Victoria University Taxation Law and Practice BL02206 Assignment

VerifiedAdded on 2020/03/07

|12

|2298

|126

Homework Assignment

AI Summary

This assignment solution addresses key aspects of Australian taxation law, specifically focusing on the tax residency of an individual (Robyn) and the determination of assessable income for another (Paul). Part A examines Robyn's tax residency, analyzing the applicability of the domicile test based on her circumstances as a lecturer working in India and referencing relevant sections of the ITAA 1997 and tax ruling TR 98/17. It concludes that Robyn is a foreign tax resident, making only her domestic income taxable in Australia. Part B focuses on Paul's assessable income, differentiating between ordinary income from golf lessons and a gift received. It determines the appropriate method for recording assessable income, concluding that the accrual basis is suitable for the lesson revenue and that the gift is not subject to taxation. The document references relevant sections of the ITAA 1997 and tax rulings (TR 98/1, TR 1999/17, TR 2005/13), providing a comprehensive analysis of the tax implications for both individuals.

TAXATION LAW AND PRACTICE

BL02206

STUDENT ID

[Pick the date]

BL02206

STUDENT ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART A...........................................................................................................................................2

Issue.............................................................................................................................................2

Law..............................................................................................................................................2

Application..................................................................................................................................6

Conclusion...................................................................................................................................7

PART B...........................................................................................................................................8

Issue.............................................................................................................................................8

Law..............................................................................................................................................8

Application..................................................................................................................................9

Conclusion.................................................................................................................................10

References......................................................................................................................................10

1

PART A...........................................................................................................................................2

Issue.............................................................................................................................................2

Law..............................................................................................................................................2

Application..................................................................................................................................6

Conclusion...................................................................................................................................7

PART B...........................................................................................................................................8

Issue.............................................................................................................................................8

Law..............................................................................................................................................8

Application..................................................................................................................................9

Conclusion.................................................................................................................................10

References......................................................................................................................................10

1

PART A

Issue

The major issue is to determine whether the taxpayer Robyn from Victoria University would be

taxed as per Australian tax law for the tax year 2016/17.

Law

The tax liability on the derived income of taxpayer mainly depends on the tax residency position.

When a taxpayer is termed as Australian tax resident, then the income derived from domestic

(Australian) source and from international sources would be taxed as highlighted in Section 6-

5(2), ITAA 19971. Further, when the taxpayer is foreign tax resident then only the part of income

which is derived from Australian sources would be held for taxation as per the highlights of

Section 6-5(3), ITAA 19972. Therefore, it is critical aspect to find the tax residency position of

underlying taxpayer.

Section (1), ITAA 1936, comprises imperative provisions related to the tax residency status of

individual taxpayer. Further, in order to determine the tax residency position of taxpayer tax

ruling TR 98/173 would be taken into consideration. When the taxpayer is residing in other

country rather than Australia then the tax residency positions would be determined based on

residency tests. There are four main tests (Residency tests) describe in the TR 98/17 which

comprises the requisite conditions that needs to be satisfied by the concerned taxpayer in order to

recognized as Australia tax resident. It is essential that taxpayer must fulfill the conditions of at

least one of residency test4.

1 ATO, INCOME TAX ASSESSMENT ACT 1997, < https://www.ato.gov.au/law/view/document?DocID=PAC/19970038/6-5>

2 Commonwealth Consolidated Acts: Income Tax Assessment Act 1997 –SECT 6.5

<http://www.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.5.html>

3 Australian Taxation Office, TR 98/17-Income tax: residency status of individuals entering Australia [ (25 November 1998), <

http://www3.austlii.edu.au/au/other/rulings/ato/ATOTR/1998/tr1998-017/>

4 Sadiq, Kerrie, et. al., Principles of Taxation Law 2015, (Pymont,Thomson Reuters, 2015), p.37

2

Issue

The major issue is to determine whether the taxpayer Robyn from Victoria University would be

taxed as per Australian tax law for the tax year 2016/17.

Law

The tax liability on the derived income of taxpayer mainly depends on the tax residency position.

