HA3042 Taxation Law T2 2018 Individual Assignment Analysis

VerifiedAdded on 2023/06/06

|10

|2811

|476

Homework Assignment

AI Summary

This assignment solution for HA3042 Taxation Law, Term 2 2018, addresses four key questions. Question 1 examines the tax implications of lottery winnings, clarifying that annual payments from a 'Set for Life' lottery are taxable as 'other income' and subject to income tax. Question 2 analyzes the taxable income of Corner Pharmacy, detailing sales, cost of goods sold, and allowable deductions for salaries and rent, while also explaining the Pharmaceutical Benefits Scheme (PBS) and its non-taxable income status. Question 3 delves into the Duke of Westminster case, contrasting its historical context with current tax avoidance principles, and highlighting the shift towards assessing transactions as a whole rather than individual steps, guided by the Ramsay case law. Question 4 focuses on a rental property scenario involving joint tenants, Joseph and Jane, outlining the allocation of profits, losses, and the subsequent implications for tax assessment, including the treatment of capital gains or losses upon property sale. The assignment provides a comprehensive overview of various aspects of taxation law.

HA3042 Taxation Law T2 2018

Individual Assignment

Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................6

Question 4........................................................................................................................................8

References......................................................................................................................................10

Question 1........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................6

Question 4........................................................................................................................................8

References......................................................................................................................................10

QUESTION 1

Facts of the case

A lottery has been conducted by Lotteries Commission named as ‘SET for Life’. It has been

provided in terms of lottery that in case any participant scratches three ‘set for life’ panels will

win $5000 for each year for twenty years. Moreover in the event of death outstanding amount

will be paid to the deceased’s estate.

Australian Taxation Office provision relating to other income which comprises Lottery and

winning are as follows:

In case any individual has won something in prize draws, or lottery run through their banks,

building society, credit union or any other investment corpse, the individual should proclaim on

his tax return the value of any profits or prizes that is received by him that same are taxed under

head other income and considered as part of assessable income. Further, prizes might comprise

cash, low-interest or interest-free loans, a tour package or cars (Woellner et al. 2016). Hence,

there is no need of proclaiming prizes that are won in normal lotteries like lotto draws and

raffles. Moreover, if anyone is playing a game show and also its contestant than in that case, he

can only proclaim prizes that he had a win by receiving appearance fees or game show-winnings

commonly. Moreover, on case individual is selling or disposing of an asset which was won as a

prize from a lottery than in that case it will be considered as capital gain as it is earned by selling

off assets (Sharkey, 2016). The same will declared on the tax return.

Decision

Yes, the amount which is received by lottery or prize draw is the annual payment income since it

is the part of other income. Moreover, mode of payment does not change the core meaning of

income from lottery and winning. Thus, in the present case of Lotteries Commission, if anyone

is winning the lottery called Set for life if the winner has scratches three cards named ‘set for life

‘of the lottery than he will get $50000 each year for 20 years. The income which will be received

by winning the lottery will be taxable and recorded in other income.

Facts of the case

A lottery has been conducted by Lotteries Commission named as ‘SET for Life’. It has been

provided in terms of lottery that in case any participant scratches three ‘set for life’ panels will

win $5000 for each year for twenty years. Moreover in the event of death outstanding amount

will be paid to the deceased’s estate.

Australian Taxation Office provision relating to other income which comprises Lottery and

winning are as follows:

In case any individual has won something in prize draws, or lottery run through their banks,

building society, credit union or any other investment corpse, the individual should proclaim on

his tax return the value of any profits or prizes that is received by him that same are taxed under

head other income and considered as part of assessable income. Further, prizes might comprise

cash, low-interest or interest-free loans, a tour package or cars (Woellner et al. 2016). Hence,

there is no need of proclaiming prizes that are won in normal lotteries like lotto draws and

raffles. Moreover, if anyone is playing a game show and also its contestant than in that case, he

can only proclaim prizes that he had a win by receiving appearance fees or game show-winnings

commonly. Moreover, on case individual is selling or disposing of an asset which was won as a

prize from a lottery than in that case it will be considered as capital gain as it is earned by selling

off assets (Sharkey, 2016). The same will declared on the tax return.

