Taxation Law HA3042: Personal Exertion Income Analysis - T1 2018

VerifiedAdded on 2023/06/11

|13

|3143

|345

Homework Assignment

AI Summary

This assignment provides solutions to taxation law questions, focusing on income from personal exertion, assessable ordinary income, and capital gains tax (CGT). It analyzes scenarios involving a mountain climber's income from media rights and manuscript sales, interest earned on a loan, and the CGT implications of selling a property. The solutions reference relevant sections of the ITAA 1997 and relevant case law to determine tax liabilities. The document is available on Desklib, a platform that provides students with access to past papers and solved assignments.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to 1:...............................................................................................................................2

Issue:..........................................................................................................................................2

Laws:..........................................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................5

Answer to 2:...............................................................................................................................5

Answer to 3:...............................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................7

Answer 4:...................................................................................................................................7

Answer to question 4 A:.............................................................................................................7

Answer to 4 B:...........................................................................................................................9

Answer to 4 C:...........................................................................................................................9

Reference List:.........................................................................................................................11

Table of Contents

Answer to 1:...............................................................................................................................2

Issue:..........................................................................................................................................2

Laws:..........................................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................5

Answer to 2:...............................................................................................................................5

Answer to 3:...............................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................7

Answer 4:...................................................................................................................................7

Answer to question 4 A:.............................................................................................................7

Answer to 4 B:...........................................................................................................................9

Answer to 4 C:...........................................................................................................................9

Reference List:.........................................................................................................................11

2TAXATION LAW

Answer to 1:

Issue:

Will the taxpayer be held liable for taxation under “section 6-5 of the ITAA 1997” for

receiving the money from the media newspaper.?

Laws:

a. “Section 6-5 of the ITAA 1997”

b. “British Columbia v Ostrum (1904)”

c. “Kelly v Federal Commissioner of Taxation”

d. “Section 995-1 (1) of the ITAA 1997”

e. “Brent v Federal Commissioner of Taxation (1971)”

f. “Housden (Inspector of Taxation) v Marshall (1942)”

Applications:

For an ordinary income to for the part of the taxpayer’s assessable income during the

particular year under “section 6-5 of the ITAA 1997” it should be derived must be derived by

the taxpayer in the relevant year (Clarke, 2017). In order to consider the receipts as personal

exertion it must be produced from the employment or services rendered there must be a

sufficient connection with the activities. The court of Law in “British Columbia v Ostrum

(1904)” stated that the receipts that are produced through the employment or through the

services rendered is held as income (Stewart, 2017).

The court of law in “Kelly v Federal Commissioner of Taxation” further provides

that there is should be existence of sufficient connection between the receipts that is obtained

from the direct or the indirect sources (Peiros & Smyth, 2017). For an income to be classified

as the ordinary income usually connection to the employment or the services rendered is held

Answer to 1:

Issue:

Will the taxpayer be held liable for taxation under “section 6-5 of the ITAA 1997” for

receiving the money from the media newspaper.?

Laws:

a. “Section 6-5 of the ITAA 1997”

b. “British Columbia v Ostrum (1904)”

c. “Kelly v Federal Commissioner of Taxation”

d. “Section 995-1 (1) of the ITAA 1997”

e. “Brent v Federal Commissioner of Taxation (1971)”

f. “Housden (Inspector of Taxation) v Marshall (1942)”

Applications:

For an ordinary income to for the part of the taxpayer’s assessable income during the

particular year under “section 6-5 of the ITAA 1997” it should be derived must be derived by

the taxpayer in the relevant year (Clarke, 2017). In order to consider the receipts as personal

exertion it must be produced from the employment or services rendered there must be a

sufficient connection with the activities. The court of Law in “British Columbia v Ostrum

(1904)” stated that the receipts that are produced through the employment or through the

services rendered is held as income (Stewart, 2017).

The court of law in “Kelly v Federal Commissioner of Taxation” further provides

that there is should be existence of sufficient connection between the receipts that is obtained

from the direct or the indirect sources (Peiros & Smyth, 2017). For an income to be classified

as the ordinary income usually connection to the employment or the services rendered is held

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

as the most important factor that is associated with the revenue generating activities. The

private exertion income generally comprises of the fees, wages, salaries or any form of

business receipts.

The study here revolves around in understanding that private exertion income that is

derived by Hilary in the relevant year. Hilary evidently was the mountain climber. On one

occasion Hilary was approached by the Daily Terror that was the newspaper company who

expressed the interest in knowing the Hilary’s life story. Hilary was required to provide

service by writing the book and title into the book that was written by Hilary would remain

vested in the hands of the Daily Newspaper.

Consequently, under the “section 6-5 of the ITA Act 1997” provides an explanation

that taxpayers receiving money from the for an exclusive media interview of a life story is

considered taxable (Buchanan & Consett, 2016). The agreement that are signed by the

taxpayer before such media rights and the sum of money that are paid are taxable in the hands

of recipients. All the rights, title and interest including the copyright in the interview are

exclusively within the ownership of the media channel. The term derived has been defined

under “section 995-1 (1) of the ITAA 1997” which is only within the meaning affected under

“section 6-5 (4) of the ITAA 1997” (Jones, 2017). The personal services that are rendered by

the taxpayer are considered for assessment. In “Brent v Federal Commissioner of Taxation

(1971)” generally the receipts from the personal service income are considered for taxable

purpose.

