HI6028 Taxation Theory, Practice & Law Individual Assignment

VerifiedAdded on 2023/03/31

|12

|2415

|398

Homework Assignment

AI Summary

This assignment solution for HI6028 Taxation Theory, Practice & Law addresses key concepts in Australian taxation law. The first question focuses on capital gains tax (CGT), analyzing four different transactions involving the sale of assets like an antique painting, historical sculpture, antique jewelry, and a picture, calculating gains or losses using the indexation method. The second question examines assessable income, exploring Barbara's income from book sales, manuscript sales, and interview manuscripts under different scenarios, referencing relevant case law such as "Brent v FCT". The third question delves into the effect of a financial arrangement between David and his father on David's assessable income, considering the implications of borrowing and repaying funds with interest. The solution provides detailed calculations, legal references, and thorough analysis of the tax implications for each scenario, offering a comprehensive understanding of taxation principles and their application to real-life situations.

1

Taxation Theory, Practice

& Law

Taxation Theory, Practice

& Law

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Table of Contents

Introduction........................................................................................................................................3

Question 1..........................................................................................................................................3

Capital Gain Tax regarding antique impressionism painting................................................4

Capital Gain Tax regarding historical sculpture.......................................................................4

Capital Gain Tax regarding antique jewellery piece.................................................................5

Capital Gain Tax regarding picture..............................................................................................6

Question 2..........................................................................................................................................7

A.) Using case, discuss Barbara’s income.................................................................................7

B.) Using substitute situation, discuss Barbara’s income.....................................................8

Question 3..........................................................................................................................................8

Discuss the effect of these arrangements on the assessable income of Patrick.............8

Conclusion.........................................................................................................................................9

References.......................................................................................................................................10

Table of Contents

Introduction........................................................................................................................................3

Question 1..........................................................................................................................................3

Capital Gain Tax regarding antique impressionism painting................................................4

Capital Gain Tax regarding historical sculpture.......................................................................4

Capital Gain Tax regarding antique jewellery piece.................................................................5

Capital Gain Tax regarding picture..............................................................................................6

Question 2..........................................................................................................................................7

A.) Using case, discuss Barbara’s income.................................................................................7

B.) Using substitute situation, discuss Barbara’s income.....................................................8

Question 3..........................................................................................................................................8

Discuss the effect of these arrangements on the assessable income of Patrick.............8

Conclusion.........................................................................................................................................9

References.......................................................................................................................................10

3

Introduction

This report is categorized into three parts and all these parts include the case laws.

First question includes that Helen need to generate funds by selling their resources

and for that deal with the four transactions. Second section of this report

demonstrate the income generated by Barbara under the different case. Apart from

this, last section of this report describes the influence of arrangements on the taxable

income of Patrick.

Question 1

Capital gains/ losses are categorized as a long and short term in nature. If the

individual holds asset for more than one year or higher which would be the long-term

capital gain or loss. But on the other side, if individual hold product for one year or

less, then capital gain or loss is of short-term nature (Paolella and Durand, 2016).

In the given question, during 2018, Helen made four different transactions for

generating the funds. If any individual incurred loss then this loss needs to be set-off

in same year against the income and if the whole loss will not set off, then it needs to

carry forward for the next assessment year. But on the other side, loss will be carry

forward only when it is properly disclosed in the Income Tax return and it is filled

before the due date (Devereux and de la Feria, 2014).

According to ATO, it has been examined that if any individual conducts the events

for the capital gain, then it should be including in the tax return but in this event, only

those transactions should include who are acquired before 21st September 1999

because it is claimed to attain the maximum revenue for more than a year. For the

purchases of before 1999, indexation method needs to be used as this method

assist in making the variations by evaluating the Price Index which aid in managing

the purchasing power of an individual. This method assists in identifying the real

Introduction

This report is categorized into three parts and all these parts include the case laws.

First question includes that Helen need to generate funds by selling their resources

and for that deal with the four transactions. Second section of this report

demonstrate the income generated by Barbara under the different case. Apart from

this, last section of this report describes the influence of arrangements on the taxable

income of Patrick.

Question 1

Capital gains/ losses are categorized as a long and short term in nature. If the

individual holds asset for more than one year or higher which would be the long-term

capital gain or loss. But on the other side, if individual hold product for one year or

less, then capital gain or loss is of short-term nature (Paolella and Durand, 2016).

In the given question, during 2018, Helen made four different transactions for

generating the funds. If any individual incurred loss then this loss needs to be set-off

in same year against the income and if the whole loss will not set off, then it needs to

carry forward for the next assessment year. But on the other side, loss will be carry

forward only when it is properly disclosed in the Income Tax return and it is filled

before the due date (Devereux and de la Feria, 2014).