When a taxpayer is termed as Australian tax resident, then the income derived from domestic

(Australian) source and from international sources would be taxed as highlighted in Section 6-

5(2), ITAA 19971. Further, when the taxpayer is foreign tax resident then only the part of income

which is derived from Australian sources would be held for taxation as per the highlights of

Section 6-5(3), ITAA 19972. Therefore, it is critical aspect to find the tax residency position of

underlying taxpayer.

Section (1), ITAA 1936, comprises imperative provisions related to the tax residency status of

individual taxpayer. Further, in order to determine the tax residency position of taxpayer tax

ruling TR 98/173 would be taken into consideration. When the taxpayer is residing in other

country rather than Australia then the tax residency positions would be determined based on

residency tests. There are four main tests (Residency tests) describe in the TR 98/17 which

comprises the requisite conditions that needs to be satisfied by the concerned taxpayer in order to

recognized as Australia tax resident. It is essential that taxpayer must fulfill the conditions of at

least one of residency test4.

1 ATO, INCOME TAX ASSESSMENT ACT 1997, < https://www.ato.gov.au/law/view/document?DocID=PAC/19970038/6-5>

2 Commonwealth Consolidated Acts: Income Tax Assessment Act 1997 –SECT 6.5

<http://www.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.5.html>

3 Australian Taxation Office, TR 98/17-Income tax: residency status of individuals entering Australia [ (25 November 1998), <