The case study provides that Hilary received a payment of $10,000 which should be

classified as receipt from personal exertion. This is because Hilary was required to render the

service in order to obtain income. The amount that was provided to the Hilary by the

Newspaper was reward for service which is generally taxable as the ordinary income under

as the most important factor that is associated with the revenue generating activities. The

private exertion income generally comprises of the fees, wages, salaries or any form of

business receipts.

The study here revolves around in understanding that private exertion income that is

derived by Hilary in the relevant year. Hilary evidently was the mountain climber. On one

occasion Hilary was approached by the Daily Terror that was the newspaper company who

expressed the interest in knowing the Hilary’s life story. Hilary was required to provide

service by writing the book and title into the book that was written by Hilary would remain

vested in the hands of the Daily Newspaper.

Consequently, under the “section 6-5 of the ITA Act 1997” provides an explanation

that taxpayers receiving money from the for an exclusive media interview of a life story is

considered taxable (Buchanan & Consett, 2016). The agreement that are signed by the

taxpayer before such media rights and the sum of money that are paid are taxable in the hands

of recipients. All the rights, title and interest including the copyright in the interview are

exclusively within the ownership of the media channel. The term derived has been defined

under “section 995-1 (1) of the ITAA 1997” which is only within the meaning affected under

“section 6-5 (4) of the ITAA 1997” (Jones, 2017). The personal services that are rendered by

the taxpayer are considered for assessment. In “Brent v Federal Commissioner of Taxation

(1971)” generally the receipts from the personal service income are considered for taxable

purpose.

The case study provides that Hilary received a payment of $10,000 which should be

classified as receipt from personal exertion. This is because Hilary was required to render the

service in order to obtain income. The amount that was provided to the Hilary by the

Newspaper was reward for service which is generally taxable as the ordinary income under

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

“section 6-5 of the ITAA 1997”. The amount would be included into the Hilary taxable

income would be considered for assessment.

Latter events that unfolds in the case study provides that Hilary on one occasion sells

the manuscript to the library for $5,000. There were several photographs that was taken by

Hilary when she was climbing the mountain. The photographs were sold by Hilary and she

received $2,000. The amount of $5,000 and $2,000 should be viewed as the ordinary income

and should be included into the taxable income of Hilary. With reference to “section 6-5 of

the ITAA 1997” the amount that was received from selling was derived by the taxpayer in the

relevant income year (Krever & Mellor, 2016). Referring to the case of “Housden (Inspector

of Taxation) v Marshall (1942)” where an agreement was made by the taxpayer where he

would be making all the experience available as the Jockey that included the sale of the

newspaper cuttings and photographs.

Preceding the explanation from the above cited case it can be stated that the selling of

the photographs and manuscripts to the library would be treated as income that is derived

from the sale and was having the appropriate connection with the activities of Hilary.

An alternative situation that is faced with the case of Hilary is understanding the tax

consequences upon the event if the book was written by taxpayer for personal purpose and

then selling those books in the market. It is worth mentioning the judgement of the taxation

commissioner in “Hobbs v Hussey (1942)” provided that taxpayer had apparently been the

criminal and obtained an amount by selling the rights for his autobiography to the newspaper

media that was published (Black, 2017). Similarly, in the above considered situation is

applicable in the case of Hilary to determine the nature of receipts. The sale of book and

receipts will be considered as the royalty in the event of Hilary. These receipts should be

treated as income under “section 6-5 of the ITAA 1997” within the ordinary concepts.

“section 6-5 of the ITAA 1997”. The amount would be included into the Hilary taxable

income would be considered for assessment.

Latter events that unfolds in the case study provides that Hilary on one occasion sells

the manuscript to the library for $5,000. There were several photographs that was taken by

Hilary when she was climbing the mountain. The photographs were sold by Hilary and she

received $2,000. The amount of $5,000 and $2,000 should be viewed as the ordinary income

and should be included into the taxable income of Hilary. With reference to “section 6-5 of

the ITAA 1997” the amount that was received from selling was derived by the taxpayer in the

relevant income year (Krever & Mellor, 2016). Referring to the case of “Housden (Inspector

of Taxation) v Marshall (1942)” where an agreement was made by the taxpayer where he

would be making all the experience available as the Jockey that included the sale of the

newspaper cuttings and photographs.

Preceding the explanation from the above cited case it can be stated that the selling of

the photographs and manuscripts to the library would be treated as income that is derived

from the sale and was having the appropriate connection with the activities of Hilary.

An alternative situation that is faced with the case of Hilary is understanding the tax

consequences upon the event if the book was written by taxpayer for personal purpose and

then selling those books in the market. It is worth mentioning the judgement of the taxation

commissioner in “Hobbs v Hussey (1942)” provided that taxpayer had apparently been the

criminal and obtained an amount by selling the rights for his autobiography to the newspaper

media that was published (Black, 2017). Similarly, in the above considered situation is

applicable in the case of Hilary to determine the nature of receipts. The sale of book and

receipts will be considered as the royalty in the event of Hilary. These receipts should be

treated as income under “section 6-5 of the ITAA 1997” within the ordinary concepts.