According to ATO, it has been examined that if any individual conducts the events

for the capital gain, then it should be including in the tax return but in this event, only

those transactions should include who are acquired before 21st September 1999

because it is claimed to attain the maximum revenue for more than a year. For the

purchases of before 1999, indexation method needs to be used as this method

assist in making the variations by evaluating the Price Index which aid in managing

the purchasing power of an individual. This method assists in identifying the real

4

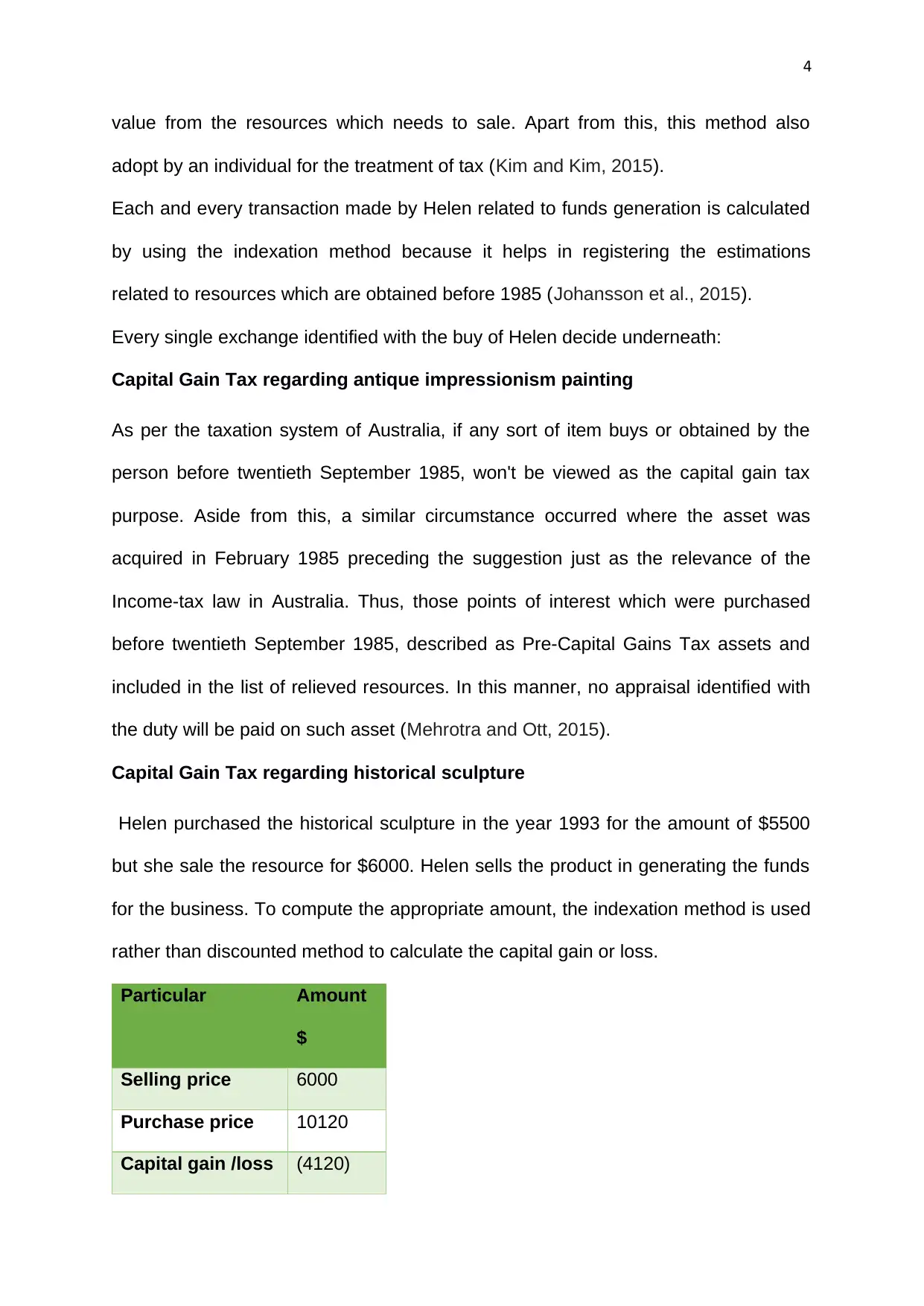

value from the resources which needs to sale. Apart from this, this method also

adopt by an individual for the treatment of tax (Kim and Kim, 2015).

Each and every transaction made by Helen related to funds generation is calculated

by using the indexation method because it helps in registering the estimations

related to resources which are obtained before 1985 (Johansson et al., 2015).

