Taxation Law Assignment: ITAA, GST, and Partnership Income

VerifiedAdded on 2020/04/07

|12

|2489

|61

Homework Assignment

AI Summary

This taxation law assignment addresses several key areas of Australian tax law. Question 1 examines allowable deductions under s 8-1 of the ITAA 1997, differentiating between capital and revenue expenses with practical examples. Question 2 analyzes GST input tax credits for a bank, assessing the eligibility of advertising expenses for input tax credit. Question 3 focuses on foreign tax offsets, calculating the taxable income and tax payable for an individual with income from both domestic and foreign sources. The calculation demonstrates the application of foreign tax offset provisions. Finally, Question 4 assesses partnership income, determining the net income or loss for a partnership engaged in selling sporting goods, considering various assessable incomes and deductible expenses, and highlighting the relevant tax implications for partnership businesses. The assignment provides detailed calculations and explanations of the relevant legal provisions.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................1

Introduction..................................................................................................................................1

Legal Provisions...........................................................................................................................1

Application...................................................................................................................................1

Conclusion...................................................................................................................................3

QUESTION 2..................................................................................................................................3

Introduction..................................................................................................................................3

Legal Provisions...........................................................................................................................3

Application...................................................................................................................................4

Conclusion...................................................................................................................................4

Question 3........................................................................................................................................5

Issue.............................................................................................................................................5

Legal provisions...........................................................................................................................5

Application of legal provisions....................................................................................................5

Calculation...................................................................................................................................5

Question 4........................................................................................................................................5

Issue.............................................................................................................................................5

Legal provisions...........................................................................................................................5

Application of legal provisions....................................................................................................5

Calculation...................................................................................................................................5

REFERENCES................................................................................................................................6

QUESTION 1..................................................................................................................................1

Introduction..................................................................................................................................1

Legal Provisions...........................................................................................................................1

Application...................................................................................................................................1

Conclusion...................................................................................................................................3

QUESTION 2..................................................................................................................................3

Introduction..................................................................................................................................3

Legal Provisions...........................................................................................................................3

Application...................................................................................................................................4

Conclusion...................................................................................................................................4

Question 3........................................................................................................................................5

Issue.............................................................................................................................................5

Legal provisions...........................................................................................................................5

Application of legal provisions....................................................................................................5

Calculation...................................................................................................................................5

Question 4........................................................................................................................................5

Issue.............................................................................................................................................5

Legal provisions...........................................................................................................................5

Application of legal provisions....................................................................................................5

Calculation...................................................................................................................................5

REFERENCES................................................................................................................................6

QUESTION 1

Introduction

This segment explains whether the discussed scenarios are allowable as deductions under

s 8-1 of the ITAA 1997 or not.

Legal Provisions

Income tax is computed based on the assessable income of an individual. This assessable

income is computed by subtracting “specific” and “general” deductions from the gross income of

the taxpayer for that year. A general deduction as per ITAA 1997 s 8-1 refers to a loss or

outgoing which is related to some income generating operations (e.g. investment or business

activity), and is not of domestic, capital or private nature. On the contrary, a specific deduction is

a sum which a provision except the general deduction provision permits as a deduction

(Woellner et al., 2011).

There are several deduction rejection provisions as well which prohibit deductions for

certain amounts.

General Deductions under s 8-1 ITAA 1997:

8-1(1) The tax payer can deduct from his/her taxable income any outgoing or loss to the limit

that:

a) It is incurred in producing or gaining the taxable income; or

b) It is incurred essentially to carry on a business to gain or produce the taxable income

(D'Ascenzo and England, 2005).

8-1(2) Nonetheless, the taxpayer cannot subtract any outgoing or loss under this Act to the limit

that:

a) It is capital or of similar nature; or

b) It is of domestic or private nature; or

c) It is incurred to produce or gain the non-taxable non-exempt income or the exempt

income; or

d) Any subsection of this section prohibits it from being deducted (Mete, Dick and

Moerman, 2010).

1

Introduction

This segment explains whether the discussed scenarios are allowable as deductions under

s 8-1 of the ITAA 1997 or not.

Legal Provisions

Income tax is computed based on the assessable income of an individual. This assessable

income is computed by subtracting “specific” and “general” deductions from the gross income of

the taxpayer for that year. A general deduction as per ITAA 1997 s 8-1 refers to a loss or

outgoing which is related to some income generating operations (e.g. investment or business

activity), and is not of domestic, capital or private nature. On the contrary, a specific deduction is

a sum which a provision except the general deduction provision permits as a deduction

(Woellner et al., 2011).

There are several deduction rejection provisions as well which prohibit deductions for

certain amounts.

General Deductions under s 8-1 ITAA 1997:

8-1(1) The tax payer can deduct from his/her taxable income any outgoing or loss to the limit

that:

a) It is incurred in producing or gaining the taxable income; or

b) It is incurred essentially to carry on a business to gain or produce the taxable income

(D'Ascenzo and England, 2005).

8-1(2) Nonetheless, the taxpayer cannot subtract any outgoing or loss under this Act to the limit

that:

a) It is capital or of similar nature; or

b) It is of domestic or private nature; or

c) It is incurred to produce or gain the non-taxable non-exempt income or the exempt

income; or

d) Any subsection of this section prohibits it from being deducted (Mete, Dick and

