article being lost or else demolished, owned priorly by taxpayer would be contemplated as

under C1 category event with respect to CGT in accordance to s 104.20, ITAA 975.

f) Any earnings the taxpayer gets falling under the required threshold amounting to $18200 will

not be comprised in assessable income for tax purposes.

g) The inclusion of the amount received from a former employer in the taxable income has been

provided for within the proceeding of Hayes v FCT (1956) 96 CLR 476. The contention has been provided

for in the proceeding that any reception that might have been availed by employee by the person who

employed him in past in relation to services with respect to employment previously extended would

require a treatment under the concept of CGT gain. This presents a glitch regarding the contention that

every income produced by the employment own exertion are to be included under the cover named

ordinary income. However, this amount even though has arisen from private exertion employed in past

1 TR 2019/1

2 The Income Tax Assessment Act 1997 (Cth), div 30

3 www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

4 The Income Tax Assessment Act 1997 (Cth), s 118.5

5 The Income Tax Assessment Act 1997 (Cth), s 104.20

6 Hayes v FCT (1956) 96 CLR 47

1)

a) The TR 2019/11, regulates the determination with respect to the instance at which any business

activity is being effected by a company.

b) the contention of the fact that gifts plus contributions can be given dealt as a deduction is

necessary to be assessed as per principle in div 30, ITAA972.

c) the uppermost rate relating to income tax that needs to be applied for the taxation year 2019-20

would be a sum of $54097 to be paid along with 45% for every dollar beyond $180,0003.

d) Both the vehicles namely a motorcycle or even a car needs to be made eligible to be counted as

an exempt from being exposed to CGT implications in accordance with s 118.5, ITAA974.

e) The article being lost or else demolished, owned priorly by taxpayer would be contemplated as

under C1 category event with respect to CGT in accordance to s 104.20, ITAA 975.

f) Any earnings the taxpayer gets falling under the required threshold amounting to $18200 will

not be comprised in assessable income for tax purposes.

g) The inclusion of the amount received from a former employer in the taxable income has been

provided for within the proceeding of Hayes v FCT (1956) 96 CLR 476. The contention has been provided

for in the proceeding that any reception that might have been availed by employee by the person who

employed him in past in relation to services with respect to employment previously extended would

require a treatment under the concept of CGT gain. This presents a glitch regarding the contention that

every income produced by the employment own exertion are to be included under the cover named

ordinary income. However, this amount even though has arisen from private exertion employed in past

1 TR 2019/1

2 The Income Tax Assessment Act 1997 (Cth), div 30

3 www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

4 The Income Tax Assessment Act 1997 (Cth), s 118.5

5 The Income Tax Assessment Act 1997 (Cth), s 104.20

6 Hayes v FCT (1956) 96 CLR 47

2TAXATION

the same is to be conceived as taxable as per CGT regime. With respect to rational provided by court in

the present context is the fact that follows. This earning has been devolved at past and was turned to lump

sum quantity, which was received by employee later on. This attaches a capital personality in that asset

leaving it to have the treatment of capital asset. The money needs to be assessed as per CGT

administration. However, the purpose of the employee in being devolved with the cash and the object

pertaining to employer in making available the cash is obligatory to be reflected prior to deciding upon

the same.

g) The taxability of an earning can be held by two mandates. The first one of the mandates

expects the earnings to be included as earnings pertaining to ordinary contemplation dominant with

respect to earnings inference of a normal person and do not need the sanction from any statutory rule for

rendering the earning assessable. Again, the another mandate necessitates the earnings to be declared as

earning only because of the statutory order. Such earnings will not be extended with recognition if

legislation backing up the earning contains no enumeration of the same. Hence, by virtue of these

mandates, it is clear that the earning of an individual needs to be categorized into 2 classes viz. the

earning under ordinary concepts in addition to statutory earnings. Ordinary earnings illustrates a receipt

that gains the status of earning, even in the absence express consideration from the legislation pertaining

to taxation. No authority is required for the purpose of rendering such an amount as an income. This is

owing to the fact that such a reception is measured as an earning denial of statutory concept. In addition,

statutory earnings would imply an earning only if it has been explicitly provided for in the legislation

governing taxation. In the event of the taxation legislation fails to make provision recognizing the same,

such earning would be denied inclusion as a assessable income belonging to the taxpayer. An illustration

of ordinary earning is any earning that the individual gains from applying personal toil along with labour.