Every single exchange identified with the buy of Helen decide underneath:

Capital Gain Tax regarding antique impressionism painting

As per the taxation system of Australia, if any sort of item buys or obtained by the

person before twentieth September 1985, won't be viewed as the capital gain tax

purpose. Aside from this, a similar circumstance occurred where the asset was

acquired in February 1985 preceding the suggestion just as the relevance of the

Income-tax law in Australia. Thus, those points of interest which were purchased

before twentieth September 1985, described as Pre-Capital Gains Tax assets and

included in the list of relieved resources. In this manner, no appraisal identified with

the duty will be paid on such asset (Mehrotra and Ott, 2015).

Capital Gain Tax regarding historical sculpture

Helen purchased the historical sculpture in the year 1993 for the amount of $5500

but she sale the resource for $6000. Helen sells the product in generating the funds

for the business. To compute the appropriate amount, the indexation method is used

rather than discounted method to calculate the capital gain or loss.

Particular Amount

$

Selling price 6000

Purchase price 10120

Capital gain /loss (4120)

value from the resources which needs to sale. Apart from this, this method also

adopt by an individual for the treatment of tax (Kim and Kim, 2015).

Each and every transaction made by Helen related to funds generation is calculated

by using the indexation method because it helps in registering the estimations

related to resources which are obtained before 1985 (Johansson et al., 2015).

Every single exchange identified with the buy of Helen decide underneath:

Capital Gain Tax regarding antique impressionism painting

As per the taxation system of Australia, if any sort of item buys or obtained by the

person before twentieth September 1985, won't be viewed as the capital gain tax

purpose. Aside from this, a similar circumstance occurred where the asset was

acquired in February 1985 preceding the suggestion just as the relevance of the

Income-tax law in Australia. Thus, those points of interest which were purchased

before twentieth September 1985, described as Pre-Capital Gains Tax assets and

included in the list of relieved resources. In this manner, no appraisal identified with

the duty will be paid on such asset (Mehrotra and Ott, 2015).

Capital Gain Tax regarding historical sculpture

Helen purchased the historical sculpture in the year 1993 for the amount of $5500

but she sale the resource for $6000. Helen sells the product in generating the funds

for the business. To compute the appropriate amount, the indexation method is used

rather than discounted method to calculate the capital gain or loss.