Moerman, 2010).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

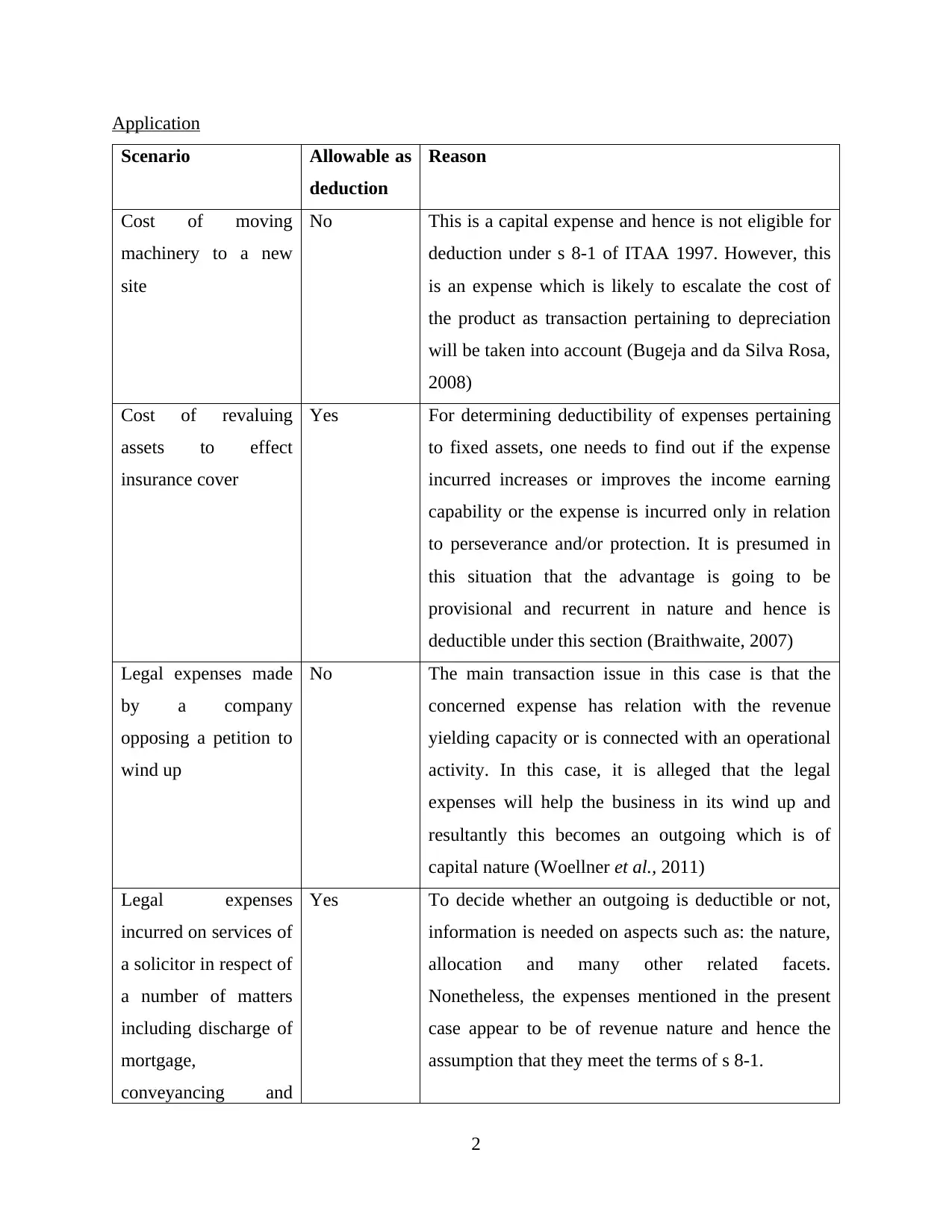

Application

Scenario Allowable as

deduction

Reason

Cost of moving

machinery to a new

site

No This is a capital expense and hence is not eligible for

deduction under s 8-1 of ITAA 1997. However, this

is an expense which is likely to escalate the cost of

the product as transaction pertaining to depreciation

will be taken into account (Bugeja and da Silva Rosa,

2008)

Cost of revaluing

assets to effect

insurance cover

Yes For determining deductibility of expenses pertaining

to fixed assets, one needs to find out if the expense

incurred increases or improves the income earning

capability or the expense is incurred only in relation

to perseverance and/or protection. It is presumed in

this situation that the advantage is going to be

provisional and recurrent in nature and hence is

deductible under this section (Braithwaite, 2007)

Legal expenses made

by a company

opposing a petition to

wind up

No The main transaction issue in this case is that the

concerned expense has relation with the revenue

yielding capacity or is connected with an operational

activity. In this case, it is alleged that the legal

expenses will help the business in its wind up and

resultantly this becomes an outgoing which is of

capital nature (Woellner et al., 2011)

Legal expenses

incurred on services of

a solicitor in respect of

a number of matters

including discharge of

mortgage,

conveyancing and

Yes To decide whether an outgoing is deductible or not,

information is needed on aspects such as: the nature,

allocation and many other related facets.

Nonetheless, the expenses mentioned in the present

case appear to be of revenue nature and hence the

assumption that they meet the terms of s 8-1.

2

Scenario Allowable as

deduction

Reason

Cost of moving

machinery to a new

site

No This is a capital expense and hence is not eligible for

deduction under s 8-1 of ITAA 1997. However, this

is an expense which is likely to escalate the cost of

the product as transaction pertaining to depreciation

will be taken into account (Bugeja and da Silva Rosa,

2008)

Cost of revaluing

assets to effect

insurance cover

Yes For determining deductibility of expenses pertaining

to fixed assets, one needs to find out if the expense

incurred increases or improves the income earning

capability or the expense is incurred only in relation

to perseverance and/or protection. It is presumed in

this situation that the advantage is going to be

provisional and recurrent in nature and hence is

deductible under this section (Braithwaite, 2007)

Legal expenses made

by a company

opposing a petition to

wind up

No The main transaction issue in this case is that the

concerned expense has relation with the revenue

yielding capacity or is connected with an operational

activity. In this case, it is alleged that the legal

expenses will help the business in its wind up and

resultantly this becomes an outgoing which is of

capital nature (Woellner et al., 2011)

Legal expenses

incurred on services of

a solicitor in respect of

a number of matters

including discharge of

mortgage,

conveyancing and

Yes To decide whether an outgoing is deductible or not,

information is needed on aspects such as: the nature,

allocation and many other related facets.