Decision

Yes, the amount which is received by lottery or prize draw is the annual payment income since it

is the part of other income. Moreover, mode of payment does not change the core meaning of

income from lottery and winning. Thus, in the present case of Lotteries Commission, if anyone

is winning the lottery called Set for life if the winner has scratches three cards named ‘set for life

‘of the lottery than he will get $50000 each year for 20 years. The income which will be received

by winning the lottery will be taxable and recorded in other income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, taxes which are deducted from winning prizes like lottery or jackpot is subjected in the

country of residence such as income tax are the duty of winners and not of the Lotter. Thus, in

the present case, the payment received as lottery income will be taxed at the rate of 30%.

However, the amount is taxable only at the time amount has been paid. It means that the amount

will be taxed annually in the same manner in which amount is being received by the winner.

QUESTION 2

Federal income tax is charged on the taxable profits of an individual or an organization. It is

calculated on the assessable income by subtracting any permissible deductions. Assessable

income is usually which is earned by the business - it does not take in any GST owed on sales

made by them, or GST credits.

Statement presenting taxable income of Corner Pharmacy:

Particular Amount $

Sales from ordinary business (Note 1) 610000

Cost of goods sold (Note2) 302459.0164

Salaries (Note 3) 60000

Rent (Note 3) 50000

Billing of PBS (Note 4) 200000

Assessable Income 397540.9836

Less : Non-Taxable Income 200000

Taxable Income 197540.9836

Note: 1

Particular Amount in $

Total Sales

Cash Sales + Credit Sales+ Credit card reimbursement 610000

300000+150000+160000

Sales of PSB 200000

country of residence such as income tax are the duty of winners and not of the Lotter. Thus, in

the present case, the payment received as lottery income will be taxed at the rate of 30%.

However, the amount is taxable only at the time amount has been paid. It means that the amount

will be taxed annually in the same manner in which amount is being received by the winner.

QUESTION 2

Federal income tax is charged on the taxable profits of an individual or an organization. It is

calculated on the assessable income by subtracting any permissible deductions. Assessable

income is usually which is earned by the business - it does not take in any GST owed on sales

made by them, or GST credits.

Statement presenting taxable income of Corner Pharmacy:

Particular Amount $

Sales from ordinary business (Note 1) 610000

Cost of goods sold (Note2) 302459.0164

Salaries (Note 3) 60000

Rent (Note 3) 50000

Billing of PBS (Note 4) 200000

Assessable Income 397540.9836

Less : Non-Taxable Income 200000

Taxable Income 197540.9836

Note: 1

Particular Amount in $

Total Sales

Cash Sales + Credit Sales+ Credit card reimbursement 610000

300000+150000+160000

Sales of PSB 200000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

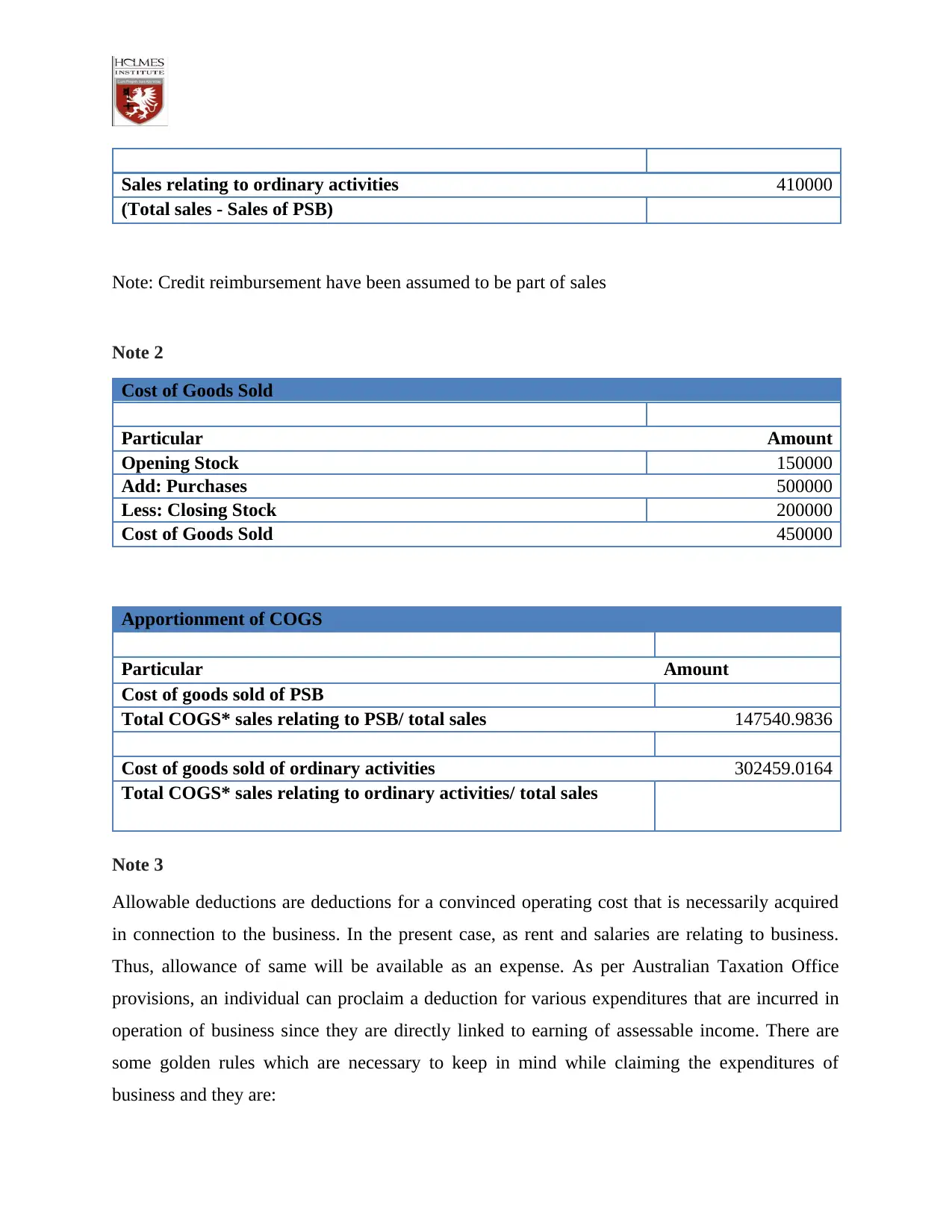

Sales relating to ordinary activities 410000

(Total sales - Sales of PSB)

Note: Credit reimbursement have been assumed to be part of sales

Note 2

Cost of Goods Sold

Particular Amount

Opening Stock 150000

Add: Purchases 500000

Less: Closing Stock 200000

Cost of Goods Sold 450000

Apportionment of COGS

Particular Amount

Cost of goods sold of PSB

Total COGS* sales relating to PSB/ total sales 147540.9836

Cost of goods sold of ordinary activities 302459.0164

Total COGS* sales relating to ordinary activities/ total sales

Note 3

Allowable deductions are deductions for a convinced operating cost that is necessarily acquired

in connection to the business. In the present case, as rent and salaries are relating to business.

Thus, allowance of same will be available as an expense. As per Australian Taxation Office

provisions, an individual can proclaim a deduction for various expenditures that are incurred in

operation of business since they are directly linked to earning of assessable income. There are

some golden rules which are necessary to keep in mind while claiming the expenditures of

business and they are:

(Total sales - Sales of PSB)

Note: Credit reimbursement have been assumed to be part of sales

Note 2

Cost of Goods Sold

Particular Amount

Opening Stock 150000

Add: Purchases 500000

Less: Closing Stock 200000

Cost of Goods Sold 450000

Apportionment of COGS

Particular Amount

Cost of goods sold of PSB

Total COGS* sales relating to PSB/ total sales 147540.9836

Cost of goods sold of ordinary activities 302459.0164

Total COGS* sales relating to ordinary activities/ total sales

Note 3

Allowable deductions are deductions for a convinced operating cost that is necessarily acquired

in connection to the business. In the present case, as rent and salaries are relating to business.