However, the most befitting illustration of statutory earning is the CGT earnings7.

7 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

the same is to be conceived as taxable as per CGT regime. With respect to rational provided by court in

the present context is the fact that follows. This earning has been devolved at past and was turned to lump

sum quantity, which was received by employee later on. This attaches a capital personality in that asset

leaving it to have the treatment of capital asset. The money needs to be assessed as per CGT

administration. However, the purpose of the employee in being devolved with the cash and the object

pertaining to employer in making available the cash is obligatory to be reflected prior to deciding upon

the same.

g) The taxability of an earning can be held by two mandates. The first one of the mandates

expects the earnings to be included as earnings pertaining to ordinary contemplation dominant with

respect to earnings inference of a normal person and do not need the sanction from any statutory rule for

rendering the earning assessable. Again, the another mandate necessitates the earnings to be declared as

earning only because of the statutory order. Such earnings will not be extended with recognition if

legislation backing up the earning contains no enumeration of the same. Hence, by virtue of these

mandates, it is clear that the earning of an individual needs to be categorized into 2 classes viz. the

earning under ordinary concepts in addition to statutory earnings. Ordinary earnings illustrates a receipt

that gains the status of earning, even in the absence express consideration from the legislation pertaining

to taxation. No authority is required for the purpose of rendering such an amount as an income. This is

owing to the fact that such a reception is measured as an earning denial of statutory concept. In addition,

statutory earnings would imply an earning only if it has been explicitly provided for in the legislation

governing taxation. In the event of the taxation legislation fails to make provision recognizing the same,

such earning would be denied inclusion as a assessable income belonging to the taxpayer. An illustration

of ordinary earning is any earning that the individual gains from applying personal toil along with labour.

However, the most befitting illustration of statutory earning is the CGT earnings7.

7 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

i) Two supplementary rates to be charged upon the liability of taxation of a being are the

Medicare levy surcharge along with the Medicare levy. These levies requires computation upon liability

of tax of a being already suffered. The Medicare levy has envisioned to extend support in relation to

Medicare operating in Australia guaranteeing the public health system being maintained. Any being

disbursing the revenue would be charged with Medicare levy to the extent of 2percent upon the net

liability of tax of a being. The legal recognition governing this levy are ITAA 368 along with the

Medicare Levy Act 19869. In addition, the other levy of the same kind is the Medicare levy surcharge as

to be levied upon beings fitting within the higher brackets of taxation to contribute in the way for personal

health insurance. This tax is being presented for keeping the load upon Medicare to be diminished. Again,

only beings who by now does not possesses any personal health Insurance will be rendered eligible for

imposition of this levy. This kind of tax requires imposition on the summation of the FBT along with

income tax pertaining to taxpayer. The percentage for this levy could be 1 percent, 1.25 percent and 1.5

percent.