Nonetheless, the expenses mentioned in the present

case appear to be of revenue nature and hence the

assumption that they meet the terms of s 8-1.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

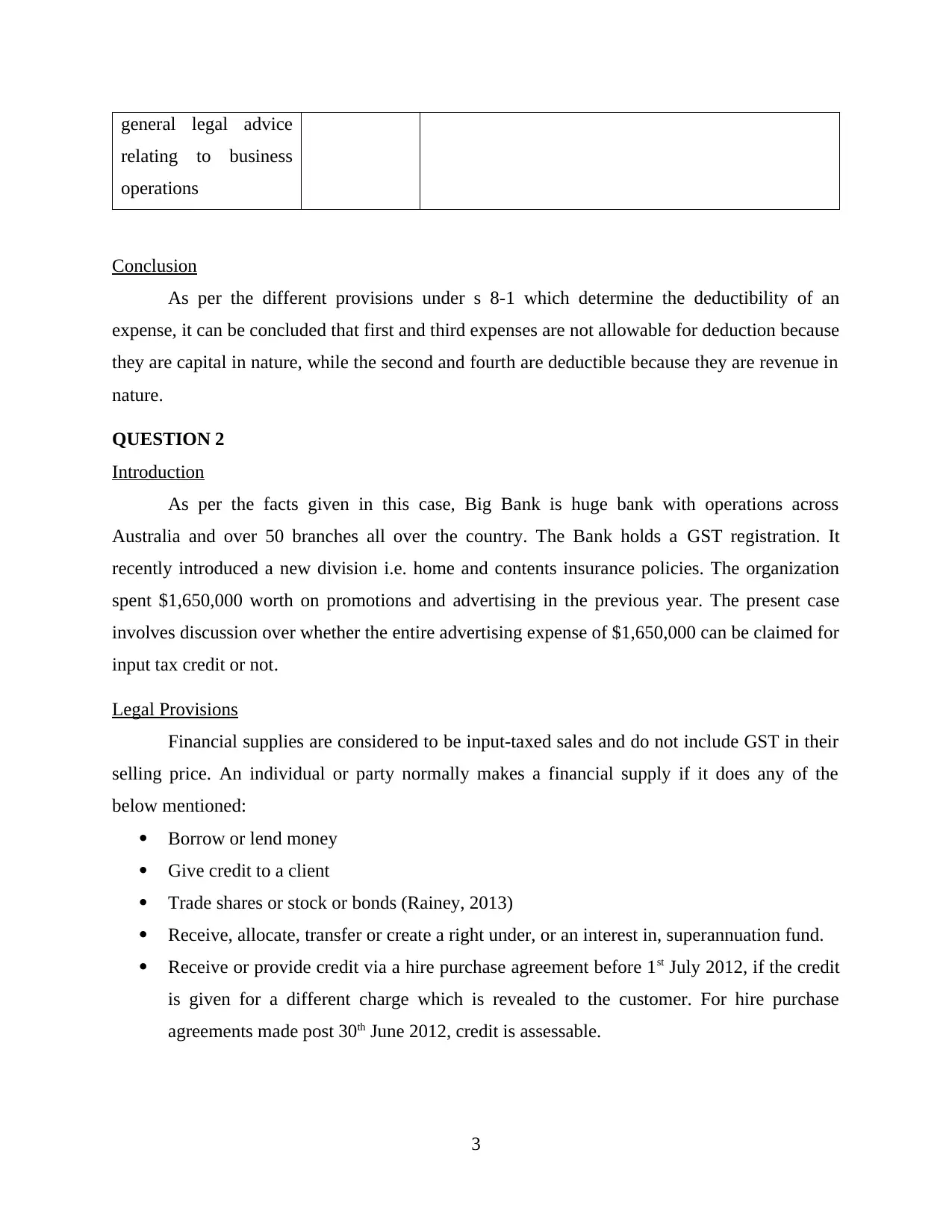

general legal advice

relating to business

operations

Conclusion

As per the different provisions under s 8-1 which determine the deductibility of an

expense, it can be concluded that first and third expenses are not allowable for deduction because

they are capital in nature, while the second and fourth are deductible because they are revenue in

nature.

QUESTION 2

Introduction

As per the facts given in this case, Big Bank is huge bank with operations across

Australia and over 50 branches all over the country. The Bank holds a GST registration. It

recently introduced a new division i.e. home and contents insurance policies. The organization

spent $1,650,000 worth on promotions and advertising in the previous year. The present case

involves discussion over whether the entire advertising expense of $1,650,000 can be claimed for

input tax credit or not.

Legal Provisions

Financial supplies are considered to be input-taxed sales and do not include GST in their

selling price. An individual or party normally makes a financial supply if it does any of the

below mentioned:

Borrow or lend money

Give credit to a client

Trade shares or stock or bonds (Rainey, 2013)

Receive, allocate, transfer or create a right under, or an interest in, superannuation fund.

Receive or provide credit via a hire purchase agreement before 1st July 2012, if the credit

is given for a different charge which is revealed to the customer. For hire purchase

agreements made post 30th June 2012, credit is assessable.

3

relating to business

operations

Conclusion

As per the different provisions under s 8-1 which determine the deductibility of an

expense, it can be concluded that first and third expenses are not allowable for deduction because

they are capital in nature, while the second and fourth are deductible because they are revenue in

nature.

QUESTION 2

Introduction

As per the facts given in this case, Big Bank is huge bank with operations across

Australia and over 50 branches all over the country. The Bank holds a GST registration. It

recently introduced a new division i.e. home and contents insurance policies. The organization

spent $1,650,000 worth on promotions and advertising in the previous year. The present case

involves discussion over whether the entire advertising expense of $1,650,000 can be claimed for

input tax credit or not.

Legal Provisions

Financial supplies are considered to be input-taxed sales and do not include GST in their

selling price. An individual or party normally makes a financial supply if it does any of the

below mentioned:

Borrow or lend money

Give credit to a client

Trade shares or stock or bonds (Rainey, 2013)

Receive, allocate, transfer or create a right under, or an interest in, superannuation fund.

Receive or provide credit via a hire purchase agreement before 1st July 2012, if the credit

is given for a different charge which is revealed to the customer. For hire purchase

agreements made post 30th June 2012, credit is assessable.

3

In some exceptional circumstances, the taxpayer could be eligible to claim input credit for a

purchase that is used to make a financial supply, provided any of the below mentioned is

applicable:

The financial acquisition threshold is not exceeded (Schwenzer, Hachem and Kee, 2012)

The purchase is related to a sum that was borrowed and utilized to make a non-input

taxed supply

The purchase is eligible as “reduced credit acquisition” – the taxpayer would be qualified

to a decreased input tax credit (Braithwaite, 2007).