http://www3.austlii.edu.au/au/other/rulings/ato/ATOTR/1998/tr1998-017/>

4 Sadiq, Kerrie, et. al., Principles of Taxation Law 2015, (Pymont,Thomson Reuters, 2015), p.37

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

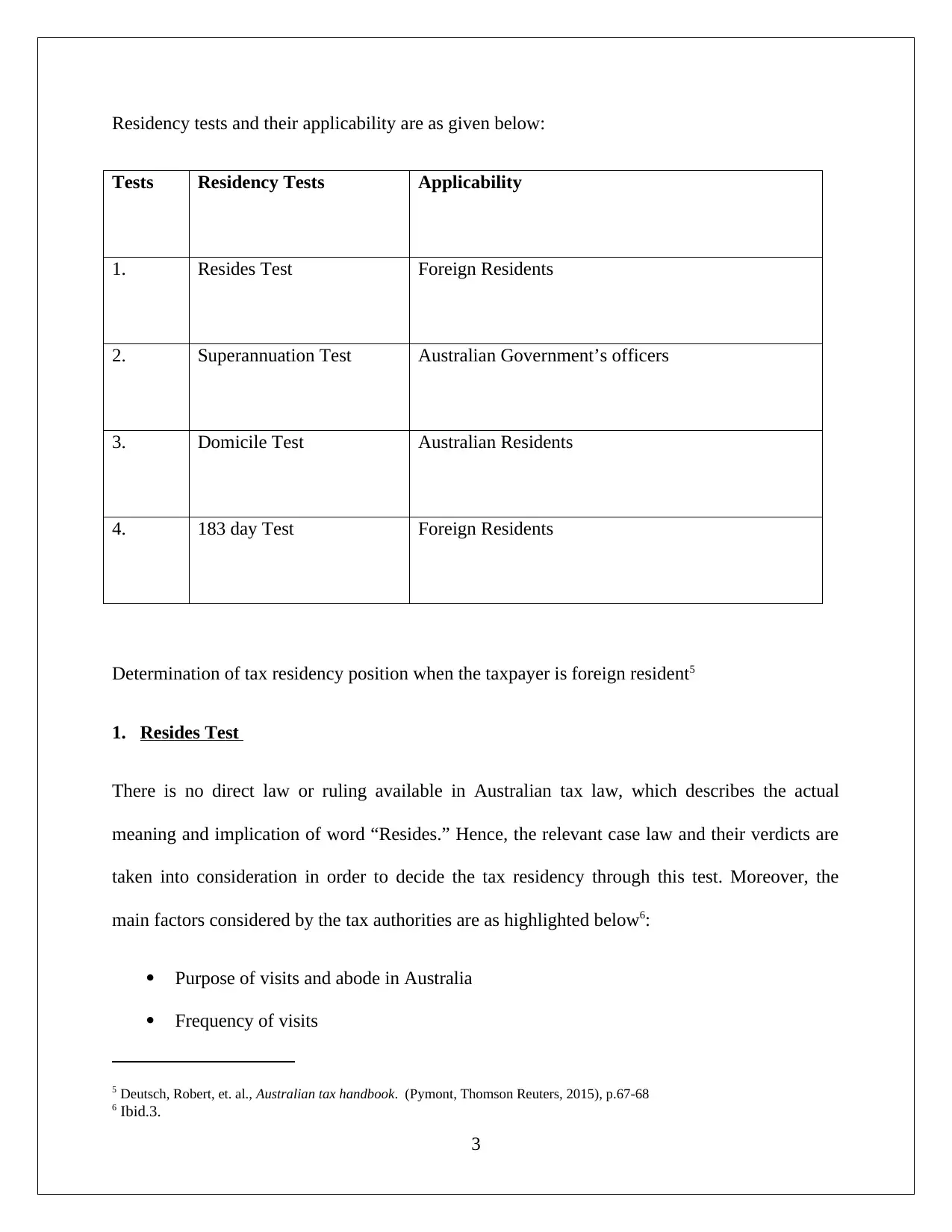

Residency tests and their applicability are as given below:

Tests Residency Tests Applicability

1. Resides Test Foreign Residents

2. Superannuation Test Australian Government’s officers

3. Domicile Test Australian Residents

4. 183 day Test Foreign Residents

Determination of tax residency position when the taxpayer is foreign resident5

1. Resides Test

There is no direct law or ruling available in Australian tax law, which describes the actual

meaning and implication of word “Resides.” Hence, the relevant case law and their verdicts are

taken into consideration in order to decide the tax residency through this test. Moreover, the

main factors considered by the tax authorities are as highlighted below6:

Purpose of visits and abode in Australia

Frequency of visits

5 Deutsch, Robert, et. al., Australian tax handbook. (Pymont, Thomson Reuters, 2015), p.67-68

6 Ibid.3.

3

Tests Residency Tests Applicability

1. Resides Test Foreign Residents

2. Superannuation Test Australian Government’s officers

3. Domicile Test Australian Residents

4. 183 day Test Foreign Residents

Determination of tax residency position when the taxpayer is foreign resident5

1. Resides Test

There is no direct law or ruling available in Australian tax law, which describes the actual

meaning and implication of word “Resides.” Hence, the relevant case law and their verdicts are

taken into consideration in order to decide the tax residency through this test. Moreover, the

main factors considered by the tax authorities are as highlighted below6:

Purpose of visits and abode in Australia

Frequency of visits

5 Deutsch, Robert, et. al., Australian tax handbook. (Pymont, Thomson Reuters, 2015), p.67-68

6 Ibid.3.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presence of any personal/professional/educational tie with Australia

Social arrangement of taxpayer with Australia

Also, the nationality of the taxpayer would be taken into account while deciding the tax

residency status for the given tax year.

2. 183-day test

When the taxpayer who is foreign resident and has stayed in Australia, then the following

conditions need to be satiated by the taxpayer in order to pass this test.

Taxpayer has stayed in Australia for minimum 183 days in the given assessment tax year

Taxpayer must has strong will to permanently settle in Australia

3. Superannuation test

When the government of Australia has sent their officers to overseas in order to fulfill the

government duties, then this test is used to check the tax residency of officer taxpayer. It is

essential that the taxpayer has systematic and steady contribution in any of the superannuation

scheme of Australian government. These schemes are as given below:

Commonwealth Superannuation Scheme (CSS)

Public Sector Superannuation Scheme (PSSS)

4. Domicile test

The taxpayer must satisfied the following two conditions of domicile test in regards to termed as

Australian tax resident irrespective of the fact that taxpayer has resided in foreign land7.

7 Ibid.4.

4

Social arrangement of taxpayer with Australia

Also, the nationality of the taxpayer would be taken into account while deciding the tax

residency status for the given tax year.