2)

The two assessments to executed upon beings originating from Australia and leaving the territory of

Australia will be the resides test along with the domicile test included within s 6-1, ITAA3610. Two ideas

contained within this provision demands attention. These terminologies are “permanent place of abode”

along with “ usual place of abode”. These two terminologies are generally portrayed as identical yet again

these two has contained a negligible extent of variances remaining among them. The scrutiny of the two

ideas demands the preceding scrutiny of the terminology place of abode. The contented principle evolving

in the proceeding Levene v IRC (1928) AC 217 11, place of abode needs to be inferred as a living location

of the being where the being paying the tax has been residing in a particular instance. Again, the idea of

‘permanent place of abode’ is needed to be recognized in perspective of the situation of FC of T v

8 The Income Tax Assessment Act 1936 (Cth)

9 The Medicare Levy Act 1986

10 The Income Tax Assessment Act 1936 (Cth), s 6.1

11 Levene v IRC (1928) AC 217

i) Two supplementary rates to be charged upon the liability of taxation of a being are the

Medicare levy surcharge along with the Medicare levy. These levies requires computation upon liability

of tax of a being already suffered. The Medicare levy has envisioned to extend support in relation to

Medicare operating in Australia guaranteeing the public health system being maintained. Any being

disbursing the revenue would be charged with Medicare levy to the extent of 2percent upon the net

liability of tax of a being. The legal recognition governing this levy are ITAA 368 along with the

Medicare Levy Act 19869. In addition, the other levy of the same kind is the Medicare levy surcharge as

to be levied upon beings fitting within the higher brackets of taxation to contribute in the way for personal

health insurance. This tax is being presented for keeping the load upon Medicare to be diminished. Again,

only beings who by now does not possesses any personal health Insurance will be rendered eligible for

imposition of this levy. This kind of tax requires imposition on the summation of the FBT along with

income tax pertaining to taxpayer. The percentage for this levy could be 1 percent, 1.25 percent and 1.5

percent.

2)

The two assessments to executed upon beings originating from Australia and leaving the territory of

Australia will be the resides test along with the domicile test included within s 6-1, ITAA3610. Two ideas

contained within this provision demands attention. These terminologies are “permanent place of abode”

along with “ usual place of abode”. These two terminologies are generally portrayed as identical yet again

these two has contained a negligible extent of variances remaining among them. The scrutiny of the two

ideas demands the preceding scrutiny of the terminology place of abode. The contented principle evolving

in the proceeding Levene v IRC (1928) AC 217 11, place of abode needs to be inferred as a living location

of the being where the being paying the tax has been residing in a particular instance. Again, the idea of

‘permanent place of abode’ is needed to be recognized in perspective of the situation of FC of T v

8 The Income Tax Assessment Act 1936 (Cth)

9 The Medicare Levy Act 1986

10 The Income Tax Assessment Act 1936 (Cth), s 6.1

11 Levene v IRC (1928) AC 217

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

Applegate 79 ATC 430712. Under this perspective, the court formulated as rule that all the residence

owned and possessed by a being for unfixed period and not necessarily forever based on the object of the

beign living in it is required to be referred as a ‘permanent place of abode’. However, the legal authority

growing with the proceeding of F.C. of T. v. Jenkins 82 ATC 409813, a dwelling where the being has been

living, which points more towards a customary and habitual dwelling is required to be preserved as a

‘usual place of abode’. Moreover, the accommodations, that are being availed on the basis of rent requires

to be included under this kind.

3)

a) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 14.

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 515,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. The outgoing incurred while paying for HECS-HELP a sum of $850 with respect to student

loan private in essence should not inserted among the deductible outgoings as it has arisen from private

purpose.

b) Outgoings suffered during travelling to workplace requires to be allowed as deduction according to s

25.100, ITAA9716. In the present instance, one hundred and ten dollars has been suffered as an outgoing

during travelling towards workplace from the University, which needs to be regarded as connected with

the earning process. So, needs recognition as deductible outgoings.

c) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 17.