5TAXATION LAW

Conclusion:

Taking into the consideration the above stated analysis it can be stated that the

information provided as the result of exclusive media rights by Hilary would be considered as

the assessable income since it constituted personal service income. The income should be

classified as the personal exertion income and should be considered for taxation under the

ordinary concepts of “section 6-5 of the ITAA 1997”. On the other hand, selling the

manuscripts and photographs constitutes income from personal exertion and taxable as the

ordinary income under “section 6-5 of the ITAA 1997”.

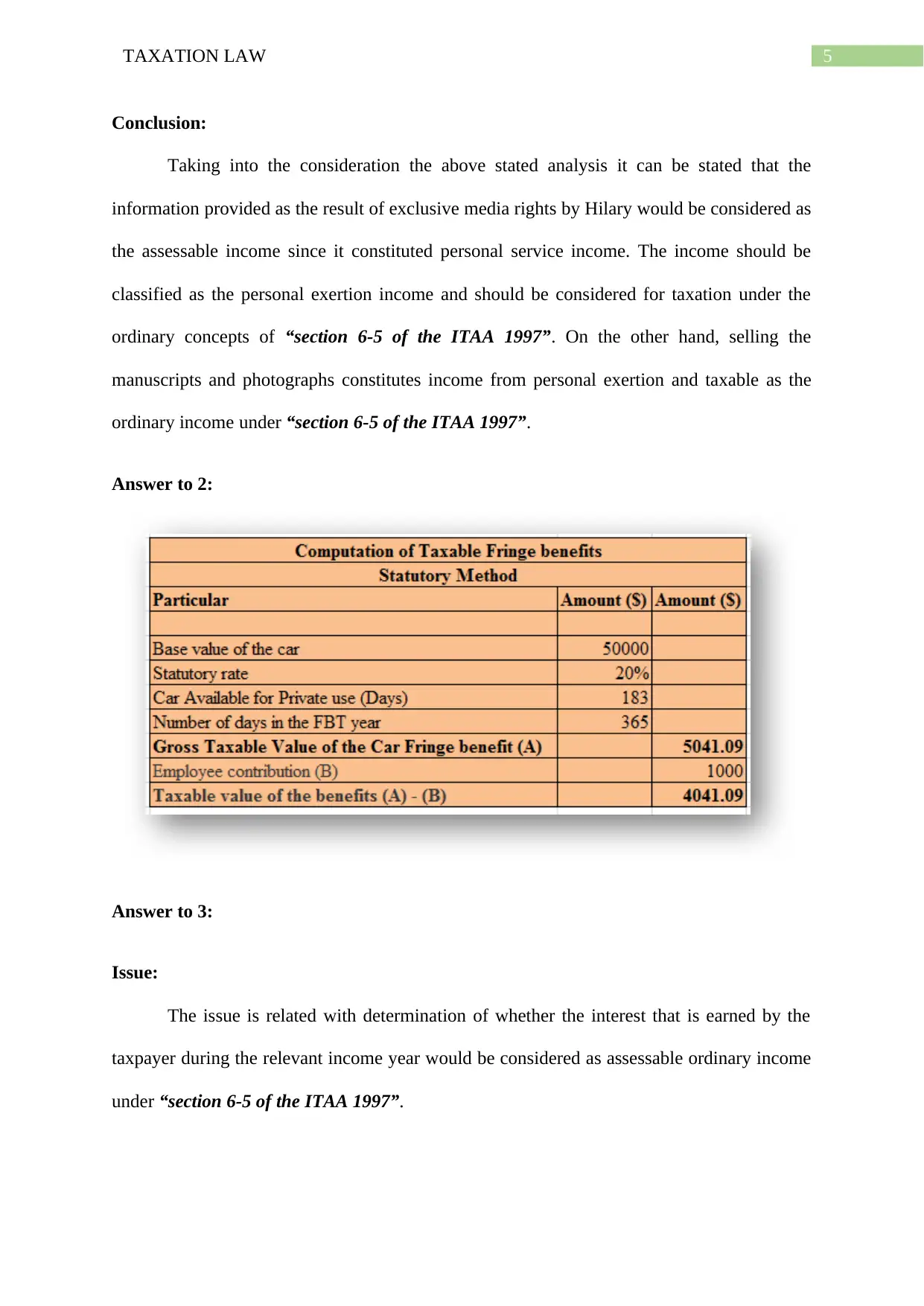

Answer to 2:

Answer to 3:

Issue:

The issue is related with determination of whether the interest that is earned by the

taxpayer during the relevant income year would be considered as assessable ordinary income

under “section 6-5 of the ITAA 1997”.

Conclusion:

Taking into the consideration the above stated analysis it can be stated that the

information provided as the result of exclusive media rights by Hilary would be considered as

the assessable income since it constituted personal service income. The income should be

classified as the personal exertion income and should be considered for taxation under the

ordinary concepts of “section 6-5 of the ITAA 1997”. On the other hand, selling the

manuscripts and photographs constitutes income from personal exertion and taxable as the

ordinary income under “section 6-5 of the ITAA 1997”.