2. 183-day test

When the taxpayer who is foreign resident and has stayed in Australia, then the following

conditions need to be satiated by the taxpayer in order to pass this test.

Taxpayer has stayed in Australia for minimum 183 days in the given assessment tax year

Taxpayer must has strong will to permanently settle in Australia

3. Superannuation test

When the government of Australia has sent their officers to overseas in order to fulfill the

government duties, then this test is used to check the tax residency of officer taxpayer. It is

essential that the taxpayer has systematic and steady contribution in any of the superannuation

scheme of Australian government. These schemes are as given below:

Commonwealth Superannuation Scheme (CSS)

Public Sector Superannuation Scheme (PSSS)

4. Domicile test

The taxpayer must satisfied the following two conditions of domicile test in regards to termed as

Australian tax resident irrespective of the fact that taxpayer has resided in foreign land7.

7 Ibid.4.

4

Taxpayer must hold Australian domicile under the provisions of Domicile Act 1982

Taxpayer’s permanent abode must located in Australia only (the Levene v, I.R.C.8 case is

the testimony of this condition)

When the taxpayer who holds Australian domicile but the permanent abode is located in foreign

land, then he/she would be categorized as foreign resident. Therefore, it is imperative to check

the location of permanent abode of taxpayer. As per the verdict of Applegate per Franki9case, if

the taxpayer holds Australian domicile but resides in foreign land for substantial period of time

(i.e. atleast 2 years) or having intention to extend the abode than it would be assumed that the

permanent place of abode has been shifted from Australia. In such case, the person would not be

termed as Australian tax resident. The main features related to the permanent abode of taxpayer

are described in the tax ruling IT 2650 and are given below10:

Difference in the actual and expected abode in foreign land

Taxpayer’s intention to purchase home in foreign country

Intention of the taxpayer to make another visits to any other country or to go back to

Australia after a definite but substantial time period

Total duration of stay in foreign land and willingness to extent the stay

Strength of association (professional/private and so forth) with Australia

Activity of taxpayer which highlights the intent to make permanent abode in foreign land

8Levene v, I.R.C. (1928) A.C.2017

9 Applegate per Franki J 79 ATC at 4314; 9ATR at p. 907

10 Australian Taxation Office, Taxation Ruling No. IT 2650, (1991) <https://www.ato.gov.au/Individuals/Income-and-

deductions/Income-you-must-declare/ >

5

Taxpayer’s permanent abode must located in Australia only (the Levene v, I.R.C.8 case is

the testimony of this condition)

When the taxpayer who holds Australian domicile but the permanent abode is located in foreign

land, then he/she would be categorized as foreign resident. Therefore, it is imperative to check

the location of permanent abode of taxpayer. As per the verdict of Applegate per Franki9case, if

the taxpayer holds Australian domicile but resides in foreign land for substantial period of time

(i.e. atleast 2 years) or having intention to extend the abode than it would be assumed that the

permanent place of abode has been shifted from Australia. In such case, the person would not be

termed as Australian tax resident. The main features related to the permanent abode of taxpayer

are described in the tax ruling IT 2650 and are given below10:

Difference in the actual and expected abode in foreign land

Taxpayer’s intention to purchase home in foreign country

Intention of the taxpayer to make another visits to any other country or to go back to

Australia after a definite but substantial time period

Total duration of stay in foreign land and willingness to extent the stay

Strength of association (professional/private and so forth) with Australia

Activity of taxpayer which highlights the intent to make permanent abode in foreign land

8Levene v, I.R.C. (1928) A.C.2017

9 Applegate per Franki J 79 ATC at 4314; 9ATR at p. 907

10 Australian Taxation Office, Taxation Ruling No. IT 2650, (1991) <https://www.ato.gov.au/Individuals/Income-and-

deductions/Income-you-must-declare/ >

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Application

Robyn Rainer is the concerned taxpayer who was working as a lecturer in Victoria University in

Australia. The university also conducted business courses in Calcutta University India. Jason

Holm who was the coordinator in Calcutta University India has resigned from the job. After his

resignation, the university was looking for a lecturer who can go and stay in India and continue

the work. Taxpayer who was looking for a career opportunity as a course coordinator has

expressed her interest and also gets approved for the post. On January 14, she has joined the

Calcutta University India.