12 FC of T v Applegate 79 ATC 4307

13 F.C. of T. v. Jenkins 82 ATC 4098

14 The Income Tax Assessment Act 1997 (Cth), s 8.1

15 Lunney v Commissioner of Taxation [1958] HCA 5

16 The Income Tax Assessment Act 1997 (Cth), s 25.100

17 The Income Tax Assessment Act 1997 (Cth), s 8.1

Applegate 79 ATC 430712. Under this perspective, the court formulated as rule that all the residence

owned and possessed by a being for unfixed period and not necessarily forever based on the object of the

beign living in it is required to be referred as a ‘permanent place of abode’. However, the legal authority

growing with the proceeding of F.C. of T. v. Jenkins 82 ATC 409813, a dwelling where the being has been

living, which points more towards a customary and habitual dwelling is required to be preserved as a

‘usual place of abode’. Moreover, the accommodations, that are being availed on the basis of rent requires

to be included under this kind.

3)

a) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 14.

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 515,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. The outgoing incurred while paying for HECS-HELP a sum of $850 with respect to student

loan private in essence should not inserted among the deductible outgoings as it has arisen from private

purpose.

b) Outgoings suffered during travelling to workplace requires to be allowed as deduction according to s

25.100, ITAA9716. In the present instance, one hundred and ten dollars has been suffered as an outgoing

during travelling towards workplace from the University, which needs to be regarded as connected with

the earning process. So, needs recognition as deductible outgoings.

c) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 17.

12 FC of T v Applegate 79 ATC 4307

13 F.C. of T. v. Jenkins 82 ATC 4098

14 The Income Tax Assessment Act 1997 (Cth), s 8.1

15 Lunney v Commissioner of Taxation [1958] HCA 5

16 The Income Tax Assessment Act 1997 (Cth), s 25.100

17 The Income Tax Assessment Act 1997 (Cth), s 8.1

5TAXATION

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 518,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. The outgoing of $200 suffered for procuring of books relating to accounting demands to be

extended with treatment as deductible in the form of an outgoing since the books are purchased for

betterment of skills of the individual in accounting connected with the profession. Hence, to be conceived

as deduction.

d) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 19.

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 520,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. Outgoings for care of children summing up to 80 dollars during the person busy with classes

in the evening has no link with profession producing earnings for the taxpayer and needs to be considered

as non-deductible outgoings.

e) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 21.

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 522,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. The sum of $250 as an outgoing to repair the fridge should not be acceptable as deduction to

assessable earning as fridge was kept in the home and is personal in nature.

f) The legal principle inculcated within s 8.1, ITAA9723 do not comprise outgoings in relation to

workplace clothing as deduction. Consequently, amount of cash summing to $145 suffered for getting

shirts along with black trousers would not find place in deductions.

18 Lunney v Commissioner of Taxation [1958] HCA 5

19 The Income Tax Assessment Act 1997 (Cth), s 8.1

20 Lunney v Commissioner of Taxation [1958] HCA 5

21 The Income Tax Assessment Act 1997 (Cth), s 8.1

22 Lunney v Commissioner of Taxation [1958] HCA 5

23 The Income Tax Assessment Act 1997 (Cth), s 8.1

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 518,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. The outgoing of $200 suffered for procuring of books relating to accounting demands to be

extended with treatment as deductible in the form of an outgoing since the books are purchased for

betterment of skills of the individual in accounting connected with the profession. Hence, to be conceived

as deduction.

d) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 19.

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 520,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. Outgoings for care of children summing up to 80 dollars during the person busy with classes

in the evening has no link with profession producing earnings for the taxpayer and needs to be considered

as non-deductible outgoings.

e) The outgoings incidental towards the procedure of grossing earnings, which will be included in the

assessment of revenue would depict towards a deduction of that expense according to s 8.1, ITAA97 21.

But, the principles inculcated with the judgment of Lunney v Commissioner of Taxation [1958] HCA 522,

the link of this outgoing with the home or personal drive would bring to the under the non-deductible

outgoings. The sum of $250 as an outgoing to repair the fridge should not be acceptable as deduction to

assessable earning as fridge was kept in the home and is personal in nature.

f) The legal principle inculcated within s 8.1, ITAA9723 do not comprise outgoings in relation to

workplace clothing as deduction. Consequently, amount of cash summing to $145 suffered for getting

shirts along with black trousers would not find place in deductions.