Particular Amount

$

Selling price 6000

Purchase price 10120

Capital gain /loss (4120)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

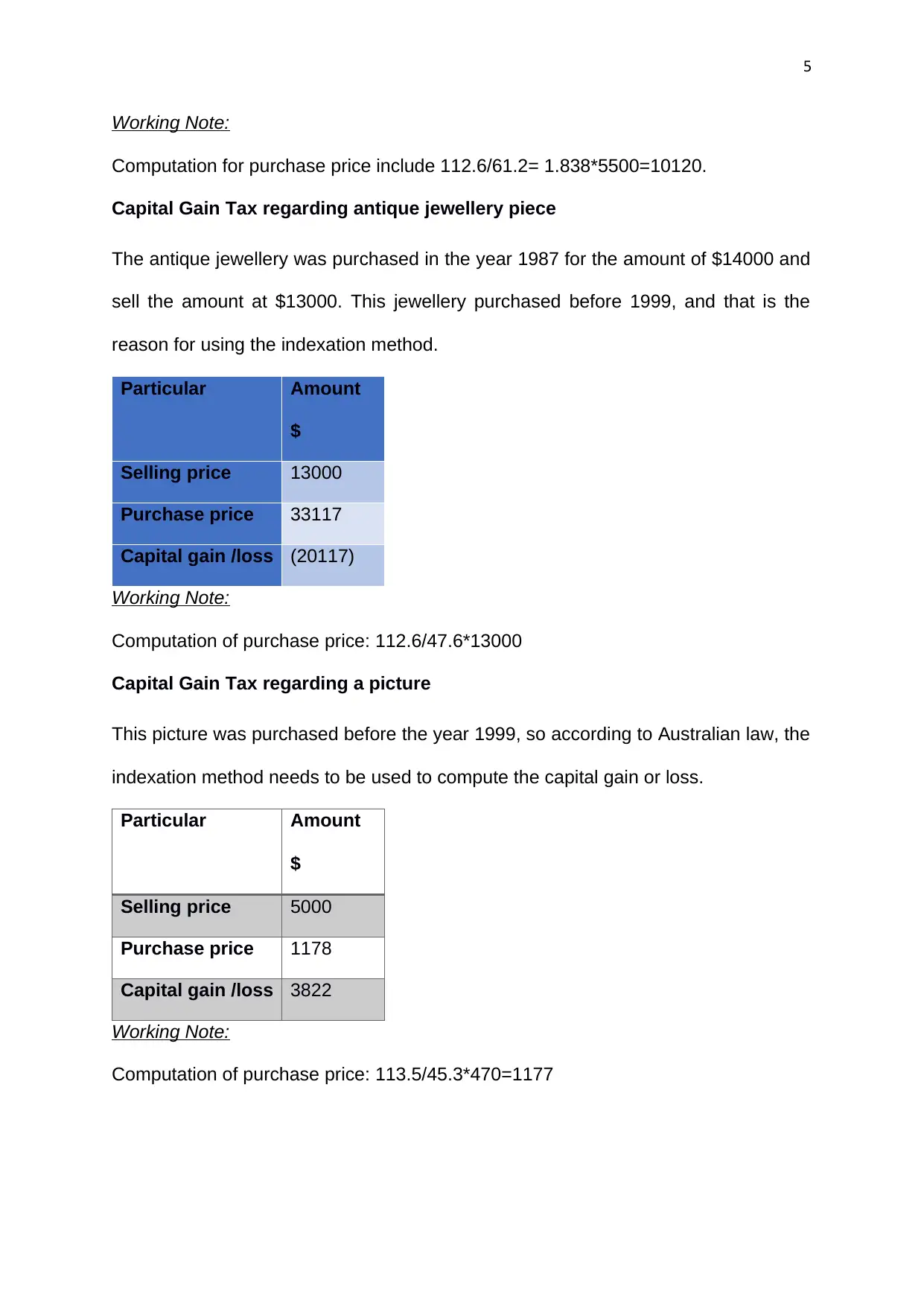

Working Note:

Computation for purchase price include 112.6/61.2= 1.838*5500=10120.

Capital Gain Tax regarding antique jewellery piece

The antique jewellery was purchased in the year 1987 for the amount of $14000 and

sell the amount at $13000. This jewellery purchased before 1999, and that is the

reason for using the indexation method.

Particular Amount

$

Selling price 13000

Purchase price 33117

Capital gain /loss (20117)

Working Note:

Computation of purchase price: 112.6/47.6*13000

Capital Gain Tax regarding a picture

This picture was purchased before the year 1999, so according to Australian law, the

indexation method needs to be used to compute the capital gain or loss.

Particular Amount

$

Selling price 5000

Purchase price 1178

Capital gain /loss 3822

Working Note:

Computation of purchase price: 113.5/45.3*470=1177

Working Note:

Computation for purchase price include 112.6/61.2= 1.838*5500=10120.

Capital Gain Tax regarding antique jewellery piece

The antique jewellery was purchased in the year 1987 for the amount of $14000 and

sell the amount at $13000. This jewellery purchased before 1999, and that is the

reason for using the indexation method.

Particular Amount

$

Selling price 13000

Purchase price 33117

Capital gain /loss (20117)

Working Note:

Computation of purchase price: 112.6/47.6*13000

Capital Gain Tax regarding a picture

This picture was purchased before the year 1999, so according to Australian law, the

indexation method needs to be used to compute the capital gain or loss.

Particular Amount

$

Selling price 5000

Purchase price 1178

Capital gain /loss 3822

Working Note:

Computation of purchase price: 113.5/45.3*470=1177

6

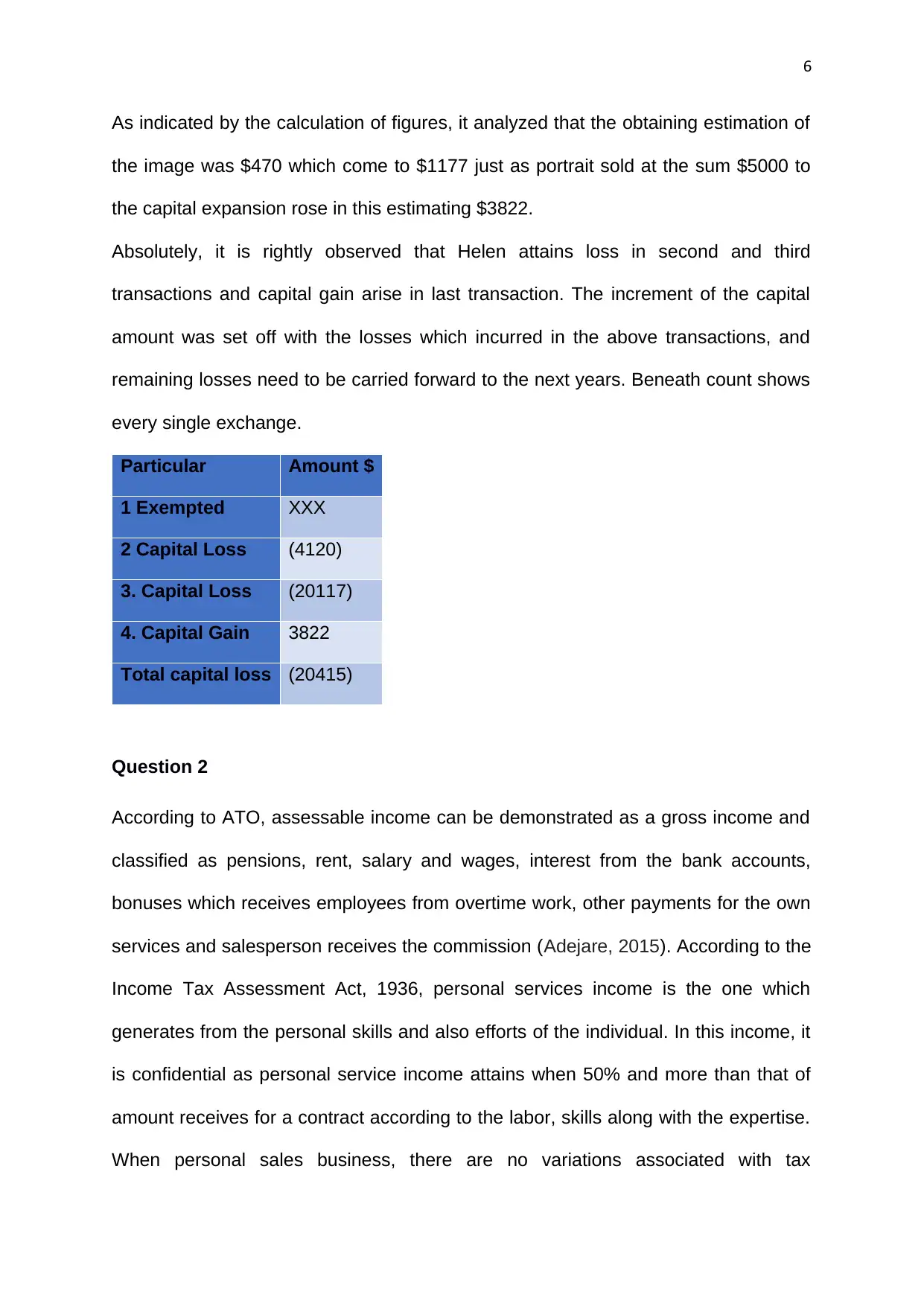

As indicated by the calculation of figures, it analyzed that the obtaining estimation of

the image was $470 which come to $1177 just as portrait sold at the sum $5000 to

the capital expansion rose in this estimating $3822.

Absolutely, it is rightly observed that Helen attains loss in second and third

transactions and capital gain arise in last transaction. The increment of the capital

amount was set off with the losses which incurred in the above transactions, and

remaining losses need to be carried forward to the next years. Beneath count shows

every single exchange.

Particular Amount $

1 Exempted XXX

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20415)

Question 2

According to ATO, assessable income can be demonstrated as a gross income and

classified as pensions, rent, salary and wages, interest from the bank accounts,

bonuses which receives employees from overtime work, other payments for the own

services and salesperson receives the commission (Adejare, 2015). According to the

Income Tax Assessment Act, 1936, personal services income is the one which

generates from the personal skills and also efforts of the individual. In this income, it

is confidential as personal service income attains when 50% and more than that of

amount receives for a contract according to the labor, skills along with the expertise.

When personal sales business, there are no variations associated with tax

As indicated by the calculation of figures, it analyzed that the obtaining estimation of

the image was $470 which come to $1177 just as portrait sold at the sum $5000 to

the capital expansion rose in this estimating $3822.

Absolutely, it is rightly observed that Helen attains loss in second and third

transactions and capital gain arise in last transaction. The increment of the capital

amount was set off with the losses which incurred in the above transactions, and

remaining losses need to be carried forward to the next years. Beneath count shows

every single exchange.

Particular Amount $

1 Exempted XXX

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20415)

Question 2

According to ATO, assessable income can be demonstrated as a gross income and

classified as pensions, rent, salary and wages, interest from the bank accounts,

bonuses which receives employees from overtime work, other payments for the own

services and salesperson receives the commission (Adejare, 2015). According to the

Income Tax Assessment Act, 1936, personal services income is the one which

generates from the personal skills and also efforts of the individual. In this income, it

is confidential as personal service income attains when 50% and more than that of

amount receives for a contract according to the labor, skills along with the expertise.

When personal sales business, there are no variations associated with tax

7

obligations, and it needs to declare the personal service income on the tax return

(Australian Government, 2017).

According to Australian Taxation Authority, the individual can reform the tax code

which provide the permission for a limited of income splitting between the spouses

with a maximum tax benefit of $2000 (Mccallum, 2018). According to Income Tax

Assessment Act, 1936, Australian Taxation Office issues the diversified decisions

which requires the extra efforts as it aid in creating the certainty for taxpayers. This

can be categorized as a labor intensive and according to this practice become

worse. The main reason of this is income splitting among the contractors instead of

employees (Braithwaite, 2017).