It is apparent that the taxpayer is neither an Australian government officer nor a foreign resident

and hence, “superannuation test, 183 day test and resides test” are not applicable. Further, she is

an Australian resident and therefore, the only valid test is domicile test in order to check the tax

residency status of Robyn.

Applicable test – Domicile test

Robyn has Australia domicile.

Permanent place of abode needs to be determined as per tax ruling IT 2650. It is apparent

from the case facts that she lives in a company owned flat in India. She has also opened a

bank account in Indian bank where she has receiving half of her salary. She has rented her

flat located in Melbourne for a period of 12 months. She has intention to remain in the

position of coordinator in Calcutta as long as the course is conducted in India. Hence, it

would be fair to conclude that Robyn has arrived India for a substantial time and thus, her

permanent place of abode has shifted from Australian and located in India. Based on the

6

Robyn Rainer is the concerned taxpayer who was working as a lecturer in Victoria University in

Australia. The university also conducted business courses in Calcutta University India. Jason

Holm who was the coordinator in Calcutta University India has resigned from the job. After his

resignation, the university was looking for a lecturer who can go and stay in India and continue

the work. Taxpayer who was looking for a career opportunity as a course coordinator has

expressed her interest and also gets approved for the post. On January 14, she has joined the

Calcutta University India.

It is apparent that the taxpayer is neither an Australian government officer nor a foreign resident

and hence, “superannuation test, 183 day test and resides test” are not applicable. Further, she is

an Australian resident and therefore, the only valid test is domicile test in order to check the tax

residency status of Robyn.

Applicable test – Domicile test

Robyn has Australia domicile.

Permanent place of abode needs to be determined as per tax ruling IT 2650. It is apparent

from the case facts that she lives in a company owned flat in India. She has also opened a

bank account in Indian bank where she has receiving half of her salary. She has rented her

flat located in Melbourne for a period of 12 months. She has intention to remain in the

position of coordinator in Calcutta as long as the course is conducted in India. Hence, it

would be fair to conclude that Robyn has arrived India for a substantial time and thus, her

permanent place of abode has shifted from Australian and located in India. Based on the

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

facts, it can be concluded that Robyn fails to pass domicile test because her permanent place

of abode is not in Australia. Therefore, her salary would be taxed in Australia for 2016/17.

Conclusion

It is apparent from the above that the only applicable test is domicile test. Further, the permanent

place of abode of taxpayer Robyn is shifted from Australian and hence, during the tax year

2016/17 her permanent place of abode is located in India. Therefore, it is fair to conclude that

taxpayer is not an Australian tax resident. Also, she would be categorized as foreign tax resident

and thus, the domestic income would be liable for taxation. Therefore, under section 6-5(3),

ITAA 1997 her salary from Victoria University would be taxed in Australia for the tax year

2016/17.

PART B

Issue

The central issue is to identify the amounts that would be included as assessable income for Paul

for the taxation year 2016/2017 i.e. year ending on June 30, 2017.

7

of abode is not in Australia. Therefore, her salary would be taxed in Australia for 2016/17.

Conclusion

It is apparent from the above that the only applicable test is domicile test. Further, the permanent

place of abode of taxpayer Robyn is shifted from Australian and hence, during the tax year

2016/17 her permanent place of abode is located in India. Therefore, it is fair to conclude that

taxpayer is not an Australian tax resident. Also, she would be categorized as foreign tax resident

and thus, the domestic income would be liable for taxation. Therefore, under section 6-5(3),

ITAA 1997 her salary from Victoria University would be taxed in Australia for the tax year

2016/17.

PART B

Issue

The central issue is to identify the amounts that would be included as assessable income for Paul

for the taxation year 2016/2017 i.e. year ending on June 30, 2017.