18 Lunney v Commissioner of Taxation [1958] HCA 5

19 The Income Tax Assessment Act 1997 (Cth), s 8.1

20 Lunney v Commissioner of Taxation [1958] HCA 5

21 The Income Tax Assessment Act 1997 (Cth), s 8.1

22 Lunney v Commissioner of Taxation [1958] HCA 5

23 The Income Tax Assessment Act 1997 (Cth), s 8.1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

g) The outgoings incidental towards route of earning revenue, which would be included a deductible

outgoing as under s 8.1, ITAA 9724. Outgoings with respect to establishment of employment contract

should not be included as deductible earnings as it lays down expected earning of future income and not

associated in relation to accruing of current earning.

4)

a) The capital gain tax event F2 class includes circumstances where person owning the estate rents the on

lease. That lease could be fresh lease or a renewal of the old one along with at items also extra time of a

prevailing one. The discount pertaining to fifty percent requires to be implemented while figuring the

CGT gain. In this case, John is the owner pertaining to the estate and extended the estate by way of lease

towards David upon a rent summing to $7,000. This makes the circumstances to be included within the

Capital Gain event F2 which would be applied with fifty percent discount25.

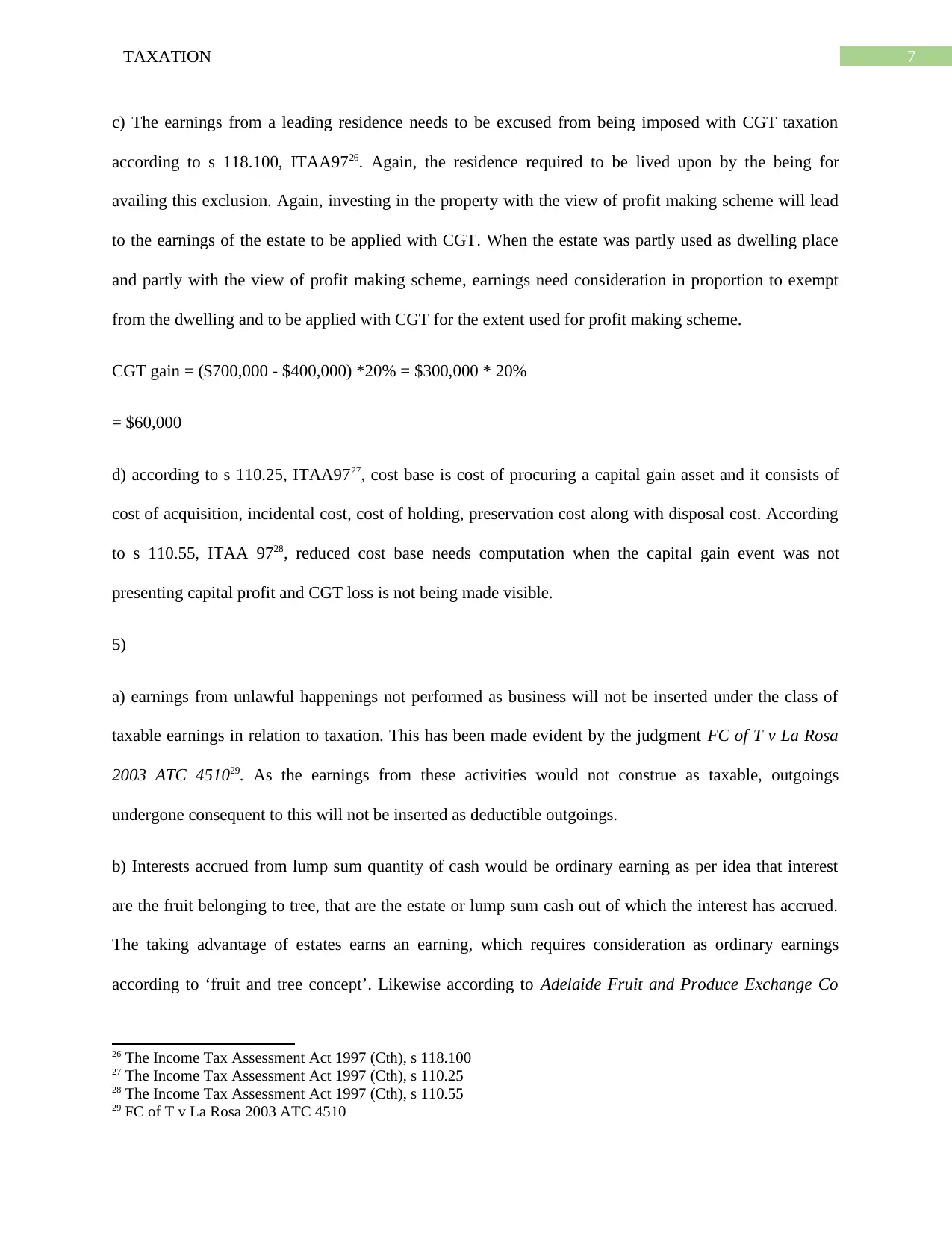

b)

CGT liability

Item $ $

IOOF Shares

CGT gain 1200

CP from shares 6700

CB from shares 5500

Greencross Shares

CGT gain 5880

CP from shares 14160

CB from shares 20040

Capital Loss

4580

24 ibid

25 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016)

g) The outgoings incidental towards route of earning revenue, which would be included a deductible

outgoing as under s 8.1, ITAA 9724. Outgoings with respect to establishment of employment contract

should not be included as deductible earnings as it lays down expected earning of future income and not

associated in relation to accruing of current earning.

4)

a) The capital gain tax event F2 class includes circumstances where person owning the estate rents the on

lease. That lease could be fresh lease or a renewal of the old one along with at items also extra time of a