Application

Whether or not the Big Bank satisfies the main terms to be eligible to claim input tax

credit, is determined below:

Registration – The organization has GST registration as per the facts of the case.

Commercial Transaction – The expenses of advertisements are incurred with respect to

the business and have a direct relation with the company. The purchase price includes

GST and the transaction amount is greater than $82.50 (Blacklow, Nicholas and Ray,

2010).

Tax invoices – The Big Bank Ltd. has enough invoice to show as evidence for the

incurrence of expense and payment of tax on the same.

Conclusion

From the understanding of the legal provision related to GST input credit and the

applicability on the concerned case, it can be concluded that Big Bank is eligible to make a claim

for input credits for the advertisement expense on home and content insurance division, however,

it cannot claim credit for the remaining amount of 1,100,000. This is because general banking

does not fall under the purview of this deduction, however, insurance does and hence any

expense on insurance related products or services are also entitled to claim input credit.

4

purchase that is used to make a financial supply, provided any of the below mentioned is

applicable:

The financial acquisition threshold is not exceeded (Schwenzer, Hachem and Kee, 2012)

The purchase is related to a sum that was borrowed and utilized to make a non-input

taxed supply

The purchase is eligible as “reduced credit acquisition” – the taxpayer would be qualified

to a decreased input tax credit (Braithwaite, 2007).

Application

Whether or not the Big Bank satisfies the main terms to be eligible to claim input tax

credit, is determined below:

Registration – The organization has GST registration as per the facts of the case.

Commercial Transaction – The expenses of advertisements are incurred with respect to

the business and have a direct relation with the company. The purchase price includes

GST and the transaction amount is greater than $82.50 (Blacklow, Nicholas and Ray,

2010).

Tax invoices – The Big Bank Ltd. has enough invoice to show as evidence for the

incurrence of expense and payment of tax on the same.

Conclusion

From the understanding of the legal provision related to GST input credit and the

applicability on the concerned case, it can be concluded that Big Bank is eligible to make a claim

for input credits for the advertisement expense on home and content insurance division, however,

it cannot claim credit for the remaining amount of 1,100,000. This is because general banking

does not fall under the purview of this deduction, however, insurance does and hence any

expense on insurance related products or services are also entitled to claim input credit.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

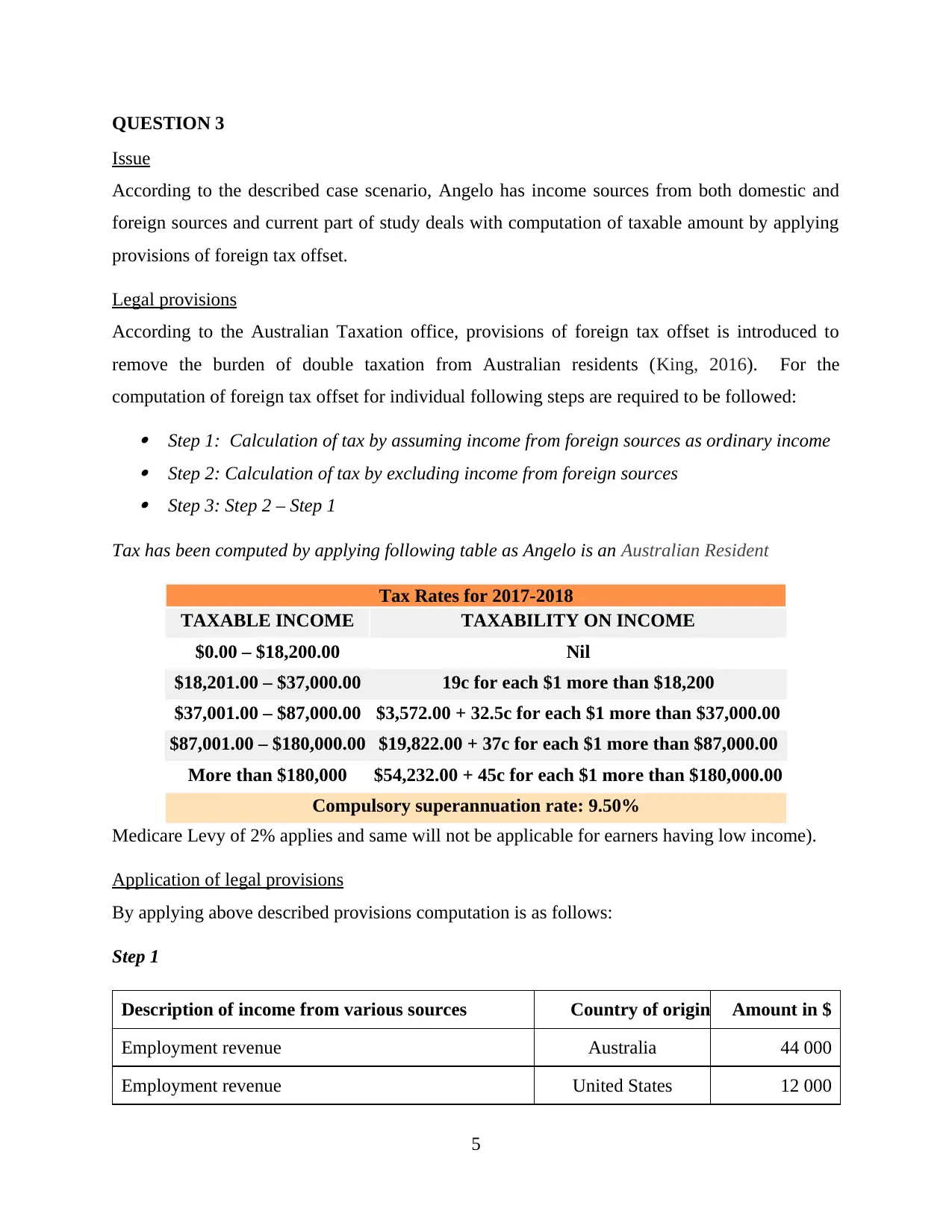

QUESTION 3

Issue

According to the described case scenario, Angelo has income sources from both domestic and

foreign sources and current part of study deals with computation of taxable amount by applying

provisions of foreign tax offset.