7

Law

One of the components of assessable income for a taxpayer in Australia is ordinary income as

defined by s. 6(5), ITAA 1997. The section defines ordinary income as that derived from

ordinary sources. However, the ordinary sources are not defined in the statute and hence the

various case laws and ATO rulings are relied on interpreting the various sources that are covered

under the ambit of ordinary income. One of the key sources of ordinary income is employment

income. Also, the income derived from any business or profession is also included in the fold of

ordinary income as apparent from tax ruling TR 98/1. Besides, income received in kind instead

of cash would also be included in taxable income as per TR 1999/17. It is noteworthy that there

are various general business expenses related deductions that the taxpayer may assess in order to

compute the taxable income in accordance with s. 8(1) ITAA 1997.

Another critical issue while determination of assessable income arising from business is to

determine whether the same should be done on a cash basis (Receipts Basis) or accrual basis

(Earnings Basis). In accordance with TR 98/1, the taxpayer ought to choose the method which

most appropriately captures the income. For instance, if the money received for clients is non-

refundable, then the cash basis is more suitable because irrespective of service provided in the

future or not, the money would not be given back and hence it makes sense to book revenues. On

the other hand, if the cash collected from customer can be broken into smaller payments for

particular milestones and excess payment is refundable, then the earnings method makes more

sense for computation of assessable income11.

11 Ibid.3

8

One of the components of assessable income for a taxpayer in Australia is ordinary income as

defined by s. 6(5), ITAA 1997. The section defines ordinary income as that derived from

ordinary sources. However, the ordinary sources are not defined in the statute and hence the

various case laws and ATO rulings are relied on interpreting the various sources that are covered

under the ambit of ordinary income. One of the key sources of ordinary income is employment

income. Also, the income derived from any business or profession is also included in the fold of

ordinary income as apparent from tax ruling TR 98/1. Besides, income received in kind instead

of cash would also be included in taxable income as per TR 1999/17. It is noteworthy that there

are various general business expenses related deductions that the taxpayer may assess in order to

compute the taxable income in accordance with s. 8(1) ITAA 1997.

Another critical issue while determination of assessable income arising from business is to

determine whether the same should be done on a cash basis (Receipts Basis) or accrual basis

(Earnings Basis). In accordance with TR 98/1, the taxpayer ought to choose the method which

most appropriately captures the income. For instance, if the money received for clients is non-

refundable, then the cash basis is more suitable because irrespective of service provided in the

future or not, the money would not be given back and hence it makes sense to book revenues. On

the other hand, if the cash collected from customer can be broken into smaller payments for

particular milestones and excess payment is refundable, then the earnings method makes more

sense for computation of assessable income11.

11 Ibid.3

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Also, with regards to determination of gift, TR 2005/13 is relevant as division 30; ITAA 1997

has been rather silent in this regard. Based on the various case laws, it highlights the four

conditions which are needed for a payment to be recognized as gift. These are as follows12.

There needs to be an ownership transfer in the favor of the transferee.

The transfer should be carried out on a voluntary basis.

The transferor must not have any reciprocal material expectations from the transferee in

exchange for the gift extended.

The transfer must arise on account of benefaction.

If a given payment fulfills the above criterion, then it would be recognized as gift and no tax

would be charged on the same and hence no contribution to assessable income would be made13.

Application

It is apparent from the given facts that Paul is in the business of providing golf classes and hence

the income derived from providing these classes would be termed as ordinary income under s.

6(5). Further, with regards to the appropriate means to record assessable income for Paul, the

more appropriate means would be accrual basis as it is apparent that for the 12 lessons even

though all the money is paid upfront but the same is refundable if the client fails to attend some

lessons on a proportionate basis. This implies that for the sum collected for the 12 lessons, there

is likelihood that some portion would be refunded to the client in the event client fails to turn up

for the lessons. Thus, it is prudent that assessable income from the 12 lessons revenues should

only realize the portion for which classes have been provided till June 30, 2017. The revenue for

12

13 Ibid.4.

9

has been rather silent in this regard. Based on the various case laws, it highlights the four

conditions which are needed for a payment to be recognized as gift. These are as follows12.

There needs to be an ownership transfer in the favor of the transferee.

The transfer should be carried out on a voluntary basis.

The transferor must not have any reciprocal material expectations from the transferee in

exchange for the gift extended.