Answer to 2:

Answer to 3:

Issue:

The issue is related with determination of whether the interest that is earned by the

taxpayer during the relevant income year would be considered as assessable ordinary income

under “section 6-5 of the ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Laws: “Section 6-5 of the ITAA 1997”

“Scott v Commissioner of taxation (1935)”

“FCT v McNeil (2007)”

Applications:

Interest are generally received, unless in the interest of lending money or the interest

payment that is associated with the part of the business activities. These interest are

considered as income when the taxpayers earns those incomes either as the gain or derived

beneficially. Referring to the “section 6-5 of the ITAA 1997” ordinary income is those

incomes that comes into the taxpayer in the form of the ordinary income (Marriott, 2016).

Receipts are considered as the income and should be treated in compliance with the ordinary

concepts of “section 6-5 of the ITAA 1997”. Accordingly, in the case of “Scott v

Commissioner of taxation (1935)” receipts must be treated as ordinary income under the

ordinary concepts.

It is worth mentioning that an element carrying the nature of income is regarded as

income snice it is home coming for the taxpayer. An item of having the character of income

has been derived when it carries the realisable value (Joseph et al., 2015). It is necessary for

the taxpayer to judge the character of income in the circumstances when it is derived by the

taxpayer. In order to have the income nature an amount that is derived by the taxpayer should

be a gain.

As understood in the situations of “FCT v McNeil (2007)” the judgement explained

that income should be judged based on the circumstances of the derivation by the taxpayer

(Saez, 2014). The case study explains that the taxpayer made loan to the son for the purpose

of short term finance. The agreement of the loan provided that the son would repay the loan

Laws: “Section 6-5 of the ITAA 1997”

“Scott v Commissioner of taxation (1935)”

“FCT v McNeil (2007)”

Applications:

Interest are generally received, unless in the interest of lending money or the interest

payment that is associated with the part of the business activities. These interest are

considered as income when the taxpayers earns those incomes either as the gain or derived

beneficially. Referring to the “section 6-5 of the ITAA 1997” ordinary income is those

incomes that comes into the taxpayer in the form of the ordinary income (Marriott, 2016).

Receipts are considered as the income and should be treated in compliance with the ordinary

concepts of “section 6-5 of the ITAA 1997”. Accordingly, in the case of “Scott v

Commissioner of taxation (1935)” receipts must be treated as ordinary income under the

ordinary concepts.

It is worth mentioning that an element carrying the nature of income is regarded as

income snice it is home coming for the taxpayer. An item of having the character of income

has been derived when it carries the realisable value (Joseph et al., 2015). It is necessary for

the taxpayer to judge the character of income in the circumstances when it is derived by the

taxpayer. In order to have the income nature an amount that is derived by the taxpayer should

be a gain.

As understood in the situations of “FCT v McNeil (2007)” the judgement explained

that income should be judged based on the circumstances of the derivation by the taxpayer

(Saez, 2014). The case study explains that the taxpayer made loan to the son for the purpose

of short term finance. The agreement of the loan provided that the son would repay the loan

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

amount by within five years. However, it was noticed that the son within the span of two

years repaid the principle loan amount and also paid the interest amount.

The interest that was received by the taxpayer constituted income based on the

ordinary concepts of section 6-5 since it carried the characteristics of home coming for the

parent. Referring to “FCT v McNeil (2007)” the receipt of interest from loan carries the

character of income which attracts tax liability (Sharkey, 2015). The amount would be

included into the taxpayer’s assessable income as the chargeable income however, the parent

is not required to include the loan principle since it is regarded as the income since it carries

the element of gain for the parent.

Conclusion:

The amount of interest received would be included into the taxpayer’s assessable

income as the chargeable income under “section 6-5 of the ITAA 1997” on the basis of the

ordinary concepts.

Answer 4:

Answer to question 4 A:

According to the “section 102-5 of the ITA Act 1997” provides that an individual is

required to include into their tax return the net amount of the capital gains during the income

year into their taxable income (Richardson, 2016). The capital gains tax is applicable only on

the assets that are acquired on after the 20 September 1985. “Section 110-25 of the ITAA

1995” provides the cost base of the property (Klein, 2016). However, “section 110-35 of the

ITAA 1997” provides that the cost base of the property is also includes the incidental costs.

According to the “section 108-5 of the ITAA 1997” an explanation of the CGT assets has

been provided. The CGT assets includes any form of property or any form of legal or the

amount by within five years. However, it was noticed that the son within the span of two

years repaid the principle loan amount and also paid the interest amount.

The interest that was received by the taxpayer constituted income based on the

ordinary concepts of section 6-5 since it carried the characteristics of home coming for the

parent. Referring to “FCT v McNeil (2007)” the receipt of interest from loan carries the

character of income which attracts tax liability (Sharkey, 2015). The amount would be

included into the taxpayer’s assessable income as the chargeable income however, the parent

is not required to include the loan principle since it is regarded as the income since it carries

the element of gain for the parent.

Conclusion:

The amount of interest received would be included into the taxpayer’s assessable

income as the chargeable income under “section 6-5 of the ITAA 1997” on the basis of the

ordinary concepts.