Legal provisions

According to the Australian Taxation office, provisions of foreign tax offset is introduced to

remove the burden of double taxation from Australian residents (King, 2016). For the

computation of foreign tax offset for individual following steps are required to be followed: Step 1: Calculation of tax by assuming income from foreign sources as ordinary income Step 2: Calculation of tax by excluding income from foreign sources Step 3: Step 2 – Step 1

Tax has been computed by applying following table as Angelo is an Australian Resident

Tax Rates for 2017-2018

TAXABLE INCOME TAXABILITY ON INCOME

$0.00 – $18,200.00 Nil

$18,201.00 – $37,000.00 19c for each $1 more than $18,200

$37,001.00 – $87,000.00 $3,572.00 + 32.5c for each $1 more than $37,000.00

$87,001.00 – $180,000.00 $19,822.00 + 37c for each $1 more than $87,000.00

More than $180,000 $54,232.00 + 45c for each $1 more than $180,000.00

Compulsory superannuation rate: 9.50%

Medicare Levy of 2% applies and same will not be applicable for earners having low income).

Application of legal provisions

By applying above described provisions computation is as follows:

Step 1

Description of income from various sources Country of origin Amount in $

Employment revenue Australia 44 000

Employment revenue United States 12 000

5

Issue

According to the described case scenario, Angelo has income sources from both domestic and

foreign sources and current part of study deals with computation of taxable amount by applying

provisions of foreign tax offset.

Legal provisions

According to the Australian Taxation office, provisions of foreign tax offset is introduced to

remove the burden of double taxation from Australian residents (King, 2016). For the

computation of foreign tax offset for individual following steps are required to be followed: Step 1: Calculation of tax by assuming income from foreign sources as ordinary income Step 2: Calculation of tax by excluding income from foreign sources Step 3: Step 2 – Step 1

Tax has been computed by applying following table as Angelo is an Australian Resident

Tax Rates for 2017-2018

TAXABLE INCOME TAXABILITY ON INCOME

$0.00 – $18,200.00 Nil

$18,201.00 – $37,000.00 19c for each $1 more than $18,200

$37,001.00 – $87,000.00 $3,572.00 + 32.5c for each $1 more than $37,000.00

$87,001.00 – $180,000.00 $19,822.00 + 37c for each $1 more than $87,000.00

More than $180,000 $54,232.00 + 45c for each $1 more than $180,000.00

Compulsory superannuation rate: 9.50%

Medicare Levy of 2% applies and same will not be applicable for earners having low income).

Application of legal provisions

By applying above described provisions computation is as follows:

Step 1

Description of income from various sources Country of origin Amount in $

Employment revenue Australia 44 000

Employment revenue United States 12 000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

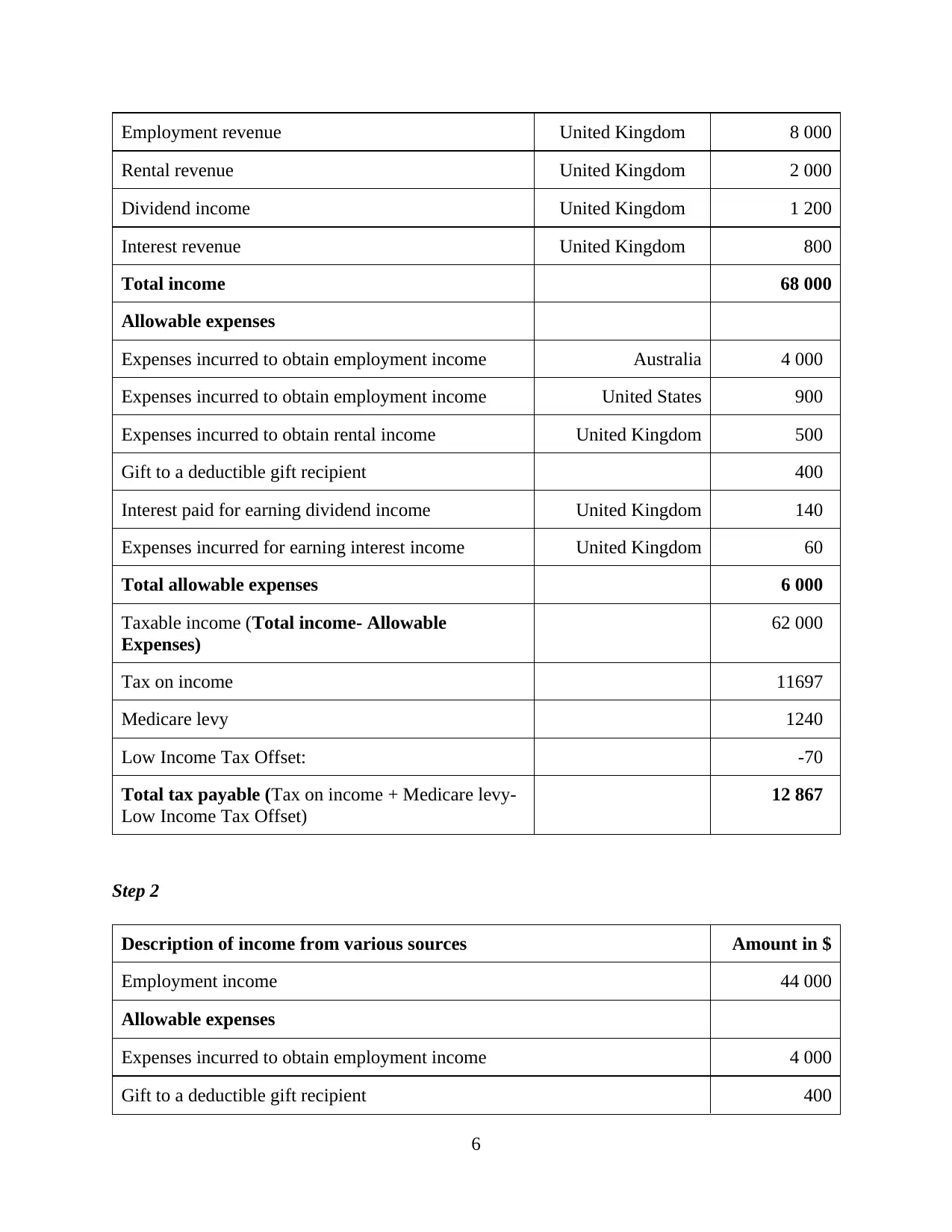

Employment revenue United Kingdom 8 000

Rental revenue United Kingdom 2 000

Dividend income United Kingdom 1 200

Interest revenue United Kingdom 800

Total income 68 000

Allowable expenses

Expenses incurred to obtain employment income Australia 4 000

Expenses incurred to obtain employment income United States 900

Expenses incurred to obtain rental income United Kingdom 500

Gift to a deductible gift recipient 400

Interest paid for earning dividend income United Kingdom 140

Expenses incurred for earning interest income United Kingdom 60

Total allowable expenses 6 000

Taxable income (Total income- Allowable

Expenses)