prevailing one. The discount pertaining to fifty percent requires to be implemented while figuring the

CGT gain. In this case, John is the owner pertaining to the estate and extended the estate by way of lease

towards David upon a rent summing to $7,000. This makes the circumstances to be included within the

Capital Gain event F2 which would be applied with fifty percent discount25.

b)

CGT liability

Item $ $

IOOF Shares

CGT gain 1200

CP from shares 6700

CB from shares 5500

Greencross Shares

CGT gain 5880

CP from shares 14160

CB from shares 20040

Capital Loss

4580

24 ibid

25 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

c) The earnings from a leading residence needs to be excused from being imposed with CGT taxation

according to s 118.100, ITAA9726. Again, the residence required to be lived upon by the being for

availing this exclusion. Again, investing in the property with the view of profit making scheme will lead

to the earnings of the estate to be applied with CGT. When the estate was partly used as dwelling place

and partly with the view of profit making scheme, earnings need consideration in proportion to exempt

from the dwelling and to be applied with CGT for the extent used for profit making scheme.

CGT gain = ($700,000 - $400,000) *20% = $300,000 * 20%

= $60,000

d) according to s 110.25, ITAA9727, cost base is cost of procuring a capital gain asset and it consists of

cost of acquisition, incidental cost, cost of holding, preservation cost along with disposal cost. According

to s 110.55, ITAA 9728, reduced cost base needs computation when the capital gain event was not

presenting capital profit and CGT loss is not being made visible.

5)

a) earnings from unlawful happenings not performed as business will not be inserted under the class of

taxable earnings in relation to taxation. This has been made evident by the judgment FC of T v La Rosa

2003 ATC 451029. As the earnings from these activities would not construe as taxable, outgoings

undergone consequent to this will not be inserted as deductible outgoings.

b) Interests accrued from lump sum quantity of cash would be ordinary earning as per idea that interest

are the fruit belonging to tree, that are the estate or lump sum cash out of which the interest has accrued.