Answer 4:

Answer to question 4 A:

According to the “section 102-5 of the ITA Act 1997” provides that an individual is

required to include into their tax return the net amount of the capital gains during the income

year into their taxable income (Richardson, 2016). The capital gains tax is applicable only on

the assets that are acquired on after the 20 September 1985. “Section 110-25 of the ITAA

1995” provides the cost base of the property (Klein, 2016). However, “section 110-35 of the

ITAA 1997” provides that the cost base of the property is also includes the incidental costs.

According to the “section 108-5 of the ITAA 1997” an explanation of the CGT assets has

been provided. The CGT assets includes any form of property or any form of legal or the

8TAXATION LAW

equitable rights. The first and the foremost step in understanding the transaction or the event

that is subjected to the CGT is to assess whether the CGT event has taken place.

Assets that are acquired prior to the introduction of the capital gains tax will be

exempted from the capital gains tax (Cao et al., 2015). The current situation provides that the

Scott was the owner of the vacant land that was purchased by him prior to the introduction of

the CGT. However, Scott started construction the land after the introduction of CGT

(Lombard, 2017). The house was built on 1st September 1986 and as a result it would

classified as the CGT asset based on the “section 105-55 (2) of the ITAA 1997”.

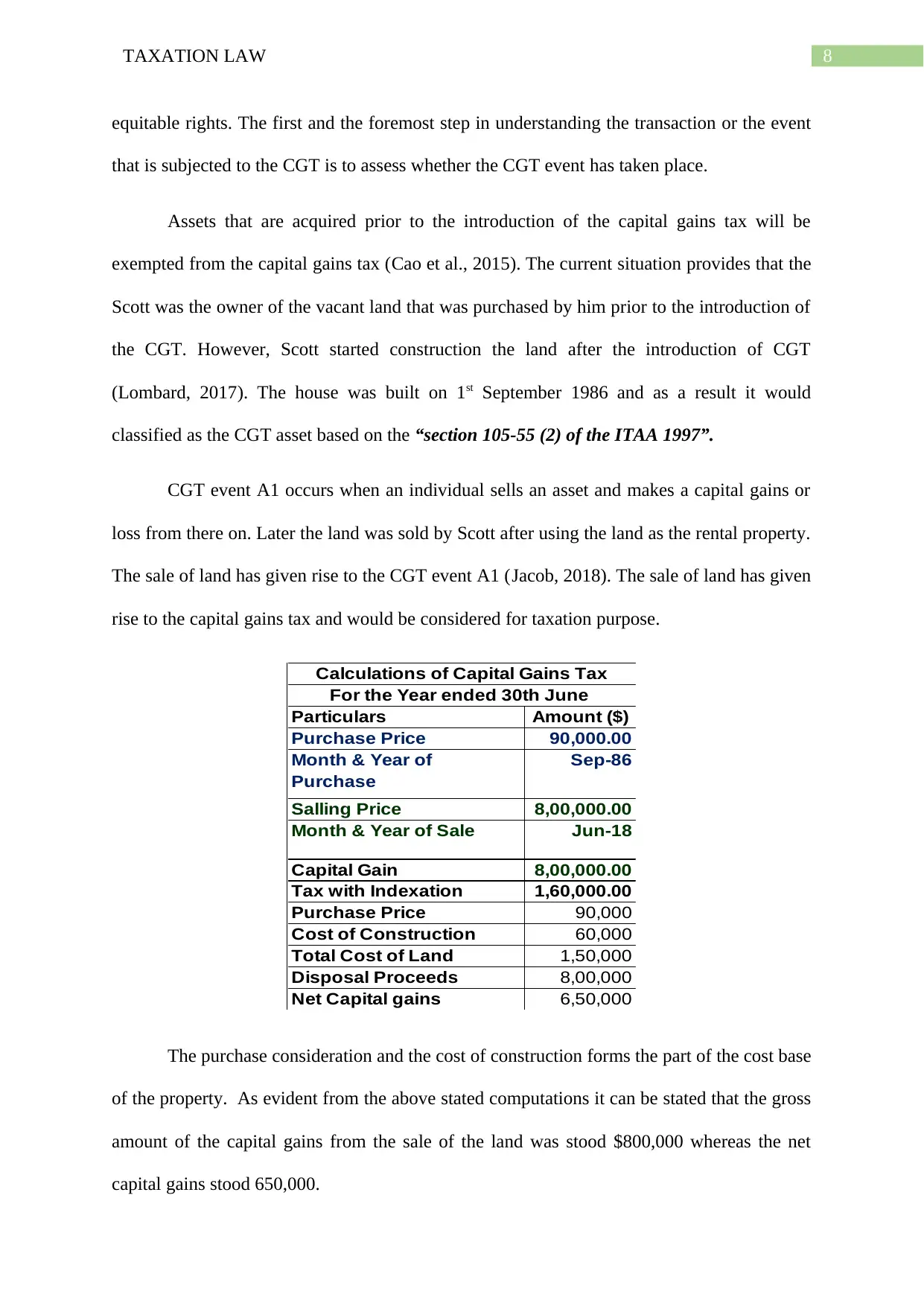

CGT event A1 occurs when an individual sells an asset and makes a capital gains or

loss from there on. Later the land was sold by Scott after using the land as the rental property.