62 000

Tax on income 11697

Medicare levy 1240

Low Income Tax Offset: -70

Total tax payable (Tax on income + Medicare levy-

Low Income Tax Offset)

12 867

Step 2

Description of income from various sources Amount in $

Employment income 44 000

Allowable expenses

Expenses incurred to obtain employment income 4 000

Gift to a deductible gift recipient 400

6

Rental revenue United Kingdom 2 000

Dividend income United Kingdom 1 200

Interest revenue United Kingdom 800

Total income 68 000

Allowable expenses

Expenses incurred to obtain employment income Australia 4 000

Expenses incurred to obtain employment income United States 900

Expenses incurred to obtain rental income United Kingdom 500

Gift to a deductible gift recipient 400

Interest paid for earning dividend income United Kingdom 140

Expenses incurred for earning interest income United Kingdom 60

Total allowable expenses 6 000

Taxable income (Total income- Allowable

Expenses)

62 000

Tax on income 11697

Medicare levy 1240

Low Income Tax Offset: -70

Total tax payable (Tax on income + Medicare levy-

Low Income Tax Offset)

12 867

Step 2

Description of income from various sources Amount in $

Employment income 44 000

Allowable expenses

Expenses incurred to obtain employment income 4 000

Gift to a deductible gift recipient 400

6

Interest paid for earning dividend income 140

Expenses incurred for earning interest income 60

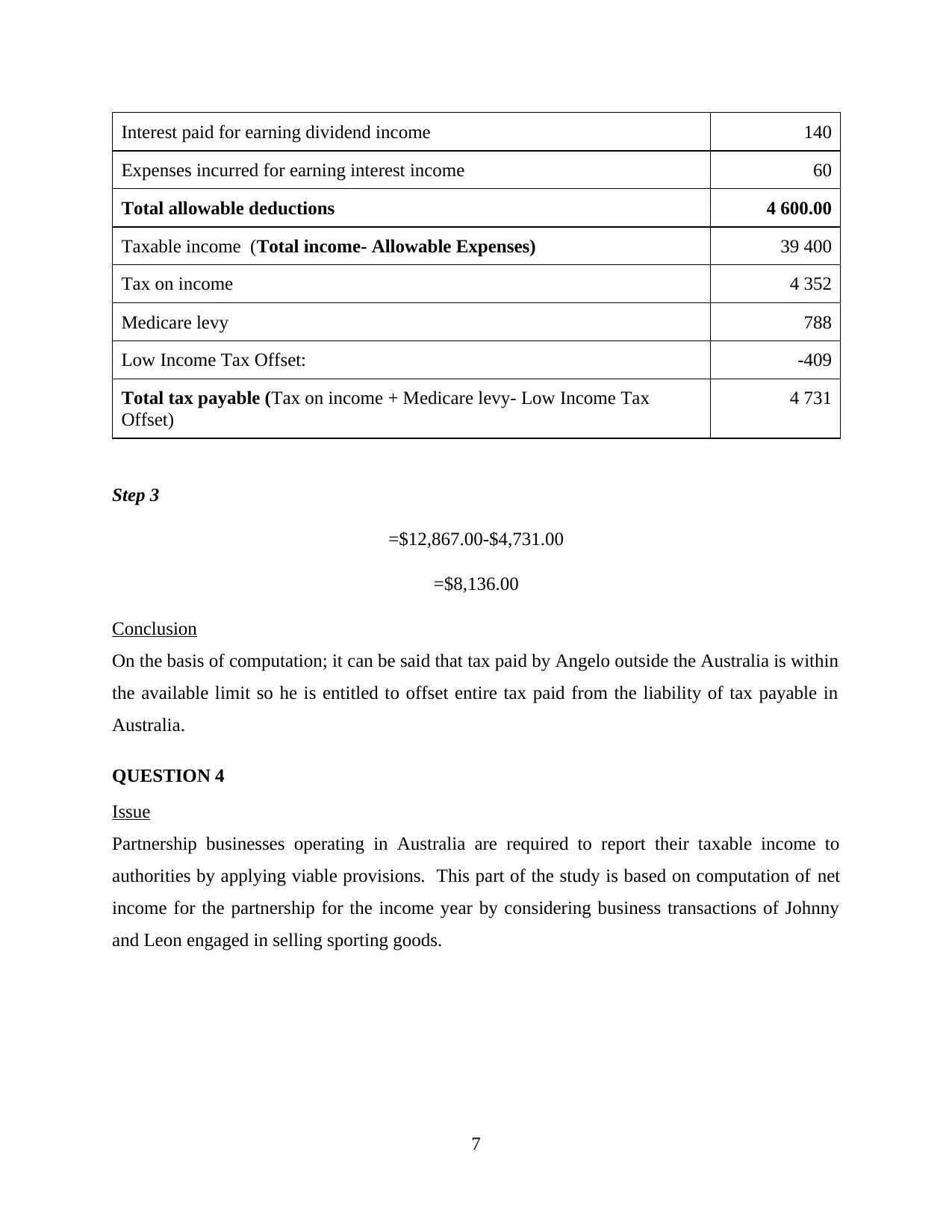

Total allowable deductions 4 600.00

Taxable income (Total income- Allowable Expenses) 39 400

Tax on income 4 352

Medicare levy 788

Low Income Tax Offset: -409

Total tax payable (Tax on income + Medicare levy- Low Income Tax

Offset)

4 731

Step 3

=$12,867.00-$4,731.00

=$8,136.00

Conclusion

On the basis of computation; it can be said that tax paid by Angelo outside the Australia is within

the available limit so he is entitled to offset entire tax paid from the liability of tax payable in

Australia.