Thus, allowance of same will be available as an expense. As per Australian Taxation Office

provisions, an individual can proclaim a deduction for various expenditures that are incurred in

operation of business since they are directly linked to earning of assessable income. There are

some golden rules which are necessary to keep in mind while claiming the expenditures of

business and they are:

The funds should have used up for business and not for private expenditures.

In case it is for a mix of business and private utilization, then, in that case, the

claim will be made on the part which is related to the business.

It is necessary that the company must have records to certify it.

In the present case as all the requirements for claiming a deduction as business expense have

been fulfilled for salary and rent; thus same have been deducted from income from business

activity.

Note 4

The Pharmaceutical Benefits Scheme (PBS) is a scheme of the Australian Government that

offers subsidized prescription drugs to the populace of Australia, in addition to convinced foreign

guests enclosed by a Reciprocal Health Care Agreement (Pharmaceutical Benefits Scheme,

2018). The PBS investigates to assure that the Australian populace has reasonable and consistent

access to a broad variety of essential medicines (Barkoczy, 2017). The PBS has a deal with the

increased inspection because its prices have greater than before. The income under same is

required to be evaluated on an accrual basis for taxation purpose; however the same is assessed

under head non-taxable income as no income tax is required to be paid on same.

Under PBS a taxpayer who is entitled to payment is assessable on the amount when it is

originated. With regards to when amounts payable under PBS are computed, it is essential to find

out time at which a recoverable debt is generated (Blakelock and King, 2017). Moreover, it is

believed that a pharmacist accounting for income is ascertained on an accrual basis, i.e. it records

PBS income at the time a product is distributed to the consumer.

QUESTION 3

Facts of case

The case of the Duke of Westminster is usually known as tax avoidance. The full title of the case

was Inland Revenue Commissioners v. Duke of Westminster A.C (1936). in which Duke of

Minister has employed a gardener and reimburses him with post-tax income. In order to lower

In case it is for a mix of business and private utilization, then, in that case, the

claim will be made on the part which is related to the business.

It is necessary that the company must have records to certify it.

In the present case as all the requirements for claiming a deduction as business expense have

been fulfilled for salary and rent; thus same have been deducted from income from business

activity.

Note 4

The Pharmaceutical Benefits Scheme (PBS) is a scheme of the Australian Government that

offers subsidized prescription drugs to the populace of Australia, in addition to convinced foreign

guests enclosed by a Reciprocal Health Care Agreement (Pharmaceutical Benefits Scheme,

2018). The PBS investigates to assure that the Australian populace has reasonable and consistent

access to a broad variety of essential medicines (Barkoczy, 2017). The PBS has a deal with the

increased inspection because its prices have greater than before. The income under same is

required to be evaluated on an accrual basis for taxation purpose; however the same is assessed

under head non-taxable income as no income tax is required to be paid on same.

Under PBS a taxpayer who is entitled to payment is assessable on the amount when it is

originated. With regards to when amounts payable under PBS are computed, it is essential to find

out time at which a recoverable debt is generated (Blakelock and King, 2017). Moreover, it is

believed that a pharmacist accounting for income is ascertained on an accrual basis, i.e. it records

PBS income at the time a product is distributed to the consumer.

QUESTION 3

Facts of case

The case of the Duke of Westminster is usually known as tax avoidance. The full title of the case

was Inland Revenue Commissioners v. Duke of Westminster A.C (1936). in which Duke of

Minister has employed a gardener and reimburses him with post-tax income. In order to lower

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the tax, he stopped paying the wages of gardener and drew up an agreement to provide equal

amount at the end of every specific period. Now, in accordance with tax law of times, Duke was

able to claim expenses as deduction through reducing its taxable income as well as the liability of

tax as well. Due to the same Inland Revenue has challenged his arrangement as a claimed that

the arrangement made by duke is eventually leading to tax avoidance and also took Duke to

court.