A.) Using case, discuss Barbara’s income

According to the given case, Barbara earned the revenue in three different ways that

are by selling the book, selling the copies of books and by selling the manuscripts of

interviews. Barbara wrote economics book for the very first time named as

“Principles of Economics” and for writing this book she made the contract with Eco

Books Ltd. and company give the copyright to her for writing this book. For this

copyright, she received $13400 because of utilizing the skills and implement

effective efforts (Wagner, 2014). This given situation is proved with the case of

“Brent v FCT (1971) 125 CLR 418” as in the given case the book named “Husband

story of life” as in this she got the copyright for this book as this to describe the story

of her husband's life and she wrote by using personal skills and on the basis of that

she generates the income. In comparison to this case, Barbara got the 13400$

because of selling the books, but it is not included in the capital gain. This received

amount was assessable or taxable, and the reason for this is attaining the outcomes

because of potentialities and skills (Howard et al., 2014).

obligations, and it needs to declare the personal service income on the tax return

(Australian Government, 2017).

According to Australian Taxation Authority, the individual can reform the tax code

which provide the permission for a limited of income splitting between the spouses

with a maximum tax benefit of $2000 (Mccallum, 2018). According to Income Tax

Assessment Act, 1936, Australian Taxation Office issues the diversified decisions

which requires the extra efforts as it aid in creating the certainty for taxpayers. This

can be categorized as a labor intensive and according to this practice become

worse. The main reason of this is income splitting among the contractors instead of

employees (Braithwaite, 2017).

A.) Using case, discuss Barbara’s income

According to the given case, Barbara earned the revenue in three different ways that

are by selling the book, selling the copies of books and by selling the manuscripts of

interviews. Barbara wrote economics book for the very first time named as

“Principles of Economics” and for writing this book she made the contract with Eco

Books Ltd. and company give the copyright to her for writing this book. For this

copyright, she received $13400 because of utilizing the skills and implement

effective efforts (Wagner, 2014). This given situation is proved with the case of

“Brent v FCT (1971) 125 CLR 418” as in the given case the book named “Husband

story of life” as in this she got the copyright for this book as this to describe the story

of her husband's life and she wrote by using personal skills and on the basis of that

she generates the income. In comparison to this case, Barbara got the 13400$

because of selling the books, but it is not included in the capital gain. This received

amount was assessable or taxable, and the reason for this is attaining the outcomes

because of potentialities and skills (Howard et al., 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Another income generates by Barbara by selling the manuscript of books to the Eco

Books Ltd., and for this, she received $4350. This is also received according to her

personal exertion, but this income can be assessable and not described as a capital

gain.

Apart from this, she also gains the $3200 for delivering the diversified interview

manuscripts which she received while writing the economics book. For writing this

book, she uses so many skills and extra efforts as well because she wrote an

economics book for the very first time. Hence, it might be portrayed as the correct

pay related to singular undertakings.

B.) Using substitute situation, discuss Barbara’s income

According to the given situation, Barbara signed the formal agreement with the Eco

Books Ltd. But on the other side, another situation occurs that if she does not make

any type of formal agreement with the book company, then is it possible that she can

generate more revenue. If Barbara does not sign any type of formal agreement and

she completed the writing of the book “Economic Principles” and after completing the

book, she sells the books to Eco Books Ltd. In this situation also Barbara can get the

payment according to their utilization of skills and also put the extra efforts in writing

the book (Basu, 2016). This situation also examines with the case of “Brent v FCT

(1971) 125 CLR 418" because in this case, women describe the husband life story to

the agency who print the newspaper that how her husband uses their skills and

made the efforts. Whereas in the given situation, there is no demand for signing the

contract, whether it is formal and informal, she earns the maximum revenue by

putting the hard work she wrote the book economic principles (Filatova, 2014).

Another income generates by Barbara by selling the manuscript of books to the Eco

Books Ltd., and for this, she received $4350. This is also received according to her

personal exertion, but this income can be assessable and not described as a capital

gain.

Apart from this, she also gains the $3200 for delivering the diversified interview

manuscripts which she received while writing the economics book. For writing this

book, she uses so many skills and extra efforts as well because she wrote an

economics book for the very first time. Hence, it might be portrayed as the correct

pay related to singular undertakings.