QUESTION 4

Issue

Partnership businesses operating in Australia are required to report their taxable income to

authorities by applying viable provisions. This part of the study is based on computation of net

income for the partnership for the income year by considering business transactions of Johnny

and Leon engaged in selling sporting goods.

7

Expenses incurred for earning interest income 60

Total allowable deductions 4 600.00

Taxable income (Total income- Allowable Expenses) 39 400

Tax on income 4 352

Medicare levy 788

Low Income Tax Offset: -409

Total tax payable (Tax on income + Medicare levy- Low Income Tax

Offset)

4 731

Step 3

=$12,867.00-$4,731.00

=$8,136.00

Conclusion

On the basis of computation; it can be said that tax paid by Angelo outside the Australia is within

the available limit so he is entitled to offset entire tax paid from the liability of tax payable in

Australia.

QUESTION 4

Issue

Partnership businesses operating in Australia are required to report their taxable income to

authorities by applying viable provisions. This part of the study is based on computation of net

income for the partnership for the income year by considering business transactions of Johnny

and Leon engaged in selling sporting goods.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

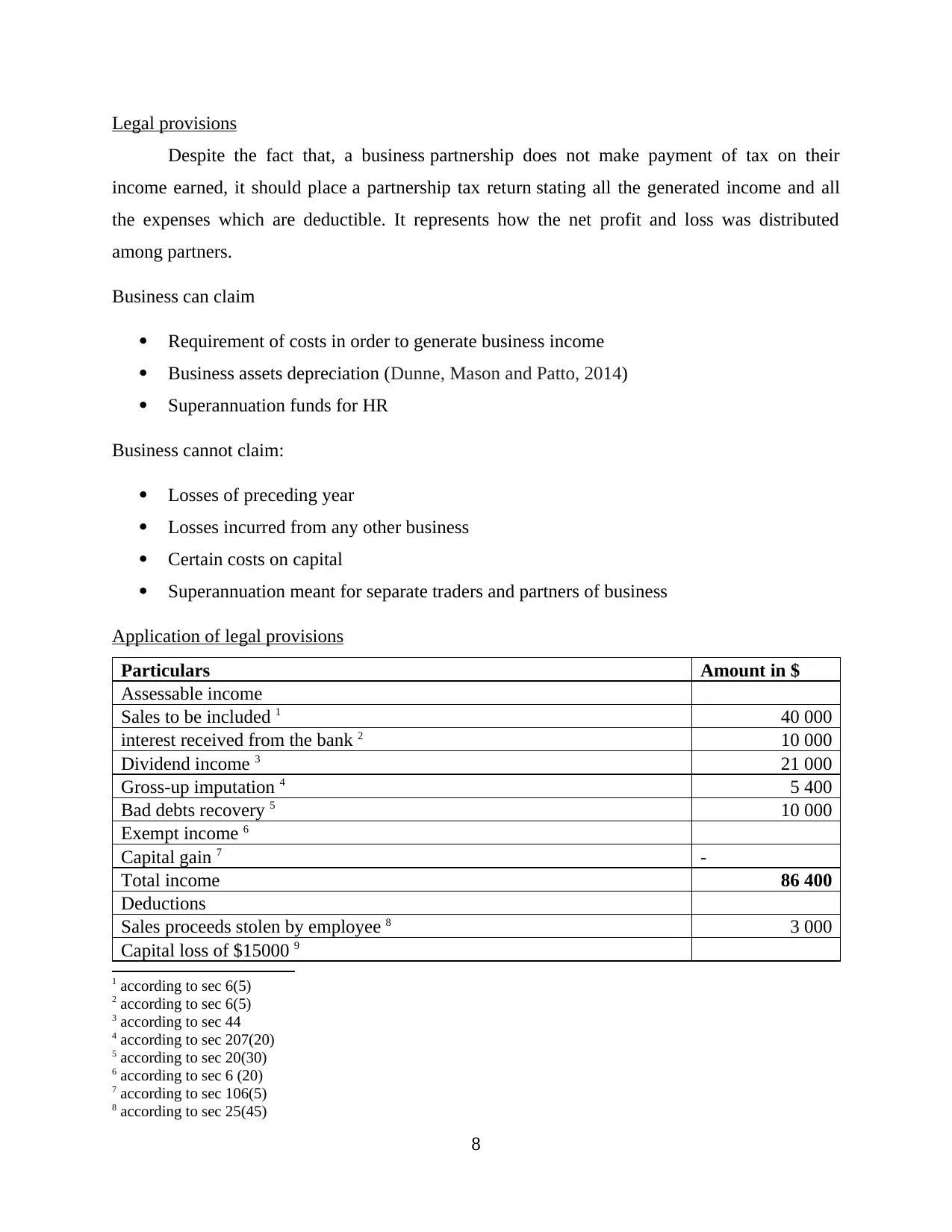

Legal provisions

Despite the fact that, a business partnership does not make payment of tax on their

income earned, it should place a partnership tax return stating all the generated income and all

the expenses which are deductible. It represents how the net profit and loss was distributed

among partners.

Business can claim

Requirement of costs in order to generate business income

Business assets depreciation (Dunne, Mason and Patto, 2014)

Superannuation funds for HR

Business cannot claim:

Losses of preceding year

Losses incurred from any other business

Certain costs on capital

Superannuation meant for separate traders and partners of business

Application of legal provisions

Particulars Amount in $

Assessable income

Sales to be included 1 40 000

interest received from the bank 2 10 000

Dividend income 3 21 000

Gross-up imputation 4 5 400

Bad debts recovery 5 10 000

Exempt income 6

Capital gain 7 -

Total income 86 400

Deductions

Sales proceeds stolen by employee 8 3 000

Capital loss of $15000 9

1 according to sec 6(5)

2 according to sec 6(5)

3 according to sec 44

4 according to sec 207(20)

5 according to sec 20(30)

6 according to sec 6 (20)

7 according to sec 106(5)

8 according to sec 25(45)

8

Despite the fact that, a business partnership does not make payment of tax on their

income earned, it should place a partnership tax return stating all the generated income and all

the expenses which are deductible. It represents how the net profit and loss was distributed

among partners.