The conclusion of the case

The decision was passed by the judge that everyone is entitled to order his transactions so that

the tax attaching under the appropriate acts is lower than it otherwise would be. At the same

time, it was considered that in case the assessee succeeded in proving the same to secure the

result that even though the commissioner of Inland Revenue or his fellow taxpayers are

ingenuity, but same will not be able to compel the assessee to pay the enhanced tax (Woellner

and et al., 2016). Hence, the decision was made in favour of the assessee, and it was proven that

an individual has appropriate right to reduce the tax liability in a legal manner to possible extent

and same does not eventually lead to tax avoidance.

The manner in which decision is taken in the present time

The decision was passed by a judge of the court that everyone is allowed to reduce the tax

liability if he is able to order his activities so that the tax connecting with the suitable acts is

lower than it otherwise would be. The same implies that if he gets success in arranging them in

to secure this outcome then unappreciative the Commissioners of IRCs or his associate taxpayers

might be inventiveness; he could not be obliged to pay an increased tax (Swarb.Co.Uk, 2018). At

the same time, it was noticed that if this rule will be continued in the same manner that all will

try to avoid tax legally through producing intricate structures. Further due to the same reason the

decision, in this case, is not continued in an exact manner, and the conclusion of the Ramsay case

law have been adopted now onwards. Virgo, 2018 asserts that the decision of case states that if

the transaction has pre-ordered imitation steps that provide up no purpose commercial objective,

however, the main aim was only to save the applicable tax, due to the same manner all the

transactions were judged as whole rather the being individual. In other words, same could be

amount at the end of every specific period. Now, in accordance with tax law of times, Duke was

able to claim expenses as deduction through reducing its taxable income as well as the liability of

tax as well. Due to the same Inland Revenue has challenged his arrangement as a claimed that

the arrangement made by duke is eventually leading to tax avoidance and also took Duke to

court.

The conclusion of the case

The decision was passed by the judge that everyone is entitled to order his transactions so that

the tax attaching under the appropriate acts is lower than it otherwise would be. At the same

time, it was considered that in case the assessee succeeded in proving the same to secure the

result that even though the commissioner of Inland Revenue or his fellow taxpayers are

ingenuity, but same will not be able to compel the assessee to pay the enhanced tax (Woellner

and et al., 2016). Hence, the decision was made in favour of the assessee, and it was proven that

an individual has appropriate right to reduce the tax liability in a legal manner to possible extent

and same does not eventually lead to tax avoidance.

The manner in which decision is taken in the present time

The decision was passed by a judge of the court that everyone is allowed to reduce the tax

liability if he is able to order his activities so that the tax connecting with the suitable acts is

lower than it otherwise would be. The same implies that if he gets success in arranging them in

to secure this outcome then unappreciative the Commissioners of IRCs or his associate taxpayers

might be inventiveness; he could not be obliged to pay an increased tax (Swarb.Co.Uk, 2018). At

the same time, it was noticed that if this rule will be continued in the same manner that all will

try to avoid tax legally through producing intricate structures. Further due to the same reason the

decision, in this case, is not continued in an exact manner, and the conclusion of the Ramsay case

law have been adopted now onwards. Virgo, 2018 asserts that the decision of case states that if

the transaction has pre-ordered imitation steps that provide up no purpose commercial objective,

however, the main aim was only to save the applicable tax, due to the same manner all the

transactions were judged as whole rather the being individual. In other words, same could be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interpreted as in a situation in which pre-ordered imitation steps have been developed which

serve no commercial goal excluding saving of tax, then it will not be considered on an individual

basis, and all the transaction will be accessed as a whole.

The courts are now concerning themselves not only with the authenticity of the transaction but

also with the anticipated cause of it on fiscal objectives granted (Alstadsæter, Johannesen and

Zucman, 2018). Now, nobody could get away from the tax evasion project with the simple

statement that there is nothing illegitimate about it. Earlier, it has been seen in previous decision

that by giving the statement it is nothing illegal about tax evasion and everyone do it they get

away, but in present time it is a moral duty of taxpayer to follow the law, they are bounded by

the laws, but are not bounded beyond the edict for except for the law, tax will be blackmailing or

racketeering. The intention behind the same is not only attainment of actual tax liability but

against crime a sovereign moral responsibility. It can be concluded from a case study of Ramsay

that by evasion of tax taxpayers are not paying off the appropriate quantum of tax, the same will

be not an ethical concept which can be allowed to be continued . Thus, the decision of the case of

Westminster which specifically stated that principal of cardinal is available here and it no

situation it is should be exaggerated or overextended in order to take inappropriate advantage of

the decision made by the court (Braithwaite, 2017). Moreover, the same be reformed, and the

decision made by the court in Ramsay case law now supersede the decision of Westminster that

the fundamental substance of the transaction will be evaluated in order to ascertain the main aim

behind same.