The taking advantage of estates earns an earning, which requires consideration as ordinary earnings

according to ‘fruit and tree concept’. Likewise according to Adelaide Fruit and Produce Exchange Co

26 The Income Tax Assessment Act 1997 (Cth), s 118.100

27 The Income Tax Assessment Act 1997 (Cth), s 110.25

28 The Income Tax Assessment Act 1997 (Cth), s 110.55

29 FC of T v La Rosa 2003 ATC 4510

c) The earnings from a leading residence needs to be excused from being imposed with CGT taxation

according to s 118.100, ITAA9726. Again, the residence required to be lived upon by the being for

availing this exclusion. Again, investing in the property with the view of profit making scheme will lead

to the earnings of the estate to be applied with CGT. When the estate was partly used as dwelling place

and partly with the view of profit making scheme, earnings need consideration in proportion to exempt

from the dwelling and to be applied with CGT for the extent used for profit making scheme.

CGT gain = ($700,000 - $400,000) *20% = $300,000 * 20%

= $60,000

d) according to s 110.25, ITAA9727, cost base is cost of procuring a capital gain asset and it consists of

cost of acquisition, incidental cost, cost of holding, preservation cost along with disposal cost. According

to s 110.55, ITAA 9728, reduced cost base needs computation when the capital gain event was not

presenting capital profit and CGT loss is not being made visible.

5)

a) earnings from unlawful happenings not performed as business will not be inserted under the class of

taxable earnings in relation to taxation. This has been made evident by the judgment FC of T v La Rosa

2003 ATC 451029. As the earnings from these activities would not construe as taxable, outgoings

undergone consequent to this will not be inserted as deductible outgoings.

b) Interests accrued from lump sum quantity of cash would be ordinary earning as per idea that interest

are the fruit belonging to tree, that are the estate or lump sum cash out of which the interest has accrued.

The taking advantage of estates earns an earning, which requires consideration as ordinary earnings

according to ‘fruit and tree concept’. Likewise according to Adelaide Fruit and Produce Exchange Co

26 The Income Tax Assessment Act 1997 (Cth), s 118.100

27 The Income Tax Assessment Act 1997 (Cth), s 110.25

28 The Income Tax Assessment Act 1997 (Cth), s 110.55

29 FC of T v La Rosa 2003 ATC 4510

8TAXATION

Ltd v DFC of T (1932) 2 ATD 130, any earning accruing from gambling along with windfall games need

not be included among the taxable earnings of a being if has been performed for main aim of amusement.

However, this needs be inclusion in the taxable earnings of a being when carried out in a way of business

as pointed out in Evans v. F.C. of T. 89 ATC 454031. In present instance, earning of $500 received from

bank as interest would demarcate ordinary earning u/s 6-5, ITAA 3632, the gain from crown casino would

be excluded from assessable earnings as it demarcates hobby but the house rent is assessable earnings as

availed from exploitation of estates.

Net Assessable Income = $500 + $2000 = $ 2500.

c) Allowance extended towards an employee in consequence to the employment facilities rendered

extended from employer will be exposed to tax according to s 15.2, ITAA 9733. In this instance, the sum

received by way of allowance grossing up to $500 needs inclusion within the taxable earnings of the

individual paying the tax.

d) taxable Income: $20,000

tax Rate: not applicable for failure to cross optimum threshold

Medicare Levy Payable: 0

Taxable Income: $24900

Tax Rate: 2%

Medicare Levy Payable: $498

Taxable Income: $100000

Tax Rate: 2%

30 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

31 Evans v. F.C. of T. 89 ATC 4540

32 The Income Tax Assessment Act 1936 (Cth), s 6.5

33 The Income Tax Assessment Act 1997 (Cth), s 15.2

Ltd v DFC of T (1932) 2 ATD 130, any earning accruing from gambling along with windfall games need

not be included among the taxable earnings of a being if has been performed for main aim of amusement.