The transfer must arise on account of benefaction.

If a given payment fulfills the above criterion, then it would be recognized as gift and no tax

would be charged on the same and hence no contribution to assessable income would be made13.

Application

It is apparent from the given facts that Paul is in the business of providing golf classes and hence

the income derived from providing these classes would be termed as ordinary income under s.

6(5). Further, with regards to the appropriate means to record assessable income for Paul, the

more appropriate means would be accrual basis as it is apparent that for the 12 lessons even

though all the money is paid upfront but the same is refundable if the client fails to attend some

lessons on a proportionate basis. This implies that for the sum collected for the 12 lessons, there

is likelihood that some portion would be refunded to the client in the event client fails to turn up

for the lessons. Thus, it is prudent that assessable income from the 12 lessons revenues should

only realize the portion for which classes have been provided till June 30, 2017. The revenue for

12

13 Ibid.4.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the remaining would be recognized in 2017/2018 as and when the lessons are imparted to the

clients.

Also, it is noteworthy that payment of $10,000 from Doreen would be recorded as a gift and

hence it will not contribute to assessable income. This is because Doreen has paid the amount on

a voluntary basis and also because the transfership of ownership has been completed. Further,

Doreen by giving the money had no material reciprocal expectations in return and was primarily

given as a token of appreciation to her teacher Paul. Additionally, the payment of two students

that went into paying for damage to David’s golf buggy would also be part of the assessable

income as per TR 1999/17.

Conclusion

Based on the above discussion, it is apparent that assessable income for Paul would consist of

income from lessons on an accrual basis coupled with payment made by the students for making

up for the damage caused to David’s golf buggy.

References

Websites

10

clients.

Also, it is noteworthy that payment of $10,000 from Doreen would be recorded as a gift and

hence it will not contribute to assessable income. This is because Doreen has paid the amount on

a voluntary basis and also because the transfership of ownership has been completed. Further,

Doreen by giving the money had no material reciprocal expectations in return and was primarily

given as a token of appreciation to her teacher Paul. Additionally, the payment of two students

that went into paying for damage to David’s golf buggy would also be part of the assessable

income as per TR 1999/17.

Conclusion

Based on the above discussion, it is apparent that assessable income for Paul would consist of

income from lessons on an accrual basis coupled with payment made by the students for making

up for the damage caused to David’s golf buggy.

References

Websites

10

ATO, INCOME TAX ASSESSMENT ACT 1997, <

https://www.ato.gov.au/law/view/document?DocID=PAC/19970038/6-5>

Australian Taxation Office: Taxation Rulings: TR 98/17-Income tax: residency status of

individuals entering Australia (25 November 1998), <

http://www3.austlii.edu.au/au/other/rulings/ato/ATOTR/1998/tr1998-017/>

Commonwealth Consolidated Acts: Income Tax Assessment Act 1997 –SECT 6.5.

<http://www.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.5.html>

Books

Sadiq, Kerrie, et. al., Principles of Taxation Law 2015, (Pymont, Thomson Reuters, 2015)

Deutsch, Robert, et. al., Australian tax handbook. (Pymont, Thomson Reuters, 2015)

Relevant Statutes

Income Tax Assessment Act, 1936

Income Tax Assessment Act, 1997

11

https://www.ato.gov.au/law/view/document?DocID=PAC/19970038/6-5>

Australian Taxation Office: Taxation Rulings: TR 98/17-Income tax: residency status of

individuals entering Australia (25 November 1998), <

http://www3.austlii.edu.au/au/other/rulings/ato/ATOTR/1998/tr1998-017/>

Commonwealth Consolidated Acts: Income Tax Assessment Act 1997 –SECT 6.5.

<http://www.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.5.html>

Books

Sadiq, Kerrie, et. al., Principles of Taxation Law 2015, (Pymont, Thomson Reuters, 2015)

Deutsch, Robert, et. al., Australian tax handbook. (Pymont, Thomson Reuters, 2015)

Relevant Statutes

Income Tax Assessment Act, 1936

Income Tax Assessment Act, 1997

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.