QUESTION 4

In the cited case, Joseph is an accountant and Jane is his wife, both borrowed money and

purchased a rental property acting as a joint tenant. In this aspect, a contract was formed, stating

that, Joseph is entitled to 20% profits while Jane is entitled to 80% profits from the rental

property. On the other hand, if the property suffers from loss, then Joseph is 100% entitled to the

loss. Last year, $40000 amount of loss took place. Further, the case is conducted on the basis of

loss evaluation and entitlement for the taxation intent and the result of profits or losses. In

addition, it will also assess the manner by which the capital loss or gain will be accounted if the

serve no commercial goal excluding saving of tax, then it will not be considered on an individual

basis, and all the transaction will be accessed as a whole.

The courts are now concerning themselves not only with the authenticity of the transaction but

also with the anticipated cause of it on fiscal objectives granted (Alstadsæter, Johannesen and

Zucman, 2018). Now, nobody could get away from the tax evasion project with the simple

statement that there is nothing illegitimate about it. Earlier, it has been seen in previous decision

that by giving the statement it is nothing illegal about tax evasion and everyone do it they get

away, but in present time it is a moral duty of taxpayer to follow the law, they are bounded by

the laws, but are not bounded beyond the edict for except for the law, tax will be blackmailing or

racketeering. The intention behind the same is not only attainment of actual tax liability but

against crime a sovereign moral responsibility. It can be concluded from a case study of Ramsay

that by evasion of tax taxpayers are not paying off the appropriate quantum of tax, the same will

be not an ethical concept which can be allowed to be continued . Thus, the decision of the case of

Westminster which specifically stated that principal of cardinal is available here and it no

situation it is should be exaggerated or overextended in order to take inappropriate advantage of

the decision made by the court (Braithwaite, 2017). Moreover, the same be reformed, and the

decision made by the court in Ramsay case law now supersede the decision of Westminster that

the fundamental substance of the transaction will be evaluated in order to ascertain the main aim

behind same.

QUESTION 4

In the cited case, Joseph is an accountant and Jane is his wife, both borrowed money and

purchased a rental property acting as a joint tenant. In this aspect, a contract was formed, stating

that, Joseph is entitled to 20% profits while Jane is entitled to 80% profits from the rental

property. On the other hand, if the property suffers from loss, then Joseph is 100% entitled to the

loss. Last year, $40000 amount of loss took place. Further, the case is conducted on the basis of

loss evaluation and entitlement for the taxation intent and the result of profits or losses. In

addition, it will also assess the manner by which the capital loss or gain will be accounted if the

property is sold by the joint tenants. Ultimately the issue in the present case scenario is that to

whom the tax is entitled.

In accordance with the applicable provision of the TR 93/32 “Income Tax: rental property for

this specified case distribution of net gain or loss amongst the partners, proportionate aspects will

be assessed by the business partners who are also justifiable for the purpose of tax if it is profit

or loss. On the other hand, there is the presence of some exemption to this user under which joint

tenancy is considered since partnership for the purpose of the tax is held if individuals conduct

business. In the context of the agreement, which is conducted for the tax purpose then in this

case loss will not be allocated according to the agreement given by both Jane and Joseph.

Further, it is also stated by the provision that joint tenants of rental premises are not meant for

partnership thereby they agreed aspects cannot create an impact on taxation. It is reasonable to

do division of the owners of rental property (Anderson, Dickfos and Brown, 2016).

Consequently, the co-owners of rental property are not stated as partners under the law; it is

because they are not on the basis of the applied general law to include the gain or loss from the

held rented premises.