B.) Using substitute situation, discuss Barbara’s income

According to the given situation, Barbara signed the formal agreement with the Eco

Books Ltd. But on the other side, another situation occurs that if she does not make

any type of formal agreement with the book company, then is it possible that she can

generate more revenue. If Barbara does not sign any type of formal agreement and

she completed the writing of the book “Economic Principles” and after completing the

book, she sells the books to Eco Books Ltd. In this situation also Barbara can get the

payment according to their utilization of skills and also put the extra efforts in writing

the book (Basu, 2016). This situation also examines with the case of “Brent v FCT

(1971) 125 CLR 418" because in this case, women describe the husband life story to

the agency who print the newspaper that how her husband uses their skills and

made the efforts. Whereas in the given situation, there is no demand for signing the

contract, whether it is formal and informal, she earns the maximum revenue by

putting the hard work she wrote the book economic principles (Filatova, 2014).

9

Question 3

Discuss the effect of this arrangement on the assessable income of Patrick

According to the case scenario, it has been examined that David needs to repay the

full amount, which was borrowed by his father after completing two years. If the

borrowed amount has utilized by individuals for the personal organization, then it

needs to be included in taxable income. But in the given situation, David has taken

the amount for her own business from his father and this description as an ordinary

income. In the Australian Taxation Law, assessable income describes as an income

which can be taxed and also offered the earnings which assist in enhancing the tax-

free threshold (Lang et al., 2018).

The assessable income is the ordinary income, and it does not include the GST as

well as include some other expectations which earned from the different activities

related to the business. This demonstrates the appropriate accounting method which

impact the amount included in the income year according to the variations in law

associated with tax rates for the not-for-profit business organization.

According to Australian Taxation Law, an individual need to pay the interest on the

received amount, and all the information should be written in contract so that

business can run effectively. But in case, there is no contract made between David

as well as Patrick, but still, David needs to repay the amount in two years with the

interest of 5% after finishing five years (Thuronyi and Brooks, 2016).

Apart from this, as per the law’s clients can make the contract by deciding their own

liabilities along with the risk as it helps in generating and maximizing more money.

But according to the given information in the case, it can be examined that David

needs to return the money to his father by managing the liabilities along with the risk

but for the two years, no need to pay the interest amount. But after years, David

Question 3

Discuss the effect of this arrangement on the assessable income of Patrick

According to the case scenario, it has been examined that David needs to repay the

full amount, which was borrowed by his father after completing two years. If the

borrowed amount has utilized by individuals for the personal organization, then it

needs to be included in taxable income. But in the given situation, David has taken

the amount for her own business from his father and this description as an ordinary

income. In the Australian Taxation Law, assessable income describes as an income

which can be taxed and also offered the earnings which assist in enhancing the tax-

free threshold (Lang et al., 2018).

The assessable income is the ordinary income, and it does not include the GST as

well as include some other expectations which earned from the different activities

related to the business. This demonstrates the appropriate accounting method which

impact the amount included in the income year according to the variations in law

associated with tax rates for the not-for-profit business organization.

According to Australian Taxation Law, an individual need to pay the interest on the

received amount, and all the information should be written in contract so that

business can run effectively. But in case, there is no contract made between David

as well as Patrick, but still, David needs to repay the amount in two years with the

interest of 5% after finishing five years (Thuronyi and Brooks, 2016).

Apart from this, as per the law’s clients can make the contract by deciding their own

liabilities along with the risk as it helps in generating and maximizing more money.

But according to the given information in the case, it can be examined that David

needs to return the money to his father by managing the liabilities along with the risk

but for the two years, no need to pay the interest amount. But after years, David

10

should pay the additional 5% amount of $52000 to Patrick, and this generation of

income can be shown to statements as a taxable income (Burman et al., 2016).

Conclusion

It has been summarized from the above report demonstrate the different provisions

given by ATO related to capital gain. This report is classified into different sections,

and the first section describes that Helen wants to increase the funds for the

business, and for that Helen sold the different products, but she attains the loss by

selling their resources. Another section of this report describes the situation of

Barbara, who wrote the first book of Economic Principles and generate the profit by

using their own skills. The last section demonstrates the impact of taxable income of

Patrick.

should pay the additional 5% amount of $52000 to Patrick, and this generation of

income can be shown to statements as a taxable income (Burman et al., 2016).

Conclusion

It has been summarized from the above report demonstrate the different provisions

given by ATO related to capital gain. This report is classified into different sections,

and the first section describes that Helen wants to increase the funds for the

business, and for that Helen sold the different products, but she attains the loss by

selling their resources. Another section of this report describes the situation of

Barbara, who wrote the first book of Economic Principles and generate the profit by

using their own skills. The last section demonstrates the impact of taxable income of

Patrick.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

References

Adejare, A. T. (2015) The analysis of the effect of corporate income tax (CIT) on

revenue profile in Nigeria, American Journal of Economics, Finance and

Management, 1(4), pp. 312-319.

Basu, S. (2016) Global perspectives on e-commerce taxation law. UK: Routledge.