The sale of land has given rise to the CGT event A1 (Jacob, 2018). The sale of land has given

rise to the capital gains tax and would be considered for taxation purpose.

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of

Purchase

Sep-86

Salling Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Tax with Indexation 1,60,000.00

Purchase Price 90,000

Cost of Construction 60,000

Total Cost of Land 1,50,000

Disposal Proceeds 8,00,000

Net Capital gains 6,50,000

Calculations of Capital Gains Tax

For the Year ended 30th June

The purchase consideration and the cost of construction forms the part of the cost base

of the property. As evident from the above stated computations it can be stated that the gross

amount of the capital gains from the sale of the land was stood $800,000 whereas the net

capital gains stood 650,000.

equitable rights. The first and the foremost step in understanding the transaction or the event

that is subjected to the CGT is to assess whether the CGT event has taken place.

Assets that are acquired prior to the introduction of the capital gains tax will be

exempted from the capital gains tax (Cao et al., 2015). The current situation provides that the

Scott was the owner of the vacant land that was purchased by him prior to the introduction of

the CGT. However, Scott started construction the land after the introduction of CGT

(Lombard, 2017). The house was built on 1st September 1986 and as a result it would

classified as the CGT asset based on the “section 105-55 (2) of the ITAA 1997”.

CGT event A1 occurs when an individual sells an asset and makes a capital gains or

loss from there on. Later the land was sold by Scott after using the land as the rental property.

The sale of land has given rise to the CGT event A1 (Jacob, 2018). The sale of land has given

rise to the capital gains tax and would be considered for taxation purpose.

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of

Purchase

Sep-86

Salling Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Tax with Indexation 1,60,000.00

Purchase Price 90,000

Cost of Construction 60,000

Total Cost of Land 1,50,000

Disposal Proceeds 8,00,000

Net Capital gains 6,50,000

Calculations of Capital Gains Tax

For the Year ended 30th June

The purchase consideration and the cost of construction forms the part of the cost base

of the property. As evident from the above stated computations it can be stated that the gross

amount of the capital gains from the sale of the land was stood $800,000 whereas the net