Business can claim

Requirement of costs in order to generate business income

Business assets depreciation (Dunne, Mason and Patto, 2014)

Superannuation funds for HR

Business cannot claim:

Losses of preceding year

Losses incurred from any other business

Certain costs on capital

Superannuation meant for separate traders and partners of business

Application of legal provisions

Particulars Amount in $

Assessable income

Sales to be included 1 40 000

interest received from the bank 2 10 000

Dividend income 3 21 000

Gross-up imputation 4 5 400

Bad debts recovery 5 10 000

Exempt income 6

Capital gain 7 -

Total income 86 400

Deductions

Sales proceeds stolen by employee 8 3 000

Capital loss of $15000 9

1 according to sec 6(5)

2 according to sec 6(5)

3 according to sec 44

4 according to sec 207(20)

5 according to sec 20(30)

6 according to sec 6 (20)

7 according to sec 106(5)

8 according to sec 25(45)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Salary to Johny and Leon

Fringe benefit tax 10 16 000

Interest on loan given by Johnny to the business 11 4 000

Interest on capital provided by Johnny 12

Travelling expenses of Johnny from home to work and return 3 000

Legal fees for the renewal of lease of the office building 2 000

Legal expenses regarding formation of a partnership agreement 1 200

Legal expenses for regarding formation new lease of business premises 700

Debt collection expenses paid to a solicitor 500

Council rates on business premises 500

Staff salaries 13 20 000

Purchase of sporting goods supplies 30 000

Rent on retail shop 20 000

Provision for doubtful debts 14

Business lunches 100 000

Total deductible expenses 110 900

Taxable Loss (Total income - Total deductible expenses) $25,500

Conclusion

By considering above computation it can be noticed that there is net loss to business however

same cannot be claimed by business in future as per described provisions.

9 according to sec 8(1)

10 note 1 Salary of partners is disallowed as it is the mere distribution of profit.

11 note 2 as per provisions of fringe benefits tax expenses of tax paid is allowable to partners

12 note 3 Loan is use for commercial purpose thus interest will be allowed

13 according to QC33728

14 according to sec (63)

9

Fringe benefit tax 10 16 000

Interest on loan given by Johnny to the business 11 4 000

Interest on capital provided by Johnny 12

Travelling expenses of Johnny from home to work and return 3 000

Legal fees for the renewal of lease of the office building 2 000

Legal expenses regarding formation of a partnership agreement 1 200

Legal expenses for regarding formation new lease of business premises 700

Debt collection expenses paid to a solicitor 500

Council rates on business premises 500

Staff salaries 13 20 000

Purchase of sporting goods supplies 30 000

Rent on retail shop 20 000

Provision for doubtful debts 14

Business lunches 100 000

Total deductible expenses 110 900

Taxable Loss (Total income - Total deductible expenses) $25,500

Conclusion

By considering above computation it can be noticed that there is net loss to business however

same cannot be claimed by business in future as per described provisions.

9 according to sec 8(1)

10 note 1 Salary of partners is disallowed as it is the mere distribution of profit.

11 note 2 as per provisions of fringe benefits tax expenses of tax paid is allowable to partners

12 note 3 Loan is use for commercial purpose thus interest will be allowed

13 according to QC33728

14 according to sec (63)

9

REFERENCES

Blacklow, P., Nicholas, A. and Ray, R., 2010. Demographic demand systems with application to

equivalence scales estimation and inequality analysis: The Australian evidence. Australian

Economic Papers, 49(3), pp.161-179.

Braithwaite, V., 2007. Responsive regulation and taxation: Introduction. Law & Policy, 29(1),

pp.3-10.

Bugeja, M. and da Silva Rosa, R., 2008. Taxation of shareholder capital gains and the choice of

payment method in takeovers. Accounting and Business Research, 38(4), pp.331-350.

D'Ascenzo, M. and England, A., 2005. The Tax and Accounting Interface. J. Australasian Tax

Tchrs. Ass'n, 1, p.24.

Dunne, J., Mason, J. and Patto, J., 2014. 2013 cases show high ATO success rate. Taxation in

Australia, 48(8), p.429.

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part 2. Taxation in

Australia, 51(1), p.12.

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning: Accounting and

taxation law perspectives of carbon permits. Critical Perspectives on Accounting, 21(7), pp.619-

630.

Rainey, S., 2013. The Law of Tug and Tow and Offshore Contracts. CRC Press.

Schwenzer, I., Hachem, P. and Kee, C., 2012. Global sales and contract law. Oxford University

Press.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2011. Australian Taxation Law

Select: legislation and commentary. CCH Australia.

10

Blacklow, P., Nicholas, A. and Ray, R., 2010. Demographic demand systems with application to

equivalence scales estimation and inequality analysis: The Australian evidence. Australian

Economic Papers, 49(3), pp.161-179.

Braithwaite, V., 2007. Responsive regulation and taxation: Introduction. Law & Policy, 29(1),

pp.3-10.

Bugeja, M. and da Silva Rosa, R., 2008. Taxation of shareholder capital gains and the choice of

payment method in takeovers. Accounting and Business Research, 38(4), pp.331-350.

D'Ascenzo, M. and England, A., 2005. The Tax and Accounting Interface. J. Australasian Tax

Tchrs. Ass'n, 1, p.24.

Dunne, J., Mason, J. and Patto, J., 2014. 2013 cases show high ATO success rate. Taxation in

Australia, 48(8), p.429.

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part 2. Taxation in

Australia, 51(1), p.12.

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning: Accounting and

taxation law perspectives of carbon permits. Critical Perspectives on Accounting, 21(7), pp.619-

630.

Rainey, S., 2013. The Law of Tug and Tow and Offshore Contracts. CRC Press.

Schwenzer, I., Hachem, P. and Kee, C., 2012. Global sales and contract law. Oxford University

Press.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2011. Australian Taxation Law

Select: legislation and commentary. CCH Australia.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.