Braithwaite, V. (2017) Taxing democracy: Understanding tax avoidance and evasion.

UK: Routledge.

Burman, L. E., Gale, W. G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S. (2016)

Financial transaction taxes in theory and practice, National Tax Journal, 69(1), pp.

171.

Devereux, M. and de la Feria, R. (2014) Designing and implementing a destination-

based corporate tax.

Filatova, T. (2014) Market-based instruments for flood risk management: a review of

theory, practice and perspectives for climate adaptation policy, Environmental

science & policy, 37, pp. 227-242.

Howard, S. J., Gordon, R. and Jones, S. C. (2014) Australian alcohol policy 2001–

2013 and implications for public health, BMC Public Health, 14(1), pp. 848.

Johansson, D., Stenkula, M. and Du Rietz, G. (2015) Capital income taxation of

Swedish households, 1862–2010, Scandinavian Economic History Review, 63(2),

pp. 154-177.

Kim, N. N. and Kim, J. (2015) Top incomes in Korea, 1933-2010: Evidence from

income tax statistics, Hitotsubashi Journal of Economics, pp. 1-19.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. (Eds.). (2018) Introduction to

European tax law on direct taxation. Linde Verlag GmbH.

References

Adejare, A. T. (2015) The analysis of the effect of corporate income tax (CIT) on

revenue profile in Nigeria, American Journal of Economics, Finance and

Management, 1(4), pp. 312-319.

Basu, S. (2016) Global perspectives on e-commerce taxation law. UK: Routledge.

Braithwaite, V. (2017) Taxing democracy: Understanding tax avoidance and evasion.

UK: Routledge.

Burman, L. E., Gale, W. G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S. (2016)

Financial transaction taxes in theory and practice, National Tax Journal, 69(1), pp.

171.

Devereux, M. and de la Feria, R. (2014) Designing and implementing a destination-

based corporate tax.

Filatova, T. (2014) Market-based instruments for flood risk management: a review of

theory, practice and perspectives for climate adaptation policy, Environmental

science & policy, 37, pp. 227-242.

Howard, S. J., Gordon, R. and Jones, S. C. (2014) Australian alcohol policy 2001–

2013 and implications for public health, BMC Public Health, 14(1), pp. 848.

Johansson, D., Stenkula, M. and Du Rietz, G. (2015) Capital income taxation of

Swedish households, 1862–2010, Scandinavian Economic History Review, 63(2),

pp. 154-177.

Kim, N. N. and Kim, J. (2015) Top incomes in Korea, 1933-2010: Evidence from

income tax statistics, Hitotsubashi Journal of Economics, pp. 1-19.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. (Eds.). (2018) Introduction to

European tax law on direct taxation. Linde Verlag GmbH.

12

Mehrotra, A. K. and Ott, J. C. (2015) The curious beginnings of the capital gains tax

preference, Fordham L. Rev., 84, pp. 2517.

Paolella, L. and Durand, R. (2016) Category spanning, evaluation, and performance:

Revised theory and test on the corporate law market, Academy of Management

Journal, 59(1), pp. 330-351.

Thuronyi, V. and Brooks, K. (2016) Comparative tax law. Kluwer Law International

BV.

Wagner, M. (2014) Regulatory Space in International Trade Law and International

Investment Law, U. Pa. J. Int'l L., 36, pp. 1.

Online

Australian Government, (2017) Personal services income [Online]. Available at:

https://www.ato.gov.au/Business/Personal-services-income/ (Accessed: 26th May

2019).

Mccallum, J. (2018) Tax office takes on professionals over income splitting [Online].

Available at: https://www.intheblack.com/articles/2018/04/05/ato-accountant-income-

splitting (Accessed: 26th May 2019).

Mehrotra, A. K. and Ott, J. C. (2015) The curious beginnings of the capital gains tax

preference, Fordham L. Rev., 84, pp. 2517.

Paolella, L. and Durand, R. (2016) Category spanning, evaluation, and performance:

Revised theory and test on the corporate law market, Academy of Management

Journal, 59(1), pp. 330-351.

Thuronyi, V. and Brooks, K. (2016) Comparative tax law. Kluwer Law International

BV.

Wagner, M. (2014) Regulatory Space in International Trade Law and International

Investment Law, U. Pa. J. Int'l L., 36, pp. 1.

Online

Australian Government, (2017) Personal services income [Online]. Available at:

https://www.ato.gov.au/Business/Personal-services-income/ (Accessed: 26th May

2019).

Mccallum, J. (2018) Tax office takes on professionals over income splitting [Online].

Available at: https://www.intheblack.com/articles/2018/04/05/ato-accountant-income-

splitting (Accessed: 26th May 2019).

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.