capital gains stood 650,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

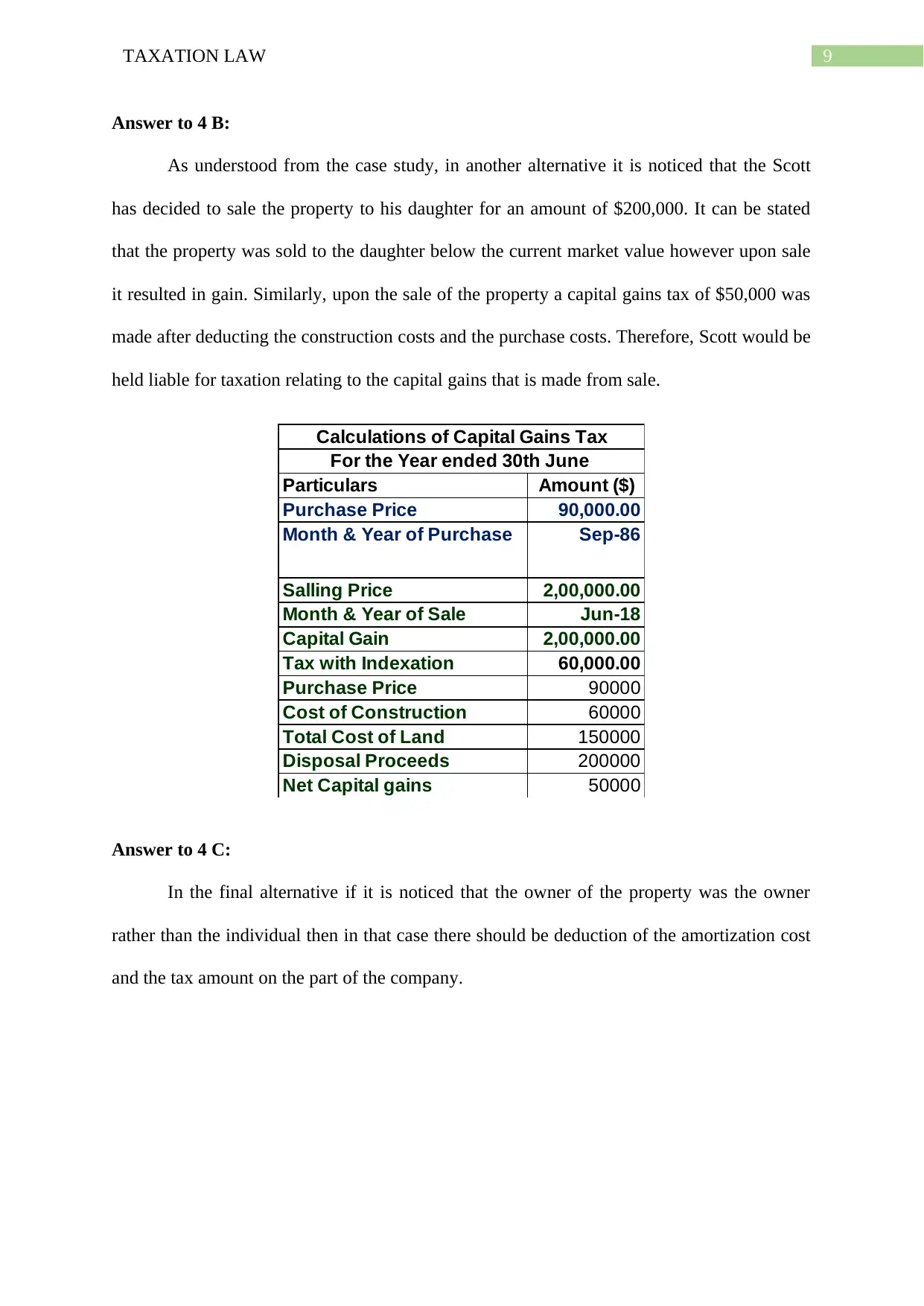

Answer to 4 B:

As understood from the case study, in another alternative it is noticed that the Scott

has decided to sale the property to his daughter for an amount of $200,000. It can be stated

that the property was sold to the daughter below the current market value however upon sale

it resulted in gain. Similarly, upon the sale of the property a capital gains tax of $50,000 was

made after deducting the construction costs and the purchase costs. Therefore, Scott would be

held liable for taxation relating to the capital gains that is made from sale.

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of Purchase Sep-86

Salling Price 2,00,000.00

Month & Year of Sale Jun-18

Capital Gain 2,00,000.00

Tax with Indexation 60,000.00

Purchase Price 90000

Cost of Construction 60000

Total Cost of Land 150000

Disposal Proceeds 200000

Net Capital gains 50000

Calculations of Capital Gains Tax

For the Year ended 30th June

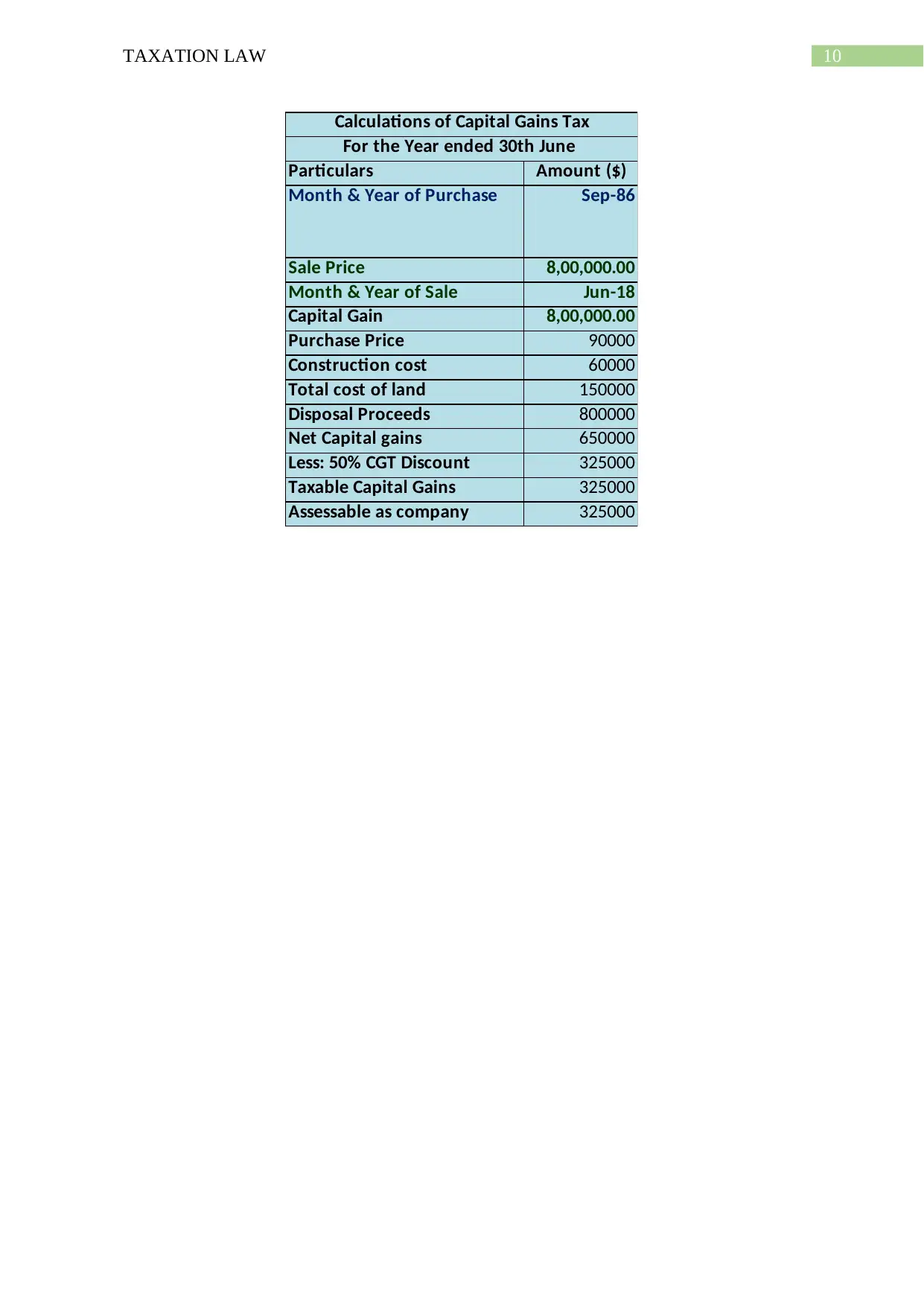

Answer to 4 C:

In the final alternative if it is noticed that the owner of the property was the owner

rather than the individual then in that case there should be deduction of the amortization cost

and the tax amount on the part of the company.