However, this needs be inclusion in the taxable earnings of a being when carried out in a way of business

as pointed out in Evans v. F.C. of T. 89 ATC 454031. In present instance, earning of $500 received from

bank as interest would demarcate ordinary earning u/s 6-5, ITAA 3632, the gain from crown casino would

be excluded from assessable earnings as it demarcates hobby but the house rent is assessable earnings as

availed from exploitation of estates.

Net Assessable Income = $500 + $2000 = $ 2500.

c) Allowance extended towards an employee in consequence to the employment facilities rendered

extended from employer will be exposed to tax according to s 15.2, ITAA 9733. In this instance, the sum

received by way of allowance grossing up to $500 needs inclusion within the taxable earnings of the

individual paying the tax.

d) taxable Income: $20,000

tax Rate: not applicable for failure to cross optimum threshold

Medicare Levy Payable: 0

Taxable Income: $24900

Tax Rate: 2%

Medicare Levy Payable: $498

Taxable Income: $100000

Tax Rate: 2%

30 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

31 Evans v. F.C. of T. 89 ATC 4540

32 The Income Tax Assessment Act 1936 (Cth), s 6.5

33 The Income Tax Assessment Act 1997 (Cth), s 15.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

Medicare Levy Payable: $2000

e) earnings: $25,000

Tax Rate: 19% on cash over $18,200

Tax Payable: $(25000 – 18200) of 19% = $6800 of 19% = $1292

Earnings: $40,000

Tax Rate: 3,572 + 32.5% on cash over $37,000

Tax Payable: $3572 + 32.5% of (40000-37000) = $3572 of 32.5% of 3000 = $(3572 + 975) = $4547

Earnings: $95,000

Tax Rate: 3,572 + 20,797 + 37% on cash over $90,000

Tax Payable: $20,797 + 37% of (95,000-90,000) = $20,797 of 37% of 5000 = $(20,797 +1850) = $22647

Medicare Levy Payable: $2000

e) earnings: $25,000

Tax Rate: 19% on cash over $18,200

Tax Payable: $(25000 – 18200) of 19% = $6800 of 19% = $1292

Earnings: $40,000

Tax Rate: 3,572 + 32.5% on cash over $37,000

Tax Payable: $3572 + 32.5% of (40000-37000) = $3572 of 32.5% of 3000 = $(3572 + 975) = $4547

Earnings: $95,000

Tax Rate: 3,572 + 20,797 + 37% on cash over $90,000

Tax Payable: $20,797 + 37% of (95,000-90,000) = $20,797 of 37% of 5000 = $(20,797 +1850) = $22647

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

Bibliography

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

Evans v. F.C. of T. 89 ATC 4540

F.C. of T. v. Jenkins 82 ATC 4098

FC of T v Applegate 79 ATC 4307

FC of T v La Rosa 2003 ATC 4510

Hayes v FCT (1956) 96 CLR 47

Levene v IRC (1928) AC 217

Lunney v Commissioner of Taxation [1958] HCA 5

The Income Tax Assessment Act 1936 (Cth)

The Income Tax Assessment Act 1997 (Cth)

The Medicare Levy Act 1986

TR 2019/1

www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

https://www.ato.gov.au/Rates/Individual-income-tax-rates/

Bibliography

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

Evans v. F.C. of T. 89 ATC 4540

F.C. of T. v. Jenkins 82 ATC 4098

FC of T v Applegate 79 ATC 4307

FC of T v La Rosa 2003 ATC 4510

Hayes v FCT (1956) 96 CLR 47

Levene v IRC (1928) AC 217

Lunney v Commissioner of Taxation [1958] HCA 5

The Income Tax Assessment Act 1936 (Cth)

The Income Tax Assessment Act 1997 (Cth)

The Medicare Levy Act 1986

TR 2019/1

www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

https://www.ato.gov.au/Rates/Individual-income-tax-rates/

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.