With the application of the provision given under TR 93/32 “Income Tax: rental property, the net

gain or loss division amongst partner, in the present scenario, it can be cited that the both Joseph

and Jane as joint tenants are only for the tax purpose of tax evasion and are not conducting

business thereby the agreement is not applied for taxation calculation and the loss will be divided

proportionately (Shaw, 2017).

whom the tax is entitled.

In accordance with the applicable provision of the TR 93/32 “Income Tax: rental property for

this specified case distribution of net gain or loss amongst the partners, proportionate aspects will

be assessed by the business partners who are also justifiable for the purpose of tax if it is profit

or loss. On the other hand, there is the presence of some exemption to this user under which joint

tenancy is considered since partnership for the purpose of the tax is held if individuals conduct

business. In the context of the agreement, which is conducted for the tax purpose then in this

case loss will not be allocated according to the agreement given by both Jane and Joseph.

Further, it is also stated by the provision that joint tenants of rental premises are not meant for

partnership thereby they agreed aspects cannot create an impact on taxation. It is reasonable to

do division of the owners of rental property (Anderson, Dickfos and Brown, 2016).

Consequently, the co-owners of rental property are not stated as partners under the law; it is

because they are not on the basis of the applied general law to include the gain or loss from the

held rented premises.

With the application of the provision given under TR 93/32 “Income Tax: rental property, the net

gain or loss division amongst partner, in the present scenario, it can be cited that the both Joseph

and Jane as joint tenants are only for the tax purpose of tax evasion and are not conducting

business thereby the agreement is not applied for taxation calculation and the loss will be divided

proportionately (Shaw, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Virgo, G., 2018. The Principles of Equity and Trusts. Oxford university press.

Alstadsæter, A., Johannesen, N. and Zucman, G., 2018. Tax Evasion and Tax Avoidance.

Routledge.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. Insolvency Law Journal, 24(2), pp.127-140.

Shaw, A., 2017. Tax files: Why small really is better: Accessing the lower corporate tax rate

for small business entities. Bulletin (Law Society of South Australia), 39(10), p.39.

Swarb.Co.Uk, 2018. INLAND REVENUE COMMISSIONERS V DUKE OF WESTMINSTER:

HL 7 MAY 1935 (online) Available through < https://swarb.co.uk/inland-revenue-

commissioners-v-duke-of-westminster-hl-7-may-1935/>. [Accessed on 6 September 2018].

Sharkey, N. 2016. Departing Australia: A complex tax situation with possible benefits and

hidden traps. Tax Specialist, 19(5), 180.

Barkoczy, S., 2017. Core Tax Legislation and Study Guide. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching.

Proctor, The, 37(6), p.18.

Pharmaceutical Benefits Scheme (PBS), 2018. (online) Available through <

http://www.pbs.gov.au/pbs/home;jsessionid=w25595c9lp6u13sbzkvwqdxq7>. [Accessed on

6 September 2018].

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Virgo, G., 2018. The Principles of Equity and Trusts. Oxford university press.

Alstadsæter, A., Johannesen, N. and Zucman, G., 2018. Tax Evasion and Tax Avoidance.

Routledge.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. Insolvency Law Journal, 24(2), pp.127-140.

Shaw, A., 2017. Tax files: Why small really is better: Accessing the lower corporate tax rate

for small business entities. Bulletin (Law Society of South Australia), 39(10), p.39.

Swarb.Co.Uk, 2018. INLAND REVENUE COMMISSIONERS V DUKE OF WESTMINSTER:

HL 7 MAY 1935 (online) Available through < https://swarb.co.uk/inland-revenue-

commissioners-v-duke-of-westminster-hl-7-may-1935/>. [Accessed on 6 September 2018].

Sharkey, N. 2016. Departing Australia: A complex tax situation with possible benefits and

hidden traps. Tax Specialist, 19(5), 180.

Barkoczy, S., 2017. Core Tax Legislation and Study Guide. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching.

Proctor, The, 37(6), p.18.

Pharmaceutical Benefits Scheme (PBS), 2018. (online) Available through <

http://www.pbs.gov.au/pbs/home;jsessionid=w25595c9lp6u13sbzkvwqdxq7>. [Accessed on

6 September 2018].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.