Answer to 4 B:

As understood from the case study, in another alternative it is noticed that the Scott

has decided to sale the property to his daughter for an amount of $200,000. It can be stated

that the property was sold to the daughter below the current market value however upon sale

it resulted in gain. Similarly, upon the sale of the property a capital gains tax of $50,000 was

made after deducting the construction costs and the purchase costs. Therefore, Scott would be

held liable for taxation relating to the capital gains that is made from sale.

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of Purchase Sep-86

Salling Price 2,00,000.00

Month & Year of Sale Jun-18

Capital Gain 2,00,000.00

Tax with Indexation 60,000.00

Purchase Price 90000

Cost of Construction 60000

Total Cost of Land 150000

Disposal Proceeds 200000

Net Capital gains 50000

Calculations of Capital Gains Tax

For the Year ended 30th June

Answer to 4 C:

In the final alternative if it is noticed that the owner of the property was the owner

rather than the individual then in that case there should be deduction of the amortization cost

and the tax amount on the part of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Particulars Amount ($)

Month & Year of Purchase Sep-86

Sale Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Purchase Price 90000

Construction cost 60000

Total cost of land 150000

Disposal Proceeds 800000

Net Capital gains 650000

Less: 50% CGT Discount 325000

Taxable Capital Gains 325000

Assessable as company 325000

Calculations of Capital Gains Tax

For the Year ended 30th June

Particulars Amount ($)

Month & Year of Purchase Sep-86

Sale Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Purchase Price 90000

Construction cost 60000

Total cost of land 150000

Disposal Proceeds 800000

Net Capital gains 650000

Less: 50% CGT Discount 325000

Taxable Capital Gains 325000

Assessable as company 325000

Calculations of Capital Gains Tax

For the Year ended 30th June

11TAXATION LAW

Reference List:

Black, C., (2017). The Attribution of Profits to Permanent Establishments: Testing the

Interaction of Domestic Taxation Laws and Tax Treaties in Practice.

Buchanan, R. & Consett, E., (2016). Section 974-80 ITAA97: The current state of play. Tax

Specialist, 19(5), p.217.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Clarke, D., (2017). Private mineral royalties in resource sector: M and A transactions-another

taxable commodity. Australian Resources and Energy Law Journal, 36(1), p.82.

Jacob, M. (2018). Tax regimes and capital gains realizations. European Accounting

Review, 27(1), 1-21.

Jones, D., (2017). Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Joseph, S.A., Walpole, M. & Deutsch, R., (2015). Taxation of Sovereign Wealth Funds-A

Suggested Approach. J. Australasian Tax Tchrs. Ass'n, 10, p.119.

Klein, E., (2016). Universal basic income. Arena Magazine (Fitzroy, Vic), (142), p.6.

Krever, R. & Mellor, P., (2016). Australia, GAARs–A Key Element of Tax Systems in the

Post-BEPS World.

Lombard, M., (2017). Everything producers need to know about tax: current

affairs. FarmBiz, 3(2), pp.10-11.

Marriott, L., (2016). Taxing corruption in Australia and New Zealand. Austl. Tax F., 31, p.37.

Reference List:

Black, C., (2017). The Attribution of Profits to Permanent Establishments: Testing the

Interaction of Domestic Taxation Laws and Tax Treaties in Practice.

Buchanan, R. & Consett, E., (2016). Section 974-80 ITAA97: The current state of play. Tax

Specialist, 19(5), p.217.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Clarke, D., (2017). Private mineral royalties in resource sector: M and A transactions-another

taxable commodity. Australian Resources and Energy Law Journal, 36(1), p.82.

Jacob, M. (2018). Tax regimes and capital gains realizations. European Accounting

Review, 27(1), 1-21.

Jones, D., (2017). Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Joseph, S.A., Walpole, M. & Deutsch, R., (2015). Taxation of Sovereign Wealth Funds-A

Suggested Approach. J. Australasian Tax Tchrs. Ass'n, 10, p.119.

Klein, E., (2016). Universal basic income. Arena Magazine (Fitzroy, Vic), (142), p.6.

Krever, R. & Mellor, P., (2016). Australia, GAARs–A Key Element of Tax Systems in the

Post-BEPS World.

Lombard, M., (2017). Everything producers need to know about tax: current

affairs. FarmBiz, 3(2), pp.10-11.

Marriott, L., (2016). Taxing corruption in Australia and New Zealand. Austl. Tax F., 31, p.37.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.